Retirement Plan

Introduction

Retirement planning, in a financial context, refers to the allocation of savings or revenue for retirement. Nothing more. Retirement planning is ideally a life-long process. You can start at any time, but it works best if you factor it into your financial planning from the beginning. That’s the best way to ensure a safe, secure—and fun—retirement. The fun part is why it makes sense to pay attention to the serious and perhaps boring part: planning how you’ll get there.

How to plan retirement?

Well, you can’t freely / properly plan your retirement in Nepal. GoN has now imposed Social Security Fund Act in Nepal. SSF has led to wide disagreement between pro-privatized retirement plan and pro-state managed retirement plans.

And how fair is the Social Security Fund? As fair as the Raven’s feather. There are lot of disagreement with the SSF in Nepal. People are afraid if the GoN will Actuarial-Valuate and Monte-Carlo-Simulate the retirement plan empty. View my other post discussing: Confusions surrounding Social Security Fund (SSF)

How does an Individual Plan Retirement?

Personal retirement planning typically includes

- Preparing working environment.

- Prepare mentally and plan to involve in hobbies and develop new interests to be engaged with retirement life.

- Plan and prepare for the transition impact of retirement with home life.

- Plan how active you want to be when you reach retirement age, engage in part-time, contract work or in activities that doesn’t overextend oneself.

- Stay connected with the community.

- Learning to appreciate leisure, moderating work-life balance and to say no without regrets.

- Building family who will take care of you or building a retirement fund suited to your needs and investing / depositing your funds safely.

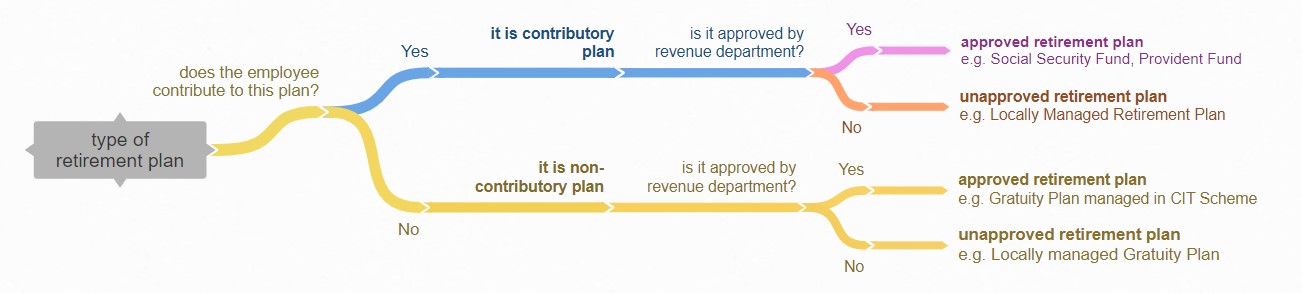

Types of Retirement Plan: On the basis of Contribution

Contributory Plan: In a contributory plan, the employee pays into the plan from their income.

It is not necessary that the employer contributes into the plan. Any plan where the employee contributes from their income is a contributory plan irrespective of whether or not the employer contributes.

Example: Social Security Fund (20%+11%), Provident Fund (10%+10%)

Non Contributory Plan: In a non contributory plan, the only the employer pays into the plan.

In a non contributory plan only the employer contributes. The employee does not.

Example: Gratuity (8.33%+0%)

Contributory Plan

In a contributory plan, the employee pays into the plan from their income. When the employee pays into a plan from their income to be later received after certain time, essentially in general understanding, it becomes a form of investment. This contribution of the employee into the plan creates an interest of the employee in the plan. In this principle, if employer also contributes into the plan, then it becomes an addition into his interest in the plan, so it becomes his taxable income. The employer’s contribution into this employee’s investment is basically the exact equivalent to cash contribution. This is a reason for why the employer’s contribution into a contributory plan is stubbed as a income head in the payslip of the employee, despite the fact that investment and employment income of employee is recognized in cash basis. This is the reason why employer’s contribution to Provident Fund is treated as income of the employee at the time of contribution while at the same time Gratuity contribution of the employer is not. Although the interest of the beneficiary in contributory plan is an investment it has been specifically excluded from the definition of the non business chargeable assets as there is separate tax mechanism to it.

Approved Contributory Plan

1. Taxation of Fund:

The gains accrued by the fund will not be subjected to income taxation. [Section 64(2) of Income Tax Act, 2058]

2. Taxation of Beneficiary at the point of contribution:

The employer’s contribution into the fund will be subjected to income tax by including it in employment income stub of the employee. [Section 8(2)(Cha) of Income Tax Act, 2058]

3. Taxation of Beneficiary at the point of distribution:

The retirement payment gain at the time of disbursement will be taxed at 5%. [Section 88(1) Proviso (1) of the Income Tax Act, 2058]

Section 65(1) of the Income Tax Act, 2058 provides the method for determining the amount of gain from approved contributory plan. Retirement Payment Gain = Retirement Payment – MAX [500000, Retirement Payment×50%]

Unapproved Contributory Plan

1. Taxation of Fund:

The gains accrued by the fund will be subjected to income taxation. [No tax exemption provided to Unapproved Plan]

2. Taxation of Beneficiary at the point of contribution:

The employer’s contribution into the fund will be subjected to income tax by including it in employment income stub of the employee. [Section 8(2)(Cha) of the Income Tax Act, 2058]

3. Taxation of Beneficiary at the point of distribution:

The retirement payment gain at the time of disbursement will be taxed at 5% if paid by resident plan, else at 15% if paid by non resident plan. [Section 88(2)(Ga) of Income Tax Act, 2058]

Clarification provided in Section 65 of the Income Tax Act, 2058 provides the method of determining the amount of gain from the unapproved contributory plan. Retirement Payment Gain = Retirement Payment – Retirement Contribution

Non Contributory Plan

In non contributory plan, only the employer contributes. When the employee doesn’t contribute to the plan, essentially in general understanding, the employee has no interest in the plan (“interest of employee” not to be confused with “entitlement of employee”). So the contribution made by the employer are not stubbed as a income head in the payslip of the employee unless they are actually paid to the employee at the point of retirement or death.

Approved Non Contributory Plan

1. Taxation of Fund:

The gains accrued by the fund will not be subjected to income taxation. [Section 64(2) of Income Tax Act, 2058]

2. Taxation of Beneficiary at the point of contribution:

The employer’s contribution will not be subjected to taxation at the point of contribution. [Section 8 read with Section 23 of the Income Tax Act, 2058]

3. Taxation of Beneficiary at the point of distribution:

The retirement payment at the time of disbursement will be taxed at 15%. [Section 88(1) of the Income Tax Act, 2058]

Unapproved Non Contributory Plan

1. Taxation of Fund:

The gains accrued by the fund will be subjected to income taxation. [No tax exemption provided to Unapproved Plan]

2. Taxation of Beneficiary at the point of contribution:

The employer’s contribution will not be subjected to taxation at the point of contribution. [Section 7 read with Section 23 of the Income Tax Act, 2058]

3. Taxation of Beneficiary at the point of distribution:

The retirement payment at the time of disbursement will be taxed at 15%. [Section 88(1) of the Income Tax Act, 2058]

Changes brought by Finance Act, 2079 and Bedbahadur vs. Rastriya Banijya Bank

Bedbahadur vs. Rastriya Banijya Bank

The court’s decision on the Bedbahadur vs. Rastriya Banijya Bank is a bit shallow. It has failed to delve into and interpret the meaning of contributory and non contributory retirement plan. Basically, it has established that the retirement plan made in the approved retirement fund are subjected to 5% taxes, whether the plan in contributory or non-contributory. It is true in the case of the contributory but could not be further from the truth in the case of non-contributory fund. View more detailed discussion on this topic here in my separate blog: Bedbahadur vs. Rastriya Banijya Bank

Finance Act, 2079

Finance Act, 2079 has introduced an additional clarification regarding the definition of “contributory interest”. It provides:

स्पष्टीकरणः यस दफाको प्रयोजनको लागि “योगदानमा आधारित हित” भन्नाले दफा ६३ को उपदफा (३) बमोजिम तोकिएको सीमाभित्र रही गरिएको अवकाश योगदानसँग सम्बन्धित हितलाई सम्झनु पर्दछ ।

Explanation: For the purposes of this Section, “Contributory Interest” means the interest related to the retirement contribution made within the limits prescribed by sub-section (3) of section 63.

This has led to differing opinions among the tax practitioners:

One view, a rather regressive view: Due to the reason of this amendment the actual amount that will be considered as gain from retirement payment from retirement fund will be limited to the amount of the retirement contribution deductible for tax purposes, year on year basis.

Another view, a better view: Through this amendment, Income Tax Act has aimed to assimilate the decision in the case of Bedbahadur vs. Rasthiya Banijya Bank into the tax laws. The case of Bedbahadur vs. Rasthiya Banijya Bank had decided that the retirement contribution made in the approved retirement fund are subjected to 5% taxes, whether the plan is contributory or non-contributory. But this amendment has still not been able to provide the basis for the 5% taxes on the amount deposited in the approved non-contributory plan (e.g. RBB Gratuity Scheme in the aforementioned Decision).

It has however been able to clarify that the amount of the non-contributory scheme that is deposited in contributory scheme (e.g. depositing the 8.33% gratuity amount into CIT’s Investment Scheme, rather than Gratuity Scheme) is subjected to taxes just like the contribution made in approved retirement plan. But this clarification was not necessary to that effect because a gratuity contribution consciously deposited in the scheme like CIT’s Investment Scheme is already a contributory retirement scheme upon such contribution and will be subjected to taxes as such. So, in conclusion, this amendment in the form of explanation has actually been for nothing.