PART I: CONCEPTUAL FOUNDATION

1.1 Definition and Core Architecture of an Asset Management Company

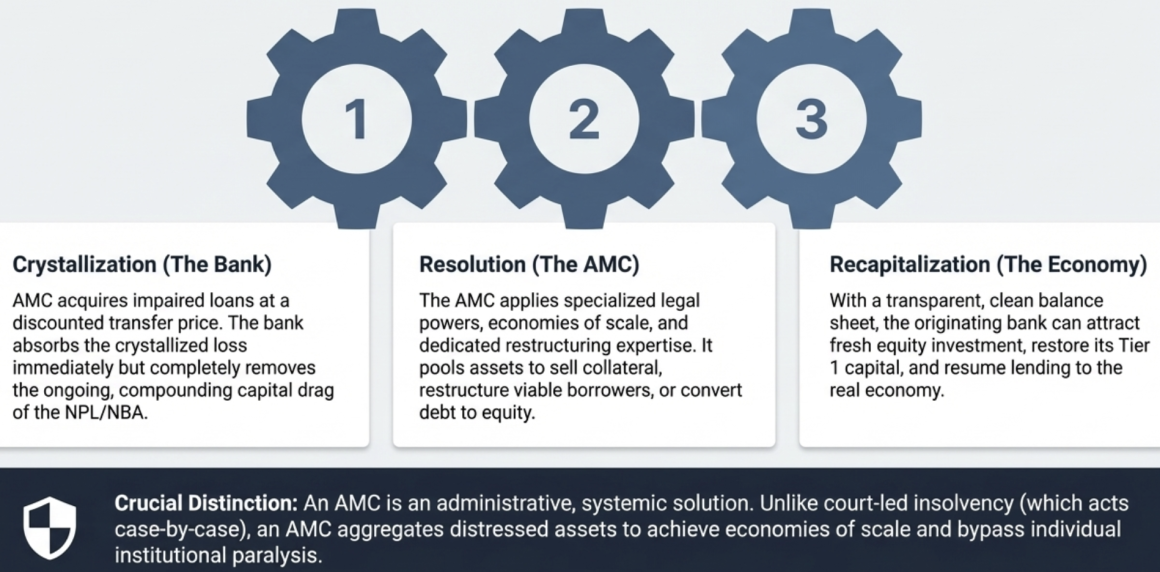

An Asset Management Company (AMC), in the context of banking sector distress, is a specialized financial entity structurally engineered to acquire non-performing loans (NPLs) and other distressed assets from the balance sheets of banks. By transferring these impaired portfolios to a centralized resolution vehicle, the originating financial institutions are relieved of punitive capital provisioning requirements, enabling them to recapitalize and resume their primary macroeconomic function of lending to the real economy. The AMC then leverages specialized legal powers, economies of scale, and dedicated restructuring expertise to maximize the recovery value of the underlying assets through loan restructuring, debt-to-equity conversions, securitization, or the liquidation of collateral.

The fundamental architecture involves three sequential steps. First, the AMC acquires impaired loans at a discounted transfer price, thereby crystallizing the losses on the originating bank’s balance sheet but removing the ongoing capital drag. Second, the AMC applies resolution strategies, including restructuring viable borrowers, selling collateral, converting debt to equity, or packaging and selling loan portfolios to secondary market investors. Third, the AMC distributes recoveries to its stakeholders and, ideally, winds down within a predetermined timeframe.

It is critical to distinguish an AMC from a conventional asset management firm. In Nepal, 21 entities carry the “asset management company” designation, but these are mutual fund managers licensed by the Securities Board of Nepal (SEBON) under the Mutual Fund Regulation, 2067 and the Specialized Investment Fund Regulation, 2075, entirely unrelated to distressed asset resolution. The AMC concept discussed here refers exclusively to a distressed debt resolution vehicle.

1.2 Global Typologies: Rapid Disposition versus Restructuring Vehicles

The World Bank’s Klingebiel framework classifies AMCs along two dimensions: centralized versus decentralized models, and rapid asset disposition versus corporate restructuring mandates. The international experience reveals two dominant typologies, each dictated by the nature of the distressed assets and the depth of local capital markets.

Typology | Primary Objective | Strategy & Asset Focus | Historical Examples |

Rapid Disposition Vehicle | Maximize immediate cash recovery, minimize holding costs, return assets to the private market swiftly | Bulk portfolio sales, deep-discount public auctions, securitization; typically applied to homogenous retail loans and real estate; strict sunset clause | US RTC (1989), Sweden Securum (1992) |

Restructuring & Warehousing Vehicle | Preserve the going-concern value of borrowers, restructure viable enterprises, hold illiquid assets until market conditions improve | Debt-to-equity swaps, operational turnaround of corporate firms, long-term real estate holding | China Big Four AMCs (1999), Spain SAREB (2012), India NARCL (2021) |

Rapid disposition vehicles handling easily liquefiable assets have historically outperformed corporate restructuring AMCs, which face greater political exposure and complexity. The choice of typology must be driven by the composition of distressed assets. Where NPLs are predominantly collateralized by real estate, as in Nepal, the rapid disposition model faces fundamental challenges because real estate markets are inherently illiquid and recovery depends on macroeconomic conditions rather than operational turnaround.

1.3 Global Evolution: Three Waves of AMC Deployment

The modern AMC emerged across three distinct global waves of financial distress. The first wave was characterized by the United States’ Resolution Trust Corporation (RTC) in 1989, established in the wake of the savings and loan crisis. The RTC resolved 747 failed savings institutions holding $394 billion in assets, achieving an 85-87% asset recovery rate before its planned dissolution in 1995. It pioneered securitization of distressed assets and public-private partnerships, establishing the template of a temporary, well-funded, politically insulated entity with special powers and a clear sunset clause.

The second wave occurred during the Asian Financial Crisis of 1997-1998. South Korea’s KAMCO acquired NPLs with a face value of KRW 110.2 trillion (~$88 billion) for KRW 39.8 trillion, eventually recovering KRW 48.1 trillion, exceeding its acquisition cost. KAMCO pioneered Asia’s first asset-backed securities market and transformed into the world’s first permanent public AMC. Malaysia’s Danaharta acquired RM 52.4 billion in distressed assets using zero-coupon government-guaranteed bonds, achieving a 58% recovery rate before winding down on schedule in 2005. Its special powers, including statutory vesting of asset titles without third-party consent and authority to appoint special administrators over distressed borrowers, proved critical to its effectiveness.

China’s experience illustrates both the potential and peril of AMCs. The Big Four AMCs (Huarong, Cinda, Orient, and Great Wall) were created in 1999 to absorb RMB 1.39 trillion (~$170 billion) in NPLs from the four large state-owned commercial banks. Purchased at book value and financed through central bank loans and non-marketable bonds, these entities achieved an initial recovery rate of only 33.6%. Rather than winding down, they diversified into investment banking, securities, and insurance, growing from RMB 451 billion in total assets (2010) to approximately RMB 5 trillion (2018). The Huarong crisis of 2020-2021, an RMB 106 billion loss followed by a $6.6 billion bailout, demonstrated the dangers of AMCs evolving beyond their original mandate without adequate oversight.

The third wave materialized following the 2008 Global Financial Crisis. Ireland’s NAMA acquired loans with a book value of EUR 74-77 billion at a 57% discount, generated 13 consecutive years of profitability, repaid all EUR 30.2 billion in senior debt, and transferred EUR 5.6 billion in surplus to the state, making it the most successful state-backed AMC. Spain’s SAREB, by contrast, acquired EUR 107 billion in book-value assets at a 53% discount but suffered sustained losses, exhausted its initial capital, and was converted from a majority-private to a public institution in 2022. SAREB’s rushed creation, overly optimistic business plan, and portfolio dominated by difficult-to-sell undeveloped land explain its underperformance.

AMC | Country | Year | Assets Acquired | Recovery/Outcome | Key Lesson |

RTC | USA | 1989 | $394 bn (747 institutions) | 85-87% recovery; dissolved 1995 | Sunset clause + private partnerships |

KAMCO | South Korea | 1997 | KRW 110.2 tn (~$88 bn) | Recovered KRW 48.1 tn (exceeded cost) | Securitization + special legal powers |

Danaharta | Malaysia | 1998 | RM 52.4 bn | 58% recovery; wound down 2005 | Statutory vesting + special administrators |

Big Four | China | 1999 | RMB 1.39 tn (~$170 bn) | 33.6% initial recovery; became permanent | Mission creep without oversight = fiscal risk |

NAMA | Ireland | 2009 | EUR 74-77 bn | Repaid all EUR 30.2 bn debt + EUR 5.6 bn surplus | Deep discount + professional governance |

SAREB | Spain | 2012 | EUR 107 bn | Sustained losses; converted to public entity | Illiquid real estate portfolios destroy AMC viability |

NARCL | India | 2021 | Rs 50,000 cr target | Acquired Rs 21,350 cr; 95-97% haircuts on first resolutions | Legal ecosystem (SARFAESI + IBC) matters more than AMC itself |

1.4 The Economic Rationale: Balance Sheet Paralysis and Credit Transmission Breakdown

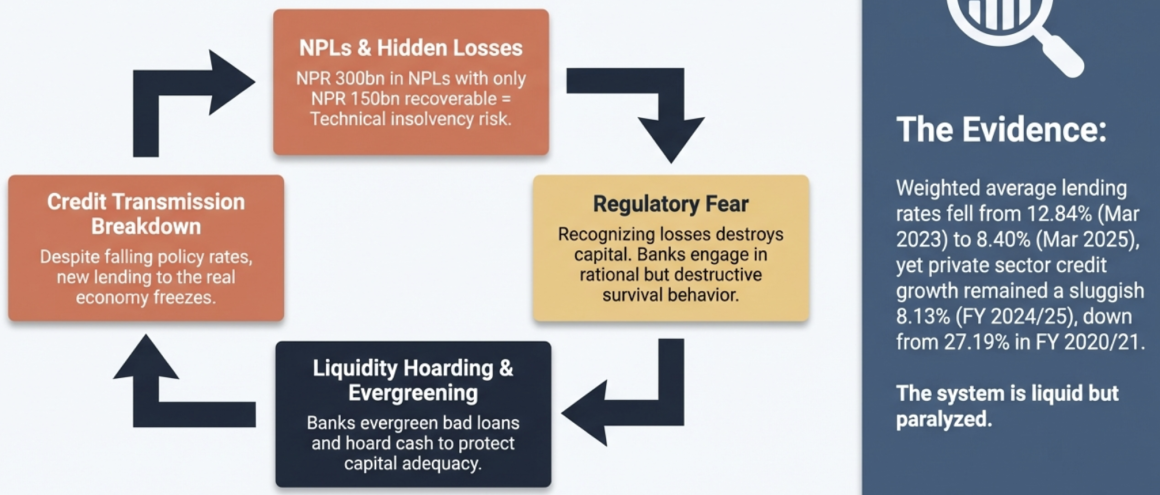

The core economic rationale for an AMC rests on the concept of balance sheet paralysis. When a significant volume of loans becomes non-performing, banks face a compounding set of problems that freeze their ability to function as credit intermediaries.

Consider a simplified illustration. A bank holds NPR 1,000 billion in loans, with capital of NPR 100 billion (a 10% capital ratio). If NPR 300 billion of those loans become non-performing and the true recoverable value is only NPR 150 billion, the bank faces a hidden loss of NPR 150 billion. Its true capital is negative NPR 50 billion (700 performing loans + 150 recoverable part of non-performing loans – 900 in deposits), rendering it technically insolvent. However, because recognizing this loss would destroy the bank’s capital and trigger regulatory intervention, the bank engages in a rational but economically destructive behavior: it avoids lending, evergreens existing loans, and hoards liquidity. The credit transmission mechanism, through which monetary policy easing should stimulate economic activity, breaks down entirely.

An AMC does not eliminate these losses. What it does is force transparent recognition of losses by purchasing NPLs at their true recoverable value, enabling the bank to absorb the crystallized loss, recover a discounted cash inflow form the NPLs, and then recapitalize through fresh equity issuance, regulatory intervention, or merger. The bank’s balance sheet becomes transparent, lending resumes, and the broader economy recovers. The AMC separately applies specialized resolution expertise to maximize recovery from the distressed portfolio.

This mechanism explains a paradox observable in Nepal’s current banking data: despite excess systemic liquidity and declining policy rates, private sector credit growth remains sluggish. The weighted average lending rate fell from 12.84% in mid-March 2023 (as referenced in “Financial Stability Report 2022/23) to 8.40% by mid-March 2025 (as referenced in Monthly Statistics Falgun 2081), yet credit growth was only 8.13% in FY 2024/25 (as referenced in Monthly Statistics Asar 2082), far below the 27.19% recorded in FY 2020/21 (as referenced in Monthly Statistics Asar 2080). The banking system is liquid but paralyzed, a classic symptom of impaired balance sheets suppressing credit supply.

1.5 Why Loss Recognition Alone Does Not Solve the Problem

Under Nepal Financial Reporting Standards (NFRS), aligned with IFRS 9, banks are required to recognize Expected Credit Losses (ECL) through a three-stage impairment model. Stage 1 loans carry a 12-month ECL provision; Stage 2 (deteriorating) loans carry a lifetime ECL; and Stage 3 (credit-impaired) loans carry a lifetime ECL based on estimated recoverable cash flows discounted to present value. Concurrently, the NRB’s Unified Directive No. 2/2081 mandates minimum provisioning rates: 1.1% for Pass loans, 5% for Watch List, 25% for Sub-standard, 50% for Doubtful, and 100% for Loss category loans.

If banks already provision for expected losses under both NFRS and NRB directives, why is an AMC necessary? The answer lies in several compounding factors. First, provisioning may be delayed or optimistic, particularly where collateral valuations are inflated or evergreening masks true asset quality. The IMF’s independent Loan Portfolio Review of Nepal’s ten largest commercial banks found an average NPL ratio of 7.70%, substantially above the self-reported 4.62%, with two banks exceeding 10%. Second, even when provisions are adequate on paper, the NPL remains on the balance sheet, consuming management attention, generating zero yield, and creating uncertainty about the bank’s true condition that deters new equity investment. Third, the regulatory treatment of provisions, particularly the 100% provisioning requirement for Non-Banking Assets (NBAs) from the date of acceptance, creates a capital trap where banks cannot hold distressed assets long enough for market conditions to improve without suffering crippling capital erosion. Fourth, the bank’s recovery department lacks the specialized skills, legal powers, and economies of scale that a dedicated resolution entity can deploy.

1.6 Moral Hazard and Discipline Mechanisms

The most significant policy risk of a government-backed AMC is moral hazard: the expectation of future bailouts may encourage reckless lending. If banks believe that their bad loans will ultimately be purchased by an AMC at generous prices, the incentive to maintain credit discipline is fundamentally undermined.

Well-designed AMC regimes employ multiple discipline mechanisms to mitigate this risk. First, deep discount transfers (haircuts) force banks to recognize upfront capital losses when selling NPLs to the AMC. If a loan with a book value of NPR 100 is sold at NPR 40, the bank immediately absorbs an NPR 60 loss, which directly punishes poor lending decisions. Second, loss-sharing structures may require banks to retain residual exposure through security receipts (instruments whose value depends on actual final AMC recovery) rather than receiving full cash payment. Third, eligibility criteria restrict AMC acquisitions to vintage NPLs (those originated before a specified cutoff date), preventing banks from dumping freshly originated bad loans, thereby reducing incentives for banks to engage in opportunistic or excessively risky lending in new sectors under the assumption of eventual AMC absorption. Fourth, a strict sunset clause on the AMC’s acquisition window (typically 3-5 years) prevents the formation of a permanent expectation of bailout. Fifth, management accountability provisions require parallel investigation of bank officials responsible for negligent lending, ensuring that balance sheet cleanup does not equate to accountability cleanup. Sixth, the AMC’s governance structure must be insulated from political interference through independent boards, professional management, and transparent audit procedures.

The critical insight is that a discounted purchase price alone is insufficient to prevent moral hazard. Real discipline comes from the combination of loss recognition, limited access, accountability for originating officers, and a credible commitment that the AMC will not be repeated.

1.7 AMC versus Insolvency Frameworks

An AMC and a court-led insolvency regime serve related but distinct functions. An insolvency framework provides a judicial mechanism for resolving individual distressed borrowers through restructuring or liquidation, operating case by case. An AMC is an administrative solution that aggregates distressed assets from multiple lenders, achieves economies of scale in resolution, and addresses the systemic dimension of the problem, namely the collective impairment of banking sector balance sheets.

The two mechanisms are complementary, not substitutive. India’s dramatic reduction in NPLs from 11.2% in March 2018 to 3.2% in March 2024 is attributed primarily to the credible threat created by the IBC, enhanced risk management, and economic recovery, rather than to Asset Reconstruction Companies (ARCs) alone. The IBC created a credible threat of insolvency resolution that fundamentally changed borrower behavior and recovery dynamics.

Nepal’s Insolvency Act, 2063 exists but is predominantly utilized for terminal liquidation rather than enterprise rehabilitation, and lacks a formalized framework for out-of-court centralized corporate debt restructuring. Any AMC design for Nepal must therefore be paired with insolvency reform to create the credible enforcement backstop that makes the AMC effective. While the Act includes a restructuring chapter (preparation of plans by restructuring managers, creditor meetings, and court oversight), it lacks a formalized framework for out-of-court centralized corporate debt restructuring, leading to financial institutions relying instead on ad-hoc NRB-guided workouts or bilateral creditor negotiations without statutory backing.

PART II: NEPAL'S BANKING SECTOR - THE CASE FOR OR AGAINST AN AMC

2.1 Macro-Financial Context

The Nepalese economy entered a phase of severe deceleration following the COVID-19 pandemic. In response to global inflationary pressures and rapid depletion of foreign exchange reserves, Nepal Rastra Bank (NRB) instituted aggressive monetary tightening and import restrictions. While these measures stabilized the external sector, propelling foreign exchange reserves to a record high of NPR 2.88 trillion (~ USD 21 billion) by late 2025 and moderating consumer price inflation to 3.57% in FY 2023/24, the domestic real economy absorbed a profound shock.

Economic growth plummeted to -2.42% in FY 2019/20, recovered to 5.28% by FY 2021/22, but then slumped to a mere 1.95% in FY 2022/23 before modestly recovering to 3.87% in FY 2023/24 and an estimated 4.61% in FY 2024/25.

Fiscal Year | Real GDP Growth (%) | CPI Inflation (%) | Private Sector Credit Growth (%) | Credit-to-GDP Ratio (%) |

2019/20 | -2.42 | 6.15 | 11.96 | 86.88 |

2020/21 | 4.49 | 3.60 | 27.19 | 97.85 |

2021/22 | 5.28 | 6.32 | 11.93 | 97.17 |

2022/23 | 1.95 | 7.44 | 4.31 | 90.65 |

2023/24 | 3.87 | 3.57 | 5.65 | 90.63 |

2024/25 (est.) | 4.61 | 3.75 | 8.13 | 91.60 |

Nepal’s private sector credit-to-GDP ratio, which temporarily breached 110% in mid-March 2022 before correcting to approximately 91% by mid-2025, is exceptionally high for a country at its income level. The IMF has described this as reflecting credit growth that was “too fast,” with the ratio roughly doubling from 50% to 100% in a decade. This rapid credit expansion laid the foundation for the asset quality deterioration that followed.

Nepal’s private sector credit-to-GDP ratio, which temporarily breached 110% in mid-March 2022 (as referenced in Banking & Financial Statistics 2022) before correcting to approximately 91% by mid-2025 (as referenced in Banking & Financial Statistics 2025), is exceptionally high for a country at its income level.

The IMF has described this as reflecting credit growth that was “too fast,” with the ratio roughly doubling from 50% to 100% in a decade (as referenced in the IMF’s Nepal: Technical Assistance Report – Financial Sector Stability Review, cited within the Financial Stability Report 2022/2023). This rapid credit expansion laid the foundation for the asset quality deterioration that followed (as referenced in the Financial Stability Report Fiscal Year 2022/2023). Despite eventual adoption of a cautiously accommodative monetary stance, reducing average lending rates from a peak of 12.84% in mid-March 2023 to 8.40% by mid-March 2025, private sector credit expansion remained sluggish at 5.6% to 8.1%. This paradox of high systemic liquidity alongside stagnant credit demand is a direct symptom of impaired bank balance sheets and degraded borrower creditworthiness, the condition that AMCs are designed to address.

2.2 NPL Trajectory and Composition

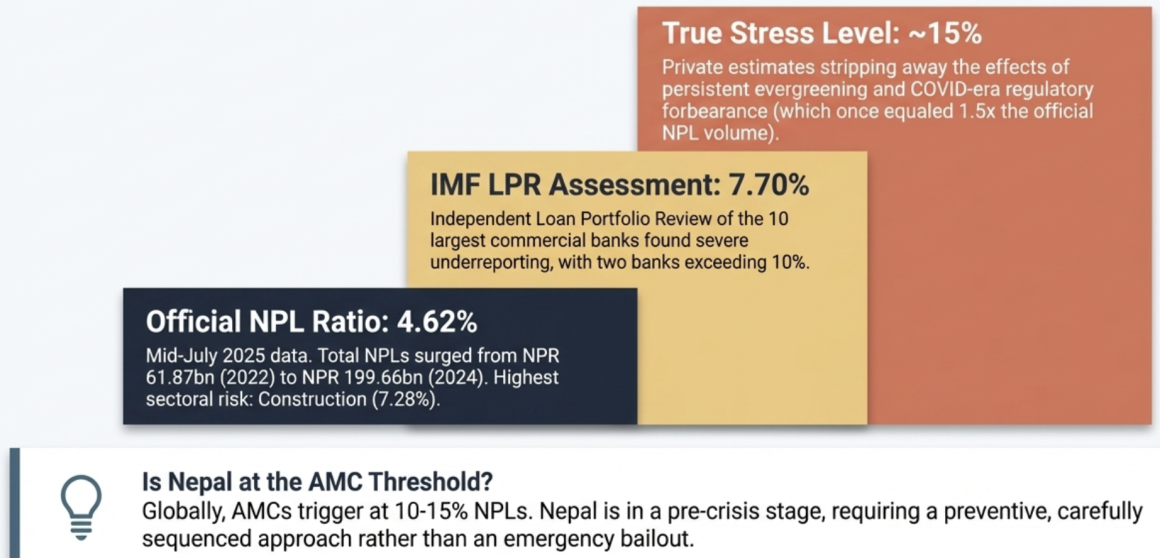

The Banking and Financial Institutions (BFI) system has experienced a dramatic deterioration in asset quality since the withdrawal of COVID-era regulatory forbearance / restrains. The overall NPL-to-total-loan ratio has risen from 1.31% in mid-July 2022 to 4.62% by mid-July 2025, the first time the 5% threshold was approached in over two decades. In absolute terms, total NPLs surged from NPR 61.87 billion in mid-July 2022 to NPR 199.66 billion by mid-July 2024, more than tripling in just two years.

Date (Mid-July) | Class A (%) | Class B (%) | Class C (%) | Class D (%) | Overall (%) |

2018 | 1.39 | 1.09 | 10.83 | – | 1.60 |

2019 | 1.40 | 0.92 | 8.80 | – | 1.52 |

2020 | 1.81 | 1.52 | 6.18 | – | 1.89 |

2021 | 1.41 | 1.30 | 6.19 | -≈ | 1.48 |

2022 | 1.20 | 1.36 | 6.23 | – | 1.31 |

2023 | 2.98 | 2.45 | 7.60 | 4.85 | 3.02 |

2024 | 3.76 | 3.62 | 9.87 | 5.72 | 3.86 |

2025 | 4.44 | 5.03 | 11.05 | – | 4.62 |

The composition of NPLs is dominated by the most severe category. Historically (2015-2019), the Loss category, representing loans overdue by more than one year with 100% provisioning requirements, constituted 60% to 71% of all non-performing loans. By mid-July 2019, Loss loans accounted for 69.88% of total NPLs (NPR 26.25 billion). By mid-July 2023, while the Loss share had declined to 38.20%, this occurred alongside a massive surge in the Doubtful category, which more than doubled compared to the previous year, indicating a rapid deterioration of newer loans into advanced delinquency. Following numbers has been extracted from Financial Stability Reports published by NRB:

Date (Mid-July) | Total NPL Volume (NPR Billion) |

2015 | 37.43 |

2016 | 36.83 |

2017 | 36.10 |

2018 | 38.51 |

2019 | 44.18 |

2022 | 61.87 |

2023 | 147.43 |

2024 | 199.66 |

Sectoral concentration amplifies the risk. By mid-July 2024, the sectors exhibiting the highest NPL ratios were Construction (7.28%), Fishery (6.65%), Agriculture (6.22%), and Metal Production, Machinery and Electrical Tools (6.09%) (as referenced in the Financial Stability Report 2023/24). The Construction sector has persistently been a top contributor to bad loans, appearing among the highest NPL sectors both during the 2020 pandemic period and in the latest industry-wide data.

The distribution of stress across individual institutions is uneven. Among the three state-owned commercial banks, Rastriya Banijya Bank (RBBL) reported an NPL of 3.65%, Agriculture Development Bank (ADBL) 3.44%, and Nepal Bank Limited (NBL) 3.28% as of mid-July 2024 (as referenced in the Financial Stability Report 2024). The average NPL for private commercial banks was slightly higher at 3.81%. At the extreme end, Himalayan Bank reported 7.68% and Karnali Development Bank was declared a troubled institution after NRB discovered NPLs exceeding 40%.

2.3 The Evergreening Problem and True Asset Quality

The official NPL figures almost certainly understate reality. Evergreening, the practice of extending new credit to troubled borrowers to keep loans classified as performing, has been pervasive. During FY 2020/21, COVID-19-related restructuring and rescheduling stood at a volume approximately 1.5 times the size of the entire banking system’s official NPL, representing a vast shadow portfolio of stressed assets (Financial Stability Report 2020/21). The NRB itself acknowledged that without these regulatory forbearance provisions, the NPL for development banks alone would have breached 10%.

Targeted forbearance was reintroduced in 2023 through NRB Circular No. 10, permitting restructuring for sectors including Hotels and Restaurants, Agriculture and Livestock, Construction, SMEs, and other sectors for credits up to NPR 50 million. The stated objective was “to prevent the degradation of asset quality,” an explicit acknowledgment that true stress levels exceeded reported figures.

The independent Loan Portfolio Review (LPR) commissioned under IMF Extended Credit Facility conditionality, conducted by Hawlader Yunus & Company, found the average NPL among the ten largest commercial banks was 7.70%, with two banks exceeding 10%, substantially above the self-reported system-wide figure of 4.62%. Private analysts estimate that without evergreening and forbearance effects, the true NPL rate could exceed 15%.

AMC | Country | Year | Assets Acquired | Recovery/Outcome | Key Lesson |

RTC | USA | 1989 | $394 bn (747 institutions) | 85-87% recovery; dissolved 1995 | Sunset clause + private partnerships |

KAMCO | South Korea | 1997 | KRW 110.2 tn (~$88 bn) | Recovered KRW 48.1 tn (exceeded cost) | Securitization + special legal powers |

Danaharta | Malaysia | 1998 | RM 52.4 bn | 58% recovery; wound down 2005 | Statutory vesting + special administrators |

Big Four | China | 1999 | RMB 1.39 tn (~$170 bn) | 33.6% initial recovery; became permanent | Mission creep without oversight = fiscal risk |

NAMA | Ireland | 2009 | EUR 74-77 bn | Repaid all EUR 30.2 bn debt + EUR 5.6 bn surplus | Deep discount + professional governance |

SAREB | Spain | 2012 | EUR 107 bn | Sustained losses; converted to public entity | Illiquid real estate portfolios destroy AMC viability |

NARCL | India | 2021 | Rs 50,000 cr target | Acquired Rs 21,350 cr; 95-97% haircuts on first resolutions | Legal ecosystem (SARFAESI + IBC) matters more than AMC itself |

2.4 Non-Banking Assets: The Capital Trap

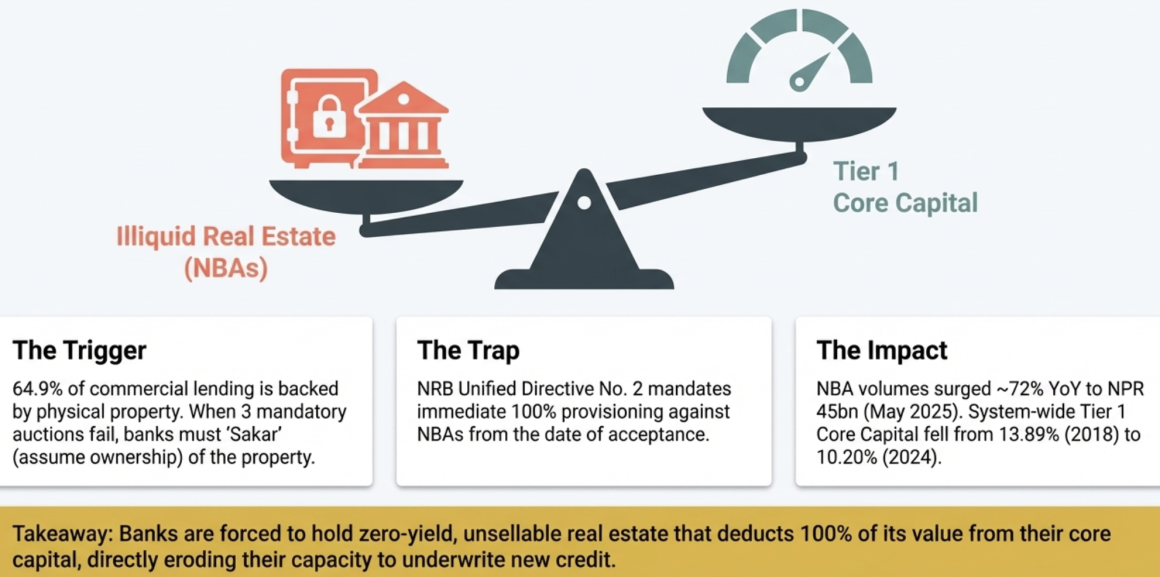

A defining characteristic of Nepal’s banking distress is the systemic reliance on real estate collateral and the resulting accumulation of Non-Banking Assets (NBAs). Approximately 64.9% of all commercial bank lending is backed by physical property, primarily land and buildings. When borrowers default, banks initiate foreclosure and attempt to liquidate collateral via public auction. However, a severely contracted real estate market means these auctions frequently fail to attract viable bids.

The contraction of the real estate market has been driven by the Land Use Regulation, 2022, which restricted plotting and kittakat (land divisions), while expiring renewals by mid-2025 led to suspensions that further curtailed supply; combined with urban out-migration (e.g., Kathmandu Valley deals fell ~25% YoY), rising construction costs, and speculative overpricing that deter buyers; developers have held back amid uncertainty, while NRB-mandated credit curbs to real estate (~65% of loans) have amplified the contraction, halving transactions in FY 2022/23 and sustaining the slump.

When an auction fails after the mandated minimum of three attempts, the bank is compelled under NRB Unified Directive No. 2, Section 11(1) to assume direct ownership of the physical property as an NBA. The regulatory treatment is highly punitive: banks must immediately provision 100% against the value of the NBA from the date of acceptance. NBA volumes surged by approximately 72% year-on-year to NPR 45 billion by mid-May 2025, with some estimates placing the 18-month increase at 123%.

This regulatory architecture creates a paralyzing capital trap. Banks hold highly illiquid physical properties that generate zero yield while simultaneously deducting the entirety of the asset’s value from their core capital base. This capital erosion directly constrains the banks’ capacity to underwrite new credit, trapping the broader economy in a low-growth equilibrium. The operational paralysis induced by rapid NBA accumulation serves as the primary domestic justification for establishing a centralized AMC to offload these physical assets from commercial balance sheets.

2.5 Capital Adequacy Erosion and Profitability Decline

Capital adequacy, while still above regulatory minimums, has been trending steadily downward. The system-wide overall Capital Adequacy Ratio (CAR) declined from 15.15% in mid-July 2018 to 12.92% by mid-July 2024, while the Tier 1 Core Capital ratio fell from 13.89% to 10.20% over the same period, approaching the 8.5% regulatory floor. If banks were properly provisioned for the LPR-identified NPL levels, several could face capital shortfalls.

Fiscal Year End | Tier 1 Ratio (%) | Overall CAR (%) | Net Profit (NPR Bn) | ROA (%) | ROE (%) |

Mid-Jul 2018 | 13.89 | 15.15 | 61.34 | 1.72 | 16.58 |

Mid-Jul 2019 | 11.58 | 14.29 | 74.23 | 1.73 | 16.62 |

Mid-Jul 2020 | 12.01 | 14.16 | 58.92 | 1.19 | 12.09 |

Mid-Jul 2021 | 11.12 | 14.19 | 71.30 | 1.17 | 12.76 |

Mid-Jul 2022 | 10.81 | 13.58 | 83.44 | 1.23 | 13.48 |

Mid-Jul 2023 | 10.59 | 13.42 | 76.99 | 1.06 | 11.27 |

Mid-Jul 2024 | 10.20 | 12.92 | 71.43 | 0.87 | 9.67 |

Profitability has declined sharply. Net profit fell from NPR 83.44 billion in mid-July 2022 to NPR 71.43 billion in mid-July 2024. Return on Assets dropped below 1% (to 0.87%) and Return on Equity dropped to single digits (9.67%) for the first time in the tracked period. The banking system remains overwhelmingly dependent on interest income: approximately 85% to 92% of total gross income derives from loans and advances, indicating a lack of diversified revenue streams.

Write-off volumes, while still modest in absolute terms, have been accelerating: from NPR 411 million in mid-June 2020 to NPR 917 million in mid-June 2019, NPR 1,607 million by mid-October 2022, and NPR 2,823 million by mid-October 2023.

2.6 Is Nepal at AMC Threshold? Comparative Assessment

Globally, AMCs have typically been established when NPL ratios reach 10-15% or higher, reflecting systemic crisis conditions. Nepal’s official 4.62% is below this threshold, but the IMF-assessed 7.70% for the ten largest banks, with private estimates of 15% if evergreening is removed, places the true figure in the range where AMC discussions become relevant.

Country | NPL at AMC Establishment | AMC Year | Nepal (Official) | Nepal (LPR Estimate) | Nepal (Private Est.) |

South Korea | ~17% | 1997 | 4.62% | 7.70% | ~15% |

Malaysia | ~25% | 1998 | 4.62% | 7.70% | ~15% |

China | >20% (SOBs >50%) | 1999 | 4.62% | 7.70% | ~15% |

Ireland | ~15% | 2009 | 4.62% | 7.70% | ~15% |

Spain | ~10% | 2012 | 4.62% | 7.70% | ~15% |

India | ~11% | 2021 | 4.62% | 7.70% | ~15% |

The conclusion is that Nepal is in a pre-crisis stage rather than a full systemic crisis. The banking system is under genuine stress, with NPL levels that are high by Nepal’s own historical standards, capital buffers that are eroding, and an acute NBA problem that has no parallel in recent Nepali banking history. However, the system has not reached the catastrophic NPL levels (17-50%) that historically justified centralized crisis AMCs. This positioning has important implications for AMC design: Nepal needs a preventive, carefully sequenced AMC, not an emergency crisis-response vehicle. The IMF’s explicit recommendation to exhaust supervisory measures, reform debt enforcement, and develop distressed debt markets before establishing an AMC reflects this assessment.

PART III: LEGAL AND REGULATORY FRAMEWORK ANALYSIS

This section provides an exhaustive assessment of Nepal’s existing statutory framework as it pertains to the feasibility of establishing and operating an Asset Management Company. The analysis spans the entire credit lifecycle, from loan origination and collateral creation through default, enforcement, recovery, insolvency, and asset transfer. Each legal domain is assessed against the functional requirements of an AMC: the ability to acquire distressed assets cleanly, enforce security interests rapidly, manage and sell collateral efficiently, and do so without prohibitive transactional friction.

3.1 Land and Immovable Collateral Regime

Given that approximately 64.9% of all commercial bank lending in Nepal is backed by physical property, the land law regime is the single most important legal dimension for AMC feasibility. Any AMC acquiring distressed bank portfolios will overwhelmingly be dealing with land-secured claims, and its success will depend entirely on the speed, cost, and certainty with which it can take, manage, and sell immovable collateral.

Title and Ownership Integrity. Legal ownership of land is established by the Land Revenue Office (Malpot Karyalaya), which registers every parcel into the land registration book (Darta Kitab) based on cadastral surveys or existing records (Land Revenue Act, 2034, Section 6(1) and 6(2)). A recognized landowner (Jaggadhani) is the individual in whose name the land is registered and who bears liability for land revenue (Lands Act, 2021, Section 2(a)). Ownership is verified through the Landowner Registration Certificate (Jaggadhani Darta Praman Purja) and the Landowner Registration Record (Jaggadhani Darta Sresta – held by the District Land Revenue Office / Malpot Karyalaya). To execute name transfers (Dakhil Kharej) or verify details, the Land Revenue Office requires original ownership certificate, citizenship certificates, and local government recommendations (Land Revenue Rules, 2036, Rule 5Ka(1) and (2)). These records verify the owner’s details, parcel number, area, land-use zone, and joint ownership conditions (Land Revenue Rules, 2036, Schedules 6 and 7).

Common Title Defects. Several defects pose direct risks to collateral held by banks. Discrepancies in the Registry include double registration of the same parcel or incorrect records concerning name, address, age, parcel number, and area (Land Revenue Act, 2034, Section 7(3)). Unlawful Registration of Public Land means that government, public, or community land registered in a private name is automatically void (badar), and records must be cancelled (Section 24(1) and (2)). Fraudulent Registration based on deliberately false information is punishable by fines, imprisonment, and confiscation (Sections 29, 29A, and 30). Any collateral claim on a void title would be compromised. An AMC acquiring such a portfolio inherits these defects without remedy.

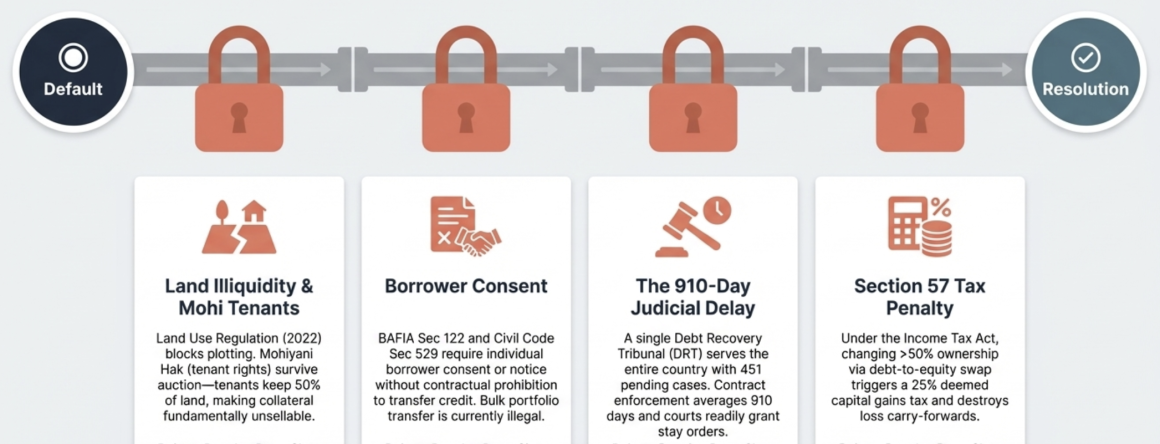

Parallel Claims Affecting Collateral. Three categories of parallel claims heavily impact collateral viability. First, Tenancy (Mohi): tenants possess statutory rights (Mohiyani Hak) over cultivated land (Lands Act, 2021, Section 25(1)), which survive changes in ownership, including auction sales (Land Revenue Act, 2034, Section 16(3)). The Landowner Registration Certificate must record tenant details alongside the landowner (Land Revenue Rules, 2036, Schedules 6 and 7). Most critically for AMC operations, the Lands Act explicitly provides that tenant rights (Mohiyani Hak) cannot be auctioned off to recover debts, whether government or non-government. If collateralized land has registered tenants, the AMC cannot sell free and clear; tenants are entitled to 50% of the land, requiring a joint separation process that is time-consuming and often contentious. Second, Guthi (trust) land: official certificates include dedicated Guthi fields (Land Revenue Rules, 2036, Schedules 6 and 7), and Guthi lands are exempt from land ceiling provisions (Lands Act, 2021, Section 12(f)). Third, Public/Government Land: any private registration is illegal and automatically void (Land Revenue Act, 2034, Section 24(1) and (2)).

Mortgage Creation and Security. Banks secure transactions by requesting the Land Revenue Office to freeze (Rokka) the property (Land Revenue Act, 2034, Section 8b(3); Land Revenue Rules, 2036, Rule 5Gha(1)). Once frozen, the landowner cannot sell or transfer ownership rights. However, the land legislation does not detail the system for determining priority between multiple mortgages, whether priority can be contractually altered, or what happens to priority upon reassignment. The government holds a primary statutory lien for unpaid land revenue (Malpot): the Land Revenue Office can freeze property, auction it, and if no bids, ownership transfers automatically to the Government. This statutory lien takes priority over all private security interests.

Transferability of Mortgage Rights (AMC-Critical Gap). The land legislation contains no provisions regarding the assignment of mortgage rights independently of the loan, the necessity of fresh deed execution, borrower or guarantor consent for mortgage transfer, vesting certificates, or evidentiary requirements for proving transfer. This is the most significant gap from an AMC perspective. While BAFIA, 2073, Section 122 permits the sale or purchase of rights in property obtained as security, the operational mechanics of how this transfer is effected at the Land Revenue Office level, how the Rokka is reassigned, and whether borrower consent is needed at the land registry remain unaddressed. The AMC Act must provide for statutory vesting of mortgage rights without fresh deed execution and must mandate the Land Revenue Office to recognize the AMC’s vesting certificate as sufficient for updating land records.

Registration and Administrative Burden. Updating the land registry post-transfer requires document submission to the Land Revenue Office, notification to the local government within 15 days of any transfer, and formal requests to update registry and certificates. The average time for mutation is not specified, but for missed cadastral survey registrations, the Office must decide within two years. Officials hold discretionary powers creating delay: the Land Revenue Office can freeze property for disputes or other reasons; the Director General can unilaterally cancel completed name transfers if a serious error occurred; specialized committees chaired by the Chief District Officer determine minimum land valuation; and land-use changes require approval from Local, Provincial, and Federal Land Use Councils. Positively, a Land Information System (Bhu-Suchana Pranali) has been established as a computerized system for land administration, alongside authorized online Land Service Centers for digital transactions.

Enforcement, Possession, and Sale. The land legislation does not contain explicit provisions for creditor possession in the commercial lending context. In analogous contexts, a landowner defaulting on revenue retains physical possession until actual auction (interim protection), remaining auction proceeds after deductions must be refunded to the landowner, and decisions can be appealed to the District or High Court within 35 days. A landlord cannot legally evict a tenant without a court or municipality order, and unlawful dispossession results in fines up to NPR 10,000 and mandatory reinstatement. For recovery of land revenue, auctions must follow a competitive bidding process. If no bids, ownership transfers to the Government, which then attempts annual resale. If subsequent bids also fail, sale at prevailing market rate without auction is permitted. The existing laws do not address AMC-specific private sale authority. The AMC Act must explicitly authorize private treaty sales, portfolio sales, and sales to pre-qualified investors.

AMC-Critical Land Constraints (Summary). The land regime creates a highly illiquid environment for any AMC. Subdivision restrictions prevent breaking large parcels into sellable plots (500-1,000 sq.m. minimum for agricultural land; 130 sq.m. for residential/commercial). Land-use changes require lengthy multi-tier approval. Land distributed to landless individuals carries a 10-year transfer ban. Corporate land ceilings (10 Bigha in Terai, 25 Ropani in Kathmandu) prohibit selling excess land. Active real estate trading requires a separate license under recent Malpot Rules amendments. Tenant rights cannot be extinguished by sale, requiring costly joint separation. Realistically taking, managing, and selling land collateral within 6-12 months is practically and legally impossible under current regulations for most transactions.

3.2 Banking and NRB Regulatory Framework

Credit Origination and Due Diligence. The legal framework mandates rigorous due diligence. Under BAFIA, 2073, Section 55(1), every BFI must clarify the loan’s purpose before disbursement. Section 55(7) requires complete details regarding the borrower, guarantors, and directors/shareholders holding above a specified percentage. NRB Unified Directive No. 2/2081, Section 2 mandates comprehensive analysis of repayment capacity, future cash flows, and reliable income sources. BFIs must obtain a CIC credit report before sanctioning any facility, and lending to blacklisted entities is prohibited.

An internal Credit Risk Rating System is mandatory for Class A commercial banks and national-level Class B development banks and other financial institutions also follow simplified or outsourced systems rather than full internal models, per supervisory capacity and asset thresholds. Environmental and social risk analysis is required under NRB Unified Directive No. 29. Customer Due Diligence and, for high-risk customers, Enhanced Customer Due Diligence (ECDD) are mandatory under the Money Laundering Prevention Act, 2064, Section 7, and NRB Unified Directive No. 19. These standards establish the baseline quality of documentation an AMC would inherit.

Sectoral Exposure Limits. NRB Unified Directive No. 3/2081 Section 12(3) generally permits up to 40% of total credit to a single sector. Real estate is capped at 10% under NRB Unified Directive No. 3/2081, Section 12(4)(gh). Margin lending cannot exceed 40% of Core Capital under NRB Unified Directive No. 2/2081, Section 17(7). The Single Obligor Limit is 25% of Core Capital NRB under Unified Directive No. 3/2081, Section 2 (30% for exports, SMEs, agriculture, tourism, manufacturing). For NIFRA, the SOL is 50% of Core Capital under NRB Unified Directive No. 3 for Infrastructure Development Banks, Section 2. These limits shape the predictable composition of NPL portfolios an AMC would acquire.

Collateral Valuation at Origination. Valuation must be by independent professional valuators (NRB Unified Directive No. 12, Section 7) based on Fair Market Value. LTV ratios are capped at 50% for real estate. For residential home loans, the LTV can reach 70% for first-time buyers and up to 80% for electrical vehicles or specific residential reconstruction following natural disasters. For margin lending, value is the lower of 180-day average or market price, with lending up to 70%. Revaluation to increase loan limits is prohibited. Under the Banking Offence and Punishment Act, if auction reveals a valuation discrepancy of more than one-third without justifiable economic reasons, the valuer can be blacklisted or prosecuted.

NPL Classification Dynamics. Loans are classified by overdue duration supplemented by event-based triggers. For commercial banks and microfinance: Pass (up to 1 month), Watch List (1-3 months), Sub-standard (3-6 months), Doubtful (6 months to 1 year), Loss (over 1 year). For Infrastructure Development Banks: Pass (up to 3 months), Sub-standard (3 months to 1 year). Additional Watch List triggers include: working capital loans not renewed within 1 month; loans to borrowers classified as NPL in any other BFI; firms with negative net worth or three consecutive years of net loss; debt-to-equity exceeding 80:20; and DTI ratio failures. Event-based Loss triggers (regardless of overdue period) include: borrower bankruptcy/insolvency, borrower missing for 90 days, loan misuse, non-operational project, CIC blacklisting, insufficient collateral value, and initiation of auction or court proceedings. This last trigger is critically important: the moment a bank takes legal action, the loan automatically becomes Loss requiring 100% provisioning, destroying its book value before any AMC transfer.

Reversibility via Restructuring. Under NRB Unified Directive No. 2/2081 – the Two-Year Rule applies: restructured loans can only be reclassified as Pass after two years of continuous regular payments following any grace period. Already-classified NPL loans must maintain existing provisioning during restructuring. For microfinance, the threshold is six months. Non-restructured NPL loans with cleared overdue amounts are upgraded to Watch List for six months before reaching Pass. Infrastructure projects in national priority areas can be classified as Pass with only 1.1% provision after restructuring if expanding capacity. This two-year timeline means even successful AMC restructuring takes at least two years to produce a performing asset – assuming similar LLP provisions (or part thereof) are translated to AMC under NRB’s supervision.

Loan Transfer Legality Under BAFIA. BAFIA, 2073, Section 122 explicitly allows a BFI to sell or buy a loan, liability, or right in property obtained as security, unless otherwise provided in the loan agreement. NRB Unified Directive No. 14 provides the regulatory framework for Credit Sale, Purchase, Repurchase, and Takeover. The purchasing institution must maintain provisions according to existing classification. In consortium loans, departing members may sell shares at discount or premium with other members’ consent. Agriculture and energy sector loans may be transferred without customer consent if the originating institution continues relationship management. For standard credit purchases, however, customer consent is required. A Letter of Assignment is recognized as a valid legal instrument. This consent requirement is the single most significant barrier to bulk AMC transfers and must be overridden by AMC legislation.

Confidentiality. BAFIA Section 109 mandates strict confidentiality regarding bank-customer relationships, accounts, records, and financial information. Exceptions exist for NRB information sharing and inter-BFI credit information exchange. Bulk AMC transfers without individual consent would require a statutory carve-out allowing the AMC to receive borrower credit files.

Self-Help Enforcement Powers. BAFIA Section 57(1) empowers BFIs to recover principal and interest by managing or selling pledged property without a prior court decree. Auction must be through public notice in a national daily newspaper. Notice to guarantors specifying debt amount and repayment timeframe is required. Independent valuation is required before auction or NBA takeover. The moment auction proceedings are initiated, the loan is reclassified as Loss requiring 100% provisioning. CIC blacklisting of defaulters is mandatory (Section 57(11)). The government must provide police and administrative assistance on request (Section 57(13)).

Non-Banking Assets. When collateral fails to sell after three auction attempts, the BFI must take over (Sakar) the asset (NRB Unified Directive No. 2, Section 11(1)). The NBA is valued at the lower of total dues or current market value. If market value is lower, the shortfall is immediately charged as an expense. NBAs carry 100% provisioning. The AMC Act must provide that the AMC can hold assets without this punitive provisioning, otherwise the transfer achieves no balance sheet relief.

NRB Resolution Powers. NRB can order asset sales under management control (NRB Act Section 86G(1)(b), 86E(1)(b)), transfer assets to other BFIs or any other entity (Section 86E(1)(d)), delegate asset management to specialized companies during resolution (Section 88G(13)), establish bridge institutions (Section 88H, 88J(1)), transfer assets without stakeholder consent (Section 88C(4)), and mandate share capital reduction and forced share sales (Sections 86J, 86F(3)). Prompt Corrective Action Bylaws, 2074 allow graduated restrictions. However, these powers apply to resolution of failing institutions, not a standalone AMC. An AMC Act must create a separate statutory basis for AMC operations independent of the resolution framework.

The composition of NPLs is dominated by the most severe category. Historically (2015-2019), the Loss category, representing loans overdue by more than one year with 100% provisioning requirements, constituted 60% to 71% of all non-performing loans. By mid-July 2019, Loss loans accounted for 69.88% of total NPLs (NPR 26.25 billion). By mid-July 2023, while the Loss share had declined to 38.20%, this occurred alongside a massive surge in the Doubtful category, which more than doubled compared to the previous year, indicating a rapid deterioration of newer loans into advanced delinquency. Following numbers has been extracted from Financial Stability Reports published by NRB:

3.3 Secured Transactions Framework

The Secured Transactions Act, 2063. This Act provides the legal basis for creating security interests in movable and intangible property, with a centralized collateral registry for priority claims. Hypothecation (Drishtibandak) is defined under BAFIA Section 2(hhh) as credit where movable asset possession remains with the borrower.

Enforcement Mechanisms. Under BAFIA Section 57(1), the BFI can auction hypothecated collateral upon default. The STA, Section 46(2) grants the secured party the right to take possession upon default. Section 50(1) allows sale, lease, or licensing of collateral in any condition. The STA provides a dual repossession framework: self-help without court proceedings if the borrower gave written consent (Section 48(1)); or court-ordered repossession if self-help fails (Section 48(2)). For high-value cases, BFIs may use the DRT (Debt Recovery Act, Section 15), with Debt Recovery Officers empowered to seize and auction assets or arrest defaulters (Section 25(2)).

AMC Stepping into Hypothecation Rights. BAFIA Section 122 allows transfer of rights in property obtained as security. NRB Act Section 88G(13) empowers transfer to asset management companies during resolution. NRB Unified Directive No. 14 provides the credit sale/purchase framework.

Critical Gap: Immovable Property. The STA does not cover immovable property, a fundamental gap given that 64.9% of lending is secured by land and buildings. Nepal has no equivalent of India’s SARFAESI Act, which empowers ARCs to bypass judicial delays, seize immovable collateral, and assume management control of defaulting borrowers. Without SARFAESI-like powers extending to immovable property, a Nepali AMC inherits the same enforcement bottlenecks paralysing banks. The AMC Act must create comprehensive enforcement powers covering both movable and immovable property.

3.4 Civil Procedure, Assignment Doctrine, and Evidence

Assignment Doctrine. The National Civil Code, 2074, Section 529(1) provides that contractual rights may be transferred unless personal performance is required. Section 529(2) requires: (a) writing; (b) unconditional transfer; (c) no prohibition by law or contract; (d) notice to the other party with time-limit. The condition that transfers not be prohibited by the original contract means anti-assignment clauses could block AMC acquisition. The AMC Act must override such clauses through a non-obstante provision.

Ancillary Rights and Guarantees. Section 529(1) provides that contractual rights are transferable, including the creditor’s security rights. Under Section 438, mortgagee possessory rights are transferable. Guarantor liability persists until the borrower is released (Section 564(1)(b)), and subrogation (Section 567(1)) confirms creditor rights follow the debt during assignment. The AMC Act should explicitly confirm these principles.

Debtor Defenses. Under the Civil Procedure Act, 2017, debtors can submit defense statements, raise preliminary pleas (locus standi, limitation, jurisdiction), rebut documentary evidence including challenging deeds of assignment as forged, and file counterclaims. These rights are constitutionally protected. The AMC must ensure procedurally unimpeachable assignment: statutory vesting, NRB confirmation, proper notice, and clean documentation.

Procedural Delays. Statutory timelines suggest several months: process issuance within 3 days, service within 7 days, defense within 21 days, evidence examination within 7 days, hearing and decision within 1 month, judgment within 21 working days, property delivery within 6 months. Multiple delay mechanisms exist: 15-day evidence extensions, witness non-attendance requiring 7-day rescheduling, 15-day delay for complex questions, force majeure extensions (21 days mourning, 45 days childbirth, 7-15 days natural disasters), time-limit extensions of 15 days (once) and appearance extensions of 21 days (twice), adjournments pending interlinked cases, and translation requirements. The appellate phase adds 30 days for filing and six months for hearing.

Interim Relief and Stay Orders. Borrowers can seek interlocutory orders if their claim would be meaningless without intervention. Courts exercise discretion and may require compensation commitments. Under Section 54(2)(b) of National Civil Code 2017, in bankruptcy, a debtor may request up to five years to repay before bankruptcy proceedings commence. Once bankruptcy is initiated, asset transfers, mortgage enforcement, and debt repayment are ipso facto stayed. These provisions mean AMC enforcement could be stayed; the AMC Act must restrict stay availability against AMC actions.

Execution Phase. Post-judgment, court records go to the bailiff section within 3 days. Property possession enforcement must complete within 6 months. Money recovery gives the debtor 35 days to pay. Hidden property can be auctioned upon discovery. Transfers during pendency can be reversed. Hiding assets with mala fide intention grounds a separate lawsuit. Obstructing execution constitutes contempt (fine, up to 3 months imprisonment, or both).

Evidentiary Framework. Bank records are presumed correct (Evidence Act, 2031, Section 6(c), Section 14; BAFIA Section 58). Electronic records are admissible (Evidence Act Section 35). However, DRT Rule 10 requires original loan deeds (Sakkal) for filing claims. The AMC must physically receive originals from assignor banks. A Letter of Assignment bridges the proof chain, establishing AMC locus standi. Under Evidence Act: Section 9(1): Statements are admissible against the party who made them. Section 9(3)(a): Statements by a representative are treated as statements of the party. Section 9(3)(c): Statements by a predecessor in interest (assignor bank) are treated as statements of the current party (assignee/AMC). Therefore, it can be implied that Section 9(3)(c) allows an AMC to adopt the evidentiary position of the original bank, while Section 9(1) ensures that the borrower’s prior admissions (made to the bank) remain admissible against the borrower even after the loan is assigned to the AMC.

3.5 Debt Recovery Tribunal

The DRT, established under the Debt Recovery Act, 2058, has exclusive jurisdiction over bank debt recovery cases exceeding NPR 500,000 under Section 3(d). Section 17 mandates resolution within 150 days. Appeals to the Appellate Tribunal require decision within 90 days (Section 23). Filing limitation is four years from default (five for pre-existing overdue loans) under Section 15(1). The DRT can issue interim asset-freeze orders (Section 16(1)). The Debt Recovery Officer can seize assets, auction them, or arrest defaulters (Section 25(2)).

Under the Debt Recovery Act, 2058, Section 14(7), a BFI is permitted to file a petition with the Tribunal only after the following conditions have been met: Settlement Attempts: There must have been sufficient discussion and action taken between the bank and the borrower to settle the debt. Exhaustion of Internal Recovery: The BFI must have taken “sufficient action” for recovery on its own, and those actions must have failed to recover the debt.

Performance data reveals severe constraints. As of mid-July 2024: 451 pending cases. In FY 2022/23: 238 proceedings handled, 139 cases settled (58.40% of target). FY 2023/24 recoveries: NPR 35.28 billion. Only one DRT exists for the entire country in Kathmandu, with chronic staff shortages. Contract enforcement nationally takes 910 days and costs 26.8% of the claim value.

For AMC operations, the DRT is both essential and insufficient. The 150-day statutory timeline, even if achieved, is too slow for an AMC targeting 12-24 month asset turnover. The four-year limitation period means some acquired assets may be approaching filing deadlines. The DRT’s interim order power is valuable for preventing asset dissipation but can also be exploited by debtors to stall enforcement. The AMC Act should create a fast-track window within the DRT for AMC cases or establish a parallel mechanism with shorter timelines.

3.6 Insolvency Regime

Insolvency Triggers. Under the Insolvency Act, 2063, Section 7: Board resolution (Section 7(1)(a)); shareholder special resolution (Section 7(1)(b)); failure to comply with court-ordered payment within 35 days (Section 7(1)(c)); failure to respond to creditor demand within 35 days (Section 7(1)(d)); or proof that liabilities exceed assets (Section 7(1)(e)). Under Companies Act, 2063, Section 60, directors must act if net worth falls below half of paid-up capital.

Control Shifts. During investigation: Board continues under Inquiry Officer supervision (Section 15(1)), removable by court (Section 15(2)). During restructuring: Restructuring Manager assumes full control (Section 31(1)), directors suspended (Section 31(6)). During liquidation: directors relieved automatically (Section 38(1)(a)), Liquidator takes full control (Section 40).

Secured Creditor Rights. Automatically stayed during inquiry (Section 19), overriding BAFIA auction powers. During reconstruction, not bound unless consenting or court-ordered to prevent reconstruction failure. During liquidation, secured creditors regain enforcement rights; the liquidator has no claim over specifically secured property. For AMC design, the automatic stay is a double-edged sword: it preserves reconstruction possibility but prevents AMC enforcement during investigation and restructuring.

Restructuring versus Liquidation. The law prioritizes restructuring, allows fluid transition between the two, and supports going-concern sales. Creditors’ Meetings decide through proportional voting (by debt amount, not per-entity). Secured creditors generally cannot vote on restructuring unless waiving security. Court approval required for binding effect. Nepal lacks standardized informal workout mechanisms, forcing all complex resolutions into protracted litigation.

AMC’s Role. The AMC can function as a creditor: initiate insolvency (by formal demand, then court application after 35 days), vote in creditors’ meetings proportionally, participate in restructuring plans. The AMC cannot directly take management control unless appointed as Restructuring Manager or Liquidator. The AMC Act should provide standing for such appointments and clarify AMC rights during the automatic stay period.

3.7 Tax Frictions

NPL Sale as Taxable Event. Under the Income Tax Act, 2058, disposal of business assets is taxable. Banks may deduct up to 5% of total outstanding loans for NPL provisions; recovered or sold provisions are adjusted in that year’s income.

The Section 57 Penalty. If more than 50% of company ownership changes within three years, the company is deemed to have disposed of all assets at market value, subjected to 25% tax on deemed gains, and permanently loses loss carry-forward rights. This destroys the viability of AMC-led debt-to-equity swaps for corporate restructuring.

Loss Carry-Forward. General losses carry forward for 7 years; infrastructure, electricity, and petroleum for 12 years. The Section 57 ownership-change restriction specifically penalizes restructuring.

Capital Gains. Non-business assets (land, buildings): 5% if held over 5 years, 7.5% if less. Listed shares: 5% over 365 days, 7.5% under. Entities: 10% on listed, 15% on non-listed shares. M&A exemption exists for bank mergers (share sales within 2 years exempt, dividends within 2 years exempt, golden handshake at 50% discount).

Property Transfer Taxes. Transfer from bank to AMC and AMC to buyer triggers taxes at each step. No AMC-specific exemptions exist. The only partial relief is VAT Act Section 5A (going-concern transfer exemption between VAT-registered persons).

Tax Summary. Triple barrier: (a) transfer taxes erode recovery margins at each step; (b) Section 57 prevents debt-to-equity restructuring; (c) capital gains taxes reduce net recovery. Without comprehensive tax neutrality provisions, the AMC is commercially unviable from inception.

3.8 Securities and Capital Markets Framework

Legal Form. A review of the current capital market framework suggests that an AMC could be incorporated as a company (SIF Regulation 2075, Rule 3(1)(Ka); Portfolio Management Guidelines 2067, Rule 2(Ga)). Its operations could also be structured and managed in a manner similar to mutual funds, with fiduciary oversight by a Fund Supervisor (Mutual Fund Regulation 2067, Rule 6(1)). Eligible investors include pension, retirement, provident, welfare funds, and the Citizen Investment Trust (SIF Regulation 2075). Foreign investment is permissible with government approval, and NRN companies may hold up to 49% in a Scheme Manager. However, as these frameworks are not specifically designed for AMC functions, the introduction of a dedicated NRB or SEBON regulation – or preferably a separate legislation, given the multi-regulatory nature of AMC operations – would be more appropriate.

Critical Gaps. Security receipts are not legally recognized. No securitization law exists. No loan trading platform exists. No secondary NPL market, distressed debt specialists, or institutional distressed investors exist. FATF grey-list status deters international capital. Foreigners generally cannot own Nepali real estate, limiting the buyer universe for AMC assets. These gaps must be addressed through companion securitization legislation.

3.9 Criminal Overlay: Banking Offences

Willful Default versus Business Failure. NRB Unified Directive No. 12/2081, Section 5 distinguishes willful defaulters (out of contact for one-year, intentional avoidance, fund diversion, document fraud, collusion) from circumstantial defaulters (natural disasters, adverse conditions, regular contact, good-faith efforts, government land acquisition).

Criminal Proceedings and Recovery. The Banking Offence and Punishment Act, 2064 mandates Bigo recovery alongside fines (Section 15), allows confiscation of hidden assets from family (BAFIA Section 104(6)), creates personal liability (up to 12 years imprisonment), and permits asset freezing (Section 24). However, criminal proceedings delay civil recovery through document seizure (Section 20), potential civil tribunal stays, criminal asset freezes preventing auctions, lengthy investigation (60-day custody) and trial processes. Settlement exists for cheque bounce cases (Section 26k) but not other offences.

AMC Implications. The AMC Act should require police to provide certified document copies to the AMC for civil enforcement, and should provide that criminal proceedings do not automatically stay AMC enforcement actions.

PART IV: GAP ANALYSIS - NEPAL VERSUS THE IDEAL AMC ECOSYSTEM

4.1 Gap Matrix

The following matrix identifies the critical gaps between Nepal’s current legal and institutional framework and the prerequisites for a functioning AMC ecosystem, benchmarked against international best practice.

Dimension | International Best Practice | Nepal’s Current Status | Gap Severity |

Extra-judicial enforcement (immovable property) | SARFAESI-type powers: seize, possess, sell immovable collateral without prior court order | No equivalent. BAFIA Section 57 allows bank auction but no step-in/management takeover powers. Land regime is court-dependent for disputes. | Critical |

Statutory vesting of transferred assets | Upon issuance of vesting certificate, all rights, title and interest automatically transfer to AMC (Danaharta model) | No statutory vesting mechanism. Each transfer requires individual documentation, registry updates, and potentially borrower consent. | Critical |

Tax neutrality for NPL transfers | Exemption from stamp duty, capital gains, registration fees for AMC transactions | Full taxation at each transfer step. Section 57 Income Tax Act penalizes ownership changes above 50% by destroying loss carry-forwards. | Critical |

Securitization framework | Legal recognition of security receipts; issuance and trading infrastructure | No securitization law. Security receipts not legally recognized. No distressed asset instruments. | Critical |

Secondary market for distressed assets | Active institutional investors, distressed debt funds, pricing benchmarks | No secondary market, no specialized investors, no foreign participation framework. FATF grey-list deters international capital. | Severe |

Borrower consent for bulk transfer | Non-consensual transfer with notice only (special AMC legislation overrides general contract law) | BAFIA Section 122 generally requires customer consent for credit purchase. Exception exists only for agriculture/energy sectors. | Severe |

DRT capacity | Multiple specialized tribunals, 90-150 day resolution | Single DRT for entire country. 451 pending cases. 910 days average contract enforcement. | Severe |

Insolvency framework | Time-bound resolution, creditor-in-possession, going-concern priority | Insolvency Act 2063 exists but used mainly for liquidation. No informal workout framework. No fast-track restructuring. | Moderate |

Valuation infrastructure | Independent, certified, standardized valuation professionals | Severe deficit of internationally certified valuation professionals. Opaque real estate valuations. | Moderate |

Professional AMC workforce | Specialists in distressed asset management, investment banking, corporate restructuring | Skills scarce within traditional Nepali banking sector. | Moderate |

4.2 The Binding Constraint: Judicial Bottlenecks

Of all the gaps identified, judicial enforcement capacity represents the binding constraint. Without judicial reform, expanded DRT capacity, streamlined foreclosure processes, and resolution of land title disputes, an AMC would simply warehouse distressed assets rather than resolve them. The AMC would face the same 910-day enforcement timeline, the same single DRT, and the same susceptibility to injunctive stay orders that currently impede bank-level recovery.

This is precisely why the IMF recommends reforming debt enforcement before establishing an AMC. The global evidence is clear: AMCs that operated within efficient judicial environments (NAMA in Ireland, KAMCO in South Korea, Danaharta in Malaysia) achieved high recovery rates. Those that operated in weak judicial environments became permanent warehouses (SAREB in Spain with its illiquid land portfolio, China’s Big Four that diversified away from resolution entirely).

PART V: POLICY DEVELOPMENTS AND CURRENT STATUS

5.1 Historical Timeline: 2001 to 2026

The AMC concept in Nepal has a 24-year history. NRB formed its first task force on asset management in 2001, chaired by Executive Director Rajan Singh Bhandari, following the Financial Sector Reform Program that addressed catastrophic NPLs in state-owned banks (where NPL ratios exceeded 50%). The task force submitted recommendations that were shelved on the grounds that banks already possessed sufficient legal authority for loan recovery.

The idea languished for over two decades until the post-COVID surge in bad loans revived urgency. The current momentum began with NRB Governor Maha Prasad Adhikari’s Monetary Policy for FY 2024/25 (July 2024), which formally committed to preparing draft AMC legislation. NRB concluded that establishing an AMC under existing company law would effectively create a “real estate company” rather than a resolution vehicle, necessitating specialized legislation with special powers.

In October 2024, the cabinet formed a High-Level Economic Reform Advisory Commission chaired by former Finance Secretary Rameshore Khanal, which submitted a 447-page report in March 2025 recommending establishment of a bad bank through a public-private partnership model requiring separate legislation. President Ramchandra Paudel included AMC establishment in the government’s official policy and programs for FY 2025/26 (May 2025). Finance Minister Bishnu Prasad Paudel reiterated the commitment in his budget speech (June 2025). The Monetary Policy for FY 2025/26 (July 2025), under new Governor Dr. Biswo Nath Poudel, continued the agenda, committing to draft AMC legislation alongside an asset quality review. As of late 2025, the NRB finalized a preliminary draft of the Asset Management Company Act.

5.2 Proposed Institutional Design

The proposed AMC design envisions a Public-Private Partnership (PPP), with capital participation from the Government of Nepal, NRB, and the commercial banks themselves, a structure mirroring the existing Deposit and Credit Guarantee Fund (DCGF). The draft legislation aims to endow the AMC with authority to acquire NPLs at discounted rates, hold NBAs without punitive 100% provisioning, and orchestrate gradual liquidation as market conditions improve.

Key design disagreements persist. Nepal Bankers’ Association President Santosh Koirala advocates a PPP model with joint government-BFI ownership. Former banker Parshuram Kunwar Kshetri favors full government ownership to prevent conflicts of interest, suggesting the AMC issue bonds countable toward banks’ statutory liquidity requirements. Dr. Gunakar Bhatta of NRB’s Financial Research Department has flagged the fundamental capitalization challenge: an estimated NPR 10 billion in initial capital may be insufficient given the scale of distressed assets. Former task force chair Rajan Singh Bhandari argues that current NPL levels do not warrant a full AMC.

5.3 The IMF Position

The IMF’s engagement has been the most significant external influence. Its 6th ECF Review (October 2025) includes a dedicated Annex IV on AMC design considerations that explicitly cautions against premature establishment. The IMF’s pre-conditions include: (a) exhaustion of supervisory measures compelling banks to use all internal restructuring tools; (b) strict governance and political independence with IFRS-based audit; (c) defined scope limited to specific asset classes with a non-renewable sunset clause, explicitly excluding unregulated entities like SACCOs; (d) no regulatory forbearance allowing the AMC to delay necessary loss recognition by banks; and (e) completion of the Loan Portfolio Review to establish an accurate baseline of true asset quality.

IMF Deputy Managing Director Bo Li stated that AMC establishment “should be approached with caution given potential risks.” The IMF’s recommendation represents not a rejection of the concept but a logical sequencing that maximizes the probability of success.

5.4 Existing Functional Equivalents

In the absence of a formal AMC, Nepal operates several functional equivalents. First, each commercial bank operates internal recovery and NBA management departments, processing restructuring, rescheduling, and auctioning in accordance with NRB Unified Directives. Second, NRB-directed mergers have consolidated BFIs from over 200 to approximately 107, with 245 BFIs involved in mergers and acquisitions by mid-July 2022, resulting in 178 license revocations to form 67 consolidated entities. Third, the Credit Information Bureau’s blacklisting system creates indirect enforcement pressure. Fourth, consortium lending requirements mandate that loans of NPR 1 billion and above must be issued on a consortium basis. Fifth, Specialized Investment Fund (SIF) licensees under SEBON regulations possess the theoretical legal mandate to target undervalued or distressed companies, but the framework was designed for growth equity, not mass distressed debt resolution, and is constrained by the Section 57 tax penalty.

PART VI: COMPARATIVE INSTITUTIONAL ANALYSIS

6.1 What KAMCO Did Differently

South Korea’s KAMCO provides the most instructive positive case study for Nepal. KAMCO’s effectiveness relative to the originating banks derived from six structural advantages. First, special legal authority: KAMCO had faster foreclosure rights, the ability to override procedural delays, and centralized enforcement, powers that banks operating under standard judicial processes did not possess. Second, scale and aggregation: KAMCO aggregated portfolios from multiple banks, enabling it to sell entire asset pools and restructure large corporate groups, overcoming the coordination failure that plagues individual bank recovery efforts. Third, multi-creditor coordination: KAMCO could lead restructuring binding all creditors, whereas individual banks faced the “who takes the loss first” problem. Fourth, market-making: KAMCO created Asia’s first secondary market for distressed assets, attracting international private equity and distressed debt investors. Fifth, professional specialization: KAMCO employed asset turnaround specialists, legal enforcement strategists, and investor sales professionals, distinct from the lending-focused skillset of commercial bankers. Sixth, funding flexibility: KAMCO could issue government-backed bonds and take a longer-term recovery view, unconstrained by the depositor pressure and short-term liquidity requirements facing banks.

6.2 South Asian Experience: Caution Rather Than Urgency

The experiences of Nepal’s regional peers offer sobering lessons. India’s NARCL, the most directly comparable recent initiative, has underperformed expectations since its 2021 establishment. After initially targeting Rs 50,000 crore in acquisitions, NARCL had acquired only Rs 21,350 crore by late 2023. Its first resolution payouts, for Metenere Ltd and Helios Photo Voltaic, involved haircuts of 95% and 97% respectively, with cash recoveries of only 4.5-6%. India’s broader ARC sector, with 27-28 registered entities, recovered only 14.29% historically. India’s dramatic NPL improvement is attributed primarily to the Insolvency and Bankruptcy Code, enhanced risk management, and economic recovery, not to ARCs.

Bangladesh’s experience is even more cautionary. With NPL ratios of 16.93% as of September 2024, Bangladesh drafted a state-run AMC act (BAMCO) in 2020. The World Bank and IFC heavily criticized the draft for lacking key design elements: no sunset clause, no clear asset transfer methodology, potential conflicts of interest, and no transparency requirements. Bangladesh has since abandoned the public AMC model entirely, pivoting toward private-sector-led NPL resolution under a Distressed Asset Management Ordinance.

Pakistan’s Corporate Restructuring Company (PCRCL), established in 2019 by ten major banks, illustrates the limits of a small-scale AMC: with only seven employees, its impact has been negligible. The collective lesson is stark: no South Asian country has achieved transformative NPL resolution through AMCs alone.

PART VII: CRITICAL ASSESSMENT, REFORM ROADMAP, AND LEGISLATIVE BLUEPRINT

7.1 The Pricing Dilemma and Fiscal Risk

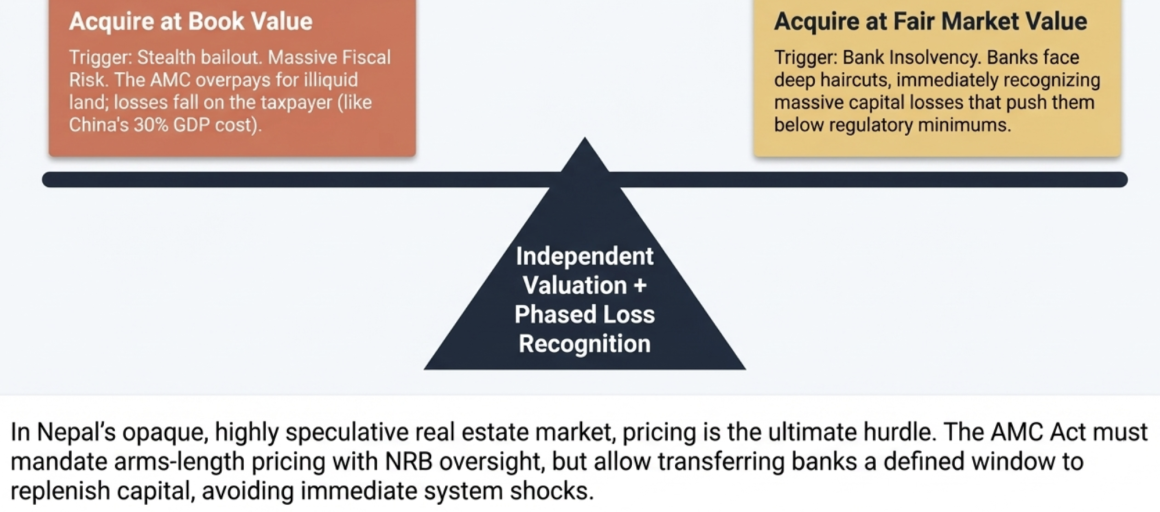

The most formidable operational obstacle to a successful AMC in Nepal is transfer pricing. If the AMC acquires NPLs and NBAs at near book value to protect originating banks from capital losses, it will grossly overpay, and when it eventually sells the underlying real estate at depressed market value, the loss falls on its shareholders, which under the PPP model includes the government and taxpayer. This constitutes a stealth bailout of private banking failures using public funds. The fiscal cost of China’s original bank clean-up, which involved book-value transfers, was estimated at roughly 30% of GDP.

Conversely, if the AMC enforces strict commercial discipline and acquires at deep discount reflecting fair market value, the transferring banks must immediately recognize massive capital losses, potentially pushing several below regulatory minimums and triggering the instability the AMC was designed to prevent. Bridging this gap requires a transparent pricing methodology (independent valuation, standardized discounting models) combined with mechanisms for phased loss recognition by transferring banks (allowing capital replenishment over a defined period rather than an immediate shock).

This dilemma is particularly acute in Nepal, where real estate valuations are opaque, speculative, and historically used to mask underlying credit weakness, and where the real estate market is illiquid. The AMC Act must mandate independent, arms-length pricing with NRB oversight, prohibit transfers at above fair market value, and provide a phased capital restoration window for transferring banks.

7.2 The Risk of Permanent Warehousing

Given that Nepal’s primary distressed assets are physical real estate (NBAs) rather than operating corporate enterprises, the AMC risks becoming a static warehouse for unmarketable land. Unlike KAMCO, which could restructure manufacturing plants and sell them as yielding going concerns, a Nepali real estate AMC relies entirely on macroeconomic recovery of property prices. If the market is undergoing structural correction, the AMC holds unsellable land indefinitely, generating massive holding costs and defeating its purpose. This is precisely the problem that plagued SAREB in Spain, where a portfolio dominated by undeveloped land proved far harder to resolve than anticipated. The risk is exacerbated by Nepal’s land constraints: subdivision restrictions, zoning locks, tenant rights, and corporate ceiling limits all prevent the AMC from actively creating value through land development or fragmentation for sale.

7.3 Sequencing: Reform the Ecosystem Before Building the Institution

Three insights emerge from global evidence and Nepal’s specific circumstances. First, the AMCs that succeeded (RTC, KAMCO, Danaharta, NAMA) operated within legal environments providing special powers, adequate funding, political insulation, and efficient judicial enforcement. Nepal currently lacks all of these. Second, at approximately NPR 254 billion in estimated NPLs across 107 institutions, Nepal’s distressed asset market may be too small to justify centralized AMC overhead, particularly when the problem is concentrated in a sluggish real estate market. Third, the IMF’s recommendation to exhaust supervisory measures, reform debt enforcement, develop distressed debt markets, and complete the LPR before establishing an AMC represents logical sequencing that maximizes success probability. Nepal is attempting to build the institution before the ecosystem that would make it effective.

7.4 Reform Roadmap

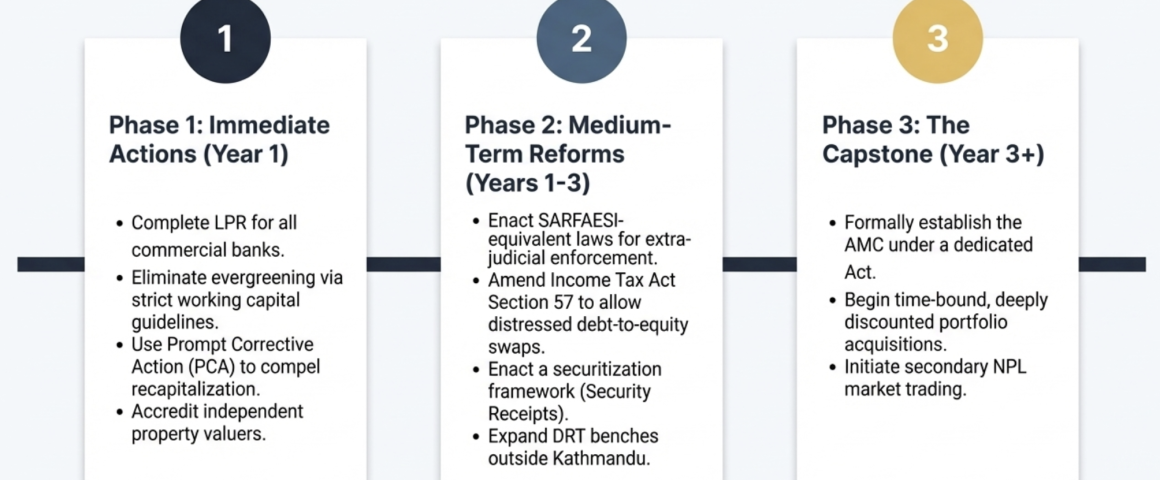

Immediate Actions (Year 1). Complete the Loan Portfolio Review for all commercial banks, not just the ten largest. Enforce honest asset classification by eliminating evergreening through strict enforcement of working capital loan guidelines and independent verification. Compel bank recapitalization where the LPR reveals capital shortfalls, using the existing PCA framework under NRB’s Prompt Corrective Action Bylaws, 2074. Strengthen DRT by expanding capacity (additional benches in regional centers outside Kathmandu), increasing staffing, enforcing the 150-day statutory timeline, and creating dedicated AMC fast-track windows. Establish an independent valuation board or accredit qualified property valuers to provide standardized, empirical valuations of real estate collateral.