The Real Constitution of Financial Power in Nepal

Central Bank Independence, Executive Control, and the Architecture of Monetary Governance

This post undertakes a comprehensive legal and institutional analysis of Nepal’s financial governance architecture, with a specific focus on the autonomy, accountability, and constitutional positioning of Nepal Rastra Bank (NRB). By integrating constitutional law, statutory frameworks, fiscal governance mechanisms, macroeconomic institutional behavior, and Supreme Court jurisprudence, it maps what Ferdinand Lassalle termed the “real constitution” – the actual distribution of financial power as opposed to its formal legal allocation. The central finding is that NRB’s independence exists not as a binary legal status but as a contested continuum: the institution simultaneously operates as a structurally subordinate executive agency under constitutional and administrative law, a functionally autonomous technocratic regulator through statutory delegation and institutional practice, and a judicially protected constitutional actor through Supreme Court intervention. The analysis reveals a model of coordinated technocratic dependence – a governance arrangement in which political supremacy is formally preserved through constitutional and appointment structures, while operational regulatory power is effectively exercised by the central bank through delegated legislation, macroeconomic narrative control, and deeply internalized compliance architectures across the banking sector.

Part I – The Judicial Crucible: Where Financial Power Meets Constitutional Law

1.1 Two Governors, Two Decades, One Constitutional Question

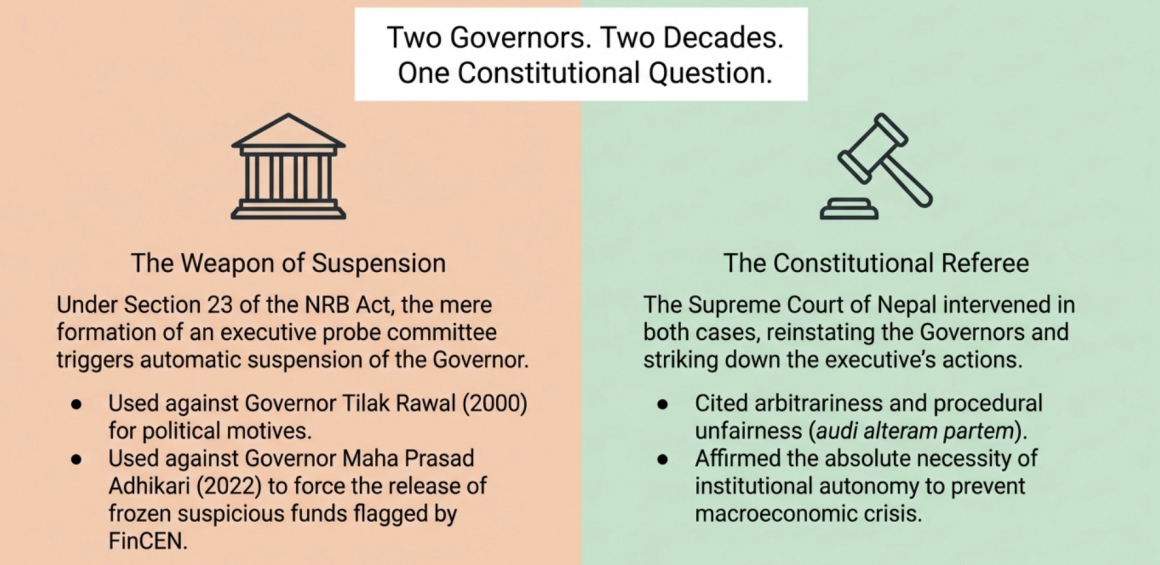

In April 2022, the Government of Nepal, led by Prime Minister Sher Bahadur Deuba, invoked Section 23 of the Nepal Rastra Bank Act, 2058, to form a three-member probe committee against Governor Maha Prasad Adhikari. The charges were sweeping but vague: “leaking sensitive information,” “systematically destroying the economy,” and “failing to fulfill responsibilities effectively.” The immediate legal effect, however, was precise and devastating – under the Act’s automatic suspension clause, the mere formation of the committee stripped the Governor of his office without a single allegation being proven.

The real conflict was neither administrative nor procedural. It was constitutional. The Finance Minister had issued written directives to the NRB ordering the release of approximately Rs 400 million in suspicious funds linked to a private businessman – funds that had been frozen following a direct alert from the United States Financial Crimes Enforcement Network (FinCEN) requesting their return. The NRB, acting under its anti-money laundering and combating the financing of terrorism (AML/CFT) obligations, maintained the freeze. The probe committee was the executive’s retaliatory instrument.

The Supreme Court of Nepal, through a division bench of Justices Sapana Pradhan Malla and Tanka Bahadur Moktan (upholding an earlier interlocutory order by Justice Hari Phuyal), reinstated Adhikari in a ruling that stands as the most significant judicial pronouncement on central bank independence in Nepali constitutional history. The Court struck down the executive’s actions on four distinct administrative law grounds:

- Arbitrariness and evidentiary insufficiency: The probe committee was constituted “without sufficient evidence” and lacked “concrete allegations” (Kathmandu Post, 30 April 2022).

- Procedural unfairness (audi alteram partem): Adhikari was “not given an opportunity for clarification” before the action triggering automatic suspension.

- Institutional autonomy: The Court affirmed that the NRB is an “autonomous body” and that the executive “cannot interfere” with its independence.

- Proportionality and macroeconomic responsibility: Suspending the central bank chief while the country was “heading towards an economic crisis” was deemed disproportionate.

This was not the first time the Supreme Court had intervened to protect central bank leadership from executive overreach. Two decades earlier, in 2000, the government of Prime Minister Girija Prasad Koirala abruptly dismissed Governor Tilak Rawal – a move widely perceived as politically motivated rather than grounded in policy failure. A bench of Justices Krishna Jung Rayamajhi and Ganesh Bahadur Singh reinstated Rawal, ruling the dismissal unlawful and arbitrary. The political fallout was immediate: Finance Minister Mahesh Acharya resigned. More significantly, the Rawal reinstatement directly catalyzed the drafting of the Nepal Rastra Bank Act, 2058 (2002), which formally entrenched the bank as an autonomous institution with legally codified removal procedures (NRB, Reflection of Former Governors, Special Publication).

Key Finding: The Supreme Court of Nepal has constructed a doctrinal shield around central bank leadership that is among the most protective in South Asia. The judiciary treats the security of gubernatorial tenure not merely as an employment right but as a structural prerequisite for monetary stability and institutional independence.

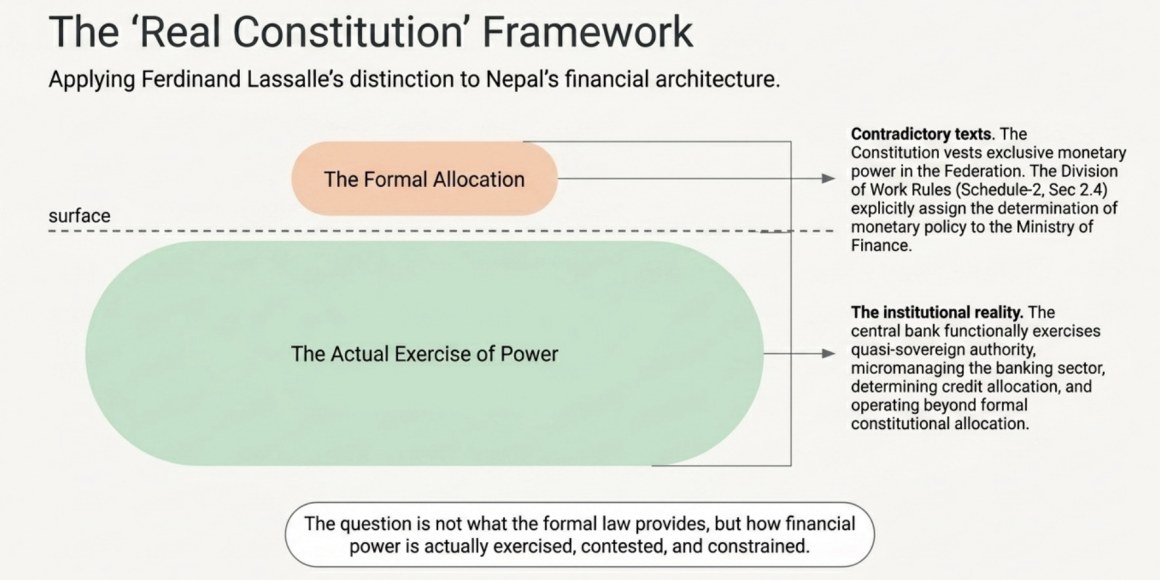

1.2 The Central Question: What Is the “Real Constitution” of Financial Power?

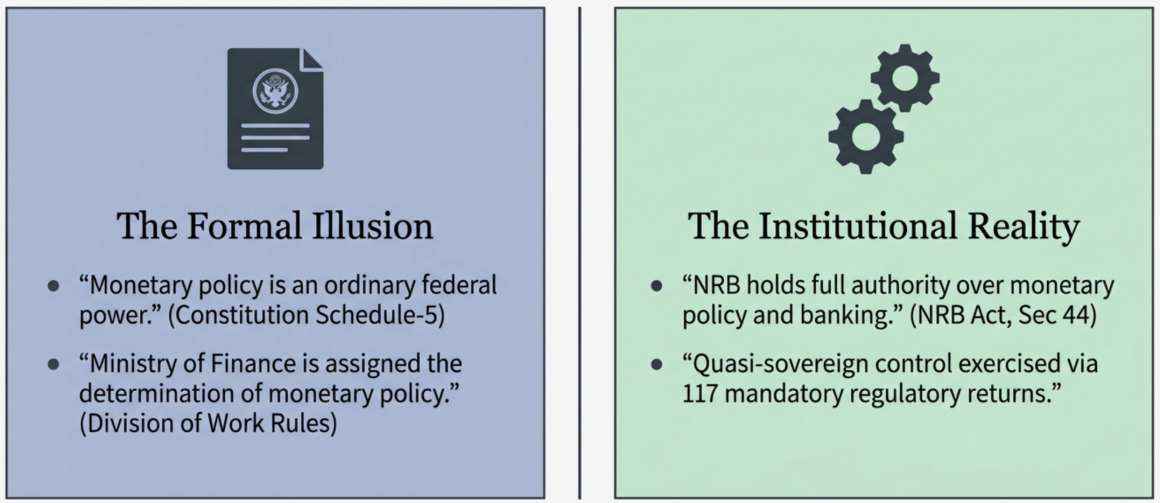

These judicial dramas expose a constitutional paradox at the heart of Nepal’s financial governance. The formal legal architecture – the Constitution, the Government Work Division Rules, the old and new NRB Acts – distributes financial power between the executive, the central bank, and the judiciary in ways that are internally contradictory. The Constitution vests “central bank, monetary policy, currency and banking” as exclusive federal powers (Schedule-5, Item 5). The Government of Nepal (Division of Work) Rules, 2072, assign the “determination and implementation of monetary policy” directly to the Ministry of Finance (Schedule-2, Section 2.4). The NRB Act, 2058, grants the central bank “full authority” (purna adhikar) over monetary policy (Section 44), foreign exchange policy (Section 62), and banking regulation (Section 79(1)). And the Supreme Court, through its extraordinary jurisdiction under Article 133 of the Constitution, acts as the final referee.

Ferdinand Lassalle’s distinction between a state’s written constitution and its “real constitution” – the actual configuration of power among institutions – provides the analytical framework for this post. In Nepal, the written instruments point in contradictory directions. The real question is not what the law formally provides, but how financial power is actually exercised, contested, and constrained.

This analysis finds that the answer is a continuum of contested autonomy – not binary independence or subordination, but a dynamic institutional arrangement shaped by four forces:

| Force | Direction of Pull |

| Constitutional and administrative design | Toward executive control and political supremacy |

| Statutory delegation and regulatory practice | Toward technocratic autonomy and operational independence |

| Fiscal-monetary coordination and sovereign debt | Toward fiscal dominance and coordination dependency |

| Judicial review and administrative law doctrine | Toward accountable independence and institutional protection |

The remainder of this analysis maps each of these forces in granular legal and institutional detail.

Part II – The Formal Constitution: From Executive Subordination to Contested Autonomy

2.1 The Old Regime: Total Executive Subordination Under the NRB Act, 2012 BS

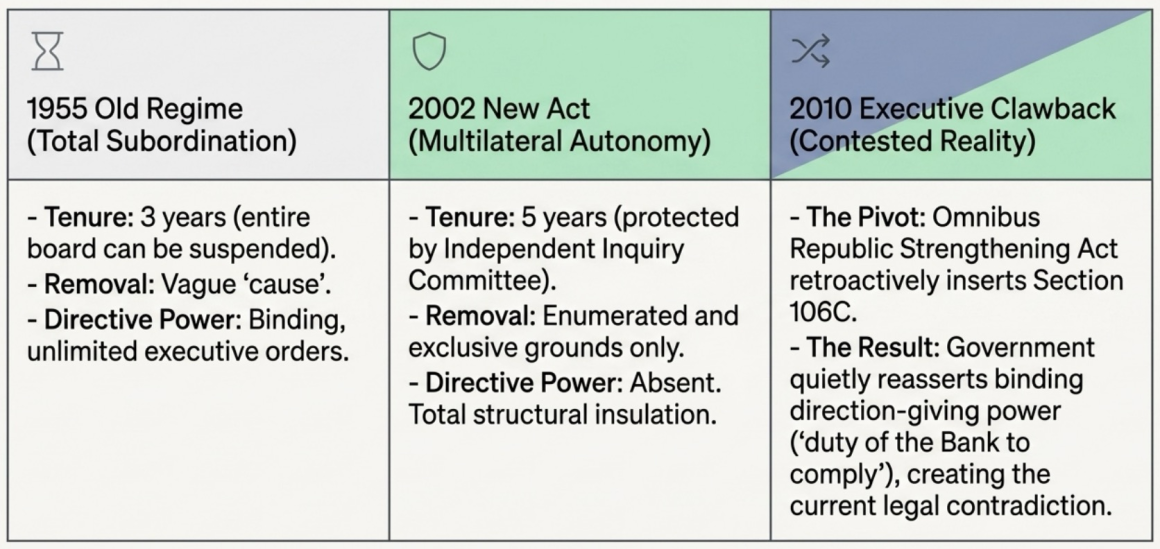

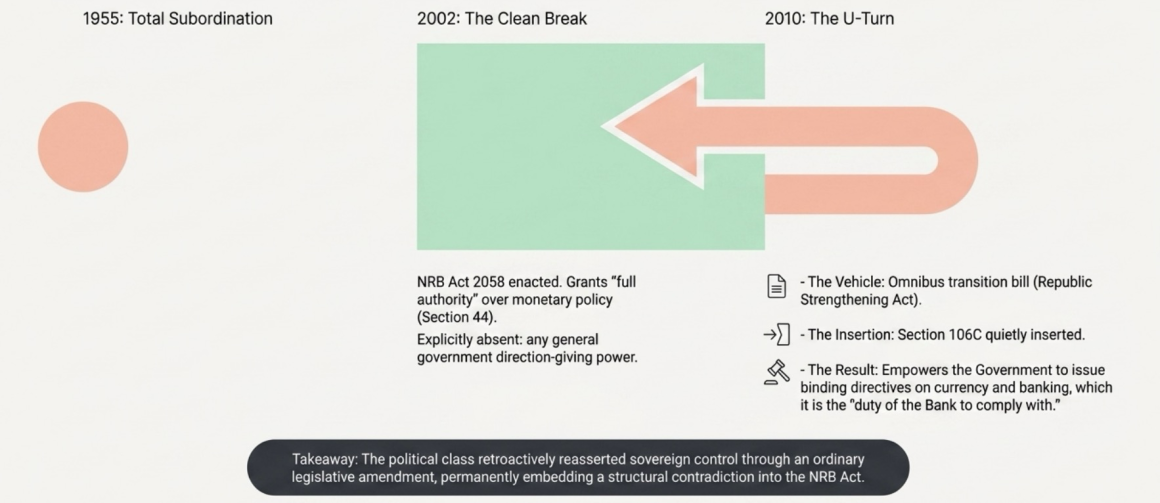

The historical legislative framework governing the NRB, dating to the Nepal Rastra Bank Act, 2012 BS (1955), was designed for a state-controlled economy in which the central bank functioned as an administrative arm of the government. The statutory architecture was one of near-total executive subordination:

- Binding directives: Section 5(1) of the old Act explicitly empowered the Government of Nepal to issue binding directives to the Governor “from time to time as it deems necessary for the national interest.” Section 5(2) legally mandated the Board of Directors to manage the Bank under these directives. Section 5(3) required rule-making to occur strictly under government supervision.

- Credit control as government function: Section 22 dictated that the Bank must attempt to control credit “according to the directives of the government.”

- Currency issuance under executive license: Section 18(1) required government approval for note issuance; Section 18(4) gave the government final authority over denomination, design, and paper for note issuance.

- Foreign exchange as government monopoly: Section 21 placed the foreign exchange monopoly under government-framed rules.

- Agency status: Section 33 explicitly declared that the Bank “shall become the agent of the Government” for specified functions.

- Precarious tenure: The Governor served a three-year term (Section 6(2)); Directors served two-year terms (Section 6(3)). Section 8 allowed the Government to remove the Governor if unable to work for 15 days or for failing to follow government orders. Section 9(2) permitted dismissal for vaguely defined “cause.” Section 11(1) allowed the Government to suspend the entire Board if deemed incapable.

Under this framework, the NRB possessed no meaningful institutional autonomy. The Bank was legally engineered as a subordinate financial bureau executing the political and economic will of the Ministry of Finance. A World Bank review of this period confirmed that the statutory architecture was fundamentally designed for an era when the NRB merely supervised government-owned commercial banks while remaining heavily subordinated to the Ministry of Finance (Legal and Judicial Environment for Financial Sector in Nepal, World Bank, 2003).

2.2 The Constitutional Framework: Federal Monopoly Over Monetary Authority

The Constitution of Nepal (2015) allocates monetary authority to the Federation but does not constitutionally entrench central bank independence. The relevant provisions establish:

- Exclusive federal power: Schedule-5, Item 5 lists “Central planning, central bank, financial policies, currency and banking, monetary policy, foreign grants, aid and loans” as exclusive federal powers.

- No constitutional body status: Unlike the Auditor General (Part-22), the Election Commission (Part-24), or the National Human Rights Commission (Part-26), the NRB receives no constitutional body designation. It remains a statutory creation, vulnerable to ordinary legislative amendment.

- State economic policies: Article 51(d) mandates strengthening the national economy through public, private, and cooperative participation. Article 51(d)(4) requires regulation to maintain fairness, accountability, and competition.

- Fiscal sovereignty of Parliament: Article 115(2) requires all government loans and guarantees to be authorized by federal law. Article 118 and 119 vest budgetary authority in Parliament.

- NNRFC as fiscal check: Article 251(1)(f) empowers the National Natural Resources and Fiscal Commission to recommend borrowing ceilings for all government tiers.

The constitutional silence on central bank independence is not neutral – it is structurally consequential. By treating monetary authority as an ordinary federal power rather than an independently protected constitutional function, the Constitution leaves the NRB’s autonomy entirely dependent on statutory provision and judicial interpretation. This stands in contrast to jurisdictions where central bank independence enjoys constitutional entrenchment.

Comparative Note: Sri Lanka’s recent Central Bank of Sri Lanka Act, No. 16 of 2023, enacted under IMF conditionality following sovereign default, faced constitutional challenge precisely because petitioners argued that granting the CBSL autonomous financial control violated Article 148 of the Sri Lankan Constitution, which vests full control of public finance in Parliament. The Sri Lankan Supreme Court’s determination harmonized parliamentary sovereignty with technocratic autonomy – affirming that central bank independence does not inherently violate constitutional fiscal sovereignty provided rigorous accountability mechanisms exist. Nepal’s constitutional framework has not yet been tested at this level of doctrinal sophistication.

2.3 The Government Work Division Rules: Ministry of Finance as Apex Authority

The Government of Nepal (Division of Work) Rules, 2072 (2015), operationalize the Constitution’s allocation of federal power. Schedule-2 assigns the Ministry of Finance sweeping jurisdiction:

| Rule Reference (Schedule-2) | Responsibility Assigned to MoF |

| Section 2.1 | Formulation, implementation, and evaluation of economic and revenue policies |

| Section 2.4 | Determination and implementation of currency and monetary policy |

| Section 2.5 | Nepal Rastra Bank, banking, financial institutions, and insurance |

| Section 2.6 | Budget preparation |

| Section 2.13 | Foreign debt, grants, bilateral and multilateral aid |

| Section 2.14 | Foreign currency exchange and control |

| Section 2.18 | Relations with World Bank, IMF, and international financial institutions |

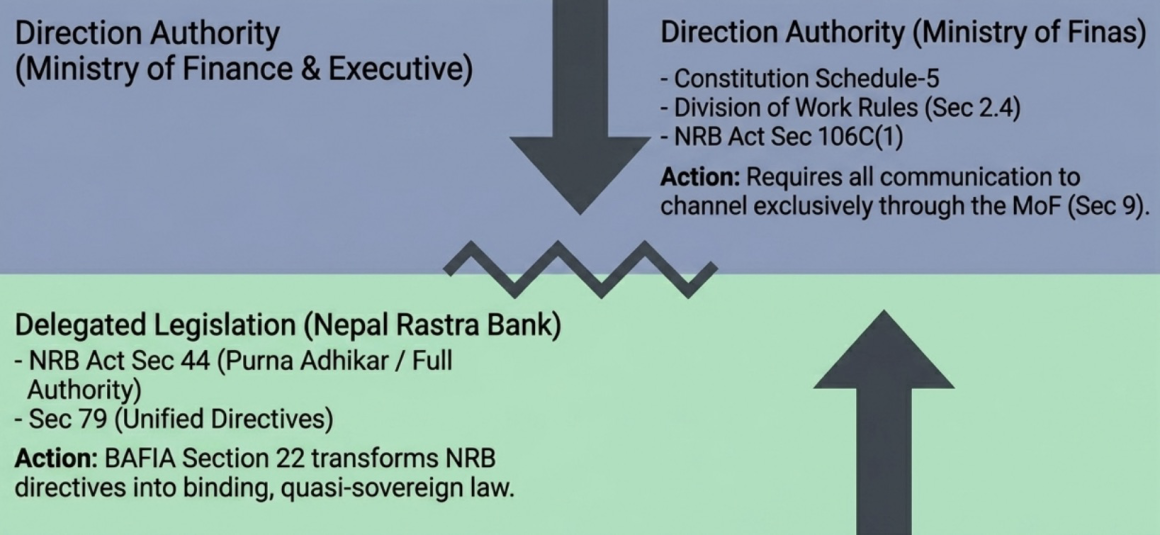

The assignment of “determination and implementation of monetary policy” to the Ministry of Finance (Section 2.4) is the single most significant administrative law provision undermining NRB independence. It means that, as a matter of executive governance, the Ministry – not the central bank – holds the formal authority to determine monetary policy. The NRB’s statutory mandate to formulate and implement monetary policy under NRB Act Section 44 thus operates within, and potentially subordinate to, the MoF’s broader administrative jurisdiction.

Furthermore, Section 9 of the NRB Act, 2058, requires that all correspondence between the NRB and the Government of Nepal be channeled exclusively through the Ministry of Finance. This channel-of-communication requirement structures the institutional relationship as one of hierarchical reporting rather than coordinate autonomy.

2.4 The Paradigm Shift: NRB Act, 2058 (2002)

The enactment of the Nepal Rastra Bank Act, 2058 represented a fundamental paradigm shift – from the old regime of total executive subordination to a new architecture of contested autonomy. The Act was directly influenced by global trends toward central bank independence and supported by conditionality frameworks from the World Bank and IMF.

Institutional identity: Section 3(3) defines the NRB as an “autonomous and corporate body with perpetual succession”. Section 3(4)-(7) grant it a separate seal, property rights, legal personality to sue and be sued, and the power to establish offices domestically and internationally.

Exclusive statutory powers: The Act grants NRB “full authority” (purna adhikar) over:

| Function | Statutory Basis |

| Monetary policy formulation and implementation | Section 44 |

| Foreign exchange policy | Section 62 |

| Banking regulation | Section 79(1) |

| Currency issuance | Section 52(1) |

Non-infringement clause: Section 5(3) states that the NRB’s exercise of its statutory powers “shall not be infringed by anyone.”

Financial autonomy: Section 32 establishes that the NRB’s authorized capital cannot be transferred, nor can any burden of debt be placed upon it, without mandatory consultation. Section 75 restricts government credit from the NRB, creating a firewall against monetization of fiscal deficits.

Qualified policy alignment: Section 4(2) requires the NRB to assist in implementing the Government’s economic policies – but only “provided such policies do not adversely affect the NRB’s primary objectives.”

Yet the 2002 Act preserves critical executive levers:

- Government direction power: Section 106C(1) empowers the Government to give directions to the NRB regarding currency, banking, and finance. Section 106C(2) declares it the “duty of the Bank to comply with such directions.”

- Appointment control: Sections 15-17 vest Governor, Deputy Governor, and Director appointments in the Council of Ministers.

- Rule-making hierarchy: Section 110(1) requires broad “Rules” to receive prior government approval, though Section 110(3) independently empowers the Governor to issue directives, procedures, and guidelines. Section 110(4) requires these to be sent to the Government “for information” – not approval.

- Automatic suspension mechanism: Section 22(4) automatically suspends the Governor upon formation of an Inquiry Committee, creating the vulnerability exploited in the Adhikari case.

The Clawback on NRB’s Authority: The NRB Act, 2058 as originally enacted in 2002 was deliberately designed as a clean legislative break toward central bank independence – granting “full authority” over monetary policy (Section 44), insulating NRB powers from “infringement by anyone” (Section 5(3)), and creating an “autonomous and corporate body” (Section 3(3)). Critically, the original Act contained no general government direction-giving power over the central bank. That power was absent by design. However, in 2010, the executive retroactively inserted Section 106C through the Republic Strengthening and Some Nepal Laws Amendment Act, 2066 (January 21, 2010) – an omnibus legislative vehicle enacted during Nepal’s post-monarchy transition, when hundreds of laws were being amended to reflect the new republican order. Through this amendment, the political class used the legislative window of “republic strengthening” to quietly reassert binding executive authority over the institution that had just been made autonomous: Section 106C(1) empowers the Government to give directions to the NRB regarding currency, banking, and finance, and Section 106C(2) declares it the “duty of the Bank to comply with such directions.” The Act now simultaneously grants full monetary authority and obliges compliance with government directions; creates an autonomous body whose Governor can be automatically suspended by executive-appointed committees (Section 22(4)); and requires the MoF to serve as the exclusive communication channel (Section 9). These contradictions are not drafting errors within a single legislative moment – they represent a retroactive political clawback of autonomy, an empirical demonstration that the political class, having conceded technocratic independence under multilateral pressure in 2002, moved within eight years to reassert sovereign control over the central bank through ordinary legislative amendment. The ease of this reassertion – requiring no constitutional amendment, no supermajority, no judicial approval – itself reveals the structural vulnerability of central bank independence that lacks constitutional entrenchment.

2.5 The Appointment and Removal Architecture

Board composition (Section 14): The NRB is governed by a seven-member Board of Directors comprising the Governor as Chairperson, the Secretary of the Ministry of Finance as an ex-officio member, two Deputy Governors, and three external Directors appointed by the Government. The inclusion of the Finance Secretary as a statutory Board member represents the most direct institutional channel of executive presence within the central bank’s governing body – a permanent seat at the decision-making table that requires no formal “direction” under Section 106C to exert influence.

The security of gubernatorial tenure is the most sensitive indicator of central bank independence. The 2002 Act establishes protections that are significantly stronger than the old regime, but fall short of international best practice:

Qualifications (Section 20): Governors, Deputy Governors, and Directors must hold at least a Master’s degree in economics, monetary, banking, finance, commerce, management, public administration, statistics, mathematics, or law, with relevant executive-level experience. This mandates technocratic expertise as a legal prerequisite.

Political disqualification (Section 21): Any member or official of a political party is disqualified from holding a Board position – a direct structural insulation from partisan politics.

Fixed tenure (Section 18): Five-year terms for the Governor, Deputy Governors, and Directors. The Governor may be reappointed once.

Restricted removal grounds (Section 22(5)-(6)): Removal is permitted only for specified grounds (misconduct, incompetence, incapability, absence from three consecutive meetings without valid reason). Section 22(6) explicitly prohibits removal “for any reasons other than those specified.”

Independent Inquiry Committee (Section 23): Before removal, the Government must constitute a committee chaired by a retired Supreme Court Justice and including two expert members. The Committee must give the individual reasonable opportunity to defend themselves, embodying audi alteram partem.

Vulnerability: automatic suspension (Section 22(4)): Formation of the Inquiry Committee automatically suspends the Governor – the mechanism weaponized against Governor Adhikari and judicially neutralized by the Supreme Court.

| Feature | Old Act (2012 BS) | New Act (2058/2002) |

| Governor tenure | 3 years | 5 years |

| Removal grounds | Vague “cause” (Sec 9(2)) | Enumerated and exclusive (Sec 22(5)-(6)) |

| Pre-removal process | None specified | Independent Inquiry Committee (Sec 23) |

| Government directive power | Binding, unlimited (Sec 5(1)) | Preserved but qualified (Sec 106C) |

| Institutional status | Government agent (Sec 33) | Autonomous corporate body (Sec 3(3)) |

| Board suspension | Government can suspend entire Board (Sec 11(1)) | Not replicated |

| Political disqualification | None | Political party members barred (Sec 21) |

This historical arc – from total subordination under the old Act to contested autonomy under the new – constitutes one of the most significant legal transformations in Nepal’s institutional history. Yet the transformation remains incomplete: the executive retains appointment power, direction-giving authority, and the communication channel monopoly. The real question is whether these residual controls amount to substantive executive dominance or merely formal political accountability.

Part III – The Regulatory State Within: Statutory Authority and the Exercise of Delegated Power

3.1 The Delegated Legislative Machinery

The NRB exercises its most consequential power not through headline monetary policy announcements but through the quotidian machinery of delegated legislation – unified directives, circulars, bylaws, and prudential norms that constitute the binding legal framework for every bank and financial institution in Nepal.

Statutory basis: The primary authorization for NRB directives is Section 79 of the NRB Act, 2058. Every unified directive issued to Class A, B, C, D, and Infrastructure Development Banks explicitly states in its preamble that it is issued by exercising authority under Section 79. Section 110(3) independently empowers the Governor to issue orders, directives, procedures, and guidelines on matters other than those matters that the board is empowered to do under Section 110(2). Section 111 allows the NRB to frame guidelines subject to the Act and its bylaws.

Binding force: NRB directives are binding subordinate legislation. BAFIA, 2073, Section 22(3)(a) and (3)(a) explicitly mandates that the Board of Directors of any BFI must operate “subject to the provisions of BAFIA and the directives of the NRB” and “and to carry out other functions as specified by the Rastra Bank from time to time”. This transforms NRB directives from advisory guidance into legally enforceable obligations carrying the force of delegated law.

Substantive scope: The NRB creates detailed substantive obligations far beyond explicit statutory language. While the parent Acts broadly task NRB with maintaining stability, the directives create:

- Precise quantitative capital adequacy requirements (Minimum Total Capital of 8.5% of Risk-Weighted Exposures under Basel III for Class A banks, with a 2.5% Capital Conservation Buffer)

- Exact Loan-to-Value ratios (50% maximum for real estate in Kathmandu valley)

- Mandatory 5-tier loan classification with specific provisioning percentages (1% for Pass, 5% for Watch List, 25% for Sub-standard, 50% for Doubtful, 100% for Loss)

- Interest rate spread caps

- Directed sector lending quotas (15% for agriculture, 10% for energy, 15% for MSMEs by 2026-27)

- AML/CFT compliance frameworks with fines ranging from Rs. 10 Lakh to Rs. 5 Crore

Frequency and dynamism: NRB exercises quasi-legislative authority dynamically, issuing circulars throughout the year and periodically consolidating them into master Unified Directives. The 2081 Unified Directives, for instance, consolidate all previous directives with all subsequent circulars and amendments issued up to the end of Poush 2081.

Procedural requirements: Under Section 110(4) and (5), NRB bylaws and directives must be sent to the Government for information and published publicly. For novel regulations, such as the Artificial Intelligence Guidelines, the NRB has engaged in public consultation. However, no statute mandates prior consultation as a general procedural requirement – a gap that distinguishes NRB’s directive-making power from more proceduralised regulatory regimes.

Limits: Section 111 requires guidelines to be framed “subject to this Act and rules or bylaws framed under this Act.” The Prompt Corrective Action Bylaw, 2074, Section 11, recognizes that any provision contradicting the NRB Act or BAFIA is automatically void to the extent of the contradiction. This establishes the ultra vires principle as an internal limiting mechanism.

Comparative Note: The question of how far delegated regulatory power can extend was dramatically reshaped in the United States by Loper Bright Enterprises v. Raimondo (2024), which overturned the Chevron doctrine of judicial deference to agency interpretation. Under Chevron (1984), courts deferred to an agency’s reasonable interpretation of ambiguous statutes – a doctrine that had insulated the Federal Reserve and other financial regulators from judicial second-guessing for four decades. Loper Bright transferred the power of statutory interpretation squarely back to the judiciary, and Corner Post v. Board of Governors of the Federal Reserve System (2024) simultaneously expanded the statute of limitations for challenging agency rules. Nepal’s judiciary has not yet developed a comparable doctrine of systematic deference or its reversal – it operates case-by-case, applying what this analysis terms “calibrated deference.”

3.2 Prudential Regulation: The NRB as Quasi-Sovereign Over the Banking Sector

The depth of NRB’s regulatory penetration into banking operations is extraordinary by any comparative standard. The NRB does not merely set macro-prudential parameters; it micromanages banking behavior across every operational dimension:

Capital adequacy: Tiered Basel frameworks – Basel III for Class A banks and NIFRA (8.5% Total Capital, 4.5% CET1, 2.5% Conservation Buffer); simplified Basel II for Class B and C (6% Tier 1, 10% total); customized flat-rate rules for Class D microfinance (4% primary capital, 8% total).

Supervisory discretion: Under the Supervisory Review Process (Pillar II), if NRB supervisors are “not convinced about a bank’s risk management practices,” they have discretionary authority to impose additional capital charges of 2% to 5% of Gross Income or increase risk-weighted exposures by up to 3%. Agricultural Development Bank Ltd reports that supervisors levied an additional 5% capital charge on gross income for operational risk shortcomings.

Qualitative loan downgrades: Irrespective of past-due status, NRB directives mandate classification as “Loss” (100% provisioning) if qualitative anomalies are detected – misuse of funds, borrower absconding, project non-operation, or inadequate collateral. This grants NRB absolute discretionary power over asset classification.

Corporate governance: NRB mandates specific Board compositions (including female and independent directors), Fit and Proper Tests for directors and executives, codes of conduct, cooling-off periods, and prohibitions on lending to directors or shareholders holding more than 1%.

Enforcement through PCA: The Prompt Corrective Action Bylaw, 2074, links enforcement directly to capital adequacy thresholds, empowering NRB to restrict dividends, halt branch expansion, cap deposits and loans, block fixed asset purchases, prohibit salary increases, or declare the BFI “problematic.”

Emergency intervention: Under BAFIA Section 102 and NRB Act Section 86C, the NRB can suspend a BFI’s Board for up to three years and completely take over management. Under Section 86D, once control is assumed, NRB can merge the bank, transfer assets and liabilities, terminate employees, or cancel operations. Under Section 86F(3), share valuations during forced sales during corrective action being taken against the bank are determined not by a ministry but by an independent expert committee including SEBON and ICAN representatives.

Nabil Bank alone reports submitting more than 117 different returns to the NRB via various reporting portals. Standard Chartered Bank Nepal explicitly states its Board has “complied with the principles and provisions of the Nepal Rastra Bank Directives on Corporate Governance.” Nepal SBI Bank describes compliance as “the foundational layer of corporate governance” and a “strategic priority.”

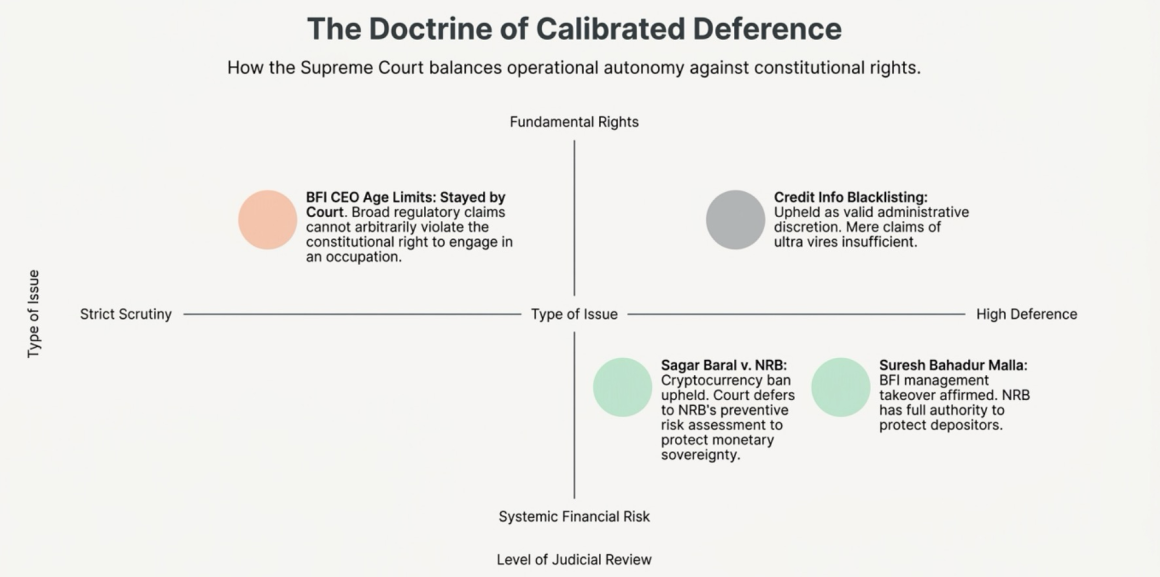

3.3 Judicial Treatment of Delegated Authority: The Doctrine of Calibrated Deference

The Supreme Court of Nepal has developed what this analysis terms a doctrine of calibrated deference – high deference to NRB on systemic financial stability, strict scrutiny when fundamental rights are engaged:

High deference – corporate governance enforcement: In Suresh Bahadur Malla v. NRB, the Court held that NRB possesses “full authority” to take over BFI management if top management fails to protect depositor interests. In Bhubanseswar Ghimire v. CIAA, the Court declared that CIAA lacks jurisdiction over internal BFI financial matters; the NRB is the “correct governing body.” In Uttam Bahadur Pun v. NRB and NRB v. Laxman Gyawali, the Court upheld severe administrative penalties and executive dismissals for financial embezzlement.

High deference – cryptocurrency ban: In the Sagar Baral v. Nepal Rastra Bank public interest litigation (2022), the Court dismissed an ultra vires challenge to NRB’s complete prohibition on cryptocurrency. The Court accepted NRB’s comprehensive risk assessment that cryptocurrencies lack legal tender status, pose unmanageable capital flight risks, facilitate financial crimes, and threaten monetary stability. The ruling validated the NRB’s pre-emptive regulatory paradigm – the power to absolutely prohibit shadow monetary instruments that threaten sovereign financial sovereignty under Sections 52 and 61 of the NRB Act and Section 9 of the Foreign Exchange (Regulation) Act, 1962.

Comparative Divergence with India: This stands in sharp contrast to the Indian Supreme Court’s ruling in Internet & Mobile Association of India (IAMAI) v. Reserve Bank of India (2020), where the Court struck down the RBI’s essentially identical cryptocurrency ban. Applying a strict empirical proportionality test, the Indian Court held that the RBI failed to demonstrate any actual damage to regulated entities from virtual currency trading. Because the RBI could not prove specific harm, the blanket ban was deemed disproportionate. Nepal’s judiciary deferred to the NRB’s theoretical and preventive risk assessment; India’s demanded empirical proof of harm. This represents fundamentally different regional tolerances for pre-emptive financial regulation.

Strict scrutiny – fundamental rights: When NRB issued a unified directive barring BFI CEOs above age 65 and prohibiting continuation past 69, the Supreme Court (via then-Chief Justice Cholendra Shumsher JB Rana) stayed implementation, finding that arbitrary age bars for employment in private corporate entities violate the constitutional right to engage in an occupation. While the NRB argued that BFIs are quasi-public institutions, the Court prioritized constitutional rights over the central bank’s expansive regulatory claims.

Ultra vires – high threshold: In challenges to the NRB’s Credit Information Center and Loan Information By-rules (issued under Sections 88(1) and 110(2) of the NRB Act), the Supreme Court established that a mere statement of ultra vires is insufficient; the petitioner must concretely demonstrate how delegated legislation breaches legal rights or contradicts the parent act. The Court found the blacklisting of defaulting directors to be perfectly intra vires, noting that “because a company’s works are carried out by its directors, holding directors liable for willful default is a valid exercise of administrative discretion.”

| Regulatory Action | Challenge Ground | Court Ruling | Standard of Review |

| BFI management takeover and executive penalties | Arbitrariness, jurisdiction | Upheld; NRB has full authority to protect depositors | High deference |

| Credit Information blacklisting | Ultra vires to Sections 88, 110 | Upheld; intra vires, valid administrative discretion | High deference |

| Cryptocurrency ban | Ultra vires; economic liberty | Upheld; within NRB statutory competence | Deference to preventive risk assessment |

| Age limit for BFI CEOs | Fundamental right to occupation | Stayed; violates constitutional employment rights | Strict scrutiny |

3.4 The Securities Regulation Interface: Dual Jurisdiction and Institutional Friction

The NRB’s regulatory perimeter intersects significantly with the Securities Board of Nepal (SEBON), creating zones of dual jurisdiction, institutional friction, and unresolved ambiguity.

SEBON is established under the Securities Act, 2063, as an autonomous corporate body (Section 4). Critically, an NRB representative sits on SEBON’s Board of Directors (Section 3(2)(gh)), providing institutional coordination at the governance level. The regulatory division is functional:

- NRB: Prudential regulation of banks (capital adequacy, liquidity, solvency)

- SEBON: Market conduct regulation (insider trading, disclosure, securities issuance)

However, because banks are primary actors in capital markets – as listed entities, ASBA collection centers, clearing banks, merchant banking sponsors, and mutual fund creators – the regulatory spheres heavily overlap. Under the Securities Registration and Issue Regulation, 2073, Rule 3(3), a bank requiring prior approval from its regulatory body (NRB) must obtain such approval before even submitting an application to SEBON for securities registration. Rule 10(2) requires NRB approval of prospectuses before SEBON’s final approval. In mergers, Rule 5(4) of the Securities Registered Corporate Bodies Merger Guidelines, 2079, requires SEBON to grant preliminary approval within 3 working days if accompanied by prior NRB consent.

A critical unresolved tension exists between SEBON’s transparency mandate and NRB’s prudential confidentiality. SEBON requires immediate disclosure of “Price Sensitive Information.” If NRB places a bank under confidential Prompt Corrective Action due to capital or liquidity stress, the bank faces a legal dilemma: SEBON demands disclosure to protect minority shareholders; NRB’s supervisory logic demands confidentiality to prevent bank runs. No statutory “safe harbor” mechanism exists to resolve this conflict.

3.5 Foreign Exchange: The Architecture of Sovereign Control

NRB’s authority over foreign exchange constitutes the most absolute dimension of its regulatory power – one that is primarily sovereign and monetary rather than merely prudential.

Under the Foreign Exchange (Regulation) Act, 2019 (FERA), Section 3(1), any entity wishing to engage in FX transactions must obtain an NRB license. Section 4(1) prohibits transacting without NRB approval. Section 4(2) mandates transactions at NRB-determined exchange rates. Section 5(1)-(2) prohibit cross-border currency movement without an NRB license. Section 6(1) grants the Government the extraordinary emergency power to declare a foreign exchange crisis and order citizens to surrender their holdings at prescribed rates.

The Act Restricting Investment Abroad, 2021 (1964), provides the other pillar: Section 3(1) strictly prohibits any outward investment; Section 2(a) broadly defines prohibited investments to include foreign securities, partnerships, bank accounts, and real estate.

NRB leverages this sovereign FX authority to exercise comprehensive micro-level control:

- Capping personal travel exchange at USD 2,500

- Limiting online service imports via prepaid cards to USD 500

- Mandating cash margins for Letters of Credit

- Declaring cryptocurrency, NFTs, and network marketing transactions illegal

- Prohibiting foreign loans for real estate or margin trading (FIFL Bylaws, Schedule-10)

- Imposing 150% risk weights on bank claims on venture capital and private equity

This FX governance architecture reveals that Nepal operates a closed capital account regime where the NRB functions as the sovereign gatekeeper of every cross-border financial flow. The regime is fundamentally precautionary rather than liberal – rooted in protecting external sector stability through comprehensive state control rather than enabling market-determined capital mobility.

Part IV – The Fiscal-Monetary Nexus: Sovereign Debt, Public Finance, and the Architecture of Coordination

4.1 The PDMO Transition: Separating Fiscal from Monetary

Nepal’s public debt management underwent a structural transformation with the Public Debt Management Act, 2079, and the establishment of the Public Debt Management Office (PDMO). Until March 30, 2024 (Chaitra 17, 2080), the NRB directly managed the issuance and administration of domestic debt. The full transition of front, middle, and back-office functions to the PDMO represents the most significant institutional separation of fiscal and monetary responsibilities in Nepal’s financial history.

However, the separation is incomplete. The NRB remains operationally linked through several statutory mechanisms:

- Mandatory purchase obligation: Under Rule 13(5) of the Public Debt Management Rules, 2080, if a Treasury Bill issue is undersubscribed, the Debt Issuance and Management Committee can request the NRB to purchase the remaining portion at the weighted average price, and it is the “duty of the Bank” to purchase such securities. This obligation directly constrains the NRB’s balance sheet management and monetary independence.

- Committee participation: NRB’s Executive Directors for Economic Research and Banking Management sit on the Debt Issuance and Management Committee, but the committee is chaired by the Finance Secretary (Rule 11(1)(a) of the PDMO Rules, 2080).

- Fiscal agent role: The NRB continues to maintain the government’s consolidated fund and operative accounts for debt transactions.

- Dual-use instruments: Treasury Bills serve simultaneously as fiscal financing instruments and monetary policy tools for liquidity management.

4.2 The Fiscal Dominance Question

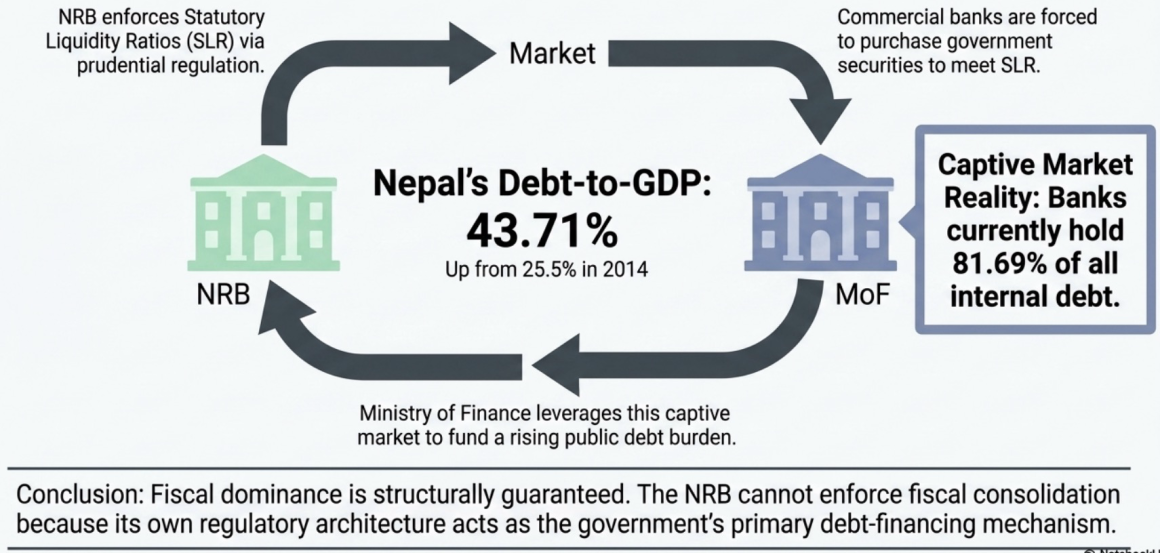

The legal framework mandates “harmony” between fiscal and monetary policy (Rule 3(g) of the PDMO Rules, 2080). In practice, this “harmony” creates conditions for fiscal dominance – where government debt needs influence interest rates and constrain monetary policy space.

Commercial banks held 81.69% of total outstanding internal debt as of mid-July 2025 (PDMO Annual Report 81/82). This means that the NRB’s prudential regulation of the banking sector – specifically through Statutory Liquidity Ratios requiring banks to hold government securities – operates simultaneously as a captive market mechanism for government debt. The Government’s borrowing is structurally guaranteed by the regulatory architecture that the NRB itself enforces.

Public debt-to-GDP has risen steadily: from 25.5% in 2014/15, to 29.7% in 2017/18, to 41.5% in 2021/22, and reaching 43.71% in 2024/25 (PDMO Annual Report). The Medium-Term Debt Management Strategy (2081/82-2083/84) targets 38.23% – a trajectory requiring fiscal consolidation that the NRB cannot enforce.

4.3 Contingent Liabilities and Hidden Fiscal Risk

A critical dimension of fiscal-monetary interaction lies in contingent liabilities from State-Owned Enterprises (SOEs). The Government’s total estimated contingent liability reached NPR 212.6 kharba (Annual Status Review of Public Enterprises, 2082). Unfunded liabilities – primarily employee pensions and gratuities without dedicated funds – increased by 18.43% in a single year, reaching Rs. 62.61 billion. Government equity in SOEs reached Rs. 70.3 kharba, with 71.39% concentrated in three entities (Nepal Electricity Authority, Civil Aviation Authority, Nepal Telecom).

Under Section 14 of the Public Debt Management Act, 2079, the Federal Government can provide financial guarantees for SOE loans. If an SOE defaults, the obligation becomes a charge on the Federal Consolidated Fund. Large-scale crystallization of these contingent liabilities would require sudden, massive government borrowing – draining market liquidity and forcing the NRB to accommodate fiscal pressures through monetary expansion or emergency liquidity operations.

4.4 Intergovernmental Fiscal Relations: Centralized Sovereignty

Despite Nepal’s federal structure, fiscal sovereignty remains centralized for the purposes of financial stability:

- External borrowing is the exclusive power of the Federal Government (Constitution, Article 59(6); IGFAA 2074, Section 12(1))

- Provinces and Local levels can raise internal loans only within NNRFC-recommended ceilings and with prior Federal Government consent (IGFAA 2074, Section 14)

- If a sub-national government fails to repay a Federal loan, the Federation can deduct the unpaid amount from revenue-sharing transfers (Public Debt Management Act, 2079, Section 8(4))

This centralization ensures that sovereign borrowing cannot fragment across sub-national jurisdictions in ways that threaten monetary stability – but it also concentrates fiscal power in the Federal Executive that already controls the appointment of NRB leadership.

Part V – The “Real Constitution”: Institutional Behavior, Macroeconomic Narrative, and Regulatory Gravity

5.1 The Lassallian Framework Applied

If the formal constitutional and statutory architecture reveals a system of contested and ambiguous autonomy, the actual institutional behavior of the NRB – as documented through its own annual reports, supervision reports, financial stability publications, and the commercial banking sector’s internalization of its directives – reveals something far more definitive: the NRB operates as the de facto supreme regulator of the Nepali financial system, exercising power that vastly exceeds what the formal constitutional allocation would predict.

This gap between formal allocation and actual exercise is precisely the Lassallian distinction. The “real constitution” of financial power in Nepal is not found in the Division of Work Rules assigning monetary policy to the MoF; it is found in the 117 regulatory returns that BFIs submits to the NRB, in the NRB’s power to single-handedly declare a bank “problematic” and take over its management, and in the fact that no commercial bank can publish its audited financial statements or declare dividends without the NRB Supervision Department’s formal authorization.

5.2 Macroeconomic Narrative as Institutional Authority

The NRB constructs economic reality through its publications in ways that expand its perceived authority and justify interventions:

Data monopoly: NRB publishes exhaustive monthly and annual “Current Macroeconomic and Financial Situation” reports tracking everything from GDP to the micro-prices of ghee, oil, and spices. By controlling the definitive narrative of what the economic problems are, the NRB implicitly dictates what the acceptable policy solutions must be.

Crisis framing as authority expansion: Policies initially introduced as emergency measures systematically normalize into permanent regulatory frameworks:

| Emergency Measure | Original Justification | Permanent Status |

| Forced mergers and acquisitions | Resolution of fragile banks | Permanent consolidation tool: 245 BFIs pushed into M&A, 178 licenses revoked |

| Directed lending quotas | Economic recovery support | Permanent mandates: 15% agriculture, 10% energy, 15% MSMEs by 2026-27 |

| Regulatory relaxation during COVID-19 | Prevent economic collapse | Loan restructuring frameworks institutionalized |

| Interest rate corridor management | Liquidity crisis response | Permanent monetary policy architecture |

Vulnerability narrative: By framing Nepal’s economy as structurally constrained (currency peg, chronic trade deficit, remittance dependency) and inherently volatile (external shocks, supply chain disruptions), the NRB establishes the necessity of its interventionist approach. The structural paradox is telling: NRB holds USD 22.47 billion in foreign exchange reserves (sufficient for 18.1 months of imports against a 7-month target) while the country faces a USD 46.5 billion infrastructure financing gap. The NRB’s conservative hoarding is legally justified under the NRB Act’s mandate that reserve management prioritize safety and liquidity above income generation – but the economic consequence is that massive national wealth is immobilized under central bank control rather than deployed for development.

Self-defined success metrics: The NRB defines “macroeconomic stability” through strict numerical targets that it itself sets and measures – inflation within target ceilings, foreign exchange reserves exceeding import-coverage thresholds, Balance of Payments surplus. When actual performance meets these self-established targets, the NRB presents this as validation of its policies, creating a self-legitimizing cycle of institutional authority.

5.3 Commercial Bank Behavior: The Evidence of Regulatory Gravity

The most powerful evidence of NRB’s actual authority comes not from the NRB’s own claims but from the institutional behavior of the commercial banks it regulates. Annual reports from across Nepal’s banking sector reveal an industry that has fully internalized the central bank as its primary institutional reality:

Identity formation: Banks do not describe themselves as independent market actors. Nepal Investment Mega Bank Ltd defines its existence as providing services “within the limits and parameters set by legislations and regulatory framework.” Nepal SBI Bank identifies as a “prominent ‘A Class’ bank” operating under BAFIA and NRB guidelines.

Governance determined by directive: Kumari Bank notes that its Board composition – including at least one female and one independent director – is “strictly formed according to” NRB regulations. Nabil Bank reports that both its Chairperson and CEO must take an oath of secrecy and fidelity in the presence of the Governor of NRB immediately after appointment.

Strategy subordinated to compliance: Standard Chartered Bank Nepal describes “directing capital allocation towards productive sectors” specifically to support NRB’s “regulatory targets under Specified Sector Lending.” Nepal SBI Bank describes its ICAAP as a way to “demonstrate to NRB the Bank’s approach to capital management.” Strategic success is defined by the ability to “operate above the regulatory capital requirement.”

Dividend distribution as NRB prerogative: NIC Asia Bank and Nepal Bank Limited both include formal letters from the NRB Bank Supervision Department in their annual reports regarding the approval or denial of dividend distribution. No bank distributes dividends without NRB authorization.

Profitability constrained by directive: Himalayan Bank explicitly states that “banks are still facing pressure in maintaining capital adequacy requirements, especially in the case of Core Capital, which has reduced the business capacity of banks.” Standard Chartered reports margin compression from being required to “park funds in low-yield government securities and NRB deposits.”

Sector homogenization: There is near-universal adoption of the Basic Indicator Approach for operational risk and the Simplified Standardized Approach for credit risk. All banks maintain identical board-level committees (Audit, Risk Management, AML/CFT, HR) following NRB Unified Directive No. 6. The “Three Lines of Defense” model is cited ubiquitously. Deviations from regulatory norms are actively penalized through Supervisory Review adjustments – additional capital charges imposed if the NRB supervisor is “not satisfied with the overall risk management policies.”

Key Finding: Nepalese commercial banks do not behave as autonomous corporations. They behave as regulated financial agents whose operational reality is defined by an internalized governance logic dictated by the NRB. Compliance is not an external constraint imposed upon market actors; it is the “foundational layer of corporate governance” (Nepal SBI Bank), the structural basis for strategic planning, and the ultimate measure of institutional success. The NRB’s authority is not merely legal – it is gravitational.

5.4 AML/CFT and the Expansion of Quasi-Sovereign Authority

The AML/CFT framework has dramatically expanded NRB’s institutional authority beyond traditional banking supervision into a quasi-sovereign function:

- The Financial Intelligence Unit (FIU-Nepal), established April 2008, operates as a functionally autonomous unit within NRB premises, serving as the national central agency for receiving, analyzing, and disseminating financial intelligence

- The 2023/24 establishment of the Money Laundering Prevention Supervision Division (MLPSD) as an independent division represented what the NRB describes as a “transformational milestone”

- NRB’s supervision now extends beyond traditional banks to remittance companies, Payment Service Providers, and large state-run pension funds

- Nepal’s 2025 FATF grey listing turned NRB’s AML/CFT functions into a “quasi-sovereign mission to restore international confidence”

- Securities Market Participants must submit Suspicious Transaction Reports directly to the FIU (NRB), embedding the entire capital market into NRB’s financial intelligence surveillance

5.5 The Supervisory Evolution: From Compliance to Risk-Based Oversight

NRB’s supervisory philosophy has undergone a fundamental transformation that further strengthens its technocratic authority:

- Pre-2014: Traditional compliance-based “CAMELS” approach – snapshot assessment of legal deviations

- Post-2014: Risk-Based Supervision (RBS) – forward-looking assessment of “chance of failure” and quality of risk management

- Implementation: Supervisory Information System (SIS), an XBRL-based reporting and analytics tool enabling automated, continuous monitoring

- Individual Bank Supervisor (IBS) model: Officers empowered to monitor specific banks continuously as part of the offsite SREP process

The NRB describes this evolution as a shift from periodic regulation to continuous supervisory management. The sector’s compliance culture is characterized by the NRB as “reactive rather than proactive,” with banks “seeking loopholes in regulatory provisions” rather than adopting the “spirit of such provisions” – a characterization that simultaneously critiques the banking sector and justifies ever-deeper regulatory intervention.

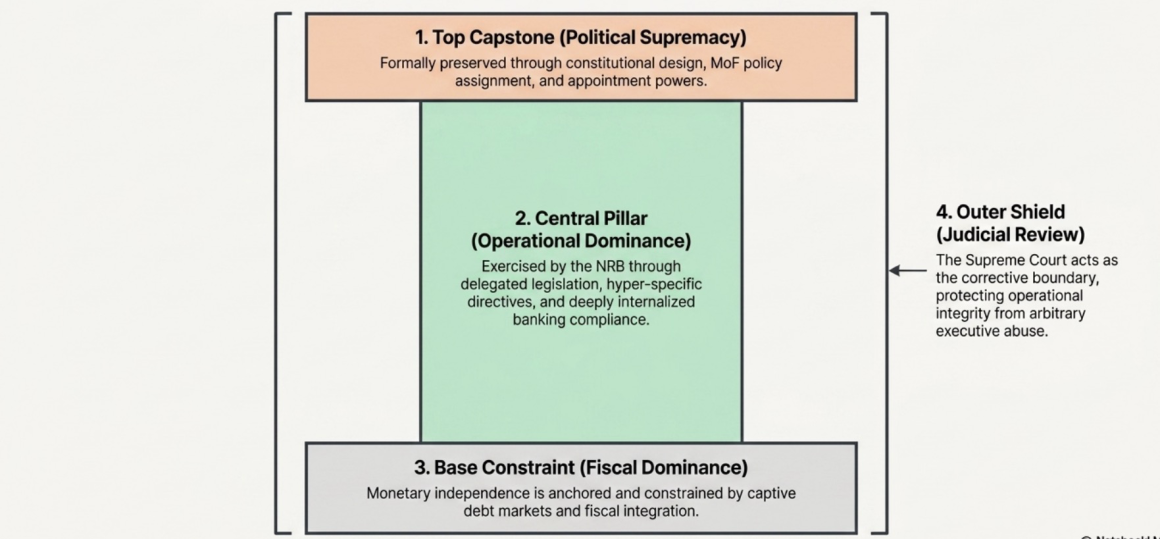

Part VI – Synthesis: Political Supremacy, Technocratic Autonomy, and the Continuum of Central Bank Independence

6.1 The Model: Coordinated Technocratic Dependence

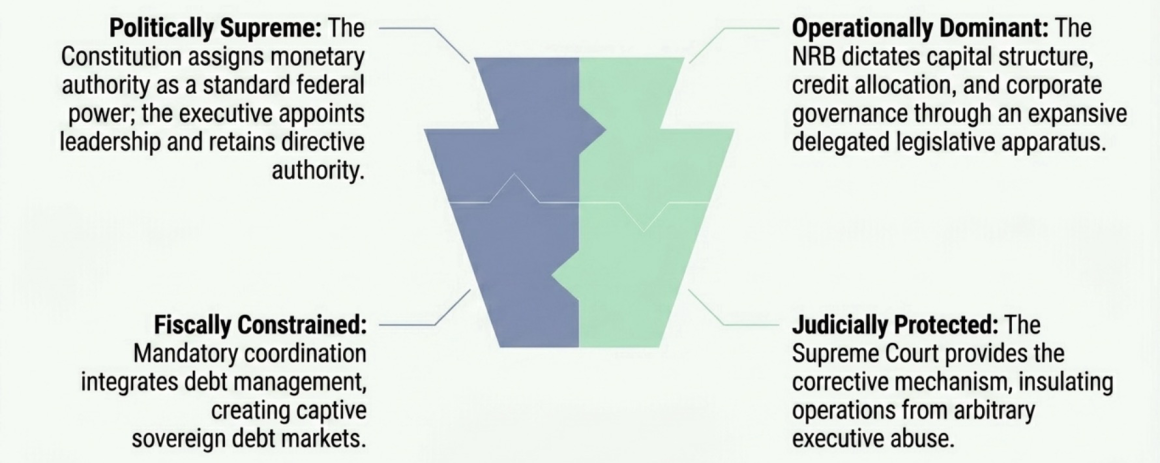

The comprehensive analysis across constitutional law, statutory frameworks, fiscal governance, institutional behavior, and judicial review reveals a governance model that defies simple categorization. Nepal’s NRB is simultaneously:

- Constitutionally subordinate: The Constitution vests monetary authority in the Federation as an ordinary federal power (Schedule-5). The Division of Work Rules assign monetary policy “determination” to the MoF. The NRB enjoys no constitutional body status.

- Statutorily autonomous: The NRB Act, 2058, grants “full authority” over monetary policy, foreign exchange, and banking regulation. It creates an “autonomous corporate body” with legal personality and financial independence.

- Operationally dominant: Through delegated legislation, the NRB exercises quasi-sovereign control over the banking sector – determining credit allocation, capital structures, governance standards, dividend policies, and even the design of internal committees.

- Judicially protected: The Supreme Court has constructed a doctrinal shield around NRB leadership and validated its pre-emptive regulatory powers, while maintaining the ability to intervene when fundamental rights are at stake.

- Fiscally constrained: The NRB remains the government’s fiscal agent, is legally obligated to purchase undersubscribed Treasury Bills, and operates within a fiscal framework where its own prudential regulations (SLR requirements) create captive markets for government debt.

This configuration constitutes what this analysis terms coordinated technocratic dependence – a governance arrangement in which:

- Political supremacy is formally preserved through constitutional design, appointment powers, and government direction authority

- Operational regulatory power is effectively delegated to the central bank through statutory mechanisms and exercised through an expansive directive-making apparatus

- Fiscal coordination constrains monetary independence through debt management integration and captive bank participation in sovereign debt markets

- Judicial review provides the corrective mechanism – protecting institutional integrity from executive abuse while maintaining the ultimate constitutional accountability of all state institutions to democratic governance

6.2 The Political Supremacy Question: A Normative Reflection

A principled argument exists that political supremacy over technocratic institutions is not merely inevitable but desirable in a democratic polity. Central banks are unelected institutions wielding immense economic power – the power to determine the cost of money, the availability of credit, the stability of prices, and the conditions under which citizens can access financial services. Democratic theory suggests that such power must ultimately be accountable to elected representatives.

Nepal’s formal legal architecture reflects this principle. The Constitution’s assignment of monetary authority to the Federation, the MoF’s jurisdiction over monetary policy “determination,” the government’s appointment power over the Governor, and Section 106C’s direction-giving authority all embody the democratic proposition that the people’s elected representatives should retain ultimate control over the institutions that shape economic outcomes.

However, the empirical evidence from Nepal’s own governance experience complicates this normative position:

- The Adhikari case demonstrates that executive control can be weaponized for purposes unrelated to democratic accountability – in this instance, to force the release of funds flagged by international AML authorities

- The Rawal dismissal demonstrated that political removal of central bank leadership can be motivated by patronage rather than policy

- The fiscal dominance dynamic shows that executive control over monetary policy can serve short-term electoral interests at the expense of long-term price stability

- The banking sector evidence reveals that the NRB’s technocratic authority has produced a stable, highly regulated, and increasingly sophisticated financial system – a governance outcome that pure political control demonstrably failed to achieve under the old NRB Act

The Supreme Court’s jurisprudence navigates this tension with considerable sophistication. It does not declare central bank independence to be a constitutional right; it declares that arbitrary executive interference in central bank operations is constitutionally impermissible. The distinction is crucial: political accountability is preserved through appointment powers, legislative oversight, and formal consultation mechanisms; but operational autonomy is protected from capricious, retaliatory, or corruption-driven executive action.

6.3 Comparative Positioning

Nepal’s model of coordinated technocratic dependence occupies a distinctive position in the global landscape:

| Jurisdiction | Model | Key Feature |

| Nepal | Coordinated technocratic dependence | Formal executive supremacy; operational regulatory autonomy; judicial protection from arbitrary interference |

| India | Constitutional deference with empirical proportionality | Supreme Court defers to RBI on macro-policy (Vivek Narayan Sharma, 2023) but requires empirical proof for regulatory bans (IAMAI, 2020) |

| Sri Lanka | Post-crisis autonomy entrenchment | CBSL Act 2023 enacted under IMF conditionality after sovereign default; constitutionality affirmed by Supreme Court |

| Pakistan | Statutory independence under judicial protection | Courts protect SBP from administrative interference; navigate complex intersection with religious law on banking |

| Bangladesh | Political vulnerability with weak judicial protection | Central bank governor vulnerable to political removal (Ahsan Mansur ouster, 2026); TIB highlights political interference |

| United States | Evolving judicial scrutiny | Post-Loper Bright (2024): end of Chevron deference; Federal Reserve exposed to unprecedented retroactive litigation |

| United Kingdom | Extreme deference in crisis | Northern Rock: Court will not intervene unless central bank action “manifestly without reasonable foundation” |

Nepal’s judiciary is more protective of central bank leadership than Bangladesh’s but less doctrinally systematic than India’s. It defers more broadly to preventive risk assessments than India’s proportionality-focused approach but maintains sharper scrutiny of executive procedure than the UK’s extreme deference standard. The absence of constitutional entrenchment for NRB independence places Nepal below Sri Lanka’s post-2023 framework, while the Supreme Court’s active intervention exceeds Pakistan’s more selective judicial engagement.

6.4 The Gap Between Formal and Real Power: The Lassallian Conclusion

The real constitution of financial power in Nepal is not the Constitution’s Schedule-5, not the Division of Work Rules’ Section 2.4, and not the NRB Act’s Section 106C. It is the institutional reality in which:

- No commercial bank publishes financial statements without NRB authorization

- No bank distributes dividends without NRB consent

- No BFI opens a branch, merges, or restructures without NRB approval

- No foreign currency enters or leaves the country without NRB intimation or licensing

- No banking executive takes office without satisfying NRB’s Fit and Proper criteria

- The NRB holds foreign exchange reserves covering 18.1 months of imports – a national wealth stockpile under central bank control

- The banking sector has internalized NRB directives as the “foundational layer of corporate governance” rather than external regulatory constraints

This is the reality of an institution that formally operates under ministerial oversight but functionally exercises quasi-sovereign authority over the financial system. The gap between formal subordination and operational dominance is not a failure of institutional design – it is the defining feature of Nepal’s financial governance. The NRB’s power derives not from constitutional entrenchment but from the indispensability of its technocratic functions in a complex, interconnected financial system that no political actor has the expertise or institutional capacity to manage directly.

The Supreme Court, through its calibrated deference doctrine, has effectively recognized and validated this reality. By protecting NRB leadership from arbitrary removal, upholding its pre-emptive regulatory paradigm, and deferring to its specialized expertise in banking supervision, the judiciary has constructed a de facto judicial constitution of central bank independence that the formal constitutional text does not provide.

What remains is the irreducible tension: an institution that must be operationally autonomous to fulfill its mandate, yet must be politically accountable because it exercises sovereign power over public economic life. Nepal’s current architecture manages this tension not through a clean constitutional settlement but through the continuous, case-by-case contestation between the executive, the central bank, and the judiciary – a contestation that, for all its messiness, has produced a financial governance system of remarkable regulatory depth and institutional resilience.

Key References and Source Documents

Primary Legislation

- Constitution of Nepal, 2072 (2015) – Articles 50, 51, 56-59, 75, 115-119, 207, 230, 234, 241, 251, 279; Schedules 5, 6, 7, 8, 9

- Nepal Rastra Bank Act, 2058 (2002) – Sections 3-5, 9, 14-23, 29-34, 44, 52, 62, 66, 69-70, 74-75, 79, 84, 86C-86I, 88, 92-93, 98-100, 106B-106C, 107, 110-111

- Nepal Rastra Bank Act, 2012 BS (1955) – Sections 4-12, 16-25, 29-30, 33

- Bank and Financial Institutions Act (BAFIA), 2073 (2017) – Sections 3-4, 11, 18-19, 22-23, 31, 33-35, 49-50, 57, 69-70, 73, 77, 99-102, 105, 116, 129/131

- Foreign Exchange (Regulation) Act, 2019 (FERA) – Sections 3-7, 10, 14

- Securities Act, 2063 (2006) – Sections 2-5, 97, 112, 116, 118; Chapter 9

- Companies Act, 2063 – Sections 7-8, 12, 29, 63, 76, 86, 103-105, 108, 111, 126, 139, 164, 177, 182, 186

- Insolvency (Damashai) Act, 2063 – Sections 8, 54-66

- Income Tax Act, 2058 – Sections 14, 24-25, 57, 59; Schedule 1

- Public Debt Management Act, 2079 – Sections 3-8, 14

- Public Debt Management Rules, 2080 – Rules 3, 9, 11-13, 43

- Inter-governmental Fiscal Management Act, 2074 – Sections 6-7, 12, 14, 25, 33

- Banking Offence and Punishment Act, 2064 – Sections 3-14, 18-19

- National Criminal (Code) Act, 2074 – Sections 29-30, 51, 85, 92, 110, 249, 251-252, 256, 265, 276, 285

- National Civil (Code) Act, 2074 – Sections 7-8, 14, 22, 42-44, 46, 50-51, 54-66, 437, 474-480, 488, 492-493, 500, 505, 518, 537, 540, 587-589

- National Criminal Procedure (Code) Act, 2074 – Sections 3-4, 8, 23, 29, 31-32, 56, 65, 99, 102, 163-165, 180, 192, 194

- National Civil Procedure (Code) Act, 2074 – Sections 7, 10, 12, 23, 26, 29, 36, 68, 85, 91, 99, 104, 151, 161, 190-194, 229, 242-244, 266

- Act Restricting Investment Abroad, 2021 (1964) – Sections 2-3

- Foreign Investment and Technology Transfer Act, 2075 – Sections 11-12, 16, 20, 25-26, 32-33

- Government of Nepal (Division of Work) Rules, 2072 (2015) – Schedule-2

NRB Regulatory Instruments

- NRB Unified Directives for Class A, B, C, D, and Infrastructure Banks (2081)

- Capital Adequacy Framework 2015 (Basel III) for Class A Banks

- Capital Adequacy Framework 2018 (Basel III) for NIFRA

- Prompt Corrective Action Bylaw, 2074

- NRB Remittance Bylaw, 2079 (First Amendment)

- Foreign Exchange Transaction Licensing and Inspection Bylaw, 2077

- NRB Money Changer Bylaw, 2077

- Foreign Investment and Foreign Loan Management Bylaw, 2078

- Hedging Rules, 2079

- Loan Information By-rules, 2059

- Internal Control and Monitoring Directive, 2080

- Corporate Governance Guidelines for Listed Companies, 2074 (SEBON)

- Margin Trading Facility Guidelines, 2074 (SEBON)

- Securities Registration and Issue Regulation, 2073 (SEBON)

- Specialized Investment Fund Regulation, 2075 (SEBON)

NRB Institutional Publications

- NRB Annual Reports (multiple years, including 2081-82 Nepali)

- Current Macroeconomic and Financial Situation (CMEs) – Annual series from 2015/16 through 2025/26

- Bank Supervision Reports (including BSD Annual Report 2022-23)

- NRB Financial Stability Reports

- NRB Special Publication: Reflection of Former Governors

Commercial Bank Annual Reports Referenced

- Nabil Bank Limited

- Nepal Investment Mega Bank Ltd (NIMB)

- Nepal SBI Bank Ltd (NSBL)

- Standard Chartered Bank Nepal Limited (SCBNL)

- Himalayan Bank Limited (HBL)

- Everest Bank Limited (EBL)

- Kumari Bank Limited

- Rastriya Banijya Bank Limited (RBB)

- Agricultural Development Bank Limited (ADBL)

- Nepal Bank Limited (NBL)

- NIC Asia Bank

- Prabhu Bank

- Machhapuchchhre Bank (MBL)

- Siddhartha Bank Limited

- Laxmi Sunrise Bank

- NMB Bank

- Prime Bank

Government Fiscal Documents

- PDMO Annual Reports (FY 2080/81, 2081/82)

- Annual Status Review of Public Enterprises (Yellow Book), 2082

- Accounting and Reporting Procedure for Contingent Liabilities of Public Enterprises, 2082

- Share and Loan Investment Policy, 2081

- National Debt Raising Act, 2082 (Bill)

Judicial Decisions and Legal References

- Tilak Rawal v. Government of Nepal (2000) – Reinstatement of Governor; Justices Krishna Jung Rayamajhi and Ganesh Bahadur Singh

- Maha Prasad Adhikari v. Government of Nepal (2022) – Reinstatement of Governor; Justices Sapana Pradhan Malla and Tanka Bahadur Moktan (interlocutory order by Justice Hari Phuyal)

- Sagar Baral v. Nepal Rastra Bank (2022) – Cryptocurrency ban upheld

- Suresh Bahadur Malla v. NRB – BFI management takeover authority affirmed

- Bhubanseswar Ghimire v. CIAA – NRB jurisdiction over BFI governance affirmed; CIAA jurisdiction limited

- Uttam Bahadur Pun v. NRB – Administrative penalties upheld

- NRB v. Laxman Gyawali – Executive dismissal for financial embezzlement upheld

- Bijay Nath Bhattarai (former Governor) – CIAA prosecution; World Bank evidence controversy

- Writ against appointment of Dr. Biswo Nath Poudel – Challenge to gubernatorial appointment under Articles 133(2) and (3)

- Age limit directive challenge – Interim order by CJ Cholendra Shumsher JB Rana staying NRB directive

Comparative International References

- Vivek Narayan Sharma v. Union of India (2023, India) – Demonetization upheld; deference to RBI/Executive

- Internet & Mobile Association of India (IAMAI) v. Reserve Bank of India (2020, India) – RBI crypto ban struck down; empirical proportionality required

- Central Bank of Sri Lanka Act, No. 16 of 2023 and Supreme Court Determinations – Constitutional harmonization of CBSL autonomy

- Loper Bright Enterprises v. Raimondo (2024, US) – Chevron deference overturned

- Corner Post v. Board of Governors of the Federal Reserve System (2024, US) – Expanded statute of limitations for agency challenges

- Northern Rock Nationalization Judicial Review (UK) – Extreme deference standard: “manifestly without reasonable foundation”

- World Bank, Legal and Judicial Environment for Financial Sector in Nepal – A Review (2003)

- IMF/World Bank Joint Debt Sustainability Analysis for Nepal (June 2024)

- FATF/APG Mutual Evaluation frameworks