I. The Problem and Why It Matters

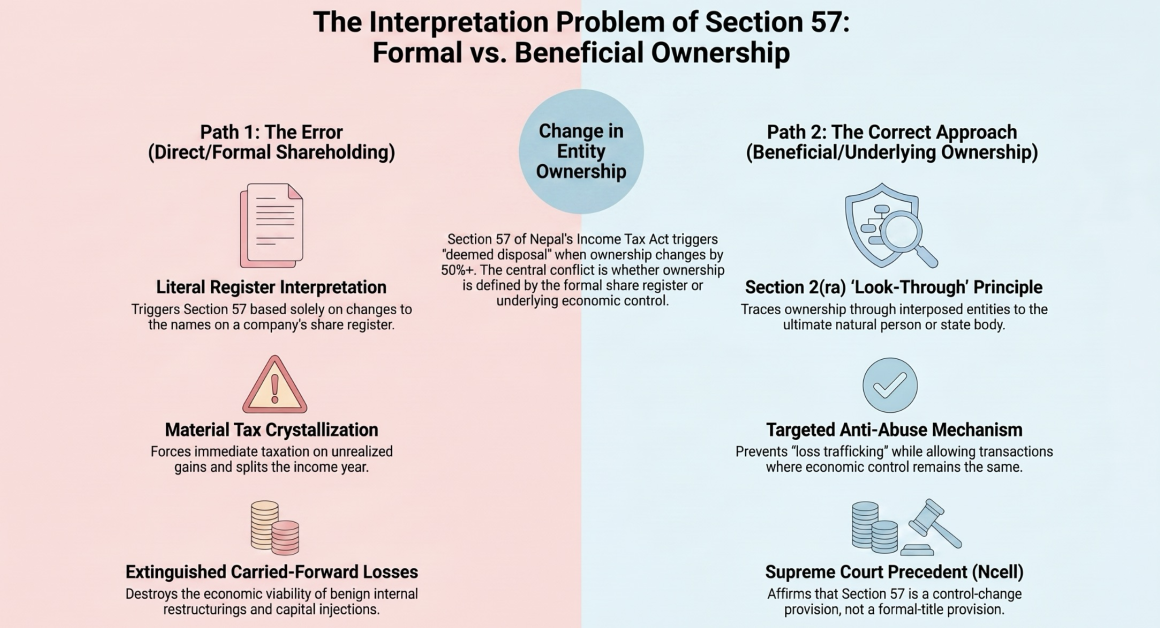

Nepal’s Income Tax Act, 2058 (“ITA”) contains, in Section 57, one of its most consequential and least examined provisions. Triggered when the “ownership” of an entity changes by fifty percent or more as compared to its ownership in the preceding three years, Section 57 deems the entity to have disposed of all its assets and liabilities at market value – extinguishing carried-forward losses, splitting the income year, and potentially producing a material tax crystallisation on unrealised gains. The consequences are severe enough that the provision, if applied incorrectly, can destroy the economic viability of transactions that are entirely benign from the perspective of the mischief the law was designed to prevent.

The interpretive question at the heart of Section 57 – one that the Inland Revenue Department (“IRD”), the tax advisory community and the courts have not yet definitively resolved in the taxpayer’s favour – is deceptively simple: when the provision speaks of a change in “ownership,” does it refer to direct, formal shareholding on the register of a company, or to the underlying, beneficial ownership that the ITA itself defines in Section 2(ra)? The answer to that question determines whether Section 57 operates as a targeted anti-abuse rule, striking only at transactions where economic control genuinely moves to new hands, or as an indiscriminate formal test, capable of triggering a deemed disposal even where the ultimate economic owner is identical before and after the transaction.

This article argues that the latter construction is both legally untenable and productive of results so absurd that they could not have been intended by any reasonable legislature. Drawing on the text of the ITA, the model law from which it derives, comparative jurisdictions that adopted the same drafting template, the Supreme Court of Nepal’s landmark decisions in the Ncell litigation, and three illustrative numerical examples, the article establishes that Section 57 can only be coherently applied by reference to underlying ownership as defined in Section 2(ra) – and that a direct change in formal shareholding, unaccompanied by any change in underlying ownership, does not and cannot trigger the provision.

The point is not merely academic. As Nepal’s infrastructure and institutional capital markets deepen, group restructurings, inter-agency capital injections and intra-state capitalisation transactions will become increasingly common. If Section 57 is permitted to operate as a blunt formal test, each such transaction will carry a contingent tax liability that rational investors will price into the cost of capital, with direct consequences for the pace and cost of project development. Getting the interpretation right is therefore a matter of policy consequence, not just technical tax law.

II. The Statutory Architecture: What Section 57 Says and What It Is For

2.1 The Charging Provision

Section 57(1) of the ITA provides, in its official English translation:

“If the ownership of any entity changes by fifty per cent or more as compared to its ownership until before the last three years, the entity shall be deemed to have disposed of the property under its ownership or the liability borne by it.”

The consequences of a trigger are set out in the surrounding provisions. The entity is treated as having disposed of all its assets and liabilities at fair market value (Section 41), its accumulated losses are extinguished (Section 20), and the income year is split at the date of the ownership change (Section 57(3)). In practical terms, a triggered Section 57 can convert years of accumulated tax losses – the normal financial profile of a capital-intensive project in its construction and early-operation phase – into a deemed taxable gain crystallised at precisely the moment when the project is least able to absorb it.

Section 57(1ka) prescribes the counting rule: the change in ownership is measured cumulatively over the rolling three-year window, counting shareholders with interests of one percent or more (together with their associates). The test is thus quantitative and aggregate, not transactional.

2.2 The Definition That Governs the Test

Critically, the ITA does not leave “ownership” undefined for the purposes of Section 57. Section 2(ra) provides an express definition of “underlying ownership”:

“An ownership created on the basis of an interest held in the entity directly or indirectly through one or more interposed entities by an individual or by an entity in which no individual has an interest.”

This is a look-through definition. It requires the analyst to trace through interposed entities until reaching either a natural person or an entity in which no individual holds an interest – paradigmatically, a State body or a public statutory institution. The definition is not confined to Section 2(ra) as a standalone concept; it is the definitional substrate that gives meaning to the word “ownership” wherever it appears in the Act in a context where the legislature intended beneficial, not formal, ownership to govern.

2.3 The Anti-Abuse Purpose

Section 57 is not a primary charging provision of the kind that taxes income as it accrues. It is an anti-abuse rule, and its purpose is specific and well-documented. The provision is designed to prevent “loss trafficking” – the acquisition of a loss-making entity by a new, economically unrelated owner for the primary purpose of utilising the accumulated tax attributes (principally carried-forward losses) that belong to a business the acquirer did not build and did not bear the economic risk of developing. In the absence of Section 57, a profitable group could purchase a loss-laden shell at a discount, merge its profitable operations into it, and shelter future income behind losses generated by an entirely different enterprise under entirely different ownership. Section 57 forecloses that strategy by treating the ownership change as a deemed disposal, resetting the tax base and extinguishing the inherited attributes.

The hallmarks of the mischief Section 57 targets are therefore precise: a new economic owner, acquiring a controlling interest from a departing economic owner, for a consideration that reflects the value of the target’s tax attributes as well as its operating assets. Where those hallmarks are absent – where the economic owner is the same before and after, and where the transaction produces no transfer of value to a person previously unconnected with the entity – the provision simply has no work to do.

III. The Look-Through Principle: Section 2(ra) and the Supreme Court’s Construction

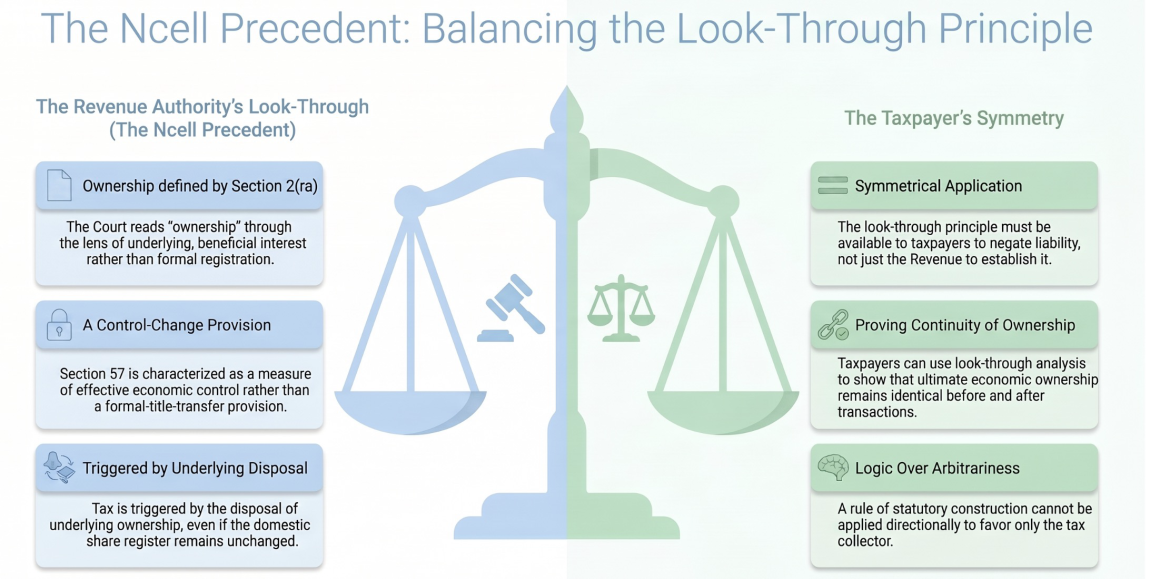

3.1 The Ncell Decisions: The Court Reads “Ownership” Substantively

The Supreme Court of Nepal’s decisions in the Ncell litigation – Dwarikanath Dhungel v. Large Taxpayer’s Office (decided 6 February 2019, Brihat Purna Ijalas, निर्णय नं. १०१६३) – represent the authoritative judicial construction of Section 57 and constitute the foundation on which any analysis of the provision must be built.

The facts of that case require brief description because they are the precise analytical mirror of the question addressed in this article. Ncell Private Limited was Nepal’s leading telecommunications operator. Its direct shareholder, Reynolds Holdings Limited (a company registered in Saint Kitts and Nevis), remained nominally unchanged throughout the disputed period – Reynolds continued to hold 80% of Ncell on the company’s register before and after the transaction. What changed was the ultimate, underlying owner of Reynolds: TeliaSonera AB of Sweden sold its controlling interest in Reynolds to Axiata Berhad of Malaysia, so that the beneficial controller of Ncell shifted from one foreign corporate group to another, entirely through the medium of offshore interposed entities, without any alteration to the Nepalese share register.

The petitioner took the position that Section 57 was triggered. Ncell and Reynolds argued that the domestic share register was unchanged and that the offshore transaction was beyond the reach of Nepalese tax law. The Supreme Court, sitting as a full bench of five justices, held unambiguously in favour of the petitioner. Its reasoning on the interpretive question is what matters for present purposes.

The Court’s analysis proceeded in three logically distinct steps, each of which is directly material to the argument developed in this article.

First, the Court established that the word “ownership” in Section 57(1) must be read through the lens of Section 2(ra). At paragraph 21 of the decision, the Court expressly grounded its finding not in the formal shareholding on the register but in the underlying ownership as defined in the Act:

“ऐनको दफा २(र) मा ‘निहित स्वामित्व’ को परिभाषा गरिएको छ… एनसेलमा रहेको टेलिया सोनेरा स्वीडेनको ८० प्रतिशत ‘निहित स्वामित्व’ को निसर्ग भएको”

The Court did not find that “80% of direct shareholding changed.” It found that “80% of the underlying ownership of TeliaSonera Sweden in Ncell was disposed of.” The trigger, on the Court’s own analysis, was a change in underlying ownership – not a change in the name on the share register.

Second, the Court characterised Section 57 itself as a control-change provision rather than a formal-title-transfer provision. At paragraph 22, the Court stated in terms:

“दफा ५७ ले नियन्त्रण परिवर्तनबारे व्यवस्था गरेको”

Translated: “Section 57 provides for change in control.” The statutory test, in the Court’s understanding, is not whether the name of a registered shareholder has changed but whether effective economic control has passed from one set of ultimate owners to another.

Third, at paragraph 23, the Court identified the triggering event with forensic precision:

“विवादित जुन कारोबार छ यो मध्यस्थ निकायमार्फत एनसेलमा निहित स्वामित्वको निसर्ग गरेको अवस्था हो”

Translated: “The disputed transaction is a situation of disposal of underlying ownership in Ncell through intermediary entities.” The trigger was, in the Court’s words, the disposal of underlying ownership. Not the disposal of registered shares. Not the change of a name on a register. The disposal of underlying ownership.

The analytical significance of this three-part construction cannot be overstated. By grounding the Section 57 trigger exclusively in underlying ownership, the Court simultaneously and necessarily established that where underlying ownership does not change, the triggering condition is not satisfied. The Court did not say “Section 57 fires whenever the share register changes.” The Court said “Section 57 fires when underlying ownership changes.” These are logically opposite propositions, and only the latter is consistent with the decision.

3.2 The Principle of Symmetry: The Look-Through Cannot Be One-Directional

The Ncell decisions established the look-through principle in the context of a transaction where the IRD sought to pierce through an unchanged direct shareholder to find a changed ultimate owner. The question that follows – and the question on which no direct Supreme Court authority exists – is whether the same look-through principle operates in the taxpayer’s favour, to recognise continuity of ultimate ownership where the direct shareholders change but the underlying owner does not.

The answer must be yes, as a matter of both logic and legal principle. A rule of statutory construction cannot be applied directionally – available to the revenue authority to establish a tax liability but unavailable to the taxpayer to negate one. The look-through is not a weapon of the IRD; it is the correct method of applying Section 57 to any transaction. If the correct method, when applied to a transaction where the register changes but the ultimate owner does not, reveals continuity rather than change, the provision is not triggered. To hold otherwise would be to assert that the word “ownership” in Section 57(1) means “underlying ownership” when it favours the revenue and “registered shareholding” when it favours the taxpayer. That is not statutory interpretation; it is arbitrariness.

The Court itself, at paragraph 16, articulated the look-through as a general analytical tool for understanding economic reality:

“माध्यम वा मध्यस्थ कम्पनीहरू आफैँ कुनै कार्य गर्दैनन्”

Translated: “intermediary companies do not themselves carry out any activity.” The function of the look-through is to identify who actually controls and who actually benefits – before and after. Where the answer is the same person, both before and after, the section is inapplicable on its own terms as construed by the Supreme Court.

IV. Three Illustrative Examples: The Absurdity of the Literal Reading

The theoretical argument above is reinforced, and the stakes made concrete, by three numerical examples that demonstrate the results the literal construction produces. In each case, a mechanical application of the direct-shareholding test yields a Section 57 trigger; in each case, the economic reality is one of perfect continuity of beneficial ownership; and in each case the result is not the prevention of loss trafficking but the taxation of a transaction that carries none of the mischief the provision exists to address.

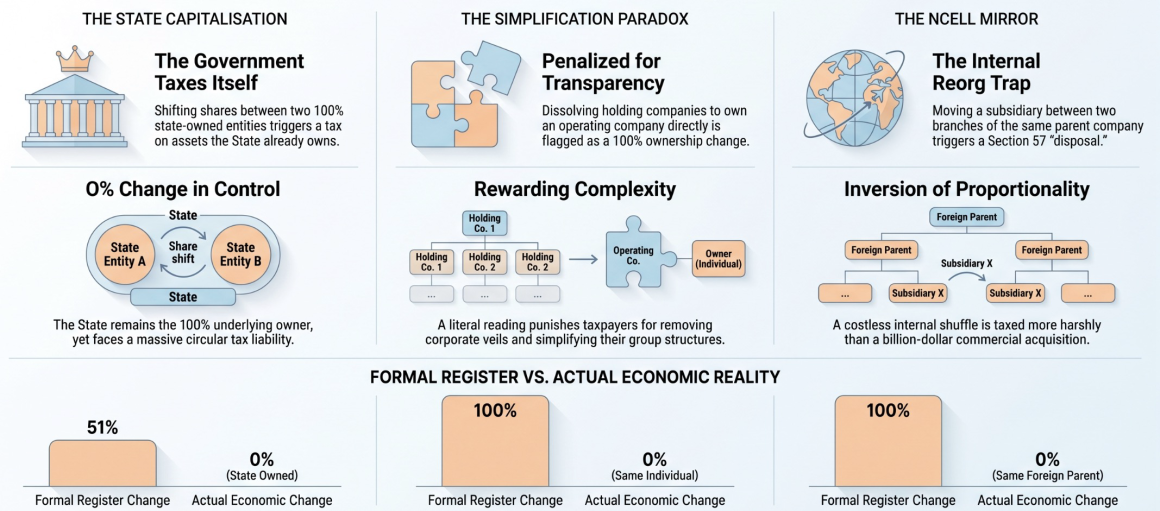

Example 1: The State Capitalising Its Own Project

Facts. ProjectCo is a public limited company incorporated to develop an infrastructure project. At its formation, it is wholly owned (100%) by State Entity A, which is itself 100% owned by the Government of Nepal. The Government, recognising that the project requires additional equity, directs State Entity B – also 100% owned by the Government – to subscribe fresh shares in ProjectCo amounting to 51% of the enlarged capital. State Entity A’s existing shares are not transferred or reduced; its absolute holding remains constant. After the transaction, the direct shareholding is as follows:

| Shareholder | Before | After |

| State Entity A (100% GoN) | 100% | 49% |

| State Entity B (100% GoN) | – | 51% |

| Total | 100% | 100% |

Literal construction. State Entity B was not a direct shareholder three years before the transaction. It now holds 51% directly. On a formal, register-based reading, 51% of ProjectCo’s ownership is held by a party that was not an owner during the preceding three years. The 50% threshold is crossed. Section 57 is triggered. ProjectCo is deemed to have disposed of all its assets – including its generation licence, civil works and project infrastructure – at market value. Its accumulated losses are extinguished.

Underlying ownership analysis. Applying Section 2(ra), the underlying owner of State Entity A is the Government of Nepal, at 100%. The underlying owner of State Entity B is the Government of Nepal, at 100%. ProjectCo’s underlying ownership, before the transaction, is 100% × 100% (GoN through Entity A) = 100% Government. After the transaction, it is (49% × 100%) + (51% × 100%) = 100% Government. The change in underlying ownership is mathematically zero. The Government’s interest does not decrease, does not transfer, and does not pass to any new economic owner. The Government is deemed, on the literal construction, to have disposed of its own assets to itself.

The absurdity. The deemed disposal produces a taxable gain on assets that have not moved. The Government, as the entity that will collect the tax and simultaneously bear the economic cost of the deemed disposal through its ownership of ProjectCo, is both taxpayer and tax collector in respect of the same transaction. The accumulated losses of a project that the Government financed, built and continues to own are extinguished – eliminating future tax deductions that would otherwise reduce the Government’s future tax receipts from the same project. No new economic owner has acquired anything. No loss has been trafficked. The entire fiscal consequence is circular: the Government taxes itself on a notional gain arising from a transaction with itself, in respect of a project it controlled entirely before and controls entirely after. This is precisely the kind of “unintended consequence” that purposive construction is designed to prevent.

Example 2: The Simplification Paradox

Facts. A private entrepreneur, Person X, owns OpCo (an operating company) through two intermediate holding companies: HoldCo A (holding 60% of OpCo) and HoldCo B (holding 40% of OpCo), both of which are 100% owned by Person X. Person X decides to simplify the group structure by dissolving the two holding companies and holding OpCo directly. After the dissolution, Person X holds 100% of OpCo directly.

| Ownership of OpCo | Before | After |

| HoldCo A (100% Person X) | 60% | – |

| HoldCo B (100% Person X) | 40% | – |

| Person X (directly) | – | 100% |

| Ultimate owner | Person X 100% | Person X 100% |

Literal construction. Before the simplification, Person X held no direct shares in OpCo. After the simplification, Person X holds 100% directly. On the register, the entire direct shareholding has changed from two companies to one individual. 100% of OpCo is now held by a party – Person X as a direct holder – who did not appear on the register three years ago. Section 57 is triggered. OpCo is deemed to have disposed of all its assets. Its accumulated losses are extinguished.

Underlying ownership analysis. Person X was the underlying owner of 100% of OpCo both before and after the simplification, through HoldCo A and HoldCo B. The simplification added no new economic owner, removed no existing one, and transferred no value to any third party. It merely collapsed two layers of corporate structure that were interposed between Person X and OpCo. The underlying owner before was Person X (100%), and the underlying owner after is Person X (100%). Change in underlying ownership: zero.

The absurdity and its additional dimension. Here the literal construction does not merely produce a result unconnected to the mischief of the provision – it produces the precise inverse of that mischief. The taxpayer has made themselves more transparent, not less. Instead of holding OpCo through two interposed entities – exactly the kind of layered structure that the look-through principle in Section 2(ra) is designed to penetrate – the taxpayer has eliminated the layers entirely and stands in direct relationship to the company they have always economically owned. The literal construction would punish the taxpayer for acting with structural transparency: the moment they remove the very corporate veil that the Act’s anti-avoidance provisions are designed to lift, Section 57 deems them to have disposed of their own assets. A rule of law that penalises simplification and rewards complexity is, by any measure of purposive construction, one that has been misapplied.

Example 3: The Ncell Mirror – The Cross-Border Symmetry Trap

Facts. Foreign Parent Corp (incorporated in Country X) owns 100% of Foreign MidCo A, which in turn holds 100% of Nepal OpCo, a resident entity carrying on business in Nepal. Foreign Parent Corp internally reorganises its holding structure, transferring Nepal OpCo’s shares from Foreign MidCo A to a newly created Foreign MidCo B, also 100% owned by Foreign Parent Corp. The reorganisation is effected at book value; no consideration passes between unrelated parties. The direct shareholder of Nepal OpCo changes from Foreign MidCo A to Foreign MidCo B – a 100% change in the direct register.

| Ownership of Nepal OpCo | Before | After |

| Foreign MidCo A (100% Foreign Parent) | 100% | – |

| Foreign MidCo B (100% Foreign Parent) | – | 100% |

| Ultimate owner | Foreign Parent 100% | Foreign Parent 100% |

Literal construction. Foreign MidCo B did not hold any interest in Nepal OpCo during the preceding three years. It now holds 100%. Section 57 is triggered on a formal reading.

The Ncell symmetry trap. The Ncell decisions held that a look-through was required – that the unchanged direct shareholder (Reynolds) should be penetrated to identify the changed ultimate owner (from TeliaSonera to Axiata). The IRD used that look-through to trigger Section 57. Now apply the identical look-through to the present example. Penetrate Foreign MidCo A. Penetrate Foreign MidCo B. In each case, the look-through reaches Foreign Parent Corp – the same entity, holding 100%, both before and after. By the Supreme Court’s own reasoning, the look-through reveals no change in underlying ownership. Section 57 cannot be triggered.

The IRD’s only available counter-argument – and why it fails. The only way the IRD could argue for a trigger in this example while maintaining consistency with Ncell is to assert that the look-through principle is directional: that it operates to identify changes (as in Ncell) but not to confirm continuity. That assertion amounts to saying that the word “ownership” in Section 57(1) bears two different meanings depending on which party benefits from the finding. That is not a legal position – it is a confession that the section is being applied arbitrarily. The Supreme Court established the look-through as the correct method of applying Section 57 to any transaction involving interposed entities. The method, applied correctly, produces the correct result in both directions. In Ncell, it produced a trigger because underlying ownership changed. In this example, applied by the same method, it produces no trigger because underlying ownership did not change.

The proportionality inversion. There is a further dimension that compounds the absurdity. The Ncell transaction involved the sale of a controlling interest in Nepal’s largest telecommunications operator for approximately USD 1.36 billion – a genuine commercial transaction between unrelated parties, generating a very large realised gain, effected specifically through offshore interposed entities. This example involves a costless internal reorganisation, no consideration, no new economic owner, and no tax-base migration. The literal construction would apply Section 57 more harshly to a transaction of nil economic significance than it did to a multi-billion dollar commercial acquisition. That inversion of proportionality is itself evidence that the literal construction is wrong.

V. Legislative Architecture and Comparative Authority

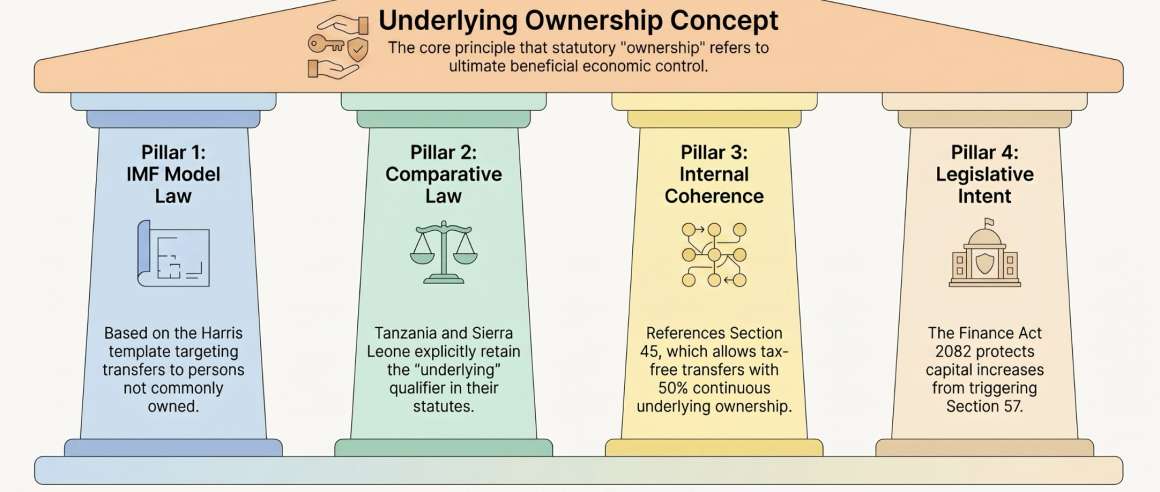

5.1 The Model Law: The Harris/IMF Template

Nepal’s Income Tax Act, 2058 is modelled closely on the IMF’s Commonwealth of Symmetrica Income Tax Act, a model statute developed under the direction of Professor Peter Harris. The equivalent of Section 57 in the model law is Section 171, which provides in terms:

“Where there is a change of 50 percent or more in the underlying ownership of an entity as compared with that ownership three years previously, the entity is treated as realising any assets owned by it and any liabilities owed by it immediately before the change.”

The model provision uses the phrase “underlying ownership” explicitly, not the unqualified word “ownership.” The accompanying Commentary to the model, at paragraph 281, states the purpose with precision:

“Section 171 is of an opposite nature in seeking to prevent an indirect transfer of tax attributes of an entity to persons who do not own or are not commonly owned with the entity… It treats an entity as realising all its assets and liabilities where there is a change of 50 percent or more in the underlying ownership of the entity within a three year period.”

Two conclusions follow directly from the model law and its Commentary. First, the intended trigger is a change in underlying ownership – the Commentary says so in terms. Second, the target is a transfer to “persons who do not own or are not commonly owned with the entity.” Where the persons who own the entity before and after are the same, or are commonly owned by the same ultimate principal, the mischief the provision was designed to prevent is absent by definition. A provision cannot be triggered by the very condition that its own Commentary identifies as outside its scope.

The omission of the word “underlying” from Nepal’s Section 57(1) in the official Nepali text is, on this analysis, a translation artefact rather than a deliberate policy choice to widen the trigger to formal ownership changes. The drafting history, the model law, and the Commentary all point consistently to underlying ownership as the intended measure.

5.2 Comparative Jurisdictions: Tanzania and Sierra Leone

Two jurisdictions that adopted the same Harris/IMF model retained the express “underlying ownership” language, confirming the drafter’s intent and providing a useful comparative baseline.

Tanzania’s Income Tax Act, Cap. 332 (R.E. 2023) provides at Section 56(1):

“Where the underlying ownership of an entity changes by more than fifty percent as compared with that ownership at any time during the previous three years, the entity shall be treated as realising any assets owned and any liabilities owed by it immediately before the change.”

Sierra Leone’s Income Tax Act 2000 provides at Section 88:

“Where there has been a change of fifty percent or more in the underlying ownership or control of a company, no deduction shall be allowed… for losses suffered before the change unless the company (a) continues to conduct the same business; and (b) does not engage in a new business or investment except with the approval of the Commissioner, for a period of three years after the change.”

Both jurisdictions use “underlying ownership.” Both pair the rule with a continuity-of-business relief that confirms the anti-loss-trafficking purpose. The common drafting template, across three jurisdictions sharing the same model statute, demonstrates that the word “underlying” is integral to the provision’s design, not incidental to it. Nepal’s translation rendered the operative noun without its qualifier; the comparative evidence restores it.

5.3 Internal Coherence: Section 45 of the ITA

A further textual argument for the underlying-ownership construction derives from the internal architecture of the ITA itself. Section 45 permits transfers of assets between associated persons at tax base – that is, without triggering a deemed disposal at market value – where there is continuity of underlying ownership of at least 50%. The 50% threshold in Section 45 is the deliberate mirror of the 50% threshold in Section 57. The Act embodies, in Section 45, the principle that intra-group movements within a common underlying ownership structure are not realisation events. Reading Section 57 to tax exactly such a movement – a transfer within a group sharing common underlying ownership – would set the two provisions in direct conflict. Section 45 would permit the transfer without tax; Section 57 would deem a disposal. A construction that generates internal incoherence within the same statute is presumptively incorrect.

5.4 The Finance Act, 2082 Proviso: Legislative Confirmation of Purpose

With effect from 1 Shrawan 2082, the Nepal legislature enacted a new proviso to Section 57(1), subsequently continued by the Finance Bill 2083, that disapplies the section in certain circumstances where new shareholders are added to increase capital without displacing existing shareholders’ holdings. By its express terms, the capital-increase limb of the proviso is confined to start-up companies, venture capital funds and private equity funds.

The significance of this proviso for the present analysis is not as a ground of direct relief for all entities – it is vehicle-specific – but as legislative confirmation of purpose. The legislature itself identified the exact fact pattern of “new shareholders added to raise capital while existing owners’ holdings remain intact” and characterised it as falling outside the mischief of Section 57. That characterisation holds as a statement of legislative intent for all transactions of the same economic character. The proviso is, in this sense, a legislative gloss on the section: it confirms what the section was not designed to reach, even where the specific procedural relief is confined to particular vehicle types. It would be a striking incongruity if the law, having just exempted private capital vehicles whose new investors may include genuine third parties, were read to tax transactions where all participating entities share a common economic owner throughout – a result more benign still than the very case the legislature chose to exempt.

VI. The Opposing View and Its Rebuttal

A complete analysis requires candid engagement with the arguments the IRD could advance in favour of the literal construction, and with the weight those arguments carry.

The literal text argument. The IRD’s strongest argument is textual: Section 57(1) as enacted in Nepali says “स्वामित्व परिवर्तन” – “ownership change” – without the qualifier “underlying.” Where a new direct shareholder acquires more than 50% of a company, the 50% threshold is crossed on its face.

The rebuttal is threefold. First, the Supreme Court in Ncell did not apply the literal text. The Court applied the underlying-ownership construction, grounding the trigger in Section 2(ra) and in the concept of निहित स्वामित्व throughout its analysis. The Court had before it the same literal text; it chose to read it substantively. Second, the omission of “underlying” is shown by the model law and the comparative evidence to be a translation artefact. Third, a literal reading that produces the results illustrated in the three examples above – the Government taxing itself, the transparent taxpayer penalised for simplification, the costless reorganisation attracting harsher treatment than a billion-dollar acquisition – violates the settled principle of Nepalese statutory construction that an interpretation producing an absurd or manifestly unintended result should be rejected in favour of a purposive one.

The directness argument. A related IRD argument is that the change in direct shareholding is real and cannot be ignored: new names appear on the register; the previous majority holder is now a minority. This is factually true but legally irrelevant if the Court’s construction of Section 57 is followed. In Ncell, the name on the register (Reynolds) did not change at all – yet Section 57 was triggered because underlying ownership changed. The register is not the operative instrument. Economic reality is. Where economic reality, traced through Section 2(ra), reveals continuity, the register entry is legally insufficient to produce a trigger.

The Section 47Ka argument. Some may argue that the existence of Section 47Ka – which provides express restructuring relief for mergers and acquisitions in the banking and insurance sectors – implies by negative inference that other sectors are intended to be subject to Section 57 without relief. The short answer is that this argument mistakes the relationship between Section 47Ka and Section 57. Section 47Ka is procedural relief for a situation in which Section 57 applies – it ameliorates the consequences for certain restructurings that do fall within the provision’s scope. The argument developed in this article is anterior: Section 57 is not triggered at all where underlying ownership is continuous. A taxpayer who is not within Section 57’s scope requires no express carve-out; the provision simply does not apply to them by its own terms as the Supreme Court construed them.

VII. Synthesis: The Correct Construction and Its Policy Implications

The analysis above converges on a single conclusion: Section 57 of the ITA is a provision concerned with underlying ownership, not with the formal register of direct shareholders. This conclusion rests on six independent and mutually reinforcing grounds.

First, the Supreme Court in Ncell grounded the trigger of Section 57 exclusively in the concept of underlying ownership (निहित स्वामित्व) as defined in Section 2(ra). The Court’s own words at paragraphs 21, 22 and 23 of the decision make this clear beyond reasonable argument.

Second, the symmetry principle derived from Ncell requires that the same look-through which the IRD used to find a trigger in that case must also be available to confirm continuity where the underlying owner does not change. A unidirectional look-through is not a legal principle; it is an arbitrary exercise of power.

Third, the model law from which Section 57 derives, and the Commentary that explains it, use “underlying ownership” explicitly and define the provision’s target as transfers to persons “not commonly owned” with the entity. Transactions within a single economic group under common ultimate ownership are not, on the model law’s own terms, within the provision’s scope.

Fourth, two jurisdictions adopting the same model statute retained the word “underlying” in their equivalent provisions, confirming that Nepal’s translation omission was not deliberate.

Fifth, the internal coherence of the ITA, and specifically the relationship between Section 57 and Section 45, requires a construction under which intra-group movements sharing common underlying ownership do not constitute realisation events.

Sixth, the three illustrative examples demonstrate that the literal construction produces outcomes – the State taxing itself, the transparent taxpayer penalised for structural simplification, the costless reorganisation treated more harshly than a billion-dollar acquisition – that no reasonable legislature could have intended and that a purposive construction is obliged to avoid.

The policy implication is straightforward. Where a transaction produces no change in the underlying ownership of an entity – where the ultimate beneficial owners hold the same economic interest, directly or through interposed entities, both before and after – Section 57 should not apply, regardless of what the formal share register shows. The provision’s reach is defined by economic reality, not corporate form. That is what the Supreme Court held in Ncell; and the principle it there established for the purposes of finding a trigger applies with equal force, and in the opposite direction, to confirm that no trigger arises where underlying ownership is continuous.

VIII. Conclusion

The question of whether Section 57 applies to a direct change in formal shareholding unaccompanied by any change in underlying ownership is not a question to which the literal text of the ITA gives a self-evident answer. It is a question of statutory construction, and the tools of construction – the defined terms, the model law, the comparative evidence, the judicial authority, the internal architecture of the Act and the principles of purposive interpretation – all point in the same direction.

Section 57 is an anti-abuse provision of precise and limited purpose: to prevent the trafficking of accumulated tax attributes to new, unrelated economic owners. It is not a provision that taxes corporate form-changes within a single economic group, internal capitalisations by a common parent, or structural simplifications that leave the ultimate beneficial owner unchanged. Applied consistently with the Supreme Court’s construction of “ownership” as underlying ownership, Section 57 operates where it should – against genuine changes in economic control – and remains dormant where it should – within groups sharing a continuous underlying ownership.

The Ncell decisions gave Nepal a powerful and principled tool for taxing offshore indirect transfers of underlying ownership. The same decisions, read with the symmetry and intellectual honesty that legal principle requires, also give taxpayers a principled defence where the underlying ownership has not, in truth, changed at all. The IRD and the courts should apply both halves of that principle with equal rigour. A tax system that applies the look-through selectively – to find liability but not to confirm continuity – does not serve the rule of law; it undermines it.