I. Framing the Comparison

This analysis evaluates two distinct legal pathways for deploying debt capital into Nepali borrowers: an onshore debt fund structured under Nepal’s securities framework, and an offshore fund lending directly across borders under Nepal’s foreign exchange regime. The comparison is anchored in the specific legal instruments that govern each pathway and examines their relative competitiveness across formation, pricing, tax, repatriation, flexibility, and enforcement.

The Two Structures Defined

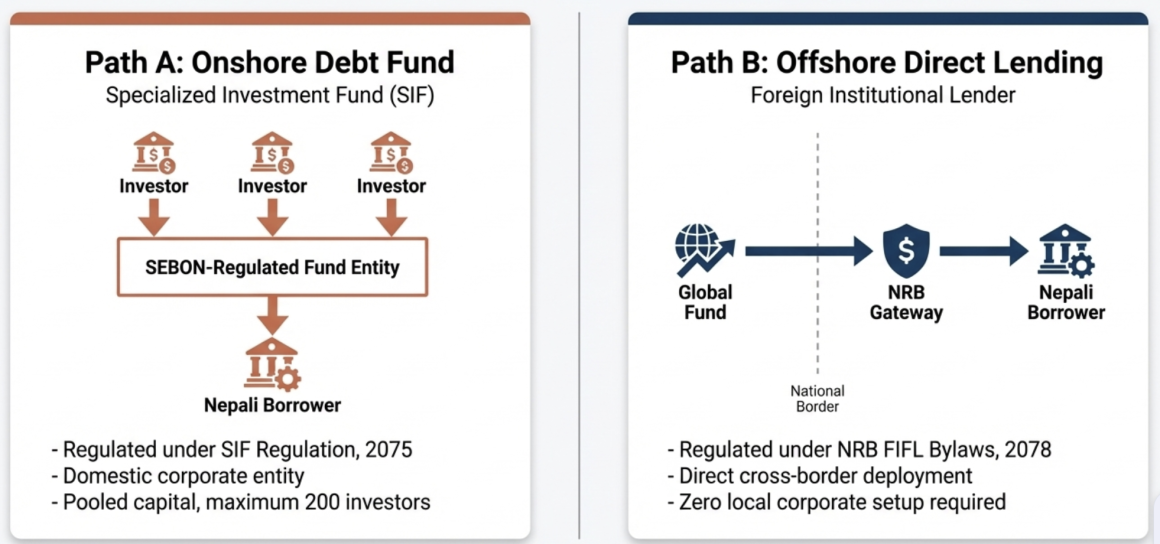

Onshore: A Debt-Focused Specialized Investment Fund (SIF). Under the Specialized Investment Fund Regulation, 2075, Rule 14(2), the Securities Board of Nepal (SEBON) permits registration of Private Equity Funds, Venture Capital Funds, Hedge Funds, and “other funds as prescribed by the Board from time to time” (Rule 14(2)(d)). A standalone “debt fund” is not explicitly listed as a category. However, Rule 14(3)(1) defines a Private Equity Fund as one that may invest in “initial equity, or other instruments related to equity, or making investments as per the desire of partners of a company” – and critically, the explanatory definition permits investment in “debt instruments”. The fund vehicle is a corporate entity registered with SEBON that pools capital from Qualified Investors by issuing units, subject to a 200-investor cap (Rule 16(c)), a minimum fund corpus of NPR 15 Crore (approximately USD 1.1 million) (Rule 16(a)), and a mandatory closed-end structure (Rule 16(d)).

Offshore: A Foreign Institutional Lender Deploying Direct Cross-Border Loans. Under the NRB Foreign Investment and Foreign Loan Management Bylaws, 2078 (Fifth Amendment), Schedule-10 (annexed to Bylaw 7(1)), eligible foreign creditors – defined in Bylaw 2(Ja) to include foreign banks, Development Finance Institutions (DFIs), pension funds, hedge funds, regulated investment companies, and parent/group companies – may lend directly to Nepali firms, companies, industries, and licensed BFIs. Each loan requires NRB’s prior approval (Bylaw 7(1)), must enter through the banking system (Bylaw 7(2)), and must be formally recorded with the NRB within six months of inflow (Bylaw 8(1)). Additionally, the Foreign Investment and Technology Transfer Act (FITTA), 2075 and its associated Rules prescribe a minimum foreign investment ticket size, which also defines the floor for foreign debt deployment into Nepal.

Why This Comparison Matters

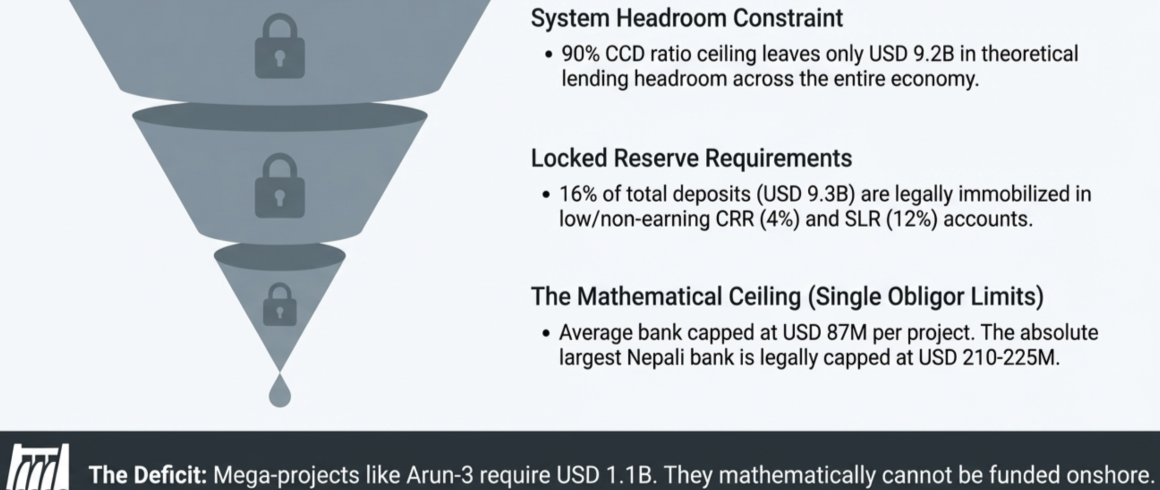

Nepal’s infrastructure financing gap is estimated at USD 46 billion in the energy sector alone through 2035. As of mid-February 2026, the Nepali banking system’s total deposits stand at NPR 7,793 billion (approximately USD 58.4 billion) with total lending of NPR 5,814 billion (approximately USD 43.6 billion). Despite this nominal scale, a constellation of regulatory constraints, capital structure rigidities, and market infrastructure deficiencies creates a deep structural inadequacy in domestic debt financing – for both the banking system and the onshore capital markets. These constraints operate simultaneously and cumulatively, making offshore debt not merely an alternative but often the only viable pathway for large-scale infrastructure financing.

A. Domestic Banking System: Quantified Constraints

- Lending Capacity Ceilings. The 90% CCD ratio ceiling (NRB Unified Directive No. 15/081, Clause 6) is the primary brake on credit expansion. With the current system-wide CD ratio at approximately 74.3%, the theoretical remaining headroom is approximately NPR 1,222 billion (USD 9.2 billion). However, this headroom must serve the entire economy – agriculture, manufacturing, trade, real estate, consumption – not just infrastructure. The share available for long-tenor infrastructure debt is a small fraction of this figure.

- Non-Earning and Low-Earning Reserve Requirements. A significant portion of bank liabilities is locked in non-productive reserves. The Cash Reserve Ratio (CRR) of 4% immobilizes approximately NPR 309 billion (USD 2.3 billion) as non-interest-bearing balances with NRB. The Statutory Liquidity Ratio (SLR) of 12% for Class A banks locks a further NPR 927 billion (USD 6.9 billion) in government securities and other liquid assets. Combined, approximately NPR 1,236 billion (USD 9.3 billion) – nearly 16% of total deposits – earns little or no commercial return, compressing the margin available for infrastructure lending. Additionally, the “Watch List” classification drag forces banks to provision 5% against loans where the borrower has been in net loss for three consecutive years (Unified Directive No. 2/081, Clause 1.2) – a common profile for infrastructure projects in their pre-revenue construction phase and profit strained operational years.

- Single Obligor Limits and Concentration Ceilings. The Single Obligor Limit (SOL) creates a hard mathematical ceiling on how much any single project can access from a single bank. The standard SOL is 25% of primary capital (Unified Directive No. 3/081, Clause 2). Even the enhanced 50% SOL for hydropower, transmission lines, and cable cars (Unified Directive No. 3/081, Clause 3) translates to modest absolute amounts. With the aggregate paid-up capital of all 20 Class A commercial banks at NPR 463.8 billion (USD 3.5 billion), the average bank’s paid-up capital is approximately NPR 23.2 billion (USD 174 million). A 50% SOL on the average bank therefore caps exposure to a single hydropower project at approximately NPR 11.6 billion (USD 87 million). Even the largest Nepali bank, with an estimated primary capital of NPR 55–60 billion (USD 410–450 million), can commit at most NPR 28–30 billion (USD 210–225 million) to a single energy project. Compare this to the capital requirements of Nepal’s flagship projects: Arun-3 at USD 1.1 billion, West Seti at USD 1.32 billion, or Upper Karnali at USD 1.05 billion. No single domestic bank – and in many cases, no realistic domestic consortium – can fill these tickets. The SOL also applies to “groups” of related borrowers, defined broadly to include firms with cross-shareholding of 25% or more, cross-guarantees, or family connections among directors (Unified Directive No. 3/081). This prevents diversified Nepali conglomerates from accessing separate credit lines for different projects. Sectoral exposure is further capped: no institution may lend more than 40% of its total outstanding credit to any single economic sector (Unified Directive No. 3/081, Clause 12). Breaching these limits carries draconian penalties: an additional 10% risk weight on the entire excess SOL exposure, and a 100% additional Loan Loss Provision plus 150% risk weight on sectoral excess amounts.

- Foreign Exchange Net Open Position Limits. Domestic banks are severely constrained in holding or managing foreign currency. A bank’s daily net open position (NOP) in foreign currency is capped at 30% of its primary capital from the previous quarter (NRB Unified Directive). For the average Class A bank, this translates to approximately NPR 7 billion (USD 52 million); even for the largest bank, the NOP ceiling is roughly NPR 17–18 billion (USD 127–135 million). The system-wide theoretical maximum NOP across all 20 commercial banks is approximately NPR 139 billion (USD 1.04 billion). This is the aggregate FX exposure the entire Nepali banking system can theoretically absorb – a fraction of the multi-billion-dollar equipment import requirements for large infrastructure projects.

- NSFR, Tenor Mismatches, and Basel III Constraints. The transition to Basel III liquidity standards creates a structural hurdle for long-term lending. NRB has mandated implementation of the Net Stable Funding Ratio (NSFR), requiring banks to match Available Stable Funding (ASF) with Required Stable Funding (RSF). By mid-July 2025, this migrates to Pillar 1 (Mandatory). Because the deposit base is predominantly short-to-medium term – savings deposits constitute 42.2% of total Class A deposits and fixed deposits 41.4% (mid-February 2026 data) – banks will struggle to provide the 15–20 year debt required for hydropower without breaching NSFR limits. Significant mismatches in the “Above 1 Year” maturity bucket attract supervisory penalties including additional risk-weighting charges.

- High Risk-Weighting for Alternative Investments. The capital cost of providing equity-like or subordinated debt to infrastructure is prohibitive for domestic banks. Claims on venture capital and private equity investments attract a 150% risk weight under the Capital Adequacy Framework, 2015. Unrated domestic corporates – which describes most Nepali infrastructure SPVs – attract a 100% risk weight, whereas offshore lenders often benefit from the credit ratings of their parent funds or DFI backing.

- Mandatory Consortium Financing Threshold. Loans exceeding NPR 2 Arba (NPR 2 billion, approximately USD 15 million) must be structured as Consortium/Co-financing (Unified Directive No. 3/081). This requires a Lead Bank and a consensus-based decision-making process across multiple member institutions, typically meeting at least every six months. For an offshore debt fund capable of providing a single-ticket solution, this consortium overhead is eliminated entirely, offering significant speed and execution advantages.

B. Onshore Capital Market: Structural Deficiencies

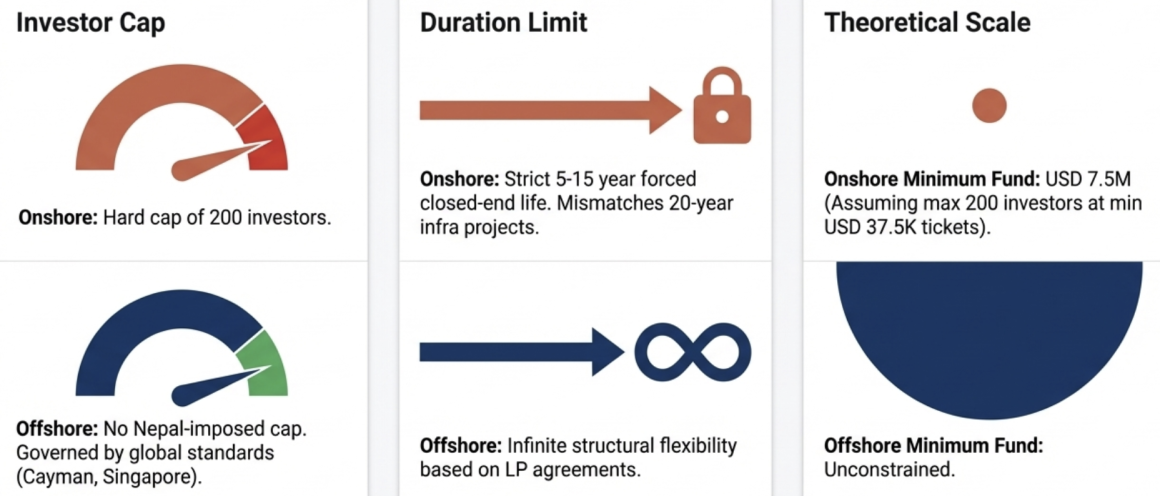

- Duration Mismatch. Large-scale infrastructure projects require gestation, construction, and operational horizons spanning 20 to 30 years. However, the SIF Regulation, 2075 mandates that a fund must have a lifespan of only 5 to 15 years (Rule 19). This forces the fund to liquidate and terminate precisely when an infrastructure project might just be reaching operational maturity, creating a severe asset-liability mismatch that no amount of structuring can fully resolve.

- The 200-Investor Ceiling. The SIF’s hard cap of 200 unit holders (Rule 16(c)) inherently prevents broad-based pooling of mid-tier institutional or high-net-worth capital. For context, with a minimum investment of NPR 50 Lakh (approximately USD 37,500) per investor and a maximum of 200 investors, the theoretical maximum fund size from minimum tickets is only NPR 100 Crore (approximately USD 7.5 million) – far below the scale needed for meaningful infrastructure financing.

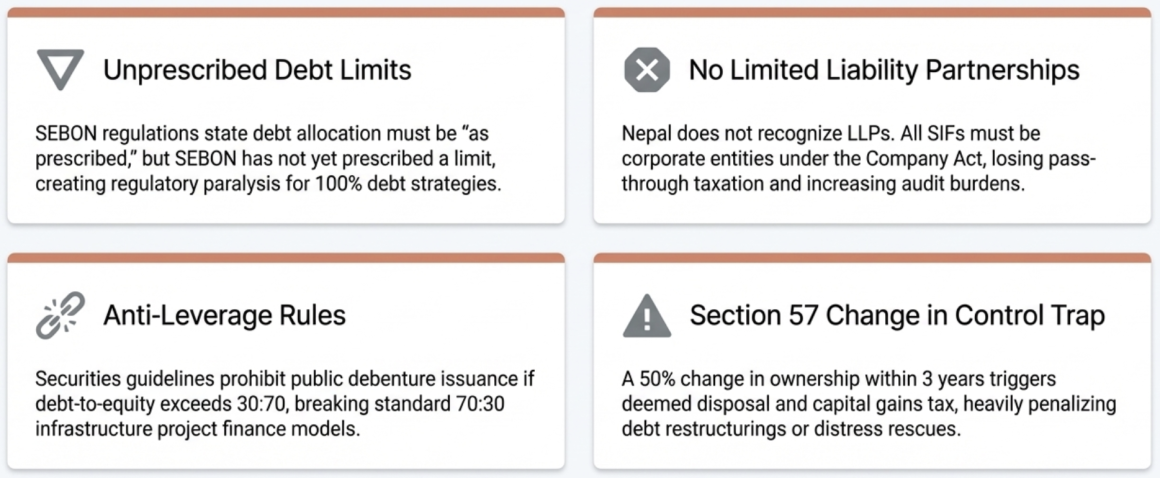

- SEBON’s Unprescribed Debt Allocation Limit. Even if a SIF is specifically established to operate as a private credit fund, the regulations dictate that the exact percentage of the fund’s total capital that can be allocated to debt instruments is “strictly prescribed by the Securities Board of Nepal” (Rule 14(3)(1)). As of this analysis, SEBON has not issued any such prescription. A fund manager cannot dynamically pursue a 100% debt strategy without explicit regulatory permission, stripping the vehicle of the flexibility needed to act as a pure infrastructure debt provider.

- Anti-Leverage Restrictions on Public Debt Issuance. Infrastructure financing globally relies on project finance leverage of 70–80% debt. Nepal’s Securities Issue and Allotment Guidelines, 2074, Section 9(1)(ga), generally prohibit a company from issuing public debentures if its debt-to-equity ratio exceeds 30:70 over the tenure of the debenture. This means an infrastructure developer cannot use public bond markets to raise the heavy debt required; its debt capacity is artificially constrained by the size of its direct equity.

- Absence of Limited Liability Partnerships. Under the Partnership Act, 2020, all partnerships carry unlimited liability. Nepal does not recognize Limited Liability Partnerships (LLPs). This forces all pooled investment vehicles into the corporate form under the Company Act, which carries higher regulatory overhead, mandatory audit requirements, and no pass-through taxation – a critical disadvantage compared to LP structures used in Cayman Islands, Singapore, India, and virtually every other fund jurisdiction.

- Rigid Fee Structures and Manager Disincentives. If the market attempts to bypass the SIF’s 200-investor cap by using a Mutual Fund structure, it loses all structuring flexibility. Mutual Fund Regulation, 2067, Rule 23 strictly caps the fund manager’s service fee as a percentage of Net Asset Value. There is no provision for standard offshore-style carried interest or bespoke waterfall distributions. This inability to structure performance-based upside severely disincentivizes specialized infrastructure fund managers from operating onshore.

- Heavy Issuance Frictions and Mandatory Intermediary Costs. Any public issuance of debt securities requires mandatory credit rating by a licensed agency and the appointment of a licensed merchant banker as Issue Manager (Securities Registration and Issue Regulation, 2073). The intermediary capital requirements are massive – NPR 1.5 billion (approximately USD 11.2 million) for securities dealers – limiting the number of capable institutional market makers and driving up debt syndication costs.

- Illiquid Secondary Debt Markets. While Nepal permits secondary trading of government bonds through designated Market Makers (Government Securities Secondary Market Transaction Bylaws, 2062), there is no formalized corporate repo (repurchase agreement) market – i.e., short-term borrowing using corporate bonds as collateral – within the Securities Board of Nepal-regulated securities framework. Without such a repo market to provide liquidity against corporate infrastructure bonds, domestic institutions demand a substantial illiquidity premium, increasing the cost of capital for infrastructure developers.

- Tax-Induced Economic Inefficiency. Entities engaged in “capital market business” or financial transactions face a 30% corporate income tax rate under the Income Tax Act, 2058, versus 25% for standard industry. Additionally, because core financial services (interest income, capital market business) are VAT-exempt under Schedule 1, Group 11 of the VAT Act, 2052, onshore fund vehicles cannot claim input tax credits on their operational expenses. The 13% VAT on office rent, professional services, and equipment becomes an unrecoverable sunk cost, creating a direct drag on investor returns.

- The Section 57 “Change in Control” Trap. Section 57(1) of the Income Tax Act, 2058 stipulates that if a company’s ownership changes by 50% or more compared to three years prior, the entity is deemed to have disposed of its assets, triggering capital gains tax. For infrastructure debt workouts where a debt-to-equity swap or buyout of a distressed project changes the shareholder base, this provision penalizes new investors attempting to rescue projects. The Finance Bill 2081 introduced a limited exception: Section 57 does not apply if existing shareholders’ share count and capital remain unchanged while new shareholders are added for capital increase. However, this exception only protects the entry phase. Upon exit – when existing investors sell or transfer shares – Section 57 is re-triggered because the share units of existing holders change. A share buyback within three years of investment avoids this, but this narrow window provides little comfort for long-gestation infrastructure investments.

- No Informal Workout Mechanisms. Nepal lacks a recognized legal or regulatory framework for informal multi-creditor workouts (restructuring debt outside of court). The Insolvency Act, 2063 provides formal court-supervised processes, but without a “Statement of Principles” for pre-insolvency restructuring, negotiations between banks and developers often deadlock, leaving formal insolvency as the only option. This adds a significant liquidity risk premium to long-term infrastructure debt.

C. Offshore Debt: Powerful but Constrained

While offshore debt addresses many of the above limitations – bypassing SOL constraints, eliminating consortium friction, and accessing deeper capital pools – it carries its own structural constraints. ‘

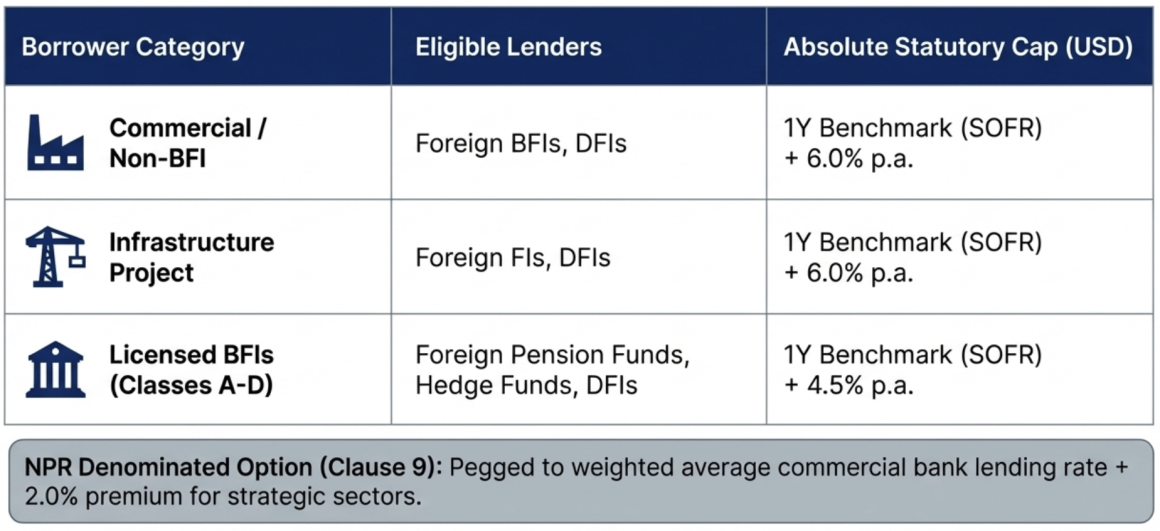

- Strict Pricing Caps: NRB imposes absolute interest rate ceilings. Standard commercial foreign loans are capped at One Year Benchmark Interest Rate + 6.0% p.a., and DFI loans to infrastructure at Benchmark + 4.5% p.a. (FIFL Bylaws, 2078, Schedule-10). This prevents high-yield or mezzanine offshore debt from filling the financing gap.

- Hedging Costs: Even with government subsidies for large infrastructure (5–20% government contribution, 30–40% from designated entities), the project itself absorbs the remaining hedging premium, directly reducing equity returns.

- Dual-Regulator Bottleneck: Cross-border debt issuance requires approvals from both NRB (for foreign exchange) and SEBON (for securities), plus a Ministry recommendation for project loans, creating structural unpredictability and execution risk.

- Repatriation Friction: While FITTA guarantees repatriation, exit is bottlenecked by mandatory tax clearances, NRB recording certificates, CIB checks, and audit submissions before any foreign currency can leave the country.

Dimensions of Competitiveness

This analysis evaluates competitiveness across six dimensions: (a) total cost of capital to the borrower, including regulatory caps, fees, and tax leakage; (b) net return to the investor after all tax layers, FX costs, and repatriation friction; (c) regulatory friction, measured by approval timelines, documentation burden, and multi-agency coordination; (d) structural flexibility, including waterfall distributions, investor classes, and leverage; (e) enforceability, encompassing collateral, security, and insolvency protections; and (f) time-to-deploy, from fund formation or loan approval to first disbursement.

Target Borrower Universe: The analysis considers three borrower profiles: (i) infrastructure project SPVs under the IBN/PPP framework (projects above NPR 6 billion (approximately USD 45 million) or 200 MW); (ii) mid-market corporates in non-restricted sectors; and (iii) licensed Banks and Financial Institutions (Classes A through D) seeking foreign currency liabilities for onward lending.

II. Formation, Capital Raising, and Regulatory Gateway

A. Regulatory Setup: Two Fundamentally Different Entry Points

Onshore SIF: The SEBON Pathway

Establishing an onshore debt fund under the SIF Regulation requires navigating a two-step approval process with the Securities Board of Nepal. First, the corporate entity seeking to manage the fund must obtain approval as a Fund Manager (Rule 3(1)). The applicant must be a body corporate registered under prevailing law (Rule 7(1)(a)), must include “fund manager” as an objective in its Memorandum and Articles of Association (Rule 7(1)(b)), and must maintain minimum paid-up capital of NPR 2 Crore (approximately USD 150,000) (Rule 7(1)(c)). The application is submitted in the format prescribed in Schedule-1, accompanied by fees per Schedule-2 (a registration fee of NPR 3 Lakh), and SEBON must grant or refuse the approval within 35 days after making necessary inquiry (Rule 4(1)).

Second, the approved Fund Manager must separately register each fund scheme with SEBON (Rule 14(1)). The fund application is submitted per Schedule-5 with fees per Schedule-2 (ranging from NPR 5 Lakh for funds up to NPR 50 Crore, to NPR 10 Lakh for funds above NPR 1 Arba). SEBON retains broad discretionary power to reject registration if the fund’s proposal contradicts prevailing laws, if minimum standards under Rule 16 are not met, if the fund cannot operate given securities market conditions, or if it judges investor interests are inadequately protected (Rule 17(1)(a)–(d)).

The Fund Manager’s board must comprise 5–7 directors (Rule 9(1)), including at least one Independent Director (Rule 9(2)) with a master’s degree and five years’ experience in economics, commerce, finance, or commercial law (Rule 11(a)). The Chief Executive Officer requires ten years’ experience with a master’s degree, or fifteen years with a bachelor’s (Rule 12). No director or CEO may have been convicted of cheating, embezzlement, or moral turpitude (Rule 13(d)–(e)), or appear on the Credit Information Centre’s blacklist within three years of clearance (Rule 13(b)). In sophisticated jurisdictions like the Cayman Islands or Singapore, fund manager licensing typically requires demonstrating competence and capital adequacy but does not mandate specific board composition rules or academic qualifications at the statutory level – these are left to the fund’s constitutional documents and investor negotiation.

Offshore Fund: The NRB Pathway

An offshore fund deploying debt into Nepal requires no local fund formation, no SEBON registration, and no local corporate establishment. The fund simply lends from its offshore jurisdiction directly to a Nepali borrower. What it does require is NRB’s prior approval for each individual loan.

Under FIFL Bylaw 7(1), any Nepali entity seeking to borrow from abroad must obtain NRB’s prior approval before the foreign currency enters Nepal. The borrower submits the loan agreement (or Term Sheet, if a full agreement is not yet executed, per Schedule-11, Note (a)), along with extensive documentation including the lender’s registration certificate, beneficial owner identification, audited financials (unless the loan is below USD 1 million), the borrower’s own registration, PAN, latest audit report, CIB clearance, and a self-declaration on AML/CFT compliance (Schedule-11). NRB must decide within 15 working days of receiving a complete application (Bylaw 7(3)).

For project loans by foreign-invested companies, FITTA, 2075, Section 12 additionally requires a recommendation from the relevant line Ministry before NRB approval. For investments above NPR 6 billion (approximately USD 45 million), the Investment Board Nepal (IBN) is the approving authority for the underlying foreign investment (FITTA Section 17(2)), while the Department of Industry handles investments below that threshold (FITTA Section 17(1)).

The Critical Jurisdictional Question: Can a SIF Originate Loans Without a BFI License?

The SIF Regulation explicitly permits PE and VC funds to invest in “debt instruments” and provide “loans” to target companies (Rule 14(3)(1)–(2)). However, the Bank and Financial Institutions Act (BAFIA), 2073, Section 31 establishes that no entity other than a licensed BFI shall conduct “banking and financial transactions.” This creates an unresolved regulatory grey zone.

However, a rigorous legal analysis supports the position that SIFs should be excluded from BFI licensing requirements, based on four statutory principles:

- First, the “general public” threshold. The NRB Act, 2058, Section 2(Chha) defines a “Financial Institution” as an entity established with the objective of providing loans or collecting deposits from the “general public”. SIFs do not solicit deposits from the general public; they pool committed capital from a maximum of 200 Qualified Investors through a knowing investment contract. The fund therefore does not meet the statutory definition that triggers NRB’s licensing mandate.

- Second, “deposits” versus “investment capital.” BAFIA Section 2(Na) defines a “Deposit” as money received from “customers” for safekeeping. SIF investors are not customers seeking deposit services; they are unit holders providing equity commitments. Because a SIF lends its own pooled capital rather than leveraging public deposits, it is not engaging in “banking business” as defined by the fiduciary duty to return public funds on demand.

- Third, regulatory precedent. NRB’s own Unified Directives already recognize PE/VC funds as a distinct category. Unified Directive No. 12/081, Clause 9(nga) specifically exempts Private Equity Venture Capital (PEVC) institutions with more than 50% foreign investment from certain “Group Blacklisting” consequences. By creating specific carve-outs for PEVCs, NRB implicitly acknowledges these entities operate under securities law, not BFI licensing.

Fourth, the scope of BAFIA Section 31. While Section 31 restricts “banking and financial transactions” to licensed BFIs, the scope of these transactions is defined in Section 49 by license class. For a SIF, providing debt is a tool for investment management, not a banking service offered to the general market. The target company is an investee under a securities-based contractual relationship, not a banking customer.

B. Investor Architecture: Who Can Invest and How

The SIF Regulation restricts the fund to “Qualified Investors” (Rule 22), which include: (a) Banks and Financial Institutions; (b) Insurance Companies; (c) Pension funds, welfare funds, provident funds, and the Citizen Investment Trust; (d) Bilateral or multilateral international institutional investors; (e) Bodies corporate established in Nepal with an investment objective; (f) Nepali citizens and Non-Resident Nepalis; and (h) Other entities as prescribed by the Board. The fund is hard-capped at 200 investors (Rule 16(c)), each must invest a minimum of NPR 50 Lakh (approximately USD 37,500) (Rule 16(f)), the fund must be closed-ended (Rule 16(d)), and its life must be between 5 and 15 years (Rule 19). The fund manager must maintain at least 2% of the fund as skin-in-the-game, maintained continually (Rule 16(b)) – though this requirement does not apply to investments by bilateral or multilateral international agencies.

The offshore fund faces none of these constraints for its own fundraising. It raises capital in its home jurisdiction under local securities law – whether as a Cayman exempted limited partnership, a Singapore Variable Capital Company, or an Indian AIF Category II – with no investor caps, minimum thresholds, or mandatory closed-end requirements imposed by Nepal. For context, India’s AIF Regulation, 2012 permits Category II AIFs (which include debt funds) to have up to 1,000 investors with a minimum commitment of INR 1 Crore, and no mandatory closed-end requirement for debt funds. The Cayman Islands imposes no investor caps whatsoever on exempted limited partnerships. Nepal’s 200-investor cap and 5–15 year mandatory closed-end structure are among the most restrictive in the region.

C. Comparative Formation: Cost, Timeline, and Friction

Dimension | Onshore SIF | Offshore Direct Lending |

Regulatory Approval | Two-step: Fund Manager (35 days) + Fund Registration (discretionary) | Per-loan NRB approval (15 working days statutory) |

Formation Entity Required | Nepali company with NPR 2 Crore (USD 150K) paid-up capital | None in Nepal; offshore vehicle suffices |

Minimum Fund/Loan Size | NPR 15 Crore (USD 1.1M) fund corpus (Rule 16(a)) | No minimum per loan |

Investor Cap | 200 investors maximum (Rule 16(c)) | No Nepal-imposed cap |

Minimum Investment | NPR 50 Lakh (USD 37,500) per investor (Rule 16(f)) | No Nepal-imposed minimum |

Structure | Closed-end only; 5–15 year life (Rules 16(d), 19) | Any structure permitted in home jurisdiction |

Regulatory Fees (Initial) | NPR 3L (manager) + NPR 5–10L (fund) + NPR 5K (application) | Nil in Nepal (loan approval is free) |

Annual Fees | NPR 1.5L (manager annual) + ongoing audit/compliance | Nil recurring Nepal fees |

Estimated Time to First Deployment | 6–12 months (formation + fundraising + first investment) | 2–4 months (loan negotiation + NRB approval + recording) |

Verdict: The offshore pathway offers dramatically lower formation friction – no entity setup in Nepal, no securities regulator approval, no investor caps, and a faster path to first deployment.

III. Deployment Mechanics, Pricing Architecture, and the All-In Cost Cap

This section – the analytical core of this post – examines what each structure can actually do with its capital, the pricing constraints it faces, and the critical interpretive questions around fees that determine the real cost of offshore debt to Nepali borrowers.

A. Onshore SIF: Deployment Powers and Constraints

First, SEBON must prescribe the percentage of the fund’s capital allocable to debt instruments. Rule 14(3)(1) explicitly states that the percentage shall be “as prescribed by the Board.” As of this analysis, SEBON has not issued such a directive. This creates structural paralysis. Reform recommendation: SEBON should issue a directive permitting a dedicated “Debt Fund” category under Rule 14(2)(d) with up to 100% debt allocation, aligned with India’s AIF Category II framework.

Second, the fund’s investment areas must be specified in its prospectus (Rule 24(2)) and constitution (Rule 15(1)(f)), and the fund is restricted to investing only in those specified areas (Rule 24(4)). The fund cannot lend outside its approved mandate without amending its constitution.

On the positive side, the SIF’s domestic lending is not subject to NRB’s foreign loan interest rate caps. On the other hand, domestic bank lending rates are market-driven, and borrowers must satisfy NRB-mandated Debt-to-Equity ratios (80:20 per Unified Directive No. 2/081, Clause 43). The SIF can price its loans competitively against domestic bank lending rates, which are structurally elevated due to banks’ burden of low-yield mandatory sector lending (Base Rate + 2% for priority sectors) and high non-interest liquidity buffers.

B. Offshore Fund: The FIFL Schedule-10 Pricing Matrix

The offshore fund’s lending into Nepal is governed by a detailed matrix of borrower-lender categories, each with specific interest rate caps, volume limits, and tenure restrictions. Schedule-10 of the FIFL Bylaws, 2078 (as amended through the Fifth Amendment) establishes the framework reproduced below. The interest rate caps are absolute statutory maximums – NRB officials are legally barred from approving applications that exceed them (Schedule-18, Row 6 explicitly limits delegated authority to approvals “within the prescribed interest rate limit”).

# | Borrower | Eligible Foreign Lender | Maximum Amount / Limit | Interest Rate Cap | Tenure | Specific Conditions & Purpose Restrictions | Approval Body |

1 | Firm, company, industry, or institution (Excluding licensed BFIs) | a) Foreign BFIs, Gov/Inter-gov DFIs. | No stated maximum limit. | USD/Other: Max 1Y Benchmark Rate* + 6.0% p.a. | Not explicitly specified. | Standard commercial borrowing. | FXMD |

2 | Firm, company, institution, and Nepali citizens | Relatives abroad, other foreign individuals, Non-Resident Nepalis (NRNs), or foreign organizations/institutions. | USD 1 Million (or equivalent). | USD/Other: Interest-free OR Max 1Y Benchmark Rate* + 2.0% p.a. | Minimum 1 Year. | Prohibited Sectors: The loan cannot be used for Real Estate or Securities/Margin trading. | FXMD |

3 | Foreign-invested industry/company (Excluding licensed BFIs) | Foreign investor of the company (Including Parent Company or Group of Companies). | Up to 2x (200%) of the paid-up capital maintained by the foreign investor. Exception: Allowed to exceed this if average interest is maintained on new/existing loans, provided annual interest does not exceed 50% of the premium rate. | USD/Other: Interest-free OR Max 1Y Benchmark Rate* + 3.5% p.a. | Not explicitly specified. | Purpose: Must be strictly utilized in the specified sector of the industry/company. | OSSC |

4 | Foreign-invested industry/company (Excluding licensed BFIs) | Foreign financial institutions, Gov/Inter-gov DFIs. | Project-based (No stated cap). | Exactly the same as S.N. 1 (e.g., 1Y Benchmark + 6.0% p.a.). | Not explicitly specified. | Purpose: Must be strictly used for Project Loans or Project Financing. | OSSC |

5 | Infrastructure development projects OR suppliers/contractors constructing such projects | Parent Company / Group of Companies of the project or supplier/contractor. | No stated cap (Based on project requirement). | Interest-free | As per the requirement of the project. | Purpose: For current/operational expenses related to project construction. | FXMD |

6 | Class “A”, “B”, “C”, and “D” BFIs and Infrastructure Dev. Banks | Indian BFIs, Gov/Inter-gov DFIs. | Up to 100% of Primary Capital (includes existing loans in convertible foreign currency). | INR (India): Max 1Y MCLR + 0.5% p.a. | Min 6 Months to Max 15 Years. | Allowed Sectors: Energy, infrastructure, tourism, agriculture, micro-enterprises. | FXMD |

7 | Class “A”, “B”, “C”, and “D” BFIs and Infrastructure Dev. Banks | Foreign BFIs, approved foreign Pension Funds, Hedge Funds, Gov/Inter-gov DFIs. | Up to 100% of Primary Capital (includes existing loans in Indian currency). | USD/Other: Max 1Y Benchmark Rate* + 4.5% p.a. CNY (China): Max 1Y LPR + 1.0% p.a. | Min 6 Months to Max 15 Years. | Allowed Sectors: Energy, infrastructure, tourism, agriculture, micro-enterprises. | FXMD |

8 | Public Limited Company established in Nepal (or entity authorized to issue securities) | Foreign buyers in the foreign capital market. | Based on issuance. | Exactly the same as S.N. 1 (e.g., 1Y Benchmark + 6.0% p.a.). | Per instrument terms. | Instrument: Must be raised by issuing bonds, debentures, or other securities. | OSSC |

*Benchmark Interest Rates: SOFR (USD), SONIA (GBP), SARON (CHF), TONA (JPY), €STER (EUR). For INR: MCLR. For CNY: LPR.

NPR-denominated option (Clause 9): Foreign loans can be denominated in NPR with FX risk on the lender. In this case the cap shifts to the weighted average commercial bank lending rate published by NRB. For strategic sectors (IT, agriculture, manufacturing, infrastructure, tourism, green bonds), an additional 2% premium above that weighted average is permitted.

Fixed rate option (Clause 10): Locked for maximum two years per tranche. The fixed rate must not exceed the benchmark + applicable spread + 25 basis points. For NPR-denominated loans, the fixed rate lock extends to ten years.

C. The All-In Cost Cap: Guarantee Fees, Hedging Fees, and the Absolute Ceiling

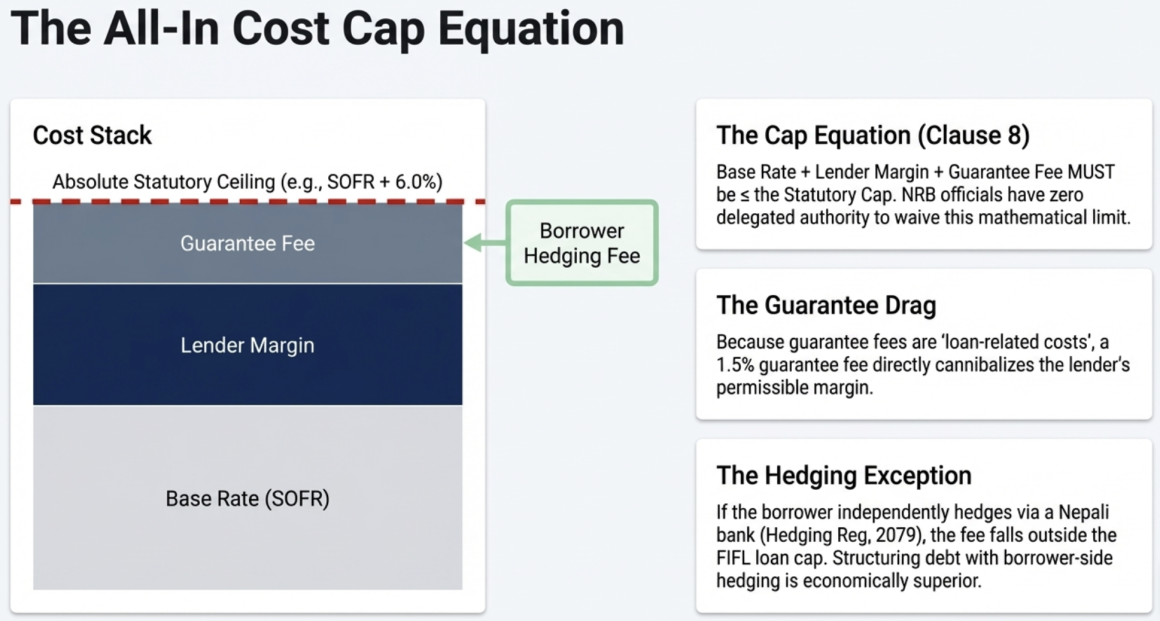

Schedule-10, Other Conditions, Clause 8 establishes the critical all-in cost rule: all expenses, fees, commissions, and charges related to the loan must fall within the prescribed interest rate cap. This is not a soft guideline – it is an absolute statutory ceiling. Schedule-18 (Delegation of Authority), Row 6 explicitly limits the authority of all NRB officials – from the Department Director to the Governor – to approving foreign loans and associated fee payments strictly “within the prescribed interest rate limit”. NRB officials have no statutory power to grant a discretionary waiver if the all-in cost exceeds the prescribed cap. If the proposed interest rate plus fees exceed the mathematical limit in Schedule-10, the application is rejected – not approved with a waiver.

The only way the cap itself can be changed is through a structural amendment to the Bylaws’ schedules. Under Bylaw 18, only the Governor of NRB holds the exclusive authority to alter schedules. The Governor’s general “Removing Difficulties” power under Bylaw 17 is an administrative safeguard for procedural deadlocks, not a pathway for offshore funds to negotiate higher commercial yields.

The Carved-Out Contingent Fees

For institutional loans under S.N. 1, S.N. 6, and S.N. 7, the Bylaw carve out specific contingent fees that may be charged outside the general interest rate cap without requiring any NRB approval:

Fee Type | Maximum Permitted |

Penal interest | Max 2% above stipulated rate, on overdue principal/interest |

Prepayment fee | Lump sum max 0.25% (NRB approval required for the early repayment itself) |

Commitment fee | Lump sum max 0.25% |

Administrative fee (if loan fails) | Max USD 5,000 per year per borrower |

This list is exhaustive. Any other fee – whether contingent or non-contingent – must fit within the prescribed interest rate cap. There is no mechanism to obtain NRB approval for a higher all-in cost; the ceiling is absolute.

The Guarantee Fee: Squarely Within the Cap

A guarantee fee is the cost paid by the borrower to a third-party guarantor to enhance creditworthiness. It is unambiguously a “loan-related cost” under Clause 8’s general rule. It arises because of the loan, is paid to facilitate or improve the loan’s terms, and is directly linked to the credit transaction. It is not among the four carved-out contingent fees. Therefore, a guarantee fee must fit within the interest rate cap. If the guarantee fee, when added to the interest rate and all other loan-related costs, pushes the all-in cost above the prescribed benchmark, the loan application will be rejected.

Practical implication: For a USD loan at the maximum permissible rate of 1Y SOFR + 6.0%, if the current 1Y SOFR term rate is approximately 4.3%, the maximum all-in cost is roughly 10.3% per annum. A guarantee fee of 1.5% per annum would consume nearly one-quarter of the available spread, leaving only 4.5% for the lender’s margin, operating costs, and profit. Offshore funds structuring guaranteed loans must model the guarantee fee into their all-in cost stack from the outset.

The Hedging Fee: Building a Case for Exclusion

The hedging fee presents a fundamentally different analytical question. When a Nepali borrower independently enters into a hedging agreement under the Hedging Regulation, 2079 to lock in the exchange rate on its foreign currency loan, is that hedging fee part of the “loan-related costs” subject to Schedule-10’s interest rate cap?

Three arguments support exclusion:

First, separate legal instrument and regulatory framework. The hedging fee is governed by the Hedging Regulation, 2079, promulgated under a distinct policy objective of FX risk neutralization. The FIFL Bylaws, 2078 govern the credit relationship. These are two different regulatory regimes. The hedging agreement is a separate contract between the borrower and a Nepali commercial bank – it is not a clause of the loan agreement.

Second, different counterparty. The hedging fee is paid to a Nepali commercial bank or designated hedging institution, not to the foreign lender. Clause 8’s language targets costs payable in connection with the loan agreement to or through the lender.

Third, government subsidy element. Under Hedging Regulation 2079, Rule 5, the Government of Nepal bears 5–20% of the hedging fee for priority projects, and the relevant government entity bears 30–40%. Treating a government-subsidized FX cost as part of the lender’s interest rate cap would be internally contradictory.

The Clause 9 complication: When the FX risk sits with the lender (NPR-denominated foreign loans under Clause 9), the lender’s hedging cost is embedded in the interest rate itself, which is within the cap. This reveals a structural principle: the regulatory treatment of hedging costs depends on who contractually bears the FX risk.

Conclusion: When the borrower independently hedges under the Hedging Regulation, 2079, the hedging fee should fall outside the FIFL interest rate cap. When the lender hedges and passes the cost through as interest (Clause 9), it falls within. Offshore funds should structure loans in foreign currency with borrower-side hedging to keep hedging costs outside the regulatory cap.

Caveat and reform recommendation: The FIFL Bylaws do not explicitly address this question. NRB should amend Clause 8 to explicitly exclude Hedging Regulation 2079 costs incurred with a Nepali financial institution from the all-in cost calculation.

D. Security, Collateral, and Prohibited Sectors

Schedule-10, Clause 13 permits foreign financial institutions providing project loans to take movable or immovable property as collateral pledged in the foreign lender’s name. FITTA, 2075, Section 20(4) grants foreign lenders the right to auction such pledged property and repatriate the proceeds with the same enforcement powers as a domestic BFI. FITTA Section 14 permits tripartite escrow agreements between the foreign investor, its partner, and a Nepali commercial bank.

Both structures face sectoral restrictions. The FITTA negative list (Schedule to FITTA, 2075, Section 3(2)) prohibits foreign investment in real estate trading, micro/cottage enterprises, primary agriculture, retail, mass media, arms, and personal services. Schedule-10, Clause 14 additionally prohibits use of foreign loan proceeds for housing, land development, and share-collateral lending. The onshore SIF faces no statutory negative list beyond prevailing law, but SEBON controls its mandate through the fund’s approved constitution and prospectus.

IV. Tax Efficiency and Net Investor Returns

Taxation is frequently the decisive layer in determining whether an onshore structure can compete with an offshore alternative.

A. Comparative Tax Waterfall

Tax Layer | Onshore SIF (as Company) | Onshore Mutual Fund | Offshore (DTAA) | Offshore (No DTAA) |

Entity-level CIT | 25–30% | 0% (ITA S.10(ठ)) | 0% (no PE) | 0% (no PE) |

WHT on interest income | 15% (ITA S.88(1)) | N/A (exempt entity) | 10% (treaty) or 5% (BFI FX loan, ITA S.88(9)) | 15% (ITA S.88(1)) |

WHT on distributions | 5% dividend (ITA S.88(2)(k)) | 5% (ITA S.88(1)(6)) | 5–10% (DTAA Art.10) | 5% |

Capital gains on exit | 10–15% (ITA S.95क) | 5–7.5% (listed units) | Exempt (DTAA Art.13(6) for bonds) | 25% (ITA S.95क(2)) |

VAT on operations | 13% unrecoverable input | 13% unrecoverable input | N/A | N/A |

The Mutual Fund Alternative: A SEBON-approved Mutual Fund enjoys full entity-level tax exemption under ITA Section 10(Tha). Distributions to resident individuals are subject to only 5% final WHT. However, Mutual Funds cap manager fees as a percentage of NAV (Mutual Fund Regulation, 2067, Rule 23), offer no carried interest mechanism, and require daily NAV calculation and continuous redemption for open-ended schemes. For a debt fund seeking PE-style economics, the SIF structure is more appropriate – but the tax penalty is severe.

B. The Critical Tax Question for Onshore SIF

Does the Mutual Fund exemption extend to SIFs? Almost certainly no. Section 10(Tha) specifically exempts “Collective Investment Fund (Mutual Fund)” approved by SEBON. A SIF is a distinct regulatory category under separate legislation. The Income Tax Act treats trusts, unit trusts, and similar entities as “companies” under Section 2(d), subjecting them to the standard 25% rate or the elevated 30% rate for “capital market business.” This 25–30% entity-level CIT versus 0% on a Mutual Fund and 0% on an offshore fund with no PE is the most significant structural disadvantage of the onshore SIF.

C. Worked Example: Net Return Comparison

Assume an NPR 100 Crore portfolio generating a 12% gross annual yield (NPR 12 Crore), deployed across infrastructure project loans.

Particulars | Onshore SIF | Offshore (DTAA, 10% WHT) |

Gross yield | NPR 12.0 Cr | NPR 12.0 Cr |

Entity-level CIT (25%) | (NPR 3.0 Cr) | Nil |

WHT on distribution / interest (5% / 10%) | (NPR 0.45 Cr) on dividend | (NPR 1.2 Cr) WHT at source |

Net to investor | NPR 8.55 Cr (71.3%) | NPR 10.8 Cr (90.0%) |

Tax leakage | 28.7% | 10.0% |

The offshore fund delivers NPR 2.25 Crore more per year on an identical NPR 100 Crore portfolio – a 187-basis point annual advantage purely from tax efficiency. Over a 10-year fund life, this compounds to a substantial difference in total returns.

V. Repatriation, FX Risk, and Exit Mechanics

A. Repatriation: The Procedural Bottleneck

For the offshore fund, repatriation of principal and interest is legally guaranteed under FITTA, 2075, Section 20(1)–(2) and FIFL Bylaw 9. Once a loan has been pre-approved by NRB (Bylaw 7) and formally recorded (Bylaw 8), the borrower can obtain foreign exchange facilities from commercial banks to service the debt without further NRB approval (Bylaw 9(1)). The commercial bank must process the request within seven working days (Bylaw 9(3)).

However, “complete documentation” per Schedule-16 requires: (a) the NRB recording certificate with approved repayment schedule; (b) latest tax clearance or proof of tax return filing; (c) proof of TDS payment on the interest being remitted; and (d) CIB clearance confirming the borrower is not blacklisted (valid only if within six months). Any discrepancy halts the process.

For the onshore SIF, domestic investors receive distributions only as cash dividends during the fund’s life (Rule 16(e)), and can fully exit only upon termination (Rule 20). Foreign investors in the SIF must navigate FIFL Bylaw 6 for dividend repatriation, with the same documentary bottleneck.

B. FX Risk and the Hedging Architecture

The currency mismatch – NPR revenue against foreign currency obligations – is the central structural risk. The Hedging Regulation, 2079 permits borrowers to lock in the exchange rate at the moment foreign currency enters a Nepali bank. For priority sectors, government cost-sharing is substantial: for storage hydropower over 100 MW, the government bears 5% and the relevant entity (e.g., NEA) bears 40%. For green infrastructure loans of at least USD 20 million, the government may bear up to 10% over seven years.

The onshore SIF lending in NPR eliminates FX risk for the borrower – a significant competitive advantage. However, foreign investors in the SIF still face NPR/USD conversion risk at repatriation, and the tail risk for both structures is the Government’s emergency FX capture power under FERA, 2019, Section 6.

C. Exit Comparison

The offshore fund’s exit is loan-maturity-driven. Early prepayment requires NRB approval and incurs a maximum 0.25% fee. Debt-to-equity conversion is possible under Schedule-10, Clause 15.

The onshore SIF investor has no redemption right before expiry (5–15 years). No secondary trading mechanism exists for SIF units. Early termination requires 75% capital / 50% unitholder resolution (Rule 20(3)). In comparison, India’s AIF framework permits inter se transfers of units with fund manager consent, and offshore jurisdictions allow LP interest transfers subject to GP approval. Reform recommendation: Amend the SIF Regulation to explicitly permit secondary transfers between Qualified Investors with SEBON notification.

VI. Structural Flexibility, Enforcement, and Practical Reality

A. Fund-Level Structuring Flexibility

Carried interest and performance fees: The SIF Regulation recognizes a “hurdle rate” as the projected minimum annual return stated in the fund’s constitution (Rule 2(s)). Rule 21(2) permits the fund manager to levy an “additional fee on annual net profit” above the hurdle rate. This is effectively a carried interest mechanism. The management fee is payable on a trimestral basis or within one month of each fiscal period (Rule 21(3)). Notably, 2% of all service fees collected during each fiscal year must be deposited with SEBON within two months (Rule 21(4)); failure to deposit on time attracts a 10% annual interest penalty calculated on a daily basis. The offshore fund faces no Nepal-imposed fee constraints.

Investor class differentiation: The SIF Regulation does not explicitly provide for multiple unit classes with different economic rights. Globally, multi-class structures are standard in debt funds. Reform recommendation: SEBON should issue guidelines clarifying that SIFs may issue multiple classes of units with different economic rights, including priority of distributions.

Leverage at fund level: The SIF Regulation is silent on fund-level borrowing. Reform recommendation: Address fund-level leverage explicitly, either permitting it within defined limits (e.g., up to 1x NAV, as India’s SEBI permits for Category II AIFs) or prohibiting it with a clear rationale.

B. Enforcement and Creditor Protection

The Insolvency Act, 2063 grants secured creditors independent enforcement rights (Section 35) and permits foreign creditor claims (Section 48(6)). The Loan Recovery Act, 2058 provides the DRT with court-equivalent powers including interim orders (Section 16) and arrest/detention of willful defaulters (Section 25(2)). Under BAFIA, 2073, Section 57, BFIs can auction collateral without prior court order.

For the offshore fund, FITTA Section 20(4) provides BFI-equivalent auction and repatriation rights for foreign lenders with pledged Nepali property. The onshore SIF, not being a BFI, does not automatically benefit from BAFIA’s streamlined enforcement powers and must rely on standard civil enforcement.

C. Practical Friction and Regulatory Predictability

The Fifth Amendment to the FIFL Bylaws represents meaningful streamlining: (a) expanding the OSSC’s role for S.N. 3 and 4 approvals; (b) clarifying that commercial banks can directly process repatriation without case-by-case NRB approval; (c) allowing Term Sheets to substitute for full loan agreements at approval stage (Schedule-11, Note (a)); and (d) establishing the Foreign Investment and Foreign Loan Facilitation Committee (Bylaw 16), chaired by the NRB Deputy Governor, with power to resolve grievances and remove procedural hurdles.

VII. Comparative Scoreboard and Verdict

Dimension | Onshore SIF | Offshore Direct Lending |

Time to first deployment | 6–12 months | 2–4 months |

Formation cost | NPR 8–13L + intermediaries | Nil in Nepal |

Capital raising flexibility | 200 investors, NPR 50L min, closed-end | Unconstrained by Nepal law |

Interest rate flexibility | Market-driven (no NRB cap) | Capped at Benchmark + 3.5–6.0% |

Tax efficiency (entity) | 25–30% CIT | 0% (no PE) |

Tax efficiency (investor) | 5% WHT on dividends | 5–10% WHT + CGT exempt (DTAA) |

FX risk for borrower | None (NPR lending) | Significant (hedging required) |

Repatriation certainty | NPR distributions; FX risk on foreign LPs | Guaranteed; procedurally bottlenecked |

Structural flexibility | No LP, no multi-class, leverage unclear | Full global standard mechanics |

Enforcement / security | Standard civil enforcement | FITTA S.20(4) BFI-equivalent rights |

Regulatory predictability | SEBON + NRB overlap; debt allocation unknown | NRB single-window (FIFL 5th Amendment) |

Verdict

The offshore direct lending structure and onshore SIF are compared across multiple dimensions above. The onshore SIF’s advantages are limited to two areas: interest rate flexibility (no NRB cap on domestic lending) and elimination of FX risk for the borrower. These are meaningful advantages, but they are overwhelmed by the offshore structure’s superiority in tax efficiency, formation speed, capital raising flexibility, structural mechanics, and enforcement rights.

When the Onshore SIF Makes Sense

Despite its structural disadvantages, the onshore SIF occupies a defensible niche: (a) when the investor base is exclusively domestic institutional capital (insurance companies, pension funds, Citizen Investment Trust) that cannot or prefers not to invest through offshore vehicles; (b) when borrowers require NPR-denominated debt and cannot bear FX risk (mid-market corporates without export revenue); (c) when the government enacts recommended structural reforms (debt fund category, SEBON-NRB joint directive, unit transferability) that would reduce the current friction; and (d) for sectors where NRB’s foreign loan interest rate caps make offshore lending uneconomical.

When the Offshore Fund Wins

The offshore structure is superior for: (a) international investors seeking DTAA-optimized returns with capital gains protection under Article 13(6); (b) large-scale infrastructure project finance (IBN-scale projects above NPR 6 billion) where domestic banks cannot fill the financing gap; (c) situations requiring structural flexibility (multiple investor classes, LP/GP mechanics, leverage); and (d) any context where the 25–30% entity-level tax on the SIF makes the onshore structure non-competitive.

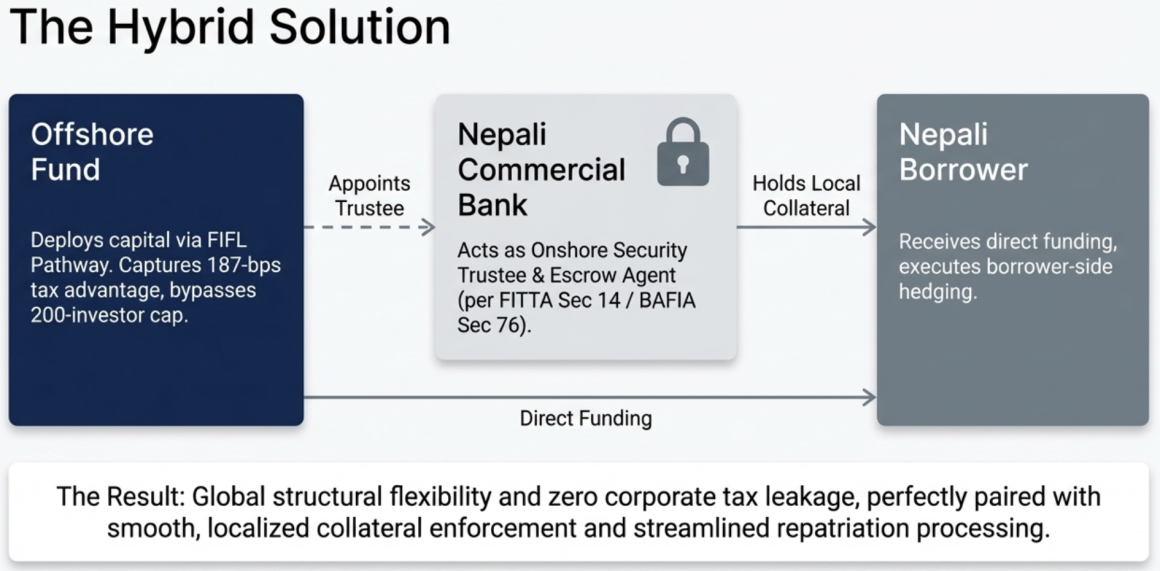

The Hybrid Option

A third pathway worth considering is a hybrid structure: an offshore fund that lends directly under the FIFL Bylaws but appoints a Nepali commercial bank as its onshore security trustee and escrow agent (per FITTA Section 14 and BAFIA Section 76). This captures the offshore fund’s tax efficiency and structural flexibility while establishing a credible onshore enforcement presence. The offshore fund can also partner with a local fund manager or investment advisor to source deals and monitor borrowers, keeping the substantive relationship onshore while the legal and economic structure remains offshore.