‘“It is a capital mistake to theorize before one has data. Insensibly one begins to twist facts to suit theories, instead of theories to suit facts” says Holmes to Dr. Watson.

While I acknowledge the importance of having data to support any theory, it is absolutely challenging to obtain complete data on the topic at hand. That being said, it is worth noting that the theory presented here regarding the potential bubble in Nepal’s real estate market is not without merit. In fact, the Nepal Rastra Bank (NRB) has also acknowledged this possibility. Besides the limitations in obtaining the complete data, this post is an attempt to support this theory with the available datasets and charts. But isn’t this topic related to Working Capital Loan Guidelines from NRB? Yes, that as well.

Loan Composition and Securities

Below is the financial sector data from Nepal Rastra Bank. Positive figures indicate the lending of Financial Institutions categorized by product and the negative figures indicate the lending by the composition of the security. It is important to note that both positive and negative figures are the amount of lending, not the valuation of security against the lending.

The above data shows that over the past good decade of Nepal’s economy, around 70 to 75% of the total lending in Nepal has been secured against the real estate land and buildings. Although the security against land and building is a safe bet from a security perspective, this certainly is not a good indication of a growing economy. One essential element of lending is that lending should be backed by reliable security. Despite the fact that real estate lending has been perceived as a reliable security in Nepal (probably because of the family and sentimental value attached to it), real estate itself is not a productive asset so high concentration indicates that it potentially means credit bubble. Moreover the housing and utilities price index in Nepal is few points below the average overall index of consumer price index, which could very well be an indication that the operational income (considering both opportunity cost and rent income) derived from rental and similar property income is barely sufficient to meet the cost of the real estate investment in housing, if capital appreciation were to be altogether ignored. Again, this is just a theory, and no reliable data could be obtained in this regard. This obviously has to be viewed in the conjunction of the house development cost, increasing cost in import materials, increasing wage price indices, life of the commercial and domestic buildings, overall quality of living and similar indices.

Data Sources from NRB:

1. Loans of the BFIs (Product-wise)

2. Loan to the BFIs (Sector-wise)

3. Loan to the BFIs (Security-wise)

Real Estate Backed Lending in Nepal

Let’s go back to the same chart in the section above, between Residential Personal Home Loan (Up to Rs. 80 Lakh) and Real Estate Loan, they constitute about 10% to 15% of the total lendings in Nepal by the financial institutions. Well that at face doesn’t seem to be a huge number at least in terms of the percentage composition. But why do we keep hearing the claim that the real estate sector in Nepa (formal and informal, combined) has been one of the main sectors absorbing a large chunk of banks’ lending?

Well the answer is multifaceted in the context of Nepal and quite troublesome. Even NRB acknowledges this in its 2011 report titled Real Estate Financing in Nepal: – A Case Study of Kathmandu Valley. Even around a decade ago, the financial institutions’s direct exposure was not particularly high at about 20% of the total portfolio, and since then, NRB being the central bank of the country, with its basic concern to discourage the risky lending in the real estate and encourage lending in the productive sectors for the country’s economic growth the imposed a cap (to 15% of the total total loans by 2011 and to 10% by 2012) in the lending to the real estate sector. This led to the decrease in the total volume of lending in the real estate sector, steadily decreasing from around 20% in 2010 to around 12% in 2022. This should have meant that since banking access to the real estate sector went down, the real estate price indices should have been influenced and gone downwards, but quite opposite, the prices kept on with its steady course. Several studies around the world have found that real estate itself is not a productive asset so high concentration indicates that potentially means there is an existence of credit or asset price bubble. Reference: Managing Credit Bubbles, Alberto Martin CREI

But why? The reason is likely misclassification of the loans and diversion of the funds into the real estate sector. According to the Nepal: Selected Issues; IMF Country Report 10/184; May 17, 2010, although banks’ direct exposure to real estate and housing loans is not particularly high compared as percentage of the total loan portfolio, the actual exposure could be higher due to loan misclassification problems. In addition, total exposure, including loans collateralized with real estate properties, account for 70 percent of total.” IMF’s report not implies the possibility of the real estate loan misclassification but also indicates that a large part of the many forms of lending are secured by the real estate assets. This huge dependency of the banking sector in the collateralization of real estate assets (around 70% to 75%) makes the banking sector very vulnerable to the price level, development, sensitivities and busts that may occur in the real estate sector, impacting the entire lending market.

The concept that we are discussing is pretty obvious here. Despite the various types of lending products existing in the financial market, if all that the financial institutions prefer in form of security is the security of real estate assets, then obviously, essentially and axiomatically either (1) most of these lending are being diverted to real estate investment, or (2) assets other than real estate are underperforming in the economy, or (3) or a mix of both.

Land related measurements used in Nepal:

(A) 1 Ropani is equivalent to: 16 Anna / 64 Paisa / 256 Daam / 508.72 Mtr. Sqr. / 5476 Sq. Feet

(B) 1 Bigha is equivalent to: 20 Kattha / 6772.63 Mtr. Sqr. / 72900 Sq. Feet / 13.31 Ropani

Credit and GDP Compared with Other Countries

Domestic credit to the private sector expressed as a percentage of GDP is a financial indicator that measures the extent to which the private sector in a country has access to credit provided by domestic financial institutions such as banks, credit unions, and other lending institutions. This indicator reflects the degree to which the financial system in a country is able to support private sector growth and investment. A higher percentage indicates that there is a greater availability of credit to private sector borrowers, which can stimulate economic growth and development. However, a very high percentage may also indicate the potential risk of excessive debt levels in the private sector and the potential for financial instability. Overall, this indicator can be used to assess the level of financial deepening and access to credit in a country, as well as the overall health and stability of its financial sector. However, this index should not be viewed in isolation but in conjunction with other indices like capital formation within the country, correlation with the increase in GDP, achieving balance of payments, achieving sectoral expertise or self-sufficient economy as per the country’s objective and so on.

Domestic Credit to GDP %

Compared with Regional Global Averages

Compared with Countries with Similar Averages

GDP of Nepal by Economic Activities (at 2010/11 Prices)

Perhaps it is better to view the above chart in a stacked column that shows how the sectoral composition of the GDP has changed over the years keeping in mind the composition of the gross domestic product contributed by the real estate sector. The real estate sector’s contribution to the total GDP has remained consistently around 10% of the total throughout the period. The GDP data obviously doesn’t suggest any swings in the composition of the GDP, but has only increased in tandem with the growth in GDP.

Okay then, the composition basically remains the same in terms of the real estate sector’s contribution to the overall GDP. Isn’t this a strange observation? Is there something nebulous and hidden? Okay let’s again paint this data with a theory.

One of the limitations of using GDP as a measure of economic performance is that it is a consumption-led index. This means that it focuses primarily on the amount of goods and services that are produced and consumed within an economy, without considering other factors that may be important for overall well-being or even productive growth of the economy. Increase in the GDP doesn’t always mean a corresponding increase in the productive economy because it is a consumption led index. The large trade deficits and the balance of payment being supported by the remittance income clearly indicates that the GDP growth of Nepal is consumption led. In such a scenario the GDP index in itself is not very reliable data to conclude about the real estate sector in Nepal. We will try to look into this with many charts and datasets below.

Another reason why the facts about the real estate transaction cannot be derived from the GDP figures is that, the gross fixed capital formation component of the GDP calculation process doesn’t typically include land transactions as capital formation. Only if a real estate transaction results in the creation of a new fixed asset, such as the construction of a new building or the purchase of a commercial property, then it would be included in fixed capital formation. However, if the transaction only involves the transfer of ownership of an existing property, then it would not be included in fixed capital formation. So real estate sector GDP from national accounting only includes land development costs, housing and real estate development costs but not the transactions of land.

Capital Formation Status of Nepal compared with the Global Averages

Yes, the figures of gross capital formation in the national accounting doesn’t consider the transactions of the change in ownership of existing real estate property, but still what’s the harm in observing these statistics? It will at the least give us the idea for the trend of development costs in the real estate sector.

On the one hand the above chart is based on the logarithmic Y axis and on the other this is something that should be viewed in relation to the size of the economy, so let’s instead refer to a chart with gross capital formation expressed as a percentage of GDP for relative measure.

There is no fixed ideal percentage of gross fixed capital formation (GFCF) compared to GDP that applies to all countries. The appropriate level of investment in fixed assets depends on factors such as a country’s stage of economic development, its infrastructure needs, and its investment climate. Generally, developing countries may need to allocate a larger share of GDP to GFCF to build up their infrastructure and capital stock, while developed countries may have lower GFCF/GDP ratios as they focus on maintaining and upgrading existing infrastructure. In addition, the level of GFCF that is appropriate for a given country can also vary over time, depending on changes in economic conditions, policy priorities, and other factors.

National Income Statistics of Nepal Recapped

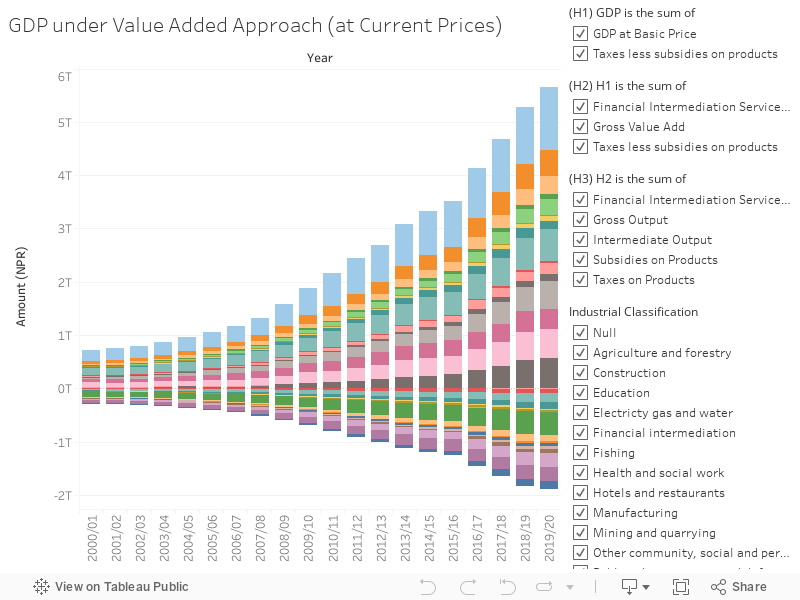

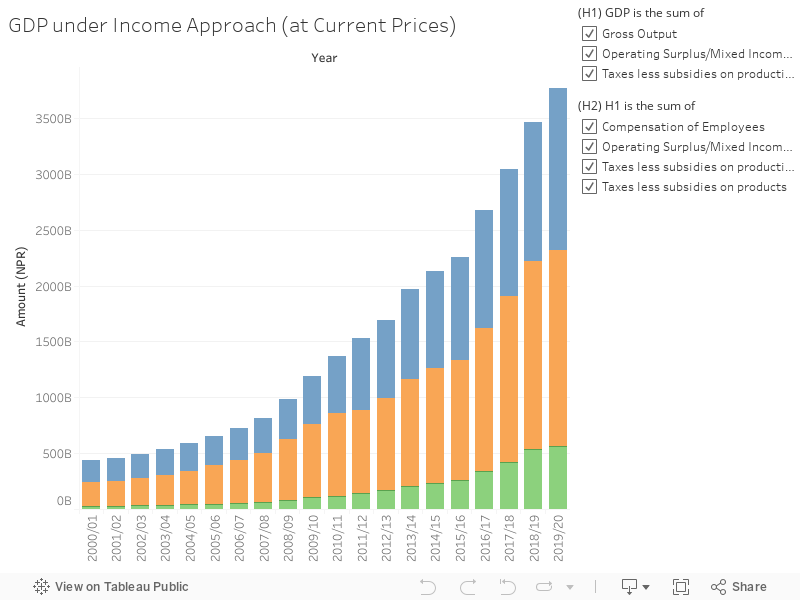

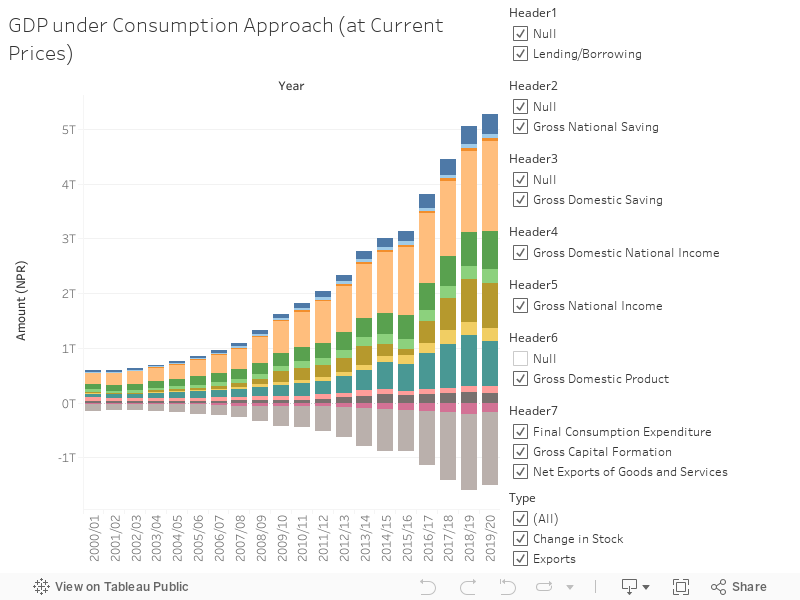

To get things connected along the way, here is a recap on some concepts of national accounting. Gross Domestic Product (GDP) is a measure of the total economic output of a country over a specific period of time, typically one year. It represents the monetary value of all final goods and services produced within a country’s borders during the period under consideration, regardless of the nationality of the individuals or firms that produced them. The Standard for National Income Accounting follows three approaches to calculate the GDP: Value Added Approach, Income Approach and Consumption Approach to arrive at the figure of the GDP, a graphical illustration is given above. GDP is not the only concept covered by the National Income Accounting, concepts of Consumption Expenditure, Capital Formulation, National Income, National Saving and Lendings/Borrowings are the figures calculated in the national income account. We will take a snapshot of these figures in the context of Nepal in the table below.

Consumption-led growth of GDP refers to an economic model where economic growth is primarily driven by increased consumer spending. The huge trade imbalance, massive dependence of Nepal’s economy on remittance income and the bad trend of the modern consumerism culture in Nepal has been the primary reason for the consumption-led growth of GDP in Nepal – mostly led by consumer spending in the country.

It is so unfortunate in Nepal that consumer demand for goods and services is what stimulates the economy. The need to consume has been the reason for driving the youths of the country into the foreign employment, which in turn leads to increased remittance income and further consumer spending. This at face creates a positive feedback loop that drives economic growth of the country, but consumption led GDP growth is not a sustainable economic growth.

While consumption-led growth can be a driver of economic growth in the short term, it can also be unsustainable in the long run. This is because it relies on continuous growth in consumer spending, which can eventually lead to overconsumption and a depletion of resources. In addition, in the context of Nepal, this consumption-led growth has also been assisted by the foreign assistance, massive government spending due to weak public capacity, unproductive capital formation (eg. real estate and capital market bubble), increasing domestic and foreign debts, which could lead to financial instability and a potential economic downturn if it becomes unmanageable.

To create a sustainable economy, it is important to have a balance between consumption, investment, and government spending. This can help to ensure that economic growth is not solely reliant on consumer spending and can be maintained over the long term. Additionally, sustainable economic growth should take into account the environmental and social impacts of economic activity, as well as the need for equitable distribution of benefits across society.

GDP under Value Added Approach (at Current Prices)

GDP under Income Approach (at Current Prices)

GDP under Consumption Approach (at Current Prices)

Numbeo’s Housing Affordability Index

Slide one is presented as a geo chart while slide two is presented as a time series data spanning from 2009 to 2023. The above chart should be interpreted as follows from the perspective of the tenant:

- Affordability Index: Higher the better

- Mortgage As A Percentage Of Income: Lower the better

- Price To Income Ratio: Lower the better

- Gross Rental Yield City Centre: Lower the better

- Gross Rental Yield Outside of Centre: Lower the better

- Price To Rent Ratio City Centre: Lower the better

- Price To Rent Ratio Outside Of City Centre: Lower the better

Numbeo.com is a crowd-sourced database of user-contributed data about the cost of living, property prices, crime rates, health care, pollution, traffic, and other indicators of quality of life in cities and countries around the world. Numbeo collects its data through online surveys and user contributions. Users can enter data about their local area, and Numbeo aggregates the data to provide an overall picture of living conditions in different places. Numbeo also uses official government data and other reliable sources, such as international organizations, to supplement the user-contributed data. It is however important to note that Numbeo does not independently verify the accuracy of the data provided by users, and therefore the data should be taken with a grain of salt and used as a general guide rather than definitive information.

Source:

1. Property Prices Index by Country 2023

2. World Development Indicators | Data Catalog

Data such as those collected by Numbeo are primarily focused on such indicators that are very likely to point asset price bubbles in an economy. In an economy, typically the following factors could indicate the real estate price bubbles:

- High price-to-income and price-to-rent ratios

- High levels of household debt

- Speculative activity in real estate transactions

- High vacancy rates

- Oversupply of mortgage backed securities

- Lack of transparency in transactions

- Over reliance on short-term investments

Real Estate Prices in Nepal

According to the financial survey of 2073, household income has increased by 56 percent in six years but land prices have increased 330 percent over the past 30 years. This is bad news not only for the poor but also for the upper middle class people who want to purchase land through their income.

The high property prices in Kathmandu are due to various reasons, including large-scale migration from rural areas during the Maoist insurgency, lack of economic opportunities in rural areas, massive capital inflow, availability of credit at low interest rates, increasing trend of remittances, and increasing tax rates. The influx of people into the valley has put pressure on the limited land and housing available, and real estate was seen as a safe investment haven during the political and economic uncertainty of the time. Banks and financial institutions also contributed to the price surge by evergreening bad loans, leading to a correction by the central bank.

Reference:

Sectoral Analysis of Loans

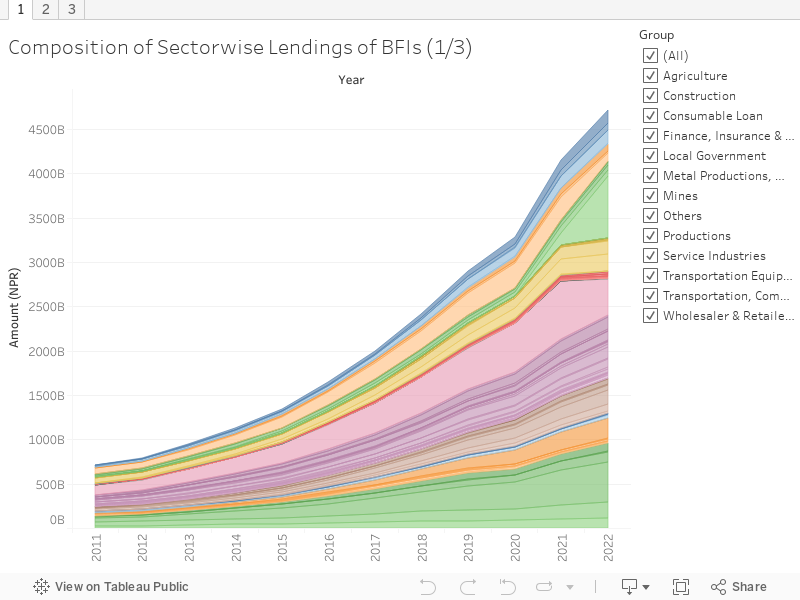

Sectoral lending of financial institutions provides information on the lending made to different economic sectors. The sectors include agriculture, manufacturing, services, real estate, and others. This information is important as it gives insight into which sectors are receiving more investment and credit, which can help to determine the health and growth of different sectors of the economy. It can also help to identify any imbalances in the distribution of credit and investment, which can have significant impacts on economic growth and stability. In the context of Nepal, credit growth has been observed in all the sectors of the economy and relative composition has remained consistent throughout.

Normality Distribution of Working Capital Lending in Nepal

Below is the analysis of a commercial bank’s loan mass from mid 2019. Working capital loans like: Business Overdraft Loan (P02), Business Other Working Capital Loan (P03), Trust Receipt / Import Loan (P04) have been filtered from the loan mass for the analysis below.

Note: Please note that this analysis only covers working capital lending of one commercial bank in Nepal and data are from the year 2019.

Working Capital Loan Composition by District

Working Capital Loan Composition by Type of Product

Normality Distribution of Working Capital Loans

Again, the data that has been used for the analysis above is from 2019 but there are good many reasons to assume that the composition and the average mode of the lending size has remained more or less the same even at the time of writing this post. There are some products that are extreme outliers in the above data, outliers have not been excluded in the above analysis. Even so the cutoff of 10 million that has been provided in the Working Capital Guideline, (where the bank may lend as per its own lending policies) is not so random. In fact the data above suggests that this gives banks the optimum headroom to brace for the changes in the working capital guidelines. In the loan mass that has been referred for the analysis above, the average size of the working capital lending is 7 million NPR, which is well below the cut off provided in the amended working capital guideline. However, only data obtained from loan mass of one commercial bank has been included in the analysis above. If you can help me with obtaining the data for more financial institutions, of course, research for purely research purposes would be a basic help for all.

Working Capital Loan Guideline: Need, Guideline and Amendment

Working Capital Guidelines, 2079 was first issued in 2079.05.07 set to be effective from 2079.07.01 to Class A, Class B, Class C and Infrastructure Development Banks. Link to the file here: Working Capital Guidelines, 2079. Later on 2079.09.20 the Working Capital Guidelines, 2079 was reissued with amendment. Link to the file here: Working Capital Guidelines, 2079 (With First Amendment).

Before the issue, NRB had issued notices for consultative documents and requests for suggestions and the draft version was released to the stakeholders. Before the issue of the working capital guidelines the provisions under Paragraph 36 for Provisions on working capital loans under Chapter 2 Classification of Loans/advances and Loan Losses of the Unified Directive, 2078 was applicable. Reference: Page 25-27 (Unified Directive, 2078)

NRB’s intention behind the issuance of the Working Capital Guidelines was to prevent the unwarranted credit surge to the real estate sector that was believed to have suffered an asset price bubble leading to financial and productivity fragility in the country. In this regard, the attention of Nepal Rastra Bank has been drawn to the growing trend of credit flows to the real estate sector despite sluggish overall economic situation. To address this situation, the NRB has issued a number of directives to reduce the credit flows to this sector and minimize the risk profiles of the banking sector, in an attempt to preempt the situation of domestic financial crisis, and the major objective of the Working Capital Guidelines has also been the same.

The other intents of the NRB in issuing this new working capital loan guidelines are:

- To ensure the uniformity between the banks and financial institutions on the credit limit determination and monitoring of the working capital loans.

- To strengthen the inspection and analysis of the borrower’s capacity for servicing the working capital loans.

- To make the working capital lending process methodical and transparent.

The need and necessity for affordable real estate prices

Affordable housing has been proven to be a fundamental necessity to a developing country which allows even people with moderate income to own real estate properties. Countries around the world have often provided affordable housing through government subsidies and other forms of assistance to prioritize the housing needs of the public realizing its necessity.

Countries such as Singapore, China, and India have made significant progress in developing affordable housing programs to meet the housing needs of their growing populations. For example, Singapore’s government implemented the Housing and Development Board (HDB) in the 1960s, which provided affordable public housing to citizens. China has implemented a similar program with the construction of millions of affordable homes in recent years. India has also made strides in providing affordable housing, with the implementation of the Pradhan Mantri Awas Yojana (PMAY) program, which aims to provide affordable housing to all eligible beneficiaries by early 2020s. Developing affordable housing not only provides much-needed housing for people with low to moderate incomes, but it also has significant economic benefits. It can create jobs in the construction industry and other related sectors, stimulate economic growth and investment, and improve living conditions and overall quality of life for citizens.

So real estate development in itself is not a business of sin. It is the most basic physical need of a human being. But the unaffordable real estate prices, the rampant informal market for real estate transactions always casts a doubt over any Nepali’s purchase decision. So often it is viewed as a business of pain and sin. Some substandard real estate market practices in Nepal are:

- Investment in personal residences account for 75–90 percent of household wealth in emerging-market countries like Nepal, which amounts to 6 – 12 times their annual income. Reference: Expanding Housing Finance to the Underserved in South Asia, Real Estate Financing in Bangladesh: Problems, Programs, and Prospects

- There is no reliable housing price or real estate price index published in Nepal. NRB needs to pay close attention towards property prices in order to regulate and prevent financial risks through monetary and credit policies. It is crucial to develop Real Estate or Housing Price Index. Independent and specialized institutions for asset management, credit rating and securitization need to be set up in Nepal.

- The real estate business in Nepal is being done largely in the unorganized sector that purchases large areas of land and does plotting with or without developing residential facilities. In an ideal situation the enthusiasm and investment interest of the Nepalese in the real estate sector should have allowed for the development of the distinct fields of the real estate industry like: Appraisals (Professional Valuation Services), Brokerage (Assisting buyers and sellers in transactions), Professional Real Estate Developers, Property Management Industry, Real Estate Marketing, Relocation Industries etc. But unfortunately these areas of the real estate industry in Nepal have not been able to flourish because of the large prevalence of the unorganized sector brokers and speculative buyers often derogatorily known as “dalal”.

- The economic and geo-political shortsightedness in Nepal has hindered the development of better cities in all parts of Nepal including the development of the satellite cities in the dense metros. The tendency of migrating from rural areas to urban areas has also fueled the real estate business in Nepal. Even if the real estate bubble settled or did not exist in the first place the limited migration option to Kathmandu for opportunities certainly has a lot of impact on the real estate prices surging in the cities. Reference: Bank Lending and Real Estate in Asia: Market Optimism and Asset Bubbles

- Excessive bank lending to the real estate sector was one of the responsible factors that led to the Asian financial crisis and the recent global financial crisis of the late 2000s. If the credit growth and consumption led GDP growth of the country remains unchecked, Nepal may be facing its own internal asset bubble crisis. Reference: Bank Lending and Real Estate in Asia: Market Optimism and Asset Bubbles

- Although real estate business is considered as an unproductive and risky business it has many backward and forward linkages with many other sectors in the economy and generates positive impacts, too. The real estate sector may contribute significantly in employment generation and in developing land and housing in the country. In addition, it may contribute through the consumption of building materials. Moreover, it is a sector associated with fulfillment of basic needs of people. So there needs to be some policy intervention in this sector to adapt to the much essential value chain of the real estate sector rather than letting it slip to the informal exorbitant industry.

- The NRB directives should not be directed only by the price movements and pressure from the major players of the real estate market (be it bankers or real estate brokers). They should mitigate public sentiments, consider the vulnerability of the sector and come up with long term policies. Financing for real estate and housing is an emerging and immediate need in Nepal for overall development in the human index. There is a need to explore new sources, products, and mechanisms for the successful financing of the real estate sector and make it affordable to even middle and low income communities.

- Asset price bubbles left unchecked will cause the crowding-out effect in the economy. This is caused when the other productive sectors of the economy are not able to get the finances and lending because the financiers are driven by the expectation of making massive profits in the bubbly collaterals, as a result this will lead to a situation where the alternative investments and economic output of the country are very low.

NRB discontinued to collect the Housing Price Index

The International Monetary Fund (IMF) has developed the financial soundness indicator (FSI) to respond to the need for better tools to assess the strengths and vulnerabilities of the financial system. But it doesn’t have the data pertaining to Nepal because we do not have the national system of collecting the real estate price indices. NRB had tried to collect these indices but it was later dropped. IMFs data, for comparative with other countries, has four indicators related to the real estate market: Residential real estate prices, Commercial real estate prices, Residential real estate loans to total loans and Commercial real estate loans to total loans. Source: Government Finance Statistics – IMF Data

NRB dropped the publication of a survey on real estate or housing prices due to the lack of credible data. NRB has stated this survey for the first time and collected the data for 2076/77 and 2077/78 but with a plan to continue to release the report every three months. The main reason behind the central bank’s move is the lack of credibility of the real estate price obtained from the survey.

References:

- Housing Price Index Survey Report released in 2078: HPI Survey Report 2078

- New Business Age News Article: NRB Halts Survey on Real Estate Price Citing Lack of Authentic Data

Constructing a real estate price index is naturally a complicated issue in Nepal due to the nature and characteristics of real estate, and the lack of official prices and maximum transactions being made through the gray channels. In the HPI survey made by NRB, data was collected from various sources, including property valuation during home loan transactions and real estate sales advertisements published in various newspapers, sales notices placed on online portals, data received from various accounting professionals, real estate outsourcing companies and land revenue offices for certain city centers of Nepal.

Therefore, the real estate price index in Nepal developed by NRB was based on the records of land revenue office and bank valuations when real estate is used as collateral for loans. Loan disbursement in Nepal shows a cyclical trend with the value of real estate, and if the flow of credit is too high, it can affect the overall price level and external balance. In Nepal, about two-thirds of bank loans are secured by real estate mortgages. Morocco and Oman have developed real estate price indices to measure the cost of building residential and commercial real estate. Thus creating a real estate price index is necessary as the majority of the total credit of the banking sector of Nepal is found to flow in real estate mortgage protection, and significant fluctuations in the price of real estate can create financial and macroeconomic instability in the country. Unfortunately even NRB had to withdraw its HPI survey plan from this weird real estate sector of Nepal.

References:

So what changed with the new Working Capital Loan Guidelines?

Let’s discuss the changes with the help of a comparative table.

| Basis | Former Working Capital Loan Provisions in Chapter 2 of Unified Directive for BFIs | Working Capital Loan Guidelines, 2079 (With First Amendment) |

| Reference | Chapter 2 of the Unified Directive, 2078 – Page 25-27 Unified Directive, 2078 | Working Capital Guidelines, 2079 With First Amendment |

| Applicable to | Class A, Class B, Class C BFIs | Class A, Class B, Class C BFIs and Infrastructure Development Banks |

| Multiple Banking Declaration | The borrower should make a self declaration for multiple banking services in the format prescribed in form number 2.6 of Unified Directive. | |

| Pari Passu Agreement | Where a BFI is lending working capital loan ≥ 1 crore and the borrower is obtaining working capital loan from more than one BFIs, a pari passu agreement has to be drawn between the lenders. | Where the borrower is availing working capital loan ≥ 10 crore from multiple BFIs, a pari passu agreement has to be drawn between the lenders. |

| Reporting of multiple banking borrowers | BFIs are required to submit the details of the borrowers who avail credit from multiple banks to NRB in the format prescribed in the form number 2.5 of Unified Directive. | |

| No Objection Letter | Where a BFI is lending working capital loan < 1 crore and the borrower is obtaining working capital loan from more than one BFIs, a no objection letter has to be obtained from the other lenders by the BFI. | If it is revealed in the credit information of the borrower that the borrower has been availing more credit facilities > 1 crore from other BFIs, the lender shall have to obtain the No Objection letter from the other BFIs before approving the working capital credit. This credit information has to be obtained and updated on a semi annual basis. |

| Determining Credit Limit | BFIs will establish the credit limit for working capital loan based on the amount of stocks and receivables. | BFIs will establish the credit limit for working capital loan based on the amount of stocks and receivables and subject to the following provisions: (1) For borrowers with WC loans ≤ 1 Crore As per the bank’s own credit policy. (2) For borrowers with WC loans 1-2 Crore Credit limit will be set at 20% of the total annual turnover of the business. However, it can be set upto 40% of the turnover based on operating cycle, cash conversion cycle, days sales outstanding, inventory conversion period, lead time, account payable period and other criteria specific to the business. If any permanent working capital need has also been identified for borrowers availing working capital loans ≤ 2 crore then, term loan for at least 3-10 years can be provided for permanent working capital need to such borrowers within the limit of 2 crore. (3) For borrowers with WC loans > 2 crore For Fluctuating Working Capital Fluctuating working capital credit limit will be 25% of the total annual turnover of the business. For Permanent Working Capital At least a 3-10 year term loan shall be provided for the identified permanent working capital need. Credit limit for permanent working capital loan will be based on the analysis of the previous 3 year’s audited figures, 3 years projected figures of the borrower. For enterprises which have not operated for 3 years, the working capital need shall be determined based on the trend of operating expenses, estimated cash and funds flow of the business. |

| Drawing Power | Drawing power will be assessed based on the valuation and physical inspection of the current assets of the borrower before determining the credit limit. | |

| Audited and Projected Financial Statement | Credit limit will be based on the analysis of the previous year’s audited figures, 3 years projected figures and commercial and business plan of the borrower. However, a reasonable extension can be provided for the audit of the previous year’s financial statement. Similarly, micro, cottage and small scale industries availing working capital loan not exceeding 50 lakhs are not required to submit the projected financial statements. | A reasonable extension can be provided for the audit of the previous year’s financial statement. However, as soon as the audited financials are received it should be followed by the variance analysis and adjustment of credit limit and drawing power as required. Projected financial statements should be obtained on an annual basis. |

| Stock and Receivables Analysis | BFIs should perform a quarterly stock and receivables analysis (obtaining details from borrower followed by inspection from BFI) and if the analysis shows that the level of the current assets is not enough for the facility, the credit limit of the facility should be drawn down as required. Provisions should be made to inter-exchange such information with the other lenders if the borrowing is subjected to pari pasu lending. | BFIs should perform a quarterly current assets analysis (obtaining details from the borrower followed by inspection from BFI). Once a year such inspection should be made in unannounced impromptu inspection. The inspection should include the review of the VAT Registers, Excise Registers, Accounts Receivables, Account Payables, Quality and realizability of the goods and so on. The analysis should also entail if the utilization of the working capital loan matches with the collection and payment relating to the working capital. If the payment for the raw materials are overdue than as agreed with the supplier, such stock of raw materials cannot be treated as a part of the inventory for working capital analysis. Attention should be given by the BFIs if the borrower has been regularly making payment for the statutory liabilities like employee payables, social securities, taxes, fees to be paid to government, and ensure or obtain assurance that they will be paid, before the renewal of the loan. BFIs should develop a continuous monitoring system for the working capital details of the borrower into the Core Banking System or appropriate Management Information System (MIS). |

| Renewal and Review of Credit Limit | General tenure of less than 1 year with renewal facility was followed. | The renewal of the working capital loan should be made after the variance analysis. Once the credit limit has been set based on the projected financials submitted, the limit cannot be revised by obtaining other projected financials, until the previous audited financial statement has been obtained. For no reason, the credit limit can be reviewed within 6 months from the date of disbursement of loan. No increment in the credit limit for working capital loan or new working capital credit may be provided to the existing borrowers on the quarter end months i.e. Ashoj, Poush, Chaitra and Ashad. However, this provision shall not prevent renewing the working capital loan and disbursing the working capital loan within the approved credit limit. (1) For borrowers with WC loans ≤ 1 Crore Renewal and review of the credit limit is made as per the bank’s own credit policy. (2) For borrowers with WC loans > 1 Crore For Fluctuating Working Capital Loans The tenure of the loan shall be ≤ 1 year and these loans are renewable. For Permanent Working Capital Loans Permanent Working Capital Loans are in the nature of term loan for the period of 3-10 years. |

| Certification of Working Capital Details from Auditor | For working capital loans exceeding 25 crore, the details of the working capital submitted by the borrower should be certified by an Auditor. As per the decision of 231st council meeting dated 2075/09/08, an independent auditor, excluding the following CoP holders, are eligible to certify the working capital statement of the borrower: Reference: Guideline on Verification of Working Capital Statement (Page 12) | Following statement of the details of net current assets should be kept updated in the loan file: (a) For working capital loan ≤ 5 crore, quarterly statements attested by the customer himself (b) For working capital loans > 5 crore, semi-annual statements certified by the internal auditor of the borrower. Reference: |

| Information Board | The borrower must place a notice board with the name of the firm/institution/company, address of the mortgaged place, registration number and the details of the mortgaging BFI in the place, shop, warehouse or industry where the inventories are kept. | |

| Secured Transaction | The details of the movable property accepted as collateral by the BFIs while issuing or renewing the credit should be registered at the Secured Transaction Registration Office. BFIs must accept movable property as collateral only after confirming that there is no collateral in other banks and financial institutions by taking details from the Secured Transaction Registration Office before accepting the collateral. | |

| Insurance of Working Capital | Where the working capital loan is secured by the stock, the stock should be insured. However, fire, earthquake, riot insurance is not required for Iron Rod, Steel Billets, Bricks, Clinker. | BFIs must arrange for compulsory insurance based on the analysis of the risks that may occur in the collateral goods while approving current capital loans. BFIs should inform the respective borrowers to renew the insurance policy at least 15 days before the expiry of the insurance policy. If the borrower does not renew the insurance policy even before one day from the expiration, BFIs must renew the insurance by spending from the loan account. If there is any reason that the inventory is not required to be insured it should be mentioned compulsorily while approving the loan. The first claim of insured current assets should be of the lending BFI. BFIs can transfer the amount received from the payment of insurance claims to the borrower only if the repayment of the loan is regular. |

| Hypothecation, Pledge and Mortgage | Class B and Class C institutions cannot provide credit against the hypothecation of current assets. General practice among the lenders was to obtain multiple primary securities (e.g. hypothecation and mortgage) and abundant secondary collaterals to secure the working capital lending. | Class B and Class C BFIs cannot provide credit against the hypothecation of current assets. As working capital loan is for the working capital requirement of the borrower, such loan should be secured by current assets. The working capital lending policy of the bank should disclose the amount and margin required for the credit. Fixed and/or immovable assets (such as house, land, etc.) will not be required to be secured for working capital loans other than movable assets. |

| Variance | Variance analysis for Working Capital Loans for renewal or review of the credit limit entails the followings: For Fluctuating Working Capital Loans If the actual audited turnover varies from the projected turnover by more than 20% negatively for previous year, then Revised Credit Limit for current year = ( Projected Turnover for current year × Applicable Credit Limit % ) × ( 1 – Variance % × 50 % ) For Permanent Working Capital Loans If the actual audited turnover varies from the projected turnover by more than 25% negatively for previous 3 years in average, then Revised Credit Limit for current year = ( Projected Turnover for current year × Applicable Credit Limit % ) × ( 1 – Variance % × 50 % ) Any permanent working capital credit released in excess of the revised credit limit should be repaid within a period of 1 year. | |

| Account Operation | The current account and the loan account of the borrower of the working capital loan has to be operated separately. Arrangement has to be made for depositing all the revenue proceeds of the business into the current account of the borrower. Also, the borrower can give a standing instruction to the bank to transfer the current account amount to the loan account. The amount in the loan account should be transacted only by direct transfer for commercial purposes. Cash withdrawal or non business account transfers cannot be made in excess of 2% of the total credit limit. | |

| Zero Arrears Test | All renewable working capital loans must have zero arrears for at least 7 consecutive days according to the nature of the business at any one time during the year. However, this arrangement can be implemented as follows for 3 years from the effective date of the guideline: (a) For the first year, the borrower can maintain arrears of less than 30% of the call loan limit for 7 consecutive days. (b) For the second year, the borrower can maintain arrears of less than 20% of the total loan limit for 7 consecutive days. (c) For the third year, the borrower can maintain arrears of less than 10% of the total credit limit for 7 consecutive days. | |

| Debt to Equity Ratio | Clause 1 of Chapter 2 Classification of Loans/advances and Loan Losses of the Unified Directive classifies lending with debt equity ratio exceeding 80:20 under watchlist category. | The debt equity ratio prevailing according to the prevailing directive should be complied with while determining the current capital loan limit. |

| Ad Hoc Working Capital | If there is an unexpected need for financial resources for any purpose related to the borrower’s business, an ad hoc working capital loan can be provided in a way that the amount is directly released for the related purpose. Such ad hoc working capital loans cannot be renewed ro utilized for other purposes. If a borrower needs an ad hoc loan of this nature more than once in a financial year, the board of directors of the concerned bank and financial institution may decide to grant such a credit. | |

| Lending in Excess of Credit Limit | Working capital loan provided prior to 2079.07.01 in excess of the prescribed limit under this guideline shall be repaid on semi annual basis and settled before Ashadh 2082 in the following manner:

| |

Some Key Concepts:

💡What is Pari-passu agreement?

Pari-passu is a form of “equal footing” is a financing arrangement that gives multiple lenders equal/agreed claim to the assets used to secure a loan. If the borrower is unable to fulfill the payment terms, the assets can be sold, and each lender receives their agreed share of the proceeds at the same time. Pari Passu agreement should contain the amount being lent, the assed being secured, agreed share of the lenders on the asset, process for credit recovery, auction proceedings and dispute resolution mechanism between the lenders. The agreement is typically entered into between the borrower and the lenders.

💡What is a operating cycle?

The operating cycle refers to the time it takes for a company to convert its current assets (such as inventory and accounts receivable) into cash. It is essentially the period of time from when a company invests in inventory and other resources to the time it collects cash from the sale of those resources. It is typically calculated using the formula = Inventory Conversion Period + Accounts Receivable Period – Accounts Payable Period

💡What does limiting credit to 20% of turnover mean in term of the operating cycle in days?

When the working capital credit is limited to 20% of the turnover it is comparable to the business having an operating cycle of (12×20%) 2.4 months. Any business that has the operating cycle more than 2.4 months will not be able to fully rely on the working capital loan to meet their working capital needs, they will have to apportion a part of their capital as working capital fund to be utilized for working capital need.

💡What is a Credit Limit and Drawing Power?

Credit limit refers to the maximum amount of credit that a bank is willing to provide to a borrower under a specific credit facility. It represents the upper limit of the amount that the borrower can borrow at any given point in time. The credit limit is determined by the bank based on various factors such as the creditworthiness of the borrower, the purpose of the credit facility, and the collateral provided by the borrower. Example: A company has a projected sales of 2 crore. As per the Working Capital Loan Guidelines, the bank is required to set the credit limit at a maximum of 20% of 2 crore, i.e. 40 lakhs.

Drawing power, on the other hand, refers to the amount that the borrower can actually draw or utilize from the credit facility at any given point in time. The drawing power is calculated by the bank based on the value of the collateral provided by the borrower and other factors such as the age and quality of the inventory or receivables, the market value of the collateral, and the loan-to-value ratio. The drawing power is always less than or equal to the credit limit, depending on the value of the collateral and other factors. Example: A company has a projected sales of 2 crore. As per the Working Capital Loan Guidelines, the bank is required to set the credit limit at a maximum of 20% of 2 crore, i.e. 40 lakhs. However, the working capital position (Current Assets – Current Liabilities) of the company is only 30 lakhs and the bank has the policy of lending at 20% margin against the net current assets. Then the drawing power of the company is set at 80% of 30 lakhs, i.e. 24 lakhs.

💡Difference between renewal (नवीकरण) and review of credit limit (कर्जा सीमा पुनरावलोकन).

Renewal of a working capital loan refers to the extension of an existing loan agreement after the expiry of its original term. In contrast, a review of the credit limit for a working capital loan is a periodic assessment conducted by the lender to determine the borrower’s creditworthiness and the adequacy of the existing credit limit. When a working capital loan is renewed, the borrower and lender usually negotiate new terms and conditions for the loan, including interest rates, repayment schedules, and other relevant factors. Based on this review, the lender may decide to increase or decrease the credit limit or maintain it at the current level. The review is usually conducted without the need for a formal loan renewal process.

💡What is Secured Transaction Registry?

Link: Secured Transaction Registry Office of Nepal

Secured Transaction Act, 2063 provides a data framework for lenders to take security interests in a borrower’s assets to secure a loan.

Under the Secured Transaction Act (STR Act), when a debtor, such as a business owner, trader or entrepreneur, seeks a loan or credit line from a lender, they may offer a security interest in their equipment, inventory, accounts receivable or other assets. The lender must then search the records of the secured transactions filing office to determine if the proposed collateral is subject to a prior security interest or lien. This search is typically done using the debtor’s citizenship number or the institutional name or company registration number. If there is no prior notice of a security interest in the proposed collateral, the lender can file a notice of its prospective interest in the debtor’s collateral, giving it priority over other lenders. However, if a notice of security interest in the proposed collateral has already been filed by another party, the lender has several options. They may contact the prior secured party to determine if the existing obligation is small enough that there is sufficient excess value in the collateral to secure the proposed loan and file their own notice of security interest. Alternatively, they may try to obtain an agreement with the prior secured party to subordinate their prior interest to the current secured party’s interest, or they may choose not to lend based on the risk of the prior security interest. Overall, the STR Act provides a data framework for lenders and borrowers to secure transactions involving personal property, with the aim of reducing risk and increasing confidence in lending.

💡Difference between Hypothecation, Pledge and Mortgage in the context of working capital lending?

Hypothecation: Hypothecation involves offering movable assets, such as inventory or accounts receivable, as security for a loan, without transferring possession of the assets to the lender. In case of default, the lender has the right to take possession of the assets and sell them to recover the loan amount.

Pledge: Pledge involves offering a specific asset, such as jewelry or stocks, as security for a loan by transferring its possession to the lender. The ownership of the asset remains with the borrower, but the lender has the right to sell it in case of default.

Mortgage: Mortgage involves offering immovable property, such as a house or land, as security for a loan. The lender has a security interest in the asset, which means that if the borrower fails to repay the loan, the lender has the right to foreclose on the property and sell it to recover the outstanding loan amount.

💡What is Zero Arrears Test?

Zero Arrears Test ensures that the borrower is managing their working capital effectively. If a borrower is able to operate their business with the cash generated from their operations and without relying on the working capital loan for some period during the year, it shows that the borrower is managing their working capital effectively in their business.

Reference: Aspects of Analyzing and Managing Working Capital Loans

Temporary, Permanent and Ad Hoc Working Capital Requirement

Remember your cost functions from the elementary chapters of financial management lectures?

Profit = Units Sold × (Sales Price – Variable Cost) – Fixed Costs

Is there a test to distinguish temporary and permanent working capital like the one we have for distinguishing variable and fixed costs? Well, although we might be tempted to think that the working capital needs created by the fixed costs are permanent working capital and those created by variable costs are temporary working capital, that is not the case. The difference is quite subtle to put in words but totally drastic from the concept of fixed and variable costs.

So, what is the “litmus” test? What is permanent working capital?

Permanent working capital can be defined as the minimum level of net current assets that a business needs to maintain in order to ensure its smooth and efficient day-to-day operations. Without this minimum level of working capital, the business would experience significant disruption and may even be forced to cease operations.

So, isn’t permanent working capital the level of working capital that is typically maintained at the level of break even sales?

Not necessarily. Sustaining fixed cost is a very mathematical approach at looking at what level of sales is required for a company to exist. Cost Function Analysis (discussed above) is extremely useful in product pricing, variable cost analysis and appraisals of the new sales opportunities, but a business for practical purposes may be forced to cease or discontinue well before hitting low into the break even sales point. Similarly, some businesses may be able to sustain the losses even while operating at level below the break even sales.

So, if it is not the level of fixed costs that necessarily/solely drive the level of the permanent working capital requirement. It may be the level of working capital that is maintained at the level of break even sales, or at any point below or above it. Factors like nature of the company, capital structure, size of business, goods conversion period, AR and AP period, business cycle, profitability, size of orders and contracts all impact on what the permanent capital need for the business may be.

In general, the permanent working capital requirement tends to be higher than the temporary working capital requirement. This is because the permanent working capital requirement represents the ongoing needs of the business to maintain its day-to-day operations, while the temporary working capital requirement is typically related to seasonal or short-term fluctuations in sales or expenses. However, the relative level of each type of working capital requirement will vary depending on the specific characteristics of the business.

Let’s take two examples:

- Let’s say a business sells seasonal products, such as Holi toys. The business requires a certain level of permanent working capital to carry out its day-to-day operations, such as paying rent, utilities, and salaries. However, as Holi approaches, the business experiences a surge in sales and needs to increase its inventory and accounts receivable to meet the demand. The increase in inventory and accounts receivable is a temporary fluctuation in the business’s working capital requirement, as it is driven by the seasonal increase in sales. Once Holi is over, the business will sell off its excess inventory and collect on its accounts receivable, returning to its normal level of working capital. On the other hand, the business’s permanent working capital requirement remains relatively constant throughout the year, as it is driven by the fixed costs of the business that must be covered regardless of sales fluctuations.

- Let’s take an example of a drug importer. The business has three categories of sales: Category A Sales of 50% that defines the brand, existence and profitability of the business; Category B Sales of other 50% that are really competitive. The business must maintain an ample inventory for Category A goods and provide extended credit to customers because the profitability and brand of the business really depends on this category. The business cannot afford to hold lesser inventory and backorder these products because if it loses this share, the other 50% in another category could very well be lost due to fierce competition. This will mean that, although mathematically the company could have a break even sales at 25% of the Category A products, the working capital needed to sustain the entire Category A sales should be treated as permanent working capital because in any other case the business could experience significant disruption and may even be forced to cease operations. Thus the level of working capital required to enable the Category A sales will be treated as permanent working capital.

So what is ad hoc working capital? And how is it different from the temporary working capital need?

Ad hoc working capital refers to the additional working capital that a business may require for a specific, one-time purpose or project, such as launching a new product line, expanding to a new market, or acquiring another company. Ad hoc working capital needs are typically short-term and may not recur in the future. On the other hand, the temporary working capital is required to finance the temporary increase in current assets during a business cycle or a seasonal increase in sales. Temporary working capital is required only for a short period of time, and once the business cycle or seasonal period is over, the need for temporary working capital decreases. “Anticipation” of the need is the key difference between the two. The need for temporary working capital would depend on the seasonal variations in demand, inventory build up before peak sales, unexpected delay in receiving payments from debtors, unexpected increase in production or sales due to new orders, additional fund requirements due to liquidity problems etc.

Reference: Working Capital Management: Concept, Importance and Objectives