This post synthesises findings from a technical research covering twenty-one commercial bank annual reports, NRB Bank Supervision Reports 2013–2024, NRB Current Macroeconomic and Financial Situation Reports 2016–2026, FIU-Nepal Annual Reports, and primary legislations including BAFIA 2017, NRB Act 2002, National Civil Code 2017, Companies Act 2006, Securities Act 2006, Secured Transactions Act 2006, FITTA 2019, Lands Act 2021, Land Revenue Act 1978, and Land Use Act 2019.

The Core Finding

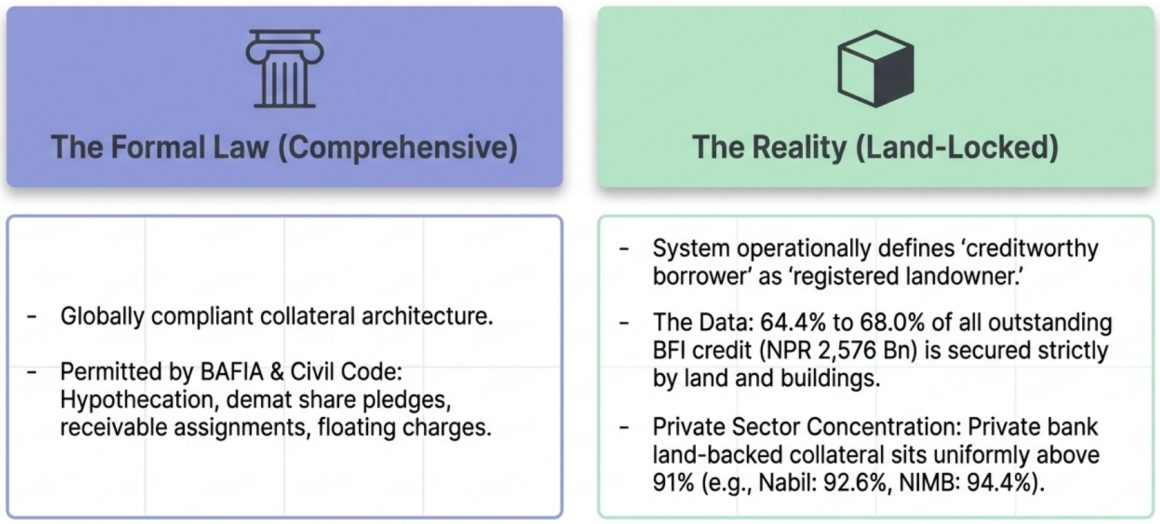

Nepal’s legal framework for lending security is formally comprehensive. The Bank and Financial Institutions Act, 2017 (BAFIA), the National Civil Code, 2017, the Companies Act, 2006, the Securities Act, 2007, the Secured Transactions Act, 2006, and the Foreign Investment and Technology Transfer Act, 2019 (FITTA) collectively authorise mortgages (non possessory mortgage drishtibandhak, possessory mortgage bhogbandhak over immovable assets), pledges (dharautbandhak), hypothecation (chal sampati mathiko dhito byabastha), debenture trust structures, demat share pledges, receivable assignments, floating charges, and personal and institutional guarantees. [Dhitobandhak (collateral / security) is a general umbrella term that means security arrangement over any asset.] In formal design, Nepal’s collateral (Dhito) architecture is broadly consistent with international norms.

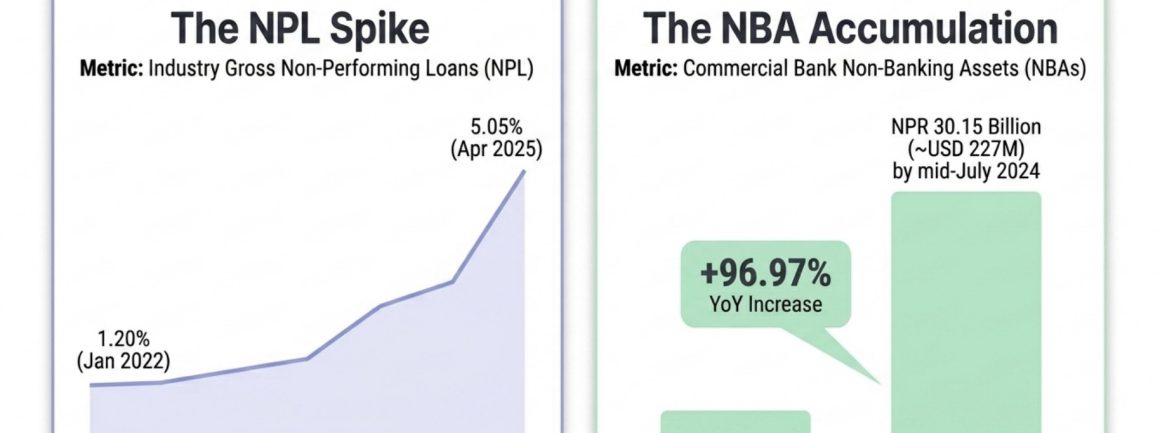

In practice, it is not. Between 60.8% and 68.0% of all outstanding BFI credit has been secured by land and buildings throughout the decade 2016–2025, peaking at 68.0% in 2023 and standing at 64.4% as of November 2025 (NRB Current Macroeconomic and Financial Situation Reports, 2016–2026). At approximately NPR 2,576 billion (~USD 19.1 billion at NPR 135/USD 1), land-backed credit is the largest single category of financial obligation in Nepal’s formal economy. The Secured Transactions Act, 2006, enacted specifically to build a modern movable asset registry and end this dependence, has remained not much effective for nearly two decades. SME organic credit has stood at 2.6% of commercial bank portfolios when measured without government subsidy – identical in 2016 and 2017, unchanged after a decade of policy attention (NRB CMFS Report 2016/17, Monetary Situation, p.10). The industry Non-Performing Loan (NPL) ratio has risen from 1.20% in early 2022 to 5.05% by April 2025 (NRB CMFS Report November 2025), and commercial bank non-banking assets (NBAs “Non Banking Assets” – properties seized from defaulted borrowers after failed auctions, governed by NRB Unified Directive 2/2081, Clause 11) increased 96.97% in FY 2023/24 alone, reaching NPR 30.15 billion (~USD 226.7 million at NPR 133/USD) (NRB Bank Supervision Report 2023/24, Sections 3.7–3.8).

These are not incidental problems. They are structural symptoms of a credit system that has operationally defined a creditworthy borrower as a registered landowner – not because law requires this, not because economics demands it, but because land is the only asset class for which Nepal has built an administrative infrastructure closest to satisfying all four conditions a rational lender requires: reliable creation, real-time searchability, third-party exclusion, and reasonably predictable enforcement – but with constraints (discussed later).

This post diagnoses the five structural constraints producing that outcome, documents their economic consequences, and advances a specific, institution-mapped reform agenda capable of resolving them.

What the Law Permits and What Banks Do

Table 1: BFI Credit Collateral Composition and Credit Growth, 2016–2025

Year | Land & Buildings (% total BFI credit) | Current Assets (%) | Pvt Sector Credit Growth (%) |

2016 | 60.8% | 15.2% | 23.7% |

2018 | 61.7% | 14.4% | 22.5% |

2020 | 65.7% | 13.0% | 12.6% |

2021 | 66.1% | 12.7% | 27.3% |

2022 | 66.4% | 12.3% | 13.1% |

2023 | 68.0% | 11.6% | 3.8% |

2024 | 66.5% | 13.5% | 5.8% |

Nov 2025 | 64.4% | 15.0% | 6.1% |

Sources: NRB CMFS Reports 2016–2026.

The law formally permits hypothecation of inventory and receivables (National Civil Code, 2017, and Working Capital Loan Guidelines, 2079); share pledges through the CDS/CDSC electronic depository system (Securities Central Depository Service Bylaws, 2012, Rule 26); functional floating charge equivalents over company undertakings (Companies Act, 2006, Sections 34–36); receivable assignments for movable and intangible assets (Civil Code, 2017, Section 529); project cash flow financing for hydropower and infrastructure (BAFIA 2017, Section 49(1)(Gha), Section 55(2)); and unsecured lending against group guarantees in the deprived sector (NRB Unified Directive 17/2081). Banks do not meaningfully use most of these. Overdraft facilities – the primary vehicle for working capital against hypothecated stock – collapsed from 14.85% of commercial bank credit in FY 2021/22 to 2.01% in FY 2023/24, largely reclassified following the Working Capital Loan Guidelines, 2079 (NRB CMFS Report 2023/24, Table 7). Share-backed margin lending has oscillated between 1.36% and 2.45% of total commercial bank credit over the period of 2019-2025 (NRB CMFS Reports). Receivable financing outside documentary trade finance is functionally absent: no commercial bank in the reviewed corpus of twenty-one annual reports identifies domestic receivables financing as a product line.

Table 2: Selected Commercial Bank Collateral Composition, FY 2023/24–2024/25

Bank | Type | Gross Loans (NPR Bn) | USD Equiv. | Land/Bldg (%) | Gold (%) | Guarantees (%) | NPL (%) |

Nabil Bank | Private | 391.30 | ~USD 2,941M | 92.6% | <0.1% | 0.5% | 4.45% |

NIMB | Private | 326.37 | ~USD 2,453M | 94.4% | 0.5% | 0.1% | 4.91% |

Himalayan | Private | 247.10 | ~USD 1,858M | 92.4% | <0.1% | <0.1% | 4.98% |

Kumari | Private | 291.00 | ~USD 2,156M | ~92.0% | <0.1% | 0.1% | 5.96% |

Everest Bank | JV | 226.51 | ~USD 1,678M | 87.1% | 0.0% | 0.5% | 0.38% |

Standard Chartered | JV | 72.89 | ~USD 540M | 83.8% | 0.0% | 11.9% | 1.41% |

Nepal Bank | State | 205.58 | ~USD 1,546M | 67.2% | 10.9% | 4.8% | 4.28% |

ADBL | State | 222.46 | ~USD 1,648M | 97.5% | 0.003% | 0.0% | 3.26% |

Sources: Individual bank annual reports FY 2080/81–2081/82, Note 4.7.3. USD conversions at NPR 133/USD 1 (2080/81) and NPR 135/USD 1 (2081/82).

The bank-level data is unambiguous. Private sector banks show land-backed collateral uniformly above 91%. The only commercial bank with meaningful collateral diversification at scale is Nepal Bank Limited – and that diversification is attributable to physical gold (10.9% of secured portfolio, NPR 22.33 billion, ~USD 167.9 million at NPR 133/USD), not to any productive-sector movable asset class. Agricultural Development Bank of Nepal (ADBL), Nepal’s dedicated agricultural lender, shows 97.5% land concentration despite an explicit mandate to serve rural and agricultural borrowers. Standard Chartered’s 11.9% guarantee exposure reflects rated foreign bank SBLCs (Standby Letters of Credit) for its corporate trade finance client base – not replicable across the sector. Everest Bank’s NPL of 0.38% against the sector’s 5.05% reflects a deliberate conservative lending culture and trade finance orientation, not a template for broader application.

Why This Happens: Five Structural Locks

The gap between legal permission and banking practice is produced by five interlocking constraints operating simultaneously. Resolving any one of them in isolation produces limited impact. Resolving them in sequence and combination – as the reform agenda could produce systemic change.

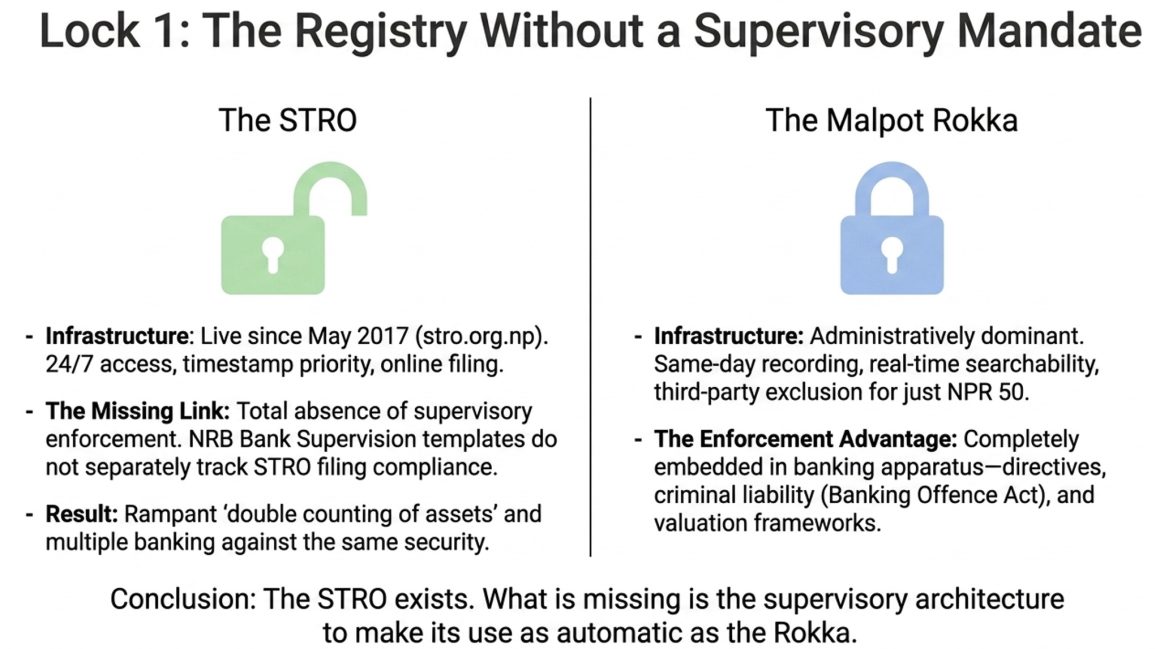

Lock 1 - Non-Functional Movable Asset Registry

The Secured Transactions Act, 2006 enacted a complete framework: any person could create a security interest in movable property – machinery, inventory, receivables, livestock, warehouse receipts, intellectual property – and perfect it through notice-filing in a centralised, publicly searchable registry. Priority would be determined by filing date. Enforcement would proceed without full civil court proceedings. The Act is modelled on the UNCITRAL Model Law on Secured Transactions.

The registry – the Secured Transactions Registration Office (STRO) – went live May 2017. Operated by Karja Suchana Kendra Limited (KSKL) under Ministry of Finance authorisation and accessible 24x7x365 at stro.org.np, the STRO provides free public search with no login required; client and non-client account access for BFI filers; online notice-filing for initial security interests, amendments, continuations, corrections, and terminations; priority dating from filing timestamp; search by debtor citizenship number, company registration number, or vehicle serial number; certified search reports with legal authentication; and a flat filing fee of NPR 565 per notice. The legal framework is complete. The technical infrastructure has been live for eight years.

The consequence for banking practice is direct and structural. A lender extending a working capital line against hypothecated inventory (a security interest in movable goods remaining in the borrower’s possession, governed by Working Capital Loan Guidelines, 2079) cannot verify whether the same inventory is already charged to another lender. NRB Bank Supervision Report 2013 (Section 5.12) identified “double counting of assets” and “multiple banking against the same security without pari-passu agreements” (pari-passu – equal ranking of creditors against shared security requiring proportional documentation) as systemic problems. The same finding appears in Bank Supervision Reports through 2024. Without a registry, it is unresolvable.

The rational institutional response is to demand land as additional or primary security – which moves the transaction back into the Malpot (Land Revenue Office, the administrative body responsible for land title registration under the Land Revenue Act, 2034) system. The Rokka (an administrative restriction on the transfer or disposal of a registered land parcel, recorded in the Rokka Kitab, the restriction register, under Land Revenue Act, 1978, Section 8kha, Fifth Amendment) provides what the STRO has not yet delivered in practice: same-day recording, real-time searchability, administrative third-party exclusion at a fee of NPR 50 (Land Revenue Rules, 1979, Schedule 1ka, approximately USD 0.37). The problem is not that banks irrationally prefer land. The problem is that land is the only asset class whose administrative infrastructure is embedded in the full institutional apparatus of banking – directives, criminal liability under the Banking Offence and Punishment Act 2008, valuation frameworks, supervision templates. The STRO exists. What does not yet exist is the supervisory enforcement architecture that would make its use as routine and automatic as the Malpot Rokka.

NRB has further embedded STRO use in its regulatory framework. Under the Working Capital Loan Guidelines, 2022 (integrated into the NRB Unified Directives), BFIs must obtain a STRO search report before accepting any movable property as collateral, to verify prior claims and establish priority. NRB Unified Directive 21/2081 mandates STRO filing at the time of loan disbursement or renewal for both hypothecation and pledge of current and movable assets. The Capital Adequacy Framework 2015, Clause 3.4 (Legal Certainty) requires that to claim credit risk mitigation capital relief, banks must take all necessary steps to fulfil “local contractual and statutory requirements” for enforceability – specifically listing “registering it with a registrar” as the operative step. Without STRO filing, movable collateral does not qualify for CRM capital relief. On paper, the system is complete: the registry is live, the mandate exists, and the capital incentive is written into the framework. Yet land-backed lending stands at 64–68% of total BFI credit, and NRB Bank Supervision Reports continue to identify “double counting of assets” and “multiple banking against the same security” as recurring sector-wide problems year after year through 2024.

The STRO has recorded approximately 537,000 total entries since going live in May 2017, of which around 411,000 are initial notices of security interest – averaging roughly 51,000 new filings per year. This is not a dormant registry. However, the continuation of land dominance patterns unchanged since 2017 – land-backed credit peaking at 68.0% of total BFI credit in 2023 despite eight years of STRO operation – indicates that filing volume has not translated into a structural shift in movable asset lending. The most probable explanation is sectoral concentration: the bulk of STRO filings are likely concentrated in hire purchase, vehicle finance, and microfinance – categories where filing is straightforward and collateral is a discrete physical asset – rather than in commercial bank working capital and enterprise lending, where the credit allocation impact would be largest. Without a publicly available breakdown of filings by institution type and collateral category, this assessment cannot be confirmed. That data should be published by KSKL as a mandatory quarterly reporting obligation to the Ministry of Finance and NRB.

The explanation is supervisory: NRB Bank Supervision templates do not separately track STRO filing compliance as a discrete audit metric for public disclosure, and the CAF’s CRM disqualification for unregistered movable charges is not routinely enforced at the level of individual loan file review.

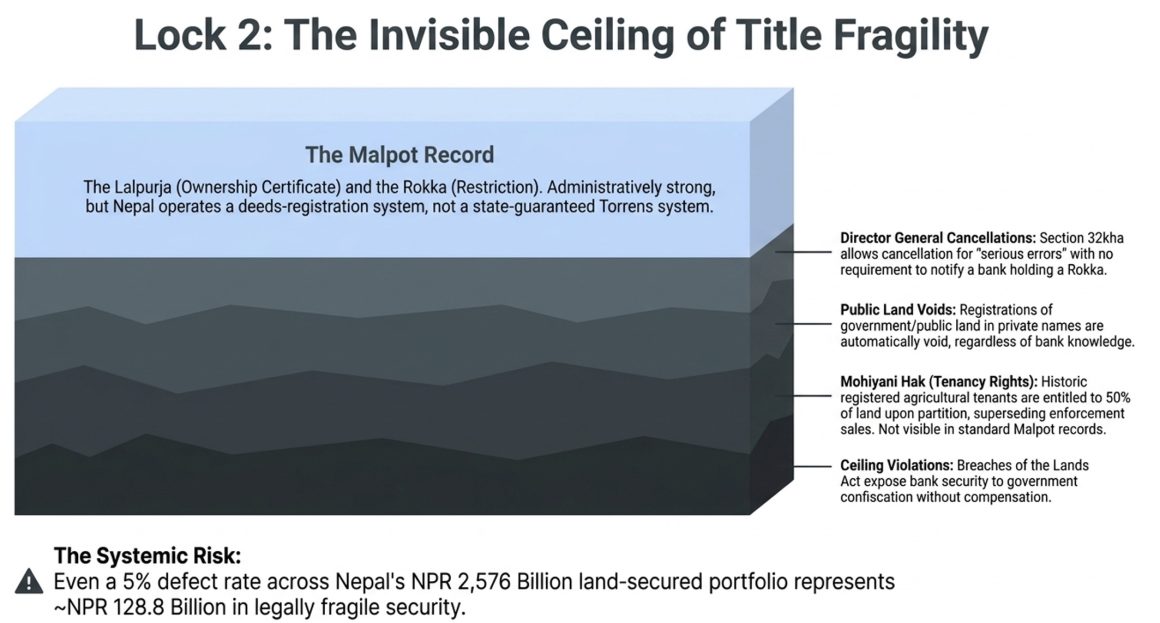

Lock 2 - Administratively Uncertain Land Title

The Rokka is administratively strong but substantively fragile. The Lalpurja (Jaggadhani Darta Pramanpurja – the official land ownership certificate issued by the Malpot office) is not an indefeasible title. Nepal operates a deeds-registration system – the state records transactions as presented, without guaranteeing their accuracy – rather than a Torrens system where the state investigates and guarantees title.

Four categories of latent defect can impair or extinguish a bank’s security interest after disbursement without appearing in the Malpot record:

- The Director General of the Department of Land Management may cancel a registration for “serious errors” (gambhir truti) before any court complaint is filed (Land Revenue Act, 1978, Section 32kha), with no requirement to notify a bank holding a Rokka against the affected title.

- Registrations of government, public, or community land in private names are automatically void regardless of bank knowledge (Land Revenue Act, Section 24(2)).

- Mohiyani hak (the statutory tenancy rights of registered agricultural tenants) entitles existing tenants to 50% of the land upon partition and survives all transfers and enforcement sales (Lands Act, 1964, Section 26(1) and Section 26gha(1)). Although Section 25(2) of the Act explicitly prohibits the creation of any new tenancy rights, historically registered rights remain fully protected and enforceable. Consequently, they present a significant hidden risk for lenders, as these existing encumbrances are not visible in the standard Malpot title records, which are maintained separately from the Bhumi Sudhar (land reform) tenancy records.

- Land ceiling violations expose bank security to government confiscation without compensation (Lands Act, 2021, Section 15), with landowners required to self-declare compliance and no systematic cross-verification.

The NRB Bank Supervision Report 2023/24 (Section 5.1.4) explicitly lists “fake collateral” and “false valuation” as emerging categories of banking fraud identified during on-site inspections. The scale of latent title defects across Nepal’s NPR 2,576 billion (~USD 19.1 billion) land-secured credit portfolio is unknown – no systematic title quality audit has been conducted – but even a 5% prevalence of material defects represents approximately NPR 128.8 billion (~USD 954 million at NPR 135/USD) in security whose legal basis is fragile.

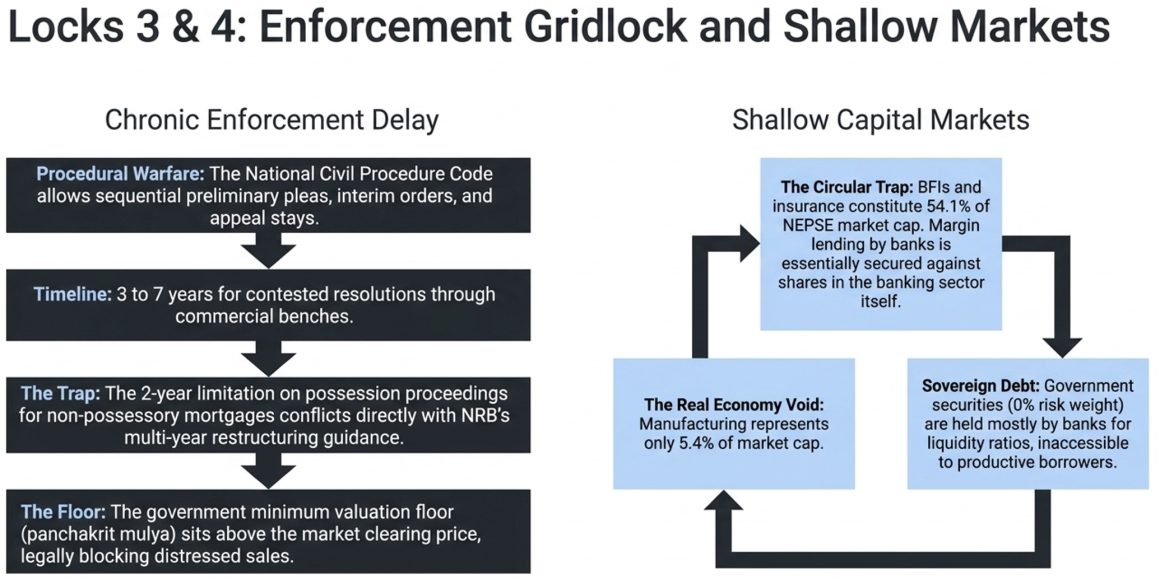

Lock 3 - Chronic Enforcement Delay and NBA Accumulation

A security right has economic value only to the extent it can be converted to cash within a commercially reasonable timeframe upon default. Nepal’s enforcement system cannot currently do this at the scale required.

The National Civil Procedure Code, 2017 (NCPC) provides borrowers multiple procedural avenues to delay enforcement: sequential preliminary pleas on jurisdiction, limitation, and locus standi (NCPC, Sections 131–133); interim orders maintaining the status quo of collateral pending petition (NCPC, Section 158(2)(c)), which are rarely enforced against losing petitioners; challenge rights within 15 days of any execution act (NCPC, Section 250(1)); and appeal stays through District Court, High Court, and Supreme Court, extending contested timelines to three to seven years. The two-year limitation on initiating possession proceedings for non-possessory mortgages, the standard commercial bank mortgage form) under Civil Code, 2017, Section 437(1)–(4) – which converts the mortgage to a kapali (unsecured bond) upon expiry – creates a hidden deadline that conflicts directly with NRB’s encouragement of multi-year restructuring for distressed borrowers.

The result is documented in Table 3. NBAs nearly doubled in a single fiscal year. Banks are not failing to create security interests. They are failing to convert those interests to cash.

Table 3: Industry NPL and NBA Trends, 2022–2025

Period | Industry Gross NPL (%) | Commercial Bank NBA (NPR Bn) | NBA Annual Change |

January 2022 | 1.20% | 8.64 | +27.51% YoY |

mid-July 2023 | 2.98% | 15.31 | +77.15% YoY |

mid-July 2024 | 3.94% | 30.15 (~USD 227M) | +96.97% YoY |

April 2025 | 5.05% | – | – |

Sources: NRB Bank Supervision Reports 2022–2024; NRB Annual Report 2081/82; NRB CMFS Report November 2025.

The additional constraint is the government minimum valuation floor (panchakrit mulya – set annually by district Minimum Valuation Committees under Land Revenue Rules, 1979, Rule 5kha(4)): transactions cannot be legally registered below this floor. In a stagnant market, the floor sits above the market clearing price, preventing distressed sales from completing. Nabil Bank’s Annual Report 2023/24 (p. 111) states explicitly that “disposal of NBAs is progressing slowly due to legal disputes and the real estate slowdown.” Global IME Bank (Annual Report 2081/82) publicly endorsed the need for a state-backed Asset Management Company to absorb NBAs – a recommendation appearing in a bank’s own annual report rather than in regulatory planning documents, which signals how acute the problem has become institutionally.

Lock 4 - Shallow Capital Markets

The CDS system operated by CDSC (CDS and Clearing Limited, licensed under the Securities Act, 2006) provides a technically sound electronic pledge mechanism for listed securities (Securities Central Depository Service Bylaws, 2011, Rule 26). The barrier to securities-based lending at scale is not the pledge mechanism – it is market composition.

NEPSE (Nepal Stock Exchange) market capitalisation stood at 69.85% of GDP as of November 2025 (NRB Annual Report 2024/25). Of that, BFIs and insurance companies constitute 54.1% of market capitalisation by mid-2025, down from 85.4% in 2017. Manufacturing – the productive sector most in need of enterprise credit – represents approximately 5.4%. This composition creates a dangerous circularity: margin lending by banks is secured against shares in the banking sector itself. A broad market decline simultaneously impairs the collateral value of margin loans and the capital position of the lending banks. The volatility this produces is structurally embedded: margin lending grew 110.8% in 2020/21 and contracted 24.3% in 2021/22 (NRB CMFS Reports 2020–2022). At 1.36%–2.45% of total commercial bank credit across the measurement period, it cannot serve as a structural alternative to land.

The government securities market, while carrying a 0% risk weight under the Capital Adequacy Framework 2015 and eligible for full credit risk mitigation treatment, is held primarily by banks themselves as part of their statutory liquidity ratio obligations. Productive sector borrowers do not hold government securities in lending-relevant quantities. The most capital-efficient collateral class in Nepal’s prudential framework is inaccessible to the borrowers the system most needs to serve.

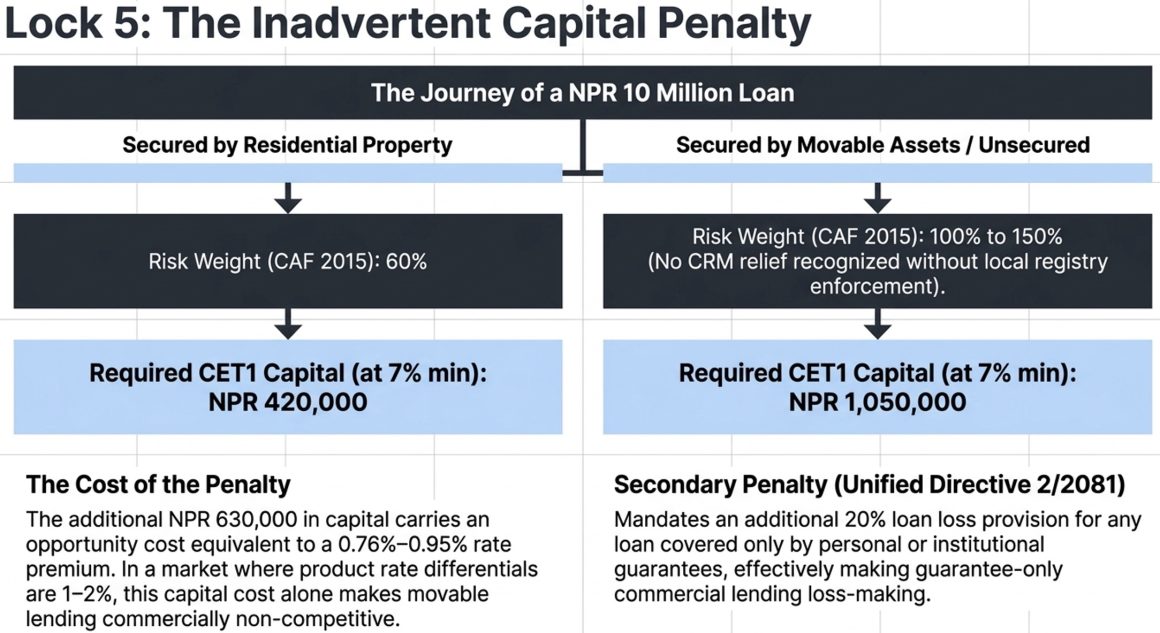

Lock 5 - Prudential Rules That Inadvertently Reinforce Land Preference

The Capital Adequacy Framework 2015 (CAF 2015) assigns residential property-secured loans a 60% risk weight and unsecured claims 150%. For movable-asset-backed lending – which carries 100% risk weight without credit risk mitigation (CRM) recognition – the differential versus residential property is 40 percentage points of capital efficiency. At Nepal’s minimum Common Equity Tier 1 ratio of 7% of risk-weighted assets (CAF 2015), a NPR 10 million unsecured loan requires CET1 capital of approximately NPR 1.05 million; the same loan against residential property requires only NPR 420,000. The additional NPR 630,000 in capital carries an opportunity cost of approximately NPR 75,600–94,500 annually at a 12–15% return on equity – equivalent to a 0.76–0.95% rate premium before any credit risk differential. On a market where product rate differentials are typically 1–2%, this capital cost alone makes unsecured commercial lending non-competitive.

The NRB Unified Directive 2/2081, Clause 10(10) compounds this by mandating an additional 20% loan loss provision for any portion of a loan covered only by personal or institutional guarantees. For a Pass-classified loan (1.3% base provision), a guarantee-only loan requires 21.3%. This penalty effectively makes guarantee-only commercial lending loss-making relative to collateralised alternatives and eliminates personal and institutional guarantees as viable primary security for SME borrowers.

The CAF 2015’s narrow definition of “eligible financial collateral” (yogya vittiya dhitamanpatra) – restricted to own-bank FDRs, physical gold, government securities, and rated institutional guarantees – means that every collateral class outside this tier attracts standard or elevated risk weights regardless of actual quality. This is the correct regulatory response to information asymmetry in the absence of a movable registry. It becomes a perverse incentive the moment a functioning registry is built. The prudential framework is calibrated for the infrastructure Nepal has, not the infrastructure Nepal needs.

What This Costs

The economic consequences of Nepal’s collateral regime extend well beyond bank balance sheets. Three deserve specific quantification.

SME exclusion and the missing middle. Organic SME credit – without government subsidy or mandatory targets – constituted 2.6% (NPR 35.87 billion, ~USD 335 million at NPR 107/USD) of commercial bank portfolios in 2016, and identically 2.6% (NPR 45.59 billion, ~USD 426 million) in 2017 (NRB CMFS Report 2016/17). A decade’s worth of policy attention produced zero organic growth. Apparent expansion has been entirely state-funded: government concessional loan programmes peaked at NPR 213.89 billion (~USD 1.61 billion at NPR 133/USD) for 147,393 borrowers in 2021/22 and have unwound to NPR 78.66 billion (~USD 583 million at NPR 135/USD) for 94,920 borrowers by 2024/25 (NRB Annual Report 2081/82). The Deposit and Credit Guarantee Fund (DCGF – the state-backed credit guarantee institution) guaranteed NPR 327.42 billion (~USD 2.42 billion at NPR 135/USD) in micro, agriculture, and SME loans as of mid-July 2025, up from NPR 65.11 billion (~USD 551 million at NPR 118/USD) in 2020 – a 402% increase representing a growing fiscal contingent liability substituting for a movable collateral market that does not work. A software company with NPR 50 million in annual contracts and no owned real estate cannot access a working capital line from any commercial bank in Nepal. A manufacturer with NPR 200 million in revenues secured against a NPR 20 million factory plot can access only NPR 10 million in credit at 50% LTV – 5% of annual revenue. Manufacturing’s share of GDP has declined from approximately 15.2% in 2018/19 to 12.83% in 2024/25 (NRB CMFS Report 2024/25, Real Sector, Table 1).

Infrastructure finance gap. Nepal requires approximately USD 46.5 billion in energy sector investment alone to reach its 2035 hydropower target of 28,500 MW installed capacity. Domestic commercial banking capacity – with total commercial bank assets of approximately NPR 5,500 billion (~USD 40.7 billion at NPR 135/USD) and Single Obligor Limits (SOL – maximum credit exposure to a single borrower or group as a percentage of BFI core capital, per NRB Unified Directive 3/2081) of 25% of core capital for standard exposures – cannot absorb this demand without foreign co-financing. Foreign co-financing requires enforceable security (partially addressed by FITTA, 2019, Section 20(4)), currency risk management (partially addressed by the Hedging Rules, 2079 for projects above 100 MW), and commercially reasonable enforcement certainty (substantially absent). The Hedging Rules, 2079 exclude the 50–100 MW hydropower range entirely: projects in this band are too large for domestic bank SOL without consortium financing and too small to access hedging protection, creating a structural financing gap for the most numerous segment of Nepal’s hydropower pipeline.

Wealth concentration and systemic inequality. The collateral regime functions as a systematic wealth transfer mechanism. Access to formal credit is gated by land ownership. Land appreciation increases credit capacity. Expanded credit capacity funds further land acquisition. Remittance inflows – reaching NPR 1,445.32 billion (~USD 10.87 billion at NPR 133/USD) in FY 2023/24, representing approximately 19.2% growth in FY 2024/25 (NRB CMFS Report 2024/25) – sustain this loop by providing liquidity that banks channel back into land-backed credit. Households with no path to land ownership – urban renters, landless agricultural workers, educated professionals without inherited property – are excluded from the formal credit-capital formation cycle regardless of their income, productivity, or creditworthiness. The criterion for credit access is asset class, not economic capacity.

The remittance-credit transmission mechanism is now structurally decoupling. Remittances grew 16.5% in FY 2023/24 and 19.2% in FY 2024/25, yet private sector credit expanded only 5.8% and 8.4% respectively – the lowest growth rates since the 2009/10 crisis. This decoupling signals that the credit expansion model of the previous decade – remittances fund deposits; deposits fund land-backed credit; land prices support the cycle – has reached structural exhaustion. What replaces it depends entirely on whether Nepal builds alternative collateral infrastructure before the current reform window closes.

The Reform Agenda

Twelve reforms constitute the minimum necessary agenda. They are organised into three time horizons based on institutional complexity and legislative requirements, not urgency – Reforms 1 through 6 are all urgent.

Table 4: Reform Blueprint Summary

Reform | Problem | Primary Institution | Timeline | Key Outcome Metric |

1. Operationalise Secured Transactions Act | STRO live since 2017; NRB mandate exists; supervisory enforcement and BFI adoption absent | Ministry of Finance / KSKL / NRB | 2025–2026 | STRO compliance tracked in BSR; quarterly stats published; CRM disqualification enforced |

2. Expand Eligible CRM to ESTR-registered charges | 40 ppt capital cost disadvantage vs land | NRB | 2026–2027 (post-ESTR) | Movable credit share +5–10 ppts |

3. Standardised Forced Sale Discount Matrix | Inconsistent NRV; minimum valuation gridlock | NRB (Part A); Ministry of Land Management (Part B) | 2025–2026 | Sector NRV consistency; NBA disposal improvement |

4. Banking Sector Asset Management Company | NPR 30Bn NBA accumulation | NRB; Ministry of Finance | 2025–2027 | NPR 30Bn NBA transferred; 30% disposed within 24 months |

5. Extend Hedging to Projects Above 50 MW | 50–100 MW infrastructure finance gap | Ministry of Finance | 2025–2026 | 20+ projects newly eligible |

6. Civil Code Limitation Conflict Resolution | Two-year mortgage limitation vs restructuring | Ministry of Law | 2026–2027 | Amendment enacted |

7. Operationalise Warehouse Receipt System | Agricultural credit access | Ministry of Agriculture | 2027–2029 | 50 warehouses; NPR 50Bn agri-WR credit |

8. Commercial Insolvency Courts | 3–7 year insolvency resolution | Ministry of Law; Supreme Court | 2027–2030 | Median resolution <18 months |

9. BFI Mortgage Title Protection | Latent title defect risk | Ministry of Land Management | 2027–2029 | Safe harbour provision enacted |

10. Corporate Bond Market Development | Absent debt capital market | SEBON | 2027–2030 | 50 rated issuers; NPR 200Bn outstanding |

11. Land Tenure Rationalisation | Mohiyani hak; ceiling complexity | Ministry of Land Management | 2030–2035 | Integrated digital land system |

12. SME Cashflow Lending Framework | Collateral-centric credit assessment | NRB | 2028–2032 | SME credit 8–10% organic |

Reform 1: Operationalise the Secured Transactions Act, 2006

The STRO is already built. The Secured Transactions Registration Office (STRO), operated by Karja Suchana Kendra Limited (KSKL) at stro.org.np under Ministry of Finance oversight, has been live since May 2017. NRB already mandates pre-lending STRO search (Working Capital Loan Guidelines, 2079) and post-disbursement STRO filing (Unified Directive 21/2081). The Capital Adequacy Framework 2015, Clause 3.4 already withholds CRM capital relief for movable charges not registered with a registrar. The reform required is not institutional construction – it is supervisory enforcement of what already exists.

The STRO’s design already replicates the Malpot Rokka’s core features: online notice-filing, real-time public search, priority dating from filing timestamp, and nominal fees (NPR 565 per filing). What it lacks is the institutional embedding that makes the Rokka automatic – mandatory pre-lending searches, post-disbursement filing timelines enforced on-site, and capital consequences for non-compliance enforced at the loan file level. The Malpot Rokka works not only because it is functional but because the entire supervision and credit culture apparatus is built around it. The STRO requires the same surrounding architecture, applied by NRB through its existing directive authority.

Responsible institutions: Ministry of Finance (primary oversight of STRO through KSKL); NRB (supervisory mandate enforcement; CAF Clause 3.4 operationalisation; BFI participation requirements); KSKL (STRO operations; quarterly statistics publication). Estimated credit capacity that enforced STRO compliance could unlock: NPR 300–500 billion (~USD 2.2–3.7 billion at NPR 135/USD) within 24 months, by enabling verification and priority establishment for movable security without additional bank capitalisation.

Three specific NRB actions – all within existing authority under NRB Act, 2002, Section 79, none requiring parliamentary legislation – would transform STRO from an available option to a functional component of the credit system: First, add STRO filing compliance as a mandatory, separately reported metric in NRB Bank Supervision templates and on-site inspection checklists. Banks must demonstrate, per loan file, that a STRO search was conducted before movable collateral was accepted and that a STRO notice was filed within the prescribed timeline at disbursement. Non-compliance should be treated as a collateral documentation failure, triggering the same provisioning consequence as any other documentation deficiency. Second, issue explicit supervisory guidance operationalising CAF Clause 3.4: any movable asset collateral for which no STRO filing can be evidenced in the credit file is automatically excluded from Credit Risk Mitigation calculation, and the full counterparty risk weight (100% or 150%) applies. This guidance requires no amendment to the CAF – it operationalises what Clause 3.4 already says. Third, require KSKL to publish quarterly STRO aggregate statistics – number of initial notices filed, active notice count, search volume, and geographic and sectoral distribution – as part of its regulatory reporting to the Ministry of Finance and NRB. Without transparency on adoption rates, neither regulators nor the banking sector can assess whether the mandate is being followed.

Reform 2: Expand Eligible CRM to ESTR-Registered Movable Charges

Once Reform 1 is operational, the 40-percentage-point capital cost differential between land-backed and movable-backed lending loses its justification. The differential exists because movable collateral cannot be verified without a registry. Once verifiable, the information asymmetry is resolved and the capital penalty is unwarranted.

Amend the Capital Adequacy Framework 2015 to create a new eligible collateral category: “Registered Movable Asset Charge – ESTR-Perfected.” For charges registered in the ESTR within 30 days of creation and verified as first-priority through ESTR search: apply a 20% supervisory haircut to qualifying movable assets (consistent with the haircut applied to other-BFI FDRs under NRB Unified Directive 2/2081); allow the net value after haircut to reduce credit exposure for risk-weighting, producing a blended risk weight between 100% and the reduced exposure; set a minimum floor risk weight of 50% for the most liquid registered categories such as trade receivables from rated counterparties.

This reform must follow, not precede, Reform 1. Risk weight reduction before the registry exists creates a perverse incentive to assert unverifiable filings. Responsible institution: NRB (CAF amendment falls within existing authority under NRB Act, 2002, Section 79).

Reform 3: Standardised Forced Sale Discount Matrix and Minimum Valuation Reform

No standardised methodology exists for calculating Net Realizable Value (NRV – the estimated collateral recovery after forced-sale discounts, foreclosure costs, and time adjustment) for loan loss provisioning. Each bank determines its own haircut methodology, producing inconsistent Expected Credit Loss (ECL) calculations and unreliable system-level capital adequacy assessments. The NRB ECL Related Guidelines, 2024 require the methodology; they do not prescribe its content.

- Part A: NRB to publish, in consultation with the Institute of Chartered Accountants of Nepal (ICAN), a Collateral Valuation and Forced Sale Discount Guideline establishing category-specific discount ranges by urban/peri-urban/rural classification and road access status; maximum valuation report age for provisioning purposes (24 months maximum; annual for Watch List classification and below); mandatory use of ICAN-registered valuers for property above NPR 50 million (~USD 370,400 at NPR 135/USD 1); and annual back-testing comparing NRV estimates against actual auction realisations.

- Part B: Ministry of Land Management to amend the Land Revenue Rules, 1979, Rule 5kha to permit BFI-initiated distressed sales to proceed below the government minimum valuation (panchakrit mulya) where three auction attempts have failed at minimum valuation, the transaction involves an arm’s-length purchaser and a bank acting under court or NRB supervision, and applicable capital gains tax is calculated on the actual transaction price. This removes the minimum valuation floor as a barrier to distressed asset clearing without eliminating it for voluntary market transactions.

Reform 4: Establish a Banking Sector Asset Management Company

Global IME Bank (Annual Report 2023/24) and Nabil Bank (Annual Report 2023/24) have publicly endorsed the need for a sector-level AMC. NPR 30.15 billion (~USD 226.7 million) in seized properties sitting on bank balance sheets confirms the urgency. Individual banks lack the scale, specialisation, and market presence to conduct systematic property portfolio management.

Establish a licensed AMC with joint ownership: NRB (minority equity), commercial banks (proportional equity based on NBA transfer volume), and optionally ADB or IFC as development finance institution co-investors. The AMC acquires distressed NBAs at NRV – providing banks immediate loss recognition and balance sheet relief – manages and auctions through a dedicated online platform with verified buyer pools and integrated legal clearance service, and issues AMC bonds backed by the diversified NBA portfolio as an alternative financing mechanism. NRB Act, 2002, Section 79 likely provides sufficient authority to license and regulate the AMC; parliamentary legislation may be required for its special powers over minimum valuation mechanics.

Reform 5: Extend Hedging Framework to Projects Above 50 MW

Amend the Hedging Rules, 2022, Rule 3(1)(ka) to reduce the minimum hydropower threshold from 100 MW to 50 MW. Simultaneously: increase Nepal Infrastructure Bank’s (NIFRA) authorised capital to at least NPR 30 billion (~USD 222 million at NPR 135/USD 1) to expand net open position capacity; develop a Partial Hedging Product covering 50–70% of foreign currency exposure at reduced premium, making hedging accessible for projects that cannot afford full premium; and explore co-guarantee arrangements with ADB’s MIGA and World Bank Partial Credit Guarantee products to amplify NIFRA’s hedging capacity through risk-sharing rather than capital expansion alone.

The current interest rate caps in the Nepal Rastra Bank Foreign Investment and Foreign Loan Management Bylaw, 2078 (FIFL Bylaw, Fifth Amendment, 2082/08/25) – benchmark plus 3.5% to 6.0% – may also require upward revision. Projects requiring higher-cost foreign capital to attract international lenders cannot access it under the current framework, leaving the domestic banking system to finance projects exceeding its capacity.

Responsible institutions: Ministry of Finance (Hedging Rules amendment); NRB (NIFRA capitalisation); Investment Board Nepal (project coordination). Estimated impact: 20–30 additional mid-range hydropower projects eligible for foreign co-financing, potentially mobilising USD 2–5 billion from the existing project pipeline.

Reform 6: Resolve the Civil Code - NRB Restructuring Limitation Conflict

Amend Civil Code, 2017, Section 437 to add a tolling (suspension) provision: the two-year limitation on initiating possession proceedings for non-possessory mortgages shall be suspended for any period during which the loan is subject to a formal NRB-approved restructuring or rescheduling arrangement, the borrower is subject to court-ordered insolvency proceedings, or the parties have executed a written standstill agreement registered with the Malpot office. The limitation resumes from the date of termination of any such suspension.

A bank following NRB guidance on structured rehabilitation of a distressed SME borrower – which NRB’s own Directive 2/2081 encourages – may inadvertently lose its mortgage security under Civil Code provisions. This conflict requires parliamentary legislation; it is not resolvable through NRB directive action alone. Responsible institution: Ministry of Law, Justice and Parliamentary Affairs (Civil Code amendment); Attorney General’s Office (drafting).

Reform 7: Operationalise the Warehouse Receipt System

The Commodities Act, 2017, Section 28 and the Central Depository Service Regulation, 2010, Rule 24(2) already provide the complete legal framework for dematerialised warehouse receipts as pledgeable instruments through the CDSC system. Nepal’s agricultural sector produces approximately NPR 800–1,000 billion (~USD 5.9–7.4 billion at NPR 135/USD) in annual output. Even 10–15% penetration by warehouse receipt-backed credit would represent NPR 80–150 billion (~USD 593 million–USD 1.1 billion) in new productive sector credit without any legal amendment.

Implementation requires: licensing at least 50 commodity-grade warehouses in major agricultural production regions with NRB-approved grading, insurance, and inventory management standards; connecting warehouse operators to the CDSC electronic system for real-time dematerialised receipt issuance; BFI product guidelines permitting warehouse receipt-backed credit at 60–70% LTV; and a Warehouse Insurance Fund covering theft, fire, and deterioration losses. Responsible institutions: Ministry of Agriculture (warehouse licensing); NRB (BFI guidelines; Warehouse Insurance Fund); CDSC (technical integration).

Reform 8: Establish Commercial Insolvency Courts

Corporate insolvency proceedings in Nepal currently take three to seven years from petition to liquidation distribution, conducted through Commercial Benches of general High Courts without dedicated expertise. This eliminates going-concern value and reduces recovery to distressed land liquidation – the worst outcome for both creditors and debtors, and a direct driver of NBA accumulation.

Establish dedicated Commercial Insolvency Benches in at least five High Court locations – Kathmandu, Pokhara, Biratnagar, Butwal, Birgunj – with: enforceable case management timelines (initial determination within 90 days; reorganisation plan within 180 days; liquidation distribution within 24 months); an Insolvency Practitioners licensing regime modelled on ICAN’s auditor licensing creating a qualified private sector professional pool; pre-packaged insolvency procedures enabling creditor-agreed restructuring plans to be court-confirmed without full proceedings; and cross-border insolvency recognition provisions based on the UNCITRAL Model Law. Responsible institutions: Ministry of Law, Justice and Parliamentary Affairs (legislation); Supreme Court (institutional framework).

Reform 9: Create Modified Land Title Protection for Registered BFI Mortgages

Amend the Land Revenue Act, 1978 by adding a new Section 8kha1: where a BFI registers a Rokka after conducting prescribed due diligence – verified Malpot search confirming clean title; valuation by a licensed NRB-approved valuer; land-use zone confirmation from the local authority; ceiling declaration by the borrower counter-signed by the ward office – the BFI’s security interest is protected against automatic voidance provisions under Section 24 (where the BFI had no actual notice of public land status), Director General cancellation powers under Section 32kha (the BFI must be notified and given 30 days to lodge objection before cancellation proceeds), and mohiyani hak partition claims (the BFI’s charge is maintained on the full parcel until enforcement proceeds are distributed, with the tenant compensated from surplus).

This does not create indefeasible title. It creates a defined safe harbour for institutional lenders who follow prescribed due diligence – preserving government rights against the landowner personally while protecting the bank’s registered security interest from post-disbursement administrative surprise. Responsible institutions: Ministry of Land Management (legislative amendment); NRB (prescribed due diligence standards).

Reform 10: Develop a Domestic Corporate Bond Market

The Companies Act, 2006, Sections 34–36 and the Securities Act, 2006 provide a complete legal framework for secured debentures, licensed debenture trustees, and public corporate bond issuance. The market does not function because of rating infrastructure constraints, SLR treatment of corporate bonds, tax disadvantages relative to bank deposits, and the absence of a government guarantee product for infrastructure bonds.

SEBON to issue a Corporate Bond Development Action Plan incorporating: mandatory rating for public bond issues above NPR 500 million (~USD 3.7 million at NPR 135/USD 1) from at least two SEBON-licensed rating agencies (currently ICRA Nepal and Care Ratings Nepal); an NRB directive permitting BFIs to hold AA-rated corporate bonds as part of their liquid asset buffer up to 20% of the statutory liquidity ratio requirement; tax treatment alignment removing withholding tax differentiation between bank deposits and corporate bonds; and an infrastructure bond guarantee scheme through the Alternative Development Finance (ADF) framework (pending ADF Mobilization Bill 2082 implementation). Responsible institutions: SEBON (action plan); NRB (SLR treatment); Ministry of Finance (tax treatment; ADF implementation).

Reform 11: Rationalise Land Tenure

Mohiyani hak (the statutory tenancy rights of registered agricultural tenants under Lands Act, 2021, Section 26(1)), land ceiling provisions (Lands Act, 2021, Section 7 – maxima of 10 Bigha in the Terai, 25 Ropani in Kathmandu, 70 Ropani in hill regions), government-granted land restrictions, and co-ownership consent requirements are embedded in Nepal’s agrarian social structure and cannot be resolved through banking sector reform alone.

Commission a National Land Tenure Reform Study examining: the mohiyani hak regime’s distributional impact versus its credit market cost and options for voluntary buyout programmes; modernisation of ceiling provisions to reflect contemporary urbanisation (current ceilings date from the 1964 Lands Act); and integration of Malpot, Bhumi Sudhar, and Land Use classification databases into a unified digital land information system. Responsible institution: Ministry of Land Management (lead), with NRB, Ministry of Agriculture, Ministry of Finance, and Ministry of Law as co-participants.

Reform 12: Develop an SME Cashflow Lending Framework

NRB to issue an SME Cashflow Lending Framework Directive (within existing authority under NRB Act, 2002, Section 79) establishing: a standardised cashflow template for SME credit applications supplementing the collateral-centric appraisal format; a credit scoring model framework permitting BFIs to develop NRB-approved credit scorecards for SME loans up to NPR 50 million (~USD 370,400 at NPR 135/USD); an 85% risk weight category for SME loans underwritten under the Framework with at least 24 months of verified cashflow history; and digital transaction data integration permitting banks to use Nepal Payment and Clearing System (NPCS) transaction data, Inland Revenue Department records, and customs records as verifiable cashflow evidence alongside audited financial statements. Responsible institutions: NRB (primary); ICAN (financial statement standards); Inland Revenue Department (data sharing protocol); NPCS (transaction data access).

The Conclusion

The current period presents an unusual alignment of conditions for structural reform. Banking sector stress makes the inadequacy of the collateral enforcement mechanism visible in a way that routine supervision findings have not. NBAs nearly doubling in a single year, NPLs at a 15-year high, and concessional loan schemes unwinding without organic SME credit to replace them – these create political and institutional urgency that does not exist in normal conditions. NRB’s adoption of NFRS 9 ECL methodology creates demand for the standardised NRV framework that Reform 3 provides. The Investment Facilitation Amendment Act, 2024 has already crossed the political threshold of allowing financial institutions to hold land after failed auctions – demonstrating that land enforcement reform is achievable. The ADF Bill, if enacted, creates the institutional chassis for the infrastructure bond and guarantee products that Reform 10 contemplates.

This window will not remain open indefinitely. As credit conditions ease – remittances remain strong, monetary policy is loosening, GDP growth is recovering toward 4–5% – the urgency generated by the current stress period will diminish. Reform becomes hardest to achieve when the consequences of inaction are least visible.

Nepal is not a country without security law. The Secured Transactions Act exists. The Commodities Act exists. The CDS Bylaws exist. The Companies Act’s floating charge equivalent exists. FITTA grants foreign lenders enforcement rights equivalent to domestic banks. The legal instruments are already enacted. What remains to be built is the institutional infrastructure that gives them operational effect.

The administrative system has made, by default, a choice that the legal system was too carefully designed to make explicitly: that the creditworthy actor in Nepal’s formal financial system is, for all practical purposes, a registered landowner.

That default is not permanent. It is a product of institutional inaction, not of legal necessity. The reforms described above are specific, sequenced, institution-mapped, and – for the most consequential among them – achievable within the current regulatory mandate without waiting for parliamentary cycles. What is required is not new law. What is required is the institutional will to implement the law Nepal already has.