Stephanie Kelton’s The Deficit Myth

Stephanie Kelton’s book “The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy” was a strange and thought provoking addition among both the advocates and critics of the Modern Monetary Theory (MMT). It made us believe that many conventional beliefs about government deficits and debt are based on flawed assumptions and misunderstandings. But her theories from the book revolve around the economy of the USA – a monetary sovereign – a country that has a floating exchange system, independent monetary regulations, and its public debts are denominated in the home currency. Kelton is an economist and one of the leading proponents of MMT – so her views are quite drastic in terms of the balanced budget and fiscally responsible government expenditures. Moreover, the US Dollar is a reserve currency – countries all around the globe hold USD as a means to facilitate international trade and as a security against their currency in circulation. But of course there is no comparison between Nepal and the USA – and it’s not just because one is a monetary sovereign and the other is not. There is a huge difference between the two in terms of Gross Domestic Product, Per Capita Income, Human Development Index, Income Equality and Industrialization.

Obviously even if one agrees with Kelton’s idea of a Modern Monetary Theory – it is only practically applicable to monetary sovereigns like the USA, Japan, UK, Australia etc. who have the economic privilege and capacity to borrow in their own currency. Countries like Nepal – a small and relatively open economy – with exchange and monetary policies dependent substantially with India – Kelton’s idea of MMT and free lunch of unlimited public debt is simply not an option to a country like Nepal.

What is a “monetary sovereign”?

Well, what is a monetary sovereign? The term “monetary sovereign” refers to a country that has the power to issue its own currency and control its money supply. A monetary sovereign has the authority to create new money and regulate its value through monetary policy tools such as interest rates, reserve requirements, and open market operations.

In practice, most countries are monetary sovereigns, including the United States, Japan, China, and the United Kingdom. As a monetary sovereign, a country has the ability to spend as much money as it deems necessary to achieve its economic goals, without the constraint of needing to obtain money from external sources. This is because the government has the power to create new money through its central bank, which can then be used to finance public spending or pay off government debt.

However, being a monetary sovereign does not mean that a country can spend without limit or without consequences. Inflation, for example, is a potential risk associated with excessive money creation, which can erode the value of a currency and reduce the purchasing power of consumers. Therefore, monetary sovereignty also requires responsible management of the money supply, in order to maintain price stability and avoid economic instability.

Well by that standards isn’t Nepal a monetary sovereign? Yes, but not quite. Although Nepal has its own currency, a central bank, power to create its own currency, control its money supply, and conduct monetary policy to achieve its economic goals – it’s worth noting that Nepalse economy is relatively small and less developed than many other monetary sovereign countries, and the NRB’s ability to conduct monetary policy may be more constrained due to factors such as limited international reserves and a small financial, capital and monetary market. Nonetheless, Nepal’s status as a monetary sovereign means that it has the authority to manage its own currency and money supply, and to finance its own government spending.

What is public debt?

All the debts in a sovereign nation can broadly be separated into:

- Public Debt: Public debt is the total amount of money that a government owes to its creditors, both domestic and foreign. This includes all types of debt obligations incurred by the government, such as loans, bonds, and other forms of borrowing. Public debt includes all government debts and the debts of the state owned enterprises as well. However, the terms “public debt” and “government debt” are used interchangeably but there is this subtle difference between the two.

- Corporate Debts: This is the amount that the private sector companies owe to financial institutions, multilateral/bilateral institutions to finance their operations, expansion, or investment in new projects. It can take the form of bonds, loans, or other types of debt securities.

- Household Debts: Household debt is the combined debt of all people in a household, including consumer debt and mortgage loans. This could include home loans, credit card debt, car loans, and student loans that serve a household or individual needs.

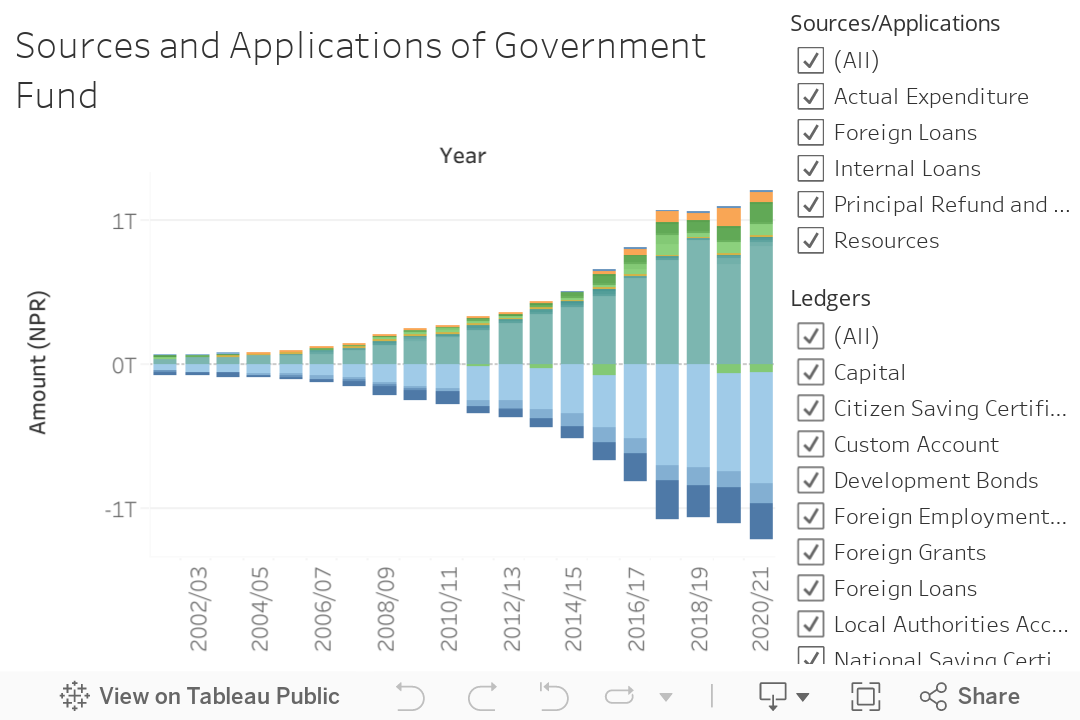

A country’s gross government debt / public debt / sovereign debt is the financial liabilities of the government sector. Public debts are raised by the government to finance the deficit spendings of the government. Governments can borrow this debt from domestic sources and foreign bilateral and multilateral sources. When borrowed from external sources, these funds come in the form of foreign currency denominated liabilities for small country like Nepal because Nepal doesn’t have the capacity, market or global economic trust and strength to borrow them in local currency.

In 2020, the value of government debt worldwide was $87.4 US trillion, or 99% measured as a share of GDP. Government debt accounted for almost 40% of all debt (which includes corporate and household debt), the highest share since the 1960s. The rise in government debt since 2007 is largely attributable to the global financial crisis of 2007–2008, and the COVID-19 pandemic.

Let’s draw the meaning from the above figures. Is there something inherently wrong in comparing public debt as a percentage of GDP? GDP is not the government’s revenue – it is the country’s revenue and the assets and productions leading to the GDP constitutes more from the private sector rather than the government sector. It is so misguided. If you were a company would you compare your debt with your income or with the total income of your industry. Of course – it’s obviously your income – the other doesn’t make sense. Of course the government is not an organization like a company – but it is in many ways. The debt to GDP ratio only exaggerates the government’s results and that too is not working out too much for them. Governments around the world run on almost 100% debt to GDP ratio – we will look independently at Nepal’s statistics below.

Why public debt?

This all has to do with who you vote for in your general election. The political promises are unachievable and are costly most of the time. The government will head into a budget deficit and they will have to resort to either printing the money or to borrow the money. Printing money against the government security is not an easy or wise option to countries like Nepal where it is difficult to practice independent monetary practices and policies and also due to NPR being pegged to INR. So most of the time the government resorts to domestic and foreign debts to finance the expenses of the country. But why does the government not have money – even when it is capable of raising taxes to fund its expenses? Why are the public expenditures not financed entirely by public revenue?

The way to understand it is by dividing the population into two parts – the rich 10% of the and the poor 90% of the population. What do they each want? Each group doesn’t want to pay the taxes and they want the maximum benefits from the government. The government statutorily has to spend on the security, health, education, justice and system of infrastructure in the country. But the problems are (i) nobody wants to pay the taxes, (ii) everyone wants the government to spend the most on their benefits (iii) the government is a huge inefficient engine that tends to always spend more than what is necessary. This is true for all the nations of the countries in the world – United States and Nepal alike.

So what does the government do? How can you massively spend without collecting taxes? Obviously you borrow. So the government borrows and everyone is happy. What would you do if you had to keep delivering the things to the people who didn’t want to pay for them? That’s all fine and dandy at the start but when the lenders realize that the government doesn’t have the money to repay the loans – government will have to find resort to austerity measures – that could be (i) repaying the debts by issuing further loans (ii) stop delivering the services and benefits (iii) raising taxes (iv) repaying loans through further issue of currencies. These measures leads to many negative impacts like:

- Reduced government services will lead to a negative impact on the vulnerable populations of low income families, seniors and people with disabilities.

- Austerity measures often involve cuts to government spending and public sector jobs leading to unemployment in the government and industries that rely heavily on the public sector spendings.

- Austerity measures will lead to reduced consumer spending that contributes to slowing down of the business and economies.

- Austerity measures disproportionately impact low-income households and marginalized communities that exacerbates existing social and economic inequalities.

- It can lead to public unrest and controversies leading to social and political unrest.

Borrowing allows a country to invest and consume beyond its current level of revenue mobilization and capacity to save and produce. However, no country can borrow indefinitely since an unsustainable level of borrowing results in a debt crisis. If not managed properly, it can be a huge burden to the economy and future generations.

Public Debt was not so popular until Keynes

Historically, there is great debate among economists about the role of public debt. The classical economists were, generally, against public borrowing.

Classical economists assumed that in the long-run, actual GDP automatically adjusts to the potential GDP. So, due to this reason, classical economists were not in favor of counter-cyclical fiscal policy. They further assumed that the private sector can employ resources more efficiently than the public sector. They were, generally, in favor of a balanced budget.

But, Keynes was against the view of classical economists. When actual GDP is lower than potential GDP, it indicates that there is spare capacity in the economy that is not being utilized. This could happen due to various reasons such as a decrease in aggregate demand, increase in unemployment or structural unemployment, supply-side factors like a decrease in the labor force or capital stock, or policy interventions that discourage economic activity. So he argued that resources in the private sector may remain unemployed for a long period, if corrective or compensatory action is not employed by the government. So, in such a situation, when the government borrows the idle resources from the private sector, it would not be unproductive but rather would have positive effects on the income of the country.

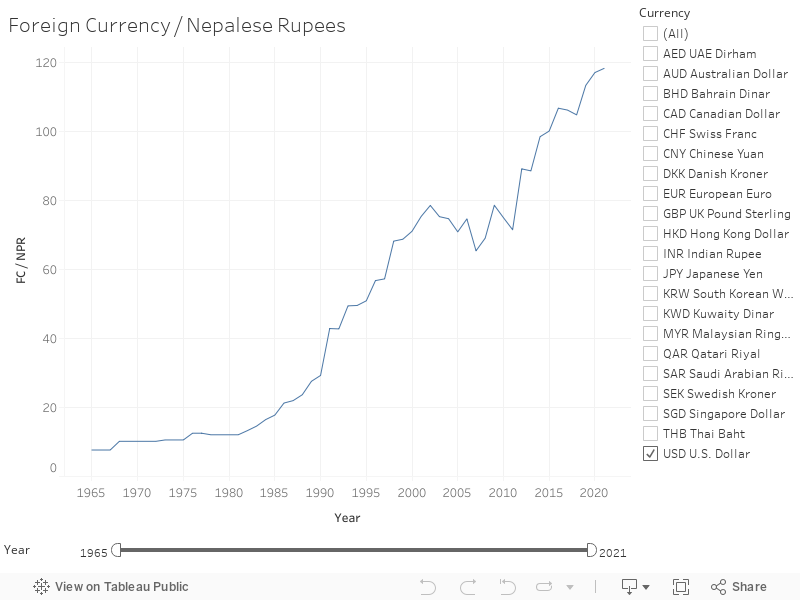

The alternative to raising loans is taxation. It is generally said that, if possible, it is better to finance the government expenditure through taxation. It is because the taxed amount is not required to be refunded but loan should be refunded; foreign loan can create the interference in the domestic economic and political issues; if the size of borrowing is large, ultimately it calls for heavy taxation; and due to the easiness to borrow money, government may fail to maintain the fiscal discipline. However, in least developed countries like Nepal there are many limitations on raising resources through taxation. Low levels of income of people, low level of economic transactions, possible inflationary effects, etc. are the limiting factors in the collection of tax revenue in Nepal. On the other hand, as a least developed country, Nepal can get foreign loans at a relatively lower rate of interest. So, if the economy can utilize the foreign loans in an efficient way, it will create more opportunities for the people. Foreign loans provide the resources in foreign currency, which the government cannot get by means of taxation, which is its benefit but there really needs to be an ideal balance because foreign loans might be costly to countries like Nepal where the real effective exchange rate is depreciating most of the time.

Public Debt Status of Nepal

As of 2021, Nepal’s total public debt was estimated to be around $12.7 billion, with the external debt accounting for around 25% of the total debt. The major sources of Nepal’s public debt include multilateral institutions such as the World Bank and the Asian Development Bank, bilateral creditors such as China and India, and international capital markets.

Despite the high level of public debt, Nepal has maintained a stable debt-to-GDP ratio, which was around 30% in 2020. The government has implemented various measures to improve the debt sustainability, including controlling the fiscal deficit, increasing revenue mobilization, and prioritizing expenditure on development projects. However, there are concerns over the sustainability of Nepal’s public debt, given the country’s high reliance on external borrowing, limited revenue sources, and susceptibility to external shocks such as natural disasters and pandemics. Therefore, the government needs to implement effective debt management strategies to ensure the long-term sustainability of the public debt.

Nepal has seen a rapid rise in debt in recent years after the country was forced to spend more on reconstruction after the 2015 earthquakes as well as during the Covid-19 crisis and the implementation of federalism.

By the first quarter of 2022, outstanding debt of Sri Lanka had reached 127 percent of the GDP, according to official data. In May, Sri Lanka defaulted for the first time in history with the country facing a crunch of foreign currency due to reduced tourism income, curtailed revenue and rising import bills. The economic crisis resulted in the disgraceful departure of the Rajapakya family from power in Sri Lanka. Likewise, Pakistan is also facing an economic crisis as it struggles to pay its enormous debt with its limited foreign exchange reserves. By December 2021, Pakistan’s debt to GDP ratio stood at 70.7 percent of the GDP, according to the World Bank. El Salvador, Ghana, Egypt, Tunisia and Pakistan are nations that Bloomberg Economics sees as vulnerable to default. Nepal is not on the list.

The above statistics begs a question: How are countries like Japan, USA, UK and Germany able to sustain such a massive level of the public debt while other countries like Egypt, El Salvador, Ghana, Tunisia find it difficult to even level at lower debt to GDP ratios? The answer is that the countries like Japan, USA, UK and Germany are monetary sovereigns. They do not have the need to borrow in the foreign currency because they have a positive balance of payment and/or their currencies are held as monetary reserves by the central banks all around the world, which imperatively leads to the relative strength of their currencies.

Monetary sovereigns usually do not default in the public debt because their debts are denominated mostly in their own currencies and because they have the power to create their own currency and control its supply. This means that they can always print more money to pay off their debts, as long as the debt is denominated in their own currency. Since the government controls the supply of its currency, it can create new money to pay off its debt obligations, without the need to rely on external sources of funding. In other words, the government can simply “monetize” its debt, which means printing new currency to finance the deficit.

However, this is not a complete free lunch. It does not mean that monetizing debt is always a desirable or sustainable option. Excessive money creation can lead to inflation and currency devaluation, which can have negative consequences for the economy and the standard of living of the population, and create a vicious cycle of inflation, currency devaluation, leading to having to resort to the foreign debts.

The above stacked chart shows the composition of the public debt of some of the strong and weak (in terms of public debt austerity) countries around the world. It is observable that despite the strong economies of monetary sovereigns having a high degree of public debt (as observed in the table above), the unique advantage they have is that the debt is mostly composed of the local currencies. As discussed above, monetary sovereigns usually do not default in the public debt because their debts are denominated mostly in their own currencies and because they have the power to create their own currency and control its supply.

Public Debt Regime in Nepal

Budgeting in Nepal began in 1951 AD, but deficit budgeting became frequent soon after. To finance these deficits, the government has relied on foreign and internal loans, as well as changes in cash reserves. Public debt has thus become an important tool for Nepal’s fiscal policy. However, public debt was not introduced until 11 years after the initiation of budgetary practices. Domestic loans were first taken in 1962, followed by external loans in 1963 from countries such as the former USSR and UK. Since then, public debt has played a crucial role in the government’s budget.

In making borrowing decisions, the debt managers of the country faces such choices as:

- Whether to borrow from official sources (e.g., bilateral sources and international financial institutions) or from commercial creditors.

- Whether to borrow in the offshore capital market or in the syndicated bank loan market.

- Decisions on the size, timing, schedule and spread of their borrowings.

- Whether to use derivatives in borrowing (e.g., whether to borrow through “plain vanilla” capital market instruments or through more structured transactions involving private placements), and, if derivatives are used, how to manage the ensuing counterparty credit risk.

Monetization of Fiscal Deficit in Nepal

Automatic monetization of fiscal deficit occurs when the central bank (such as the Nepal Rastra Bank) directly finances the government’s budget deficit by creating new money. This means that the government spends more money than it collects in revenue, and the central bank prints new money to buy government bonds and finance the deficit. This process can lead to inflation as the increased money supply leads to a decrease in the value of the currency. Additionally, it can reduce the confidence of investors in the economy, leading to lower investment and economic growth. In contrast, a more sustainable approach to financing the government’s deficit is through borrowing from the private sector or from external sources. This reduces the pressure on the central bank to print new money, and helps to maintain the stability of the economy in the long term.

Automatic monetization of fiscal deficits is a controversial policy and is generally discouraged by international organizations such as the International Monetary Fund (IMF). Many central banks have laws or regulations in place to limit or prohibit direct financing of government deficits to maintain the independence of the central bank and prevent inflation. However, in some cases, such as in Zimbabwe in the early 2000s, automatic monetization of the deficit has been practiced, leading to high inflation and economic instability.

However, it is important to note that the provisions of the NRB Act (which we will discuss below), allows for certain forms of credit to the government under specific conditions, that can be repaid in the form of cash or marketable government bonds. But there is a percentage limit as to how much of such amount can be monetized and NRB Act also lays the composition on how the currency in circulation should be backed – it cannot be all backed by the government bonds and treasuries.

PDMO and PDMC

Public Debt Management Office (PDMO) under the Ministry of Finance is the main government agency responsible for public debt management. It was formally inaugurated on Poush 11, 2075 and started to perform the preliminary functions. Front office functions, middle office functions and back office functions are the main responsibilities of the PDMO. Under previous legal regime, Nepal Rastra Bank (NRB) was responsible for the front office function (managing internal borrowing for the government), Financial Comptroller General Office (FCGO) for back office function (debt servicing) and Ministry of Finance for middle and back office function as well as overall public debt management. With the introduction of the new Public Debt Management Act it has provided legal backup to the PDMO to perform given responsibilities. As well as functional clarity will be enhanced between the concerned entities for the public debt management functions.

The steering committee of the PDMO is Public Debt Management Committee (PDMC) which is constituted with the following members:

- Secretary (Revenue), Ministry of Finance

- Financial Comptroller General, Financial Comptroller General Office

- Executive Director, Research Department Nepal Rastra Bank

- Executive director, Monetary Management Department Nepal Rastra Bank

- Joint-Secretary, Economic Policy Analysis Division Ministry Of Finance

- Head Of Office, Public Debt Management Office

The old and transitory public debt management practices in Nepal

The process of raising public debt in Nepal typically involves the Ministry of Finance deciding on the amount of debt required to meet budgetary needs. The Ministry then submits a debt management plan to the Cabinet, which must approve any new debt issuance. The Central Bank of Nepal then conducts auctions to sell the debt instruments to investors, both domestic and foreign. Once the debt is issued, the government is responsible for making regular interest and principal payments according to the terms of the borrowing agreement. The Office of the Financial Comptroller General is responsible for monitoring and managing the government’s debt service payments.

The process of determining external or domestic finance requirements in Nepal involves a resource committee comprising the Vice Chairman of the National Planning Commission, the Finance Secretary, and the Governor of Nepal Rastra Bank. Once the requirements are determined, the Ministry of Finance (usually through the Foreign Aid Coordination Division) signs loan or grant agreements with bilateral or multilateral donors. These loans or grants are then utilized by various line ministries.

Disbursement of funds can be made in various forms, including cash disbursement, reimbursement, and direct payments. The Office of the Financial Comptroller General is responsible for issuing debt service payment instructions according to the repayment schedule specified in the loan agreement. In turn, the Nepal Rastra Bank’s Foreign Exchange Management Department externalizes debt service payments in the specified currency.

If debt rescheduling or restructuring is required, it is carried out by the Ministry of Finance in consultation with the Office of the Financial Comptroller General. Additionally, the Ministry of Finance, in consultation with the Nepal Rastra Bank, decides on domestic borrowing instruments and the share of each instrument. The Nepal Rastra Bank administers domestic borrowings on behalf of the Ministry of Finance. Finally, the Office of the Financial Comptroller General is responsible for paying principle, interest, and other domestic debt service obligations.

With the establishment of the PDMO Office under the Ministry of Finance, much of these front office, mid office and back office functions carried out though the various units of the government are expected to be coordinated and managed by the Public Debt Management Office. With the introduction of the new Public Debt Management Act it has provided legal backup to the PDMO to perform given responsibilities. As well as functional clarity will be enhanced between the concerned entities for the public debt management functions. So we are in a transition phase for the public debt management issues.

Legal power to obtain the public loan

Article 59(6) of the Constitution of Nepal, 2015 provides that the Government of Nepal shall have power to obtain foreign assistance and borrow loans. Such assistance or loans shall be so obtained or borrowed as to have macro-economic stability of the country. Article 115(2) of the Constitution prevents the government from collecting loans and providing guarantees except as provided in the Federal Law. Federal Law, Public Debt Management Act, 2079 (PDMA) allows the government to obtain foreign and local loans and to provide the guarantees as per the provision within. This we will discuss below.

The Constitution of Nepal

PDMO and NNRFC

Public Debt Management Office (PDMO) as the name suggests is the management office. It is not a unit that takes the decisions on raising the public debts. PDMO, as per the limits, guidelines and framework set by the National Natural Resources and Fiscal Commission (NNRFC) and the budgetary projections and requirements submitted by the various levels of the government, projects the annual requirement for the government debts and preparing payment schedules. PDMO is also responsible for reporting public debt statistics, collecting debts and disbursing them to the various levels of the government, documenting the records of the guarantees issued by the government and releasing and auctioning the internal debts and treasuries.

NNRFC is a constitutional body of Nepal established with the objective to ensure just and equitable distribution of natural and fiscal resources among federal, state and local governments. The commission makes recommendations to the governments regarding revenue distribution, equalization grant, conditional grant, internal borrowing and sharing of natural resources among the three tiers of governments.

सार्वजनिक ऋण व्यवस्थापन कार्यालय

राष्ट्रिय प्राकृतिक स्रोत तथा वित्त आयोग

Raising foreign and domestic loans under PDMA

Foreign loans are obtained by the authority of Nepal Government and it is a federal liability unless it is specifically obtained for the purposes of the provincial or the local government. Domestic loans can be obtained by the authority of Nepal Government or the local and provincial government on the consent of the Nepal Government. The domestic loans may be raised in the form of treasury stock, promissory notes, prize bonds or other form of loan instruments. (Prize Bond means a non-interest bearing Security which is entered into a prize draw whereby the owner of a randomly selected bond receives a prize payout). Domestic loans are obtained through the auction process. The details on the type of the loan instrument, amount, interest rate, payment schedule, timeframe to participate in the auction process and other conditions are disclosed in the national level newspaper before the auction. These instruments may be listed in and transacted through the stock exchange. Till the date of writing this blog, there has not been any publicly listed government bonds and treasury bills, they have been publicly auctioned off, but not listed in stock exchange.

In addition to the foreign and domestic loans, Nepal Government is also authorized by the power of the Act to provide guarantees to other governments and financial institutions for the projects approved by the government. For example Nepal Government had provided guarantee to Employees Provident Fund and Citizen Investment Trust on behalf of Nepal Airlines Corporation for the purchase of two airplanes A330-200 in 2074/01/07. Nepal Government may also provide counter guarantees on the loans obtained by the local and provincial governments. But the Nepal Government should ensure the purpose of the loan, national interest in obtaining the loan and servicing capacity of the country while providing such guarantees and counter guarantees.

Public Debt ceilings in Nepal

Public debt ceilings are maximum limits on the amount of public debt that a government is allowed to incur. These ceilings are set by the government or a legislative body and are typically expressed as a percentage of the country’s gross domestic product (GDP). The purpose of public debt ceilings is to limit the amount of debt a government can incur in order to prevent excessive borrowing and to ensure that the government’s debt remains sustainable over the long term. By establishing debt ceilings, governments can control their debt levels and avoid the negative economic consequences of excessive debt, such as high interest payments, inflation, and reduced access to credit markets.

Public debt ceilings in Nepal are constructed in both the mathematical and proprietary framework. Constitution of Nepal, 2015 authorizes the government to obtain public debt. All public debts obtained by the government should be borrowed considering the macroeconomic stability of the country – this is a proprietary limit. Similarly the Section 5(2) of the Public Debt Management Act, 2075 prevents the government from obtaining a total foreign currency loan in excess of one-third of the total GDP of the previous fiscal year (expressed in current prices and adjusted for exchange rate).

सार्वजनिक ऋण व्यवस्थापन ऐन, २०७९: वैदेशिक ऋण

दफा ५(१): वैदेशिक ऋण लिने अधिकार नेपाल सरकारलाई हुनेछ।

दफा ५(२): नेपाल सरकार, प्रदेश सरकार तथा स्थानीय तहको योजना तथा कार्यक्रम वा नेपाल सरकारद्वारा स्वीकृत परियोजना कार्यान्वयनको लागि नेपाल सरकारले कुनै विदेशी सरकार, विदेशी सरकारी बैङ्क वा वित्तीय संस्था वा एजेन्सीबाट आवश्यकता अनुसार जम्मा ऋणको कूल अङ्क अघिल्लो आर्थिक वर्षको कुल ग्राहस्थ उत्पादनको प्रचलित मूल्यमा कायम गर्दा हुने रकमको एकतिहाइमा नबढ्ने गरी त्यतिसम्म अङ्कको प्रचलित विनिमय दरले हुने विदेशी मुद्रा एकै पटक वा पटक पटक गरी ऋण लिन सक्नेछ ।

This is a debt ceiling set for the foreign currency loan but there isn’t any debt limit set for the domestic loans. Only the proprietary framework ceilings apply in the case of domestic debt, nothing mathematical. Though Nepal’s debt level is not alarming, the country’s total debt is in increasing trend. As of 2022, with the share of external debt reaching an equivalent of 21.14 percent of the GDP, there is still room for Nepal to increase foreign debt acceptance by around 12 percent following the new law’s introduction. Nepal is not a highly indebted country, most debts have long payback periods, and they have been taken at concessional interest rates but the major pain of the foreign debt in Nepal despite lower borrowing cost is the depreciation in राष्ट्र ऋण उठाउने ऐन, २०७७the real effective exchange rate of NPR against other currencies.

As the budget is set and announced annually, along with the Annual Finance Act (after the Annual Finance Bill has been ratified by the parliament), an Annual National Debt Issue Act is also introduced as a fiscal law. This National Debt Issue Act specifies the amount of the national debt that the government can issue for the fiscal year based on the proposed budget of income and expense for the year. This typically includes provisions where the overdraft of the government can be converted into treasury bills or issue fresh bonds and treasury bills. However, this limit set annually through the National Debt Issue Act doesn’t include the overdraft facility that the government enjoys from the Nepal Rastra Bank.

Credits from NRB to GON

As per Section 75 of the Nepal Rastra Bank Act, 2058 NRB is prohibited from providing any form of financial assistance to the GON or any institution wholly or partially owned by the GON except as provided for in the Act. Following credit or monetary facilities may be provided to GON by NRB in Nepalese currency bearing interest at market rate with a condition to repay within 180 days in cash or marketable debt bond.

- Overdraft Credit / Ways and Means Advances (WMAs): Overdraft credit provided by NRB to GON shall not be more than 5% of the revenue income of the GON in the preceding fiscal year. Overdraft credit allows the government to continue with the expenses when there is insufficient recovery of income.

- Special Credit: Special long-term credit may also be extended to the GON by the NRB for the purpose of payments resulting from subscription/membership of Nepal with international organizations. (Example – fulfilling liabilities of multilateral organizations)

- Other Credit: NRB may provide credit to GON by the means of purchase of debt bonds from GON. The total amount of debt bond purchased by NRB from GON and taken into its ownership shall not be more than 10% of the revenue income of the preceding fiscal year. In the following circumstances, the debt bond issued by GON and purchased by NRB shall not be treated as the credit extended to GON:

- If the purchase is made in the secondary market for the operation of open market consistent with the monetary policy of NRB;

- If the purchase is made in the primary market, when it is necessary in the opinion of NRB, to maintain stability in the market at the time of primary issue of such securities and such securities are divested within 60 days of purchase.

Relevant Laws and Regulations

Some FAQs

Why does the central bank usually not buy government bonds directly?

Government debt managers usually have more information on financial flows in their domestic market. However, for several reasons, most governments consider it unwise to tactically trade in this market in an attempt to make profits so the central banks are not involved in direct purchase of the government debts/bonds/treasuries. The government is usually the dominant issuer of bonds in the domestic market, and the government would risk being accused of manipulating the market or using inside information of a regulatory and budgetary nature if it became a market maker or trader in government bonds for the purposes of trying to generate additional income. If it took currency or interest rate positions, its actions might be interpreted as signaling a government view on the desired direction of the exchange rate and interest rates, making the central bank’s task more difficult. In the context of Nepal, NRB may engage in the direct purchase of the government debt/bond but there is a mathematical cap on the amount (discussed above).

How does the presence of a certain amount of public debt develop the debt market of the country?

The decisions made by government debt managers about issuing instruments and supporting infrastructure are crucial for developing domestic securities markets. Establishing a liquid government yield curve is instrumental in reducing transaction costs and supporting the development of other markets such as stock and derivative markets. Government benchmark bonds can serve as a useful hedging instrument for the private sector, especially when they are liquid and yield movements on private sector instruments correlate with those on government bonds. In emerging market countries, the issuance of domestic currency bonds can help governments reduce balance sheet risk, smooth out adverse budgetary shocks, diversify funding sources, and reduce dependence on foreign currency borrowing. The government bond markets also generate externalities for the private sector and provide almost credit-risk-free assets for investors.

MMT and Public Debt is not a free lunch: This has to be principled

The concept of Modern Monetary Theory (MMT) should not be misunderstood as unrestricted access to funds. It cannot be perceived as a means to increase the size of the government, nor does it endorse a laissez-faire approach towards funding new programs. Rather, MMT provides an analytical framework to identify untapped potential in the economy, which is referred to as fiscal space.

If there are resources available, and unemployed people are seeking paid employment, then we can utilize our fiscal space to employ these resources in productive activities without raising prices. The decision on how to use this fiscal space is a political matter, which can be applied to defend liberal policies, such as social security funds, free education, or middle-class tax cuts, or conservative policies, such as security spendings or corporate tax cuts. The underutilized fiscal spaces in the country’s economy can be made productive through the targeted use of debts in the economy. Thus an irrational fear of the government debt (both local and foreign) is not helpful to utilizing the full potential of our economy. But like a household and personal life when the debts are not utilized in productive and beneficial sectors the economy should sustain austerity through the decreased revenues or increase in unproductive expenses. Austerity is obviously painful but the obsession with austerity measures should not hinder the movement of the potential economy. It is very hard to put these things in a perfect balance, if gone wrong the MMT policies destroys a country’s economy.

Here are some real-life examples of the potential negative consequences of using MMT measures and debt policies wrongly:

- Hyperinflation: One classic example of the negative consequences of MMT measures gone wrong is the case of Zimbabwe. In the early 2000s, the Zimbabwean government began printing money to finance its budget deficit, leading to a rapid increase in the money supply and hyperinflation. Prices skyrocketed, basic goods became unaffordable, and the economy collapsed.

- Currency Devaluation: Another example is the case of Venezuela, which has been using MMT-style policies for years to fund government spending. The government has been running large deficits, financed by the central bank, which has led to a rapid depreciation of the country’s currency. As a result, imports have become much more expensive, leading to shortages of basic goods and rising inflation.

- Economic Instability: A third example is the case of Greece, which in the early 2000s relied heavily on external borrowing to finance its budget deficit. When the global financial crisis hit, investors became worried about the country’s ability to repay its debt, leading to a spike in interest rates and a loss of confidence in the country’s ability to repay its debts. This led to a severe economic downturn, with high unemployment, falling GDP, and social unrest.

- Burden on Future Generations: A fourth example is the case of Japan, which has been using MMT-style policies for years to finance government spending. The country has been running large budget deficits, financed by the central bank, which has led to a significant increase in the national debt. While Japan has not yet experienced the negative consequences of this approach, some economists worry that the country’s high debt levels will place a burden on future generations, who will have to repay the debt through higher taxes or reduced government spending.

- Recession and Unrest: In the early 2000s, the government of Argentina implemented MMT measures to finance public spending, leading to a sharp increase in inflation and a decline in the value of the country’s currency. The government’s printing of money led to a loss of confidence in the economy, resulting in a deep recession and social unrest.

Public Debt Challenges in Nepal

Many countries’ financial defaults originate from situations of excessive short-term debt, excessive borrowings in the foreign currencies and weak macroeconomic fundamentals. Nepal also faces a number of challenges related to public debt which we will discuss below:

High Debt-to-GDP Ratio

A high debt-to-GDP ratio poses several challenges in public debt management, including:

- Increased interest payments that reduces the funds being available to other public expenditures such as infrastructure, education and healthcare

- Reduced ability to respond to economic shocks such as recession and natural disasters as the government may not have the fiscal space to implement countercyclical policies or provide fiscal stimulus.

- Increase in borrowing costs as the lenders may perceive the government with high debt to GDP as a higher credit risk, leading to higher interest rates and reduced access to credit markets.

- Negative impact on credit rating: A high debt-to-GDP ratio may lead to a downgrade in the government’s credit rating, which may increase the cost of borrowing and reduce investor confidence in the government’s ability to manage its finances.

The birthing center for migrant workers - that is Nepal

Nepal, a beautiful country nestled between the towering Himalayas, is known for its rich cultural heritage, majestic mountain ranges, and natural beauty. But beyond the idyllic facade lies a harsh reality – one of economic dependence on the foreign remittance sent by migrant workers.

Nepal’s economy is not strong, and the government and the economy has been unable to provide adequate employment opportunities for its citizens. This has resulted in a mass exodus of people from the country, with estimates suggesting that over 3.5 million Nepalis are working abroad, primarily in Gulf countries, Malaysia, and South Korea. These migrant workers often leave their families behind in search of better employment opportunities, and their remittances have become a lifeline for the Nepali economy.

In 2022 alone, Nepali migrant workers sent home around 10 billion, accounting for over 25% of the country’s GDP. These funds have helped to alleviate poverty, improve access to education and healthcare, and boost the country’s overall standard of living. However, this reliance on remittances also highlights the failure of the Nepali government to create sustainable economic opportunities for its citizens. The plight of Nepali migrant workers is heartbreaking. Many of them leave their families behind, including young children, in search of employment opportunities that are not available in their home country. They endure grueling work conditions, often for low wages, and live in overcrowded and substandard housing. Despite the hardships, they persevere, driven by the hope of providing a better life for their loved ones back home.

It is a tragic reality that Nepal has become a “birthing center” for migrant workers. This is not what the people of this beautiful country deserve. They deserve a government that can provide for them, create jobs, and improve their quality of life. It is time for the government to take responsibility and create sustainable economic opportunities for its citizens, so that they no longer have to rely on the hard work and sacrifice of their loved ones abroad.

In the meantime, we must acknowledge and appreciate the hard work and dedication of Nepali migrant workers. Their remittances are not just numbers on a balance sheet – they represent the sweat, tears, and sacrifice of millions of people. As we enjoy the comforts of our own lives, let us not forget the sacrifices made by these brave men and women, and let us do our part to support them and their families in any way we can. This topic definitely warrants separate research so we will stop this discussion here.

Huge Loan Servicing Costs relative to Revenues

Nepal is heavily dependent on external loans and grants to fund its development projects. This has led to a situation where a significant portion of the country’s budget goes towards servicing these loans, leaving little room for other important expenditures such as education, healthcare, and infrastructure.

Nepal is one of the poorest countries in the world, with a per capita income of just $1,208 in 2021. Its economy heavily relies on external loans and grants to fund its development projects. According to the World Bank, Nepal received a total of $2 billion in official development assistance (ODA) in 2020, which was equivalent to 7% of its gross domestic product (GDP).

Moreover, the country’s debt-to-GDP ratio has been increasing in recent years, reaching 28.7% in 2020. This means that a significant portion of the country’s budget goes towards servicing these loans, leaving little room for other important expenditures such as education, healthcare, and infrastructure. In fact, Nepal spent 22.3% of its budget on debt servicing in 2020, which was more than what it spent on education and healthcare combined.

In conclusion, Nepal’s heavy reliance on external loans and grants has resulted in a high debt-to-GDP ratio, which in turn limits the government’s ability to allocate funds to important areas such as education, healthcare, and infrastructure. The loss of foreign remittance due to the COVID-19 pandemic has only worsened the situation. The country needs to focus on developing its economy and reducing its dependence on external funding sources in order to achieve sustainable development.

Servicing Cost of Foreign Currency Debt

Servicing Cost of Foreign Currency Debt

Limited Revenue Sources

Nepal’s tax base is relatively narrow, with only a small percentage of the population paying income tax. This limits the government’s ability to raise revenue and makes it more difficult to service the country’s debt obligations.

According to data from the World Bank, in 2020, only around 5.5% of Nepal’s population paid income tax. This is a relatively low percentage compared to other countries in the region, such as India and Sri Lanka, where the tax base is much wider. The narrow tax base in Nepal is one of the reasons why the government is heavily dependent on external loans and grants to fund its development projects, as mentioned earlier.

According to a report by the International Monetary Fund (IMF) in 2020, Nepal’s tax-to-GDP ratio was only 18.4%, which is significantly lower than the average for countries in the region. The low tax base in Nepal is partly due to the large informal sector in the economy, which is estimated to account for around 65% of the country’s GDP. Many small businesses and individuals in the informal sector are not registered and do not pay taxes. In addition, tax evasion and avoidance are also prevalent in the country. According to a report by the Nepal Rastra Bank, the country’s central bank, only around 3.3% of the population paid income tax in the fiscal year 2019. The majority of those who paid income tax were salaried employees in the formal sector, while many businesses in the informal sector were not subject to income tax.

In countries like Nepal, which is not a monetary sovereign and highly reliant on the taxes as revenues, narrow tax bases, and overly weak economic fundamentals, the concept of MMT and monetization of public debt is not a feasible option. But advanced economies with monetary sovereignty see taxes as a means to redress income and wealth inequality, discourage harmful behaviors, and incentivize desirable ones. Extreme concentrations of wealth and income can harm the economy and democracy, and sophisticated nations use taxes to address these issues. These sovereigns can spend more than they tax without creating an inflation problem, but taxes remain an indispensable policy tool.

Why do we not use taxes as a policy tool rather than resorting to debt? And what can we learn from Professor Calvin Johnson’s Shelf Project?

Professor Calvin Johnson has developed a project known as the “Shelf Project” that attempts to develop proposals for Congress to increase revenue, in collaboration with other tax professionals. Johnson believes that the reforms will require a budget crisis to spur parliament to action. Johnson’s efforts are directed towards creating a tax system that is more efficient, fair, and less avoidable, by making the tax base more efficient by reducing or eliminating exemptions, loopholes, and shelters (tax expenditures). Johnson believes that tax expenditure waste is the greatest government waste. He argues that the tax base should be increased without raising rates to save the federal budget. He and his team of professionals prepare the tax plans, reform policies with a monetary value tied to them and whenever the parliament needs the budget to spur something into action, they can come and pick a reform from the shelf, put it through the parliament and get things done. More on his interesting work here: Link

The loss of Real Effective Exchange Rate

In the context of Nepal, foreign currency loans can be quite expensive due to the country’s vulnerability to exchange rate fluctuations that are usually not in its favor. This means that even if a loan has a nominal interest rate, the actual cost of servicing the loan can be much higher due to the unfavorable exchange rates. Additionally, when Nepal has to buy foreign exchange in international markets to pay back these loans in specified currencies, cross exchange rates further increase the cost of the loans.

Furthermore, a large share of Nepal’s external debt is multilateral, which means that it is borrowed from international organizations like the World Bank and the Asian Development Bank. While these loans may have more favorable interest rates, they can be comparatively difficult to reschedule or restructure. This can put a strain on Nepal’s finances and limit its ability to manage its debt effectively. In recent years, Nepal’s external debt has been steadily increasing and reached USD 14.98 billion in 2020, with the largest share of it being owed to multilateral institutions.

Vulnerability to External Shocks

Nepal’s economy is highly vulnerable to external shocks such as natural disasters, political instability, and changes in global commodity prices. These shocks can make it more difficult for the country to service its debt and can lead to increased borrowing costs.

- Dependence on external aid: Nepal is heavily reliant on external aid and grants, which make up a significant portion of the country’s foreign exchange earnings. Any disruption in the flow of aid or a decrease in the amount of aid received could significantly impact Nepal’s ability to service its external debt. According to the World Bank, Nepal received a total of $2 billion in official development assistance (ODA) in 2020, which was equivalent to 7% of its gross domestic product (GDP).

- Weak domestic revenue generation: Nepal has a direct tax-to-GDP ratio, which means that the government is heavily reliant on external borrowing to finance its expenditure. This dependence on external borrowing exposes the country to external shocks, as any disruption in the global financial markets or changes in interest rates could lead to a significant increase in the cost of borrowing for the Nepalese government.

- Currency devaluation: Nepal’s currency, the Nepalese rupee, is subject to fluctuations in the foreign exchange market. Any significant devaluation of the currency could lead to an increase in the cost of servicing external debt, as Nepal would need to use more rupees to purchase the same amount of foreign currency to service its debt.

- Natural disasters: Nepal is prone to natural disasters such as earthquakes, floods, and landslides, which can have a significant impact on the country’s economy and public debt management. In the aftermath of a disaster, the government may need to increase its borrowing to finance relief and reconstruction efforts, which could exacerbate its vulnerability to external shocks.

Socialism, Capitalism or Creditism?

What does Nepal want to be? Article 4 of the Constitution of Nepal, 2015 explains: Nepal is an independent, indivisible, sovereign, secular, inclusive, democratic, socialism oriented, federal democratic republican state.

Try to be too many things and you become none of them.

It seems that Nepal is in a state of confusion regarding its identity and direction. The country seems to be grappling with the question of what it wants to be, whether it wants to pursue a socialist path, embrace capitalism, or adopt a credit-based economic model. This confusion can be felt among the people, who may be wondering what the future holds for their country. It is not easy to reconcile these different economic models, each with its own strengths and weaknesses. However, it is important for Nepal to find a clear direction and identity in order to move forward and address the economic and social challenges it faces.

Nepal has also faced significant political and economic challenges in recent times. In the past, Nepal has experimented with various economic systems, including socialism and capitalism, but has yet to fully embrace either one. This lack of a clear economic vision has contributed to Nepal’s struggles with poverty, underdevelopment, and political instability. Additionally, Nepal has a high level of external debt, with a large share of it being multilateral debt that is difficult to restructure or reschedule. The country has also faced difficulties in managing its public debt, which makes it vulnerable to external shocks. The lack of clear economic policies and a strong debt management strategy has made Nepal’s economy more susceptible to the impact of global economic changes and other external factors.

Moreover, Nepal’s economy is heavily dependent on remittances from Nepalese working abroad, millions of Nepalese working overseas. This reliance on remittances has made Nepal’s economy vulnerable to external shocks, such as the COVID-19 pandemic, which led to a significant drop in remittance inflows. In short, Nepal is a country that is struggling to find its economic footing, with a lack of clear economic policies and a weak debt management strategy. The heavy reliance on remittances and vulnerability to external shocks has made it difficult for Nepal to achieve sustainable economic growth and development.

The point is, if we are not clear about where we want to be and what we want to do as a country, nobody is going to take us anywhere. No aid/support from multilateral, bilateral or neighboring countries and organizations will take us anywhere if we are not sure where we want to go. Here are some examples of such visible problems:

- The IMF, WTO, and World Bank, which are usually managed by bankers and diplomats from wealthy countries, do not prioritize global full employment. Their go-to solution for crisis-hit developing countries is to suggest drastic cuts in government spending (known as fiscal austerity), tight monetary policies with high interest rates to boost their currency’s value and attract investors, as well as promoting more free trade. Moreover, they often recommend that developing countries link their currency to a stronger one such as the yuan, euro, or US dollar. Essentially, this means that developing countries are advised to forego any attempts to improve their monetary sovereignty.

- International organizations such as the IMF have traditionally advised developing countries to focus on producing and selling a limited number of goods to wealthier countries. This advice stems from a concept called comparative advantage, which recommends that countries specialize in producing goods and services they are most proficient at. However, some economists have taken this idea to the extreme and argue that developing countries should only focus on producing goods that are cheap to make in the short term, rather than investing in new industries that could boost their monetary independence in the long term. This advice has been criticized for keeping developing countries in a state of perpetual “development” and hindering their ability to develop advanced and diverse economies. In contrast, countries like the US, Japan, and China have focused on producing essential goods domestically rather than relying on imports. The Chinese government has also limited the role of finance, insurance, and real estate in the industrial process to support internal trade growth.

- Nepal also has a history of being hesitant to apply for debt relief. There are several reasons of course. One of the main reasons is that Nepal is classified as a “low-income” country by international financial institutions, which means it is eligible for concessional loans with lower interest rates and longer repayment periods. If Nepal were to apply for debt relief, it could potentially lose access to these concessional loans in the future. Additionally, there is concern that accepting debt relief could harm Nepal’s credit rating and make it more difficult to borrow money in the future. Finally, there are concerns that debt relief could come with conditions that could limit Nepal’s ability to pursue its own economic policies and development goals. Overall, while debt relief could provide some relief for Nepal’s debt burden, it is a complex issue that requires careful consideration of both the short-term and long-term consequences.

Crowding out of the private sector expenditures

The crowding-out phenomenon occurs when excessive government borrowing leads to an increase in domestic interest rates and possibly the exchange rate, causing other borrowers to defer investments or seek more expensive or riskier financing sources. Public debt is not only a current risk but also an opportunity cost as it obstructs private sector efficiency in investing in similar programs. The crowding-out hypothesis suggests that government debt accumulation may lead to rising interest rates, which can compete with private firms for limited investment funds, ultimately resulting in lower growth rates, particularly for countries with debt-to-GDP ratios greater than 80 percent. According to a World Bank Group report that examined the debt levels of 100 developed and developing countries from 1980 to 2008, a debt-to-GDP ratio above 77% for developed countries and 64% for developing countries reduces future annual economic growth by 0.017 and 0.02 percentage points, respectively, for each percentage point of debt above the threshold.

The crowding out hypothesis suggests that an increase in government borrowing (usually to finance government spending or investment) can lead to a reduction in private sector investment. This happens because when the government borrows large sums of money, it competes with private sector borrowers for the limited pool of available funds. This competition drives up interest rates, making it more expensive for the private sector to borrow and invest. As a result, private sector investors may defer or cancel their investment plans, or seek riskier or more expensive sources of finance, reducing the overall level of private sector investment in the economy. This reduction in private sector investment can have a negative impact on economic growth, as private investment is an important driver of economic activity. While the crowding out hypothesis is controversial and not universally accepted, it has been a significant concern for policymakers and economists, particularly in times of high government borrowing and rising public debt.

Despite the government expenses to GDP ratio of Nepal has been relatively lower compared to other countries it still is not a sound position because a major portion of the GDP of Nepal is composed of the household consumption rather than capital formation which should have been the priority of the developing country like ours.

We are not a monetary sovereign

Lets again discuss the concept of monetary sovereignty, which is vital to understanding MMT and public debt regime. Governments need a high degree of monetary sovereignty to exercise policy autonomy and run their fiscal and monetary policies without fear of backlash from financial or foreign exchange markets. Countries like the US, UK, Japan, Canada, and Australia enjoy a high degree of monetary sovereignty, while developing countries are at the weaker end of the sovereignty spectrum. Most developing economies cannot afford to ignore fiscal and trade imbalances, and they usually borrow in US dollars and struggle to repay those loans. The article argues that the global hunger for dollars is why the US has been running a trade deficit nonstop for decades. While the US dollar’s unique role as a global reserve currency gives the US an advantage, any country with a high degree of monetary sovereignty has the ability to pursue a domestic policy agenda aimed at keeping its economy operating at full employment. In an advanced economy with monetary sovereign inflation and resources within the real economy are the real limitations of economic growth, rather than government deficits.

In a poor economy, the limitations on economic growth can be more complex and multifaceted. Government deficits may play a more significant role in limiting growth in such an economy, particularly if the government lacks access to international markets for borrowing or if it is unable to collect sufficient tax revenue. In addition, poor economies may lack the infrastructure, technology, and skilled workforce necessary for sustained growth, which can limit the productivity of their workers and businesses. Other factors such as political instability, corruption, and weak institutions may also impede growth in poor economies. Therefore, the limitations on economic growth in poor economies are more diverse and can be more challenging to address than in advanced economies with monetary sovereignty.

Bad Practices in Public Debt Management

- Some critics argue that the Nepalese government lacks transparency in managing public debt, and there is not enough information about how borrowed funds are being used and how debt will be serviced in the future.

- To reduce the debt burden, Nepal needs to use borrowed money effectively and invest in productive sectors with high levels of efficiency. This is crucial as Nepal is preparing to graduate from the LDC group in 2026, which could lead to the loss of benefits of a lower rate of interest.

- The government should avoid exposing its financial position to even low-probability risks of large or catastrophic losses, as it may lead to vulnerability in the short run. Debt managers should manage the intertemporal tradeoff between short-term and long-term costs prudently, avoid excessive reliance on short-term or floating-rate paper, manage foreign exchange exposures, debt with embedded put options, and implicit contingent liabilities to financial institutions.

- Some debt management practices can distort private and government decisions and understate the true interest cost. These include collateralization of debt by state-owned enterprises or future tax revenue, and tax-exempt or reduced-tax debt. These practices can lead to distorted asset management decisions and ambiguity in the impact on the deficit.

- The misreporting of contingent or guaranteed debt liabilities, may understate the actual level of government liabilities. There may be inadequate coordination or procedures with regard to borrowing by lower levels of government and state-owned enterprises, repeated debt forgiveness, and loan guarantees that have a high probability of being called.

- The use of non market financing channels by governments can be distortionary, including special arrangements with the central bank, forced borrowing from suppliers, and the creation of a captive market for government securities. These practices tend to raise the price of government expenditures and can have distortionary effects on debt-servicing costs and financial markets.

- The inadequate supervision or recording of debt contracting and payment, and insufficient monitoring of debtholders, can result in less control for the government over the tax base or the supply of outstanding debt. One issue is the failure to document implicit interest on long-term debt with zero-coupon. Although this may benefit the government’s cash position, it leads to understating the actual deficit.

Resources and References

- Overview of Nepal’s Public Debt Management, Capital Market and Infrastructure Capacity Support Project

- Nepal Rastra Bank Central Office Monetary Management Department Citizen Saving Bond Issue/Application Notices

- Public Debt Management Departments Archive – नेपाल राष्ट्र बैंक

- Debt concern grows as government borrowing doubles in three years

- Public Debt Management in Nepal

- Official use only Debt Management Reform Plan Nepal May 2019

- Analysing new Public Debt Management Bill – Samriddhi Foundation

- Nepal’s Public Financial Management Reform Strategy/Program (PFMRP) Phase II (2016/17-2025/26)

- Auditing Public Debt Management

- Adopting Good Practices on Public Debt Management in Asia and the Pacific

- Public Debt in Nepal: An Assessment

- Designing Legal Frameworks for Public Debt Management

- Nepal Journals Online

- Ministry of Health and Population Public Financial Management Strategic Framework FY 2020/21-2024/25

- Curbing Nepal’s Rising Debt: Current Situation and Implications

- Managing Public Debt From Diagnostics to Reform Implementation

- Guidelines for Public Debt Management, March 21, 2001, by the Staffs of the IMF and World Bank

- Guidelines in Public Debt Management: Accompanying Document — November 21, 2002

- Public Debt Management in Emerging Market Economies: Has This Time Been Different? (2010)

- Managing Public Debt: From Diagnostics to Reform Implementation (2007)

- Sound Practice in Government Debt Management (2004)

- Strengthening Debt Management Practices: Lessons from Country Experiences and Issues