Nepal stands at an economic crossroads. Ambitious national plans, from energy roadmaps to infrastructure masterpieces, outline a future of prosperity and connectivity. Yet, a persistent challenge threatens to stall this progress: the critical funding gap faced by the State-Owned Enterprises (SOEs) tasked with turning these plans into reality.

These entities, often in sectors like energy, transport, and water, require massive, long-term capital – running into billions of dollars – for transformative projects. However, their financial standing often makes direct commercial borrowing prohibitively expensive, creating a frustrating Catch-22: the nation needs investment to grow, but the vehicles for that investment struggle to access affordable finance.

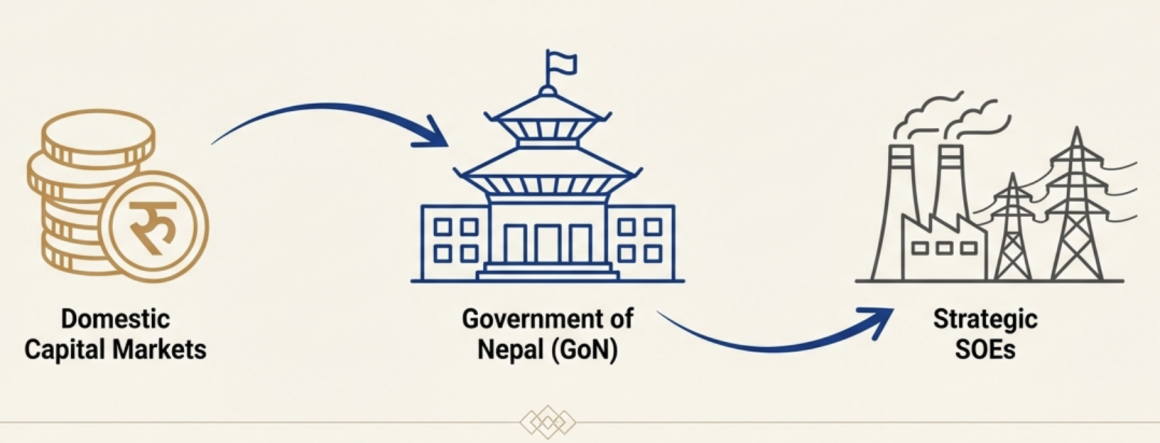

The solution to this impasse may lie not in searching for external saviors, but in strategically leveraging an underutilized domestic strength: the borrowing power of the Government of Nepal itself.

The Power of the Sovereign Balance Sheet

The Government of Nepal (GoN) possesses a unique financial advantage: the ability to borrow at the lowest interest rates in the country. This isn’t a theoretical power; it’s a practiced reality. As of the last fiscal year, the GoN’s domestic debt stock stood at a substantial NPR 1,268.22 billion (approximately USD 9.5 billion), raised through instruments like Development Bonds and Treasury Bills. The market for these securities is deep and liquid, supported by banks, pension funds, and insurance companies.

The yields on these government securities are significantly lower – often by several hundred basis points – than the rates available to even the most robust SOEs. This discrepancy creates a powerful opportunity for what is known as sovereign relending or sovereign intermediation.

What is Sovereign Relending?

In essence, sovereign relending is a process where the government acts as a financially efficient intermediary:

- The GoN raises capital from the domestic market by issuing its own bonds, benefiting from its low sovereign risk premium.

- A portion of these funds is then strategically on-lent to specific SOEs for pre-approved, high-priority national infrastructure projects.

- The SOE receives financing at a rate that is higher than the government’s cost of funds but drastically lower than what it could secure on its own.

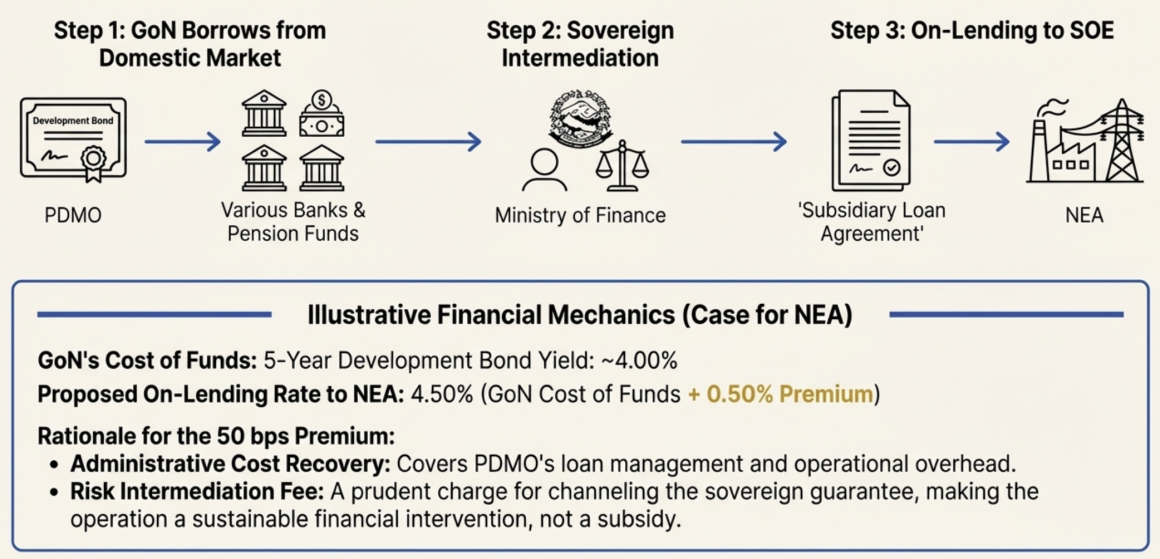

This is not a radical new idea. In fact, it’s a standard, proven practice already used by the GoN for foreign loans. When multilateral agencies like the World Bank lend to Nepal for a project implemented by an SOE, the Public Debt Management Office (PDMO) executes a formal “Subsidiary Loan Agreement” with that SOE. The proposal is simply to apply this identical, low-risk model to the domestic capital market.

Let's illustrate with a hypothetical example: GoN's Cost of Funds: The government issues a 5-year bond at a yield of 4.0%. Relending Rate to an SOE: The GoN relends the funds to a power sector SOE at 4.5%. The 0.50% Premium: This modest premium compensates the government for administrative costs and acts as a fee for the tacit sovereign backing provided. It transforms the operation from a subsidy into a sustainable financial intervention.

Illustration

This is not a radical new idea. In fact, it’s a standard, proven practice already used by the GoN for foreign loans. When multilateral agencies like the World Bank lend to Nepal for a project implemented by an SOE, the Public Debt Management Office (PDMO) executes a formal “Subsidiary Loan Agreement” with that SOE. The proposal is simply to apply this identical, low-risk model to the domestic capital market.

A Proposal Grounded in Law, Not Just Theory

Critically, this mechanism isn’t a theoretical concept waiting for new legislation. The legal architecture is already fully in place. The Public Debt Management Act, 2079, and its Regulations (2080) provide the explicit authority. Public Debt Management Rules, Rule 40 unequivocally states: “Nepal Government can make loan investments in institutions… fully or partially owned by the Government of Nepal.”

This power is derived from the highest authority: the Constitution of Nepal (Article 59(6)), which grants the GoN the power to borrow loans, a function regulated by a Federal Law (a Money Bill). This proposal is therefore an innovation in application, using existing tools in a more impactful way to solve a pressing national problem.

- Constitutional Mandate: The Constitution under Article 59(6) grants the GoN the unambiguous power to “obtain foreign assistance and borrow loans.” Article 115(2) stipulates this must be done as per Federal law, which is the PDMA – itself a Money Bill as defined by Article 110(3)(c), having passed the highest level of parliamentary authority.

- Explicit Statutory Power: The Public Debt Management Act, 2079, and the PDMR, 2080, provide the complete operational framework. PDMR, Rule 40 is unequivocal: “Nepal Government can make loan investments in institutions… fully or partially owned by the Government of Nepal.” This is the core legal basis for our proposal.

- Established Precedent in Foreign Loan Relending: This is not a novel concept. The GoN already routinely engages in this exact practice for foreign borrowings. When a multilateral agency lends to the GoN for a project implemented by an SOE, the PDMO executes a Subsidiary Loan Agreement with that SOE. We are simply proposing to apply this identical, proven model to domestically raised funds.

- Seamless Process Integration: The entire issuance process is already governed by a detailed procedure, and the resultant loan investment would be managed under the PDMO’s sophisticated Debt Operations and Management System (DOMS), ensuring full transparency and accountability.

A preliminary test for this could be the formal establishment of a “Framework for On-Lending to Strategic SOEs” under the existing mandate of the PDMO. The process is straightforward and integrates seamlessly into current operations:

- Domestic Borrowing by GoN: The Public Debt Management Office (PDMO), as part of its annual borrowing program outlined in the Internal Debt (Issuance and Management) Procedures 2081, raises funds by issuing instruments like Development Bonds to meet budget shortfalls.

- Earmarking for Strategic Investment: A discrete portion of the raised capital is explicitly allocated for “Loan Investment in Public Enterprises”, a power explicitly granted to the GoN by PDMR, Rule 40(1) & (2).

- Execution via Subsidiary Loan Agreement: The GoN, through the PDMO, enters into a Subsidiary Loan Agreement with the recipient SOE (e.g., NEA), as illustrated under PDMR, Rule 39(2). This is a standard practice already used for relending foreign loans.

- Setting Transparent Terms: The relending terms (interest rate, tenor) are set by the Ministry of Finance, considering the factors mandated by PDMR, Rule 40(3), such as the GoN’s cost of funds and the project’s rate of return.

A Win-Win-Win for Nepal

The benefits of this framework are multi-fold, creating a virtuous cycle of investment and development.

A) For Domestic Investors (Banks, Pension Funds and Insurance Sectors):

Investing in GoN securities under this framework offers arguably the most attractive and secure investment opportunity in Nepal, as codified in NRB directives:

Zero Risk Weight (Capital Efficiency): Investments in GoN securities carry a 0% risk weight. This means financial institutions do not need to hold any regulatory capital against these assets. Practical Benefit: This frees up significant capital for BFIs, allowing them to deploy more funds into other loans and investments, thereby stimulating the economy while holding the safest possible asset.

Exemption from Single Obligor Limit (Enhanced Lending Capacity): Loans and advances collateralized by GoN securities are exempt from single borrower exposure limits. Practical Benefit: This allows BFIs to concentrate their lending efficiently to large-scale projects without hitting regulatory ceilings, supporting major national initiatives.

High Liquidity & SLR Compliance (Portfolio Flexibility): Government bonds are premier liquid assets used to meet Statutory Liquidity Ratio (SLR) requirements and are actively traded on the secondary market through NEPSE. Practical Benefit: Investors can easily buy and sell these securities, ensuring their investments are never locked in and can be quickly converted to cash if needed.

Implicit Sovereign Guarantee (Ultimate Security): As per Constitution Article 118(g), debts of the GoN are a permanent charge on the Federal Consolidated Fund. Practical Benefit: This provides an unparalleled level of safety, making these instruments the benchmark for security in the Nepali market, which will ensure strong demand and competitive pricing for government issuances.

B) For State-Owned Enterprises (e.g. NEA):

Access to Large-Scale, Affordable Capital: Unlocks the funding required to execute the USD 9 billion Energy Roadmap at an interest cost likely 300-500 basis points lower than commercial alternatives.

Improved Financial Sustainability: Lower debt servicing costs directly improve SOE’s balance sheet, enhancing its long-term viability and reducing its fiscal drain on the state.

Execution Certainty for National Goals: Provides predictable, sovereign-backed funding, enabling SOEs to plan and execute multi-year infrastructure projects with confidence.

C) For the Government of Nepal:

Accelerated Infrastructure Development: Directly addresses the biggest bottleneck to economic growth without immediate fiscal expenditure.

Revenue from Intermediation: The relending premium provides a net return on deployed capital, contributing to the national treasury.

Proactive Fiscal Risk Management: This framework brings the existing, implicit guarantee for critical SOE debt on-book in a transparent manner. It allows for formal monitoring of the SOE’s repayment performance, making fiscal risk more visible and manageable compared to the current system of ad-hoc bailouts.

The Path Forward

The opportunity is clear. With a domestic debt market exceeding NPR 1.26 trillion (USD 9.5 billion) (as at FY 2023/24) and SOEs needing investment on a similar scale, the conditions are ripe for sovereign relending. The implementation can be pragmatic, starting with a pilot project – for instance, funding a specific transmission line – to demonstrate the model’s efficacy before scaling it to other sectors.

The message is compelling: Nepal does not need to reinvent the wheel to finance its future. By strategically leveraging its own sovereign strength and existing legal frameworks, the government can unlock domestic capital, empower its public enterprises, and build the infrastructure that will propel the nation toward its ambitious goals. It’s a call for the Government of Nepal to become the central architect of its financial destiny, channeling national savings into national prosperity.