Impossible to chew and digest: too long, didn’t read (TLDR)

In the Fiscal Year 2023/24, Nepal’s banking system held approximately NPR 5,076 billion (roughly USD 36 billion) in total commercial bank credit. Of that, somewhere between NPR 3,000 and 3,400 billion – depending on which reporting period you reference – was secured by land and buildings. That share has fluctuated between 60.8% and 68.0% for an entire decade, peaking at 68.0% in 2023 and still standing at 64.4% as of November 2025. This is not a recent trend. It is a structural constant that has persisted through credit booms, contractions, regulatory reforms, and repeated policy commitments to diversify the collateral base.

The prior post in this series, Land Locked Credit, diagnosed the five structural locks that produce this outcome and documented the economic cost: SME organic credit that has not grown in a decade, a software company with NPR 50 million in annual contracts that cannot access a working capital line from any commercial bank in Nepal, a manufacturing sector whose share of GDP has declined from 15.2% to 12.83% over the same period, and a credit expansion model now in structural exhaustion as remittance growth decouples from private sector credit growth.

Land Locked Credit identified Lock 1 as the non-functional movable asset registry. This article is the companion piece: a complete explanation of what the Secured Transactions Act, 2063 (2006) (hereinafter “the Act” or “STA”) – formally titled सुरक्षित कारोबार ऐन, २०७२ – actually does, how each of its sixty sections works, and what it was designed to achieve.

The Act is not obscure law. It is the legal infrastructure for everything Nepal’s financial system needs to build next: working capital loans against hypothecated inventory, securitization of banking and non-banking receivables, crop finance for landless farmers, share pledges for entrepreneurs without real estate, and the complex structured finance instruments that Nepal’s infrastructure investment pipeline demands. None of those instruments get built while the foundation sits unused.

Part I: Why This Law Exists

1.1 The Problem Before the Act

Before the Secured Transactions Act came into force, Nepal had no unified legal framework for movable asset security. Traditional instruments existed – pledge (dharauti), hypothecation (chal sampati mathiko dhito byabastha), hire purchase – but they operated under fragmented statutory provisions, primarily the Muluki Civil Code and various banking regulations, without a centralised system for establishing who held priority over any given asset.

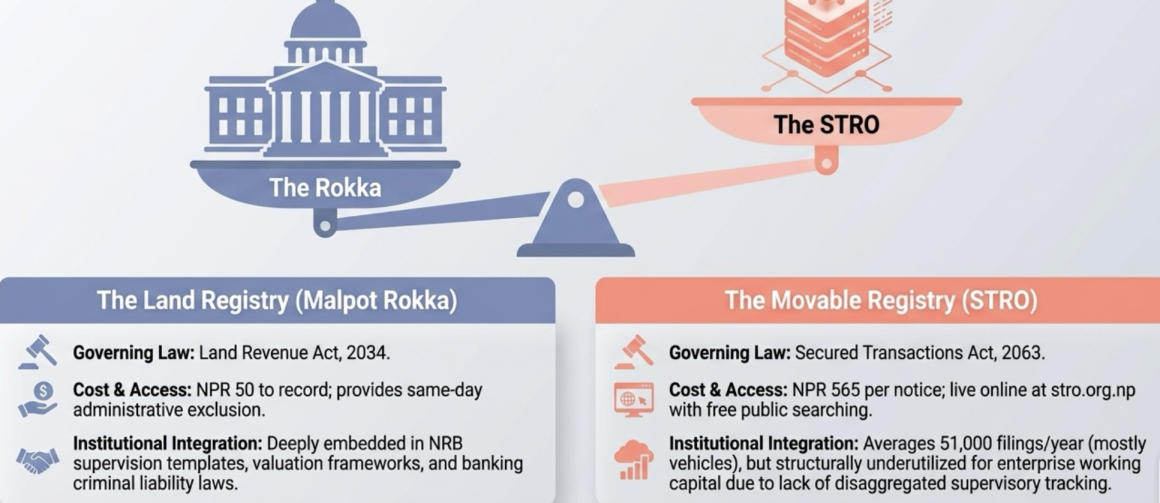

The practical consequence was the problem the NRB Bank Supervision Report 2013 (Section 5.12) captured precisely: “double counting of assets” and “multiple banking against the same security without pari-passu agreements.” A business could hypothecate the same inventory to three different banks simultaneously, and none of the three banks had any reliable means of discovering the others’ claims. The rational institutional response was to demand land – because the Land Revenue Office’s Rokka (रोक्का, the administrative restriction on land transfer recorded under Land Revenue Act, 2034, Section 8kha) provided something no movable asset arrangement could match: a publicly searchable, same-day, administratively enforced record of prior claims. The same NRB finding continues to appear in Bank Supervision Reports through 2024 – eleven years later – for the same reason.

The Secured Transactions Act was the legislative solution to this problem. Its preamble states the purpose plainly: “to promote economic activity to the maximum extent for the country’s economic development” by establishing a unified, integrated legal framework for security interests in movable and intangible property. The Act was major reform to minimize the land concentration in form of credit security by building a registry system for everything that is not land.

1.2 The International Blueprint

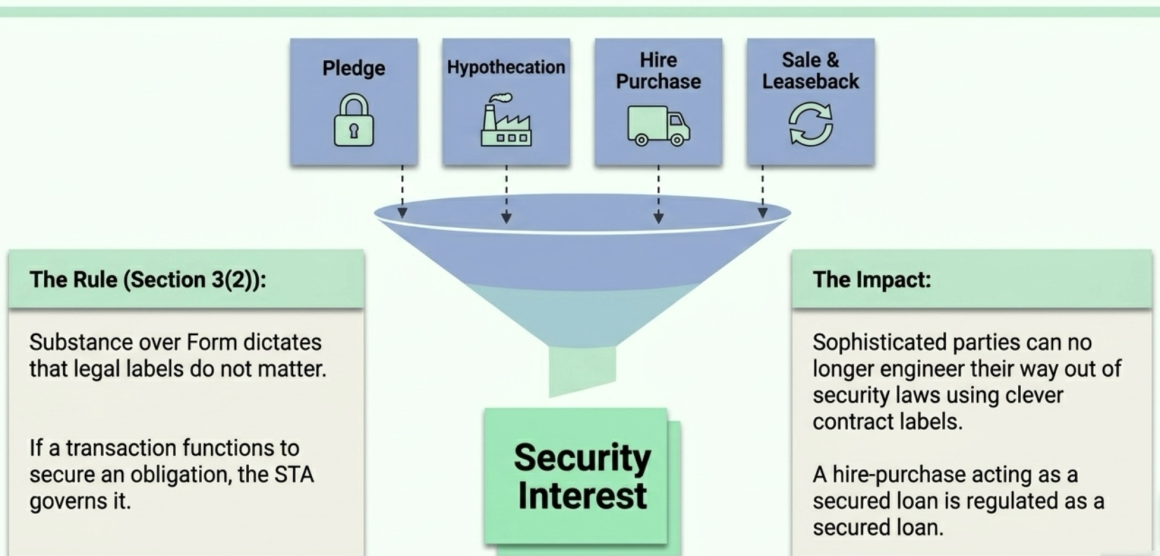

The Act is modelled on the UNCITRAL Legislative Guide on Secured Transactions and draws directly from Article 9 of the American Uniform Commercial Code (UCC) – the most widely replicated commercial law reform in the past century. Both the UNCITRAL model and Article 9 rest on a single foundational innovation: the “functional approach.” Instead of regulating pledges, hypothecations, hire purchases, and conditional sales as separate legal instruments under separate rules, the functional approach treats all transactions that have the substance of creating a security interest in an asset as the same legal thing – a “security interest” – and subjects them to the same registration, priority, and enforcement framework.

The reason this matters is straightforward. Before the functional approach, sophisticated parties could engineer around specific security law provisions by using different transaction labels. Under the functional approach codified in Section 3(2) of Nepal’s Act, the label is irrelevant. What the transaction actually does determines which law governs it. A hire purchase that is functionally a secured loan is regulated as a secured loan. A sale-and-leaseback that is functionally a security arrangement is regulated as a security arrangement. The legal form of the contract cannot override its economic substance.

A temporary precursor, the Secured Transactions Ordinance, 2062 (2005) was enacted first as a stopgap. The Act replaced it permanently. Section 60 of the Act confirms that the Ordinance’s expiry does not revive prior law, does not disturb ongoing matters, and does not affect rights, liabilities, or penalties that accrued while the Ordinance was in force. The transition was designed to be seamless.

Part II: Scope – What the Act Covers and What It Deliberately Does Not

2.1 The Three Transaction Categories

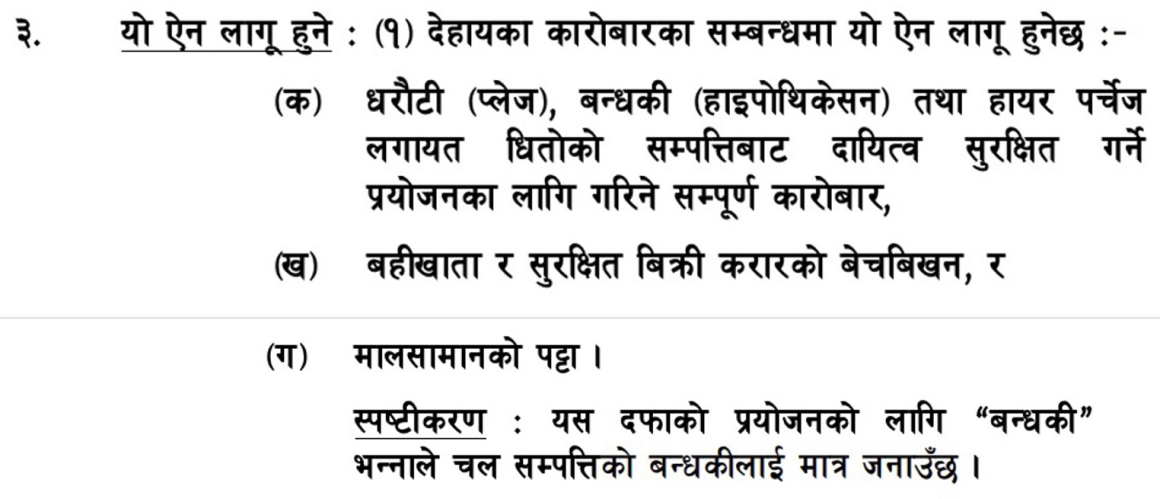

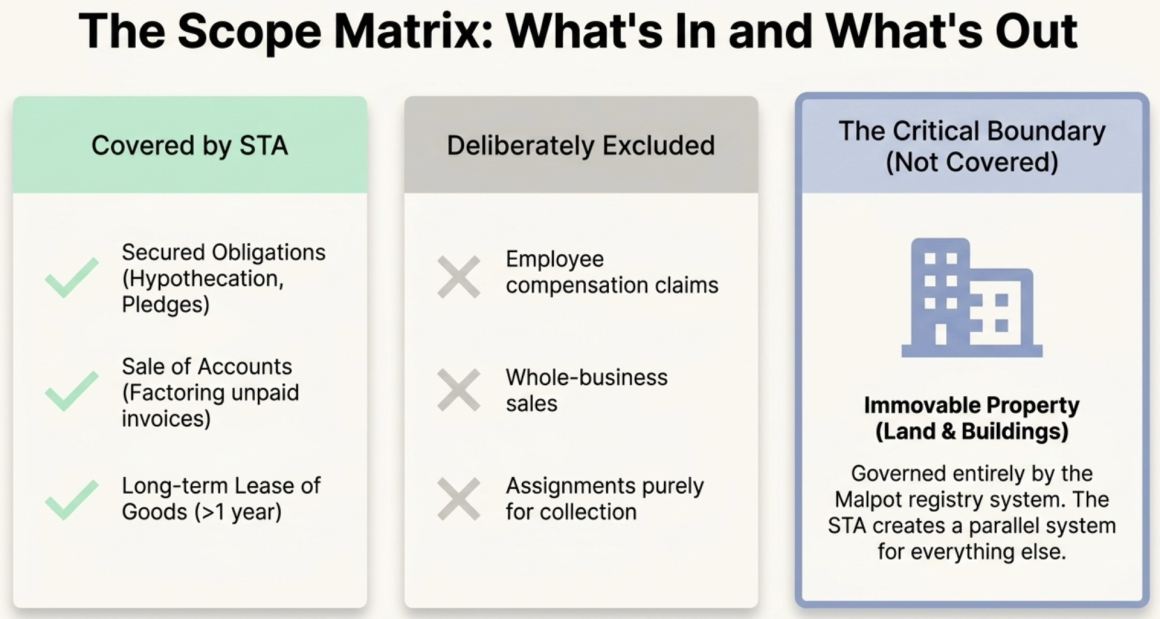

Section 3(1) of the Act establishes its scope by defining three categories of transactions to which it applies. Together, these categories cover virtually every commercial arrangement involving movable assets as security or as tradable financial rights.

Category 1: Secured Obligations – Section 3(1)(ka)

The Act applies to all transactions executed for the purpose of securing an obligation or liability using collateral property. This explicitly encompasses pledge, hypothecation, and hire purchase. The official explanation under Section 3 clarifies a critical boundary: “hypothecation” in the context of this Act means hypothecation of movable property only. Immovable property mortgages remain governed by the Land Revenue Act, 2034 and the National Civil Code, 2074. The Act does not compete with the land registry system – it creates an entirely separate system for everything that is not land.

A pledge, in this context, is the classical arrangement where the borrower physically transfers possession of the collateral to the lender until the debt is repaid. A bank holding gold bars in its vault against a loan, a pawnbroker holding a customer’s jewellery, or a cooperative physically holding share certificates all constitute pledges under this category. Hypothecation differs critically: the borrower retains physical possession of the asset and continues using it, while the lender registers a security interest that gives it enforcement rights on default. A garment factory hypothecating its industrial sewing machines to secure a term loan – where the machines remain on the factory floor and continue producing revenue – is the prototypical hypothecation. Hire purchase adds the dimension of ownership: the financier retains legal title to the asset as security until the final installment is paid, at which point ownership transfers to the buyer.

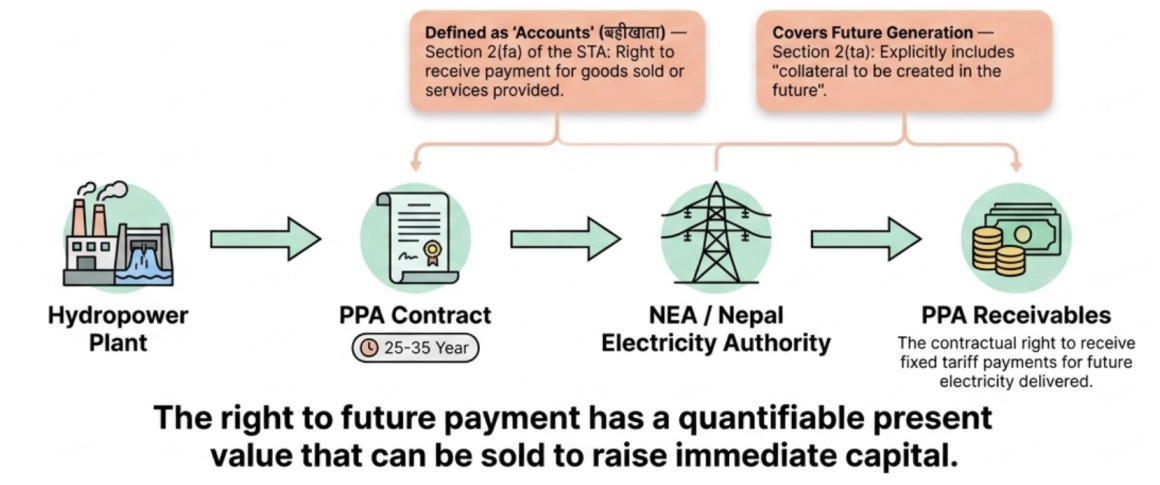

Category 2: Sale of Accounts and Secured Sales Contracts – Section 3(1)(kha)

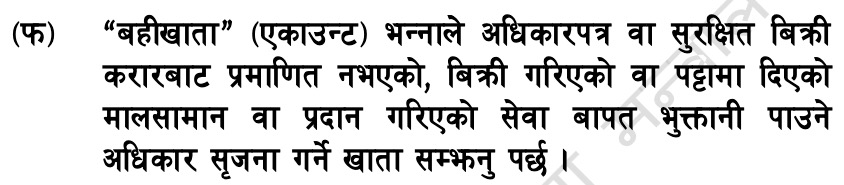

The Act also governs the buying and selling of “accounts” (बहीखाता) and “secured sales contracts” (सुरक्षित बिक्री करार). An account is the right to receive payment created by selling goods, leasing goods, or providing services – essentially, an unpaid invoice. When a wholesale distributor sells its outstanding invoices to a financial factoring company to get immediate cash, that transaction is governed by this Act. A secured sales contract is an agreement that simultaneously creates both a debt obligation and a security interest in the goods being sold. Both categories are included because they are economically similar to secured lending: the “buyer” of accounts or a secured sales contract is in the position of a lender, and the Act’s registration, priority, and enforcement framework needs to apply to protect their investment.

Category 3: Lease of Goods – Section 3(1)(ga)

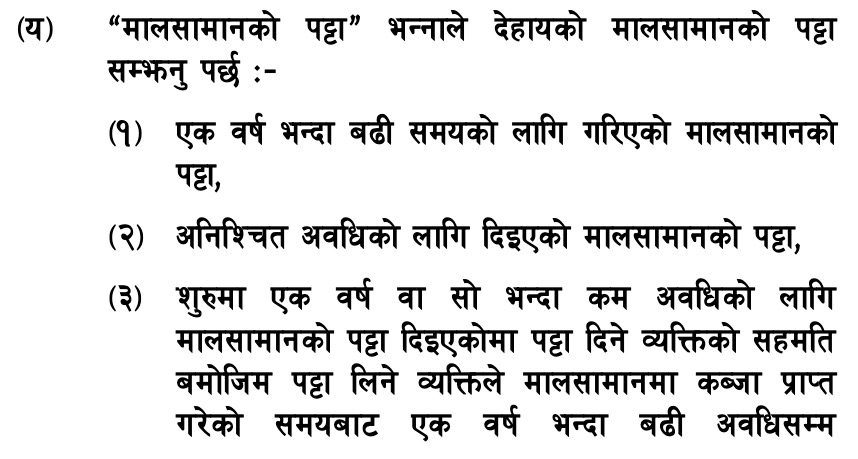

Long-term leases of goods are also governed by the Act. Section 2(ya) defines a “lease of goods” (मालसामानको पट्टा) as covering four scenarios: a lease for more than one year; a lease for an indefinite period; a lease initially for one year or less but where the lessee continuously retains possession for more than a year with the lessor’s consent; and a lease for one year or less but containing a contractual right to renew for a period exceeding one year. A lease that is purely short-term – under one year with no renewal option and where the lessee actually returns the goods within one year – is not a “lease of goods” under the Act and falls outside its scope.

The reason long-term leases are included is the “appearance of ownership” problem. When a hospital leases an MRI machine for three years, the machine sits in the hospital’s premises. To a bank or a judgment creditor looking at the hospital’s assets, that MRI machine appears to belong to the hospital. Without a publicly registered notice, the leasing company that actually owns the machine has no protection against the hospital’s creditors claiming it. The Act requires the leasing company to register its interest, making the true ownership visible to anyone who searches the registry before lending against it.

2.2 The Substance Over Form Principle – Section 3(2)

Section 3(2) is perhaps the most important single provision in the entire Act. It states that the Act applies to all transactions listed in Section 3(1) regardless of whatever terms the parties have written in their agreement, and regardless of whether ownership of the collateral property rests with the security holder or the security giver. This is the functional approach in direct statutory form: parties cannot contract out of the Act by labelling a security arrangement as something else.

A hire-purchase agreement where the financier “owns” the vehicle until the final installment is still governed by the Act, because the substance of the transaction is using the vehicle as security for a financing obligation. A sale-and-leaseback arrangement where a business “sells” its machinery to a financier and then “leases” it back is still governed by the Act if the economic substance is a secured loan. A lease that contains a bargain purchase option – allowing the lessee to buy at a nominal price at the end of the term – is likely a disguised hire-purchase and falls under Category 1 despite being labelled a “lease.”

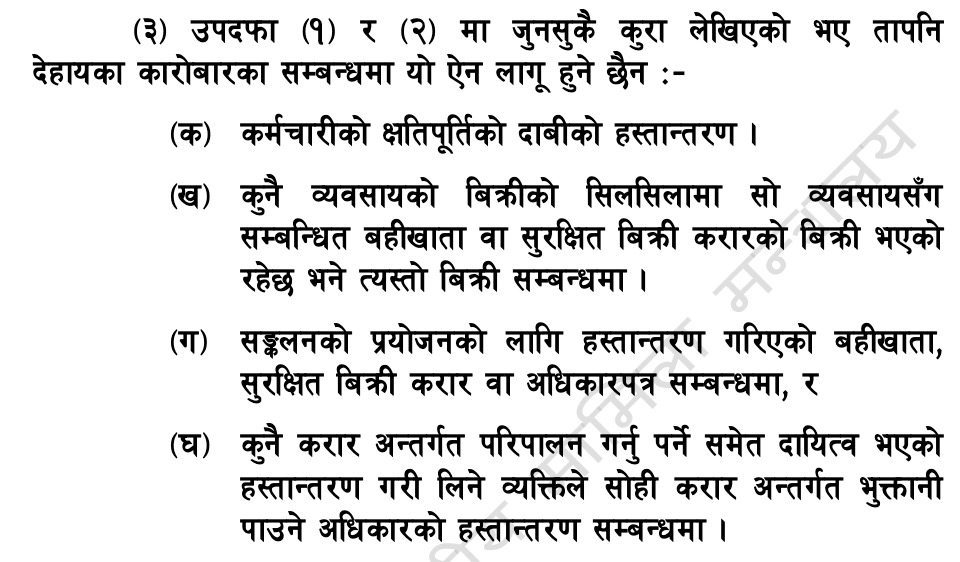

2.3 What the Act Deliberately Excludes – Section 3(3)

Section 3(3) carves out four specific transaction types from the Act’s scope, for reasons that reflect deliberate policy choices rather than technical omissions.

- Section 3(3)(ka): Transfer of employee compensation claims. Workers’ rights to wages, injury compensation, or severance are too fundamental to expose to commercial security arrangements. A worker cannot use their own compensation claim as collateral for a moneylender’s loan, and the Act ensures this.

- Section 3(3)(kha): Sale of accounts as part of a whole-business sale. When an entrepreneur sells an entire business, the outstanding invoices transfer as ordinary business assets to the new owner – not as a financing mechanism. Requiring individual STRO registration of every invoice in a corporate acquisition would create administrative paralysis for no meaningful purpose.

- Section 3(3)(ga): Assignments made purely for collection purposes. When a hospital transfers its overdue patient bills to a collection agency specifically so the agency can recover them on the hospital’s behalf – not to raise immediate financing – no security arrangement has been created. The collection agency is providing a service, not investing capital.

- Section 3(3)(gha): Assignment where the assignee also takes on the obligation to perform the contract. When a construction firm assigns both the right to be paid for completing a building project AND the obligation to actually complete the work to another contractor, this is a contractual substitution, not a financial security arrangement. The new party steps into the original contractor’s shoes entirely.

2.4 The Critical Boundary: What the Act Does Not Cover

The Act does not cover immovable property. Land and buildings remain governed by the Land Revenue Act, 2034, the Lands Act, 2021, and the National Civil Code, 2074. This is not an oversight – it is a deliberate architectural choice. Nepal’s land registry system (मालपोत) predates the Act by decades and operates through a well-established institutional infrastructure. The Act was designed to create an equivalent system for everything that is not land, not to displace the land registry.

The practical consequence of this boundary, as documented in the AMC article, is that Nepal has no equivalent of India’s SARFAESI Act – no statutory mechanism for a creditor to bypass judicial procedures and take possession of immovable collateral on default. The STA provides powerful enforcement tools (examined in Part VIII) but only for movable assets. For immovable collateral – which constitutes 64.4% of all BFI credit – enforcement still depends on the court system and the Land Revenue enforcement process, with all the delays that implies.

| Transaction Type | Category Under Act | Governing Section | STRO Registration Required? |

| Pledge of physical gold to cooperative | Secured Obligation | 3(1)(ka), 2(tha) | Optional if taking possession (Section 26(4)) |

| Hypothecation of factory machinery to bank | Secured Obligation | 3(1)(ka) | Yes – Section 26(2) |

| Hire purchase of delivery truck | Secured Obligation | 3(1)(ka) | Yes – Section 26(2) Optional if taking possession (Section 26(4)) |

| Sale of unpaid invoices to factoring company | Sale of Accounts | 3(1)(kha) | Yes – Section 26(2) |

| Three-year lease of MRI machine to hospital | Lease of Goods | 3(1)(ga) | Yes – Section 26(2) |

| Six-month equipment rental (no renewal option) | Not covered as lease | Not applicable | N/A |

| Transfer of employee injury compensation claim | Excluded | 3(3)(ka) | Not applicable |

| Land mortgage to bank | NOT COVERED by Act | Land Revenue Act, 2034 | Land Revenue Office (Malpot) |

Part III: The Cast of Characters – Key Definitions Under Section 2

The Act defines its terms with deliberate precision. Understanding these definitions is not an exercise in legal formalism – it is the foundation for understanding how the Act allocates rights, obligations, and priorities in every real-world transaction. What follows is an explanation of each major defined term under Section 2, with Nepal-specific examples.

3.1 The Core Parties

The Security Holder (धितो लिने व्यक्ति) – Section 2(dha)

The security holder is the person who acquires a security interest under a security agreement. This is the lender, the creditor, or the seller in whose favour the security interest is created. The definition is deliberately broad: it includes not only banks that make loans, but also the purchaser of accounts (a factoring company that buys invoices) and the lessor of goods under a long-term lease (a company that leases equipment for more than one year). In each case, the security holder holds a property right over the collateral that gives it priority over other creditors and enforcement rights on default.

Example: Everest Bank Limited lends NPR 50 million to a Kathmandu-based printing company secured by the company’s two offset printing machines. The bank is the security holder. Separately, a financial factoring firm buys NPR 20 million in outstanding invoices from a wholesale garment distributor. The factoring firm is also a security holder under the Act – its purchased accounts are the collateral, and it is in the same legal position as the bank with respect to those financial rights.

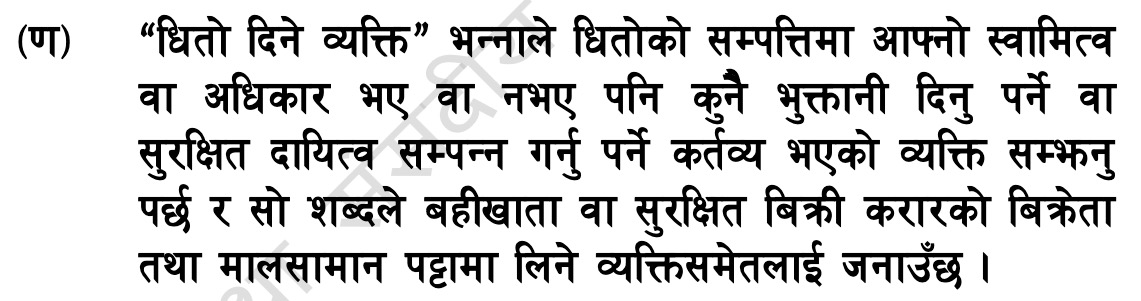

The Security Giver (धितो दिने व्यक्ति) – Section 2(na)

The security giver is the person who has a duty to make a payment or fulfil a secured obligation. The Act makes a critical clarification: the security giver need not own the collateral. They only need to have rights over it or the power to transfer those rights to the security holder. This means a lessee can pledge their leasehold interest, a consignee can pledge goods held on consignment, and a business that does not technically own its equipment under a hire-purchase arrangement is still the security giver – because it bears the obligation the security interest secures.

Example: A logistics company acquires a refrigerated truck under a three-year hire-purchase arrangement with a vehicle financing firm. The financing firm legally owns the truck until the final installment is paid. The logistics company has no legal title. Yet under the Act, the logistics company is the security giver – it is the party that owes the payment obligation that the truck secures. The Act does not care who holds the ownership certificate; it cares who carries the debt.

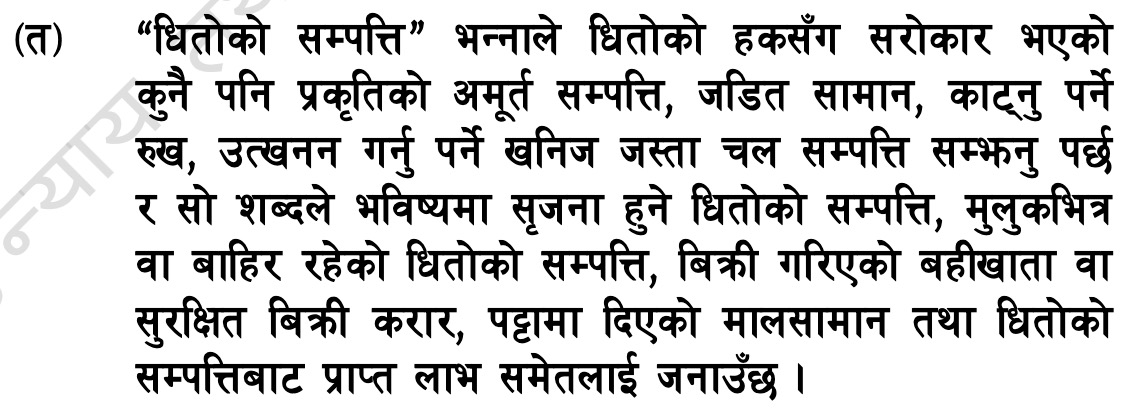

Collateral (धितोको सम्पत्ति) – Section 2(ta)

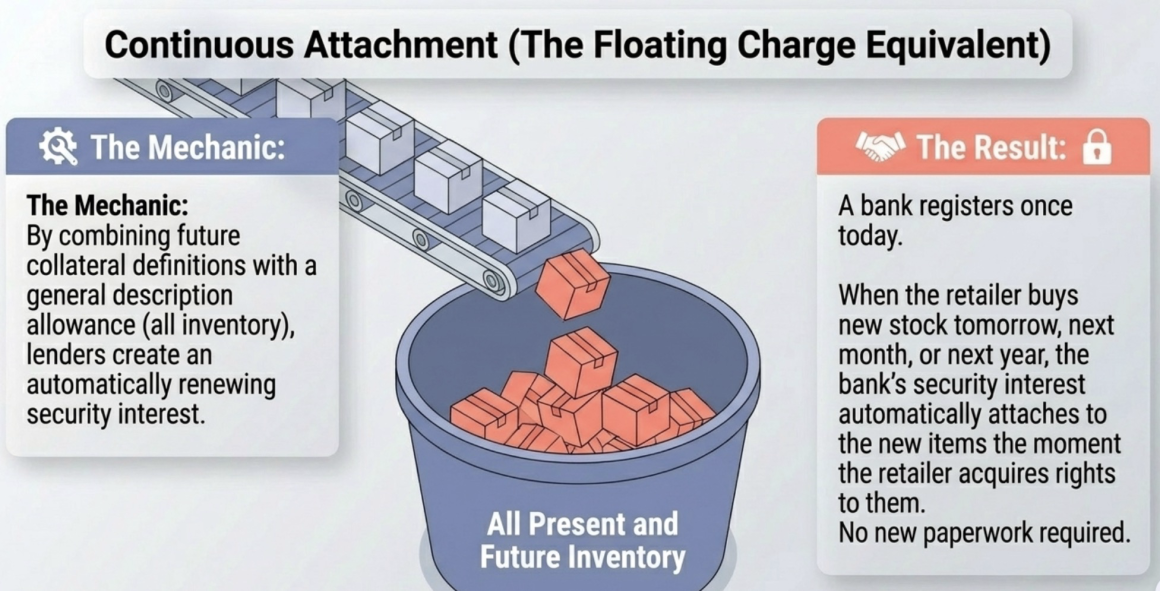

Collateral means any movable or intangible property of any nature that is subject to a security interest. The definition is deliberately expansive. It covers physical goods (machinery, inventory, livestock, vehicles), intangible property (accounts receivable, intellectual property, goodwill, digital rights), instruments (share certificates, bonds, bills of lading), and documents (warehouse receipts, delivery orders). Crucially, it also covers future collateral – assets that do not exist yet at the time the security agreement is signed. And it covers offshore collateral – property physically located outside Nepal.

The explicit inclusion of future collateral is what makes the Act functionally equivalent to a floating charge: a business can grant a security interest in “all present and future inventory” today, and the security interest automatically attaches to every new item of inventory the business acquires in the future, from the moment it acquires rights to that item. This is examined in detail in Part V.

Security Interest (धितोको हक) – Section 2(da)

A security interest is a property right in collateral created to secure the performance or payment of an obligation. It is the actual legal claim that gives the creditor power over the asset if the debtor defaults. The security interest is distinct from the debt itself: the debt is the obligation to pay; the security interest is the right to seize and sell the collateral if the debt is not paid. Without a security interest, a creditor is unsecured and must queue behind all other creditors in enforcement. With a perfected security interest, the creditor has a legally recognised priority claim that can be enforced against the specific asset, regardless of what else happens to the debtor’s financial position.

Security Agreement (धितो सम्बन्धी समझौता) – Section 2(tha) and Section 23

A security agreement is the foundational contract that creates or provides for a security interest. Under Section 23(1), it must be in record form – written or electronic documentation. It can consist of one document or multiple documents taken together.

The security agreement does not need to be a standalone document labelled “security agreement” – a loan deed that describes the collateral and grants the bank enforcement rights is a security agreement. Under Section 23(2), the terms of the security agreement are binding not only on the original parties but also on transferees of the collateral, creditors of the security giver, and lien holders.

Obligor (दायित्व वहन गर्ने व्यक्ति) – Section 2(dha-2)

The obligor is the person who has the duty to fulfil an obligation on an account, a secured sales contract, or other intangible property. In accounts receivable transactions, the obligor is the underlying customer who owes the money: not the business that created the invoice, and not the factoring company that purchased it, but the third party whose payment obligation is the economic substance of the account. When the factoring company needs to collect, it collects from the obligor.

Example: A wholesale garment manufacturer sells NPR 1 million in outstanding invoices to a factoring company. Those invoices are for delivery to three retail chains. The manufacturer is the security giver; the factoring company is the security holder; and each retail chain is an obligor – because they are the parties who ultimately owe the money that makes the accounts valuable.

3.2 Property Type Definitions

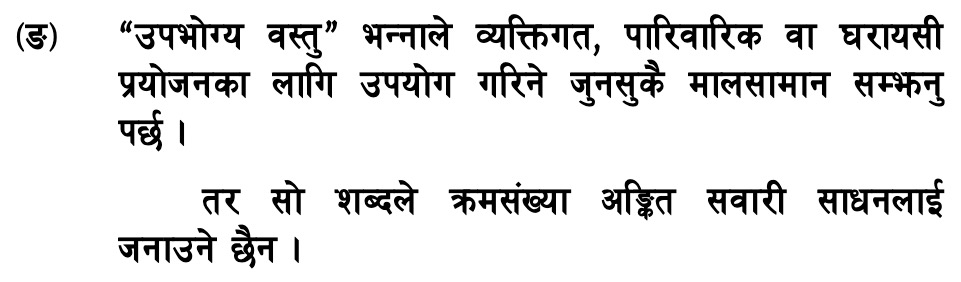

Consumer Goods (उपभोग्य वस्तु) – Section 2(nga)

Consumer goods are any goods used or intended to be used for personal, family, or household purposes. The Act explicitly excludes serial-numbered vehicles from this category. The classification depends entirely on how the item is used – not on what it physically is. A refrigerator in a family kitchen is a consumer good. The identical refrigerator in a supermarket’s storage area is equipment or inventory. A washing machine at home is a consumer good. The same machine in a commercial laundry operation is equipment.

This distinction matters greatly for two reasons. First, Section 20(2) prohibits creating a standard security interest over consumer goods – only a Purchase Money Security Interest (PMSI) is permitted. This protects families from lenders taking general floating charges over all their household possessions. Second, as examined in Part VI, PMSIs in consumer goods perfect automatically on attachment without any registry filing – creating an invisible lien that a lender searching the STRO cannot detect.

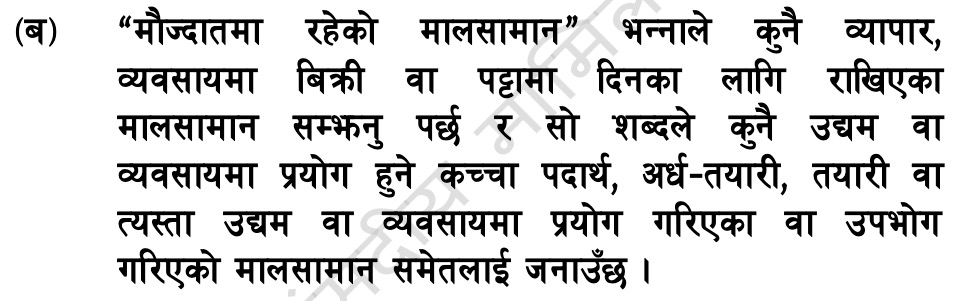

Inventory (मौज्दातमा रहेको मालसामान) – Section 2(ba)

Inventory is goods held for sale or lease in a trade or business. The definition also covers raw materials, semi-processed goods, finished goods, and materials that are consumed in the course of a business. For a furniture manufacturer, inventory includes the raw timber, the half-built chairs, the completed dining sets ready for sale, and the sandpaper and varnish used in production. For a wholesale pharmaceutical distributor, inventory is the medicines held in the warehouse awaiting distribution. For a vehicle dealer, the cars in the showroom and the spare parts in the back are inventory – but the dealer’s own delivery van used to transport those cars is equipment.

Equipment (उपकरण) – Section 2(cha)

Equipment is a residual category: goods that are neither farm products, inventory, nor consumer goods. Any commercial asset used in operating a business that is not held for sale falls here. A printing press’s offset printing machines, a hospital’s MRI scanner, a restaurant’s commercial kitchen equipment, a hotel’s elevator system – all equipment. The significance of this category emerges in priority disputes: a Purchase Money Security Interest in equipment earns super-priority with a simpler procedural requirement than the equivalent PMSI in inventory.

Farm Products (कृषिजन्य उत्पादन) – Section 2(ja)

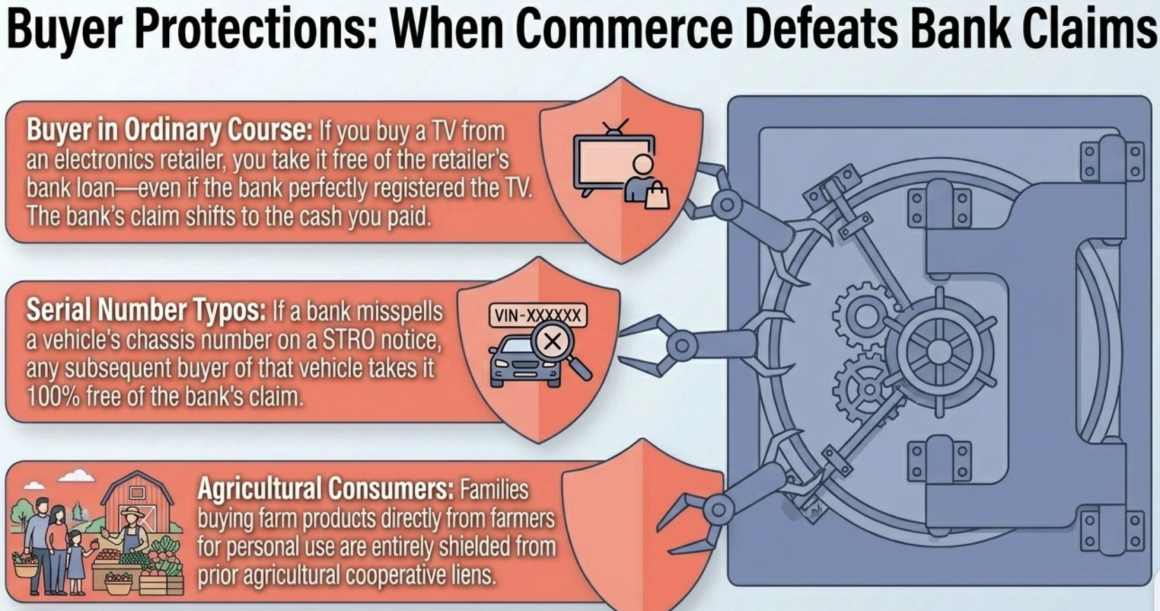

Farm products are goods belonging to a person engaged in farming, excluding uncut trees. The definition covers: growing, growing up, or future crops; aquatic animals; domesticated livestock including unborn animals; goods used in farming or produced from farming; and unprocessed products derived from crops or livestock. A poultry farmer’s flock of chickens – including the eggs not yet hatched – and the chicken feed in the barn are farm products. The significance of this category is discussed in Part VII: a security interest in crops can take priority over the rights of the landowner or the mortgagee of the land on which those crops grow.

Serial Numbered Vehicle (क्रमसंख्या अंकित सवारी साधन) – Section 2(chha)

Serial numbered vehicles are motor vehicles (cars, trucks, motorcycles), trailers, aircraft, and motorised boats – but only when they are not held as inventory by the security giver. A delivery van in a logistics company’s fleet is a serial numbered vehicle. Twenty new cars on a dealer’s lot awaiting sale are inventory, not serial numbered vehicles. This distinction affects both how the security interest must be described in a STRO filing (specific serial/chassis number required for vehicles) and which buyer protections apply (examined in Part VII).

Fixtures (जडित सामान) – Section 2(nja)

Fixtures are movable goods that are attached – or intended to be attached – to immovable property in a manner that creates property rights under prevailing real estate law. The Act explicitly excludes easily removable factory machines, office machines, and household appliances from this category. A permanent central air-conditioning system built into the walls and ceiling of a commercial building is a fixture. A standard window air-conditioning unit that can be unscrewed and removed in an afternoon is not. Fixtures occupy the boundary between the STA’s movable property framework and the immovable property regime, and the Act has specific priority rules for this boundary – examined in Part VII.

Purchase Money Security Interest (PMSI) (खरिद मूल्य सम्बन्धी धितोको हक) – Section 2(jha)

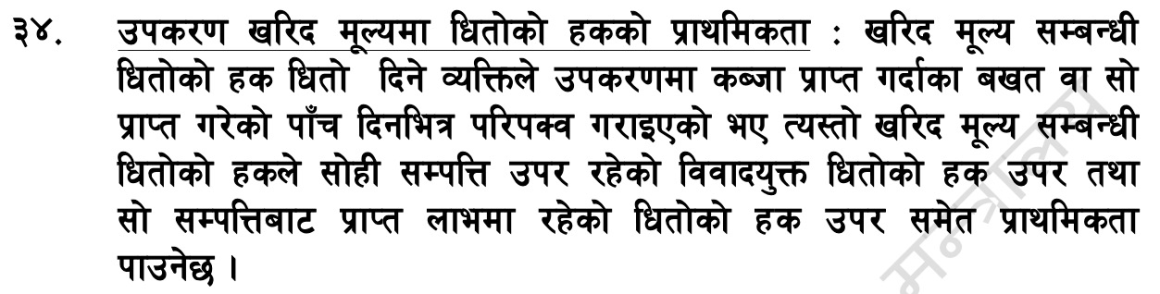

A PMSI is a security interest where the collateral itself is what the financing was used to acquire. It arises in two scenarios: when a seller retains a security interest in goods sold to secure the payment of the purchase price, or when a financier (not the seller) provides the funds specifically to enable the buyer to acquire the goods and takes a security interest in those exact goods, with the funds actually used for the stated purpose. This “superpriority” interest allows the PMSI holder to leap ahead of a prior lender who holds a general “all assets” charge, under specific conditions examined in Part VII.

Example: A bakery wants to buy a commercial oven costing NPR 1.5 million but lacks cash. A bank pays the equipment supplier directly and takes a security interest in that specific oven. The bank holds a PMSI over the oven – even if a different bank already holds a general charge over all the bakery’s equipment.

Proceeds (लाभ) – Section 2(sha)

Proceeds are anything acquired from dealing with the collateral. The Act’s definition is deliberately comprehensive: proceeds include anything received from the sale, lease, exchange, or transfer of the collateral; collections and distributions from the collateral; rights created out of the collateral; claims for loss or damage to the collateral; and insurance payouts resulting from loss, damage, or breach of conditions relating to the collateral. When a wholesale distributor pledges its inventory of laptops to a bank and then sells ten of those laptops for cash, that cash is proceeds. When the remainder of the inventory is destroyed in a fire, the insurance payout is also proceeds. The bank’s security interest automatically extends to both – without any new filing required.

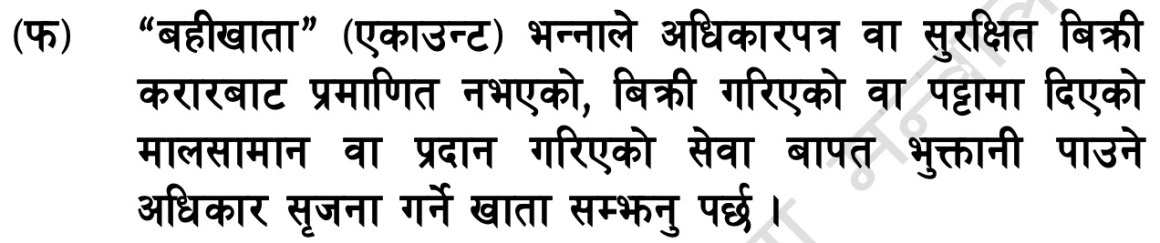

| Other Important Definitions Goods – Section 2(ma) covers all physically movable objects at the time of attachment, explicitly including fixtures, timber to be cut, and agricultural products. The exclusion of accounts, currency, documents, and instruments is deliberate: each of those is a separately defined category with its own rules. A distributor pledging warehouse stock is pledging goods; the same distributor pledging the unpaid invoices from that stock’s sale is pledging accounts. Same commercial transaction, different legal category, different treatment.  Instruments – Section 2(kha) are documents or share certificates transferable by endorsement or delivery that prove a cash payment right. The Act explicitly excludes collateral agreements and lease agreements from this definition – because instruments circulate freely in the market as quasi-currency, while a collateral or lease agreement is a bilateral contract bound to specific parties and obligations that cannot be detached and traded. A bearer bond is an instrument; the loan deed in which a company pledges its machinery is not. Instruments perfect by possession under Section 26(4), not by STRO filing.  Documents- Section 2(wa) prove a right to possess goods rather than a right to receive cash. A warehouse receipt is the principal example: the holder presents it to take delivery of stored physical goods. Perfecting a security interest in the underlying goods requires first perfecting in the document itself under Section 26(8) – which is why a bank holding a warehouse receipt has, in a single act, perfected its interest in whatever commodity that receipt represents.  Intangible property is the residual category: any movable property creating a legal right that falls outside goods, accounts, secured sales agreements, documents, instruments, and currency. What this leaves inside the definition is commercially significant – trademarks, patents, software licences, franchise rights, concession rights. A technology company whose assets are primarily intellectual property and software can pledge them under this category, perfecting at the STRO under Section 26(2). An IFRIC 12 concession right – a private operator’s contractual right to charge users for operating public-service infrastructure – fits here: it is a movable legal right of economic value, non-physical, and excluded from none of the Act’s explicit carve-outs. A hydropower developer pledging its government concession to secure a project finance loan is pledging intangible property under the Act.  Lien holder – Section 2(la) is a person who acquires rights over collateral through legal compulsion rather than a consensual security agreement – specifically through a court order, an authorised official acting under law, or an insolvency practitioner under the Insolvency Act, 2063. The priority rule in Section 29 is unambiguous: a perfected security interest always defeats a lien holder unless the lien holder both filed before the security interest was perfected and before any STRO notice was filed. A bank with a registered STRO notice has priority over any subsequent court attachment order against the same collateral.  Transfer – Section 2(Gyan) under the Act means the full or partial movement of payment rights – specifically rights to receive cash embedded in an account, secured sales agreement, instrument, or document – from transferor to transferee. This narrow definition is precisely what makes factoring and receivables securitization work under the Act: the transfer of invoice payment rights from a seller to a factoring company is a transfer in this legal sense, and Section 43’s anti-assignment rule makes any contractual restriction on that transfer unenforceable against the buyer.  |

Part IV: The Registry – Nepal’s Public Warning System

The Secured Transactions Registration Office (STRO) (सुरक्षित कारोबार दर्ता कार्यालय) is the institutional centrepiece of the Act. Everything the Act promises – publicly verifiable priority, searchable prior claims, a functioning collateral market – depends on the registry working as designed. Part IV explains how the registry is structured, how each type of filing works, and what has happened in practice over the eight years since the STRO went live.

4.1 Establishment and Administration – Sections 4–5

Section 4(1) mandates the Government of Nepal to formally establish a dedicated registration office named the Secured Transactions Registration Office. Section 4(2) provides a practical interim measure: until the permanent office is established, the government may designate any existing government office to act in its place. Section 4(3) requires that the office be headed by a Registrar who must hold at least the rank of a Gazetted Class-2 officer (Under-Secretary level) or equivalent.

Section 5(2) contains a provision that determined how the STRO actually came to operate: the government may contract a private entity to run the electronic registry, provided that entity has adequate financial, technical, and human resources and can maintain the system to appropriate commercial standards. In practice, the contract was awarded to Karja Suchana Kendra Limited (KSKL), a company operating the registry at stro.org.np under Ministry of Finance oversight. The STRO went live in May 2017 – eleven years after the Act was enacted. The registry provides free public search with no login required, client account access for BFI filers, online notice-filing for all notice types, priority dating from filing timestamp, and a flat filing fee of NPR 500 per notice.

Section 5(1) establishes the STRO’s three core duties: operate and maintain an electronic registry; provide public search access to all registered notices; and publish an annual report within six months of each fiscal year end. Section 6 makes the public access obligation explicit: all registered notices, catalogue entries, and other records maintained by the STRO are public documents, and every person has the right to inspect and obtain copies.

4.2 The Initial Notice – Section 7

An initial notice (प्रारम्भिक सूचना) is the foundational filing that creates a public record of a security interest. Section 7(1) specifies the minimum content: the name, address, and other particulars of the security giver; the name, address, and other particulars of the security holder or their representative; and a description of the collateral. Where the collateral includes timber to be cut, minerals to be extracted, or fixtures attached to real estate, the notice must also describe the relevant immovable property.

Section 7(2) provides that the notice can be filed by the security giver or any person authorised by the security giver on their behalf. The written authorisation instrument itself does not need to be physically attached to the notice. Section 7(3) goes further: once the security giver has signed a security agreement, they are legally deemed to have authorised the filing of any initial notice, amendment, or continuation covering the collateral described in that agreement – regardless of whether the agreement explicitly says so. The bank or factoring company can file on the debtor’s behalf from the moment the security agreement is signed, without needing additional paperwork.

Two further provisions give initial notices unusual flexibility. Section 7(4) allows a notice to be filed before the security agreement is signed or before the security interest has attached to the collateral. A lender can “reserve its place in the priority queue” by filing a notice in advance of closing the loan, locking in an early priority date even if the transaction takes weeks to document. Section 7(5) provides that even an incomplete notice – missing some required content – is legally effective if it substantially complies with the Act’s requirements and is not seriously misleading.

4.3 Name Sufficiency – Section 8

Because the STRO is a searchable database, the name of the security giver must be recorded with enough precision to return accurate results when searched. Section 8(1) prescribes what constitutes a “sufficient” name for each category of security giver:

- Nepali individual: the citizenship certificate number from the Nepali citizenship certificate.

- Foreign individual: the name exactly as it appears on the passport, plus the passport number and the name of the issuing country.

- Nepali body corporate: the legally registered name and the registration certificate number.

- Foreign company authorised to operate in Nepal: the name as recognised under Nepali law.

- Foreign company not registered in Nepal: the name as recognised under the laws of its home country.

Section 8(2) makes a critical negative rule explicit: a notice that lists only a trade name (व्यापारिक नाम) – a shop’s operating name, a branded identity, a “doing business as” name – without the underlying legal identifier does NOT constitute a sufficient name. A notice filed against “Himalayan Bakery” without the owner’s citizenship number or the company’s registration number is legally deficient. This is not a technical nicety – it is what makes the database searchable. If a subsequent creditor searches for “Ram Bahadur Thapa, Citizenship No. 12345,” they will find the prior notice. If the prior notice was filed under “Ram’s Bakery,” it will not appear.

4.4 How Names and Collateral Change Over Time – Section 9

The Act recognises that the world changes after a notice is filed. Two important rules govern what happens to the notice when the underlying facts change.

Section 9(1): If the security giver sells, exchanges, leases, or otherwise transfers the collateral, the notice remains valid and effective against the transferee – even if the security giver knew about or consented to the transfer. A bank’s notice over a printing company’s machines does not evaporate when those machines are sold to another business. The bank’s security interest follows the asset.

Practical Example: Scenario: “Kathmandu Printers Pvt. Ltd.” takes a 5 million Rupee loan from Bank A, pledging a heavy offset printing press as collateral. Bank A registers this security interest. Two years later, Kathmandu Printers secretly sells the printing press to a rival business, “Lalitpur Press,” for cash. Application: Under Section 9(1), Bank A’s registered notice remains 100% valid and legally effective against Lalitpur Press. The bank’s security interest “attached” to the machine itself. Therefore, if Kathmandu Printers defaults on its loan, Bank A has the absolute legal right to seize the printing press directly from the factory floor of Lalitpur Press, even though Lalitpur Press paid for it. Lalitpur Press would then have to sue Kathmandu Printers for the loss, but they cannot defeat the bank’s property right.

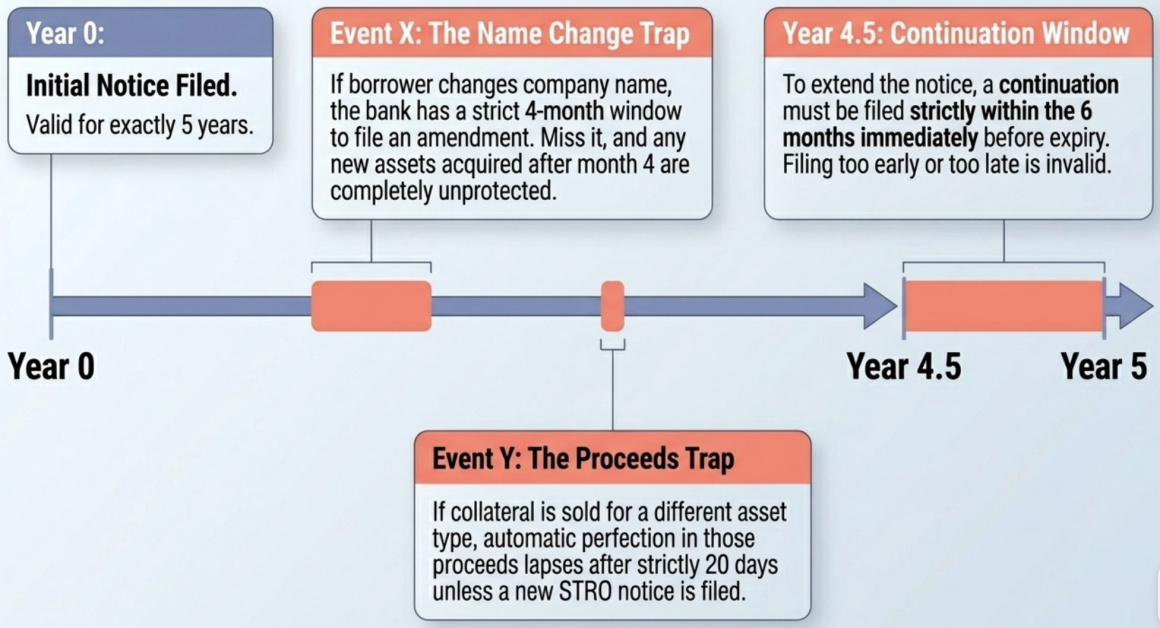

Section 9(2): If the security giver changes their legal name in a way that makes the existing notice “seriously misleading,” the notice remains valid for collateral acquired before the name change and for collateral acquired within four months after the name change. But for collateral acquired after those four months, the notice only continues to protect the security holder if an amendment correcting the name is filed within that same four-month window. This creates a critical deadline for revolving credit facilities: if a corporate borrower changes its registered name and the bank misses the four-month correction window, any inventory or receivables the debtor acquires after that window is unprotected by the original notice. The amendment filed in Month 6 only establishes perfection from the date of amendment – leaving a gap in Month 5 during which any competing creditor who registers a claim will beat the bank to that specific collateral.

Practical Example: Scenario: “Himalayan Tech Pvt. Ltd.” has a revolving credit facility with Bank B, secured by a general description of “all present and future inventory.” Bank B successfully registers the notice. On January 1, the company officially changes its registered name at the Company Registrar to “Everest Electronics Pvt. Ltd.” Because searches are name-based, this change is seriously misleading.

Application:

- The 4-Month Grace Period: Bank B’s original notice perfectly protects all inventory the company owned before January 1, plus any new inventory the company purchases between January 1 and April 30 (the 4-month window).

- The “Gap” Month 5: Bank B’s compliance team is careless and forgets to file a name-change amendment by the April 30 deadline. In May (Month 5), Everest Electronics purchases a brand-new shipment of 500 laptops. Because the 4-month window has closed, Bank B’s original notice is legally blind to these new laptops; their security interest over this specific batch is instantly unperfected upon acquisition.

- The Consequence: During that same month of May, the company goes to a local financial cooperative, pledges those 500 laptops, and the cooperative registers a new notice under the new name “Everest Electronics.” In June (Month 6), Bank B finally realizes its mistake and files the amendment correcting the name. However, because an amendment adding collateral is only valid from the date it is filed, Bank B is permanently subordinated. If the company defaults, the cooperative gets first priority over the 500 laptops, and Bank B loses millions in collateral value due to missing the statutory window.

4.5 The Notice Lifecycle – Sections 10, 12–15

Every initial notice has a defined lifecycle from filing through termination. Understanding this lifecycle is essential for any lender relying on a registered security interest.

| Stage | Section | Filing Fee | Effective Period | Key Rule |

| Initial Notice filed | 7, 15 | NPR 500 | 5 years from filing date | Minimum content: security giver name, security holder name, collateral description |

| Amendment filed | 12 | NPR 500 | Does not extend validity period | Added collateral effective only from amendment date, not original notice date |

| Continuation filed | 13 | NPR 500 | +5 years from original expiry date | Must be filed within 6 months immediately before expiry; late filing is invalid |

| Termination filed | 14 | NPR 500 | Extinguishes notice immediately | Mandatory within 20 days when all secured obligations are discharged |

| Correction filed | 16 | NPR 500 | No effect on notice validity | Flags disputed/erroneous entry; does not amend legal effectiveness of notice |

| Notice lapses (no continuation) | 10(2) | N/A | Interest becomes unperfected | Any value-paying purchaser after lapse takes free of the security interest |

Continuation – Section 13

A notice is valid for exactly five years from the date of filing – Section 10(1). If the underlying debt has not been repaid within that period, the security holder must file a continuation statement (निरन्तरताको विवरण) to extend it. Section 13(2) prescribes a strict window: the continuation must be filed within the six months immediately before the five-year expiry. A continuation filed too early – more than six months before expiry – is not valid for this purpose. Section 13(3) confirms that a timely continuation extends the notice for another five years from the original expiry date, not from the date of filing, ensuring seamless continuity with no gap in the priority position.

Amendment – Section 12

An amendment to an initial notice must cite the original notice’s registration number, identify the authorising security holder, and clearly state what is being changed. Section 12(6) establishes the most important rule for revolving facilities: if an amendment adds new collateral to the covered description, that expanded coverage is effective only from the date the amendment is filed – not backdated to the original notice. A bank that amends its notice in Year 3 to add a new category of assets to its collateral description holds Year-3 priority over those assets, not Year-0 priority. Competing creditors who registered between Year 0 and Year 3 against those specific assets will have priority. Section 12(10) confirms that filing an amendment does not extend the validity period of the original notice.

Example: If “Bank A” registers an initial notice in 2020 for a company’s “excavators” (which is legally valid for 5 years until 2025) and a competing “Bank B” registers a notice for the same company’s “bulldozers” in 2022, Bank A cannot jump ahead in line by simply altering its old paperwork. If Bank A amends its original 2020 notice in 2023 to newly add “bulldozers” to its collateral description, Section 12(6) of the Act dictates that Bank A’s priority over those bulldozers is legally valid only from the exact date of that 2023 amendment, meaning Bank B’s 2022 claim retains absolute first priority over the bulldozers. Meaning, the competing creditor wins: if the construction company defaults, the local cooperative will have absolute first priority over the bulldozers. Because the cooperative perfected its interest in the bulldozers in Year 2, it legally beats Bank A’s Year 3 amendment. (Bank A, however, still retains its top priority over the excavators dating back to Year 0). Furthermore, under Section 12(10), the mere act of filing this 2023 amendment does not reset or extend the original notice’s lifespan; Bank A’s entire notice will still automatically expire in 2025.

Termination – Section 14

When the secured debt is fully repaid and the security holder has no further commitment to advance credit, the security holder must file a termination statement (सूचनाको समाप्ति) within twenty days of receiving a written demand from the security giver – Section 14(2). The security giver can demand termination where: all secured obligations have been paid and no future advance commitment exists; the security giver never authorised the initial notice; or, for sold accounts or secured sales contracts, the obligor has fully discharged their payment obligations. Once a termination statement is filed, the security holder’s rights under that notice are extinguished – Section 14(3).

4.6 Searching the Registry – Sections 18–19

Section 18(1) sets out what the STRO must provide on request: all active notices filed against a specified security giver; registration numbers and dates; security holder and giver names and addresses; collateral descriptions; and a listing of all related filings (amendments, continuations, corrections, terminations). Section 18(2) specifies the search parameters: a notice search can be conducted using the security giver’s citizenship certificate number, company registration number, vehicle serial number, or initial notice file number. Section 19(2) is commercially significant: electronic searches of the STRO database are entirely free of charge. Only physical filings and manual searches carry the NPR 500 per-filing fee under Section 19(1). This means any bank, lawyer, or individual can run a pre-lending STRO search at stro.org.np at zero cost.

| The Rokka vs The STRO: Same Tool, Different Architecture The Land Revenue Office Rokka (रोक्का) – recorded in the Rokka Kitab under Land Revenue Act, 2034, Section 8kha – costs NPR 50 to record, provides same-day administrative exclusion of third parties, and is the backbone of every BFI’s collateral verification process for land. The STRO costs NPR 500 to register, provides equivalent legal priority protection for movable assets, and has been live and publicly searchable at stro.org.np since May 2017. The legal protection they provide is comparable. The institutional architecture around them is not. The Malpot Rokka is embedded in NRB supervision templates, criminal liability provisions under the Banking Offence and Punishment Act, 2064, valuation frameworks, and loan documentation checklists. Regarding STRO, NRB has embedded STRO use in its regulatory framework. Under the Working Capital Loan Guidelines, 2022 (integrated into the NRB Unified Directives), BFIs must obtain a STRO search report before accepting any movable property as collateral, to verify prior claims and establish priority. NRB Unified Directive 21/2081 mandates STRO filing at the time of loan disbursement or renewal for both hypothecation and pledge of current and movable assets. The Capital Adequacy Framework 2015, Clause 3.4 (Legal Certainty) requires that to claim credit risk mitigation capital relief, banks must take all necessary steps to fulfil “local contractual and statutory requirements” for enforceability – specifically listing “registering it with a registrar” as the operative step. Without STRO filing, movable collateral does not qualify for CRM capital relief. On paper, the system is complete: the registry is live, the mandate exists, and the capital incentive is written into the framework. |

4.7 The STRO in Practice: What the Data Shows

Since going live in May 2017, the STRO has recorded approximately 537,000 total entries, of which around 411,000 are initial notices of security interest – averaging roughly 51,000 new filings per year across Nepal. This is not a dormant registry. But it has not produced a structural shift in movable asset lending.

Land-backed credit peaked at 68.0% of total BFI credit in 2023 despite eight years of STRO operation. As of November 2025, it stands at 64.4%. NRB Bank Supervision Reports continue to identify “double counting of assets” and “multiple banking against the same security” as sector-wide problems in every year through 2024. The most probable explanation for this disconnect is that the bulk of STRO filings are concentrated in hire purchase and vehicle finance – where the asset is a discrete physical item and filing is straightforward – rather than in commercial bank working capital and enterprise lending, where the credit allocation impact would be largest. Without a publicly available breakdown of STRO filings by institution type and collateral category, this hypothesis cannot be confirmed. Requiring KSKL to publish quarterly disaggregated statistics – one of the three supervisory actions identified as Reform 1 in Land Locked Credit – would resolve this uncertainty.

Part V: Creating a Security Interest – Attachment

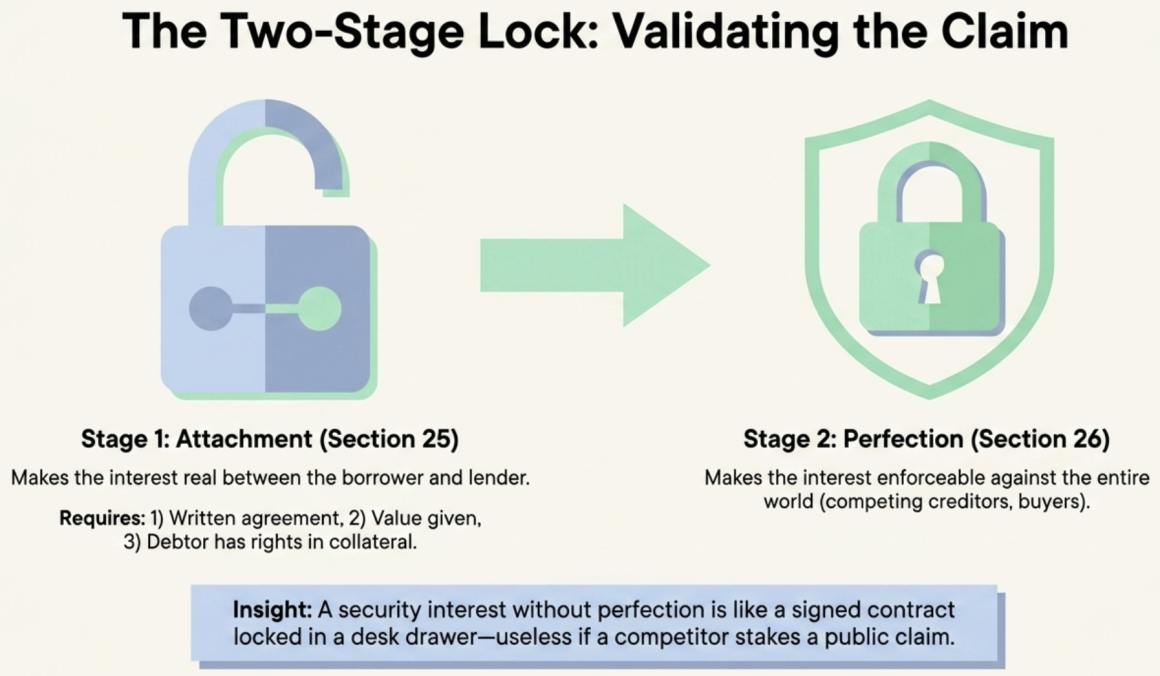

A security interest does not simply come into existence because the parties want it to. The Act establishes a specific legal threshold – called “attachment” (धितोको हकको आवद्धता) – which is the moment the security interest becomes legally enforceable between the security holder and the security giver. Attachment is to the security interest what signing a contract is to a contract: it brings the right into legal existence. Without attachment, the security holder has no claim over any specific asset, only a contractual promise from the debtor.

Attachment is conceptually distinct from perfection (examined in Part VI). Attachment creates the security interest between the parties. Perfection makes it enforceable against the entire world – third parties, competing creditors, buyers, and lien holders. In simple transactions, both happen simultaneously. In more complex arrangements, they may happen at different times, and the gap between them can have significant legal consequences.

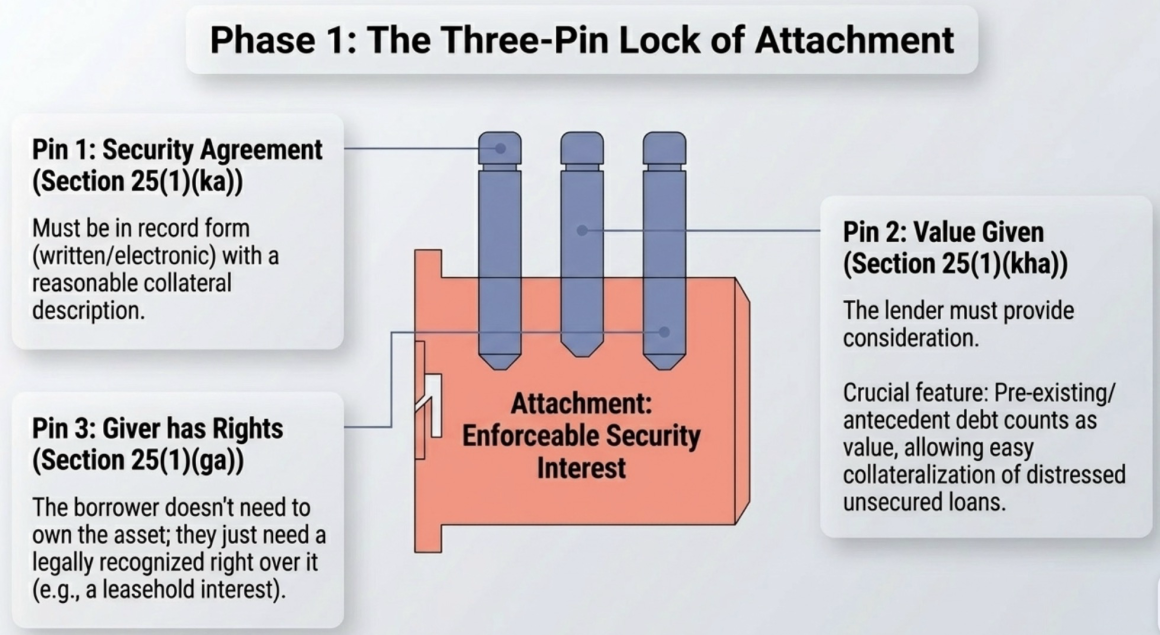

5.1 The Three Conditions for Attachment – Section 25(1)

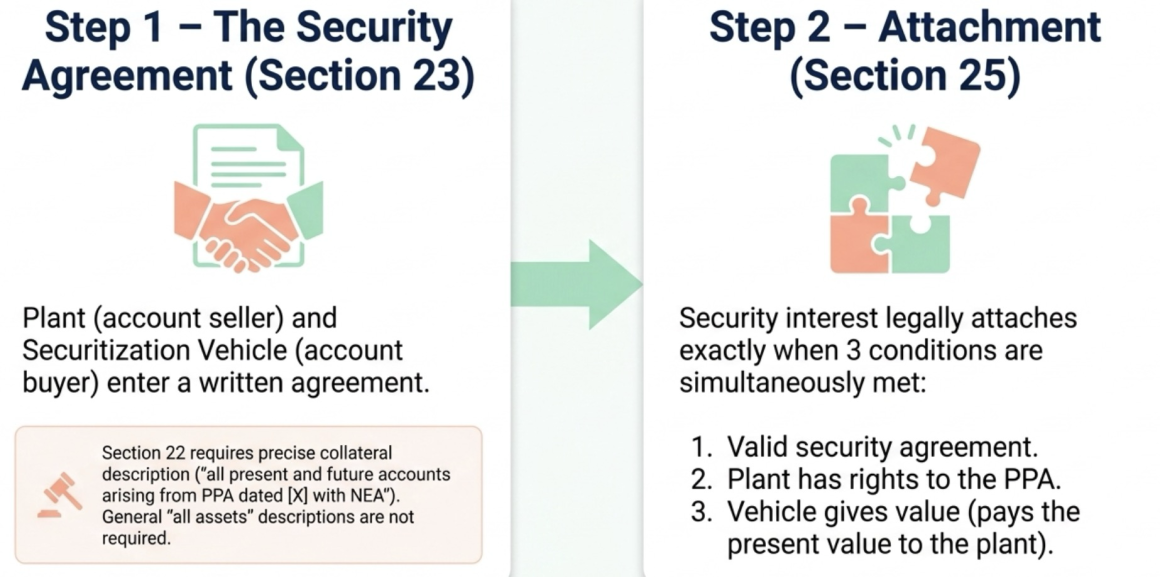

Section 25(1) establishes that a security interest attaches to collateral only when all three of the following conditions are simultaneously satisfied. Missing any one of them means the security interest has not legally come into existence.

Condition 1: A Security Agreement with a Collateral Description – Section 25(1)(ka)

There must be a valid security agreement that contains a description of the collateral property. The agreement must be in record form under Section 23(1) – written or electronic documentation is required; an oral pledge is not sufficient. The description need not be forensically precise. Section 22 establishes that a description is legally sufficient if it “reasonably identifies” what is being described. For most commercial collateral, this standard allows for general descriptions: a security agreement describing the collateral as “all current and future inventory” or “all movable property” of the debtor is legally sufficient, provided the debtor is not an individual consumer and the collateral is not a serial-numbered vehicle.

The Explanation to Section 22 specifically defines what “general manner” means in this context: phrases such as “all assets of the security giver” or “all movable property of the security giver” constitute a sufficient general description. This is the statutory equivalent of the floating charge: the security agreement can cover an entire fluctuating pool of assets without itemising each piece. The only exceptions requiring specific description are consumer goods (which cannot be covered by a general “all assets” description because they are personal household items that deserve individual identification) and serial-numbered vehicles (which must be identified by make, model, and chassis/serial number).

Condition 2: The Security Holder Has Given Value – Section 25(1)(kha)

The security holder must have actually provided “value” (मूल्य) to the security giver. Value is defined in Section 2(bha) as consideration given or to be given according to the agreement – it encompasses cash disbursements, credit extensions, delivery of goods, provision of services, or any other form of consideration. For a standard bank loan, value is given when the bank transfers the loan funds to the borrower’s account. For a hire-purchase arrangement, value is given when the financier delivers or pays for the asset. For a sale of accounts, value is given when the factoring company pays the discounted purchase price for the invoices.

Critically, Section 21(4) explicitly confirms that a pre-existing, antecedent debt constitutes value. This means a bank holding an unsecured loan that has become problematic can take new collateral to secure that old debt without disbursing any fresh cash. The act of agreeing to forbear – to not immediately demand repayment – or the act of modifying the terms of the existing debt, constitutes the consideration that satisfies the value requirement. This has significant practical implications for debt restructuring: a bank can collateralise a distressed unsecured loan by having the debtor execute a new security agreement covering movable assets, and the attachment will be legally valid from the moment of the restructuring agreement.

Condition 3: The Security Giver Has Rights in the Collateral – Section 25(1)(ga)

The security giver must have a legally recognised right over the collateral – ownership, a leasehold interest, a possessory right, a contractual entitlement – or must have the legal authority to transfer rights in the collateral to the security holder. The security giver does not need to be the owner. A lessee can pledge their right to use leased equipment. A consignee can pledge goods held on consignment up to the extent of their interest. A borrower under a hire-purchase arrangement can pledge their equitable interest in the financed asset.

What the security giver cannot do is pledge something they have no rights to at all. If a business owner attempts to pledge their neighbour’s machinery without the neighbour’s knowledge or authorisation, the security interest does not attach – there is nothing for it to attach to. The bank that takes such a pledge in good faith has no legal claim over the machinery; its remedy is only against the business owner personally for fraud or misrepresentation.

Practical Illustration: All Three Conditions in Action

A Kathmandu-based printing company, “Himalayas Press Pvt. Ltd.,” approaches Nepal Investment Mega Bank (NIMB) for a NPR 20 million working capital loan. On Monday, NIMB and the printing company sign a loan agreement that describes the collateral as “all current and future printing machinery and equipment of Himalayas Press Pvt. Ltd., together with all accounts receivable arising from printing contracts.” Condition 1 is met: a security agreement with a collateral description exists. The printing company owns two Heidelberg offset printers and has NPR 4 million in outstanding invoices from media clients. Condition 3 is met: the company has clear rights in both the machines and the receivables. But the loan is not disbursed until Wednesday, when NIMB transfers NPR 20 million to the company’s account. Condition 2 is met on Wednesday. The security interest attaches at the exact moment of disbursement on Wednesday – not when the agreement was signed on Monday.

5.2 After-Acquired Property and the Floating Charge Equivalent

The combination of three Act provisions creates what common law systems call a “floating charge” – but with greater legal strength. Section 2(ta)’s definition of collateral includes future collateral (भविष्यमा सृजना हुने धितोको सम्पत्ति). Section 22’s permission for general descriptions allows a security agreement to cover “all present and future inventory.” And Section 20(3) confirms that a security interest is not invalidated merely because the security giver retains the right to use, sell, exchange, or mix the collateral.

Put together: a bank can take a security interest in a retailer’s entire present and future inventory, registered today against the general description “all inventory,” and that security interest automatically attaches to every new item of stock the retailer acquires tomorrow, next month, and next year – from the moment the retailer acquires rights in the new stock. No amendment to the notice is needed. No new agreement is required. The Act’s attachment mechanism is continuous and automatic for properly described future collateral.

The difference from a traditional floating charge is significant. Under English floating charge law, the charge “floats” until a triggering event (like default) causes it to “crystallise” – attaching to the specific assets existing at that moment. During the floating period, a floating charge can be defeated by certain unsecured creditors and by subsequent specific charges. Under Nepal’s Act, there is no crystallisation delay: the security interest is a fixed, attached, and (once filed) perfected property right from the moment each new item of collateral is acquired. There is no window of vulnerability in which a subsequent creditor can defeat it, provided the original notice was filed and remains current.

5.3 Secured Obligations – Section 21

Section 21 establishes the types of underlying obligations that a security interest can secure, and the range is deliberately broad:

Section 21(1): one or multiple obligations, described generally or specifically. A single security agreement can secure a term loan, a revolving line of credit, and a bank guarantee obligation simultaneously.

Section 21(2): monetary or non-monetary. A business can pledge its machinery to secure not only a cash debt but also its contractual obligation to deliver 1,000 units of goods under a supply agreement.

Section 21(3): future obligations – mandatory, conditional, or optional. A bank that commits to a NPR 100 million revolving credit facility need not worry that its security interest fails to attach to advances not yet made: the agreement covers future drawdowns.

Section 21(4): pre-existing obligations. Collateral pledged today can secure a debt incurred years ago. This is the antecedent debt rule discussed in Section 5.1.

Part VI: Making It Count – Perfection and Maturity (धितोको हकको परिपक्वता)

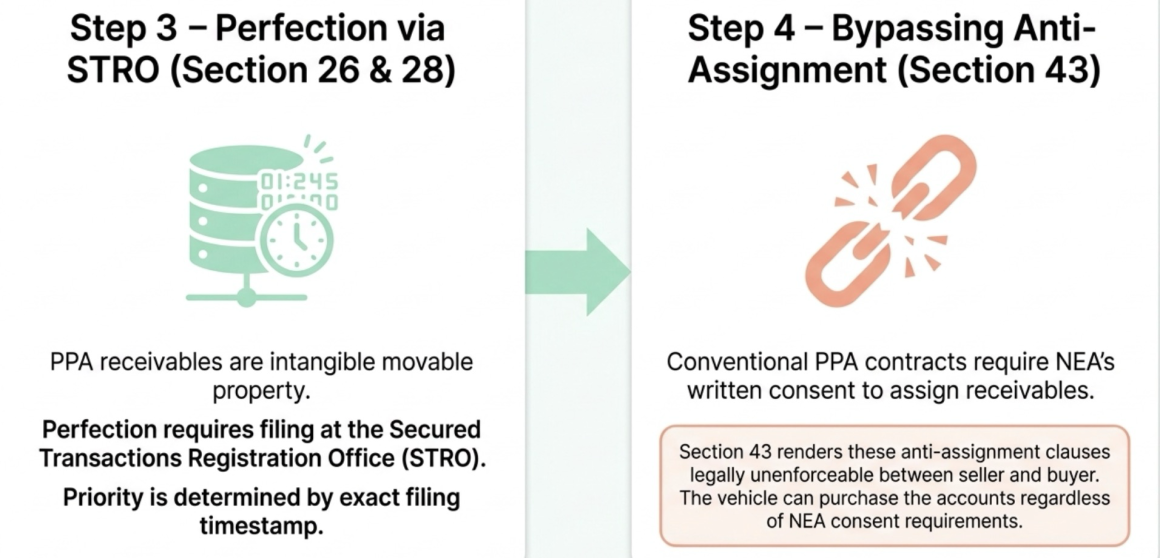

Attachment makes a security interest real between the two contracting parties. Perfection (परिपक्वता – literally “maturity”) makes it enforceable against the world. An unperfected security interest is vulnerable: a subsequent creditor who perfects their own interest first will take priority, regardless of who knew about what. A buyer who purchases the collateral for value without knowledge of the unperfected interest takes it free and clear. Even in insolvency, an unperfected interest ranks behind unsecured creditors in many circumstances. Perfection is not optional for a lender who wants to protect their investment.

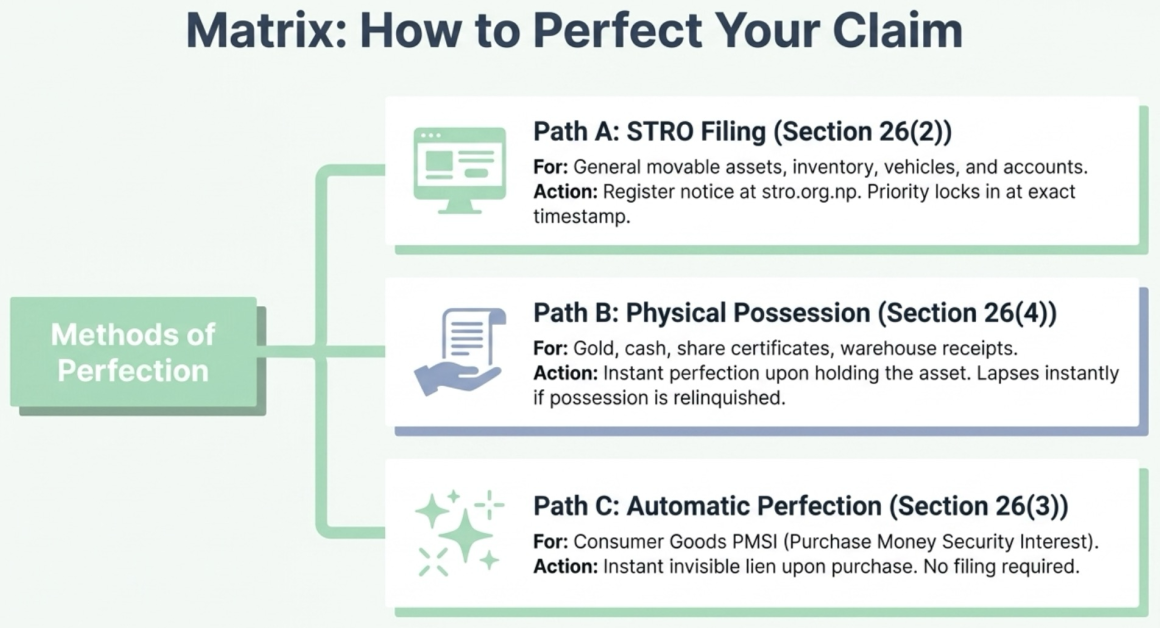

6.1 The Methods of Perfection – Section 26

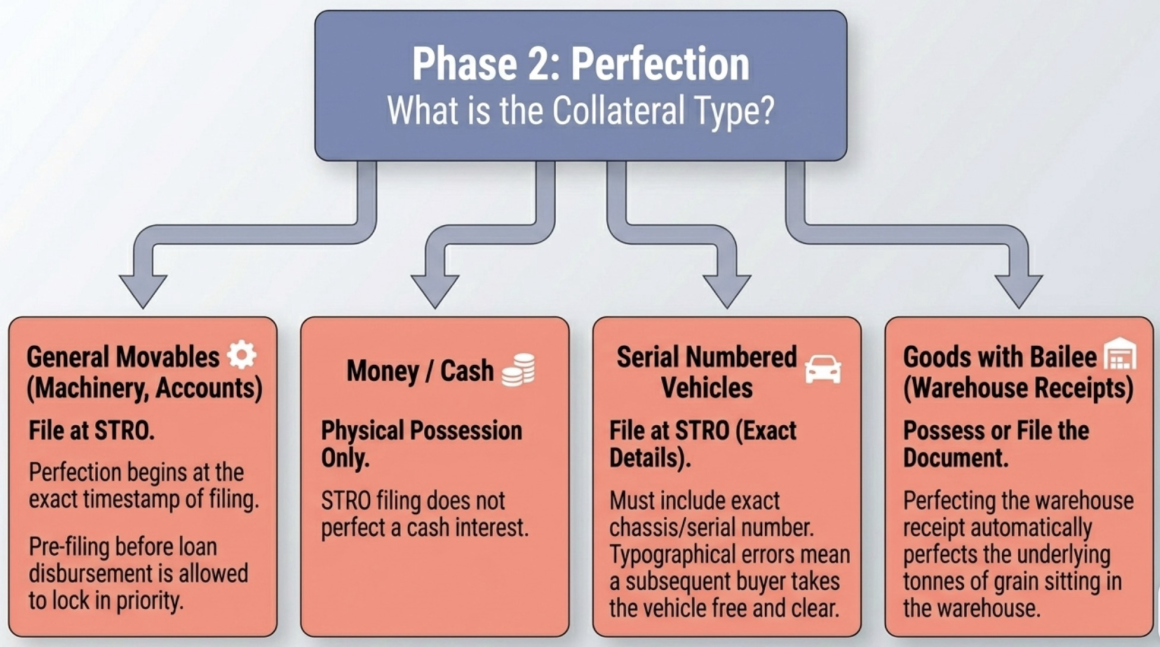

The Act provides different methods of perfection depending on the type of collateral. The general rule is filing a notice at the STRO. For specific collateral types, alternative methods – or mandatory variations – apply.

| Collateral Type | Method of Perfection | Section | Notes |

| General movable assets (machinery, inventory, accounts) | File notice at STRO | 26(2) | Default rule for all collateral not otherwise specified |

| Consumer goods (PMSI only) | Automatic on attachment; no filing required | 26(3) | Creates invisible lien; protects sellers but not subsequent lenders searching STRO |

| Goods, instruments, documents, secured sales contracts | Security holder takes possession | 26(4) | Filing optional but permitted before/during/after possession |

| Money / cash (non-proceeds) | Security holder takes physical possession only | 26(5) | STRO filing alone does NOT perfect a cash security interest |

| Serial numbered vehicle | File notice; must describe vehicle or provide serial number | 26(6) | Wrong or missing serial number in notice = buyer takes free – Section 30(2)(ga) |

| Proceeds from collateral sale/exchange | Automatic; no new filing required | 26(7), 33 | Lapses after 20 days for non-cash proceeds of a different type unless refiled |

| Guarantee supporting secured obligation | Automatic when underlying collateral is perfected | 26(9) | No separate filing required for the guarantee |

| Goods held by bailee who issued a document | Perfect interest in the document first | 26(8) | Possession of the document = perfection in the underlying goods |

6.2 The General Rule: Filing at the STRO – Section 26(2)

For most movable commercial assets, the security interest is perfected by filing an initial notice at the STRO. The Act does not specify any minimum waiting period after filing: perfection is effective from the exact timestamp of filing. This is why the priority rule in Section 28(2) refers to the date and time of filing – in a closely contested priority dispute between two lenders, the sequence of filing within a single business day can matter.

Filing before attachment is both permitted and strategically important. Section 7(4) explicitly allows a lender to file a notice before the security agreement is signed or before the security interest has attached. This allows a bank to “lockin” its priority position during due diligence and documentation, so that even if closing the transaction takes several weeks, the bank’s priority date runs from the pre-closing filing, not from the disbursement date. In a competitive lending environment, this can be decisive.

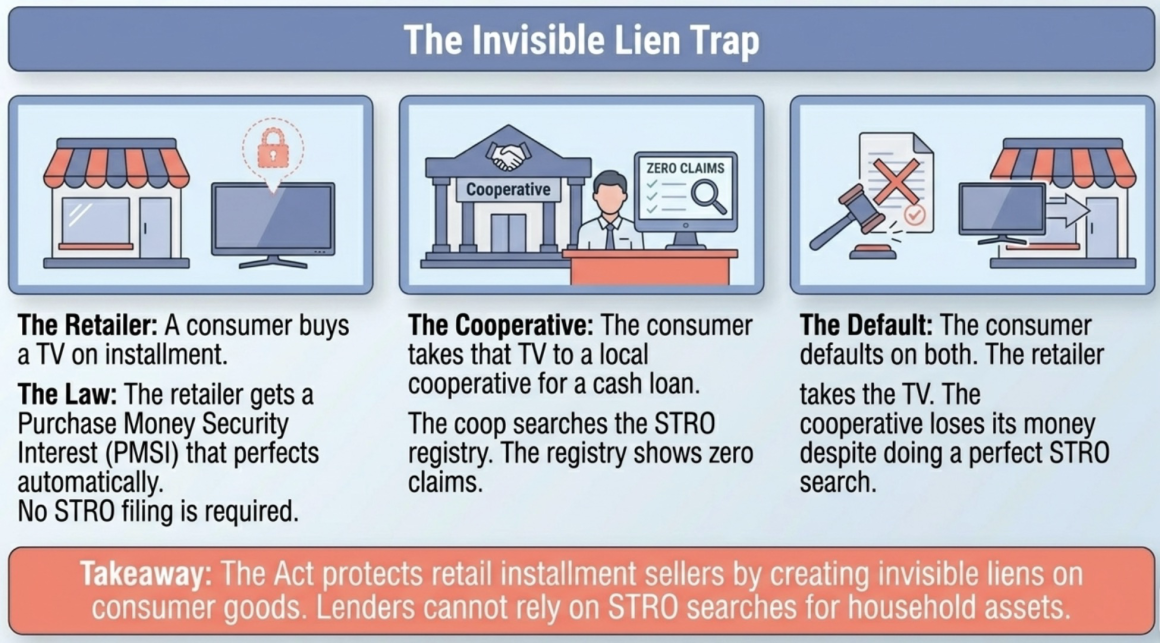

6.3 Consumer Goods PMSI: Automatic Perfection – Section 26(3)

A Purchase Money Security Interest in consumer goods – the only type of security interest the Act permits over consumer goods – perfects automatically the moment it attaches. No STRO filing is required. When a consumer buys a television on an installment plan from an electronics retailer, the retailer’s PMSI perfects at the moment the consumer signs the agreement and takes the television home. No notice appears in any public registry.

| The Invisible Lien on Your Refrigerator When you buy a television, refrigerator, or washing machine on installment from any retailer in Nepal, the retailer holds a legally perfected security interest over that item from day one – invisible in the public STRO registry. This is deliberate under Section 26(3): consumer goods PMSIs perfect automatically on attachment, with no filing required. For consumers, this is largely irrelevant. For any cooperative or informal lender who later accepts that household item as collateral for a cash loan, it is a structural trap: 1. The lender searches the STRO registry and finds no prior notice against the item. 2. The lender concludes the item is unencumbered and disburses the loan. 3. The borrower defaults on both the installment plan and the new loan. 4. The retailer, holding a perfected PMSI from day one, has first priority. 5. The lender, whose filing post-dates the retailer’s automatic perfection, loses. The Act protects innocent buyers of consumer goods in private sales (Section 30(2)(kha)) but offers no equivalent protection to innocent lenders. The only defense is physical due diligence: asking for purchase receipts and financing documents before accepting household assets as collateral. The STRO cannot help you here. |

6.4 Possession as Perfection – Section 26(4)

For goods, instruments (including share certificates and bearer bonds), documents such as warehouse receipts, and secured sales contracts, the security interest perfects when the security holder takes physical possession of the collateral. No STRO filing is required, though filing is also permitted before, during, or after taking possession. The security interest is perfected from the moment possession is taken and remains perfected only as long as possession is maintained. If the security holder voluntarily returns the collateral to the debtor without filing a STRO notice to maintain perfection, the interest becomes unperfected.

This is the classical pledge in its modern legal form. A cooperative holding a borrower’s gold bars in its vault, or a bank holding share certificates pending repayment, is perfecting by possession under this provision. The practical advantage is speed and simplicity: no filing, no fee, instant perfection. The risk is that the security holder cannot allow the collateral to leave their physical control without either maintaining a STRO filing or accepting that their perfection lapses. Section 27(1) allows a smooth transition between possession and filing without loss of priority – provided there is no gap.

6.5 Serial Numbered Vehicles – Section 26(6)

For serial-numbered vehicles, perfection requires filing a STRO notice that either generally describes the vehicle or specifies its serial and chassis numbers. The specific number matters because Section 30(2)(ga) gives a buyer of a serial-numbered vehicle the right to take it free of any prior security interest if the filed notice failed to include the serial number, or included it incorrectly. A bank that finances a truck purchase and files a STRO notice with a typographical error in the chassis number has effectively no protection against a subsequent buyer of that truck who searches the registry and finds nothing. The notice is valid between the bank and the borrower, but the buyer takes the truck clean.

6.6 Proceeds and the 20-Day Window – Sections 26(7) and 33

When collateral is sold, exchanged, or destroyed, the security interest automatically continues in the proceeds – Section 33(1). No new filing is required. If a bank holds a perfected security interest over a distributor’s inventory of laptops and the distributor sells twenty of them for cash, the bank’s interest automatically extends to the cash proceeds without any additional action.

However, Section 33(3) introduces a 20-day grace period with teeth: the automatic perfection in proceeds lapses after twenty days from the date the debtor receives the proceeds, unless one of three conditions is met:

- The original notice already describes the proceeds by type (e.g., the original filing covers “inventory and all accounts arising from inventory sales” – the resulting accounts are covered by description and the interest in them continues beyond 20 days).

- The proceeds are identifiable cash – money deposited into a traceable bank account or physical currency – which continues automatically beyond 20 days under Section 33(5)(ka).

- The security holder files a new notice or amendment within the 20-day window specifically covering the type of proceeds received.

The practical implication: if a debtor sells collateral and receives a completely different type of asset as payment – trading inventory for a motor vehicle, or exchanging pledged machinery for equity in another company – the bank must act within twenty days. It must file an amendment to its original notice that adds the new asset type to the collateral description, or it loses its perfected status in those specific proceeds on day twenty-one. A creditor who then registers a claim against the vehicle or equity stake on day twenty-two will have priority.

6.7 The Goods-with-Bailee Rule – Section 26(8)

A bailee (नासोमा लिने व्यक्ति) is a third party – typically a warehouse operator – who holds goods for the benefit of the owner. When the bailee has issued a formal title document covering the stored goods, such as a warehouse receipt, that document itself represents the legal right to the underlying goods. The Act requires that before a security interest in those goods can be perfected, the security interest in the document itself must first be perfected – either by taking possession of the document or by filing a notice covering it.

This rule has significant practical importance for agricultural and commodity lending. When a rice trader stores 100 tonnes of rice in a licensed warehouse and receives a Warehouse Receipt, that single piece of paper concentrates the legal right to all 100 tonnes. A bank that takes possession of the Warehouse Receipt or files a STRO notice covering it has, in a single act, perfected its security interest in 100 tonnes of physically stored rice – rice it has never seen, in a warehouse it may never visit. The commodities framework under the Commodities Act, 2017 and the Central Depository Service Regulation, 2010 contemplates exactly this structure through dematerialised warehouse receipts through the CDSC system.

| Case Study: The Goods-with-Bailee Rule and STRO Registration Case Background Ram is a large-scale agricultural trader. To safely keep his inventory, he deposits 100 tonnes of rice into a commercial warehouse operated by Nepal Storage Pvt. Ltd. (the bailee). Upon receiving the rice, the warehouse operator issues Ram a formal “Warehouse Receipt.” Under the Secured Transactions Act, 2063, this warehouse receipt is legally defined as a “document”. At this stage, no money has been borrowed, and no financial institution is involved; it is purely a storage arrangement. The Core Question If a transaction is purely a bailment-where a warehouse operator merely stores goods and issues a warehouse receipt to the owner without any associated loan or credit-does this constitute a secured transaction, and can this standalone warehouse receipt be registered in the Secured Transactions Registration Office (STRO)? Or does STRO registration only apply when the owner subsequently pledges that warehouse receipt to a lender as collateral to secure a debt? Analysis and Answer A pure bailment arrangement (merely storing goods and receiving a receipt) is not a secured transaction, and the standalone warehouse receipt cannot be registered in the STRO unless it is actively being used as collateral for a debt. Here is how the law applies to this scenario in two distinct phases: Phase 1: The Pure Bailment (Outside STRO Jurisdiction) When Ram simply parks his rice in the warehouse and gets a receipt, this arrangement falls entirely outside the scope of the Secured Transactions Act. According to Section 3, Subsection (1), Clause (a), the Act only applies to transactions (like pledges, hypothecations, or hire-purchases) that are specifically executed for the purpose of securing an obligation with collateral. Because no one is lending money and no debt is being secured, this is a pure storage contract. Furthermore, STRO registration is legally impossible at this stage. Under Section 7, Subsection (1), a preliminary notice filed at the STRO must contain the details of both the “security giver” (the debtor/borrower) and the “security holder” (the creditor/lender). In Ram’s pure bailment, these roles do not exist, meaning the electronic registry cannot accept the filing. Phase 2: The Security Arrangement (Triggering STRO Registration) The legal rule outlined in Section 26, Subsection (8) only activates when the transaction transforms from a simple storage arrangement into a credit facility. Assume Ram now needs cash to buy more inventory. He takes his Warehouse Receipt to Bank A and pledges it as collateral for a 5 million Rupee loan. Now, a true lender-borrower security arrangement has been created. To protect its new investment, Bank A will log into the STRO and file a notice naming Ram as the security giver, Bank A as the security holder, and the warehouse receipt as the collateral. According to Section 26, Subsection (8), because the goods are in the custody of a bailee who has issued a document covering them, Bank A must perfect its security interest in the document itself. By taking possession of the Warehouse Receipt or filing a STRO notice covering it, Bank A legally perfects its security interest over the actual 100 tonnes of rice sitting in the warehouse. Conclusion The STRO is strictly a financial registry, not a property or storage registry. The warehouse receipt cannot be registered during the pure bailment phase; STRO registration only applies-and the Goods-with-Bailee rule only activates-once the borrower (Ram) furnishes that receipt to a lender (Bank A) to secure a financial obligation. |

6.8 Continuity of Perfection – Section 27

Section 27(1) addresses a potential gap that arises when a security holder switches from one method of perfection to another. If the interest is first perfected by one method and then later perfected by another method, with no interruption in between, the law treats the interest as continuously perfected from the original date. The priority position does not reset to the date of the change in method.

Section 27(2) extends this principle to transferred interests: when a perfected security interest is legally transferred from one security holder to another, the transferee does not need to re-file a new STRO notice to maintain the perfection against third parties. The original notice, filed by the original security holder, continues to serve as the public record of the security interest, and the priority date remains unchanged. This rule is critical for loan portfolio sales and for the AMC framework examined in the AMC article: when a bank sells a perfected secured loan to another entity, the buyer does not lose the bank’s priority position.

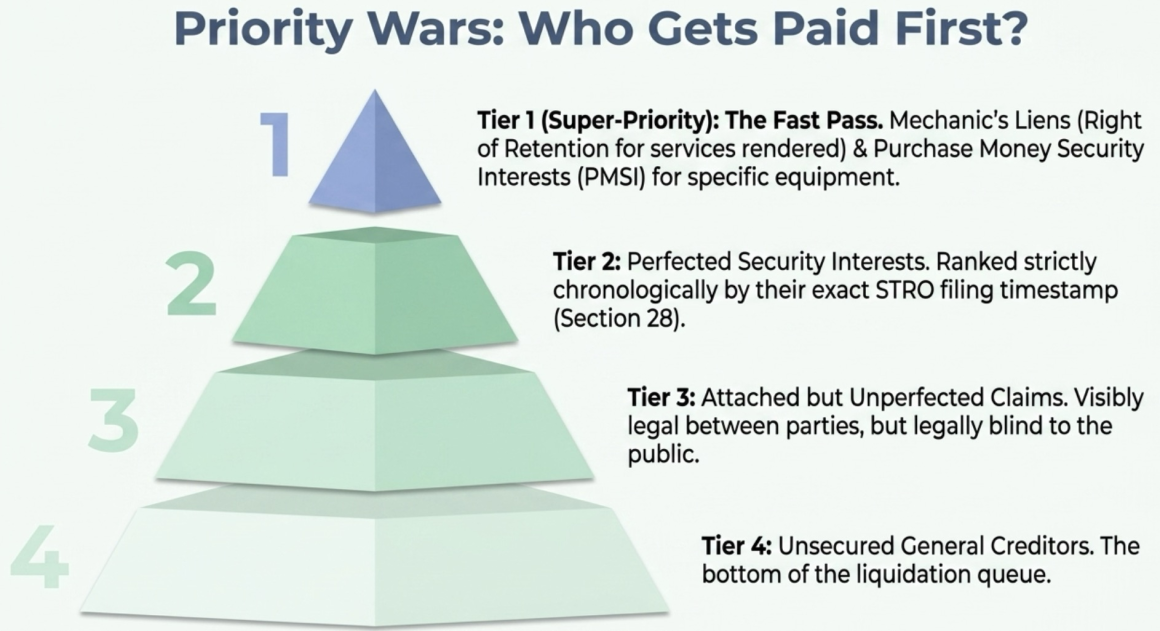

Part VII: The Priority Wars – Who Gets Paid First

Priority rules answer the question that matters most in a default: when multiple parties have claims against the same asset and the proceeds of sale are insufficient to satisfy everyone, who gets paid first and in what order? The Act’s priority framework is hierarchical, specific, and in several places, counterintuitive. This Part works through the framework systematically.

7.1 The General Rule: First to File or Perfect – Section 28

Section 28(1) establishes the foundational rule: a perfected security interest always beats an unperfected one. Among multiple perfected interests in the same collateral, priority goes to the one whose notice was first filed or whose interest was first perfected, whichever occurred earlier in time.

Section 28(2) defines this priority date precisely: it is the earlier of (a) the date the first notice covering that collateral was filed at the STRO, or (b) the date the security interest was first perfected by any other method (such as possession). The priority date runs from this earlier event, even if the security interest had not yet attached when the notice was filed. This is why pre-filing matters so much: a bank that files a STRO notice before the loan closes locks in a priority date before any subsequent creditor who files after the closing, regardless of when the security interest actually attached.

Section 28(3): the first-in-time rule applies to proceeds as well. The priority date for a security interest in proceeds is the same as the priority date for the original collateral from which those proceeds derived.

| Priority Rank | Type of Claim | Governing Section | Key Condition |

| 1st | Perfected security interest (filed first) | 28(1)(2) | Continuous coverage; no lapse in perfection |

| 2nd | Perfected security interest (filed second) | 28(1) | Must be perfected; loses only to earlier-dated perfected claim |

| 3rd | Attached but unperfected security interest | 28(3) | Loses to any perfected claim and to value-paying buyers |

| Special: 1st in class | PMSI in equipment (filed within 5 days) | 34 | Supersedes prior “all assets” claims in that specific equipment |

| Special: 1st in class | PMSI in inventory (filed with prior notice) | 35 | Requires notice to prior inventory lenders AND perfection on possession |

| Special: super-priority | Right of retention (possessory lien, services to goods) | 36 | Beats perfected interest for that specific asset, if in ordinary course of business |

| Last | Unsecured claims | N/A | No specific collateral right; general creditor only |

7.2 PMSI Super-Priority: Equipment – Section 34

A Purchase Money Security Interest in equipment jumps ahead of any prior “all assets” charge if it is perfected at the moment the security giver receives possession of the equipment or within five days after. No advance notice to prior secured creditors is required.

Nepal Investment Mega Bank has a registered STRO notice against all assets of Himalayan Hotels Pvt. Ltd. The hotel buys a new commercial kitchen system on credit from Kitchen Equipment Nepal Ltd. Kitchen Equipment Nepal registers its PMSI notice at the STRO within five days of delivery. Result: Kitchen Equipment Nepal’s PMSI takes first priority over that specific kitchen system, ahead of the bank’s general charge – even though the bank filed years earlier. The bank retains its general priority over everything else the hotel owns; it simply cannot claim the specific kitchen system against the supplier’s PMSI.

The five-day window is strict. A PMSI lender who files on day six falls back to the general first-to-file rule and likely loses to the prior all-assets lender. This creates a practical obligation for equipment suppliers providing seller financing: the STRO notice must be filed before or on the day of delivery, or within the five-day window without exception.

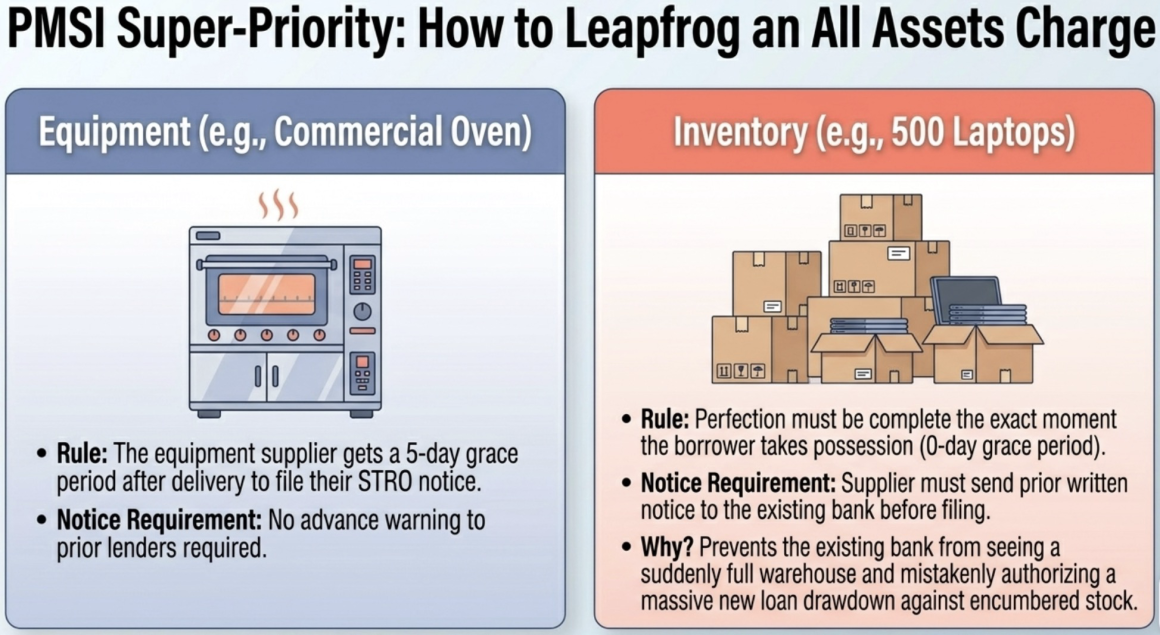

7.3 PMSI Super-Priority: Inventory and Livestock – Section 35

For inventory and livestock, the Purchase Money Security Interest (PMSI) super-priority is harder to obtain because the procedural requirements are more demanding. Two conditions must both be met:

- First, the PMSI must be perfected by the time the security giver takes possession of the inventory or livestock.

- Second – and this is the critical additional requirement – if any prior secured creditor has already filed a notice covering the same type of inventory, the PMSI lender must give that prior creditor advance written notice before filing their own PMSI notice. This written notice must: identify the inventory by description or type; and explicitly state that the sender has, or expects to acquire, a PMSI in that specific inventory.