I. INTRODUCTION AND CONCEPTUAL FOUNDATION

1.1 The Rationale for a Debenture Trustee

When a corporate body raises debt capital from the public by issuing debentures, it creates a legal relationship with potentially thousands of dispersed, passive creditors. These individual debenture holders face three interconnected problems that make direct enforcement of their rights impractical.

The Collective Action Problem: Individual debenture holders lack the incentive, resources, and coordination to monitor the issuer’s compliance with the terms of the debenture. If the issuer defaults, each holder would need to separately hire counsel, file individual claims, and compete for recovery from the same pool of assets. This fragmented enforcement is both economically irrational for small investors and legally chaotic for courts.

Information Asymmetry: The issuing company possesses significantly more information about its financial health, asset values, and operational risks than any individual investor. Without a professional intermediary, debenture holders have no practical mechanism to continuously verify that their investment is secure.

Enforcement Centralization: In the event of default, secured creditors need a single entity with legal authority to seize collateral, conduct public auctions, and distribute recovery proceeds equitably. Without this, the priority regime under insolvency law becomes unworkable in practice.

A Debenture Trustee is the institutional solution to these problems. It is an organized institution that holds the security interest on behalf of all debenture holders, monitors the issuer’s compliance with the terms of the trust deed, and exercises enforcement powers collectively when the issuer defaults.

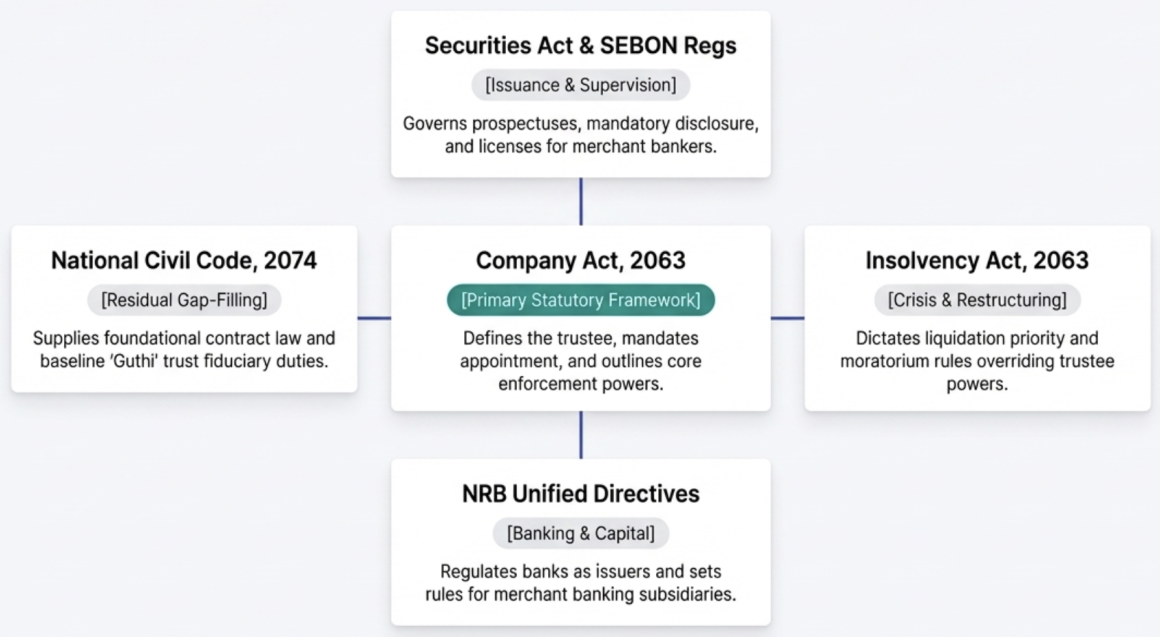

1.2 The Absence of a Unified Trust Act

Nepal does not possess a single, comprehensive “Law of Trust” analogous to the Indian Trusts Act, 1882 or the English Trustee Act, 2000. Instead, the concept of holding property for the benefit of another is fragmented across multiple statutes, each governing a specific domain:

Company Act, 2063, Sections 34–46: Contains the primary statutory framework for the appointment, powers, duties, and enforcement authority of Debenture Trustees. This is the single most important statute for the debenture trustee regime.

Securities Act, 2063 and associated regulations: Govern the issuance process, prospectus requirements, and SEBON’s supervisory authority over debenture issues and the entities involved, including trustees.

Insolvency Act, 2063: Determines the priority of debenture holders in liquidation and restructuring, the effect of moratorium on trustee enforcement, and the trustee’s role in insolvency proceedings.

National Civil (Code) Act, 2074: Provides the foundational private law framework through its Trust (Guthi) provisions in Part 4, Chapter 14 (Sections 314–350), as well as general contract law (Part 5), tort liability (General Principles), and the law of legal persons (Part 1, Chapter 2). These provisions serve a residual, gap-filling role where the special commercial laws are silent.

National Civil Procedure (Code) Act, 2074: Provides the litigation and enforcement framework, including standing requirements, interim relief, evidence standards, and execution procedures that a debenture trustee relies upon in court.

NRB Unified Directives, 2081: Shape the regime indirectly by regulating banks as issuers of debentures, governing merchant banking subsidiaries that may act as trustees, and imposing prudential norms on debenture investments.

II. LEGAL DEFINITION, RECOGNITION, AND STATUTORY BASIS

2.1 Definition under the Company Act, 2063

The Company Act, 2063 provides the most authoritative definition of a Debenture Trustee in Nepalese law. Section 2(t) defines a “Debenture Trustee” (डिबेन्चर ट्रष्टि) means a body corporate undertaking the responsibility for the protection of interests of debenture-holders at the time of issuance of debentures by a company. And Section 2(s) defines “Debenture” means any bond issued by accompany whether putting its assets as collateral or not. The use of the term “organized institution” is significant: it excludes natural persons from serving as debenture trustees and requires the trustee to be a formally incorporated legal entity. This institutional requirement reflects the legislature’s recognition that debenture trusteeship demands the permanence, professional infrastructure, and financial capacity that only a corporate body can provide.

2.2 Recognition under Other Statutes

Income Tax Act, 2058: Section 2(t)Defines “Trust” as an arrangement where a trustee holds property in “Amanat” (अमानत) for another person. The term “Trustee” encompasses liquidators, receivers, and persons managing property for incapacitated individuals. While this definition is primarily for fiscal purposes, it confirms that the concept of holding property for the benefit of another has statutory recognition across Nepalese law beyond the Company Act.

Securities Issue and Allotment Guidelines, 2074: Section 9(4) expressly mandates the appointment of a “Debenture Trustee” (डिबेन्चर ट्रष्टि) and requires that the agreement between the issuer and the trustee contain provisions favorable to investors in accordance with prevailing laws.

Securities Registration and Issue Regulation, 2073: Schedule 5 (अनुसूची–५), which prescribes the format and required contents of the Prospectus (विवरणपत्र), expressly requires the disclosure of the Trust Deed’s principal clauses, including the name, address, and major terms of the agreement between the trustee and the company.

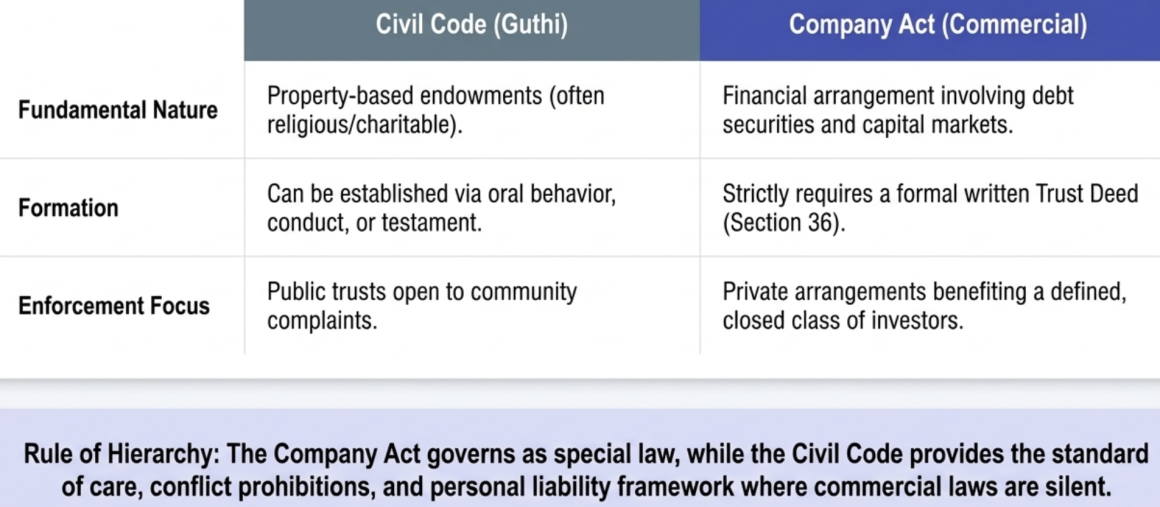

2.3 The Residual Role of the Civil Code’s Trust (Guthi) Provisions

The National Civil (Code) Act, 2074, Part 4, Chapter 6 contains a comprehensive code governing trusts (Guthi). The critical question is whether these provisions apply to a debenture trustee. The answer is nuanced:

Section 3 of the Civil Code establishes a hierarchy: if a special law provides a separate provision for a matter regulated by the Civil Code, the special provision prevails. Since the Company Act, 2063 and the Securities Act, 2063 contain specific provisions for debenture trustees, these special laws govern the primary regime. The Civil Code’s trust provisions apply residually – filling gaps where the special laws are silent.

Section 327(1) of the Civil Code explicitly provides that a body corporate incorporated pursuant to law may be appointed as a trustee (गुठी सञ्चालक). Since debenture trustees must be organized institutions under Company Act Section 14, this provision directly accommodates them within the Guthi framework.

Section 341 of the Civil Code acts as a catch-all provision, stating that a trustee possesses all necessary rights and duties required to protect the interests of the beneficiaries and the trust property, even if such duties are not explicitly detailed in the trust deed. This implied-duties provision is of particular significance for debenture trustees, because the Company Act’s provisions, while robust on powers and enforcement, are often silent on specific monitoring obligations. Section 341 provides the statutory basis for arguing that such duties are inherent in the trustee relationship.

The divergence between the Civil Code’s trust framework and the debenture trustee regime is primarily contextual: the Civil Code’s Guthi provisions were designed for property-based trusts (including religious and charitable endowments), whereas debenture trusteeship is a commercial financial arrangement. Nevertheless, the fundamental fiduciary principles – loyalty, care, separation of assets, prohibition of self-dealing – are identical, making the Civil Code an indispensable supplementary source of law.

III. MANDATORY APPOINTMENT: TIMING, AUTHORITY, AND PROCESS

3.1 Mandatory Nature of Appointment

The appointment of a debenture trustee is mandatory for any public issuance of debentures in Nepal. This mandatory character arises from the combined operation of several provisions:

Company Act, 2063, Section 34(1): A public company may raise loans or issue debentures by keeping its immovable property as security or mortgage, or without any security. However, the subsequent sections (Sections 35–41) establish that a debenture trustee must be appointed and a trust deed must be executed before the debentures can be issued to the public.

Securities Issue and Allotment Guidelines, 2074, Section 9(4): Explicitly mandates that a corporate body issuing debentures must enter into a formal agreement with a Debenture Trustee (डिबेन्चर ट्रष्टि) prior to issuance.

Securities Registration and Issue Regulation, 2073: The regulation requires the disclosure of the Trust Deed’s primary clauses as part of the Prospectus under Schedule 5, rather than the Securities Registration Book under Schedule 3. Specifically, the issuer must clearly disclose the trustee’s name, address, and the principal clauses of the agreement (Trust Deeds) established between the trustee and the company. Without a trustee appointment and an executed trust deed, the issuer cannot fulfill the disclosure requirements for the Prospectus, preventing them from completing the debenture issue process with SEBON. This effectively makes the trustee appointment and trust deed execution a mandatory precondition to regulatory approval.

3.2 Who Appoints the Trustee

The issuer (the corporate body) appoints the debenture trustee. The Securities Issue and Allotment Guidelines, 2074, Section 9(4) specifically frames the relationship as a direct contractual agreement between the “corporate body and the debenture trustee” (सङ्गठित संस्था र डिबेन्चर ट्रष्टि बीच). This creates an inherent structural tension: the trustee, whose primary duty is to protect the debenture holders, is appointed and compensated by the very entity it is meant to monitor. This is a recognized tension in capital markets globally, and its mitigation depends on the independence requirements discussed in Section IV below.

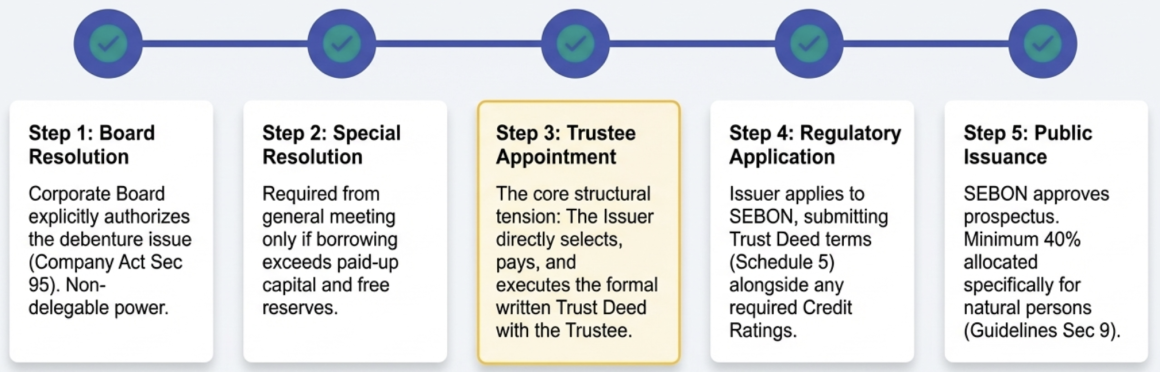

3.3 Timing of Appointment

The trustee must be appointed before the registration and public issuance of the securities. Because the Securities Registration and Issue Regulation, 2073, Schedule 3 requires the fundamental clauses of the Trust Deed to be submitted as part of the Securities Registration Book to SEBON, the trustee relationship must already be formally established at the regulatory application phase. The chronological sequence is:

- The company’s Board of Directors passes a resolution authorizing the debenture issue (Company Act, 2063, Section 95(6));

- if the borrowing exceeds the sum of paid-up capital and free reserves, a special resolution of the general meeting is obtained (Company Act, 2063, Section 105(1)(b));

- the company selects and contracts with a debenture trustee, executing the Trust Deed;

- the company applies to SEBON for registration, submitting the Trust Deed’s principal terms (Securities Registration and Issue Regulation, 2073, Schedule 5(34));

- SEBON approves the prospectus (Securities Act, 2063, Sections 29–31); and

- the debentures are offered to the public.

3.4 Corporate Approvals Required

Board Resolution: Under Company Act, 2063, Section 95(6), the power to issue debentures and raise loans is vested in the Board of Directors. This is expressly a non-delegable power; it must be exercised through a resolution passed at a board meeting and cannot be delegated to a sub-committee or an individual officer.

Special Resolution for Excess Borrowing: Under Company Act, 2063, Section 105(1)(b), if the company intends to borrow an amount that exceeds the total of its paid-up capital and free reserves, a special resolution from the general meeting is required. This limitation does not apply to short-term loans (less than six months) taken for the company’s regular business from banks or financial institutions.

Regulatory Approval: Under Securities Act, 2063, Section 29, an organized institution is absolutely prohibited from issuing securities to the public without first officially registering those securities with SEBON. The prospectus must be submitted to, scrutinized, and explicitly approved by SEBON prior to the public offering (Securities Act, 2063, Sections 30–31).

Credit Rating Regulation, 2068: For specific types of debt issuances, Section 3(1)(b) requires the corporate body to secure a credit rating from a credit rating agency prior to the public issuance of debentures and other debt securities. Furthermore, Section 3(2) expressly mandates that this credit rating must be disclosed in the offer document, prospectus (विवरणपत्र), and other publicly published documents before the securities are issued to the public.

IV. QUALIFICATIONS, ELIGIBILITY, AND INDEPENDENCE

4.1 Eligibility Requirements under Existing Law

The Company Act, 2063, Section 2(t) establishes that a debenture trustee must be an “organized institution.” Beyond this institutional requirement, the Act does not prescribe a detailed standalone licensing regime, fit-and-proper criteria, or minimum capital requirements specific to debenture trustees.

Regulatory Gap: Nepal lacks a dedicated Debenture Trustee Regulation prescribing specific licensing criteria, minimum capital requirements, infrastructure standards, or fit-and-proper tests for entities seeking to act as debenture trustees. The Securities Board of Nepal (SEBON) has not issued a separate set of regulations comparable to India’s SEBI (Debenture Trustees) Regulations, 1993.

In practice, the role is performed by entities licensed under SEBON as Merchant Bankers (मर्चेन्ट बैंकर). The Securities Businessperson (Merchant Banker) Regulation, 2064 establishes licensing requirements for these entities, including paid-up capital thresholds, infrastructure requirements, and management qualifications. Additionally, NRB Unified Directive 8/081, Section 4.2 permits banks to establish Merchant Banking Subsidiaries (with at least 51% bank ownership) that are authorized by SEBON to provide services including debenture trusteeship.

Comparative Reference: Under India’s SEBI (Debenture Trustees) Regulations, 1993, no person can act as a debenture trustee unless they hold a certificate of registration from SEBI. The regulations prescribe a minimum net worth of INR 5 crore, require the applicant to be a scheduled bank, public financial institution, insurance company, or a body corporate, and mandate the submission of detailed information about infrastructure, personnel qualifications, and past compliance history. This level of specificity is absent from the Nepalese framework.

4.2 Independence Requirements

The Company Act, 2063 does not contain an express provision mandating the independence of the debenture trustee from the issuer. However, the fiduciary nature of the role inherently demands independence, and several analogous provisions in Nepalese securities law establish this principle:

Mutual Fund Regulation, 2067, Rule 10: Mandates that there must be absolutely no conflict of interest (स्वार्थ बाझिन नहुने) between the Fund Sponsor, the Fund Supervisor, the Fund Manager, and the Depository.

Portfolio Management Guidelines, 2067, Section 6(1): Strictly prohibits portfolio managers from engaging in any transactions where their own personal interests, or the interests of their founding institutional shareholders, clash with the interests of their clients.

Credit Rating Regulation, 2068, Rules 34(1) and 34(2): Forbids a rating agency from rating a company if the agency holds fundamental shares in that company, or vice versa. Rule 34(3)(ख) requires disclosure of any “associate” relationship.

NRB Unified Directive 6/081: Under NRB Unified Directive 6/081, Section 1(2)(ख), directors are prohibited from direct or indirect involvement in transactions where they have a financial interest, and such interest in a customer can render a director ineligible to hold office. Furthermore, when a bank operates a merchant banking subsidiary, Directive 8/081, Section 4(2)(ङ) mandates that transactions between the parent and subsidiary be disclosed as ‘Related Party Transactions’ due to the inherent financial interest, and Directive 4/081, Section 5.7 requires comprehensive disclosure of these relationships in financial statements to ensure governance and transparency.

Regulatory Gap: There is no explicit statutory provision prohibiting a debenture trustee from being a subsidiary, affiliate, or associate of the issuer, the issue manager, or the underwriter. Nor is there a provision requiring the trustee to disclose and manage conflicts of interest specific to the debenture trustee role. The independence safeguards must currently be inferred from analogous provisions governing other fiduciary roles.

Comparative Reference: India’s SEBI (Debenture Trustees) Regulations, 1993, Regulation 7 explicitly prohibits a debenture trustee from being a promoter, member of the promoter group, or having any pecuniary relationship with the issuer that may affect the exercise of its duties. The trustee must also not be an associate or subsidiary of the issuer. English law under the Trustee Act 2000 imposes a “no-conflict” rule as an inherent fiduciary obligation, breach of which renders the trustee personally liable regardless of contractual exclusions.

V. THE TRUST DEED: FORMATION, CONTENT, AND LEGAL CHARACTER

5.1 Mandatory Written Agreement

Under Company Act, 2063, Section 36(1), a debenture trustee cannot act without an express written agreement. This Trust Deed is the foundational legal document that defines the trustee’s rights, duties, powers, and the specific terms of the debenture. The requirement for a written agreement is absolute – unlike the general trust provisions of the Civil Code, which recognize trusts established through oral behavior or conduct (Section 316(3)), a debenture trustee arrangement requires formal documentation.

5.2 Essential Contents of the Trust Deed

Company Act, 2063, Section 36(2) prescribes the following mandatory contents of the Trust Deed:

(a) The specific assets kept as security or mortgage for the debenture;

(b) The time period, rate of interest, and the specific procedure for the payment of principal and interest;

(c) The trustee’s right to conduct property valuations, project analyses, and management audits to evaluate the company’s capacity to fulfill its obligations;

(d) The trustee’s power to take possession of the company’s assets upon default;

(e) The trustee’s right to review the company’s balance sheets and auditor reports before entering the agreement to verify asset adequacy.

Additionally, the Securities Issue and Allotment Guidelines, 2074, Section 9(4) mandates that the agreement between the corporate body and the debenture trustee must contain provisions that are “favorable to the investors” (लगानीकर्ताको हित अनुकूलका प्रावधान) in accordance with prevailing laws. This provision serves as both a substantive standard and a regulatory backstop: any Trust Deed clause that is demonstrably unfavorable to investors could be challenged as being in violation of this statutory mandate.

5.3 Public Disclosure of Trust Deed Terms

Securities Registration and Issue Regulation, 2073: When a corporate body issues debentures, it is expressly required to publicly disclose the name and address of the Trustee, as well as the key terms and conditions of the Trust Deed executed between the trustee and the company. This disclosure is mandated by Schedule 5 (अनुसूची–५) as a required component of the Prospectus (विवरणपत्र). This comprehensive disclosure in the Prospectus ensures that SEBON, during the approval process, and the public, during the issuance, are fully informed of the protective arrangements before investors commit their capital.

5.4 Contractual Character under Civil Law

From a civil law perspective, the Trust Deed functions simultaneously as a contract and a trust instrument. Under the National Civil (Code) Act, 2074, Section 504(1), a contract is an agreement between two or more parties for performing or not performing any act which is enforceable by law. The Trust Deed satisfies all essential elements of a valid contract: competent parties (the issuer and the trustee), lawful consideration (the trustee’s fees), a lawful object (protection of investor interests), and free consent. Concurrently, it operates as a trust deed within the meaning of Section 317 of the Civil Code, which requires the trust instrument to specify the trust property, objectives, beneficiaries, the trustee’s functions, and the method of use.

This dual character means that the Trust Deed is governed by both the specific provisions of the Company Act (as the special law) and the residual principles of contract law and trust law under the Civil Code (as the general law, per Section 3 of the Civil Code). In case of conflict, the Company Act prevails; where the Company Act is silent, the Civil Code fills the gap.

VI. POWERS OF THE DEBENTURE TRUSTEE

6.1 Information and Monitoring Powers

Company Act, 2063, Section 38: The company is obligated to submit financial reports to the trustee every six months, notify the trustee within seven days if there is any change in the company’s management or ownership structure, and provide any additional information or documents requested by the trustee. This information right is not merely passive; it empowers the trustee to demand specific data at any time, creating a continuous monitoring mechanism.

Company Act, 2063, Section 36(2): The Trust Deed must grant the trustee the right to conduct property valuations, project analyses, and management audits to evaluate whether the company can fulfill its obligations. This pre-contractual and ongoing due diligence right is the trustee’s primary tool for addressing information asymmetry.

6.2 Enforcement Powers upon Default

Company Act, 2063, Section 39(1): Upon the issuer’s failure to comply with the Trust Deed, the trustee can issue a formal demand requiring the company to fulfill its obligations within a specified timeframe, including the immediate return of the principal and interest (acceleration of debt).

Company Act, 2063, Section 39(2): If the company defaults, the trustee is legally empowered to take possession of the company’s mortgaged property or assets and sell them through a public auction or any other appropriate method to recover the debt on behalf of the debenture holders. This is a statutory “self-help remedy” that permits the trustee to act without first obtaining a court order, subject to the terms of the Trust Deed.

6.3 Litigation Powers

Company Act, 2063, Section 41(2): The trustee is explicitly granted the right to initiate legal actions (claims) for the recovery of the principal and interest on behalf of the debenture holders. This statutory standing allows the trustee to sue the issuer in its own name without requiring separate authorization from each individual holder, thereby solving the collective action problem.

Company Act, 2063, Section 41(1): If the company is liquidated or falls into insolvency, the Debenture Trustee is legally empowered to represent the debenture holders in all proceedings.

The trustee’s litigation powers are reinforced by the Civil Code. Section 334(1) of the National Civil (Code) Act, 2074 mandates the trustee to take “any kind of legal action” and fulfill requirements before public authorities to maintain and protect trust property. Section 42(7) confirms that a body corporate may “sue or initiate other legal action” in its own name.

6.4 Power to Register Security

Company Act, 2063, Section 36(3): The Debenture Trustee is authorized to have the company’s property registered as security in its own name. This is a critical structural power: by holding the registered charge in its own name, the trustee becomes the legal holder of the security interest, not merely its representative. This ensures that the security cannot be released or modified without the trustee’s participation, and it simplifies enforcement in insolvency proceedings.

6.5 Implied Powers under the Civil Code

Where the Company Act is silent on a specific power, the National Civil (Code) Act, 2074, Section 341 provides that a trustee possesses all necessary rights and duties required to protect the interests of the beneficiaries and the trust property, even if not explicitly detailed in the trust deed. This catch-all provision expands the trustee’s authority to include any reasonable action necessary for investor protection, subject to the overriding requirements of good faith and the objects of the trust.

VII. DUTIES AND MONITORING OBLIGATIONS

7.1 Core Fiduciary Duties

While the Company Act, 2063 does not use the phrase “fiduciary duty” as a defined legal term, the Act and subsidiary regulations impose substantive fiduciary standards on the debenture trustee:

Duty of Loyalty and Good Faith: The trustee must act solely in the interest of the debenture holders. This duty is derived from the Company Act’s mandate (Section 99(4)) requiring officers to act loyally, and reinforced by the Civil Code’s prohibition on self-dealing (Section 342(1)(a) and (b)), which bars trustees from using trust property for personal use or for the profit of themselves or others outside the trust’s objectives.

Duty of Care and Prudence: The National Civil (Code) Act, 2074, Section 334(2) requires a trustee to manage, protect, and maintain trust property with the same “proper and reasonable care” as if it were their own property. Section 323(5) and (6) further require prudence in investment decisions, authorizing the trustee to monitor markets and seek expert opinions to ensure maximum returns and sustainability.

Prohibition on Conflicts of Interest: The Civil Code, Section 342(2) specifically prohibits financial transactions between the trustee’s private property and the trust property. Section 342(3) prohibits mixing private and trust property. The Portfolio Management Guidelines, 2067, Section 6 (applied by analogy) reinforces this by prohibiting transactions where the fiduciary’s personal interests conflict with client interests.

7.2 Specific Monitoring Obligations

Receipt of Financial Reports: Under Company Act, 2063, Section 38, the company must submit financial reports to the trustee every six months. The trustee is thereby empowered to conduct ongoing financial analysis of the issuer.

Notice of Management Changes: Under Company Act, 2063, Section 38, the company must notify the trustee within seven days of any change in management or ownership structure.

Pre-contractual Due Diligence: Under Section 36(4), the Trust Deed must grant the trustee the right to carry out the calculation of property or assets to taken as security and the project analysis of management analysis of the company.

7.3 Monitoring Gaps: Where the Law Is Silent

Despite the robust general framework, several critical monitoring obligations that are standard in international debenture trust practice are not explicitly prescribed in the Nepalese statutory framework:

7.3.1 Monitoring Use of Proceeds

Securities Registration and Issue Regulation, 2073: The regulation mandates under Schedule 5 that the issuer must detail the particulars of the debenture issue within the Prospectus, which includes disclosing the objective of the issue and the specific project to be funded. However, there is no statutory provision expressly directing the debenture trustee to independently monitor the ongoing expenditure of proceeds to verify that funds are used for the stated purposes. Such a specific monitoring mechanism would need to be contractually established within the Trust Deed.

Regulatory Gap: No statutory obligation on the debenture trustee to monitor the use of proceeds. This leaves a significant risk that issuers may divert funds to purposes other than those disclosed in the prospectus, without any institutional check. The risk of issuers diverting funds is currently mitigated by mandatory, detailed prospectus commitments regarding capital utilization, ongoing financial reporting requirements, SEBON’s statutory power to conduct onsite inspections, and the contractual monitoring rights that must be embedded within the Trust Deed to protect investors.

Comparative Reference: Under SEBI (Debenture Trustees) Regulations, 1993, Regulation 15(1)(f), the debenture trustee is specifically required to “ensure that the borrower company utilizes the money raised by issue of debentures for the purposes stated in the offer document.”

7.3.2 Monitoring Financial Covenants

The Securities Issue and Allotment Guidelines, 2074, Section 9(3) mandates that the issuer maintain a Redeemable Debenture Reserve Fund (रिडिमेबल डिबेन्चर रिजर्भ फण्ड) to ensure eventual repayment. NRB Unified Directive 16/081 further requires BFIs to establish a Capital Redemption Reserve with proportionate annual funding. However, no provision assigns the duty to the debenture trustee to audit or continuously monitor the health of these reserves.

Regulatory Gap: No explicit statutory duty on the debenture trustee to monitor compliance with financial covenants, including the adequacy of the Debenture Redemption Reserve. But this could be mitigated by contractually establishing such requirement within the Trust Deed.

7.3.3 Monitoring Security Creation and Perfection

The Securities Issue and Allotment Guidelines, 2074, Section 9(2) requires the independent valuation of collateral by an expert, and Section 9(5) caps debt at 50% of net assets for debentures with secondary rights. However, once the charge is created, there is no express statutory obligation on the debenture trustee to continuously monitor the value and legal perfection of the security.

Regulatory Gap: There is no ongoing statutory duty in the prevailing securities laws directing the trustee to monitor asset coverage ratios or verify continued perfection of the charge over the life of the debenture. Such protective mechanisms rely entirely on the contractual provisions drafted into the Trust Deed.

7.3.4 Pre-Allotment Compliance Verification

Responsibilities for pre-allotment compliance are directed toward the Issue and Sales Manager (निष्काशन तथा बिक्री प्रबन्धक), not the debenture trustee.

Regulatory Gap: No explicit role for the debenture trustee in verifying compliance with issue conditions before allotment.

VIII. SECURITY CREATION, CHARGE REGISTRATION, AND PERFECTION

8.1 Secured versus Unsecured Debentures

The law does not prohibit the issuance of uncollateralized debentures to the general public.

Securities Issue and Allotment Guidelines, 2074: The guidelines establish explicit capital protections and public allocation requirements for debentures. Under Section 9(5), if an issuer creates a secondary charge on its assets (द्वितीय हक) for the debentures, the total issued debt is strictly capped at 50% of the company’s net assets. However, the proviso to Section 9(5) creates an exception: in conditions prescribed by the regulatory body, Banks and Financial Institutions (BFIs) may issue debentures up to 100 percent of their prevailing primary capital or net assets.

Furthermore, to ensure public participation, Section 9(7) mandates that the corporate body must allocate at least 40% of the total issued debentures specifically for sale and distribution to natural persons. The proviso to this section adds a practical fallback, stating that if these allocated debentures are not purchased by natural persons within the specified timeframe, they may then be sold to other buyers.

8.2 Creation of Charge in Favor of the Trustee

Company Act, 2063, Section 36: The Trust Deed must specify the assets kept as security. The trustee is the named holder of the charge.

Company Act, 2063, Section 36(3): The Trustee is authorized to have the company’s property registered as security in its own name according to prevailing law. This registration gives the trustee legal title to the security interest, distinguishing it from a mere contractual right.

Securities Issue and Allotment Guidelines, 2074: Under Section 9(2), if an issuer is issuing secured debentures, the underlying assets used as collateral must be independently evaluated by a relevant expert prior to issuance. However, there is no explicit statutory provision in these guidelines that mandates the Issue and Sales Manager to withhold the allotment of debentures until the formal legal charge (दृष्टिबन्धक वा धितोपास) has been officially executed and registered in the name of the Debenture Trustee. Any such strict precondition for allotment would need to be enforced through contractual mechanisms rather than direct statutory securities rules.

Securities Issue and Allotment Guidelines, 2074, Section 9(2): The underlying assets used as collateral must be independently evaluated by a relevant expert prior to issuance.

8.3 Subsequent Charges

Company Act, 2063, Section 34(2): A company may create a second or subsequent charge on the same assets, provided that the details of the prior charges and the debts they secure are clearly disclosed. This disclosure requirement protects existing debenture holders by ensuring transparency regarding competing claims on the same assets.

8.4 Registration Requirements and Consequences of Failure

Company Act, 2063, Section 51: The company must submit a record of all debentures and loans to the Office of the Company Registrar (OCR) annually, within 30 days of the Annual General Meeting.

Consequences of Failure: If a company or its officers fail to report borrowings or register charges as required, they face personal fines under Section 81 (graduated based on the company’s capital) and potential criminal penalties under Sections 160, 161, and 162 of the Company Act.

8.5 The Trustee as Holder versus Representative

The Nepalese framework makes the trustee both the legal holder of the security interest and the collective representative of the debenture holders. Under Section 36(3) of the Companies Act, 2063, the charge is registered in the trustee’s own name – making the trustee the legal owner of the security right. Simultaneously, under Section 41, the trustee represents the debenture holders in proceedings, making it the representative of the beneficial owners. This dual capacity is essential: it ensures that enforcement can proceed through a single entity while the economic benefits flow to the dispersed investors.

IX. DEFAULT, ENFORCEMENT, AND REMEDIES

9.1 Default Detection

The Company Act, 2063 does not prescribe a specific statutory mechanism for default detection by the trustee. Instead, the trustee’s ability to detect default relies on:

- The six-monthly financial reports the company must provide under Section 38;

- the seven-day notice of management or ownership changes under Section 38;

- the trustee’s contractual right under the Trust Deed (Section 36(2)) to demand additional information, conduct property valuations, and perform management audits; and

- the implied duty under Civil Code Section 341 to take all necessary actions to protect beneficiary interests.

Regulatory Gap: No prescribed default-detection protocol or statutory trigger events (such as missed payments, breach of asset coverage ratios, or adverse credit rating actions) that would automatically obligate the trustee to investigate and report.

Comparative Reference: Under SEBI (Debenture Trustees) Regulations, 1993, Regulation 15(1)(e), the trustee is required to take possession of trust property in accordance with the provisions of the trust deed and to take appropriate measures for protecting the interest of the debenture holders as soon as the debentures become due.

9.2 Enforcement Mechanisms

9.2.1 Demand for Repayment and Acceleration

Company Act, 2063, Section 39(1): The trustee can demand the immediate return of the principal and interest if the company fails to comply with the Trust Deed. This constitutes a statutory acceleration right, converting the future stream of payments into an immediately due lump sum obligation.

The contractual basis for acceleration is further supported by the National Civil (Code) Act, 2074, Section 535(1), which establishes that a breach occurs when a party fails to fulfill a duty, provides notice of non-performance, or behaves in a manner demonstrating inability to perform. Section 564 requires a notice to the debtor before making a claim.

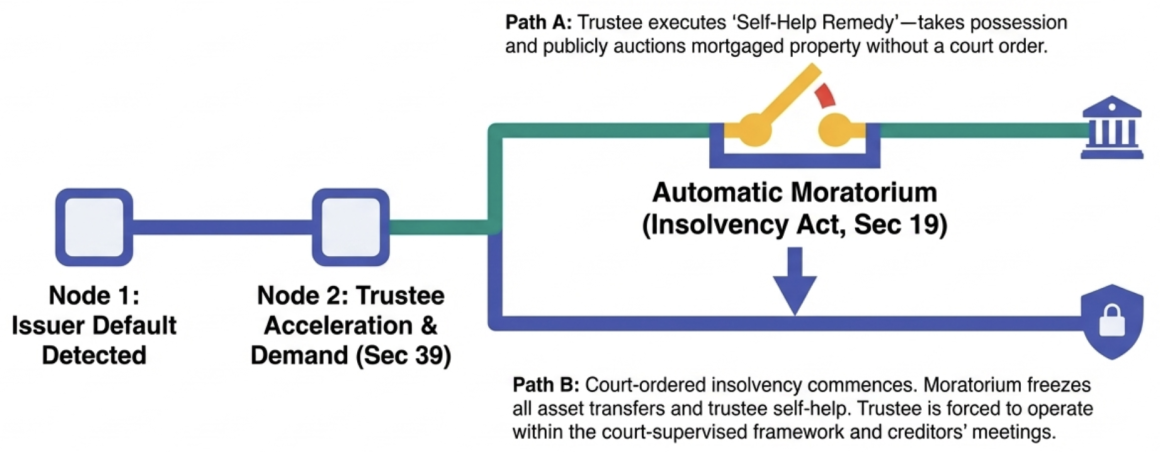

9.2.2 Self-Help Remedy: Possession and Sale

Company Act, 2063, Section 39(2): This is the trustee’s most powerful statutory remedy. Upon default, the trustee is legally empowered to take possession of the company’s mortgaged property or assets and sell them through a public auction or any other appropriate method to recover the debt. This self-help remedy can be exercised without first obtaining a court order, subject to the terms of the Trust Deed and the general requirements of due process.

9.2.3 Civil Court Remedies

Where self-help is inadequate or contested, the trustee may invoke civil court remedies under the National Civil Procedure (Code) Act, 2074:

Specific Performance: Under Civil Code Section 540, if cash compensation is inadequate, the trustee can claim specific performance of the contractual obligations.

Injunctions: Under Procedure Code Section 70(1)(g), the trustee can seek an order restraining the issuer from disposing of assets or compelling the issuer to perform specific acts.

Interim Orders: Under Procedure Code Section 158(2)(d), the court may issue an interim order to maintain the status quo of the subject matter pending final resolution.

Interlocutory Orders: Under Procedure Code Section 156, the trustee can seek immediate preventive orders to preserve the effectiveness of the eventual judgment.

Asset Freezing: Under Procedure Code Section 238 (Possession) and Section 242 (Claimed Amount Recovery), the trustee can seek the auction of property or freezing of assets if the judgment debtor fails to pay within 35 days.

9.3 Enforcement without Individual Consent

Company Act, 2063, Section 41(2): The trustee is authorized to initiate litigation or legal proceedings for the recovery of principal and interest on behalf of all holders without requiring separate, individual consent for each legal action. This is the statutory embodiment of the collective action principle: the trustee acts for the class, not for individual members.

9.4 Trustee’s Standing in Civil Proceedings

The trustee’s standing in court is established through multiple provisions:

Under the National Civil Procedure (Code) Act, 2074, Section 10, any person with a “lawful interest or concern” may file a plaint. Section 93(1) requires that a plaint filed on behalf of a body corporate be accompanied by a copy of the board resolution authorizing a specific natural person to represent the entity. The trustee must present the Trust Deed (evidencing authority), the board resolution, SEBON license (if applicable), the registration of charge (proving security interest), and the debenture certificates (evidencing the underlying debt) to establish its authority before the court.

X. INSOLVENCY, LIQUIDATION, AND RESTRUCTURING

10.1 Status of Debenture Holders in Liquidation

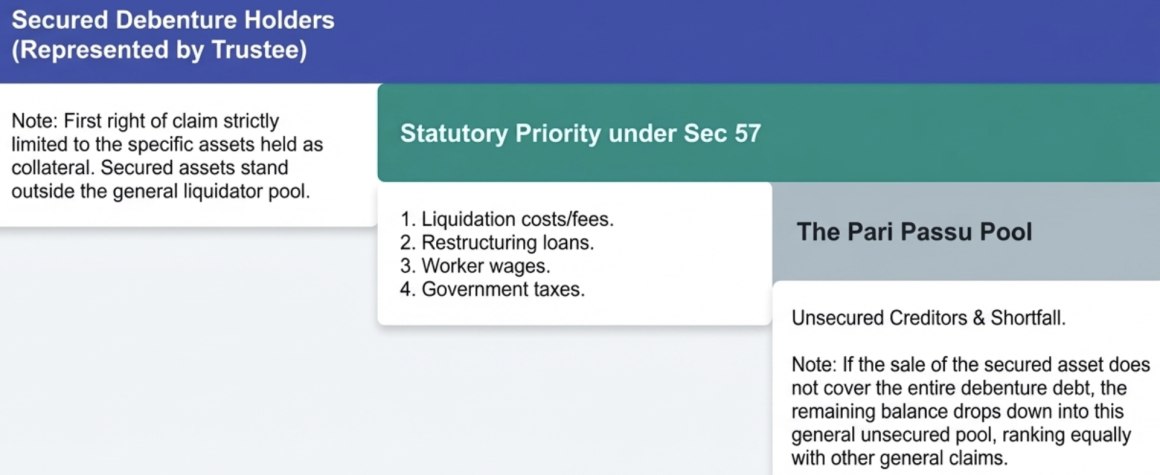

In winding-up or liquidation, debenture holders are treated as creditors of the company, distinct from shareholders. Under Company Act, 2063, Section 34, their claims are satisfied from the company’s assets before any distribution is made to shareholders. If the debentures are secured, they have a specific claim against the charged assets. Secured debenture holders generally stand outside the general pool of assets available to the liquidator: the liquidator has no right over assets specifically mortgaged or charged to a secured creditor.

10.2 Insolvency Hierarchy

Under the Insolvency Act, 2063, Section 57, the priority for distribution of the debtor’s assets is:

(a) Costs of the insolvency proceedings and the liquidator’s fees; (b) loans taken during the investigation or restructuring period; (c) wages and remuneration of workers (excluding directors); (d) leave, provident fund, and gratuity of workers; (e) other accepted unsecured claims.

Secured creditors, including debenture holders represented by the trustee, are first in the hierarchy for the specific assets they hold as collateral. If the sale of the secured asset does not cover the entire debt, the remaining balance is treated as an unsecured claim and ranks pari passu with other general unsecured creditors.

This hierarchy is reinforced by the National Civil (Code) Act, 2074, Section 61, which establishes the priority order for bankruptcy proceedings: costs of proceedings, secured creditors (to the extent of their pledge or mortgage), government taxes and fines, and then unsecured creditors.

10.3 Automatic Moratorium

Insolvency Act, 2063, Section 19: Upon the court’s order to commence insolvency proceedings, an automatic moratorium is triggered that stays: (a) the transfer or sale of company assets; (b) the enforcement of mortgages or security interests by creditors; and (c) the commencement or continuation of any other legal proceedings against the company.

This moratorium overrides the contractual self-help remedies in the Trust Deed. While Company Act Section 39(2) and the Trust Deed may grant the trustee the power to immediately seize and sell assets upon default, Section 19 of the Insolvency Act suspends these rights once formal insolvency proceedings begin. The trustee must then operate within the court-supervised framework.

10.4 The Trustee’s Role in Insolvency Proceedings

Collective Representation: Under Company Act, 2063, Section 41(1), when the company is liquidated or falls into insolvency, the Debenture Trustee represents all debenture holders in proceedings. Section 41(2) grants the trustee the right to file claims for recovery of principal and interest on behalf of the holders.

Participation in Restructuring: Under Insolvency Act, 2063, Section 24, the trustee (on behalf of holders) participates in the Creditors’ Meeting and votes on the Restructuring Program. The trustee evaluates whether the proposed resolution plan is more beneficial than immediate liquidation and ensures adequate protection for the secured assets.

10.5 Separation of Trust-Held Security from Company Assets

Company Act, 2063, Section 136(8): Provides a critical protection: if a company is struck off the register, any property held by the company as a Trustee for another person does not pass to the shareholders or owners – it remains subject to the trust. This provision ensures that trust property maintains its protected status even in the most extreme circumstances of corporate dissolution.

XI. DEBENTURE HOLDER MEETINGS AND COLLECTIVE DECISION-MAKING

The Nepalese statutory framework does not contain specific procedural rules for convening debenture holders’ meetings, prescribing quorum requirements, or establishing voting thresholds. These mechanics are left entirely to the Trust Deed and general corporate law.

Regulatory Gap: There is no statutory framework for debenture holder meetings comparable to the detailed provisions governing shareholders’ general meetings under the Company Act, 2063. The absence of prescribed rules for convening, quorum, voting, and majority binding creates significant uncertainty about collective decision-making by debenture holders.

11.1 Current Practice (Contractual Framework)

In current Nepalese practice, the Trust Deed typically provides for the following mechanisms (based on standard capital market practice rather than statutory mandate):

Convening: Meetings may be convened by the trustee (when instructions from holders are needed), by the issuer (when proposing term modifications), or by requisition of a specified minimum threshold of debenture holders.

Quorum: Typically set at holders representing 25% to 33% of outstanding debt for ordinary business, with higher thresholds for fundamental changes.

Voting: Voting power is calculated pro-rata based on the principal amount held, not “one person, one vote.” Ordinary resolutions require a simple majority; major structural modifications require a supermajority (typically 75%).

Majority Binding the Minority: Resolutions passed by the required majority bind all holders, including those who voted against and those who did not attend. This prevents holdout problems.

11.2 Trustee Acting without Instructions

In standard practice, the trustee may take routine protective actions (issuing default notices, demanding rectification, initiating standard legal proceedings) without consulting the holders. For consequential decisions – such as waiving an event of default, agreeing to restructuring, or releasing collateral – the trustee generally must seek a formal resolution from the holders.

11.3 Compelling Trustee Action

Trust Deeds typically provide that if a specified threshold of holders (e.g., 25% or more of outstanding principal) issues a written directive to the trustee, the trustee is legally compelled to act. However, as a standard prerequisite, the trustee has the right to demand an indemnity from the directing holders to cover potential legal costs and liabilities.

Comparative Reference: India’s Companies Act, 2013, Section 71(7) read with the Companies (Share Capital and Debentures) Rules, 2014, Rule 18(2), prescribes detailed procedural requirements for debenture trustee meetings, including notice periods, quorum, and the requirement for debenture trustees to call meetings within specified timeframes upon the occurrence of default events. The English law position under the Companies Act 2006, Section 754 similarly provides a statutory framework for debenture holders’ meetings.

XII. LIABILITY, REMOVAL, AND REPLACEMENT OF THE TRUSTEE

12.1 Liability for Breach of Duty

12.1.1 Criminal Liability under the Securities Act

Securities Act, 2063, Sections 94 and 98: Classify the creation of artificial markets, giving false information to manipulate prices, and making false or misleading statements to induce securities transactions as punishable offenses.

Securities Act, 2063, Section 101(2): Offenses related to false trading or price manipulation attract fines of NPR 50,000 to NPR 150,000, or imprisonment for up to one year, or both.

Securities Act, 2063, Section 101(3): For severe deceptive practices and fraudulent statements, fines range from NPR 100,000 to NPR 300,000, or imprisonment for up to two years, or both. The offender must additionally compensate the aggrieved party.

12.1.2 Criminal Liability under the Company Act

Company Act, 2063, Section 163: Any party (company, shareholder, or creditor) that suffers a loss due to unauthorized acts by a trustee or its officers can claim compensation from the responsible individual’s personal assets.

Company Act, 2063, Section 160(s): Prescribes fines of NPR 20,000 to NPR 50,000 or imprisonment for up to two years for trustees who act against the interests of debenture holders.

12.1.3 Civil Liability under the Civil Code

National Civil (Code) Act, 2074, Section 51 (Proviso): If a loss is caused by an act done beyond the objectives or competency of the legal person, or done dishonestly, the director or person performing that act shall be personally liable for the loss or damage. This pierces the corporate veil of the trustee institution.

Section 338(1) (Trust Breach): A failure to discharge duties under the Act or the trust deed constitutes a “Guthi Violation.” Under Section 338(3), the trustee must restore any income or advantage the beneficiary would have received had the breach not occurred. Under Section 338(4), if there are multiple trustees, they bear collective and joint liability.

Section 8(1) (General Tort Liability): A person who causes loss or damage by committing a wrong shall bear the liability and pay compensation. Section 266 provides the framework for calculating damages based on actual loss, loss of income, and additional consequential losses.

12.2 Standard of Care

The standard is the “prudent person” standard derived from the Civil Code. Section 334(2) requires management with “proper and reasonable care” as the trustee would apply to their own property. Section 323(1) requires the trustee to exercise competency and discretion “honestly.” The Securities Issue and Allotment Guidelines, 2074, Section 9(4) adds a statutory overlay: the agreement between the corporate body and the debenture trustee must contain provisions that serve the “favorable interests of the investors”. This sets a substantive benchmark against which trustee conduct and the terms of the Trust Deed are measured.

12.3 Trustee Not a Guarantor

The debenture trustee is not a guarantor of the issuer’s debt. If the issuing company defaults due to poor business performance or market conditions, the trustee does not have to pay the investors from its own funds. The trustee is only liable if the loss was exacerbated by the trustee’s own failure to perform its mandated duties – such as failing to register a lien, failing to initiate foreclosure promptly, or colluding with the issuer.

12.4 Limitation-of-Liability and Indemnity Clauses

The Civil Code places limits on contractual exclusions of liability. Section 7 provides that any act contrary to law is invalid. Therefore, a Trust Deed clause attempting to exempt the trustee from liability for dishonest acts (Section 51), intentional violation of civil rights (Section 27(2)), or ultra vires acts would be held invalid. However, the trustee may contractually limit the scope of compensation to actual loss, as Section 682(3) generally prohibits recovery for remote or indirect damage.

Indemnity clauses are recognized under Section 571(1) of the Civil Code. A trustee protected by an indemnity clause is entitled to recover the indemnity amount, litigation costs, and additional costs caused by the counterparty’s failure to pay. However, Section 571(3) maintains that the trustee remains personally liable for losses caused by their own dishonest intent or negligence.

12.5 Removal and Replacement

The Company Act, 2063 does not contain a detailed statutory procedure for removing a debenture trustee. The following mechanisms are available under the broader legal framework:

Voluntary Resignation: By analogy with the Mutual Fund Regulation, 2067, Rule 7, when a fiduciary submits their resignation, their position becomes automatically vacant. A successor must be appointed before the resignation takes effect to ensure continuity of investor protection.

Regulatory Removal: SEBON retains overarching authority under the Securities Act, 2063, Section 5(f) to intervene in the operations of securities market participants. Under the Securities Businessperson (Merchant Banker) Regulation, 2064, Rules 31 and 35, SEBON can suspend or permanently revoke the operating license of a fiduciary entity.

Debenture Holder Resolution: Under general trust principles and the terms of the Trust Deed, a supermajority of debenture holders may vote to remove the trustee for non-performance.

Judicial Removal: Under the Civil Code, Section 328(1), a trustee can be removed by the court for misappropriating property or failing to provide proper care.

Regulatory Gap: No dedicated statutory procedure for the removal and replacement of a debenture trustee. The process is fragmented across the Civil Code (judicial removal), SEBON regulations (administrative removal), and private contract (Trust Deed provisions).

XIII. DISCLOSURE, REPORTING, AND REGULATORY SUPERVISION

13.1 Disclosure at Issuance

When debentures are issued, the issuer is legally required to publicly disclose the name and address of the Debenture Trustee, as well as the primary clauses and key terms of the executed Trust Deed. This comprehensive disclosure is mandated by Schedule 5 as a required component of the full Prospectus. This ensures that the public and prospective investors are fully informed of the protective arrangements before they commit their capital.

13.2 Ongoing Reporting to Debenture Holders

Regulatory Gap: The Nepalese statutory framework does not prescribe specific reporting intervals, formats, or content requirements for the debenture trustee’s ongoing communications with debenture holders. There are no provisions comparable to the periodic reporting requirements imposed on portfolio managers (Portfolio Management Guidelines, 2067, Section 17) or fund supervisors (Mutual Fund Regulation, 2067, Rule 19). The ongoing reporting obligation is left entirely to the Trust Deed.

Comparative Reference: Under SEBI (Debenture Trustees) Regulations, 1993, Regulation 15(1)(c), the trustee is required to inform the debenture holders immediately of any breach of the Trust Deed or any material adverse change in the financial position of the issuer. Indian Companies (Share Capital and Debentures) Rules, 2014 further require the trustee to provide semi-annual reports to the holders.

13.3 Reporting to the Regulator (SEBON)

Regulatory Gap: There are no provisions or reporting templates explicitly detailing a Debenture Trustee’s regulatory reporting obligations to SEBON in the event of issuer default or breach. While SEBON has extensive reporting requirements for merchant bankers generally (Securities Businessperson (Merchant Banker) Regulation, 2064, Rule 25), no specialized trustee breach-reporting format exists.

13.4 SEBON’s Supervisory Role

Securities Act, 2063, Section 5: SEBON holds the exclusive authority to grant, deny, and renew operating licenses for securities businesses, controlling who may act as a fiduciary. A core duty of SEBON is to implement arrangements that prevent market offenses such as insider trading and protect investors from fraud.

Securities Businessperson (Merchant Banker) Regulation, 2064, Rule 28: SEBON is empowered to demand any operational document, financial report, or specific information from a merchant banker at any time.

Sanctions: If a fiduciary fails to perform, SEBON can deploy fines, order restructuring, or suspend and revoke operating licenses under the Securities Board Regulation, 2064, Sections 30 and 31.

13.5 Penalties for False Disclosure and Non-Compliance

The penalty regime is significant: Securities Act, 2063, Section 101(2): Fines of NPR 50,000 to NPR 150,000 or imprisonment up to one year for false trading and price manipulation. Section 101(3): Fines of NPR 100,000 to NPR 300,000 or imprisonment up to two years for fraudulent statements, plus mandatory compensation to the aggrieved party. Company Act, 2063, Section 160(s): Fines of NPR 20,000 to NPR 50,000 or imprisonment up to two years for acting against debenture holders’ interests. Commodities Act, 2074, Section 40: Fines up to NPR 500,000 and imprisonment up to 5 years for major non-compliance and fraud (applicable by analogy to fiduciary standards in the broader securities market).

XIV. THE ROLE OF BANKING REGULATION (NRB DIRECTIVES)

While the NRB Unified Directives do not directly regulate debenture trustees, they shape the regime indirectly in several important ways:

14.1 Banks as Issuers of Debentures

NRB Unified Directive 16/081, Section 5(1): A bank wishing to issue debentures must ensure its accumulated losses do not exceed 5% of its primary capital and must obtain specific NRB approval.

Capital Redemption Reserve: Under Directive 16/081, BFIs issuing debentures must establish a mandatory Capital Redemption Reserve, with funds set aside from annual profits proportionately throughout the tenure, excluding the years of issuance and maturity. This reserve is classified as a Statutory Reserve under Directive 4 and cannot be used for dividend distribution.

14.2 Merchant Banking Subsidiaries as Trustees

NRB Unified Directive 8/081, Section 4.2: Permits banks to establish Merchant Banking Subsidiaries with at least 51% bank ownership, authorized by SEBON to provide services including debenture trusteeship. This is the primary channel through which banking sector resources are deployed into the trustee function.

14.3 Conflict-of-Interest Safeguards

NRB Unified Directive 6/081, Section 1(2)(b): Prohibits directors from engaging in transactions where they have a financial interest. The Code of Conduct (Directive 6, Section 1) requires officials to ensure that personal or institutional conflicts do not compromise stakeholder interests.

NRB Unified Directive 6/081, Section 8(b): Prohibits banks from providing credit facilities to their own auditors or legal advisors, establishing a general principle of separation between service providers and the bank.

14.4 Investment Restrictions

NRB Unified Directive 8/081, Section 3(1): When a bank invests in debentures of other organized institutions, the investment must be in listed securities and for a period exceeding one year.

Directive 8/081, Section 5(2): Banks acting as underwriters must dispose of any debentures acquired through underwriting commitments within one year.

14.5 Disclosure and Reporting

NRB Unified Directive 4/081, Schedule 4.8.3: Banks must disclose specific details regarding their investments in debentures and bonds in their annual reports, including the name of the company, rate of interest, face value, purchase price, and maturity date.

Tier 2 Capital Treatment: Under the Capital Adequacy Framework 2015 (Directive 1, Annex 1.1), Tier 2 instruments like Subordinated Term Debt must be unsecured and subordinated to the claims of all depositors and general creditors. In liquidation, they are paid out only after depositors and general creditors are satisfied, but they hold seniority over common equity holders.

XV. ANALYTICAL NOTE: APPLICABILITY OF CIVIL CODE TRUST (GUTHI) PROVISIONS TO DEBENTURE TRUSTEES

15.1 The Hierarchy Framework

The National Civil (Code) Act, 2074, Section 3 establishes the foundational principle: where a special law provides a separate provision, it prevails over the Civil Code. The Company Act, 2063 and the Securities Act, 2063 are special laws governing debenture trustees. The Civil Code therefore operates as a residual, gap-filling source of law.

15.2 Provisions That Directly Apply

The following Civil Code provisions apply to debenture trustees and have been integrated throughout this analysis:

(a) Section 327(1) – Corporate Trustees: Confirms that body corporates may serve as trustees, directly accommodating the Company Act’s requirement that debenture trustees be organized institutions.

(b) Section 341 – Implied Duties: The catch-all provision that trustees possess all necessary rights and duties to protect beneficiaries, even if not specified in the deed. This fills the monitoring gaps identified in Section VII above.

(c) Sections 342(1)–(3) – Prohibition on Self-Dealing: Bars using trust property for personal purposes, conducting financial transactions between private and trust property, and commingling assets. These apply to debenture trustees as baseline prohibitions.

(d) Section 334(2) – Standard of Care: The “proper and reasonable care” standard provides the substantive benchmark for evaluating trustee conduct.

(e) Section 50 – Conflict of Interest in Decision-Making: Prevents participation in decisions involving personal interest. Section 50(2) declares conflicted decisions void.

(f) Section 51 (Proviso) – Personal Liability: Pierces the corporate veil for dishonest or ultra vires acts.

(g) Section 338 – Trust Breach and Remedies: Provides the framework for breach, restoration of benefits, and joint liability of multiple trustees.

15.3 Procedural Provisions

The National Civil Procedure (Code) Act, 2074 provides the litigation infrastructure for debenture trustee enforcement: Section 10 (standing), Section 93 (body corporate representation), Section 156 (interlocutory orders), Section 158 (interim orders), Section 70(1)(g) (injunctions), Section 161 (documentary evidence), Section 172 (genuineness depositions), Section 50(1) (extension of limitation for fraud), and Section 163 (cost allocation).

15.4 Divergences from Guthi Framework

While the fundamental fiduciary principles are shared, significant contextual divergences exist:

(a) The Guthi framework contemplates property-based trusts, including religious and charitable endowments. Debenture trusteeship is a commercial financial arrangement involving debt securities, interest payments, and capital market regulation. The economic nature of the “trust property” (a charge over company assets rather than direct ownership) is fundamentally different.

(b) The Guthi provisions allow trusts to be established through oral behavior, conduct, or testamentary donations (Section 316(3)). The Company Act mandates a formal written Trust Deed (Section 36(1)), making oral establishment irrelevant for debenture trusts.

(c) The Guthi framework provides for public trusts open to community complaints (Section 336(2)). Debenture trusts are private arrangements benefiting a defined class of investors; the enforcement mechanisms are collective but not public in the Guthi sense.

(d) The Guthi framework involves Section 323(4)’s prescribed investment categories (government bonds, fixed deposits, bank shares). Debenture trustees do not manage investment portfolios; they hold security interests and enforce terms.

Conclusion: The Civil Code’s trust provisions serve as an essential supplementary source of fiduciary law for debenture trustees, providing the standard of care, conflict prohibitions, implied duties, and personal liability framework that the Company Act and Securities regulations do not fully articulate. However, the Civil Code was not designed for capital market instruments, and its application to debenture trustees requires careful contextual adaptation.

XVI. CRITICAL GAPS, CURRENT PRACTICE, AND RECOMMENDATIONS FOR REFORM

16.1 Summary of Key Regulatory Gaps

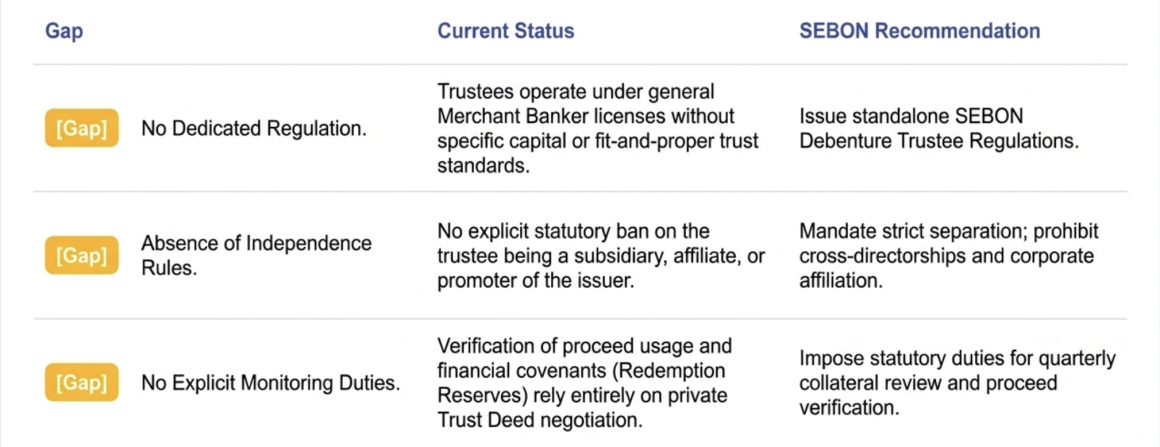

Gap 1: No Dedicated Debenture Trustee Regulation

Current Position: There is no standalone regulation or SEBON guideline prescribing licensing criteria, minimum capital, infrastructure requirements, or fit-and-proper tests specifically for debenture trustees. The role is performed by merchant bankers licensed under the general Securities Businessperson (Merchant Banker) Regulation, 2064, without any debenture-trustee-specific licensing layer.

Problem: This means that an entity may act as a debenture trustee without being specifically qualified, capitalized, or supervised for that specialized function. The fiduciary responsibility of protecting public debenture holders demands a higher regulatory threshold than general merchant banking services.

Recommendation: SEBON should issue a dedicated Debenture Trustee Regulation prescribing: minimum net worth requirements, mandatory registration and licensing with SEBON, infrastructure and human resource standards (requiring qualified legal and financial professionals), periodic renewal and compliance audits, and a mandatory code of conduct specific to trustee functions.

Gap 2: Absence of Statutory Independence Requirements

Current Position: No provision explicitly prohibits a debenture trustee from being an affiliate, subsidiary, or associate of the issuer, the issue manager, or the underwriter.

Problem: An affiliated trustee cannot objectively enforce the Trust Deed against its own group company. The inherent conflict of interest undermines the entire purpose of the trustee arrangement.

Recommendation: Statutory provisions should explicitly prohibit any person or entity from acting as a debenture trustee if it is: (a) a promoter or member of the promoter group of the issuer; (b) a subsidiary or holding company of the issuer; (c) an entity with common directors or key management personnel; (d) a substantial shareholder in the issuer; or (e) a guarantor of the debenture. Mandatory disclosure of any commercial relationship with the issuer should be required.

Gap 3: No Explicit Monitoring Obligations

Current Position: The statutory framework does not assign the debenture trustee an ongoing duty to monitor the use of proceeds, financial covenant compliance, asset coverage ratios, or the continued perfection of charges.

Problem: Without mandatory monitoring, the trustee’s role is effectively reactive – it acts only when it learns of a default, rather than proactively identifying risk.

Recommendation: The law should impose statutory monitoring duties, including: verification that debenture proceeds are used for stated purposes; periodic (at minimum semi-annual) inspection of financial covenant compliance; quarterly review of collateral adequacy and asset coverage ratios; and prompt reporting of any breach to SEBON and to debenture holders.

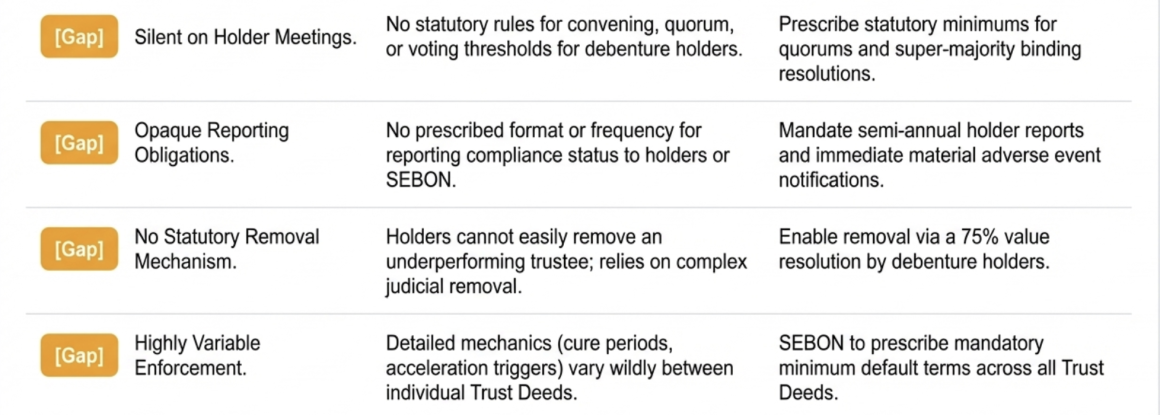

Gap 4: No Prescribed Reporting to Holders or SEBON

Current Position: Neither the Company Act nor the Securities regulations prescribe the format, frequency, or minimum content of the trustee’s reports to debenture holders or to SEBON.

Problem: Debenture holders have no statutory right to periodic information about the issuer’s compliance or the status of their security, except as voluntarily provided under the Trust Deed.

Recommendation: Mandatory semi-annual reporting to debenture holders covering the issuer’s compliance status, collateral valuation, reserve fund adequacy, and any notices of default. Immediate notification of material adverse events. Annual compliance certification to SEBON.

Gap 5: No Statutory Framework for Debenture Holder Meetings

Current Position: The law is entirely silent on how debenture holders’ meetings are convened, what quorum applies, what voting thresholds are required, and how the majority binds the minority.

Problem: Without statutory minimums, Trust Deeds may contain provisions that unfairly disadvantage debenture holders (e.g., extremely high quorum requirements that make meetings impossible, or vague voting procedures that allow the issuer to influence outcomes).

Recommendation: The Company Act or a SEBON regulation should prescribe: minimum notice periods for meetings; quorum requirements (minimum percentage of outstanding principal); voting thresholds for ordinary and special resolutions; the right of a specified minority to requisition meetings; the binding effect of majority decisions; and the trustee’s obligation to convene a meeting upon the occurrence of specified default events.

Gap 6: No Statutory Mechanism for Trustee Removal by Holders

Current Position: The Company Act does not prescribe a mechanism for debenture holders to remove an underperforming trustee. The only available routes are judicial removal (Civil Code Section 328), regulatory removal (SEBON action), or Trust Deed provisions.

Problem: Debenture holders who are dissatisfied with their trustee’s performance have no clear, accessible statutory remedy to effect a change.

Recommendation: A statutory provision should allow a specified majority of debenture holders (e.g., 75% by value) to remove the trustee by resolution, subject to the requirement that a qualified successor is appointed before the removal takes effect.

Gap 7: Enforcement Mechanics Largely Contractual

Current Position: While the Company Act provides the core enforcement powers (Sections 39 and 41), the detailed enforcement mechanics – default triggers, cure periods, notice requirements, acceleration procedures, and collateral liquidation protocols – are left to the Trust Deed.

Problem: The quality and investor-friendliness of enforcement mechanisms vary from deed to deed, depending on the relative bargaining power of the issuer and the trustee at the time of drafting.

Recommendation: SEBON should prescribe minimum mandatory terms for Trust Deeds, including standard default events (missed payment, breach of asset coverage, adverse credit rating action, insolvency filing), mandatory cure periods, acceleration triggers, and collateral liquidation procedures that must be included in every Trust Deed regardless of the parties’ negotiation.

16.2 Current Practice and Path Forward

In contemporary Nepalese capital market practice, merchant banks (such as NIBL Ace Capital, Siddhartha Capital, and Nabil Investment Banking) act as Debenture Trustees for debentures issued primarily by commercial banks. The trustee’s practical role involves overseeing the debenture terms, ensuring semi-annual interest payments are made on time, and verifying that the issuer maintains the required Debenture Redemption Reserve. Because actual corporate defaults on public debentures have been rare in Nepal’s recent history, there is extremely limited practical enforcement experience. The trustee regime has not been stress-tested by a major default event, which means the gaps identified in this analysis have not yet manifested as practical crises – but they represent latent systemic risks that would be exposed in any significant issuer default.

The Nepalese debenture trustee regime possesses a sound structural foundation: the Company Act, 2063 provides statutory enforcement powers, the Securities Act and regulations mandate appointment and disclosure, the Insolvency Act preserves secured creditor priorities, and the Civil Code supplies residual fiduciary principles. What is missing is the detailed regulatory infrastructure that transforms this framework from a set of general principles into an effective, self-executing investor protection mechanism. A dedicated SEBON regulation on debenture trustees – drawing on the Indian SEBI model while adapted to Nepalese conditions – would close the critical gaps and bring the regime to international standards of investor protection.