Pricing Hydropower Insurance in Nepal

This article is a continuation of The Cascade Effect. It builds on the market and regulatory foundation established there and should be read in that context. All references are at the closing section of this post.

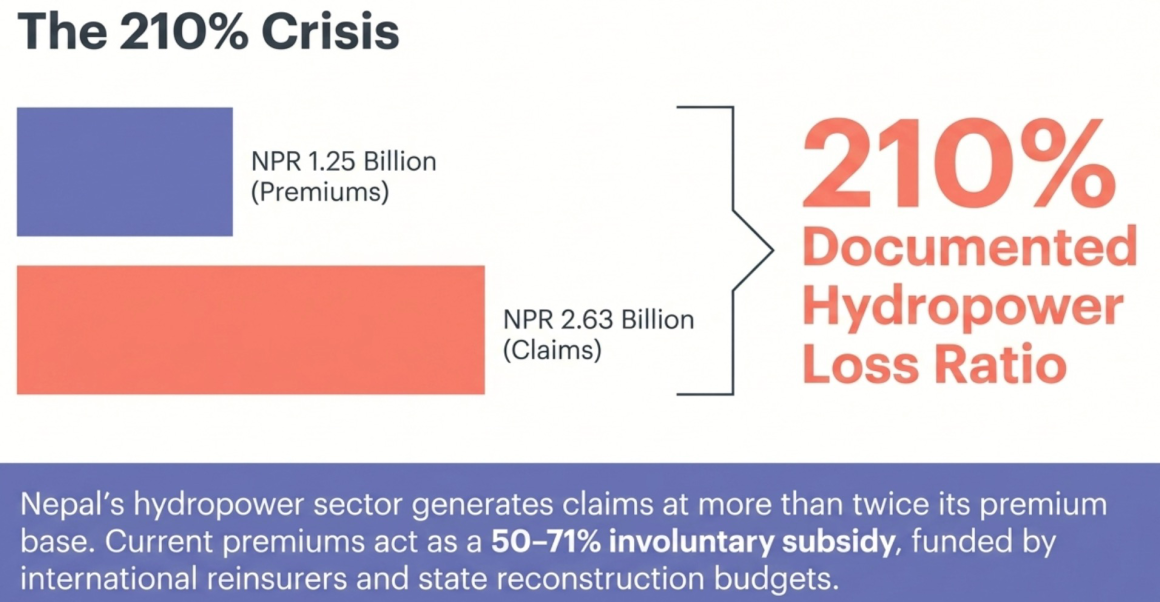

Nepal’s hydropower sector carries NPR 2.63 billion in documented insurance claims against NPR 1.25 billion in premiums – a loss ratio exceeding 210%. Yet the insurance framework governing this sector remains structurally anchored to a flat tariff of NPR 2.00 per thousand that treats a run-of-river project in the mid hills identically to one operating beneath a glacial lake. This post examines the full spectrum of risks facing Nepal’s generation, transmission, and distribution infrastructure; maps those risks against the legal obligations arising from Power Purchase Agreements, loan covenants, Insurance Law, and international development bank standards; tests the adequacy of existing insurance products against documented hazard profiles; and constructs both an academic pricing model and an indicative data-driven tariff proposal. The analysis reaches three conclusions. First, Nepal’s insurance products are structurally misaligned with the risks they are supposed to cover. Second, the transmission and distribution sector – managed by NEA through an internal fund of NPR 20 million against a PPE base of NPR 242 billion – operates in a state of near-total uninsurance, a condition that is becoming a barrier to private investment and PPP models for the grid. Third, the current flat tariff is actuarially indefensible and must be replaced with a basin-differentiated, risk-loaded pricing model if the sector is to remain commercially insurable.

1. Introduction: Building on the Cascade Effect

The Cascade Effect established that Nepal’s hydropower insurance market suffers from four compounding failures: geographic concentration of risk, inadequate domestic reinsurance capacity, a claims settlement framework ill-equipped for cascade disasters, and a tariff system that neither prices catastrophe risk correctly nor distinguishes between hazard exposures across Nepal’s vastly different river basins. That article documented NPR 2 billion claims from a single project (Upper Tamakoshi, September 2024), traced the legal architecture of the insurance market, and identified the circular economy linking insurance premiums to project equity investment.

This post takes the analysis further along three dimensions. It maps risks comprehensively across the entire power delivery chain – generation, transmission, and distribution – rather than focusing exclusively on generation assets. It tests, product-by-product and clause-by-clause, whether the insurance instruments currently available in Nepal’s market actually cover the risks that exist. It constructs a pricing framework grounded in loss data, actuarial principles, and the regulatory mechanics already embedded in the Property Insurance Directive 2080 and the Risk-Based Capital Directive 2082.

The thesis is straightforward: the gap between what Nepal’s hydropower sector needs from insurance and what it currently receives is not a marginal inadequacy. It is a structural misalignment that threatens financial closure for new projects, leaves sovereign assets exposed to catastrophic unindemnified losses, and will worsen as the climate pushes hazard frequencies and severities beyond historical baselines.

2. Risk Identification Across the Power Delivery Chain

2.1 Generation Infrastructure Risks

Nepal’s generation assets – comprising 3,591 MW of installed capacity as of FY 2024/25, of which approximately 2,283 MW belongs to IPPs and the remainder to NEA and its subsidiaries (NEA Annual Report FY 2024/25) – are exposed to six categories of natural and operational risk.

Seismic and Geological Risks. Nepal sits on an active fault line. The 2015 Gorkha earthquake damaged 31 hydropower plants representing 1,098 MW of installed capacity – 44% of the national total at the time – and left 702 MW non-operational for a significant period (IRRP Resilience Planning Guidelines Report 2022, Box 4: Hydropower Projects Damaged by the 2015 Gorkha Earthquakes). Modern powerhouses are engineered to withstand seismic loads, but the 2015 event demonstrated that peripheral infrastructure – access roads, headworks, intake structures, transmission towers – is exceptionally fragile. The main types of seismic damage documented are structural cracks in intakes, damage to pipes, and bursting of penstocks (IRRP Report 2022, Section: Earthquakes). More critically, a research study applying the 2015 earthquake model to the 273 currently operational hydropower projects across Nepal, India, and Bhutan found that 25% are likely to face severe damage from earthquake-triggered landslides (IRRP Report 2022, Section: Landslides). The Koshi and Gandaki basins, which together host 86% of Nepal’s hydropower capacity, carry the highest concentration of this seismic exposure.

Flood and Hydrological Risks. Longitudinal data proves that hydrometeorological hazards – flash floods and monsoon-driven landslides – are more frequent and collectively more damaging to Nepal’s hydropower sector over any 25-30 year project lifecycle than earthquake events, despite the benchmark severity of the 2015 Gorkha earthquake (Hydropower Disaster Damage Report, Section: Geophysical Context). The June 2021 floods damaged 26 projects simultaneously – 16 under construction and 10 operational – primarily through river cutting, debris deposition, and surges exceeding design capacity (IRRP Report 2022, Box 5: 2014 Jure Landslide; IPPAN damage assessment data). The September 2024 floods paralyzed Upper Tamakoshi (456 MW) for 88 days through destruction of control buildings and burial of headworks under sediment, not through dam or turbine failure – generating an insurance claim of approximately NPR 2 billion (Nepal Hydropower Flood Damage Assessment Report September 2024, SN 24; Hydropower Disaster Damage Report, Table 1).

Run-of-river (RoR) projects – which constitute 90% of Nepal’s hydropower stations (IRRP Report 2022, Section: Seasonal and Inter-Annual Shifts) – face the additional vulnerability of hydrological variability. These projects operate at approximately 30% capacity during dry months (IRRP Report 2022, Table 6). Climate projections indicate that pre-monsoon and monsoon seasons will become 35-52% wetter by 2050 in extreme rainfall events, while dry season flows decline 3-7% (IRRP Report 2022, Section: Precipitation, Floods and GLOFs). The Super Mai Hydropower project’s reported drop to 79% of contract energy in 2024-2025 (Hydropower Disaster Damage Report, Section: Hydrological Variations) illustrates directly how hydrology variations compress Debt Service Coverage Ratios toward the 1.0x lender covenant threshold.

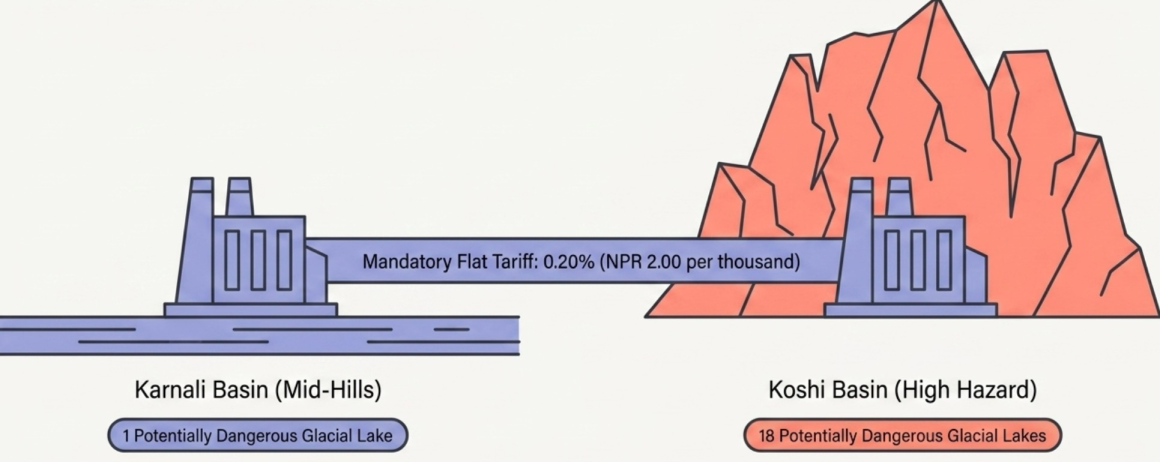

Glacial Lake Outburst Flood (GLOF) Risks. Of the 47 glacial lakes identified as potentially dangerous across the Koshi, Gandaki, and Karnali basins, Nepal hosts 21 directly and is downstream of 26 others in Tibet and India (IRRP Report 2022, Section: Precipitation, Floods and GLOFs, Table 2). The Koshi basin alone contains 18 potentially dangerous glacial lakes. The 456 MW Upper Tamakoshi faces a “probable” burst scenario from Tsho Rolpa – a lake that requires artificial lowering by 15-20 meters to cease posing a threat – and a direct downstream threat from Imja Tsho (IRRP Report 2022, Box 8: Tsho Rolpa and Imja Tsho). A 2016 Bhotekoshi GLOF caused catastrophic damage to a project already weakened by the 2015 earthquake, demonstrating the cascading compounding mechanism of these risks. The 2016 event is a paradigm case of what the sector faces: primary seismic damage reduces structural resilience, then a secondary GLOF delivers the terminal blow.

Landslide Risks. Because Nepal’s hydropower assets are concentrated in narrow, steep-walled valleys, landslides cause more cumulative damage to the sector than direct seismic shaking of concrete (Hydropower Disaster Damage Report, Section: Earthquake-Triggered Landslide Risks). Landslides block canals, bury headworks, destroy access roads, and carry “foreign debris” – boulders and mud from upstream slopes – that batter intake structures. The documented case of Thoppal Khola Hydropower (NIA Compilation of Decisions, Nirnaya Sangraha) established the proximate cause precedent: a landslide blocking a canal that caused water overflow is an insured peril, not a maintenance issue.

Sedimentation Risks. High sediment loads cause turbine runner erosion, runner seal failures, and forced desander flushing shutdowns. At Kali Gandaki A (144 MW), desander flushing during monsoon takes the plant offline for two to three days at a time – alternating between two desanders – putting 72 MW of capacity down per event (IRRP Report 2022, Box 2: Sediment Damage at Jhimruk; NEA Annual Report). The 12 MW Jhimruk installation faced efficiency losses of up to 25% from a 6,900-ton sediment load over two months (IRRP Report 2022, Box 2). Sedimentation is a chronic risk, not an acute one, and is entirely absent from standard property and business interruption policy coverage.

Cybersecurity and Operational Technology Risks. Supervisory Control and Data Acquisition (SCADA) systems and digital control infrastructure introduce new exposure vectors. Nepal is exposed to cyber threats from several technically sophisticated regional states (IRRP Report 2022, Section: Human-Caused Threats). The destruction of Upper Tamakoshi’s Dam Operation Control Building in September 2024 demonstrated that loss of control infrastructure is as disabling as loss of the dam itself – but this category of risk receives no dedicated insurance product in Nepal’s current framework.

2.2 Transmission Infrastructure Risks

Nepal’s transmission network – comprising 6,741 km of 400 kV, 220 kV, and 132 kV constructed, under-construction, planned, and proposed lines (RPGCL Transmission System Master Plan 2018, cited in IRRP Report 2022, Table 4) – is owned and operated primarily by NEA and its subsidiary Rastriya Prasaran Grid Company Limited (RPGCL). It is the most critically exposed and least insured segment of the entire power sector.

Physical disaster exposure. Transmission towers are vulnerable to landslides, floods, earthquake ground motion, and wildfire. A single 220 kV tower was destroyed in the September 2024 Upper Tamakoshi flood. The Chameliya transmission line suffered 146 hours of downtime in 2021 alone – 1.67% of the year – from direct weather damage (IRRP Report 2022, Box 11: 146 Hours of Downtime at Chameliya). In 2017, almost half of Nepali citizens suffered prolonged power outages when heavy rain damaged electricity poles, substations, and transmission stations across the country (IRRP Report 2022, Section: Transmission Vulnerabilities).

Wildfire risk. Nepal recorded 2,087 forest fires between November 2020 and March 2021, affecting 100,000 hectares of forest annually (IRRP Report 2022, Section: Wildfires). The four westernmost provinces experienced more than 27 fire events annually on average between 1971 and 2011, hosting five substations under direct threat. Transmission lines passing through forest land are especially exposed, yet no wildfire-specific insurance product exists for transmission assets in Nepal.

Temperature-efficiency degradation. Each 1°C increase in ambient temperature reduces transmission efficiency by approximately 0.7%, creating increasing losses as climate warming advances (IRRP Report 2022, Section: Transmission Vulnerabilities). Under Representative Concentration Pathway (RCP) 8.5 projections, this could represent an additional 2.9% efficiency loss by the 2080s – a financial impact that is entirely unaddressed by the insurance framework.

Right-of-way constraints. Transmission projects are increasingly routed through landslide-prone areas due to land acquisition disputes (IRRP Report 2022, Section: Governance Vulnerabilities). This directly increases the physical hazard exposure of new lines, yet insurance for these rerouted assets is structured – where it exists at all – on standard construction-phase CAR terms, not on the elevated hazard profile of the revised routing.

2.3 Distribution Infrastructure Risks

Distribution infrastructure – substations, low-voltage lines, and metering infrastructure at the consumer interface – faces the same natural hazard exposure as transmission but at a more granular geographic scale. In the context of this analysis, distribution risks are less material to project finance concerns than generation and transmission, as distribution assets are not typically subject to PPA or loan covenant insurance requirements at the project level. However, NEA’s distribution assets represent a significant portion of its NPR 683.9 billion total asset base, and their exclusion from commercial insurance compounds the systemic contingent liability already identified for transmission.

3. Basin-Specific Risk Concentration

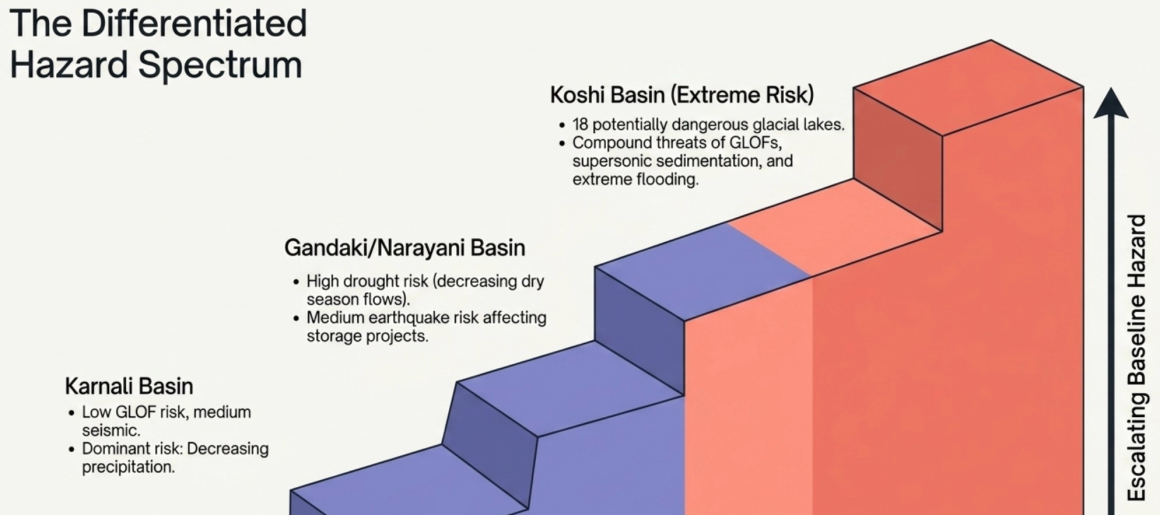

The IRRP Resilience Planning Guidelines Report 2022 provides the most rigorous basin-level risk assessment available for Nepal’s hydropower sector. Table 11 of that report, reproduced below in full, establishes the differentiated risk profile across Nepal’s major generation basins – the foundation for any actuarially defensible pricing model.

Table 1: Scenario Impacts by Basin (Source: IRRP Report 2022, Table 11: Scenario Impacts by Basin – reproduced in full)

| River Basin | Temperature Increase | Drought | Sedimentation | Earthquakes, Landslides & Floods | GLOFs |

| Karnali | Medium: estimates vary | Medium: precipitation decreasing 4.91mm/year | Unknown, likely high | Medium: <10% structures at risk, 40% of roads at risk | Low: 1 potentially dangerous glacial lake |

| Gandaki/Narayani | Medium: max temp increase 1.1–1.5°C by 2080s | High: dry season flows decreasing in most rivers | High: storage value increases under this scenario | Medium: <10% structures at risk, 40% of roads at risk | Low: 1 potentially dangerous glacial lake |

| Koshi | High: temp increase 2.5–5°C by 2100; 20–40% snowfall decrease by 2050 | Low: runoff expected to increase medium-term; consecutive dry days likely to increase | High: large-scale sediment aggregation causing superelevated channels, flooding and instability | Medium: less frequent but more intense rains causing more floods and triggering more landslides | High: 18 potentially dangerous glacial lakes |

This table has direct implications for insurance pricing. The Koshi basin – which alone hosts the Tamakoshi, Dudh Koshi, Arun, and Tamor sub-basins containing projects totaling several thousand MW of capacity – carries a GLOF risk that is categorically different from all other basins. Yet under Nepal’s current flat tariff regime, a project operating in the Koshi basin pays the same 0.20% base rate as one operating in the relatively safer Karnali basin.

The table also confirms the cascade risk profile identified in The Cascade Effect. The Gandaki basin hosts major storage projects (Kali Gandaki A, Upper Myagdi, Tanahu Seti) exposed to both high drought risk and medium earthquake/landslide risk simultaneously. An extended dry season that depletes reservoir levels, followed by a monsoon landslide that blocks an intake, represents a compound exposure that no current insurance product in Nepal explicitly prices or even acknowledges.

The RPGCL Master Plan data, synthesized in Table 4 of the IRRP Report, identifies the specific hydropower clusters at risk in each corridor – from the Karnali-West Seti-Mahakali corridor (West Seti 750 MW, Chainpur Seti 210 MW) to the Koshi-Arun-Kabeli corridor (Arun III 900 MW, Upper Arun 1,063 MW, Dudhkoshi 635 MW). The World Bank has categorized Upper Arun’s environmental and social risks as “High” (Upper Arun Hydropower Project, World Bank Project Page P178722), a classification that has direct implications for insurance requirements under World Bank’s Environmental and Social Framework.

4. Legal Obligations: What Insurance Is Required and by Whom

4.1 Mandatory Insurance Under the Power Purchase Agreement

Nepal’s standard PPAs contain a dedicated insurance clause. Section 27 of the Tamakoshi V Power Purchase Agreement between Nepal Electricity Authority and Tamakoshi Jalvidhyut Company Limited sets out the following requirements (Section 27, Tamakoshi V PPA, Nepal Electricity Authority; see also: What does a RoR PPA contain?):

Pre-Commercial Operation Phase (Section 27.1): The Company is required to maintain insurance before commercial production commences covering:

- (a) Contractor’s all risks, in an amount not less than the total contract value

- (b) Third-party liability

- (c) Workers’ compensation and similar employee liabilities

- (d) Any other insurance required by prevailing law

Post-Commercial Operation Phase (Section 27.2): Within three months of commercial production commencing, the Company must insure:

- (a) Project structures, machinery, tools, and equipment at not less than the project’s replacement cost

- (b) Third-party liability

- (c) Workers’ compensation and similar employee liabilities

- (d) Any other insurance required by prevailing law

Annual Compliance (Section 28): The Company must provide NEA with a copy of current insurance certificates and renewal documentation within one month of the start of each fiscal year.

Analysis of PPA Requirements Against Identified Risks. The PPA requirements are structured around minimum thresholds – replacement cost for physical assets, third-party liability, workers’ compensation – without specifying perils, deductible limits, indemnity periods, or business interruption coverage. Critically, the PPA makes no mention of Loss of Profit/Business Interruption insurance, the single most financially consequential product for a project-financed asset whose debt service continues regardless of whether the plant generates power. The PPA’s silence on BI/LOP means that developers can technically satisfy PPA compliance with a physical damage-only policy, leaving the debt service gap entirely uncovered.

The PPA equally makes no reference to GLOFs as a specific insured peril, despite Upper Tamakoshi’s documented exposure to Tsho Rolpa and Imja Tsho. For projects in the Koshi basin, this gap means that the PPA’s insurance clause provides no guidance on whether the project’s lenders can achieve “bankable” coverage for the sector’s most severe emerging risk.

4.2 Mandatory Insurance Under Loan Covenants

The regulatory framework for the mandatory insurance of collateral in Nepal, specifically within the context of consortium financing and infrastructure projects, is structured to ensure that the risk of asset loss is fully mitigated before and during the loan term.

Based on the NRB Unified Directives (2081/2082) and the Capital Adequacy Framework, here is a detailed breakdown of these binding requirements.

General Obligation to Insure Collateral (Directive 21/2081, Clause 1): For Class A, B, and C institutions, the NRB mandates that all physical assets accepted as security must be adequately insured.

- Borrower Choice: While insurance is mandatory, the borrower has the legal right to choose any licensed insurance company of their preference to issue the policy.

- BFI Responsibility: The bank must ensure that the policy is issued in its favor (loss payee) and that the coverage is sufficient to protect the bank’s interest in the event of damage or destruction of the collateral.

Lead Bank’s Duty in Consortiums (Directive 11/2081, Clause 8): In a consortium (joint) financing arrangement, which is mandatory for multi-banking exposures reaching Rs. 2 Billion or more, the Lead Bank holds the primary administrative responsibility for security perfection.

- Centralized Perfection: According to Directive 11, Clause 8, the Lead Bank is responsible for “arranging the mortgage/security blocking and performing all activities related to insurance and other measures to secure the investment”.

- Maintenance of Interest: This includes ensuring that insurance endorsements are valid, premiums are paid, and the bank’s interest is explicitly noted on all relevant project asset policies throughout the consortium period.

Energy Sector Specifics: 100% Insurance Rule (Directive 2/2081, Clause 37): This clause provides a unique exemption from mandatory consortium financing for energy-related hire-purchase services, provided strict insurance and loan-to-value (LTV) conditions are met.

- The Exemption: BFIs are not required to form a formal consortium for loans to authorized energy hire-purchase entities for machinery or vehicles if the loan amount is up to 50% of the purchase value.

- Insurance Requirement: To qualify for this exemption, the BFI must ensure that 100% of the asset’s full value is compulsorily insured. This ensures that even if the bank is only financing half the cost, the entire physical asset is protected against risk.

NIFRA Infrastructure Project Insurance (NIFRA Directive 2/2082, Clause 2): For the Infrastructure Development Bank (NIFRA), the rules emphasize project-wide compliance and cashflow safety.

- Statutory Compliance: Under Directive 2, Clause 2, NIFRA must ensure that all infrastructure projects comply with “relevant acts, rules, and policies,” which includes mandatory asset insurance requirements.

- Construction & Operation Phases: In project finance, NIFRA and participating lenders must ensure that project assets (civil works, machinery, and equipment) are insured for their full value during both the construction phase (Contractors All Risk – CAR) and the operational phase to safeguard the project’s future cash flows.

Prudential Penalties and Monitoring: The directives impose strict monitoring and provisioning rules to ensure these insurance requirements are not ignored:

- Renewal Tracking: BFIs must monitor policy expiration. If a borrower fails to renew a policy, the BFI is authorized to renew it 15 days before expiry and charge the borrower’s account [Directive 21/2081].

- Impact on CRM: To claim capital relief (Credit Risk Mitigation) under the Capital Adequacy Framework, “Legal Certainty” must be established. If a bank fails to perfect its security – including missing insurance endorsements – it may be denied capital relief, forcing the exposure to be risk-weighted at the full rate (100%–150%).

- Classification: Failure to maintain proper insurance on movable collateral (like stock or machinery) during physical inspections can lead to the loan being classified as “Loss”, requiring 100% provisioning.

| Directive | Institution/Sector | Mandatory Action | Exact Wording/Condition |

| 21/2081, Cl. 1 | Class A, B, C | General Collateral | BFIs must ensure assets are adequately insured. |

| 11/2081, Cl. 8 | Consortium (ABC) | Lead Bank Duty | Perform all activities related to insurance/security. |

| 2/2081, Cl. 37 | Energy Hire-Purchase | Consortium Exemption | 100% of asset value must be insured. |

| 2/2082, Cl. 2 | NIFRA (Infrastructure) | Project Assets | Ensure full value insurance for both phases. |

On minimum deductible thresholds: there is no numerical deductible floor (e.g., “maximum NPR 5 million per claim”) specified in NRB or BAFIA 2073 provisions. The threshold is market practice, governed by NIA’s minimum deductible regulations for CAR/EAR policies. But it is normal for lenders to require that actual deductibles remain “manageable”. Any reinsurer-imposed deductible substantially above the comfort level of lender interfering with DSCR covenants – such as the documented case of an “excess of 50% of Sum Insured” for one project (The Cascade Effect, Section 10.2: The “High Hazard” Trap) – could render the policy unbankable.

The NRB framework thus creates the following obligations: the Lead Bank must arrange insurance; the full replacement value must be covered; and the policy must have bankable deductibles. What the NRB framework does not do is specify which perils must be covered, what indemnity periods are required for business interruption, or how GLOFs should be treated. These critical specifications are left entirely to market practice and reinsurer appetite – which, as documented in The Cascade Effect, is increasingly hostile to Nepal’s high-hazard basins.

4.3 Mandatory Insurance Under Nepal Insurance Law

The core legal framework governing hydropower insurance is the Insurance Act 2079 (2022), the Property Insurance Directive 2080, and the NIA’s Minimum Premium Rate for Non-Tariff Insurance Business Guidelines. A critical contextual point must be stated at the outset: the Hydropower Development Policy 2001 and the Electricity Act 1992 contain no specific insurance mandates (The Cascade Effect, Section 2.5: Policy Gaps and Sovereign Risk). The Insurance Act is therefore the primary and in practice the only sector-specific legal framework.

Construction Phase: Hydropower construction falls under Engineering Insurance – a Non-Tariff regime governed by NIA minimum guidelines. Key provisions:

- CAR policies must include minimum excess of 5% of claim amount or 0.50% of Sum Insured for normal losses, and 10% of claim amount or 1% of Sum Insured for Act of God claims – whichever is higher (NIA Minimum Premium Rate for Non-Tariff Insurance Business Guidelines).

- Maximum Maintenance Period standard extension: 12 months for CAR, 6 months for EAR testing period (NIA Compilation of Decisions, Vol. 9).

- Under Public Procurement Regulation 2064, Rule 112: Any public construction work exceeding NPR 10 lakh must be insured, covering replacement cost of construction materials, professional fees, debris removal (up to 5% of replacement cost), and third-party liabilities.

Operational Phase: Property Insurance – governed by a strict Tariff Regime under Property Insurance Directive 2080.

- Basic Premium Rate for hydropower: NPR 2.00 per thousand (0.20%) of Sum Insured (Property Insurance Directive 2080, Schedule 15).

- Mandatory deductible for Act of God claims (earthquake, water-borne): 5% of assessed claim amount; for all other causes: 1% of assessed claim amount.

- Consequential Loss (Loss of Profit) add-on rates per Schedule 15: 3 months = 2.50/thousand; 6 months = 4.00/thousand; 9 months = 5.00/thousand; 12 months = 6.00/thousand.

- RSMDST add-on for LOP coverage: 0.30/thousand (3-6 months); 0.50/thousand (9-12 months).

- Riot & Strike (RS): Covers physical loss or damage caused by people taking part in a disturbance of the public peace or employees involved in a labor dispute.

- Malicious Damage (MD): Covers damage caused by the intentional “malicious” act of any person (e.g., vandalism to a hydropower powerhouse).

- Sabotage & Terrorism (ST): This is the most critical for infrastructure projects. It covers acts committed for political, religious, or ideological purposes aimed at overthrowing or influencing a government.

- Risk-Based Pricing transition: Clause 27 of the Property Insurance Directive 2080 mandates Risk-Based Pricing for natural catastrophe risks for commercial, industrial, and public properties, with premiums to be determined by geographical location, construction type, and usage – effective from Shrawan 2081 BS.

Claim Settlement Timeline: Section 65 of Insurance Act 2079 mandates claim settlement within 15 days of surveyor final report submission. Delays require written explanation. NIA has authority to intervene if surveyor report is delayed beyond 15 days from site visit (The Cascade Effect, Section 2.3).

Reinsurance Retention Limits: The regulatory framework governed by the Nepal Insurance Authority uses a highly calculated strategy to protect market solvency while forcing domestic reinsurers to mature. First, to prevent bankruptcy from catastrophic claims, a non-life insurer is legally capped at retaining only 5% of its net worth per single risk or policy, as explicitly mandated under Section 6(2) (Reinsurance Retention) of the Reinsurance Directive, 2080. This forces the insurer to pass the vast majority of its liability to the reinsurance market if its net worth capacity does not allow. Historically, the regulator forced primary insurers to hand over a slice of this risk directly to domestic reinsurers as an automatic, un-negotiated “Direct Cession”. However, to end this era of guaranteed “free handouts,” the regulator is aggressively phasing this direct cession down. According to the mandatory schedule outlined in Section 7(1) of the directive, this automatic allocation drops from 10% (applicable up to FY 2079/80) to exactly 0% by FY 2084/85, signaling that domestic reinsurers can no longer passively collect a share of every policy without effort.

While the automatic handout is disappearing, the regulator simultaneously enforces a strict protective wall for domestic capacity. Under Section 8(1) (Reinsurance with Domestic Reinsurers) of the Reinsurance Directive, 2080, and reinforced by its First Amendment, primary insurers are legally required to allocate at least 30% of their “remaining portion” of treaty reinsurance to domestic reinsurers before they are permitted to access international markets. This is the profound shift: it guarantees that domestic reinsurers still capture a massive 30% baseline of the market – which successfully prevents national capital from fleeing Nepal – but forces them to actually earn it. Because this 30% must now be secured through negotiation rather than an automatic tax, domestic reinsurers are forced to sit at the table, professionally evaluate risks, establish competitive pricing, and justify their capacities just like international reinsurers do, ultimately transforming them into globally competitive institutions.

Capital Adequacy: Under Risk Based Capital and Solvency Directive 2025 (2082), Annexure III, Section 5(52):

- Engineering LOB: Risk Factor for Outstanding Claims (Rfc) = 20%; Risk Factor for Earned Premiums (Rfp) = 25%.

- Catastrophe risk factor applied to Earthquake Premium Reserve (EPR) + Earthquake Risk Exposure (ERE) = 1.25.

- EPR must accumulate at 15% of net earthquake premiums annually, capped at 150% of the highest gross premium over the preceding five years.

Foreign Reinsurer Rating Requirements: Enlistment Guidelines for Foreign Reinsurers and Reinsurance Brokers 2024: Treaty Leaders require minimum AM Best A-, S&P A-, Moody’s A3, or Fitch A-. Facultative reinsurers require AM Best B, S&P BBB, Moody’s Baa1, or BBB Fitch. Class B CAR/EAR/ALOP/MCEAR-specific extension applies per Section 21(3) of Reinsurance Directive 2080.

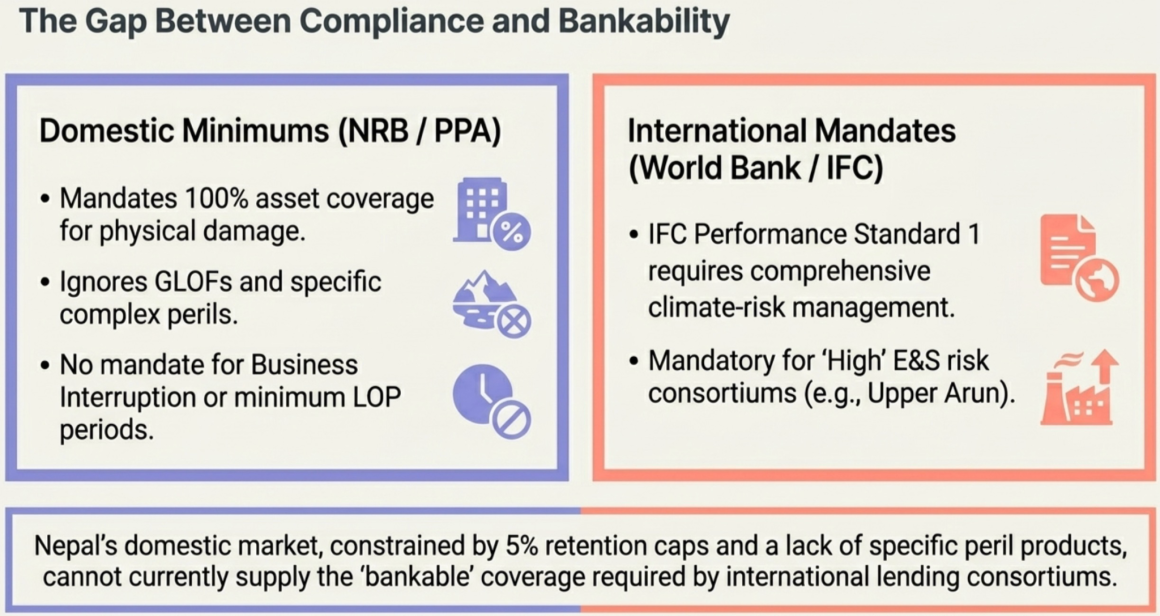

4.4 IFC, World Bank, and ADB Standards

The IFC Performance Standards (2012) do not contain explicit mandatory insurance coverage specifications in the sense of minimum deductibles or required perils lists. However, PS1 (Assessment and Management of Environmental and Social Risks) requires the client to implement an Environmental and Social Management System addressing risks and impacts across the project lifecycle, including climate change vulnerability (IFC Performance Standard 1, January 2012, paragraphs 7 and 20-21). For a hydropower project in a climate-sensitive area – which PS1’s Guidance Note explicitly defines as those potentially affected by extreme weather events, floods, and droughts – the client must identify direct and indirect climate-related adverse effects and incorporate climatologic data into infrastructure design.

PS1’s climate risk identification requirement, when applied to Nepal’s hydropower context, creates an implicit insurance obligation: if the client has identified GLOF risk, landslide risk, or extreme monsoon risk as material to its risk management framework, lenders financing the project under IFC standards will require that this identified risk be managed – which in practice means insured or hedged. The World Bank’s categorization of Upper Arun Hydropower Project as “High” environmental and social risk (WB Project P178722) similarly implies that any financing package for the project will carry commensurate insurance requirements that go beyond Nepal’s domestic PPA or NRB minimums.

In practice, IFC’s involvement in Nepal’s hydropower sector has focused primarily on environmental and social standards rather than financial insurance requirements. IFC’s Nepal Environmental and Social Hydropower Program (2016-2023) benefited 67 projects producing 3,919 MW (IFC Press Release, June 13, 2023). The IFC led a USD 453 million international credit facility for the 216 MW Upper Trishuli 1 project in 2019 – Nepal’s first internationally financed private hydropower project at that scale. That project’s insurance requirements, structured to international project finance standards, would have required comprehensive CAR coverage during construction and full property plus BI/LOP coverage at operation – at terms and deductible levels acceptable to Korean and international lenders rather than Nepal’s domestic NRB minimums alone.

ADB and World Bank have jointly committed to financing Upper Arun (1,063 MW, estimated USD 2.24 billion) and Dudhkoshi (635 MW), formalizing their collaboration in a December 2023 MOU at COP28 (ADB-World Bank MOU Press Release, December 6, 2023). For these projects, World Bank’s Environmental and Social Framework will apply, requiring – at minimum – full property insurance, comprehensive third-party liability, and documented climate-risk management protocols. The gap between these implied requirements and what Nepal’s domestic insurance market can currently deliver (given reinsurer capacity constraints, the 5% retention cap, and the documented tendency to impose unbankable deductibles for high-hazard projects) is a financing risk that neither the World Bank nor the ADB has yet formally addressed in their project documentation.

Bhutan provides a comparative reference point. The World Bank-approved USD 40 million Catastrophe Deferred Drawdown Option (Cat DDO) for Bhutan (December 2024) mandates that all new hydropower projects adopt a catchment-wide approach to disaster risk management, including integrated geohazard assessment and DRM action planning as prerequisites for financing (World Bank Press Release, December 11, 2024). Notably, a World Bank briefing note on Bhutan explicitly states that “buildings and infrastructure, except hydropower plants, are insured” – suggesting that even in Bhutan, which shares Nepal’s Himalayan risk profile, hydropower plants represent an insurance gap (World Bank Crisis Preparedness Gap Analysis Bhutan Briefing Note, 2025). Bhutan relies on General Reserves rather than commercial insurance for hydropower disaster recovery, though the Cat DDO provides a sovereign-level contingent facility. Nepal has no equivalent contingent credit line. The key governance difference is that Bhutan’s Department of Energy mandates that DGPC adhere to guidelines that incorporate comprehensive risk management strategies addressing earthquakes, floods, cloudbursts, and landslides at the catchment level (World Bank Bhutan Cat DDO Documentation, 2024). Nepal’s equivalent – the NDRRMA framework – does not yet contain mandatory insurance protocols for hydropower infrastructure.

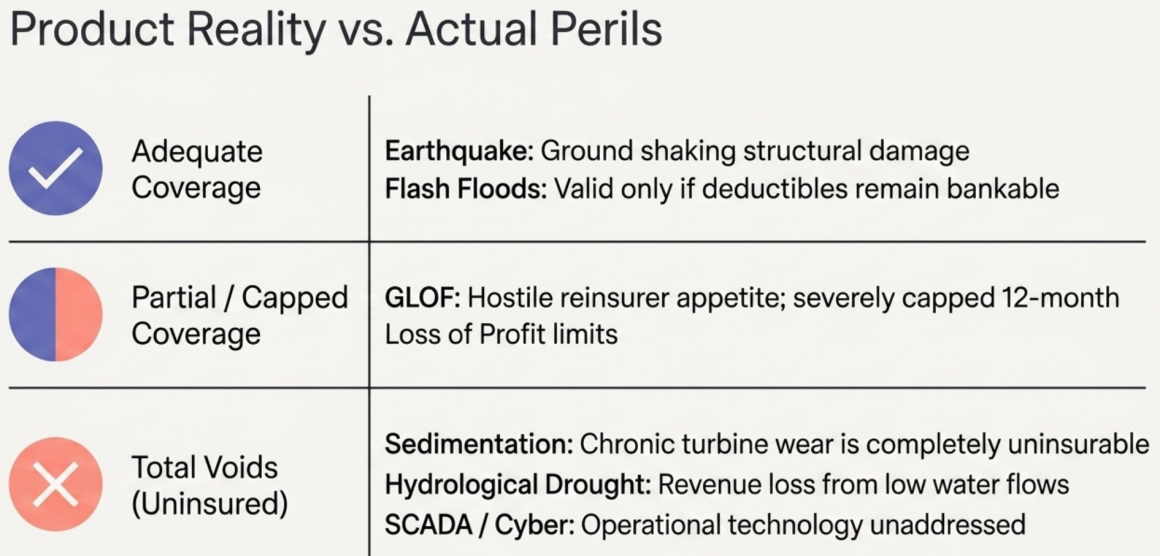

5. Coverage Gap Analysis: Products Available vs. Risks That Exist

This is the critical section of this post. The two actual insurance policy documents available for analysis – the property insurance schedule and the Loss of Profit policy issued by Sanima GIC Insurance Limited, policy dated December 2025 – are for a solar project. They are, however, issued under the same legal framework and rate schedules that govern hydropower property and LOP insurance in Nepal. The analysis that follows treats them as representative of what the Nepalese market delivers to energy infrastructure projects, which is consistent with the uniform tariff regime under Property Insurance Directive 2080 Schedule 15.

5.1 The Property Insurance Policy: Covered vs. Required

What the standard Nepal property insurance covers (confirmed from Property Insurance Directive 2080 and Ridi Power/Sanima GIC schedule):

| Covered Peril | Relevant Hydropower Risk |

| Fire, lightning, explosion | Powerhouse fire, boiler explosion |

| Earthquake | Ground shaking damage to intake structures, penstocks |

| Flood and inundation (Baadhi/Duban) | Flash flood damage to headworks, powerhouse |

| Landslide/subsidence (Pahiro/Bhasine) | Slope failure burying intakes and access roads |

| Windstorm, cyclone, tornado | Wind damage to transmission towers, cooling systems |

| Aircraft/aerial object impact | Low relevance for most Himalayan sites |

| Impact by vehicle/animal | Access road accidents |

| Self-ignition/spontaneous combustion | Transformer fires |

| RSMDST (optional add-on) | Vandalism, terrorism |

What the standard policy explicitly excludes:

| Excluded | Gap Against Identified Hydropower Risk |

| Consequential loss (business interruption) | Entire revenue loss during any shutdown – unless LOP add-on purchased |

| Machinery breakdown/electrical fault | Turbine bearing failure, generator short circuit, SCADA failure |

| Gradual deterioration/wear | Turbine runner erosion from sedimentation – the chronic risk |

| Transmission line failure | Revenue loss from NEA grid disconnect – explicit exclusion in LOP |

| Theft and burglary | Equipment theft at remote sites |

| Computer data/software loss | SCADA system data corruption |

| War, nuclear, radioactivity | Low relevance domestically |

| Third-party property damage | Covered separately under TPL add-on |

Critical gap: Sedimentation is entirely absent from both covered and excluded lists. Sedimentation is a chronic, high-frequency cause of turbine degradation and forced operational downtime in Nepal’s hydropower sector. It is not covered as physical damage (not a sudden event), not covered as mechanical breakdown (excluded from property policy), and not covered as business interruption (since no physical damage trigger exists). It exists in a complete coverage void.

Critical gap: GLOF is not listed as a separate insured peril. GLOF events could technically trigger “flood and inundation” coverage, but their scale – releasing surges of water and debris that far exceed spillway design capacity (IRRP Report 2022, Section: Generation Vulnerabilities) – means they generate losses that combine structural damage (potentially covered), debris removal (partially covered under CAR endorsement up to a sub-limit), and prolonged business interruption (covered only if LOP add-on was purchased). The structural damage and debris removal sub-limits typical in Nepal’s policies (e.g., NPR 3 million for debris removal, as seen in the Upper Dordi A case) are entirely inadequate for a GLOF event.

5.2 The Loss of Profit Policy: Covered vs. Required

Trigger condition confirmed from Ridi Power LOP (Sanima GIC, December 2025): Payout requires (1) physical damage under the underlying property policy, (2) resulting business interruption, and (3) payment or admitted liability under the property policy. The policy explicitly excludes loss due to transmission line failure.

Confirmed terms from Ridi Power LOP Schedule:

- Sum Insured: NPR 105,927,263

- Period of Indemnity: 6 months

- Deductible/Excess: 30 days

- Premium: NPR 619,674.49 (+ Pool NPR 31,778.18 = NPR 651,452.67 + VAT)

- Perils covered: Loss of revenue (excluding transmission line loss)

Gaps against identified risks:

| Risk Scenario | LOP Coverage Status |

| Flood destroys headworks → 4-month shutdown | Covered – if physical damage admitted under property policy |

| Mechanical bearing failure → 3-month shutdown | Covered – if MBI is held and admitted as physical damage trigger |

| GLOF event → 18-month reconstruction period | Partially covered – only if 12-month indemnity period was purchased; extended reconstruction not covered |

| Drought/low river flow → 30% revenue loss | Not covered – no physical damage event; hydrological shortfall is not an insured peril |

| NEA transmission line damaged → plant cannot evacuate power | Explicitly excluded – “excludes loss due to transmission line” (Ridi Power LOP, Perils Covered section) |

| Sedimentation-forced desander flushing → 2-day shutdowns × 30/year | Not covered – no physical damage trigger; chronic operational issue |

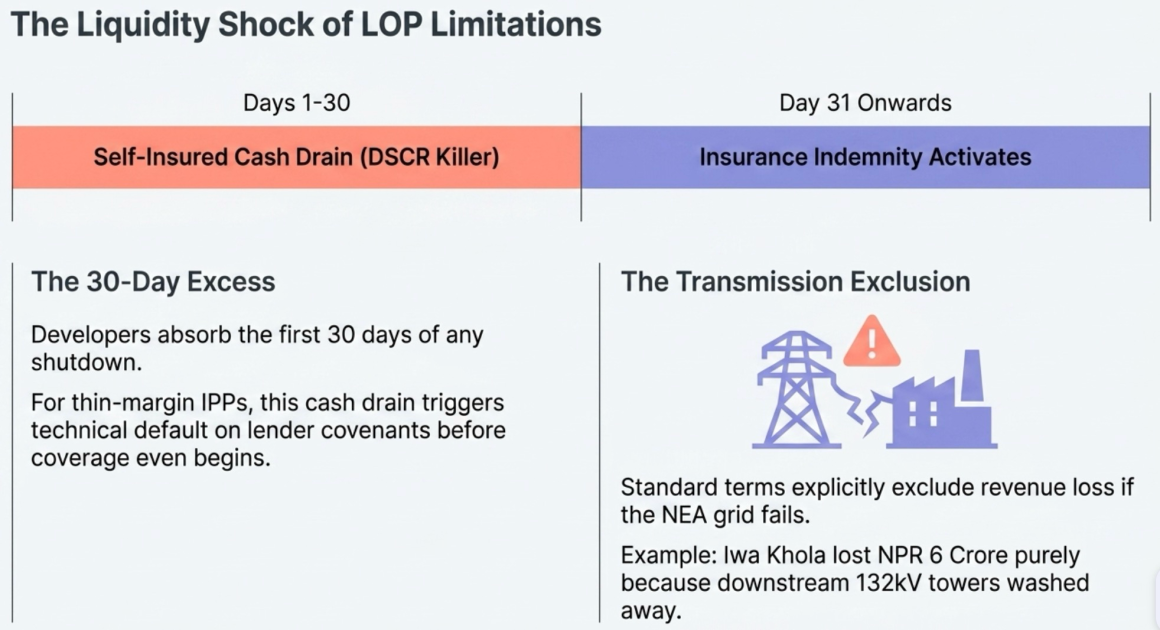

| 30-day excess period | Self-insured gap – developer absorbs first 30 days of any shutdown with zero LOP recovery |

The 30-day excess period deserves particular emphasis. For a project with NPR 100 million annual revenue, the first 30 days of any shutdown costs approximately NPR 8.2 million – entirely unindemnified. For small IPPs operating on thin margins, this immediate cash drain during the period before insurance activates is precisely the liquidity shock that drives DSCR below 1.0x and triggers technical default on bank covenants.

The transmission line exclusion is equally significant. The 9.9 MW Iwa Khola Hydropower Project suffered an estimated NPR 6 crore income loss solely because five towers of the NEA-owned Kabeli Corridor 132 kV transmission line were damaged by the 2024 floods (Nepal Hydropower Flood Damage Assessment Report September 2024, SN 18). Under current standard LOP terms, this loss is entirely unindemnified regardless of the duration or magnitude.

Table 2: Summary – Coverage Gap Matrix for Hydropower Generation

| Risk Category | Property Insurance | LOP/BI Insurance | CAR (Construction) | Coverage Verdict |

| Earthquake structural damage | Covered | Via trigger | Covered | Adequate |

| Flash flood physical damage | Covered | Via trigger | Covered | Adequate if deductibles bankable |

| GLOF – total loss scenario | Covered (if reinsurer accepts) | Via trigger, 12-month cap | N/A | Inadequate – reinsurer often excludes; LOP cap too short |

| Landslide – cascade to flood | Covered (proximate cause precedent) | Via trigger | Covered | Adequate if proximate cause documented |

| Sedimentation/turbine wear | Not covered | Not triggered | Not covered | Gap – complete void |

| Machinery breakdown (internal fault) | Excluded | Via MBI add-on | N/A | Covered only if MBI separately purchased |

| Hydrological shortfall (drought) | Not covered | Not triggered | N/A | Gap – requires parametric solution |

| NEA grid/transmission failure | Not covered | Explicitly excluded | N/A | Gap – systematic, uninsured |

| Cybersecurity/SCADA failure | Not covered | Not triggered | Not covered | Gap – complete void |

| Extended reconstruction (>12 months) | Covered (physical) | Capped at 12 months LOP | N/A | Partial gap – reconstruction may exceed LOP cap |

| Cascade debris from upstream | CAR: covered if proximate cause accepted | Via trigger | Covered (Upper Dordi A precedent) | Adequate with proper claim documentation |

| Workers’ compensation | Separate mandatory policy | N/A | Separate mandatory policy | Legally mandated – generally compliant |

6. Transmission and Distribution: The Sector Operating Without Insurance

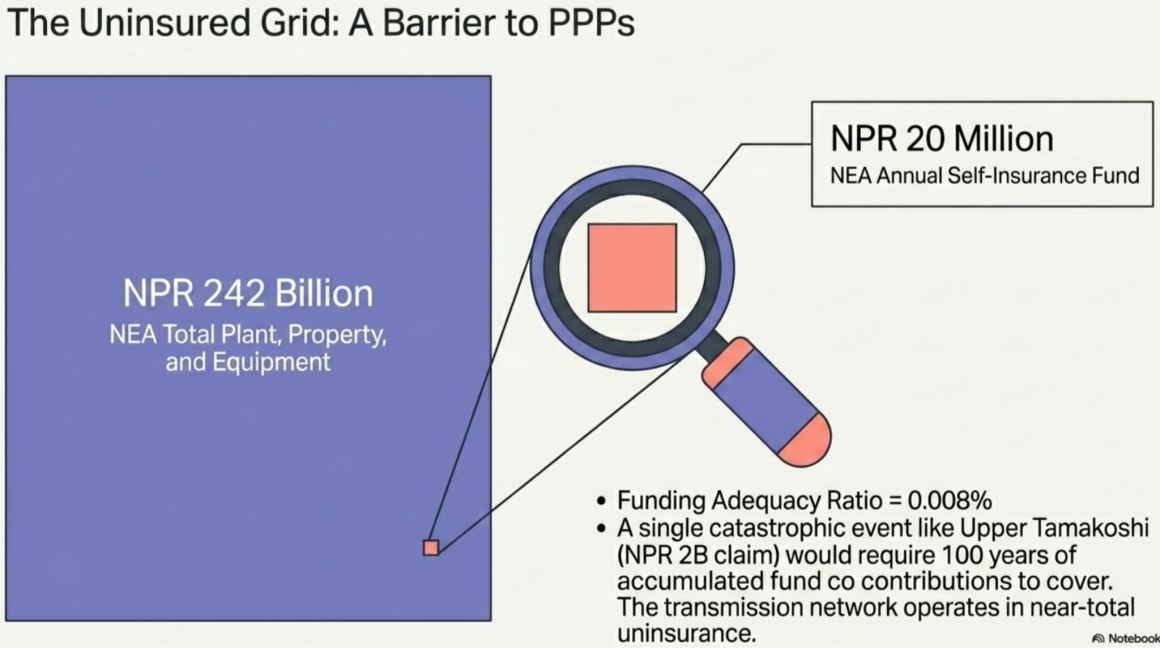

This section requires separate treatment because the insurance gap here is not a matter of product inadequacy – it is an absence of product entirely combined with a self-insurance mechanism that is, by any actuarial or financial standard, deeply inadequate.

6.1 The NEA Self-Insurance Fund: The Numbers

NEA maintains an internal Insurance Fund with an annual contribution policy of NPR 20 million (NPR 2 crore), provided the authority operates at a profit (NEA Financial Statements FY 2024/25; The Cascade Effect, Section 3: Insurance Coverage for NEA’s Hydropower Projects). Against this, the figures are stark:

| Metric | Value | Source |

| NEA Total PPE (FY 2024/25, provisional) | NPR 242.0 billion | NEA Financial Statement FY 2024/25 |

| NEA Total Assets | NPR 683.9 billion | NEA Financial Statement FY 2024/25 |

| Annual Insurance Fund Contribution | NPR 20 million (NPR 2 crore) | NEA Accounting Policy |

| Fund as % of PPE | 0.008% | Calculated |

| Fund as % of Total Assets | 0.003% | Calculated |

| Typical IPP property insurance rate | 0.20% base + 0.60% LOP = ~0.80% | Property Insurance Directive 2080, Schedule 15 |

| Equivalent annual insurance cost at IPP rates | NPR ~1.94 billion (on PPE alone) | Calculated at 0.80% of NPR 242 billion |

| Funding adequacy ratio | ~1% (NPR 20 million vs NPR 1.94 billion) | Calculated |

NEA’s operational self-insurance mechanism funds at approximately 1% of what equivalent commercial insurance would cost. A single major flood event – comparable to the NPR 2 billion claim from Upper Tamakoshi in 2024 – would require 100 years of accumulated fund contributions to cover. This is not a funding gap; it is a funding void.

6.2 The Regulatory Gap: No Product Exists

The analysis of NIA’s full product catalogue confirms: there is no specific insurance product, directive, tariff, or guideline issued by the NIA that specifically addresses transmission line insurance or substation insurance as a standalone category for NEA or similar utilities (NIA Annual Reports, all volumes; NIA Compilations of Decisions, all nine volumes reviewed). Transmission and distribution assets are absorbed into the broader Engineering Insurance and Property Insurance categories, without any hydropower-transmission-specific rating schedule, mandatory coverage requirement, or dedicated product design.

The only documented claim involving NEA transmission infrastructure in the NIA’s Compilation of Decisions is the Mudbhari and Joshi Construction case (Compilation of Decisions, Vol. 5) – a contractor’s Marine Cum Erection claim for a transformer in transit, not an NEA operational claim. This single case is the sole evidentiary marker of any commercial insurance touching NEA’s transmission network in all nine volumes of NIA regulatory decisions.

6.3 The PPP Transition: Why This Is Now Urgent

The Government of Nepal, through RPGCL, is in the process of restructuring its transmission sector toward Public-Private Partnership models, with multiple 400 kV transmission corridors identified for private participation under the RPGCL Master Plan 2018 (IRRP Report 2022, Table 4). The ADB-World Bank MOU of December 2023 explicitly identifies transmission infrastructure financing alongside Upper Arun and Dudhkoshi as a sector priority.

When transmission infrastructure moves into a PPP/private investment model, the insurance requirements that currently do not exist will be immediately demanded by lenders. Any PPP transaction for a 400 kV transmission corridor will require, at minimum, Construction All Risk insurance during the construction phase and Property Insurance plus Business Interruption coverage during operation – at terms acceptable to an international lending consortium. Nepal’s insurance market currently has no product, no tariff, and no demonstrated claims-handling capacity for transmission infrastructure at this scale.

The urgency is compounded by the cascading financial impact: as Upper Tamakoshi’s LOP policy explicitly excludes transmission line failure, and as the September 2024 event destroyed a 220 kV tower that was part of the project’s evacuation infrastructure, the distinction between generation and transmission risk is already blurring in practice. A project that cannot evacuate power because its dedicated transmission link is destroyed has suffered a total business interruption – but can claim only partial physical damage and zero LOP for the transmission component.

Policy prescription: The NIA must, as a priority regulatory action, develop a dedicated Transmission Infrastructure Insurance Product under the Property Insurance Directive, with separate tariff schedules distinguishing between: (a) 400 kV backbone transmission, (b) 220 kV regional interconnectors, (c) 132 kV project-specific evacuation lines, and (d) substations. Each category requires differentiated geographic zone loadings, separate deductible structures, and specific Business Interruption trigger conditions that account for the grid’s role as essential infrastructure for multiple generating projects simultaneously.

7. Pricing Analysis: From Loss Data to Actuarial Tariff

7.1 Available Loss Data and Its Limitations

Nepal’s available loss data for hydropower insurance pricing comes from three sources, each with significant limitations:

Source 1: NIA Annual Reports – Engineering and Property Portfolio Aggregates

| FY | Engineering Premium (NPR Crore) | Engineering Claims (NPR Crore) | Implied Loss Ratio |

| 2077/78 | 306.47 | Not isolated | N/A |

| 2080/81 (Full Year) | 710.37 | 363.68 | ~51.2% |

Fire/Property Portfolio (proxy for operational hydro):

| FY | Property Premium (NPR Crore) | Property Claims (NPR Crore) | Implied Direct Loss Ratio |

| 2080/81 | 1,144.72 | 256.01 | 22.36% |

| 2072/73 (post-earthquake) | Subset of NPR 1,504 total | 862.72 (earthquake claims only) | >200% (Fire portfolio) |

(Sources: NIA Annual Report 2080/81; A Study on Reinsurance Practice in Nepal, 2019; NotebookLM 2 response to Market Capacity and Loss Statistics questions)

Source 2: Hydropower-Sector Specific Data

The hydropower sector-specific figure of NPR 1.25 billion premiums versus NPR 2.63 billion claims – a 210% loss ratio – comes from industry-level data presented in the “Insurance and Reinsurance in Energy Sector of Nepal” presentation (Pujan Dhungel Adhikari). This figure represents the hydropower-specific portfolio, not the broad Engineering or Property portfolio. The NIA does not separately disaggregate hydropower as a line of business in its annual reporting, meaning the 210% figure represents industry knowledge rather than published regulatory statistics.

Source 3: Event-Level Loss Data

The most precise data comes from documented individual events:

- Upper Tamakoshi September 2024: NPR 1.79 billion physical damage + NPR 1.43 billion lost income = NPR 3.22 billion total; insurance claim submitted approximately NPR 2 billion (Nepal Hydropower Flood Damage Assessment Report September 2024, SN 24)

- Madhya Bhotekoshi: NPR 1.34 billion net claim under EAR (02-Insurance and Reinsurance in Energy Sector presentation)

- Panauti Hydropower Center (NEA): NPR 15.5 crore estimated loss, including destruction of VCBs, AC-DC panels, unit control boards, PLCs, SCADA (Nepal Hydropower Flood Damage Assessment Report September 2024, SN 22)

- Super Hewa Khola (5 MW): near-total asset loss, reconstruction timeline indefinite (Hydropower Disaster Damage Report, Table 1)

- Upper Hewa Khola (8.5 MW): NPR 950 million infrastructure damage, 6-month production halt (Hydropower Disaster Damage Report, Table 1)

- Total documented losses from September 2024 floods: Multiple projects across basins (Nepal Hydropower Flood Damage Assessment Report September 2024)

Limitation statement: The absence of hydropower-specific line-item data in NIA’s published Annual Reports means actuarial pricing models for this sector must rely on triangulation between the broad Engineering/Property portfolio loss ratios, the industry-specific 210% loss ratio estimate, and event-level documented losses. Any pricing model built on this data carries substantial estimation uncertainty. This is itself a major data governance failure – one that the NIA’s Clause 27 risk-based pricing transition must address by creating a mandatory sector-specific reporting requirement.

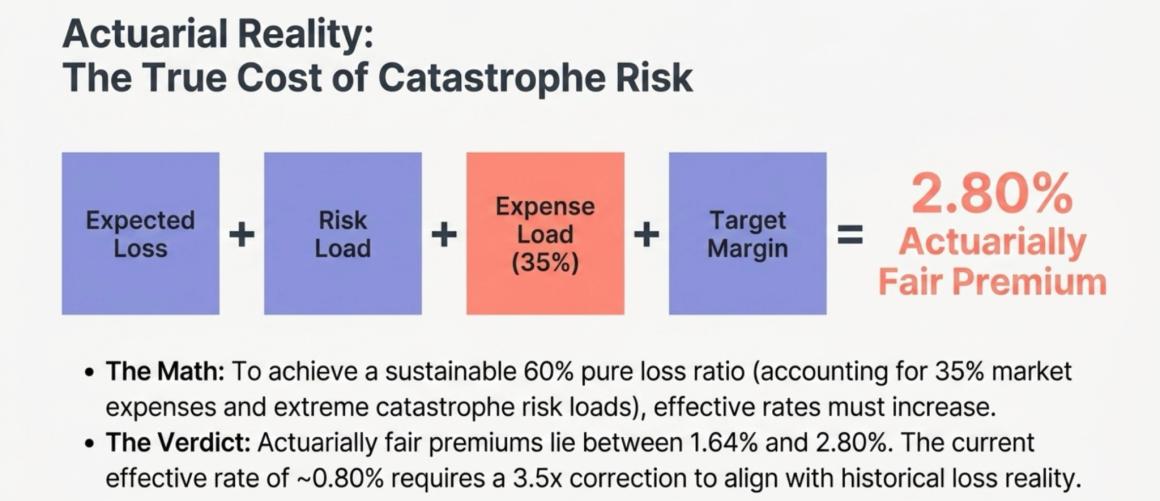

7.2 Academic Pricing Model: Theoretical Framework

The academic framework for pricing catastrophe-exposed infrastructure insurance follows a four-component structure: Expected Loss + Risk Load + Expense Load + Profit Margin.

Expected Loss Component (EL)

EL = Σ (Probability of Event_i × Expected Loss Given Event_i)

For a Nepal hydropower project, the relevant event categories and indicative annual probabilities are:

| Event Type | Return Period (years) | Annual Probability | Source/Basis |

| Major flood (localized) | 5-10 | 10-20% | Historical frequency from NDRRMA reports; IPPAN damage data |

| Cascade flood (basin-wide) | 20-30 | 3-5% | 2015, 2021, 2024 events; IRRP risk matrix |

| Damaging earthquake (M6.0+) | 40-50 | 2-2.5% | Nepal has 10% chance of damaging earthquake in 50 years (IRRP Report 2022, Section: Earthquakes) |

| GLOF event (Koshi basin) | 50-100 | 1-2% | 47 potentially dangerous lakes; Tsho Rolpa “probable” assessment (IRRP Report 2022, Box 8) |

| GLOF event (other basins) | 200-500 | 0.2-0.5% | 1 potentially dangerous lake each in Gandaki/Karnali |

| Sedimentation-forced shutdown | Annual | 100% (chronic) | Not insurable under current framework |

| Hydrological shortfall | 3-5 (low water year) | 20-33% | Climate data; Super Mai 2024-25 case |

Risk Load Component (RL)

The Risk Load adjusts for variance in outcomes. For catastrophe-exposed risks, actuarial practice applies a risk margin of 25-50% of Expected Loss for the catastrophe component, reflecting that losses cluster in bad years. Nepal’s documented experience – near-zero claims in good years, followed by NPR 2 billion claims from a single event – validates a high risk-load coefficient.

Expense Load (EL)

Industry expense ratio for Nepal’s non-life sector: approximately 35% of net premium (inferred from NIA Annual Reports and reinsurance study data). This is relatively high by international standards, reflecting the small market size, distribution costs, and regulatory compliance overhead.

Profit Margin Target

For solvency under RBC Directive 2082, the target solvency ratio is >130%. To sustain this while holding capital charges for Engineering (Rfp 25%, Rfc 20%) and catastrophe risk (ERE × 1.25), an insurer writing hydropower risks requires a combined ratio below 95% to generate adequate return on capital. Given the 35% expense load, the pure loss ratio must not exceed 60%.

Academic Model Pricing Derivation

At the current 210% loss ratio on the hydropower portfolio:

- Current effective rate (base property + LOP 12 months): approximately 0.80% of Sum Insured

- Required rate at 210% loss ratio, 35% expenses, targeting 60% loss ratio: 0.80% × (210/60) = 2.80% effective rate

- Alternatively stated: premiums must increase by a factor of 3.5x to become actuarially sound at current loss levels

- If the loss ratio is optimistically assumed at 123% (the fire portfolio catastrophe year proxy): 0.80% × (123/60) = 1.64% effective rate – still more than double current rates

The academic model thus establishes that the actuarially fair premium for Nepal hydropower insurance, at historical loss levels, lies between 1.64% and 2.80% of Sum Insured annually (including LOP). The current effective rate of ~0.80% represents a subsidy of 50-71% of the true actuarial cost – funded involuntarily by international reinsurers who absorb claims exceeding premium capacity, by NEA which absorbs unindemnified losses through its balance sheet, and ultimately by taxpayers when sovereign reconstruction funding is required.

7.3 Practical Pricing Model: Indicative Risk-Differentiated Tariff

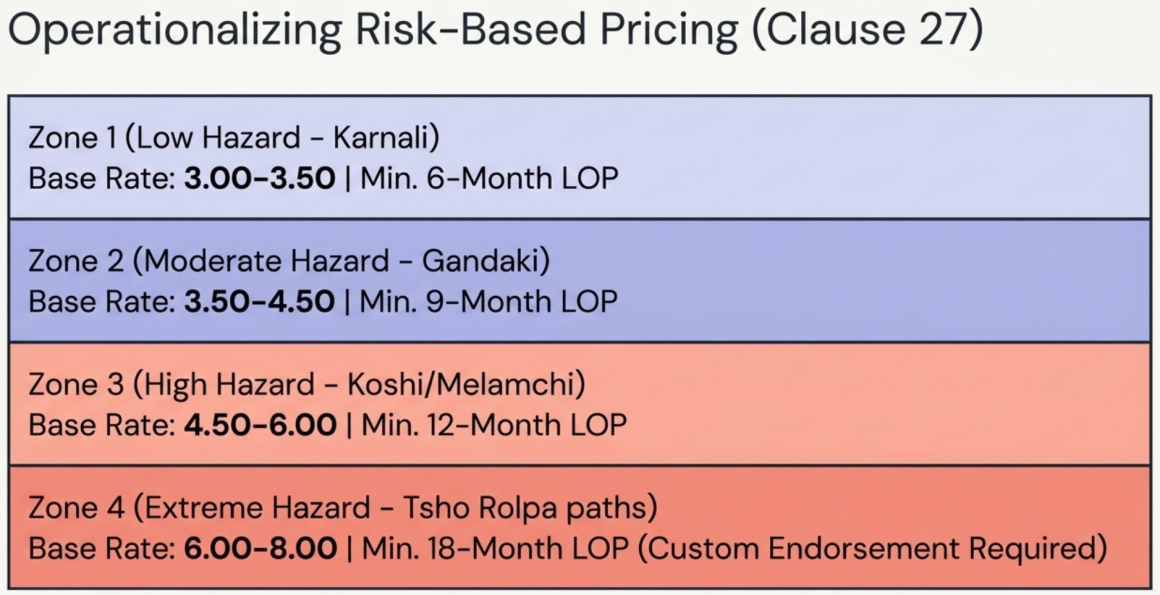

Based on the basin risk matrix (Table 1 above), loss data, and the Clause 27 framework permitting Risk-Based Pricing under Property Insurance Directive 2080, the following indicative tariff structure is proposed. This is not a regulatory submission but an evidence-based illustration of what actuarially differentiated pricing would require.

Table 3: Proposed Indicative Risk-Differentiated Tariff for Operational Hydropower (Benchmark: Property Insurance Directive 2080 Schedule 15 current base rate of NPR 2.00/thousand)

| Zone Classification | Geographic Definition | Proposed Base Rate (NPR/thousand) | Loading over Current Rate | Basis |

| Zone 1 – Low Hazard | Projects in Karnali basin below 2,000m, away from known GLOF paths, stable geology | 3.00–3.50 | +50–75% | Low GLOF, medium seismic, low cascade flood |

| Zone 2 – Moderate Hazard | Projects in Gandaki/Narayani basin, Trishuli sub-basin | 3.50–4.50 | +75–125% | Medium seismic, high drought risk, moderate landslide |

| Zone 3 – High Hazard | Projects in Koshi basin below 18 high-risk glacial lakes; Melamchi/Bhotekoshi corridors | 4.50–6.00 | +125–200% | High GLOF, high cascade flood, high seismic |

| Zone 4 – Extreme Hazard | Projects directly below Tsho Rolpa/Imja Tsho paths; Hewa Khola corridor; projects with documented reinsurer exclusions | 6.00–8.00 | +200–300% | “Probable” GLOF, superelevated channel risk, multiple cascade precedents |

Table 4: Proposed Consequential Loss/LOP Loading by Zone

| Zone | Indemnity Period Recommended | LOP Rate (NPR/thousand) | Combined Property + LOP Rate |

| Zone 1 | 6 months minimum | 6.00–7.00 (200% base × zone multiplier) | 9.00–10.50 |

| Zone 2 | 9 months minimum | 8.75–11.25 (250% base × zone multiplier) | 12.25–15.75 |

| Zone 3 | 12 months minimum | 12.00–18.00 (300% base × zone multiplier) | 16.50–24.00 |

| Zone 4 | 18 months minimum (requiring special endorsement) | 18.00–24.00 (extended, non-standard) | 24.00–32.00 |

Note on Zone 4 18-month LOP: No standard Nepal policy currently offers an 18-month indemnity period. The Upper Tamakoshi event demonstrated that 88 days of complete shutdown followed by partial recovery is a realistic outcome – and for a GLOF scenario affecting an entire cascade of projects, reconstruction could extend well beyond 12 months. The current maximum 12-month LOP cap is inadequate for mega-projects and should be extended to 18-24 months through NIA regulatory amendment.

Illustrative pricing example:

A 50 MW project in the Koshi basin (Zone 3), with a Sum Insured of NPR 10 billion (NPR 1,000 crore), currently pays:

- Property: NPR 2.00/thousand × 10 billion = NPR 20 million

- LOP 12 months: NPR 6.00/thousand × 10 billion = NPR 60 million

- Total: NPR 80 million/year (~0.80% of Sum Insured)

Under the proposed Zone 3 indicative tariff:

- Property: NPR 5.25/thousand (midpoint) × 10 billion = NPR 52.5 million

- LOP 12 months: NPR 15/thousand (midpoint) × 10 billion = NPR 150 million

- Total: NPR 202.5 million/year (~2.025% of Sum Insured)

The absolute increase – NPR 122.5 million/year – represents approximately NPR 2.45 crore per MW annually for a Koshi basin project. Relative to a typical 50 MW project’s annual PPA revenue of NPR 700-900 million at current tariff rates, this insurance cost represents approximately 2.3-2.9% of gross revenue – significant, but manageable compared to the alternative of being unindemnified during an 88-day shutdown.

8. Comparative Analysis: Bhutan and India

8.1 Bhutan

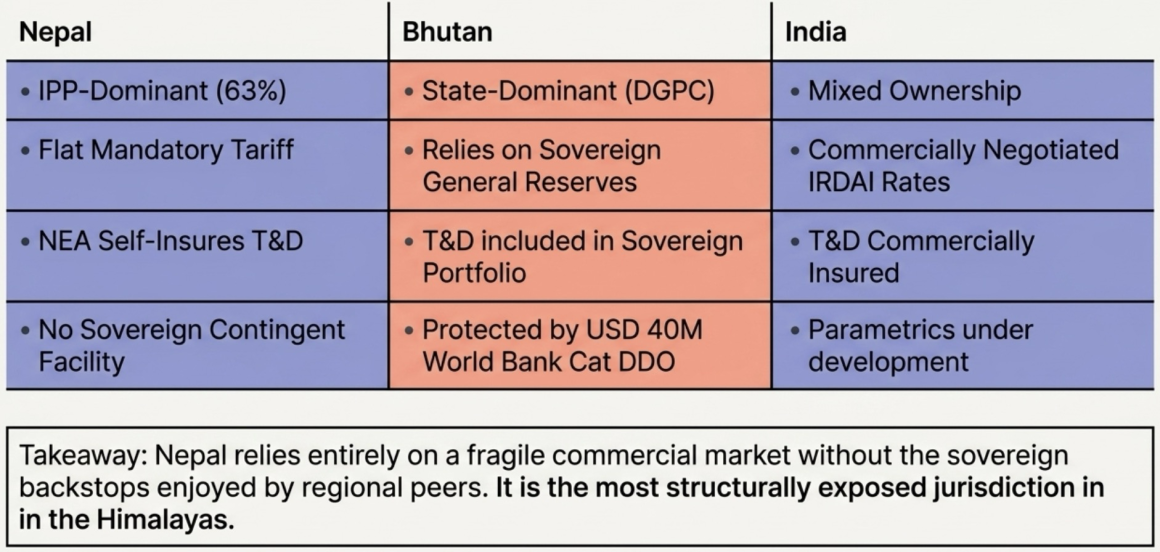

Bhutan’s hydropower sector is structurally analogous to Nepal’s – Himalayan geology, GLOF exposure, monsoon floods, and earthquake risk – but managed under a different governance model. Druk Green Power Corporation (DGPC), the state entity that operates 1,615 MW of hydropower, is directly owned by Druk Holding and Investments (DHI), the sovereign wealth fund. This structural difference matters for insurance: DGPC’s assets sit on the sovereign balance sheet, giving Bhutan access to sovereign-level risk financing instruments that Nepal’s IPP-dominated market cannot access.

Bhutan relies on General Reserves for disaster relief rather than commercial insurance, with a General Reserve maintained at the Ministry of Finance (World Bank Crisis Preparedness Gap Analysis Bhutan, 2025). However, critically, the World Bank’s explicit statement that “buildings and infrastructure, except hydropower plants, are insured” in Bhutan reveals that Bhutan shares Nepal’s core problem: hydropower infrastructure is the most economically critical sector, and it is the least commercially insured (World Bank Crisis Preparedness Gap Analysis Bhutan Briefing Note, 2025).

Bhutan’s structural advantage is the Cat DDO – the World Bank-approved USD 40 million Catastrophe Deferred Drawdown Option (December 2024) that provides immediate contingent liquidity in the event of an eligible catastrophic event. Bhutan also mandates that all new hydropower projects adopt catchment-wide disaster risk management, including geohazard assessments (World Bank Bhutan Cat DDO, 2024). These represent governance mechanisms that Nepal currently lacks.

Key comparison: Bhutan has no commercial hydropower insurance either, but it has a sovereign contingent credit line (Cat DDO) and mandatory catchment-level geohazard management that Nepal does not. Nepal’s IPP-dominated model means it needs commercial insurance where Bhutan can rely on sovereign reserves – but Nepal’s sovereign reserves are far smaller relative to its hydropower exposure, and the NPR 20 million NEA insurance fund provides no meaningful equivalent to a Cat DDO.

8.2 India (Himachal Pradesh / NHPC/SJVNL)

India’s hydropower sector – particularly NHPC and SJVNL operating in Himachal Pradesh – operates under IRDAI (Insurance Regulatory and Development Authority of India) regulations with commercially underwritten insurance for major projects. Listed public sector entities (NHPC is listed on NSE/BSE) are required to maintain property insurance for their operational assets as part of their corporate governance obligations and lender covenants.

However, India’s 2023 Himachal Pradesh floods – which caused INR 2,006 crore in state disaster losses and prompted central government assistance under NDRF (Government of India PIB, 2024) – revealed that even India’s more mature insurance framework does not fully cover cascade hydropower losses when dam operators must release water to protect infrastructure, causing downstream destruction. The “coordination failure” between dam operators, flood forecasters, and affected communities highlighted by the 2023 floods (Newslaundry, August 2023) is identical to the cascading disaster dynamic documented for Nepal.

India’s IRDA framework does not have a dedicated hydropower insurance product schedule equivalent to Nepal’s Property Insurance Directive Schedule 15. Major hydropower projects are insured under standard industrial property policies with negotiated terms – a more flexible approach that allows risk-based pricing but lacks the transparency and standardization of Nepal’s tariff framework. Parametric index-based products for hydropower are under discussion in India but are not yet commercially deployed for energy infrastructure.

Table 5: Comparative Framework Summary

| Dimension | Nepal | Bhutan | India (HP/NHPC) |

| Generation insurance framework | Mandatory tariff (0.20%), NIA-regulated | Self-insurance via sovereign reserves + Cat DDO contingency | IRDAI-regulated, commercially negotiated |

| Transmission insurance | None – NEA self-insures (0.003% of assets) | Included in DGPC sovereign portfolio | Commercial property insurance for NTPC/NHPC T&D assets |

| GLOF-specific product | None | None (Cat DDO provides sovereign backstop) | None commercially available |

| Parametric insurance | No commercial product deployed | No commercial product deployed | Under development |

| Sovereign contingent facility | None | USD 40 million Cat DDO (WB, 2024) | National Disaster Response Fund |

| Loss ratio trend | ~210% hydropower-specific | Not disclosed | Not sector-specific, but major disaster losses exceed insurance payouts |

| IPP vs. state ownership | IPP-dominant (~63% of installed capacity) | State-dominant (DGPC) | Mixed (NHPC/SJVNL state; some IPPs) |

The comparative analysis reinforces the conclusion that Nepal’s combination of IPP-dominant generation, commercially inadequate state self-insurance for T&D, and absence of any sovereign catastrophe contingency facility creates the most exposed risk position among comparable Himalayan jurisdictions.

9. Recommendations: What Must Change and Who Must Act

The following recommendations are prescriptive rather than aspirational. They are grounded in the data and legal analysis above, mapped against the institutional mandates of the relevant authorities.

Recommendation 1 – NIA: Implement Clause 27 Risk-Based Pricing Immediately

Clause 27 of Property Insurance Directive 2080 mandates Risk-Based Pricing for natural catastrophe risks for commercial and industrial properties, with an effective date of Shrawan 2081 BS. NIA must operationalize this provision by publishing a Geographic Zone Loading Table – differentiated at a minimum into the four zones proposed in Section 7.3 of this post – within FY 2082/83. The flat 0.20% base rate for hydropower must cease to apply uniformly. Projects in the Koshi basin carrying 18 potentially dangerous glacial lakes cannot be priced identically to projects in the Karnali basin carrying one.

Recommendation 2 – NIA: Create a Dedicated Transmission Infrastructure Insurance Product

The absence of any transmission-specific insurance product in Nepal’s regulatory framework is a regulatory gap that must be closed before the PPP transition for transmission infrastructure advances. NIA must develop a Transmission and Distribution Infrastructure Insurance Directive as a standalone regulatory instrument, with separate tariff schedules, mandatory minimum indemnity periods, and explicit treatment of BI triggers when a transmission line failure causes connected generation assets to shut down.

Recommendation 3 – NEA: Establish a Commercially Backed Insurance Program for Operational Assets

NEA’s NPR 20 million annual insurance fund contribution against NPR 242 billion of PPE represents a funding adequacy ratio of 0.008%. NEA must transition to a commercially insured model for its operational generation and transmission assets. The appropriate vehicle is a combination of: (a) a domestic co-insurance pool led by Rastriya Beema Company as the government-owned insurer; and (b) mandatory international facultative reinsurance for peak exposures above the domestic pool’s retention capacity. The cost – approximately NPR 1.94 billion annually at IPP-equivalent rates – should be factored into NEA’s asset maintenance and replacement planning as a non-negotiable operating cost.

Recommendation 4 – MoEWRI and MoF: Establish a Catastrophe Deferred Drawdown Option (Cat DDO)

Following Bhutan’s model, Nepal should negotiate a sovereign Cat DDO with the World Bank or ADB, providing a pre-arranged contingent credit line of at least USD 100-200 million that can be drawn immediately in the event of an eligible catastrophic event (major earthquake, GLOF, or basin-wide flood) affecting national power infrastructure. This facility would function as a bridge financing mechanism during the period between disaster occurrence and insurance claim settlement – addressing the liquidity gap that currently forces NEA and government to fund reconstruction from the national budget before insurance proceeds arrive.

Recommendation 5 – NIA and Nepal Re: Develop a Parametric Insurance Pilot for Hydropower

NIA should commission, in collaboration with the Department of Hydrology and Meteorology and the World Bank (which is already developing the Nepal Flood Model), a parametric trigger design study for hydropower projects in the Koshi and Gandaki basins. The pilot should target the flood trigger (e.g., river flow exceeding a specified cubic-meters-per-second at a designated DHM monitoring station) as the initial product, covering LOP claims without requiring physical damage assessment. The Weather Index Policy framework already operational in Nepal’s agricultural sector provides the regulatory and technical precedent for this product in a non-life context. Expanding it to energy infrastructure requires only: (a) DHM data integration, (b) NIA product approval, and (c) reinsurer participation terms.

Recommendation 6 – NRB and NIA: Mandate Minimum Insurance Specifications in Loan Covenants

NRB’s Unified Directives require that insured assets maintain insurance adequate to protect the bank’s collateral value. However, no directive specifies minimum peril coverage, indemnity periods, or LOP requirements for hydropower project loans. NRB should issue a sector-specific circular for hydropower infrastructure financing requiring: (a) CAR insurance during construction covering flood, landslide, GLOF, and earthquake at deductibles not exceeding a specified amount for standard events; (b) at operations, property insurance covering all natural perils plus RSMDST; and (c) mandatory LOP coverage at not less than a 9-month indemnity period for projects exceeding 10 MW.

Recommendation 7 – IPPAN and NIA: Establish a Hydropower Risk Pool

Nepal already has a Terrorism Pool serving as the governance model. IPPAN and NIA should jointly develop a Hydropower Natural Catastrophe Pool on the same structural basis, providing mandatory pool coverage for GLOF and major earthquake events where individual facultative reinsurance is unavailable or priced at unbankable deductibles. Pool premium contributions from all IPPs, sized at a NIA-determined percentage of each project’s sum insured, would accumulate reserves to pay cascade claims that individual policies cannot cover. Government participation as backstop provider for catastrophe claims exceeding pool reserves would be required for the pool to achieve reinsurance-grade credibility.

Recommendation 8 – NEA and NIA: Mandate Annual Insurance Compliance Certificates with Substantive Audit

Section 28 of the Tamakoshi V PPA requires annual insurance certificate submission to NEA. In practice, this is a paperwork compliance exercise without substantive review of coverage adequacy, deductible levels, or indemnity periods. NEA should require that annual insurance certificates be accompanied by a surveyor’s or actuary’s certification that the policy’s deductibles and indemnity periods are consistent with NIA’s guidelines and the project’s actual reconstruction timeline risk. NIA should publish an annual Insurance Adequacy Report for the hydropower sector, tracking aggregate premiums, claims, loss ratios, and reinsurance terms – creating the sector-specific statistical database that currently does not exist.

10. Conclusion

The title of this post – Pricing Hydropower Insurance in Nepal – frames what at first appears to be a technical exercise. It is not. Pricing this insurance correctly is a precondition for the financial closure of every major hydropower project being contemplated for Nepal’s next decade of capacity expansion. It is the difference between mega projects like Upper Arun / Budhigandaki receiving bankable lending / financing terms and stalling at the insurance step. It is the difference between NEA’s transmission PPP attracting serious investors and deterring them with a disclosure of uninsured infrastructure. It is the difference between an IPP in the Koshi basin surviving a GLOF event financially intact and defaulting on its bank covenants while waiting for a claim settlement.

The Cascade Effect documented what goes wrong when one project’s disaster triggers another’s. This post documents what goes wrong before any disaster occurs: when the pricing is wrong, the perils are wrong, the indemnity periods are wrong, the transmission sector is entirely absent, and the regulatory framework – despite containing the tools for reform in Clause 27, in the RBC Directive, and in the reinsurance framework – has not yet applied them to the sector that needs them most.

Nepal has the legal architecture for reform. It has the data – imperfect but sufficient to build on. It has regulators who understand the problem. What it needs is the commitment to act before the next GLOF demonstrates, once again, that the insurance framework arrived too late, covered too little, and paid too slowly.

References

Regulatory Documents and Legal Instruments

- Insurance Act 2079 (2022), Nepal Insurance Authority

- Property Insurance Directive 2080 (Sampatti Beema Nirdeshan 2080), NIA, Schedule 15 (Hydropower Tariff)

- Risk Based Capital and Solvency Directive 2025 (2082), NIA, Annexure III, Sections 5(51-53)

- Reinsurance Directive for Insurer 2080 (Bimakko Punarbima Nirdesha 2080), NIA, Section 5(2)

- Enlistment Guidelines for Foreign Reinsurers and Reinsurance Brokers 2024, NIA

- NIA Minimum Premium Rate for Non-Tariff Insurance Business Guidelines – Under Property Insurance Directive

- NRB Unified Directive 21/2081, Clause 1

- NRB Unified Directive 11/2081 (Consortium Financing), Clause 8

- NRB Unified Directive 2/2081, Clause 37 (Energy Sector)

- NIFRA Unified Directive 2/2082, Clause 2

- Public Procurement Regulation 2064, Rule 112

- National Insurance Policy 2080

- Section 27 and 28, Tamakoshi V Power Purchase Agreement, Nepal Electricity Authority / Tamakoshi Jalvidhyut Company Limited

Compilations of Decisions

- NIA Compilation of Decisions (Nirnaya Sangraha), Volumes 1-9 (selected cases: Thoppal Khola Hydropower/Prudential Insurance; Mudbhari and Joshi Construction/Everest Insurance; Sipring Khola/Himalayan General and National Insurance; Upper Dordi A/Prabhu Insurance; Peoples Power/Sagarmatha Insurance)

Annual Reports and Statistical Publications

- NIA Annual Reports, FY 2072/73 through 2081/82

- Beema Pratibimba (monthly), various issues, NIA

- NEA Annual Report FY 2024/25

- An Assessment of Reinsurance Practice and its Impact on Nepalese Insurance Industry 2019, NIA/Beema Samiti

- Insurance and Reinsurance in Energy Sector of Nepal, Pujan Dhungel Adhikari

Policy and Planning Documents

- IRRP Resilience Planning Guidelines Report – October 2022

- Nepal Hydropower – Flood Damage Assessment Report September 2024

- RPGCL Transmission System Master Plan 2018 (Document 1, Document 2)

- Bipad Report 8081 and Bipad Report 8182, Nepal Disaster Report 2024, NDRRMA

Insurance Policy Documents

- Loss of Profit (LoP) Insurance Policy – Sanima GIC Insurance Limited

- Sampatti Bimalekha Talika (Property Insurance Schedule) – Sanima GIC Insurance Limited

International Standards and Comparatives

- IFC Performance Standards on Environmental and Social Sustainability, January 2012, International Finance Corporation

- IFC Guidance Note 1, Assessment and Management of Environmental and Social Risks, updated June 14, 2021

- World Bank: ADB and World Bank Join Forces for Sustainable Development of Nepal’s Hydropower Sector, ADB Press Release, December 6, 2023

- World Bank: Upper Arun Hydropower Project (P178722), Environmental and Social Risk Classification: High

- World Bank: Climate and Disaster Resilience Development Policy Financing with Cat DDO, Bhutan, December 11, 2024

- World Bank: Bhutan Crisis Preparedness Gap Analysis Briefing Note, GFDRR, 2025

- IFC: Nepal E&S Hydropower Program 2016-2023, IFC Press Release June 13, 2023

- Government of India PIB: High-Level Committee approves Rs. 2006.40 crore to Himachal Pradesh for flood recovery, 2024

Preceding Article

- Parajuli, Sushil. “The Cascade Effect: Nepal’s Hydropower Insurance Market”

This post may be reproduced freely. All regulatory citations are to publicly available NIA, NRB, and NEA documents. Data triangulation and pricing models represent the author’s analysis and do not constitute actuarial certification or regulatory submission.