1. Context: Why This Regulation Exists

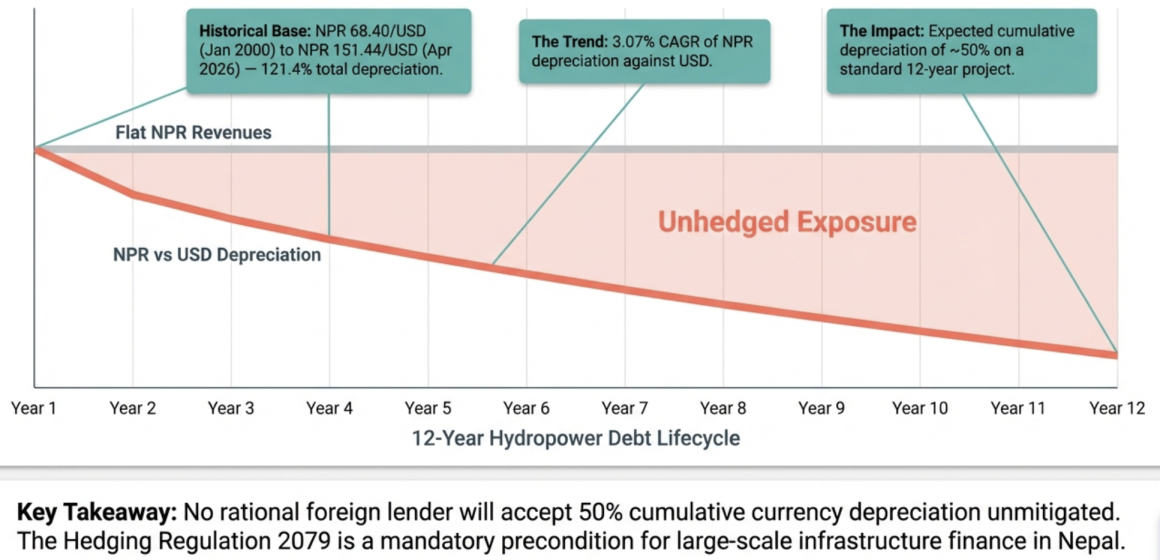

Nepal’s Hedging Regulation 2079 was issued under Section 22 of the Foreign Exchange (Regulation) Act 2019, replacing the earlier Hedging Regulation 2075. It attempts to solve a specific, well-documented problem: foreign investors willing to finance Nepal’s infrastructure – particularly hydropower, transmission, and transport – face unhedgeable currency risk. Revenue from these projects accrues in Nepali Rupees (NPR), but debt service on foreign loans must be paid in foreign currency. With the NPR depreciating against the USD at a compound annual rate of 3.07% over the past 26 years (from NPR 68.40/USD in January 2000 to NPR 151.44/USD in April 2026, a total depreciation of 121.4%), unhedged foreign debt in a 12-year hydropower project faces an expected cumulative depreciation of approximately 50%, with a worst-case historical precedent of 83.9%. No rational lender will accept this risk unmitigated.

The regulation’s premise is straightforward: allow designated institutions to lock the exchange rate at the time foreign currency enters Nepal, so the investor can repatriate principal and interest at the same rate regardless of subsequent depreciation, with the hedging cost shared among the government, a state entity, and the project. Since its enactment, no hedging transaction has been completed under the regulation. This analysis examines why.

2. The Regulation: Provision-by-Provision Analysis

Statutory Authority

The regulation is issued under Section 22 of FERA 2019, which grants the Government of Nepal rule-making power for matters addressed in the Act. FERA 2019 Section 3 grants NRB absolute authority over foreign exchange transactions – any person, firm, or institution wishing to deal in foreign exchange must obtain an NRB license, with NRB empowered to determine transaction types, limits, periods, and conditions. While Section 3 does not explicitly use the terms “hedging” or “derivatives,” FITTA 2075 Section 25(2) explicitly permits foreign-invested industries to use approved derivative instruments through licensed banks to mitigate exchange rate fluctuation risks. The regulatory authority for the hedging framework therefore rests on a composite statutory foundation: FERA 2019 provides the parent rule-making power, FITTA 2075 provides the explicit derivative authorization, and the NRB Act 2058 Section 65 provides NRB’s own authority to transact in forwards, swaps, and options.

Definition of Hedging (Rule 2(cha))

The regulation defines hedging as:

“The act of stabilizing (locking) the foreign exchange rate – so that the loan principal and interest invested in foreign currency within the SDR basket can be repaid and the investment repatriated at the exchange rate prevailing when the foreign currency was deposited into the bank – under the terms of the hedging agreement.”

Three features of this definition are analytically critical. First, the lock applies to the rate prevailing at deposit, not a negotiated rate. There is no provision for locking at a forward rate or at a rate adjusted for expected depreciation. Second, the lock covers both principal and interest, meaning the hedging exposure grows with accrued interest, not just the principal amount. Third, the lock is restricted to currencies within the IMF’s Special Drawing Rights basket (currently USD, EUR, CNY, JPY, GBP), excluding currencies like the Saudi Riyal and UAE Dirham despite their significance to Nepal’s remittance-driven foreign exchange inflows.

The full rate-lock structure is the most generous possible form of currency protection for the investor. It is also the most expensive for the counterparty. A partial hedge – covering, say, the first 25-30% of depreciation – would be substantially cheaper to provide but is not contemplated by this definition. Rule 16, which authorizes a separate “hedging service” where investors bear the full hedging fee independently, offers potential flexibility for negotiated terms, but the core facility under Rules 3-12 is a full lock.

Eligible Projects (Rule 3)

Rule 3(1) restricts hedging eligibility to seven categories of large-scale infrastructure:

# | Project Category | Threshold | Rule Reference |

(ka) | Hydropower (storage or run-of-river) | ≥100 MW | Rule 3(1)(ka) |

(kha) | Electricity transmission lines | ≥220 KV, >30 km | Rule 3(1)(kha) |

(ga) | Metro or monorail | >10 km | Rule 3(1)(ga) |

(gha) | Toll roads, flyovers, underpasses, signature bridges, tunnels; expressways | >50 km (expressways) | Rule 3(1)(gha) |

(nga) | International and regional airports | Construction or expansion | Rule 3(1)(nga) |

(cha) | Health, agriculture, mining, tourism, IT, industrial infrastructure, urban development | >Rs. 2 billion cost | Rule 3(1)(cha) |

(chha) | Other government-designated projects | As determined by GoN | Rule 3(1)(chha) |

Quantifying the eligible universe. The 100 MW hydropower threshold is restrictive. According to Investment Board Nepal’s project pipeline, approximately 30-40 projects currently in Nepal’s active pipeline exceed this capacity, including Arun-3 (900 MW), Upper Karnali (900 MW), Tamor Storage (756 MW), West Seti (750 MW), Lower Arun (669 MW), and several others in the 200-450 MW range. The IBN Annual Report 2022-2023 shows cumulative energy sector approvals of Rs. 892.76 billion across these projects. However, the vast majority of Nepal’s 300+ smaller hydropower projects (10-99 MW) are excluded, despite collectively representing significant investment volume and facing identical currency risk.

The Rs. 2 billion floor for non-energy infrastructure (Rule 3(1)(cha)) is approximately USD 13.2 million at current rates – a moderate threshold that would include most significant tourism, industrial, and urban development projects but exclude smaller municipal infrastructure.

Green infrastructure provision (Rule 3(5)). Banks and financial institutions issuing green bonds or borrowing from international institutions for green infrastructure can access hedging for transactions of at least USD 20 million in SDR currencies, with a maximum hedging period of 7 years and government bearing up to 10% of the hedging fee. The term “green infrastructure” is not defined in the regulation or elsewhere in Nepali statute. This definitional absence renders the provision difficult to operationalize – neither the hedging institution nor applicants have a clear standard for what qualifies.

Hedging applies only to foreign debt, not equity. Rule 2(ga) defines “project” as one receiving foreign currency loan investment listed under Rule 3. Rule 3(2) confirms hedging is available for the principal and interest of loans invested in eligible projects. Foreign equity investment is not covered. This is a deliberate design choice – equity investors accept business risk, including currency risk, as part of their return profile. But it means that a project structured primarily with foreign equity rather than foreign debt cannot access hedging, even if it meets all other eligibility criteria.

The Hedging Fee (Rule 4)

Rule 4(1) assigns fee determination to the hedging institution based on six specified factors:

- Foreign exchange rate risk (विदेशी विनिमय दरको जोखिम)

- Inflation risk (मुद्रा स्फीति जोखिम)

- Project debt-equity ratio and loan repayment period

- Inter-currency prevailing interest rate differentials (अन्तरमुद्रा प्रचलित ब्याजदर)

- Risk management and transfer (जोखिमको व्यवस्थापन तथा हस्तान्तरण)

- Nature of the project

Factor (4), inter-currency interest rate differentials, aligns with the principle of covered interest rate parity (CIP), which is the standard theoretical basis for pricing currency forwards in developed markets. Under CIP, the forward premium (or hedging cost) should equal the interest rate differential between the two currencies. With Nepal’s weighted average lending rate at approximately 8-10% and USD rates at 4-5%, the implied annual hedging premium based purely on interest rate parity would be approximately 4-6% [source: NRB Current Macroeconomic and Financial Situation reports]. This is broadly consistent with the 3.07% historical CAGR of NPR depreciation against USD plus a risk margin.

Factor (5), “risk management and transfer,” is particularly significant. The Nepali text जोखिमको व्यवस्थापन तथा हस्तान्तरण explicitly includes the concept of risk transfer (हस्तान्तरण). This language creates a legal basis for the hedging institution to reinsure or lay off risk to third parties, including multilateral institutions or international hedging entities. When read together with Rule 15 (cooperation with international hedging entities) and Rule 13(3) (cooperation with banking/non-banking institutions with Ministry approval), the regulation appears to contemplate – though not require – a structure where the domestic hedging institution does not retain 100% of the risk.

Rule 4(2) mandates consultation with the Ministry of Finance, NRB, the business entity, the relevant regulatory body, the project, and the investor in setting the fee. Rule 4(3) preserves pre-existing fee agreements under the replaced Regulation 2075. The regulation provides no formula, no benchmark, no reference rate, and no ceiling or floor for the premium. This is the single most consequential gap in the regulation. Every other provision – eligible projects, cost-sharing, institutional designation, rate-locking – is precisely defined. The premium, which determines whether the entire framework is financially viable, is left entirely to negotiation. The previous regulation (2075) failed precisely because of pricing disagreements, and the 2079 replacement does not resolve this.

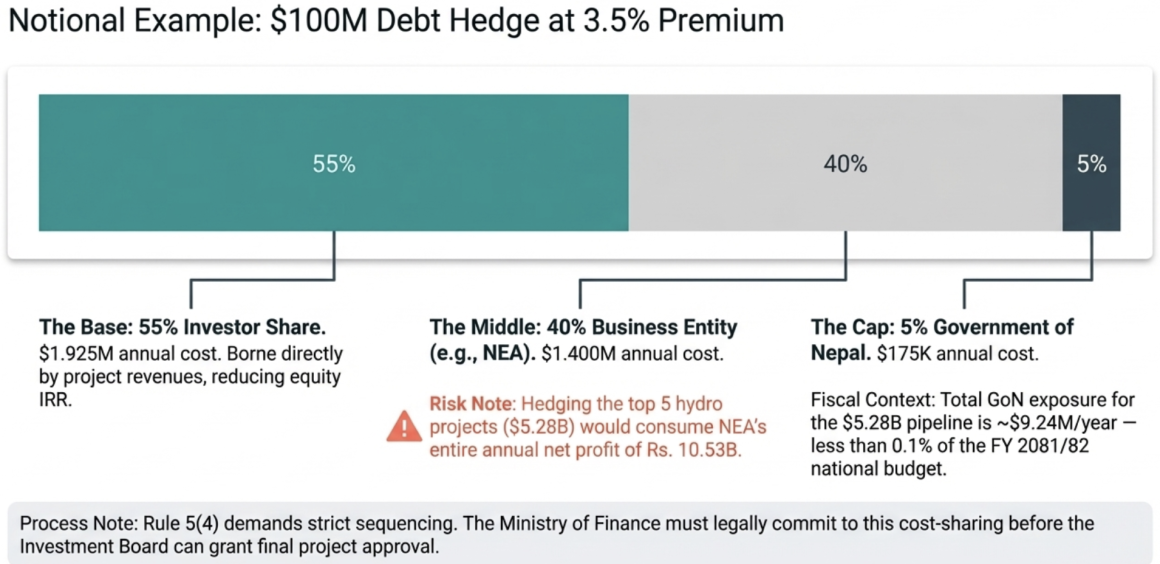

Fee Cost-Sharing (Rule 5)

Rule 5 establishes who bears the hedging fee. The provision applies only to projects implemented under public-private partnership through the PPP and Investment Act 2075 that are classified as national priorities or national pride projects (राष्ट्रिय प्राथमिकता वा राष्ट्रिय गौरवका परियोजना).

The three parties:

- Government of Nepal (नेपाल सरकार): The federal government’s direct fiscal contribution from the national budget, recoverable under Rule 5(6) from fees, royalties, or duties the government is entitled to receive from the project.

- Business Entity (व्यावसायिक संस्था): Defined in Rule 2(nga) as a fully or partially government-owned authority, corporation, institution, company, or fund established under prevailing law that approves or permits the project. For PPP projects, it includes the Investment Board Nepal established under Section 5 of the PPP and Investment Act 2075. The business entity bears the largest single component (20-40% depending on project type).

- Project/Investor: The residual share borne by the project company or the foreign lender/investor whose loan is being hedged, coming directly from project revenues and reducing the project’s return on equity.

Project Type | GoN Share | Business Entity | Investor | At 3.5% Premium: Investor Annual Cost | At 3.5% Premium: GoN Annual Cost on $100M |

100 MW+ hydropower | 5% | 40% | 55% | 1.925% ($1.925M) | 0.175% ($175K) |

220 KV+ transmission | 20% | 35% | 45% | 1.575% ($1.575M) | 0.700% ($700K) |

Metro/monorail >10km | 5% | 30% | 65% | 2.275% ($2.275M) | 0.175% ($175K) |

Toll roads, expressways | 10% | 30% | 60% | 2.100% ($2.100M) | 0.350% ($350K) |

Int’l/regional airports | 20% | 30% | 50% | 1.750% ($1.750M) | 0.700% ($700K) |

>Rs. 2B infrastructure | 10% | 20% | 70% | 2.450% ($2.450M) | 0.350% ($350K) |

Note: Dollar amounts assume $100M notional hedged amount and 3.5% annual premium (illustrative). Actual premium will be determined under Rule 4.

Quantifying the fiscal exposure. If Nepal were to hedge foreign debt across the five largest hydropower projects currently in the IBN pipeline (Arun-3 at $1.04B, Upper Karnali at $1.05B, Tamor at $1.2B, West Seti at $1.32B, Lower Arun at $670M – total approximately $5.28B), the government’s 5% share at a 3.5% annual premium would be approximately $9.24 million per year. This is a modest fiscal commitment relative to the government’s total annual expenditure of approximately Rs. 1,512.98 billion (~$12B) for FY 2081/82, representing less than 0.1% of total expenditure. However, no budget line item currently exists for this purpose, and no appropriation mechanism has been established.

The business entity burden. IBN’s 40% share on the same portfolio would be approximately $73.9 million per year. But IBN is not an investment or business wing, its is an approval unit, so this business entity for the purpose of hydropower could be interpreted to be NEA. Assuming this business entity were NEA – NEA’s most recent net profit was Rs. 10.53 billion (approximately $69.4M at current rates) [source: SOE Status Review FY 2080/81]. This means hedging the top five hydropower projects alone would consume NEA’s entire annual profit. NEA’s total accumulated profit stands at Rs. 46.47 billion and its net worth at Rs. 259.10 billion, providing some buffer, but the sustained annual drain would be significant. Rule 5(7) permits NEA to pass this cost to consumers through electricity tariffs, but whether the Electricity Regulatory Commission has the statutory authority to include hedging costs in tariff calculations requires verification against the Electricity Act.

Rule 5(4) sequencing requirement. For projects where the government will bear a share of the hedging fee, the Ministry of Finance’s consent must be obtained before the project is approved (परियोजना स्वीकृति हुनु अघि). The project, business entity, and hedging institution must submit a joint application to the Ministry (Rule 5(5)). This creates a strict sequencing: hedging terms must be negotiated and the Ministry must commit to cost-sharing before the Investment Board Nepal can grant final project approval. In practice, this means hedging is not a post-approval add-on; it must be integrated into the project approval process from the outset.

The Hedging Institution (Rule 6)

Rule 6(1) restricts eligibility to institutions meeting all of the following criteria: (a) licensed by NRB under prevailing law, (b) an infrastructure development bank or commercial bank, (c) with full or partial government ownership, and (d) willing to submit a business plan to the Ministry of Finance.

The Ministry evaluates the proposal, the business plan, and the applicant’s operational capacity before designating the institution (Rule 6(2)).

Eligible institutions and their constraints:

Institution | Govt. Ownership | Total Assets | Core Capital (est.) | 30% NOP Limit (est.) | CAR | Key Constraint |

Rastriya Banijya Bank | 99.97% | Rs. 350 bn | ~Rs. 36 bn | ~$71M | 14.31% | Weak FX risk systems, high NPL (3.07%) |

Nepal Bank Limited | 51% | Rs. 269 bn | ~Rs. 30 bn | ~$59M | 12.51% | Limited treasury infrastructure |

Agri. Dev. Bank | 51% | Moderate | ~Rs. 25 bn | ~$49M | >11% | No infrastructure mandate |

NIFRA | Partial (govt.) | Rs. 41.55 bn | Rs. 24.10 bn | ~$48M | 77.56% | Only 27 staff; NPL 0.009% |

NOP limits are estimated as 30% of core capital converted at NPR 151/USD. Actual limits depend on NRB’s quarterly publications relating to banking sector.

The 30% Net Open Position limit, prescribed in NRB Directive No. 5/081, caps each institution’s daily absolute net foreign exchange position at 30% of the previous quarter’s primary capital. This limit applies to both commercial banks and infrastructure development banks. For NIFRA, with core capital of Rs. 24.10 billion, the NOP ceiling is approximately Rs. 7.23 billion or USD 48 million. A single 200 MW hydropower project with USD 100 million in foreign debt would exceed this limit by more than double.

The aggregate NOP capacity of the entire Nepali banking system is approximately USD 1.04 billion [source: Onshore vs Offshore Debt Fund analysis]. If the hedging regulation is to accommodate even a fraction of the $5+ billion in pipeline infrastructure projects, the NOP constraint must be addressed through a specific regulatory carve-out for hedging fund positions.

NIFRA as the optimal designation. Despite its small staff, NIFRA is the strongest candidate. Its unified directive explicitly permits derivative operations (forwards, options, swaps, futures), international borrowing with NRB approval, and foreign currency account operations. It can accept unconditional guarantees from recognized multilateral development banks (World Bank Group, ADB, AIIB), and project loans backed by such guarantees can receive zero risk weight for capital adequacy purposes with NRB approval. Its infrastructure-specific mandate aligns with Rule 3’s eligible project categories. Its 77.56% CAR (against an 11% minimum) means it has substantial unused capital capacity – although much of this huge CAR has to do with its concentration of investments in the fixed deposits. Its single obligor limit for infrastructure is 50% of primary capital, allowing exposure of approximately Rs. 12 billion (~$79M) to a single project.

Hedging Duration (Rule 7)

Project Category | Maximum Hedging Period | Rule Reference |

Transmission lines, toll roads/expressways, airports | 7 years from rate-lock date | Rule 7(2)(ka) |

Hydropower, metro/monorail, >Rs. 2B infrastructure | 12 years from rate-lock date | Rule 7(2)(kha) |

Government-designated projects | As determined by GoN | Rule 7(2)(ga) |

A one-time extension of up to 5 years is available (Rule 7(3)), to be requested at least 90 days before expiry (Rule 7(4)). The hedging institution determines the extension rate and fee with Ministry approval (Rule 7(5)).

The 12-year maximum for hydropower aligns reasonably with typical debt tenors for large hydro projects (10-15 years). However, many large storage projects have construction periods of 5-7 years followed by 15+ year debt repayment, meaning the 12-year hedge (even with the 5-year extension to 17 years) may not cover the full debt lifecycle. This mismatch would leave the investor exposed to currency risk in the final years of debt service.

Rate-Lock Mechanism (Rules 11-12)

The operational mechanics are precise:

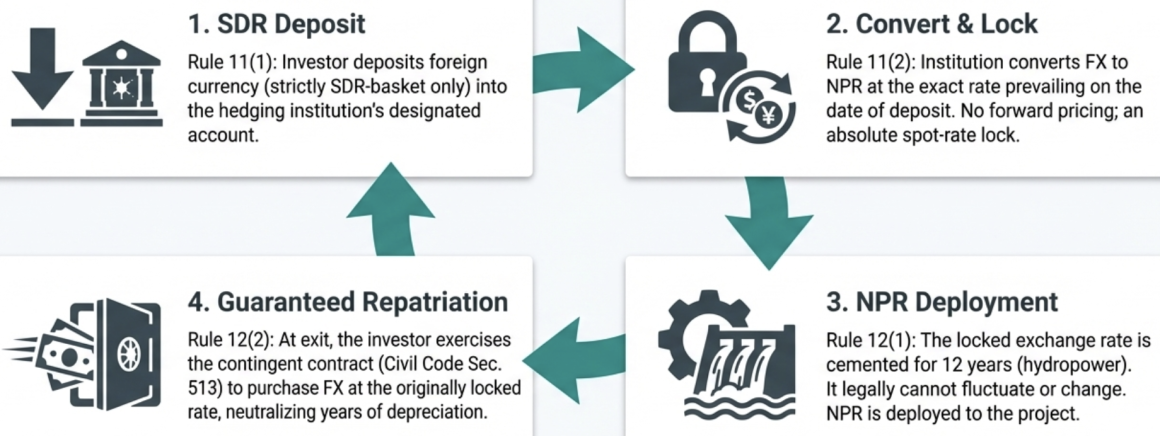

Step 1 (Rule 11(1)): The approved project or investor deposits foreign currency in SDR-basket currencies into the hedging institution’s designated bank account within the period specified by the hedging institution.

Step 2 (Rule 11(2)): The hedging institution converts the foreign currency to NPR at the exchange rate prevailing on the date of deposit (जम्मा गर्दाको दिन कायम रहेको विनिमय दर) and credits the NPR to the project’s account at a commercial bank.

Step 3 (Rule 12(1)): The exchange rate used in Step 2 is locked (स्थिर). It shall not change or fluctuate (हेरफेर वा घटबढ नहुने गरी स्थिर गर्नेछ) for the duration of the hedge.

Step 4 (Rule 12(2)): At repatriation, the hedging institution provides the investor with foreign currency at the locked rate per the hedging agreement.

This mechanism makes the hedging institution the counterparty to a currency forward – it has promised to deliver foreign currency at a fixed rate at a future date. Under the National Civil Code 2074, Section 513 (contingent contracts), this obligation is valid but only crystallizes when the investor exercises the repatriation right. The investor is not obligated to repatriate; they may choose to reinvest in Nepal, in which case the hedge is never exercised and the institution retains all collected premiums without any payout.

The Separate Fund (Rule 13)

Rule 13(1) mandates a separate fund (छुट्टै कोष) for all hedging activities. Rule 13(2) requires all hedging income to be deposited in this fund and all hedging payouts to be made from it. Rule 13(4) requires separate accounting under Nepal Financial Reporting Standards, distinct from the institution’s other business.

Rule 13(3) permits the hedging institution, with Ministry approval, to borrow (ऋण स्वीकार गर्न), co-invest (सहलगानी गर्न), or cooperate (सहकार्य गर्न) with banking or non-banking institutions for hedging purposes. The phrase “banking or non-banking institutions” is not restricted to domestic entities, providing a legal basis for cooperation with international DFIs.

Rule 14 permits the hedging fund to be invested in income-generating projects or activities (कुनै परियोजना वा आयमूलक कार्यमा) with Ministry approval. This is a broad authorization – the fund is not limited to government securities or low-yield instruments but can invest in any income-generating activity the Ministry approves. This provision could allow the hedging fund to earn returns exceeding the Treasury yield currently earned on NRB’s foreign securities portfolio, improving the fund’s financial viability.

Protected Status (Rule 22)

Rule 22 classifies hedged foreign currency as “reserved foreign exchange” under FERA 2019 Section 6(2). The full text of the relevant FERA provision: FERA Section 6(1) grants the Government emergency powers to order citizens and entities to sell foreign exchange to NRB at prescribed rates during an economic or monetary crisis. Section 6(2) provides an absolute exemption: this forced surrender order “shall not apply to foreign exchange that was legally obtained from a licensed person with the Bank’s permission and kept for a specific, permitted purpose.”

By classifying hedged forex under Section 6(2), Rule 22 creates a legal ring-fence ensuring that even during a national forex crisis – precisely the scenario in which hedging protection is most needed – the government cannot confiscate, redirect, or force-convert the hedged foreign currency. This is a powerful investor protection that no other Nepali legal instrument provides.

Regulation and Oversight (Rules 19-21)

Rule 19 requires the hedging institution to submit regular reports to both the Ministry of Finance and NRB covering hedging facility and service details, schedules, risk status, foreign currency inflows and outflows, and fund status. Rule 20 grants NRB the power to regulate and issue directives to the hedging institution. Rule 21 requires the hedging institution to consult with the Ministry, NRB, Investment Board, relevant ministries, and project stakeholders.

NRB’s regulatory authority under Rule 20 is significant because it means NRB retains supervisory control even though the hedging institution operates under a regulation issued by the Ministry of Finance, not under NRB’s own directives. This dual oversight – Ministry for policy and fee-sharing, NRB for prudential regulation and forex operations – creates a complex governance structure that requires close inter-agency coordination.

3. Interaction with Parent Laws

FERA 2019: The Foundation

FERA 2019 is the parent Act under whose Section 22 the regulation is issued. Several FERA provisions directly constrain or enable the hedging framework:

Section 3 (NRB authority): NRB controls all foreign exchange transactions. Any hedging operation requires NRB licensing or authorization. The hedging institution must be licensed by NRB (Rule 6(1)), and Rule 18 mandates NRB to provide the exchange facility at prevailing rates.

Section 4(1) (prohibition on unauthorized transactions): Dealing in foreign exchange with anyone other than an NRB-licensed person without NRB approval is prohibited. A hedging arrangement structured outside the regulation would be an illegal forex transaction – the contract would be void and unenforceable, the entities would face fines of Rs. 50,000 to Rs. 500,000 and license revocation under Section 3A, and NRB would block any repatriation attempt.

Section 6 (emergency powers): Discussed above under Rule 22.

Section 9C (payment restrictions): Foreign exchange payments are restricted unless specifically authorized. This makes Rule 18’s mandatory exchange facility provision essential – without it, the hedging payout (an NPR-to-foreign-currency conversion) would be blocked by Nepal’s standard capital controls.

Section 10Ga (NRN investment): Foreign investors including non-resident Nepalis may invest in securities including bonds. NRNs can maintain foreign currency accounts (Section 16(4)). These provisions enable NRN participation in hedging-backed instruments if such instruments are developed.

NRB Act 2058: Central Bank Powers

Section 5(e): Foreign exchange reserve management is a primary function of NRB.

Section 65: NRB is explicitly authorized to conduct foreign exchange transactions using spot, forward, swap, and option rates. This is the direct statutory authority for the derivative instruments inherent in hedging. When the hedging institution locks an exchange rate under Rule 12, it is functionally entering a long-dated forward contract. NRB’s Section 65 authority allows it to provide the forex counterparty function that makes this possible.

Section 66(1): Defines reserves (gold, foreign currency, SDRs, foreign instruments). Section 66(1)(f) allows agreements for future purchase or sale of foreign exchange with creditworthy counterparties – a direct authorization for forward and swap contracts.

Section 66(2): Reserve management must prioritize safety and liquidity over income. This means if hedging activities create risk to reserve safety, NRB is statutorily required to prioritize reserve protection over hedging income.

Section 66(3)-(4): No fixed minimum reserve ratio; instead, a qualitative “adequate reserve” standard with a mandatory government reporting protocol if reserves fall to concerning levels – which is generally determined through the monetary policy.

FITTA 2075: Foreign Investment Framework

Section 12 (foreign debt): Foreign-invested industries can obtain project loans from foreign financial institutions with NRB approval and (the previous requirement for Ministry recommendation was removed by the Investment Facilitation Amendment Act 2081). This is the provision through which foreign currency loans enter Nepal and become eligible for hedging. Under the FIFL Bylaws 2078, Bylaw 7(1), NRB pre-approval is required before foreign currency enters Nepal, and the loan must be recorded with NRB within six months (Bylaw 8(1)).

Section 20 (repatriation): Foreign investors may fully or partially repatriate investment and earnings, including sale proceeds, profits/dividends, residual amounts after liquidation, royalties, lease rents, and compensation from legal proceedings. Repatriation occurs at the prevailing exchange rate (Section 20(3)) – unless a hedging agreement exists, in which case Rule 12 of the Hedging Regulation overrides this to apply the locked rate.

Section 25(2) (derivatives): Industries with foreign investment may use approved derivative instruments through licensed banks to mitigate exchange rate fluctuation risks. This is the explicit FITTA authorization for hedging that complements FERA and the NRB Act.

Investment Facilitation Amendment Act 2081: Removed the Ministry recommendation requirement for foreign loans (amending FITTA Section 12), meaning investors now need only NRB approval to bring in foreign debt. This streamlines the path to hedging by eliminating one approval layer. The Amendment also consolidated FDI approval authority at the Department of Industry (amending FITTA Section 17), reducing jurisdictional fragmentation.

BAFIA 2073: Banking Constraints

Section 49 (permitted activities): Class A commercial banks may issue guarantees (Section 49(1)(y)). Hedging is functionally a guarantee against currency depreciation, suggesting it falls within existing banking powers.

Off-balance-sheet recognition: BAFIA defines off-balance sheet transactions to include foreign exchange swaps, options, and forward transactions. The hedging commitment is an off-balance-sheet contingent liability for the hedging institution.

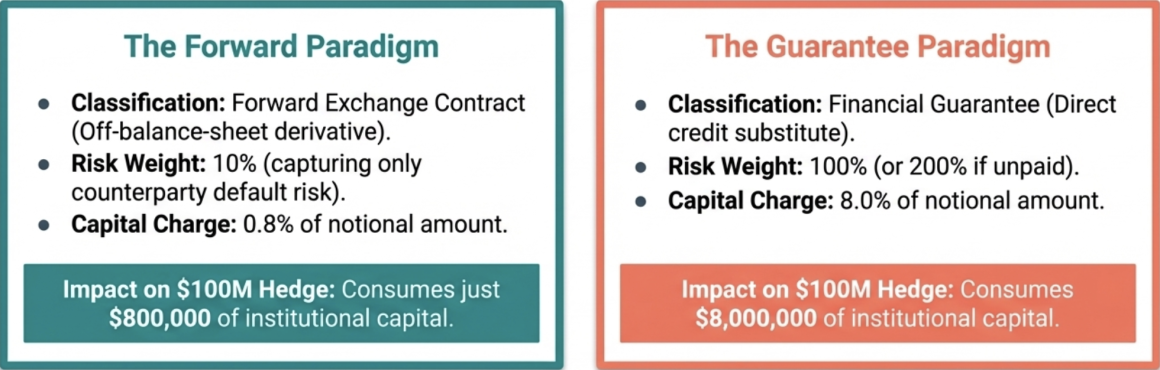

NOP and SOL limits (Unified Directives): Directive No. 5/081 prescribes the 30% NOP limit. The Single Obligor Limit (SOL) is 25% of primary capital (30% for priority sectors including hydropower and transmission lines), and 50% for NIFRA. Forward exchange contracts attract a 10% risk weight for capital adequacy. Financial guarantees attract a 100% risk weight. If the hedging obligation is classified as a financial guarantee rather than a forward contract, the capital charge is 10× higher.

Forward exchange contract: 10% risk weight × notional amount × 8% minimum capital = 0.8% capital charge

Financial guarantee: 100% risk weight × notional amount × 8% = 8.0% capital charge

On a $100M hedge, this is the difference between $800,000 and $8,000,000 in required capital. The regulation does not specify which classification applies. NRB's operational circular (when issued) must resolve this.

National Civil Code 2074: Contract Law

Section 505 (valid contracts): Hedging agreements must have consent, competent parties, definite subject matter, and lawful obligation. All are met by a properly structured hedging contract.

Section 513 (contingent contracts): A hedging obligation is a contingent contract – the obligation to pay crystallizes only when the investor exercises repatriation and the market rate differs from the locked rate. Section 513(1) validates such contracts; the obligation arises only after the triggering event occurs.

Section 529 (assignment): If the hedging institution wants to transfer its obligation to a co-guarantor or reinsurer, it requires the consent of the other party (the investor), must be in writing, and must be unconditional. Notice must be provided. This is relevant for risk transfer under Rules 15 and 13(3).

Section 531 (force majeure): Performance is excused only for genuinely impossible circumstances (war, flood, earthquake, etc.). Section 531(3) explicitly provides that performance becoming difficult or resulting in loss does not constitute force majeure. A decline in foreign currency reserves would be classified as commercial difficulty, not impossibility, meaning the hedging institution cannot suspend payouts based on reserve stress.

Sections 563-574 (guarantee and indemnity): The hedging contract functions as both a guarantee (Section 563, where the hedging institution guarantees the investor against currency loss) and an indemnity (Section 571, where the institution promises to save the investor from exchange-rate loss). Guarantees must be in writing (Section 563(4)). The limitation period for guarantee claims is 2 years from the cause of action (Section 574).

Section 540 (specific performance): An investor can seek specific performance (forcing the institution to convert at the locked rate) if monetary damages are inadequate. Given that the locked rate represents a unique contractual protection, a court may find specific performance appropriate.

National Civil Code 2074: Contract Law

Section 505 (valid contracts): Hedging agreements must have consent, competent parties, definite subject matter, and lawful obligation. All are met by a properly structured hedging contract.

Section 513 (contingent contracts): A hedging obligation is a contingent contract – the obligation to pay crystallizes only when the investor exercises repatriation and the market rate differs from the locked rate. Section 513(1) validates such contracts; the obligation arises only after the triggering event occurs.

Section 529 (assignment): If the hedging institution wants to transfer its obligation to a co-guarantor or reinsurer, it requires the consent of the other party (the investor), must be in writing, and must be unconditional. Notice must be provided. This is relevant for risk transfer under Rules 15 and 13(3).

Section 531 (force majeure): Performance is excused only for genuinely impossible circumstances (war, flood, earthquake, etc.). Section 531(3) explicitly provides that performance becoming difficult or resulting in loss does not constitute force majeure. A decline in foreign currency reserves would be classified as commercial difficulty, not impossibility, meaning the hedging institution cannot suspend payouts based on reserve stress.

Sections 563-574 (guarantee and indemnity): The hedging contract functions as both a guarantee (Section 563, where the hedging institution guarantees the investor against currency loss) and an indemnity (Section 571, where the institution promises to save the investor from exchange-rate loss). Guarantees must be in writing (Section 563(4)). The limitation period for guarantee claims is 2 years from the cause of action (Section 574).

Section 540 (specific performance): An investor can seek specific performance (forcing the institution to convert at the locked rate) if monetary damages are inadequate. Given that the locked rate represents a unique contractual protection, a court may find specific performance appropriate.

National Criminal Code 2074: Liability Framework

Section 249 (fraud): If a hedging institution accepts premiums knowing it cannot honor the hedge in a worst-case scenario, this could constitute fraud – defined as dishonestly causing someone to believe something (the validity of the guarantee) and then failing to act accordingly. “Passive deception” (dishonestly hiding material facts) is included. Punishment: up to 10 years imprisonment and Rs. 100,000 fine if the fraud is against a government-owned entity.

Section 252 (criminal breach of trust): If a hedging fund manager acts contrary to the hedging agreement to benefit themselves or others, causing loss to the investor, this constitutes criminal breach of trust. Punishment: up to 5 years imprisonment and Rs. 50,000 fine for institutional officers.

Section 30 (corporate liability): If the hedging institution commits an offense, the person who committed or caused the act is liable. If unidentifiable, directors, managing directors, or general managers bear criminal liability.

These criminal provisions create personal liability for officers of the hedging institution. Combined with the Civil Code’s guarantee and specific performance provisions, the legal framework provides substantial enforcement mechanisms for investors. However, these mechanisms have never been tested in the hedging context.

4. Operational Gap Analysis

Gap 1: No Designated Hedging Institution

Status: No institution has been formally designated under Rule 6. Without designation, no entity can receive applications (Rule 8), determine fees (Rule 4), issue hedging solicitation certificates (Rule 10(3)), or execute rate-lock transactions (Rules 11-12).

Resolution: Ministry of Finance to initiate the designation process. The most suitable candidate is NIFRA, based on the analysis in Section 2 above. Estimated timeline: 3-6 months including business plan evaluation and capacity assessment.

Gap 2: No Hedging Premium Pricing Methodology

Status: Rule 4 lists six factors but provides no formula, benchmark, or range. The predecessor regulation (2075) was amended twice due to pricing misalignment, and the 2079 replacement still does not resolve the core pricing question.

Impact: Every potential hedging transaction becomes a zero-sum negotiation. The hedging institution wants a higher premium to cover tail risk; the investor wants a lower premium to preserve project IRR. Without a reference methodology, there is no neutral ground for agreement.

Resolution: NRB should issue a pricing circular establishing a reference rate based on the 3.07% CAGR of NPR/USD depreciation (26-year historical basis), adjusted for the specific loan currency (SDR basket currencies depreciate at different rates – JPY-denominated debt faces only 13.4% depreciation over the 2015-2026 period compared to 50.6% for USD), the project’s specific risk profile, and a countercyclical buffer. The circular should specify whether CIP, historical VaR, or option-pricing approaches are to be used, and should publish a quarterly reference rate.

Gap 3: No NRB Operational Circular

Status: The NRB Unified Circular 2081 (Foreign Exchange Transactions) and all intervening circulars contain zero references to the Hedging Regulation 2079, hedging premium pricing, or operational guidelines for implementing the framework. The only derivative-related provision in recent circulars is the 25% cap on proprietary derivative transactions relative to primary capital (Chapter 19, Section 2(ga) of the Unified Circular).

Impact: Banks and NIFRA have no operational guidance on: how to account for hedging positions in their financial statements, instructions on classification of hedge contract – whether as a forward contract (10% risk weight) or a financial guarantee (100% risk weight), whether hedging fund positions are exempt from or included in the 30% NOP calculation, what reporting formats to use under Rule 19, or how to operationalize the rate-lock in their core banking systems.

Resolution: NRB’s Foreign Exchange Management Department, in coordination with the Bank Supervision Department, should issue a comprehensive hedging implementation circular addressing all of the above. This is the single most critical prerequisite for operationalizing the regulation.

Gap 4: NOP Limit Blocks Scale

Status: The 30% NOP limit on primary capital restricts the entire banking system’s aggregate FX capacity to approximately USD 1.04 billion. NIFRA’s individual limit is approximately USD 48 million. The pipeline of eligible hydropower projects alone has foreign debt requirements exceeding USD 5 billion.

Resolution: NRB should create a hedging-specific NOP exemption for positions held within the ring-fenced fund under Rule 13. The legal basis exists: NRB Act Section 79 grants broad regulatory power, and Directive 5/081 can be amended through circular to exclude Rule 13 fund positions from the NOP calculation. The ring-fencing requirement (separate fund, separate accounting, separate reporting) provides adequate prudential safeguards to justify the exemption.

Gap 5: Full Rate-Lock Only

Status: The definition in Rule 2(cha) and the rate-lock mechanism in Rule 12 contemplate only a full rate-lock. There is no explicit provision for partial coverage, caps, deductibles, or tiered products.

Impact: A full rate-lock on a 12-year USD hedge requires a premium of approximately 3.5-4.5% annually to break even against expected depreciation. At a 3.5% premium with 55% investor share (hydropower), the effective annual cost to the developer is 1.925% – potentially acceptable for high-IRR projects but prohibitive for marginal ones.

Resolution: Two paths exist. First, amend Rule 2(cha) to explicitly authorize partial hedging products. Second, use Rule 16 (hedging service), which allows the hedging institution to provide customized hedging services where the investor bears the full fee, with terms determined by agreement. Rule 16(2) states that the “type, period, and other conditions of the hedging service” are per the agreement. This language is broad enough to accommodate partial coverage, capped exposure, or any other negotiated structure.

Gap 6: No Risk Transfer Mechanism

Status: Rules 15 and 13(3) provide legal authority for international cooperation and risk-sharing. No operational framework exists to execute this.

Impact: 100% of hedging risk remains on a domestic institution with limited FX management capacity.

Resolution: Engage TCX Fund (which completed its first Nepal transaction in 2023 and covers 140+ currencies) for a back-to-back hedging arrangement. Under such an arrangement, the domestic hedging institution provides the hedge to the investor under the regulation, then enters a corresponding swap with TCX to transfer all or part of the currency risk. The domestic institution earns a margin (the spread between the premium collected from the investor and the premium paid to TCX) without retaining the tail risk. This requires FERA approval for the cross-border derivative transaction (Rule 15 provides the Hedging Regulation authority, but FERA Section 3 still requires NRB licensing for the cross-border component). NRB should issue a specific circular authorizing hedging institutions to enter into offshore derivative transactions for hedging risk transfer purposes.

Gap 7: No Fiscal Budget for Government’s Fee Share

Status: Rule 5(2) commits the government to bearing 5-20% of the hedging fee. No budget line item exists for this purpose in the Ministry of Finance’s annual appropriation. The Constitution of Nepal mandates that all government expenditures be authorized by Parliament through the Appropriation Act. Without a budgetary allocation, the government’s commitment is legally unenforceable.

Resolution: The Ministry of Finance should create a dedicated budget line under financial management expenditure. Given the modest fiscal exposure (estimated at less than $10 million annually even for a $5 billion hedging portfolio), this can be accommodated within existing fiscal space.

Gap 8: “Green Infrastructure” Undefined

Status: Rule 3(5) provides hedging for green infrastructure, but the term is not defined in the regulation or elsewhere in Nepali law.

Resolution: The Ministry should define green infrastructure through a schedule to the regulation, referencing established international taxonomies (EU Taxonomy, Climate Bonds Standard, or NRB’s own green classification under its Environmental and Social Risk Management Guidelines).

Gap 9: Treasury and Human Capital Gaps

Status: NRB’s Bank Supervision Reports consistently identify systemic weaknesses across the banking sector in derivative operations: banks lack strategies and business plans for FX operations, middle offices for treasury risk management are non-functional, many banks rely on Gap Analysis as their sole risk measurement tool, there is high staff turnover and a dearth of specialized manpower, and sensitive compliance tasks are sometimes delegated to interns. NIFRA operates with just 27 staff.

Resolution: A dedicated technical assistance program from IFC or ADB to build hedging-specific capacity at the designated institution. This could include: treasury system implementation, risk management methodology and tools, staff training (pricing, execution, accounting, reporting), and operational procedure development.

Gap 10: Repatriation Bottleneck

Status: The investor’s repatriation sequence spans multiple agencies: foreign investment approving body approval (15-day timeline under FITTA Section 20), commercial bank processing (7-day mandate under FIFL Bylaw 9(3)), NRB exchange facility provision (Rule 18), plus mandatory tax clearances, audit submissions, and CIB checks. Each step introduces delay and uncertainty.

Resolution: Create a fast-track repatriation channel specifically for hedged investments. The hedging solicitation certificate (Rule 10(3)) could serve as pre-authorization for repatriation, eliminating the need for case-by-case NRB approval at exit. The commercial bank processing mandate should be enforced with penalties for non-compliance.

5. The ADF Bill

The Alternative Development Finance Mobilization Bill 2081, though currently pending re-presentation to Parliament due to political changes, contains provisions that could strengthen the Hedging Regulation’s institutional architecture.

Section 25 (Guarantee Fund): Authorizes the ADF to establish a guarantee fund backed by GoN or international financial institution guarantees, channeling these to enable lending to infrastructure projects. The ADF can combine government-backed guarantees with its own guarantee capacity for joint guarantees (Section 25(4)). This layered guarantee architecture maps directly onto the hedging facility concept – the ADF’s guarantee fund could backstop the hedging institution’s payouts, providing an additional credit enhancement layer beyond the institution’s own capital.

Section 28 (Government-Parity Treatment): Fund-issued bonds with GoN guarantee receive the same regulatory treatment as sovereign instruments. Under the NRB Capital Adequacy Framework, this means 0% risk weight (eliminating capital charges for banks holding these instruments), eligibility for SLR compliance (where Class A banks and Infrastructure Development Banks must maintain 12% of deposits in approved liquid assets), eligibility as collateral for NRB’s Standing Liquidity Facility (at up to 90% of face value – which defines the valuation limit or the maximum loan amount an institution can borrow against its collateral of these instruments), exemption from Single Obligor Limits, and eligibility for NRB open market operations. If the hedging fund were to issue bonds backed by both the ring-fenced fund and a GoN guarantee, these bonds would become quasi-sovereign instruments, dramatically broadening the potential investor base and creating a secondary market mechanism for distributing hedging risk across the banking system.

Section 9(1)(wa) (Hedging Authorization): The ADF Bill review references Section 9(1)(wa) as explicitly directing the institution to “arrange hedging for international loans.” If enacted, this would create a statutory mandate for hedging that goes beyond the permissive framework of the current regulation.

Institutional Design Advantage: The ADF Fund, established by its own special Act and operating outside BAFIA’s standard framework, would not be subject to the NOP limits, SOL constraints, or other prudential requirements designed for deposit-taking banks. This eliminates the most binding constraint on the current hedging regulation’s implementation. However, the ADF Bill’s governance structure (4 of 7 board members are government officials) raises independence concerns that could affect credibility with international investors.

6. Conclusion

The Hedging Regulation 2079 addresses a genuine and well-documented barrier to foreign investment in Nepal’s infrastructure. Its provisions for rate-locking, cost-sharing, fund ring-fencing, international cooperation, and sovereign crisis protection are legally sound when read against Nepal’s statutory architecture. The regulation’s interaction with FERA 2019, FITTA 2075, the NRB Act 2058, and the Civil Code 2074 is coherent, with Rule 18’s mandatory exchange facility and Rule 22’s reserved forex classification solving the two most critical operational problems (capital controls blocking payouts and sovereign emergency powers confiscating hedged funds).

Specific, identifiable gaps – most critically the absence of a designated institution, pricing methodology, and NRB operational circular – have prevented the first transaction from occurring. No legislative amendment is required for the core implementation; the tools available to the Ministry of Finance and NRB under existing law seems to be sufficient to operationalize the regulation. The regulation has existed in various forms since 2019. It has been amended from 2075 to 2079. Pricing disputes have persisted through both versions. No institution has been designated. No circular has been issued. The longer this dormancy continues, the more it signals to foreign investors that Nepal’s hedging framework is legislative performance rather than operational infrastructure. Each year of inaction is a year of foregone investment in hydropower, transmission, and transport projects that the country urgently needs. The data shows the economics work. The law provides the authority. What remains is execution.