A comprehensive legal, regulatory, and high level market analysis of whether securitization model is permissible, feasible, and implementable in Nepal – and what changes are required to make it so.

1. Introduction

Nepal’s banking system is deeply concentrated, long in duration, and short on exit. Total banking and financial system assets have reached 201.8% of GDP (excluding NRB), funded almost entirely by deposits averaging one to three years in maturity – yet deployed into hydropower loans averaging twelve to twenty-one years and mortgage loans with tenors up to thirty-five years. Simultaneously, the country’s institutional investors – the Employees Provident Fund (EPF: NPR 623 billion), the Social Security Fund (SSF: NPR 119 billion, growing 21% annually), the Citizen Investment Trust (CIT: NPR 311 billion), and the insurance sector (NPR 1.09 trillion in assets) – have major of assets expected to service their long-duration liabilities deposited in bank fixed deposits and government securities. The capital market offers them very minimal real and long term investment opportunities.

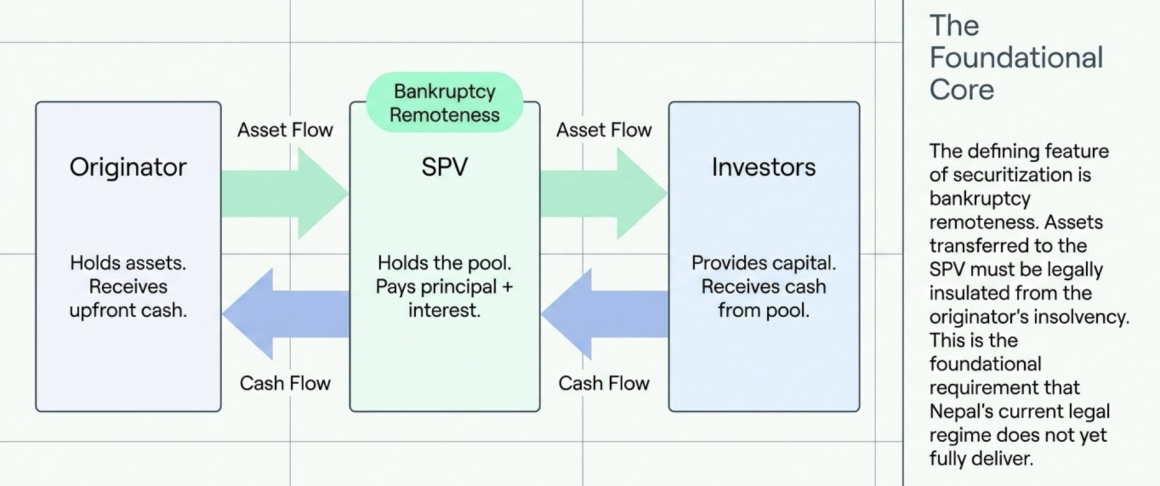

Securitization – the isolation of financial assets or contractual receivables into a bankruptcy-remote Special Purpose Vehicle (SPV) that then issues asset-backed securities to investors – is the structural mechanism that resolves this simultaneously from both sides. Banks recycle frozen liquidity. Institutional investors access long-duration, investment-grade fixed income. Infrastructure developers monetize contracted cash flows. Retail investors eventually access new instruments.

The central question this post tries to answer is: Is securitization permissible in Nepal today? If not, what precisely must change, and through which legal pathways?

Key Findings

| Finding | Status |

| Statutory recognition of outright receivable sale | ✔ Partial – STA 2081 s.3(1)(kha) |

| True-sale definition (bankruptcy remoteness for outright assignees) | ✖ Absent |

| SPV legal vehicle with bankruptcy remoteness | ✖ No dedicated provision |

| BFI loan transfer authority | ✔ BAFIA s.122 (non-obstante) |

| Anti-assignment override for receivables | ✔ STA s.42(3Ka) |

| Priority over unsecured creditors for assignees | ✔ STA s.29Ka (if registered) |

| Insolvency moratorium protection for perfected interests | ✔ STA s.58Ka |

| Capital adequacy recognition of securitization | ✔ Partial – NRB CAF s.6.3(e) |

| SEBON ABS regulatory framework | ✖ Absent |

| Pass-through tax treatment for SPV | ✖ Absent – double taxation |

| ERC framework for PPA assignment | ✖ Absent |

| Mortgage borrower consent waiver for pool transfer | ✖ Required individually |

| Private placement pathway to 50 investors | ✔ Securities Act s.30(2)(Ga) |

| Advance tax ruling mechanism | ✔ ITA s.76 |

| ARC/SARFAESI-equivalent enforcement | ✖ Absent |

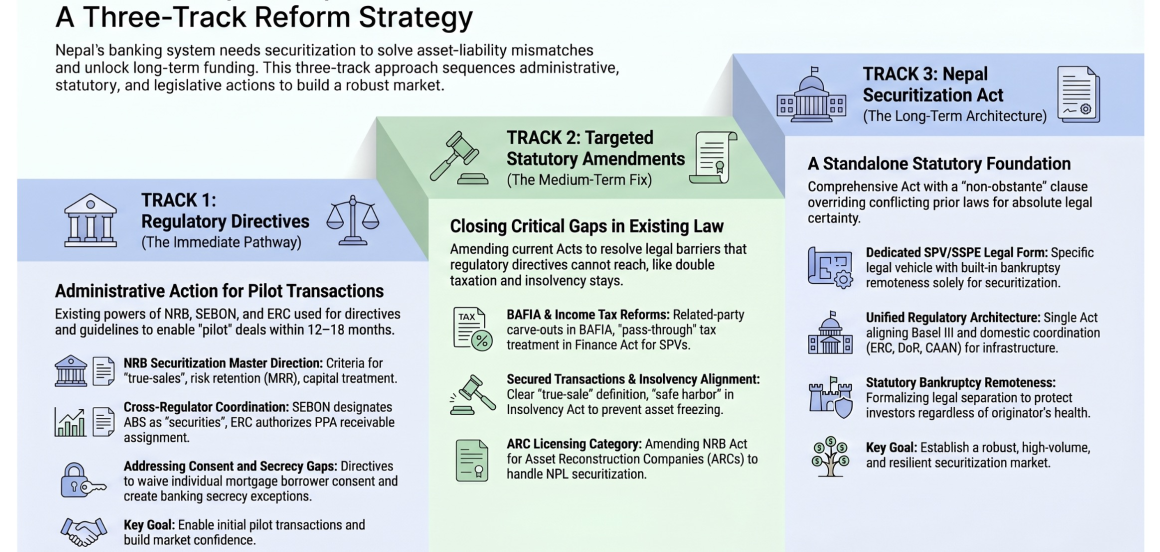

The Three Conclusions

First: Securitization in Nepal is not legally prohibited – but neither is it legally enabled. A narrow window exists under existing law for a pilot transaction, specifically a private placement of energy loan-backed ABS to fewer than fifty institutional investors, structured under BAFIA Section 122 and the Secured Transactions Act, with NRB directing capital treatment. This window is extremely narrow and carries significant legal risk, particularly around true-sale characterisation, tax architecture, and enforcement.

Second: Three options of legislative modalities can be imagined to create a proper enabling framework – (a) SEBON regulation under the Securities Act, (b) Civil Code trust amendment, and (c) a standalone Nepal Securitization Act. None is sufficient alone. The appropriate solution could be choosing one / multiple options from the three-track reform ideas: (a) immediate regulatory directives from NRB, SEBON, and ERC; (b) medium-term targeted amendments to BAFIA, the Income Tax Act, the Secured Transactions Act, and the Insolvency Act; or (c) a standalone Nepal Securitization Act as the long-term architecture.

Third: The highest-priority first transaction is BFI-originated energy loan ABS, not mortgage ABS – because mortgage loans require individual written borrower consent from every borrower (NRB Unified Directive No. 2), making pooled mortgage securitization practically impossible without a new NRB directive. Energy loans have an existing consent waiver precedent and the simplest legal pathway.

2. Introduction: Scope and Methodology

This assessment covers the legal and market feasibility of securitization in Nepal, understood as the arrangement by which an originator isolates or transfers its economic interest in the cash flows of financial assets or contractual receivables to a bankruptcy-remote Special Purpose Vehicle (SPV), which then finances the acquisition by issuing asset-backed securities to capital market investors, with repayment primarily dependent on those cash flows rather than the originator’s general credit.

The scope is deliberately broad across originator types (banks, hydropower developers, infrastructure entities, MFIs) but the legal analysis is grounded specifically in the Nepali legal regime as it exists, rather than in abstract international best practice. This assessment traces each step of a securitization transaction through existing Nepali law, identifies where that law enables, where it is silent, and where it affirmatively prohibits – and then maps three pathways to close the gaps.

The research draws from eleven legislative sources, six categories of NRB directives, SEBON regulations, ERC regulations, individual commercial bank annual reports, NRB macroeconomic surveys, and the institutional investor framework. All legal citations reference the specific section and subsection of the relevant Act or Directive.

3. The Mechanism: What Securitization Is

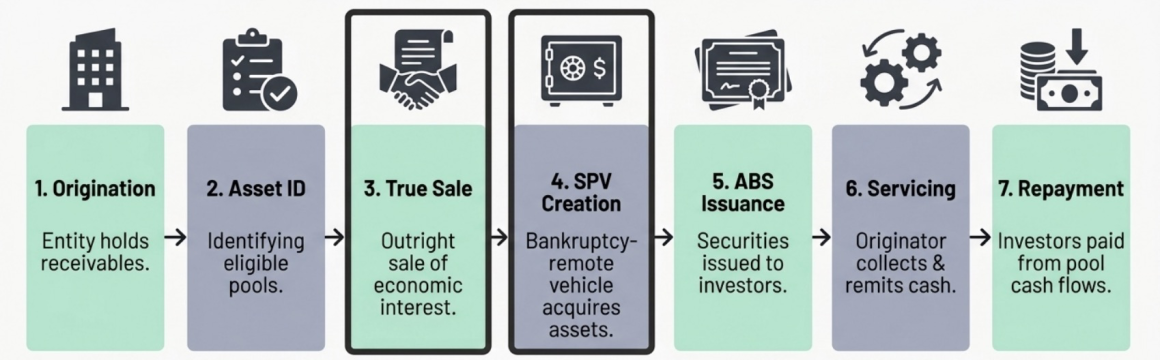

Securitization involves seven sequential steps. Each step raises a distinct legal question in the Nepali context, addressed in the case studies below.

| Step | Description | Key Legal Question (Nepal) |

| 1 | Origination – Entity holds receivables (loans, PPA revenue, toll) | Is the entity legally permitted to transfer? |

| 2 | Asset identification – Selection of eligible receivables for pool | Are the assets transferable? Non-assignment clauses? |

| 3 | Transfer / True Sale – Originator sells economic interest to SPV | Does law recognise an outright sale vs. secured loan? |

| 4 | SPV Creation – Bankruptcy-remote vehicle acquires assets | Does a suitable legal vehicle exist? |

| 5 | ABS Issuance – SPV issues securities to investors | Does SEBON’s framework accommodate ABS? |

| 6 | Servicing – Originator continues to collect, remit to SPV | Can BFI-servicer enforce collateral on SPV’s behalf? |

| 7 | Repayment – Investors receive principal + interest from cash flows | What is the tax treatment at each transfer point? |

💡 KEY CONCEPT: The defining feature is bankruptcy remoteness – the principle that assets transferred to the SPV are legally insulated from the originator’s insolvency. If the originator goes bankrupt, the SPV’s assets are not frozen or claimed by the originator’s creditors. This is the foundational legal requirement that existing Nepali law does not yet fully deliver.

4. The Systemic Case: Why Nepal Needs Securitization

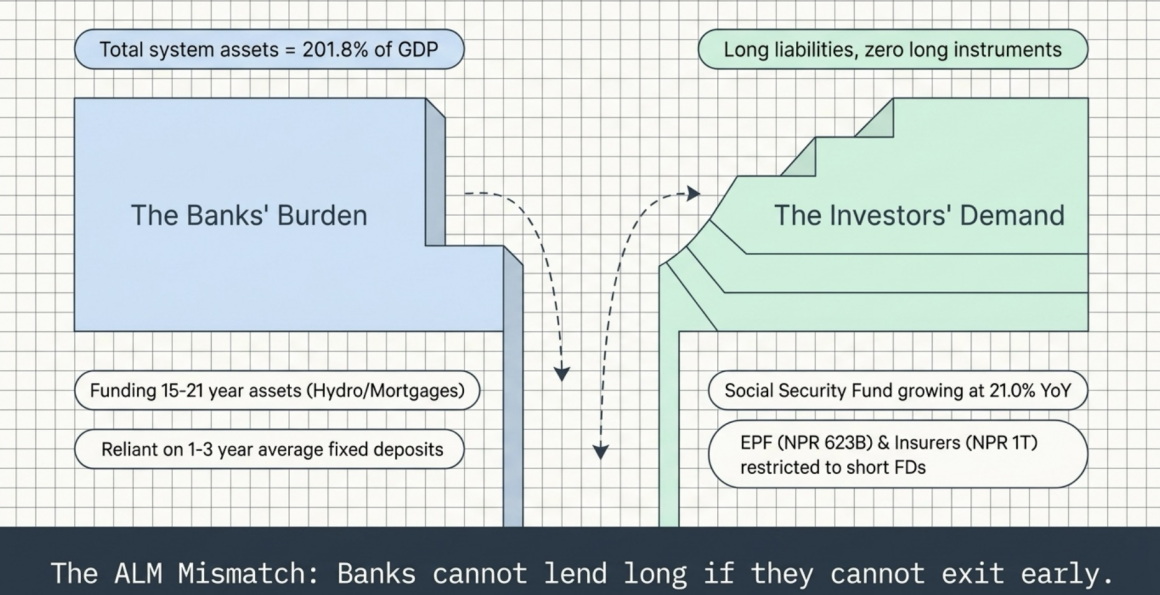

4.1 The Asset-Liability Mismatch

Nepal’s commercial banks have undergone a structural shift over the past decade: from short-term working capital lenders to de facto long-term infrastructure financiers. This is not a failure of banking – it reflects the absence of any alternative long-duration funding mechanism for Nepal’s infrastructure ambitions. But it creates a systemic vulnerability that securitization is specifically designed to address.

| Metric | Value | Source |

| Total banking system assets (excl. NRB) | 201.8% of GDP | NRB Annual Report 2081/82 |

| Total banking system assets (incl. NRB) | 235.1% of GDP | NRB Annual Report 2081/82 |

| Total commercial bank loans (FY 2023/24) | NPR 5,871.03 billion | NRB BSD Annual Report 2024 |

| Term loans as % of total credit | 37.32% (up from 25.11% two years prior) | NRB BSD Annual Report 2024 |

| Energy sector loans as % of total | 7.99% | NRB BSD Annual Report 2024 |

| Real estate collateral as % of all loans | 64.7% | NRB Current Macroeconomic Situation 2024/25 |

| System-wide CAR | 12.84% (Core: 10.10%) | NRB BSD Annual Report 2024 |

| 4 banks unable to maintain Tier 1 minimum (incl. 2.5% buffer) | FY 2022/23 | NRB BSD Annual Report |

The ALM mismatch is starkest in individual bank disclosures. Nabil Bank (Annual Report 2023/24) reports NPR 96.06 billion in loans with maturity over five years, against only NPR 14.67 billion in fixed deposits in the same bucket – a 6.5x mismatch. Standard Chartered Bank Nepal (Annual Report 2081/82) discloses an average original mortgage tenure of 21.05 years and remaining average tenure of 15.83 years. Everest Bank has issued an Energy Bond with a 12-year maturity to fund its hydropower portfolio. These assets are being financed by a deposit base where fixed deposits average one to three years.

⚠ SYSTEMIC RISK: This mismatch – 15-21 year assets funded by 1-3 year liabilities – creates precisely the liquidity fragility that securitization resolves. Banks cannot lend long if they cannot exit early. Securitization converts illiquid long-duration loans into immediate cash, while transferring duration risk to investors whose liabilities genuinely match it.

4.2 The Institutional Investor Demand Gap

On the demand side, Nepal’s institutional investors face the mirror problem: their liabilities are long (pension obligations, life insurance policy payouts, provident fund withdrawals decades away) but their permissible investments are short and narrow.

| Institution | AUM | Growth | Current Investment Concentration |

| Employees Provident Fund (EPF) | NPR 623.21 billion | 9.1% p.a. | Fixed deposits (25%), loans to contributors (37%), gov securities (6%) |

| Social Security Fund (SSF) | NPR 119.38 billion | 21.0% p.a. | Government securities, bank deposits |

| Citizen Investment Trust (CIT) | NPR 311.06 billion | 2.5% p.a. | Investments (68%), loans and advances (28%) |

| Insurance sector (combined) | NPR 1,093.95 billion | 16.5% p.a. | Diversified but restricted by IRAN Investment Guidelines |

Source: NRB Annual Report 2081/82

⚠ THE DEMAND PROBLEM: Not one of these institutions currently has investment bylaws that permit investment in ABS or MBS. EPF, SSF, CIT, and insurance companies all require bylaw amendments – board approval plus regulatory clearance – before they can deploy into securitized instruments. This is the single most important demand-side constraint, and it is entirely addressable by administrative action without Parliamentary intervention.

4.3 The Asset Quality Problem

Nepal’s NPL ratio has deteriorated sharply, creating an urgent secondary motivation for securitization on the distressed-asset side.

| Year | NPL Volume | NPL Ratio |

| Mid-2023 | Baseline | 2.98% |

| Mid-2024 | NPR 180.01 billion | 3.94% (↑39.93% YoY) |

| Mid-2025 (est.) | NPR 200+ billion | ~5.03% |

Non-banking assets (unsold auctioned collateral) surged 96.97% to NPR 30.15 billion in FY 2023/24, indicating that collateral enforcement under BAFIA Section 57 is not clearing the backlog. A distressed-asset securitization framework (ARC model) would allow banks to transfer NPA pools to specialist reconstruction entities, clean their balance sheets, and free capital for productive lending.

5. The Originator Landscape

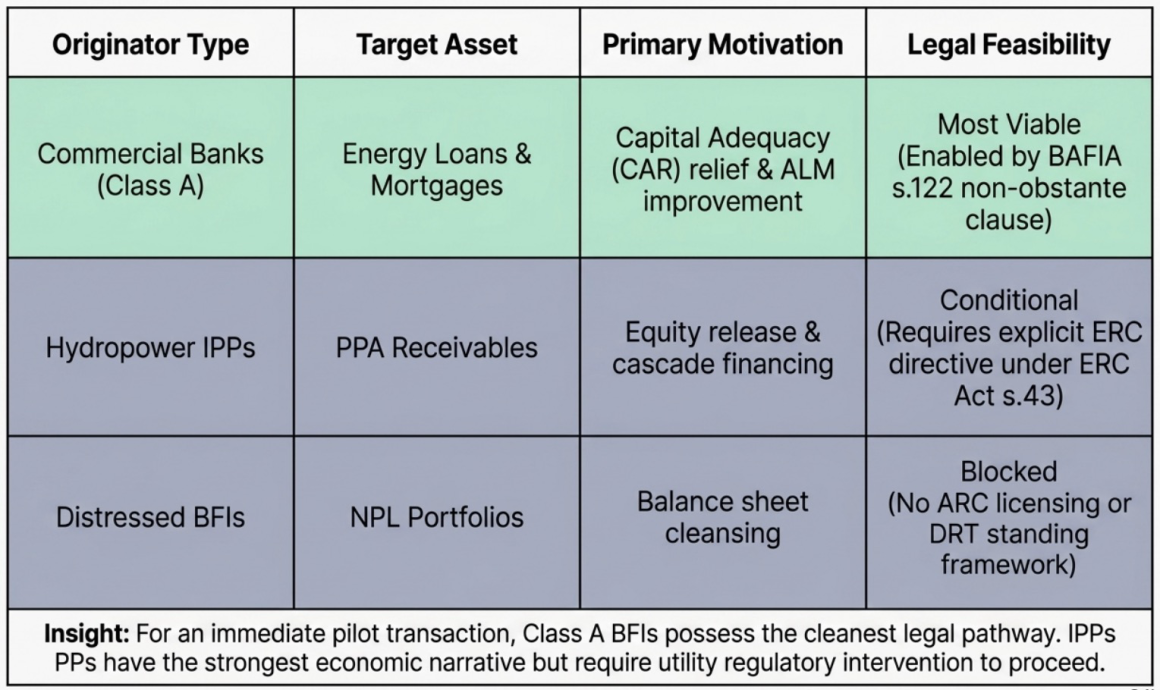

Nepal’s securitizable originator universe falls into three categories, each governed by distinct regulatory frameworks.

| Originator Type | Examples | Governing Regulator | Primary Motivation |

| Commercial Banks (Class A) | Nabil, NMB, Himalayan, Everest, Global IME | NRB / BAFIA 2073 | CAR relief, sectoral SOL headroom, ALM improvement |

| Development Banks (Class B) / Finance Companies (Class C) | Various | NRB / BAFIA 2073 | Balance sheet cleansing, NPL reduction |

| Hydropower IPPs | Upper Tamakoshi, Chilime, Rairang, 200+ operational IPPs | ERC / Electricity Act 2049 | Equity release, new project financing |

| Nepal Electricity Authority (NEA) | NEA (generation, transmission) | ERC / MoWERI | Generation and Grid expansion capital |

| Infrastructure Entities | Department of Roads (FastTrack), CAAN | MoPIT / respective acts | Infrastructure recycling |

| Microfinance Institutions (Class D) | Various MFIs | NRB / BAFIA 2073 | Social-purpose securitization, liquidity |

💡 KEY FINDING: For an immediate pilot, BFI originators have the cleanest legal pathway via BAFIA Section 122. Hydropower IPPs are the most compelling narrative but face the additional layer of ERC regulatory authorization for PPA assignment. MFIs have high-rate, homogeneous loan pools ideal for pool formation, but their regulatory framework does not address portfolio assignment.

6. The Asset Universe: What Can Be Securitized

The legal treatment of each asset class under Nepal’s current law varies significantly.

| Asset Class | Examples | Securitizable? | Key Legal Provision | Key Gap |

| Energy/Hydro loans | BFI loans to IPPs | ✔ Yes (with NRB directive) | BAFIA s.122; STA s.3(1)(Kha) | Consent waived only for original bank continuing relationship management |

| Residential mortgages | Home loans | ⚠ Conditionally | BAFIA s.122; STA s.3(1)(Kha) | Individual borrower consent required per NRB Unified Dir. No. 2 |

| PPA receivables | Monthly NEA payments to IPP | ⚠ Conditionally | STA s.3(1)(Kha); STA s.2(Jha1) | ERC consent for assignment not addressed; “bahikhata” definition gap |

| Toll revenues | FastTrack tolls | ⚠ Future receivables | STA s.2(Jha1) “future assets” | No Roads Act authorization; no revenue data history |

| NPL portfolios | Secured non-performing loans | ⚠ Medium-term only | BAFIA s.122 | No ARC licensing; no SARFAESI-equivalent enforcement |

| MFI loan portfolios | Microfinance receivables | ⚠ Conditionally | STA s.3(1)(Kha) | Consent required; resource mobilization cap (30x primary capital) |

| Wheeling charges | NEA transmission revenue | ⚠ Long-term | STA s.2(Jha1) | No ERC framework; GON approval complexity |

⚠ CRITICAL NOTE ON PPA RECEIVABLES: The STA 2081 amendment defines “bahikhata” (Section 2(fa)) as rights to payment for “goods sold or leased or services rendered.” Electricity supply under a PPA is arguably a “service rendered,” which would bring PPA receivables within the definition. However, this interpretation is not settled in Nepali law, and the expanded “movable property” definition in Section 2(Jha1) – which explicitly covers future assets and intangibles – provides a more robust legal hook for the same purpose.

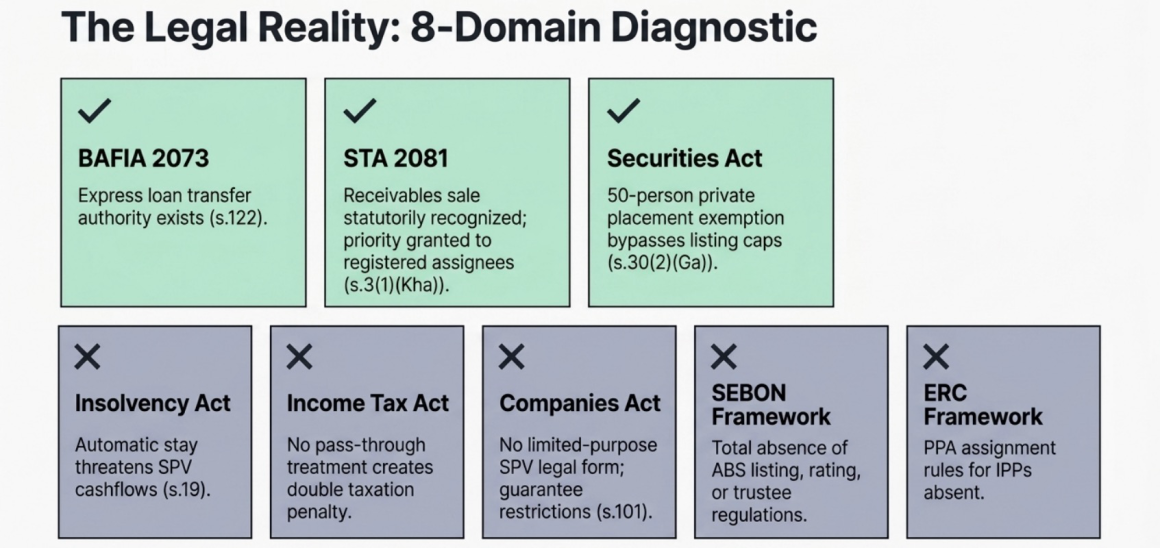

7. The Legal Framework: An Eight-Domain Gap Analysis

7.1 BAFIA 2073 and NRB Framework

Enabling Provisions

✔ ENABLING PROVISION – BAFIA Section 122: The most significant existing provision for securitization in Nepal. “Notwithstanding anything contained in the prevailing Nepal law [प्रचलित नेपाल कानूनमा जुनसुकै कुरा लेखिएको भए तापनि], except where otherwise provided in the loan agreement, any bank or financial institution may purchase or sell [खरिद बिक्री] the loans extended to any person, or the liabilities accepted by it, and the security interests [धितोको हक] held in movable or immovable property given as collateral therefor.”

Three features are critical:

- The non-obstante clause displaces conflicting general law

- The provision covers both the loan and the underlying security interest – no separate mortgage transfer required

- There is no restriction on the identity of the buyer – the buyer need not be a BFI; an SPV or trust qualifies

✔ ENABLING PROVISION – NRB CAF Section 6.3(e) / 6.4(e): The only express regulatory recognition of securitization in Nepal’s financial regulatory architecture. “Securitization or credit sale agreements with recourse may be carried out for purposes other than credit risk transfer (e.g. funding)… for an originating bank to achieve reductions in capital requirements, the risk transfer arising from a securitization or credit sale has to be deemed significant by the NRB.” This dormant provision is the statutory anchor for an NRB Securitization Master Direction.

✔ ENABLING PROVISION – BAFIA Section 50(1)(cha): The investment prohibition applies only to “securities of banks or financial institutions classified into Class A, B, and C by NRB.” A securitization SPV is not a Class A/B/C BFI. Therefore, BFIs are not prohibited from investing in ABS tranches issued by a securitization SPV.

✔ ENABLING PROVISION – BAFIA Section 50(1)(chha) + NRB Unified Directive No. 8: BFI investment in any single non-BFI organized institution is capped at 10% of Primary Capital; aggregate investment in all non-BFI organized institutions is capped at 30% of Primary Capital. ABS investment by BFIs is permitted within these caps.

Critical Gaps

✖ CRITICAL BARRIER – BAFIA Section 52 (Related Party Prohibition): A BFI may not provide “any loan or facility” to a “related person.” “Related person” includes any entity in which a BFI’s directors or significant shareholders (≥1% by NRB Directive, ≥2% by BAFIA Section 2(cha)) hold financial interest. If an SPV is established by the BFI, its directors or officers may overlap, making the SPV a related person and blocking credit enhancement, liquidity support, or first-loss guarantees from the BFI to the SPV. This cannot be resolved by NRB directive alone – it requires a statutory proviso to Section 52.

✖ CRITICAL BARRIER – BAFIA Section 109 (Banking Secrecy): The four enumerated exceptions to banking secrecy (information to NRB, credit exchange among BFIs, court orders, government requests) do not cover disclosure of borrower information to SPV trustees, rating agencies, or ABS investors. This makes any bulk portfolio transfer technically a breach of banking secrecy. Requires statutory amendment or NRB directive creating a fifth exception.

⚠ GAP – BAFIA Section 57 and SPV Enforcement: Section 57(5)-(8) grants BFIs the right to auction collateral and compel Land Revenue Offices to transfer title to auction buyers. These rights are granted to “bank or financial institution” specifically. When a loan is sold to a non-BFI SPV under Section 122, the SPV does not automatically inherit Section 57 powers. The BFI-servicer can conduct auctions on the SPV’s behalf under an agency arrangement, but there is no explicit statutory authorization for this delegation. Requires NRB directive recognizing delegated enforcement by servicer.

⚠ GAP – Borrower Consent for Mortgage Transfers: NRB Unified Directive No. 2 requires individual written consent from each borrower for loan transfers. The waiver (no consent needed if original bank continues relationship management) applies only to agriculture and energy sectors. For residential mortgage loans, individual written consent is required from every borrower. For a pool of 5,000 mortgages, this is practically impossible. Requires a new NRB directive extending the consent waiver to mortgage pools in a securitization context.

| Gap | Severity | Can NRB Fix by Directive? | Requires Statute? |

| Banking secrecy (s.109) | Critical | Arguable under s.109(2)(Ka) broad reading | Yes, for certainty |

| Related party prohibition (s.52) | Critical | No – express prohibition | Yes |

| SPV inheritance of s.57 enforcement | High | Yes – directive on servicer delegation | Preferred |

| Mortgage borrower consent | Critical | Yes – extend energy precedent | Not required |

| No true-sale definition | Critical | Partial – NRB can prescribe criteria | Yes, for full certainty |

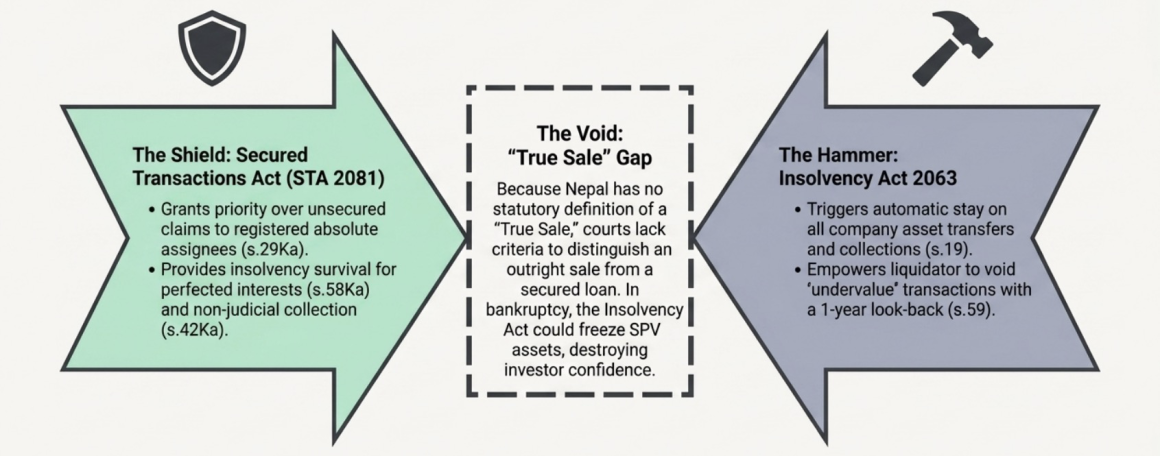

7.2 Secured Transactions Act 2063 (2081 Amendment)

The 2081 amendment to the STA is the single most positive recent development for securitization in Nepal. It materially repositioned the Act toward receivables-based finance. The key provisions, with their exact text, are as follows.

✔ ENABLING – Section 3(1)(Kha): Expressly brings within the Act’s scope “the sale of receivables (बहीखाताको बेचबिखन), whether or not for the purpose of securing an obligation.” This is the textual basis for treating an outright sale of receivables under the same registration, priority, and enforcement regime as a security assignment.

✔ ENABLING – Section 2(Jha1) (Movable Property): Includes “any nature of tangible or intangible property” and explicitly covers “future assets” (भविष्यमा सिर्जना हुने सम्पत्ति) and bank accounts. PPA receivables not yet accrued and toll revenues not yet collected are clearly within scope – even if it were to be argued that they do not form financial or intangible assets under Nepal Financial Reporting Frameworks (IFRIC 12) .

✔ ENABLING – Section 2(da) (Security Interest definition includes absolute assignee): The amended definition explicitly provides: “the term also includes the interest of a person who takes bahikhata/receivables by transfer [बहीखाता हस्तान्तरण गरी लिने व्यक्तिको अधिकार लाई समेत जनाउँछ].” This is the critical bridge: an absolute assignee (SPV) that registers its interest is treated as a “secured party” for priority and insolvency purposes.

✔ ENABLING – Section 29Ka (Priority over unsecured claims): A perfected security interest – including, by the amended definition, the interest of an absolute assignee – has priority over employee dues, tax arrears, and government claims. For securitization, this means the SPV’s registered interest in the receivables pool ranks above the originator’s unsecured creditors, including tax authorities, in insolvency.

✔ ENABLING – Section 58Ka (Insolvency survival): A perfected interest “shall remain intact [यथावत कायम रहनेछ]” when insolvency proceedings commence against the grantor. Combined with the amended Section 2(da), this provides the closest existing provision to statutory bankruptcy remoteness for an SPV that has registered its receivables assignment.

✔ ENABLING – Section 42(3Ka) (Anti-assignment override): Contractual restrictions on assignment are rendered unenforceable: “Notwithstanding anything contained in an agreement… the transfer of such account shall be effective.” Contractual non-assignment clauses in loan agreements, supply contracts, and PPAs cannot block securitization. Note: This nullifies contractual restrictions; it may not nullify the ERC Act’s statutory regulatory consent requirement under Section 13 (see Section 7.8 below).

✔ ENABLING – Section 42Ka (Direct collection right): An absolute assignee “may directly proceed to collect from the obligor at any time after default, without judicial proceedings.” This is a non-judicial enforcement right directly available to the SPV.

✔ ENABLING – Section 22 (Floating pool registration): “A description that identifies the property shall be considered sufficient.” Pool descriptions (e.g., “all housing loans originated between date X and date Y” or “all PPA receivables under Agreement No. Z”) are accepted – specific receivable-by-receivable identification is not required for perfection.

Critical Gaps

⚠ GAP – No True-Sale Characterization Criteria: Section 3(1)(Kha) brings outright sales within scope but provides no criteria to distinguish a true sale from a sale by way of security. Courts faced with an originator insolvency can apply common law tests (transfer of risk and rewards, recourse provisions, repurchase rights) without a domestic statutory anchor. Requires either statutory amendment inserting a true-sale definition, or an NRB directive prescribing true-sale criteria.

⚠ GAP – “Bahikhata” Definition Still Goods/Services Anchored: Section 2(fa) remains: “rights to receive payment for goods sold or leased or services rendered.” PPA receivables and toll revenues are arguably within “services rendered” but this is not settled. Section 2(Jha1)’s broad movable property definition provides a workaround, but the definitional ambiguity creates legal uncertainty for investors and rating agencies.

⚠ GAP – No Non-Obstante Override Clause: The STA contains no provision stating its provisions override conflicting laws. The Civil Code assignment formalities and the Insolvency Act’s avoidance provisions all potentially conflict with the STA’s registry-based regime without being expressly overridden.

7.3 Securities Act 2063 and SEBON Framework

✔ ENABLING – Securities Act Section 2(cha) Residual Clause: Securities are defined to include “other securities specified by the Board that can be traded or transferred through the securities market.” SEBON can designate ABS, pass-through certificates, and securitized debt instruments as “securities” by administrative notification – without parliamentary amendment.

✔ ENABLING – Securities Act Section 30(2)(Ga) (50-Person Private Placement Exemption): Where an offer is made to “a maximum of up to fifty persons at a time [एक पटकमा बढीमा पचास जनासम्म व्यक्तिलाई],” a full public prospectus is not required. This is the most important existing provision for a pilot ABS transaction. An SPV can privately place ABS to EPF, CIT, SSF, and a consortium of insurance companies (fewer than 50 institutional counterparties) using only a Private Placement Memorandum, entirely bypassing the 30:70 leverage cap, credit rating mandate, and NEPSE listing requirements.

✔ ENABLING – SIF Regulation Rule 22 (Qualified Investors): Defines institutional investor categories eligible for alternative investment vehicles – BFIs, insurance companies, pension/provident/welfare funds, CIT, bilateral/multilateral institutional investors, and Nepali corporate bodies with investment objectives. This definition can serve as the template for ABS investor eligibility in a future SEBON ABS Regulation.

✔ ENABLING – SEBON’s Directive Authority (Securities Act Sections 84, 116, 118): SEBON has broad power to issue regulations and directives on any capital market matter. It can issue a comprehensive “SEBON Guidelines on Asset-Backed Securities” covering SPV eligibility, disclosure, trustee requirements, private placement conditions, and eventually listing – all without parliamentary action.

Critical Gaps

✖ CRITICAL BARRIER – No SEBON ABS Regulatory Framework: There is no regulation governing the issuance, listing, trading, or disclosure requirements for ABS, MBS, or pass-through certificates. The Credit Rating Regulation 2068 contains no methodology for structured finance. The Securities Registration and Issuance Regulation 2073 prescribes only bullet-repayment fixed-rate instruments. The Securities Listing Regulation 2075 has no listing category for amortizing instruments. CDSC’s infrastructure cannot dynamically write down par value monthly as principal amortizes.

✖ CRITICAL BARRIER – No Listed ABS Pathway (30:70 Leverage Cap): Securities Registration and Issuance Regulation Rule 9 prohibits public debenture issuance if debt-to-equity exceeds 30:70. A securitization SPV by definition operates at 80-95% leverage. It cannot issue publicly listed debentures under current law. The 50-person private placement exemption is the only workable near-term pathway.

⚠ GAP – No Securitization Trustee License Category: Section 63’s list of licensable securities businesses does not include securitization trustees or servicers. No institution in Nepal currently provides securitization trustee services. Requires SEBON regulation creating a new license category.

⚠ GAP – Credit Rating Agencies Lack Structured Finance Methodology: Neither ICRA Nepal nor CARE Ratings Nepal has a published ABS rating methodology. Under Credit Rating Regulation Rule 27, any methodology must be made public before use.

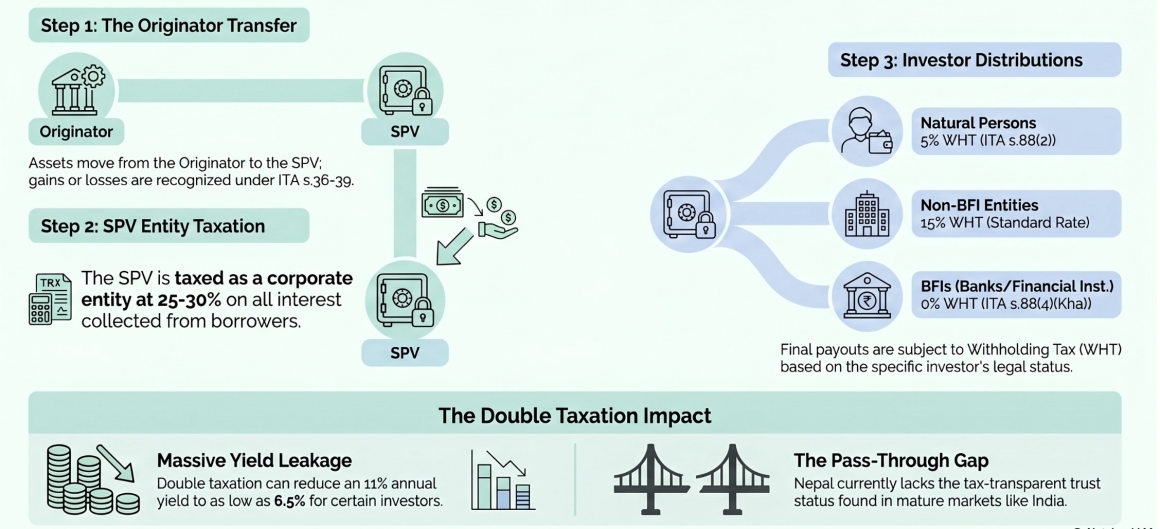

7.4 Income Tax Act 2058 – The Most Consequential Gap

✖ CRITICAL BARRIER – No Pass-Through Treatment: A securitization SPV is taxed as an entity (25-30% corporate rate as a company or trust) on receivables interest collected. Distributions to investors are then subject to further taxation (5% dividend WHT for individuals; 15% WHT for non-BFI entities; 6% for resident natural persons on interest). This double taxation – entity level then investor level – is the single most expensive structural problem.

The India Comparison: India resolved this via ITA Sections 115TCA and 194LBC (Finance Act 2016): securitization trust income is not taxed at entity level; investors are taxed directly; trustee withholds at a differentiated rate. This single Finance Act amendment transformed India’s securitization economics.

✔ ENABLING – ITA Section 10(Tha) (Mutual Fund Exemption): Income of a “Collective Investment Scheme (Mutual Fund) [सामूहिक लगानी कोष (म्युचुअल फण्ड)] approved by SEBON earned in accordance with its objectives” is fully tax exempt. However, the parenthetical “(म्युचुअल फण्ड)” strongly suggests this exemption was intended for entities licensed under the Mutual Fund Regulation 2067, not SIFs or ABS vehicles. IRD has not confirmed the exemption extends to SIFs.

✔ ENABLING – ITA Section 76 (Advance Ruling): A securitization SPV or originator can request a formal written ruling from IRD on how the law applies to its specific structure – including confirmation that the transfer will be treated as a true sale rather than a secured loan for tax purposes. This mechanism should be used in any pilot transaction.

⚠ GAP – ITA Section 35 (Anti-Avoidance): The IRD may disregard arrangements that have “no substantial economic effect [सारभूत आर्थिक असर]” or where the “principal purpose [मुख्य उद्देश्य]” is to obtain a tax benefit. A securitization structured for genuine capital relief, risk transfer, and liquidity – and documented with genuine commercial purpose evidence – should survive Section 35 scrutiny. An advance ruling under Section 76 provides written protection.

⚠ GAP – ITA Section 44 (Associated Person Rule): Transfers to associated persons (≥50% ownership/control) must be at market value. An originator retaining a 5-10% MRR (minimum retention requirement) does not trigger the 50% threshold and does not create an associated person relationship. However, if the originator nominates trustees and controls SPV governance, the IRD may still challenge the arm’s length character.

⚠ GAP – VAT on Servicing Fees: Financial services are generally VAT-exempt under Schedule 1 of the VAT Act 2052. However, a purely administrative servicing fee (collecting loan repayments, remitting to SPV) may be characterized as a taxable service rather than an integral financial transaction. This requires IRD clarification.

Nepal-India DTA (directly relevant for institutional cross-border ABS): Article 11(2): maximum 10% withholding on interest paid to Indian residents. Article 23: India provides tax credit for Nepal withholding, eliminating double taxation. This makes Nepali ABS economically accessible to Indian institutional investors at a net withholding cost of 10%.

7.5 Insolvency Act 2063

This Act is the single largest unresolved legal risk for securitization in Nepal. Even with STA 2081’s improved provisions, the Insolvency Act’s moratorium, avoidance powers, and priority waterfall create risks that override the STA protections in the event of originator insolvency.

✖ CRITICAL BARRIER – Section 19 (Automatic Stay): Upon commencement of insolvency proceedings, any “transfer, sale, or mortgaging of company assets [कम्पनीको सम्पत्ति हस्तान्तरण, बिक्री वा धितो राख्ने]” is automatically stayed, and collection of debts is suspended. There is no express carve-out for assets that were validly sold to an SPV before the insolvency commenced. The STA Section 58Ka protection helps, but the Insolvency Act’s moratorium could still be applied to freeze collections flowing from the pool to the SPV.

✖ CRITICAL BARRIER – Section 59 (Voidable Transactions): A liquidator may set aside:

- Preferential transactions: 6 months look-back (1 year for related parties)

- Undervalue transactions: 1 year look-back

- Fraudulent transactions: 2 years look-back

A discounted transfer of receivables to an SPV could be challenged as an “undervalue transaction” if the liquidator argues the originator received less than market value. Defense: the originator received fair market price; the transfer was a true sale not intended to defraud creditors.

⚠ GAP – Section 31 (Restructuring Manager’s Asset Powers): During restructuring, the manager can “end or sell any business or asset.” There is no express exclusion for assets previously sold to an SPV. A restructuring manager who does not acknowledge the true-sale nature of a prior securitization may attempt to treat the pooled assets as part of the originator’s estate.

⚠ GAP – Section 57 (Priority Waterfall): In liquidation, distribution follows: (1) liquidation costs, (2) inquiry/restructuring fees, (3) debts during inquiry period, (4) employee wages, (5) government dues, (6) unsecured creditors, (7) shareholders. If securitized assets are incorrectly brought into the originator’s estate, the SPV ranks only as an unsecured creditor (sixth priority) – far below employees and tax authorities.

Required Amendments:

- Section 19: Carve-out for assets validly transferred to a registered SPV prior to insolvency commencement

- Section 59: Safe harbour for true-sale transfers at arm’s length for fair market value

- Section 31: Exclusion of SPV-held assets from restructuring manager’s powers

- Section 57: Recognition that assets in a registered SPV do not form part of the originator’s estate

7.6 Companies Act 2063

⚠ GAP – No Special Purpose Company Provision: The Act provides no dedicated framework for limited-purpose companies. Any SPV must incorporate as a standard private (no minimum capital required) or public (minimum NPR 1 crore paid-up capital – Section 11(1)) limited company with full corporate formalities.

✔ ENABLING – Section 176(1) Guarantee Exemption for BFIs: The 60% of equity cap on guarantees does not apply to banking or financial institutions engaged in their ordinary course of business. An originator BFI providing credit enhancement to an SPV in its ordinary banking business is exempt from this cap.

✖ CRITICAL BARRIER – Section 101(1): Companies may not provide guarantees for loans taken by their directors, substantial shareholders, or their families. If an SPV has overlapping directors with the originator, the SPV cannot guarantee loans for those individuals. More significantly, this provision means SPV governance must be designed with independent directors.

7.7 Foreign Investment Law (FITTA 2075 and FERA 2019)

⚠ GAP – ABS Not Expressly Defined as Foreign Investment: FITTA Section 2(ञ) defines foreign investment exhaustively. ABS or MBS instruments are not named. Listed securities (Section 2(wyan)(5)) and instruments issued in foreign capital markets (Section 11) provide potential hooks, but an ABS issued domestically by an SPV and purchased by a foreign investor sits in a definitional gap.

✔ ENABLING – FITTA Section 26(1)(Kha): Foreign-invested companies may obtain foreign exchange to pay “principal and interest (सावाँ वा ब्याज) on bonds or debentures issued to foreign investors.” ABS coupon payments can be framed as interest on debentures for repatriation purposes.

✔ ENABLING – FERA Section 10Ga(1): NRB has authority to determine the process for repatriating investments in securities and their profits by administrative notice – no legislative amendment required for NRB to permit ABS coupon remittances to foreign investors.

⚠ GAP – Hedging Rules 2079: The Hedging Rules are focused on currency forward/peg arrangements for infrastructure FX debt. They do not provide interest rate swap or cross-currency swap mechanisms that ABS investors would need to hedge NPR interest rate exposure. Only entities with bond issuances above USD 20 million can access FX hedging facilities under Rule 3(5).

7.8 Sectoral Regulations – The ERC and PPA Assignment Problem

⚠ THE CORE QUESTION: Does ERC consent under Section 13(1)(Ga) of the ERC Act 2074 extend beyond the initial PPA execution to cover subsequent assignments of PPA receivables to a securitization SPV?

The ERC Act Section 13(1)(Ga) grants the Commission power to “grant consent to conclude electricity purchase agreements between licensed persons.” The statutory text uses only the word “conclude” (गर्न) – it does not expressly address assignment or novation of an existing PPA. However, ERC’s Five-Year Roadmap discloses that the Commission has reviewed and decided on 494 petitions for PPA amendment approvals, suggesting it treats subsequent modifications as within its jurisdiction.

✖ CRITICAL BARRIER: The standard NEA PPA templates are not publicly available for review, but they predate ERC’s full functionality and may contain contractual non-assignment clauses. The STA Section 42(3Ka) anti-assignment override nullifies contractual restrictions on receivables transfer. However, the ERC Act’s statutory regulatory consent requirement under Section 13 is not merely contractual – it is a statutory mandate. Whether the STA’s non-obstante framework overrides the ERC Act’s statutory requirement is unsettled in Nepali law and represents one of the most significant legal uncertainties in Case Study 1.

✔ SOLUTION PATH: ERC Act Section 43 grants the Commission authority to “frame and implement directives, standards, or codes on matters within its functions, duties, and jurisdiction, provided they are not contrary to this Act.” Because PPAs fall within ERC’s jurisdiction under Sections 13(1)(Kha) and (Ga), the ERC can issue a directive under Section 43 explicitly permitting the assignment of PPA receivables to qualifying securitization SPVs without requiring Parliamentary action. This is the cleanest resolution.

8. The SPV Vehicle Problem: Four Options, Four Limitations

Nepal’s law provides four possible legal vehicles for a securitization SPV. None is adequate as-is. Each has a distinct set of problems.

Comparison Matrix

| Feature | Company (Companies Act) | SIF (SIF Regulation 2075) | Mutual Fund Trust (MF Regulation 2067) | Guthi (Civil Code Sections 314-351) |

| Legal form | Company | Corporate body (company) | Trust (quasi) | Trust |

| Separate legal personality | ✔ Yes | ✔ Yes | ⚠ Partial (via Fund Supervisor) | ✖ No |

| Perpetual succession | ✔ Yes | ⚠ 5-15 yr lifespan | ⚠ Until dissolution | ✖ No |

| Bankruptcy remoteness | ✖ No statutory provision | ✖ No statutory provision | ✖ No statutory provision | ✖ No |

| Minimum capital | NPR 1 crore (public co.) | NPR 2 crore (fund manager) | None specified | None |

| Tranche waterfall | ✖ None (shares/debentures) | ✖ None (pro-rata units) | ✖ None (equal distribution) | ✖ None |

| Maximum investors | Unlimited (public) | 200 investors (Rule 16(Ga)) | Unlimited | Undefined |

| NEPSE listing | ✔ Possible | ✖ Not available | ✔ Possible | ✖ Not available |

| Pass-through tax | ✖ 25-30% entity + 5% dividend | ✖ 25-30% entity + 5% dividend | ✔ If treated as Mutual Fund (ITA s.10(Tha)) | ✖ Unclear |

| Debt-to-equity cap | ✖ 30:70 for public debentures | ✖ Same | ✖ Same | N/A |

| Commercial purpose | ✔ Yes | ✔ Yes | ✔ Yes | ⚠ Section 315(3) allows “profit for specific group” but Registrar refusal risk |

| Transferable investor units | ✔ Shares/debentures | ✔ Units (but closed, OTC only) | ✔ Units (listed) | ✖ No |

💡 KEY FINDING: The Mutual Fund Trust is the closest existing analog – it has a trustee structure, asset segregation via the Depository, investor units, and the ITA Section 10(Tha) exemption potentially available. However, it has no tranche waterfall (all unitholders rank equally at dissolution), and its income tax exemption may not extend to an ABS vehicle. The 50-person private placement using a SIF avoids NEPSE listing complications but creates double taxation. The most viable near-term approach is a private placement SPV incorporated as a company, using the Securities Act Section 30(2)(Ga) exemption, with GoN prescribing pass-through tax treatment via Finance Act amendment.

✔ THE MUTUAL FUND PRECEDENT: SEBON has already created a functional trust-based investment vehicle (the Mutual Fund) without a dedicated commercial Trust Act, using only regulatory authority. This precedent proves that NRB and SEBON can create a securitization trust vehicle through directives and regulations – a standalone Commercial Trust Act is not required for the first generation of Nepali securitization.

⚠ THE GUTHI QUESTION (MODALITY 2): Section 315(3) of the Civil Code defines a Private Guthi as one “kept with the objective of providing benefit, profit [लाभ], or facility to a specific person or group.” The inclusion of “profit” creates a hook for a commercial securitization trust. However, Section 319(1)(Ga) gives the Registrar power to refuse registration if the objective is “inappropriate or undesirable due to public interest or morality.” A Guthi holding financial receivables for investor profit faces real registration risk under this provision. The Civil Code Guthi does not contain transferable units, no tranche waterfall, and no bankruptcy remoteness – making it an inadequate SPV vehicle without significant amendment.

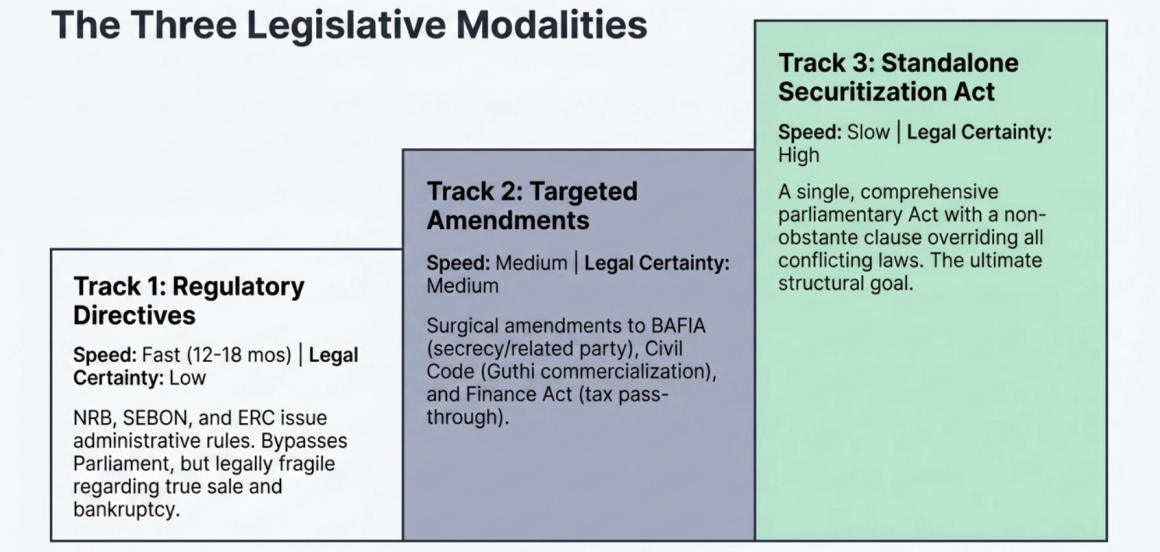

9. The Three Legislative Modalities

9.1 Modality 1: Securities Act Amendment + SEBON Regulation

Concept: SEBON exercises its existing directive-making authority under Securities Act Sections 84, 116, and 118 to issue comprehensive ABS Guidelines. Simultaneously, the Securities Act is amended to add ABS-specific definitions, a qualified investor framework, and a private placement memorandum regime. NRB issues a companion Securitization Master Direction for BFI originators.

What This Modality Covers:

- ABS designated as securities under Section 2(cha) (by SEBON notification)

- SPV as “Asset-Backed CIS” sub-category under Sections 71-75

- Securitization trustee and servicer licensing under Section 63

- ABS-specific disclosure standards (pool composition, waterfall, credit enhancement)

- Private placement to qualified institutional investors

- NRB capital adequacy treatment for ABS originators and investors

- NRB Securitization Master Direction: MHP, MRR, true-sale criteria, servicer standards

What This Modality Cannot Cover:

- True-sale statutory recognition (requires Secured Transactions Act or Insolvency Act amendment)

- Bankruptcy remoteness for SPV (requires Insolvency Act amendment)

- BAFIA Section 52 related-party carve-out (requires BAFIA amendment)

- BAFIA Section 109 banking secrecy exception (requires BAFIA amendment or robust NRB directive)

- Pass-through tax treatment (requires ITA amendment via Finance Act)

- ERC PPA assignment framework (requires ERC directive or Electricity Act amendment)

Minimum Viable Intervention (no parliamentary action):

| Action | Authority |

| SEBON notification designating ABS as securities | Securities Act s.2(cha) |

| SEBON ABS Guidelines (SPV criteria, disclosure, trustee, private placement) | Securities Act s.84/118 |

| NRB Securitization Master Direction | NRB Act s.79/80/111 |

| NRB directive on mortgage borrower consent waiver | BAFIA s.54/132 |

| NRB directive on banking secrecy exception for loan transfers | BAFIA s.54/132 |

| ERC directive on PPA receivable assignment | ERC Act s.43 |

| Institutional investor bylaw amendments (EPF, CIT, SSF, insurance) | Board approval + regulatory clearance |

Assessment: This modality can enable pilot transactions without parliamentary action. However, it creates a fragile legal edifice – every transaction operates under legal uncertainty about true-sale characterization and bankruptcy remoteness. Sophisticated investors and rating agencies will demand legal opinions that cannot be given with confidence without statutory clarity. This modality is necessary but insufficient as a long-term framework.

9.2 Modality 2: Civil Code Trust Amendment

Concept: Amend Part 4, Chapter 6 of the National Civil Code 2074 (the Guthi provisions, Sections 314-351) to explicitly recognize a “Securitization Trust” (मौद्रिकीकरण गुठी) as a distinct legal category with transferable beneficial interests, waterfall distribution mechanics, registration with OPMCM/MoF/SEBON and limited bankruptcy exposure.

Current Hook – Section 315(3): Private Guthi for “profit [लाभ] of a specific group” is currently recognized. This is theoretically available for a commercial securitization trust.

What Amendments Are Required:

- Explicit definition of “Securitization Trust” with permissible purpose: holding financial receivables and distributing cash flows to investor-beneficiaries

- Mechanism for issuing transferable “beneficial interest certificates” in multiple classes (senior, mezzanine, junior) with defined priority of distribution

- Explicit bankruptcy remoteness provision: Guthi assets are not available to the originator/settlor’s creditors upon its insolvency

- Trustee fiduciary duties: independent trustee with duties to all investor-beneficiary classes

- Dissolution mechanism preserving waterfall priority

- Coordination with Securities Act for SEBON registration of issued certificates

Structural Limitations (even with amendment):

- A Guthi is not a legal person – it cannot sue or be sued in its own name without the trustee acting

- No equivalent of Companies Act “perpetual succession” – dissolution triggers may be complex

- The Registrar-based registration system (currently under Land Revenue Office) (under Sections 316-320) is designed for religious/charitable trusts, not commercial financial vehicles

- Interaction with Insolvency Act still unresolved – Civil Code cannot override the Insolvency Act’s moratorium without a non-obstante clause

Assessment: Modality 2 addresses the SPV vehicle gap more elegantly than Modality 1 (which relies on a company form) by creating a true trust structure. However, it leaves the most critical gaps unresolved: true-sale, bankruptcy remoteness (unless the Civil Code amendment includes an explicit override of the Insolvency Act’s moratorium), amendment in who is the registrar for such trusts, and tax pass-through (still requires ITA amendment). As a standalone modality, it is inadequate. As one element of a three-track reform, amending the Guthi provisions to create a commercial trust vehicle is valuable and should be pursued alongside the other tracks.

9.3 Modality 3: Standalone Nepal Securitization Act

Concept: Parliamentary enactment of a comprehensive Nepal Securitization Act covering the full securitization architecture – SPV creation, true sale, bankruptcy remoteness, enforcement, ARC licensing, investor protection, and cross-regulatory coordination – with a non-obstante clause overriding conflicting provisions of BAFIA, the Insolvency Act, the Income Tax Act, and the ERC Act.

What This Act Should Contain:

| Chapter | Key Provisions |

| Definitions | Securitization, true sale, SPV/SSPE, originator, servicer, securitization trustee, pass-through certificate, credit enhancement, tranching, waterfall, MRR, security receipt |

| True Sale | Statutory criteria for characterizing an asset transfer as a true sale; non-obstante override of Insolvency Act avoidance provisions; registry-validated bankruptcy remoteness |

| SPV/SSPE | Dedicated “Securitization Special Purpose Entity” legal form; statutory bankruptcy remoteness; perpetual succession; ring-fenced compartments for different pools |

| ABS Issuance | SEBON-regulated issuance framework; mandatory credit rating; qualified investor private placement regime; listed ABS on dedicated NEPSE segment |

| Enforcement | SARFAESI-equivalent non-judicial enforcement for SPVs and ARCs; DRT standing for non-BFI entities; servicer delegation authority |

| ARC Licensing | NRB-licensed Asset Reconstruction Companies for NPA securitization; security receipt issuance framework |

| Tax Provisions | Pass-through treatment for securitization trusts; originator gain deferral; TDS at investor level at differentiated rates |

| Sectoral Coordination | ERC PPA assignment authorization; Roads Act receivable assignment; CAAN revenue securitization authority and others as applicable |

| Non-Obstante | “Notwithstanding anything contained in BAFIA, the Insolvency Act, the Income Tax Act, the ERC Act, or any other prevailing law…” or in coordination with amendment within these other conflicting laws as well |

International Models to Draw From:

- Philippines RA 9267 (Securitization Act 2004): Best structural template for SPV legal form and bankruptcy remoteness

- India SARFAESI Act 2002: ARC model for NPA securitization; enforcement framework

- Thailand Royal Enactment B.E. 2540: Standalone securitization statute for a civil law jurisdiction

- EU Securitisation Regulation 2017/2402: STS designation framework; risk retention; disclosure standards

Assessment: The most complete and legally certain approach. A non-obstante clause can override every conflicting provision across all regulatory domains in a single instrument. However, it requires parliamentary action – at minimum an ordinary majority in the House of Representatives (financial sector laws do not require special majority under the Constitution). If tax provisions are included (ITA amendment), the Act may qualify as a “Finance Bill” (अर्थ विधेयक) and must originate in the House of Representatives.

9.4 Comparative Assessment

| Criterion | Modality 1 (SEBON Reg) | Modality 2 (Civil Code) | Modality 3 (Standalone Act) |

| Speed | 1 | 2 | 3 |

| Parliamentary action required | No (regulatory action only) | Yes (Civil Code amendment) | Yes |

| True-sale legal certainty | Low | Medium | High |

| Bankruptcy remoteness | Low | Medium | High |

| Tax pass-through | Requires separate Finance Act | Requires separate Finance Act | Built-in / seperate |

| ARC/NPL securitization | Cannot cover | Cannot cover | Built-in |

| Cross-regulatory (ERC, Roads, CAAN) | Partial (ERC directive only) | Partial | Full / seperate |

| Investor confidence / rating agency acceptance | Medium | Medium | High |

| Cost of implementation | Low | Medium | High |

💡 ASSESSMENT: Modality 1 enables the first pilot transaction within 12-18 months. Modality 2 creates a trust-based SPV vehicle superior to the company form for the medium term. Modality 3 creates the complete, legally certain architecture that will define Nepal’s securitization market for decades.

10. The Tax Architecture

The tax treatment of securitization cash flows at each step of the transaction is the most consequential determinant of economic viability. Under current law, double taxation makes securitization uneconomic for most asset classes.

Current Tax Treatment – Step by Step

The Double Taxation Problem

If a securitization pool generates 11% annual yield from underlying loans:

- SPV pays 25-30% corporate tax → net yield ≈ 7.7-8.25%

- Investors then pay 5-15% WHT → net yield ≈ 6.5-7.8%

The double taxation could render securitization economically inferior to other alternative investments when considering the risk-return ratio. Thus a Finance Act amendment creating ITA equivalent pass-through treatment for securitization SPV could be arguged as prerequisite reform for their economic viability.

Recommended Tax Architecture

| Tax Treatment | Recommended Approach | Legal Pathway |

| SPV entity-level tax | Zero – treat securitization trust as transparent | Finance Act: new ITA section modeled on India’s s.115TCA |

| Investor-level WHT | Differentiated: 5% (natural persons), 0% (BFIs, EPF), 10% (foreign per DTA) | New ITA section prescribing rates; ITA s.76 advance ruling for interim |

| Originator gain on transfer | Spread over pool life per accounting convention (not recognized upfront) | ITA amendment; interim: advance ruling under s.76 |

| VAT on servicing fees | Exempt as integral financial service | VAT Act Schedule 1 clarification; IRD ruling |

| Associated person (s.44) | 5-10% MRR does not trigger 50% threshold | No amendment required; document arm’s length / include exceptions for investor’s confidence. |

Tax Efficient Pathway Under Current Law

Without any legislative change, the most tax-efficient approach available today is:

- Structure the ABS vehicle as a Mutual Fund (if SEBON will approve a hybrid CIS)

- The Mutual Fund exemption under ITA Section 10(Tha) eliminates entity-level tax

- Distributions taxed at 5% WHT (final for natural persons)

- Risk: IRD may not accept that an ABS vehicle qualifies as a “Mutual Fund” under the parenthetical in ITA s.10(Tha) – advance ruling under Section 76 is essential before structuring this way

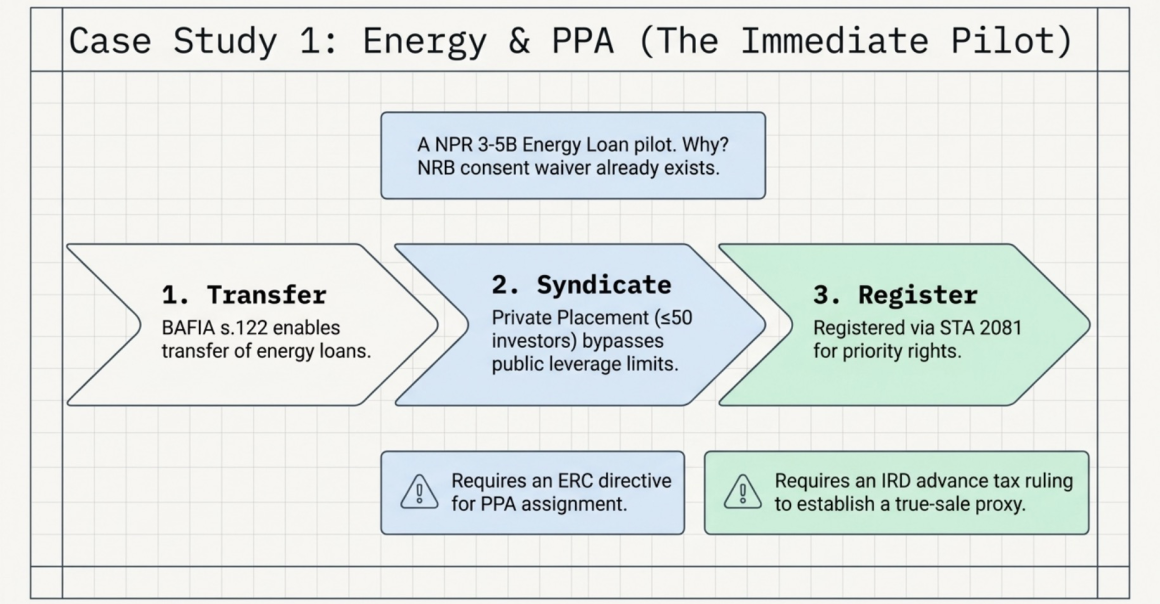

11. Case Study 1 – Hydropower PPA Receivable Securitization

Scenario: A cash-strapped hydropower developer (50 MW, post-COD, PPA with NEA at NPR 8.50/kWh, 20 years residual PPA life) wishes to securitize NPV of its future PPA receivables to fund a new cascade project.

Step-by-Step Legal Analysis

Step 1: Originator Eligibility and Sectoral Authorization

| Question | Answer | Legal Provision | Gap? |

| Can IPP transfer PPA receivables? | Conditional | STA s.3(1)(Kha); s.2(Jha1) | See ERC consent issue below |

| Does ERC consent apply to assignment? | Unclear | ERC Act s.13(1)(Ga) | ⚠ Critical uncertainty |

| Can STA anti-assignment override nullify PPA no-assign clause? | Yes (contractual) | STA s.42(3Ka) | Statutory ERC requirement not nullified |

| Can ERC issue directive permitting assignment? | Yes | ERC Act s.43 | ✔ This is the resolution path |

⚠ THE ERC BOTTLENECK: The Electricity Regulatory Commission has approved 494 PPA amendment petitions historically, confirming its de facto jurisdiction over PPA modifications. However, it has never issued a directive on PPA receivable assignment to SPVs. Under Section 43, it has full authority to do so. The ERC must issue a Directive on PPA Receivable Assignment before Case 1 can proceed with full legal certainty. The directive should:

- Define “qualifying securitization SPV” eligible to receive PPA receivables

- Confirm NEA’s payment obligations to the SPV are unaffected by the originator’s financial distress

- Require SPV to notify ERC of any material change in pool composition

- Preserve ERC’s right to regulate tariffs applicable to the underlying PPA

Step 2: Asset Transfer to SPV

The PPA receivables (monthly payments from NEA) are transferred to the SPV. The STA provides the operative framework:

| Legal Element | Provision | Status |

| Receivables within scope | STA s.3(1)(Kha) – sale of receivables | ✔ Enabled |

| Future receivables included | STA s.2(Jha1) – future assets explicitly included | ✔ Enabled |

| Anti-assignment override | STA s.42(3Ka) – contractual restrictions unenforceable | ✔ Enabled (contractual only) |

| Registration of assignment | STA s.22 – floating pool description accepted | ✔ Enabled |

| Priority over unsecured claims | STA s.29Ka – perfected interest of assignee | ✔ Enabled upon registration |

| Insolvency protection | STA s.58Ka – survives originator insolvency | ✔ Enabled |

| True-sale characterization | Not defined in any Nepali statute | ✖ Gap – IRD advance ruling needed |

Step 3: SPV Incorporation

Under current law, the SPV must be incorporated as a company under the Companies Act 2063, with:

- Minimum paid-up capital: NPR 1 crore (if public company) or as determined (if private)

- Independent directors (recommended) to address BAFIA Section 52 related-party risk

- SEBON registration once SEBON designates ABS as securities under Section 2(cha)

- STA registry registration of the PPA receivables assignment

STRUCTURAL RISK: No bankruptcy remoteness provision exists for the company-form SPV. If the originator IPP is placed in insolvency, the Insolvency Act’s automatic stay (Section 19) could be applied to freeze NEA payments flowing to the SPV unless the SPV can demonstrate (a) the assets were validly sold (true sale) and (b) the STA registration creates legal separation recognized by the insolvency court.

Step 4: ABS Issuance to Investors

Near-Term (Pilot): Using Securities Act Section 30(2)(Ga) – private placement to ≤50 investors:

- Issue pass-through certificates to EPF, CIT, SSF, and a consortium of insurance companies

- No public prospectus required; use Private Placement Memorandum

- No NEPSE listing required

- No 30:70 leverage cap applicable

- Rating not mandatory (though highly recommended; 12-18 months to develop ICRA Nepal/CARE methodology)

Investor Eligibility Matrix:

| Investor | Current Bylaw | ABS Permitted? | Required Change |

| EPF | Government securities, bank FD, equity, debentures | ✖ | Board + GoN approval of revised policy |

| CIT | Government securities, bank FD, equity, listed debentures | ✖ | Board + GoN approval |

| SSF | Government securities, bank FD | ✖ | Board + GoN approval |

| Life insurance companies | Gov securities, bank FD, equity, rated debentures | ✖ | NAI Investment Guideline amendment |

| Commercial banks | Securities of non-BFI entities (10% per entity cap) | ✔ Subject to cap | No amendment required |

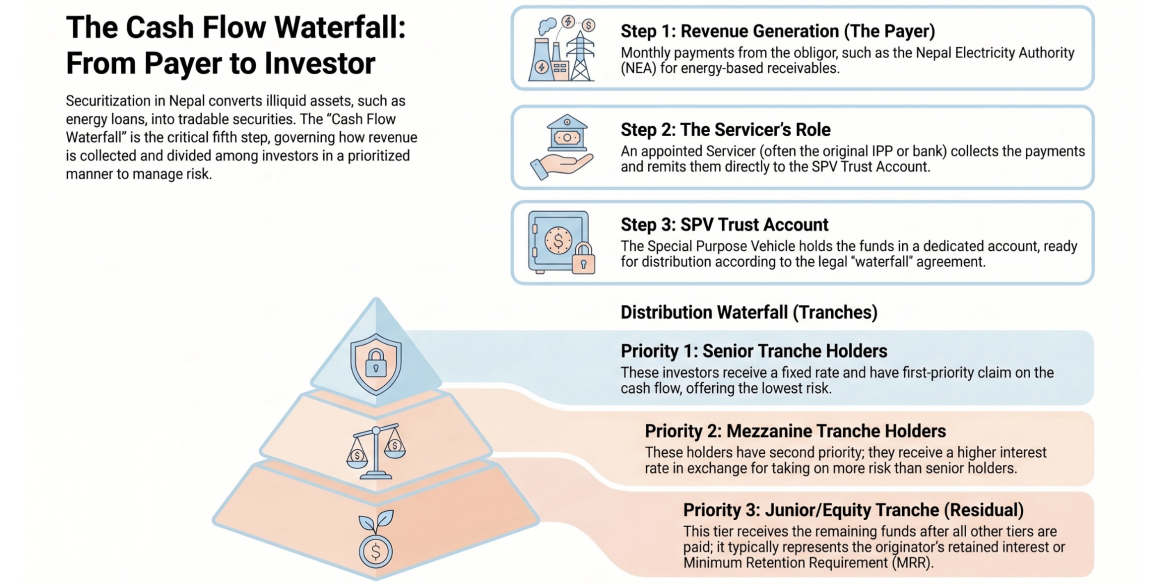

Step 5: Cash Flow Waterfall

Key legal risk here: The SPV’s right to step into the originator’s shoes upon IPP default is not expressly provided in the Electricity Act 2049. If the IPP’s generation license is suspended or revoked, the underlying PPA may be affected. Government-guaranteed structures (unlikely for most private IPPs) would significantly improve credit quality.

Step 6: Default, Enforcement, and Termination

Upon borrower/counterparty default:

- STA Section 42Ka: SPV may collect directly from NEA without court proceedings

- BAFIA Section 57: Not directly available to SPV (only to BFIs)

- BFI-servicer: Can enforce collateral on SPV’s behalf under NRB Unified Directive No. 2 if servicer is the original lending bank

- ERC step-in rights: If ERC directive is properly drafted, SPV can request ERC to enforce NEA’s PPA payment obligations

Case 1: Gap Summary

| Gap | Severity | Resolution |

| ERC framework for PPA assignment | Critical | ERC directive under s.43 |

| True-sale statutory recognition | Critical | ITA advance ruling; eventual STA amendment |

| SPV bankruptcy remoteness | Critical | Insolvency Act amendment; Modality 3 |

| Pass-through tax treatment | Critical | Finance Act amendment |

| ABS regulatory framework (SEBON) | High | SEBON ABS Guidelines |

| Investor bylaw amendments | High | Institutional board approvals |

| Rating agency methodology | High | 12-18 months development |

| Step-in rights under Electricity Act | High | Electricity Act amendment or ERC directive |

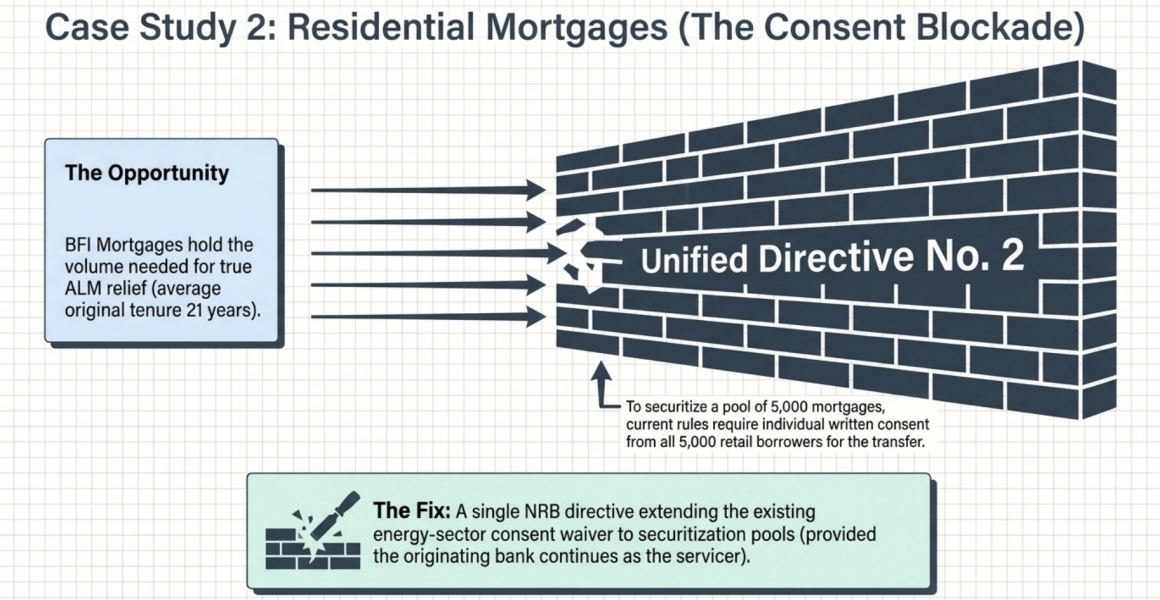

12. Case Study 2 – BFI Residential Mortgage Securitization

Scenario: A large commercial bank (NPR 400 billion in assets, CAR 12.5%, holding NPR 40 billion in residential mortgage loans with average remaining tenor of 15 years) wishes to securitize a pool of NPR 5 billion in performing mortgages to improve its ALM profile and free up capital.

Step-by-Step Legal Analysis

Step 1: Originator Eligibility

Class A commercial banks have the cleanest originator eligibility in Nepal’s legal framework:

- Governed by BAFIA 2073 – the most mature regulatory framework

- NRB is both supervisor and securitization regulator (potential for NRB directive alone to create meaningful change)

- BAFIA Section 122 explicitly permits loan and security interest transfer

Step 2: Asset Transfer – The Borrower Consent Problem

THE MOST CRITICAL BARRIER FOR CASE 2:

NRB Unified Directive No. 2 requires individual written consent from each borrower for loan transfers. The consent waiver (agriculture/energy: no consent needed if original bank continues relationship management) does not extend to residential mortgages.

Practical impact: A pool of 500 mortgage borrowers requires 500 individual written consents. For a pool of 5,000, the compliance burden becomes operationally impossible. Unlike the PPA context (where one corporate counterparty NEA exists), retail mortgage pools involve thousands of individual natural persons.

| Consent Requirement | Category | Current Rule | Can NRB Fix? |

| Agriculture loans | No consent if bank continues relationship management | ✔ Waived | N/A |

| Energy/hydropower loans | No consent if bank continues relationship management | ✔ Waived | N/A |

| Residential mortgages | Individual written consent required | ✖ Not waived | ✔ Yes – NRB can extend the waiver by directive under BAFIA s.54/132 |

Recommended NRB directive language: “In securitization transactions involving pools of residential mortgage loans where (a) the originating BFI continues as servicer maintaining the borrower relationship, (b) the transfer does not alter the borrower’s contractual obligations, interest rate, or payment schedule, and (c) the borrower is notified in writing within 30 days of transfer, the requirement of individual written borrower consent under this Directive shall not apply.”

Step 3: Transfer Mechanics

If the consent issue is resolved (by NRB directive):

| Legal Element | Provision | Status |

| Loan transfer authority | BAFIA s.122 (non-obstante) | ✔ Enabled |

| Mortgage security interest transfer | BAFIA s.122 (expressly covers immovable property security) | ✔ Enabled |

| Registration of assignment | STA s.22 (floating pool description) | ✔ Enabled |

| True-sale recognition | Not defined | ✖ Gap – advance ruling needed |

| Banking secrecy exception | No express exception in BAFIA s.109 | ✖ Gap – NRB directive needed |

| Insolvency protection | STA s.58Ka + 29Ka | ✔ Partial |

Banking Secrecy Resolution Path: NRB can issue a directive under BAFIA Section 109(2)(Ka) (existing broad reading: information as required by NRB directives) creating a fifth exception for disclosures to SPVs, trustees, rating agencies, and ABS investors in connection with loan transfers under Section 122.

Step 4: Collateral Enforcement – The SPV and BAFIA Section 57

When a mortgaged property becomes defaulted in the SPV’s pool:

- The SPV does not hold a BAFIA license and cannot directly invoke Section 57 auction powers

- The BFI-servicer (the originating bank) can conduct the auction as agent of the SPV

- The statutory basis: NRB Unified Directive No. 2 requires the purchasing entity (SPV) to ensure it has the “legal right to recover the loan from the customer” – the BFI-servicer fulfills this on the SPV’s behalf under a Servicing Agreement

- Legal gap: There is no express statutory authorization for the BFI to exercise Section 57 powers on behalf of a non-BFI principal. NRB directive on servicer delegation is essential.

Step 5: ABS Issuance

Same as Case 1: private placement to ≤50 institutional investors under Securities Act Section 30(2)(Ga).

Capital Relief Calculation (Illustrative):

If Nabil Bank securitizes NPR 5 billion in performing mortgage loans (60% LTV, no recourse):

- Current RWA for residential mortgages: 60% risk weight (NRB Capital Adequacy Framework)

- RWA removed: NPR 5 billion × 60% = NPR 3 billion

- Capital freed: NPR 3 billion × 11% CAR = NPR 330 million

- This freed capital can support NPR 330 million in additional Tier 1 base or extend NPR 3 billion in new lending at 11% CAR requirement

💡 MOTIVATION CHECK: Banks in Nepal are motivated to securitize energy loans (sectoral SOL headroom), not primarily mortgages (LTV caps are conservative, NPL on mortgages is low). The ALM improvement is the primary motivation for mortgage securitization, not capital relief per se. However, as the energy sector approaches the 10% NRB target by 2084 and SOL limits are reached at individual bank level, mortgage securitization becomes the next logical release valve.

Case 2: Gap Summary

| Gap | Severity | Resolution |

| Mortgage borrower consent waiver | Critical | NRB directive extending energy-sector precedent to mortgages |

| Banking secrecy exception | Critical | NRB directive; BAFIA s.109 amendment |

| BAFIA s.52 related party (if SPV is bank subsidiary) | Critical | Design SPV with independent directors; or BAFIA amendment |

| SPV bankruptcy remoteness | Critical | Insolvency Act amendment; Modality 3 |

| BFI-servicer Section 57 delegation | High | NRB directive on servicer delegation authority |

| Pass-through tax | Critical | Finance Act amendment |

| SEBON ABS framework | High | SEBON ABS Guidelines |

13. Case Study 3 – Toll Road Revenue Securitization

Scenario: The Department of Roads or a PPP concessionaire for the Kathmandu-Terai Fast Track Expressway wishes to securitize future toll revenue streams to fund further expressway construction.

Legal Analysis (Summary)

Asset Type: Toll revenues are “future receivables” under STA Section 2(Jha1)’s definition of movable property, which explicitly includes future assets and intangibles. The assignment of future toll revenues to an SPV is technically within the STA’s scope.

Key Differences from Cases 1 and 2:

| Feature | Toll Revenue vs. Cases 1 & 2 |

| Originator type | Government entity (DoR) or PPP concessionaire (private) |

| Revenue predictability | Lower than PPA (usage-dependent, no take-or-pay) |

| Enabling sectoral law | Roads Act – silent on receivable assignment |

| Regulatory consent needed | Ministry of Physical Infrastructure + MOF |

| Credit quality | Quasi-sovereign if DoR is originator; government guarantee possible |

| Data availability | No traffic revenue history for FastTrack (new toll road) |

Critical Gaps Specific to Case 3:

- No Roads Act provision authorizing toll receivable assignment to SPV (unlike ERC Act Section 43 which gives ERC directive authority)

- No traffic/revenue data history makes rating agency assessment impossible initially (minimum 2-3 years of operational revenue data needed)

- If DoR (government department) is originator, PDMA Section 14 guarantee framework could be used – but the 1% of GDP annual guarantee ceiling (PDMA Rule 36(5)) and existing NAC contingent liability (NPR 52.46 billion) severely constrain fiscal space

💡 ASSESSMENT: Toll road securitization is a long-term (Phase 3) opportunity. It requires (a) a Roads Act amendment authorizing receivable assignment, (b) minimum 2-3 years of revenue data, and (c) fiscal space for any government credit enhancement. Unlike hydro (strong PPA framework) and mortgages (clear regulatory base), toll roads require greenfield legal architecture.

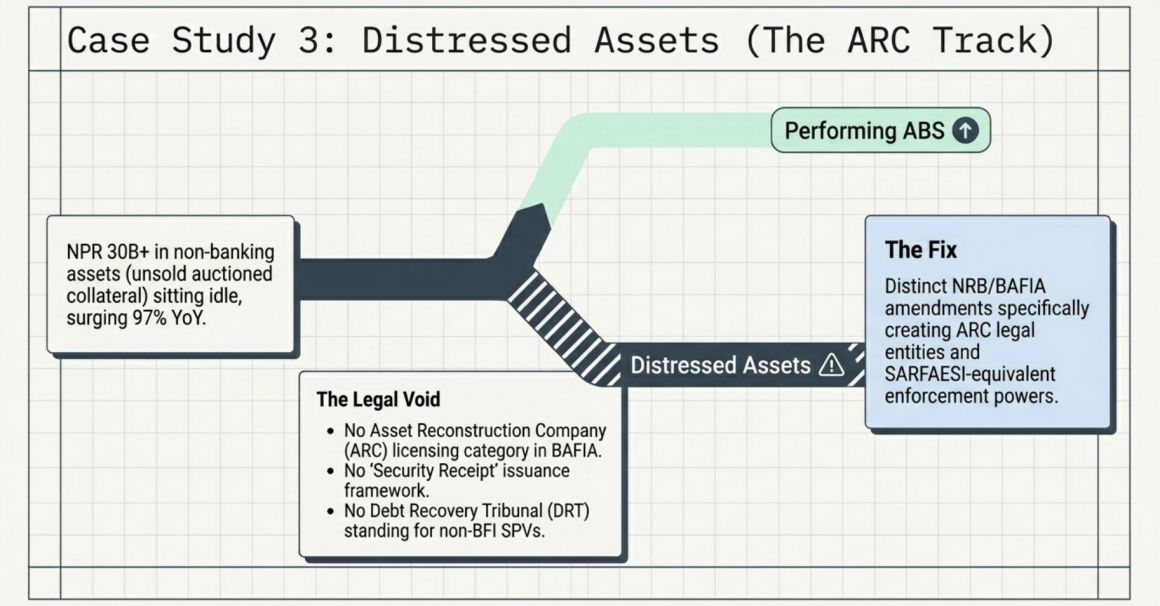

14. Distressed Asset Securitization: The ARC Track

Nepal’s NPL problem is sufficiently acute – rising year-on-year, with non-banking assets (unsold auctioned collateral) surging 97% to NPR 30.15 billion – to justify a parallel and distinct securitization track: distressed asset securitization through an Asset Reconstruction Company (ARC) model.

Why the ARC Model is Different

| Feature | Performing Asset Securitization | Distressed Asset Securitization (ARC) |

| SPV type | Pass-through trust or SIF | Licensed ARC company |

| Asset quality | Performing loans | Non-performing loans |

| Primary investors | EPF, CIT, insurance companies | Distressed debt funds, specialist ARCs |

| Instruments issued | Pass-through certificates, ABS | Security receipts (SRs) |

| Recovery mechanism | Contractual cash flows | Restructuring, auction, workout |

| Enforcement regime | STA direct collection | SARFAESI-equivalent (currently absent) |

| Regulatory framework | NRB + SEBON | NRB licensing of ARC |

The Current Legal Void

CRITICAL ABSENCE: There is no ARC licensing category under BAFIA 2073 or the NRB Act 2058. NRB Act Section 86Ga(13) authorizes “securitization” as a resolution tool for problem banks – but this provision is applicable only in the context of NRB’s resolution powers over distressed BFIs, not for routine NPA portfolio transfers by going-concern banks.

DRT STANDING GAP: The Debt Recovery Act 2058 grants Debt Recovery Tribunal jurisdiction only to designated BFIs (Section 3). An ARC that acquires an NPA pool from a bank has no DRT standing – it must use ordinary civil courts for enforcement, which can take 5-10 years versus the DRT’s mandated 150-day timeline.

SECURITY RECEIPT FRAMEWORK: Security receipts (the instrument ARCs issue to investors against NPA pools) are not defined, regulated, or recognized anywhere in Nepali law.

What Needs to Be Done for the ARC Track

Short-term (NRB directive):

- NRB can designate ARCs as “financial institutions” under Debt Recovery Act Section 3(Gha) – giving them DRT standing without parliamentary action

- NRB can issue a directive under BAFIA Section 54 prescribing minimum capital, conduct, and reporting standards for ARC operations as a condition of licensing

Medium-term (BAFIA or NRB Act amendment):

- Add ARC as a distinct licensed entity category under BAFIA Section 78 or NRB Act Section 86Ga

- Define security receipts as regulated instruments

- Prescribe SR issuance framework, qualified buyer categories, and SR listing on NEPSE

Long-term (Securitization Act Chapter):

- Comprehensive ARC chapter in the Nepal Securitization Act

- SARFAESI-equivalent non-judicial enforcement: demand notice → 60-day cure period → SPV/ARC takes possession and sells without court order; borrower appeals to DRT afterward

- ARC restructuring powers: interest capitalization, maturity extension, debt-to-equity conversion

💡 IMMEDIATE OPPORTUNITY: NPR 30.15 billion in non-banking assets (banks holding unsold auctioned collateral on balance sheet) is ideal for immediate ARC acquisition. These are already resolved assets with clear title – not stressed performing loans requiring restructuring. A pilot ARC transaction could be structured around this inventory using BAFIA Section 122 and NRB’s Section 86Ga resolution authority, even before formal ARC licensing legislation is enacted.

15. The Pilot Pathway: What Can Be Done Without Parliament

A pilot securitization transaction is legally possible under existing law, without any parliamentary action, if the following regulatory interventions are made:

Minimum Viable Regulatory Package

| # | Intervention | Authority | Who Needs to Act |

| 1 | Designate ABS as securities under Securities Act s.2(cha) | Securities Act s.2(cha) | SEBON |

| 2 | Issue NRB Securitization Master Direction (MHP, MRR, true-sale criteria, capital treatment, servicer standards) | NRB Act s.79/80/111; BAFIA s.54/132/133 | NRB |

| 3 | Extend mortgage borrower consent waiver to securitization pools | NRB Unified Directive No. 2 amendment | NRB |

| 4 | Create banking secrecy exception for loan transfer data sharing | BAFIA s.109(2) interpretation or NRB directive | NRB |

| 5 | Issue SEBON ABS Guidelines (SPV criteria, disclosure, trustee licensing, private placement rules) | Securities Act s.84/118 | SEBON |

| 6 | Issue ERC directive permitting PPA receivable assignment to qualifying SPVs | ERC Act s.43 | ERC |

| 7 | Amend EPF, CIT, SSF, insurance company investment bylaws to include rated ABS | Board resolutions + NRB/SEBON/NIA approval | Institutional boards + regulators |

| 8 | Rating agency structured finance methodology development | Credit Rating Regulation Rule 27 | ICRA Nepal / CARE Nepal with parent company support |

| 9 | IRD Advance Ruling on true-sale treatment and tax characterization | ITA s.76 | IRD |

| 10 | NRB directive on servicer delegation of Section 57 enforcement authority | BAFIA s.54 | NRB |

The Recommended Pilot Transaction

Structure: BFI-originated energy loan ABS, private placement to ≤50 institutional investors

Why energy loans and not mortgages first:

- Energy loans: consent waiver already exists (agriculture/energy precedent) → no borrower consent required

- Mortgage loans: individual consent required from thousands of borrowers → impossible without new directive

- Energy loans: clear sectoral narrative (NRB’s 10% energy target creates bank motivation)

- Energy loans: ERC framework for underlying revenue (NEA PPA backstop)

Target originator: Tier 1 commercial bank (Nabil, NMB, Himalayan, or Everest) with energy loan portfolio at or near sectoral concentration limit

Pool: NPR 3-5 billion in performing energy/hydropower loans, 3+ year seasoning, NPL rate <2%, all secured

Investors: EPF (anchor buyer), CIT, 2-3 insurance companies – total below 50 persons

Structure: Company-form SPV, BAFIA Section 122 transfer, STA registry registration, private placement PPM under Securities Act Section 30(2)(ग)

Credit enhancement: 10-15% overcollateralization (originator retains junior tranche as MRR)

Rating: Internal credit assessment initially; ICRA Nepal structured finance rating once methodology is ready

Tax: IRD advance ruling under ITA Section 76 for true-sale treatment; entity-level taxation acknowledged as temporary impairment pending Finance Act amendment

16. The Three Modalities: Comparative Assessment and Reform Roadmap

Recommended Three Modalities

The Recommendation

💡 EDITORIAL ASSESSMENT: Of the three modalities, Modality 3 (Standalone Nepal Securitization Act) is the most complete long-term solution because only a non-obstante statute can override conflicting provisions of BAFIA, the Insolvency Act, the Income Tax Act, and the ERC Act simultaneously. The Philippines RA 9267, India’s SARFAESI, and Thailand’s Royal Enactment all demonstrate that a single dedicated statute creates the legal certainty that investors and rating agencies require. However, under this modality Nepal might have to wait years for a Securitization Act while its banking system’s ALM mismatch widens and its institutional investors have nowhere to deploy their growing assets.

⚠ THE SEQUENCING IMPERATIVE: Tax reform must precede or accompany market building. If the Finance Act amendment creating pass-through treatment is delayed, the economics of securitization remain impaired and even a legally clean pilot transaction will underperform. Stakeholders should formally recommend the Finance Act amendment to the Ministry of Finance.

17. References

Primary Legislation

| Document | Citation |

| Bank and Financial Institutions Act (BAFIA), 2073 | Sections 2(cha), 2(KaNa), 50(1)(cha), 50(1)(chha), 52, 54, 57, 109, 122, 132, 133 |

| Nepal Rastra Bank Act, 2058 | Sections 74(3), 79, 80, 86Ga(13), 105, 111 |

| Secured Transactions Act, 2063 (2081 Amendment) | Sections 2(v), 2(JhA1), 2(da), 3(1)(Kha), 19, 22, 29Ka, 42(3Ka), 42Ka, 43, 58Ka |

| Securities Act, 2063 | Sections 2(ch), 29(1), 30(2)(Ga), 71-75, 84, 116, 118 |

| Income Tax Act, 2058 | Sections 2(Na), 2(Da), 2(KaNa1), 10(Tha), 35, 44, 57, 76, 87, 88 |

| Value Added Tax Act, 2052 | Schedule 1 |

| Companies Act, 2063 | Sections 11(1), 51(2), 101(1), 176(1) |

| Insolvency Act, 2063 | Sections 19, 20Ka, 31, 53, 57, 59 |

| National Civil (Code) Act (Muluki Civil Code), 2074 | Sections 314, 315, 319, 342, 529 |

| Electricity Regulatory Commission Act, 2074 | Sections 13(1)(Kha) & (Ga), 43 |

| Foreign Investment and Technology Transfer Act (FITTA), 2075 | Sections 2(wyan), 20, 26(1)(Kha) |

| Foreign Exchange (Regulation) Act (FERA), 2019 | Section 10Ga(1) |

| Bank and Financial Institutions Debt Recovery Act, 2058 | Sections 3, 14(7), 25 |

| Public Debt Management Act (PDMA), 2079 | Section 14 |

| Government of Nepal Work Division Rules (Karyavibhajan Niyamavali), 2072 | Schedule 2 |

| Constitution of Nepal, 2072 | Articles 59(6), 110(3)(c), 115 |

NRB Regulations and Directives

| Document | Relevant Provisions |

| NRB Capital Adequacy Framework, 2015 | Section 6.3(e)/6.4(e): Significance of Risk Transfer; Section 3.3(k): Asset sales with recourse |

| NRB Unified Directive No. 2 (Loan Classification, Loss Provisioning, Credit Sale/Purchase) | Credit Sale/Purchase provisions; borrower consent requirements |

| NRB Unified Directive No. 8 (Investment and Subsidiary Companies) | 10% per-entity cap; 30% aggregate cap for non-BFI investments |

| NRB Unified Directive No. 3 (Capital Fund and Capital Adequacy) | SOL provisions; energy sector targets |

| NRB Circular No. 12/081 (March 2026) | Tradable Reporting Rights for energy sector lending |

| NIFRA Unified Directive, 2082 | SPV investment restrictions; credit sale provisions |

| MFI (Class D) Unified Directive, 2082 | Resource mobilization limits |

SEBON Regulations

| Document | Relevant Provisions |

| Specialized Investment Fund Regulation, 2075 | Rules 3(1), 7(1), 14(2-3), 16, 19, 20, 22 |

| Mutual Fund Regulation, 2067 (as amended) | Rules 10, 19-21, 32 |

| Credit Rating Regulation, 2068 | Rules 3, 21, 23, 25, 27 |

| Securities Registration and Issuance Regulation, 2073 | Rules 3(3), 9 |

| Securities Listing and Trading Regulation, 2075 | Rule 3 |

| Central Depository Service Regulation, 2067 | Rules 2(Jha), 2(Tha) |

Market Data Sources

| Document | Key Data Points Used |

| NRB Annual Report 2081/82 | Banking system assets: 201.8%/235.1% of GDP; EPF, CIT, SSF, insurance asset sizes |

| NRB Bank Supervision Department Annual Report 2024 | Total loans NPR 5,871.03 billion; Energy 7.99%; NPL NPR 180.01 billion (3.94%); CAR 12.84% |

| NRB Current Macroeconomic and Financial Situation 2024/25 | Real estate collateral 64.7%; term loan shift |

| Hedging Blueprint (Pricing the Unpriceable) | 12-year hydropower debt regulatory ceiling |

| Nabil Bank Annual Report 2023/24 | ALM mismatch data; energy sector 7.98%; >5yr loan vs deposit gap |

| Standard Chartered Bank Nepal Annual Report 2081/82 | Mortgage average original tenure 21.05 years; remaining 15.83 years |

| Everest Bank Annual Report 2081-82 | Energy Bond maturity 12 years; energy sector 8.50% |