Nepal is taking a bold step towards a sustainable future with the introduction of the Nepal Green Finance Taxonomy (NGFT). If you’re in banking, insurance, investments this guide breaks down things you might need to know about NGFT:

Link to my notebook: Notebook Link

Category 1: The Basics - What is the NGFT and Why Does it Matter?

1. What is the Nepal Green Finance Taxonomy (NGFT)?

NGFT is a detailed guidebook or a common dictionary for “green” finance. It’s a standardized classification system that helps financial institutions and investors determine whether an economic activity or investment project is environmentally sustainable. By categorizing activities as “Green,” “Amber,” or “Red,” it creates a clear, transparent language for the entire financial sector, ensuring everyone defines “green” in the same way.

2. Why was the NGFT created? What problem does it solve?

The NGFT was born out of necessity. First, Nepal has ambitious climate goals, but achieving them is expensive. It’s estimated that the country needs about USD 77 billion by 2030 to meet its adaptation, mitigation, and sustainable development targets. The government alone cannot bridge this gap; private capital is essential.

Second, without a standard definition, “green” could mean different things to different institutions, leading to confusion and “greenwashing” – where investments are misleadingly branded as eco-friendly. The NGFT solves this by providing a science-based, consistent benchmark to prevent such practices and direct capital genuinely towards Nepal’s sustainable development.

3. What is the financial and environmental rationale for the NGFT?

The rationale rests on three pillars:

- Mobilizing Capital: The NGFT is a tool to unlock and channel the massive investments needed from both domestic and international sources towards national priorities like the National Adaptation Plan (NAP), Nationally Determined Contributions (NDC), and the Green, Resilient, and Inclusive Development (GRID) approach.

- Standardizing Definitions: It brings clarity and transparency to the market, building investor confidence by ensuring that a “green” label actually means something.

- Strengthening the Financial System: It helps integrate environmental risks and opportunities into the heart of financial decision-making, making the entire system more resilient and forward-looking.

4. What are the primary goals of the NGFT?

The primary goals are to:

- Guide and incentivize the financial sector to fund green innovations.

- “Green” the entire financial system by aligning investments with climate and environmental objectives.

- Attract foreign investment dedicated to sustainable projects.

- Support the government in implementing its climate change strategies.

5. Is the application of the NGFT compulsory or voluntary?

Currently, the adoption of the NGFT is voluntary. This means financial institutions are encouraged, but not legally required, to use the taxonomy to classify their investments. The approach is designed to be flexible, allowing the market to learn and adapt without imposing immediate rigid mandates.

6. If it’s not compulsory, who is it recommended for?

While voluntary, the NGFT is recommended as an essential tool for the entire financial ecosystem of Nepal. This includes:

- All Banks and Financial Institutions (Commercial, Development, Finance, and Microfinance).

- Capital Market Participants (like merchant banks), regulated by the Securities Board of Nepal (SEBON).

- The Insurance Market (life, non-life, reinsurance), regulated by the Nepal Insurance Authority (NIA).

- The Broader Private Sector, including MSMEs, pension funds, venture capital, and impact investors.

Category 2: The Framework - How Does the Classification Work?

7. What are the core environmental principles (AMNP) of the NGFT?

The taxonomy is built on four core environmental objectives, easily remembered as AMNP:

- A – Climate Change Adaptation: Activities that help people and assets become more resilient to current and future climate impacts (e.g., drought-resistant crops, climate-resilient infrastructure).

- M – Climate Change Mitigation: Activities that reduce or prevent greenhouse gas emissions (e.g., renewable energy, energy efficiency, electric transport).

- N – Natural Resource Conservation & Management: Activities that protect and sustainably manage ecosystems, biodiversity, and natural resources (e.g., sustainable forestry, watershed management).

- P – Pollution Prevention & Control: Activities that reduce pollution of air, water, and land, and promote circular economy practices (e.g., waste management, cleaner production).

8. Does an activity need to meet all four AMNP principles to be classified as “Green”?

No. An activity can be classified as “Green” if it makes a substantial contribution to at least one of the four principles. The critical condition is that it must not harm others, which leads us to the most important rule.

9. What is the “Do No Significant Harm” (DNSH) principle and why is it critical?

DNSH is the essential safeguard. It means that an activity contributing to, say, Mitigation (like a solar farm) must not cause significant harm to the other three principles (e.g., by degrading a natural habitat or creating pollution during panel manufacturing). It ensures that a “green” investment is truly sustainable overall, not just in one narrow aspect. An investment must pass both the “positive contribution” test and the “no significant harm” test to be certified “Green.”

10. How are the “Amber” and “Red” categories defined?

The taxonomy uses a traffic light system for clarity:

- Green (Go): Activities that are fully aligned with the taxonomy (substantial contribution to one principle + DNSH).

- Amber (Transition): This is a crucial category for activities on a pathway to becoming green. They are not fully sustainable yet but are not severely harmful. They may be neutral or require specific remedial measures to improve. Investment is encouraged here with a plan for transition.

- Red (Stop): Activities that are not compliant with environmental objectives and cause significant harm without plans for remediation. Investment is discouraged.

11. What happens if an activity causes harm but plans to fix it?

This is where the “Amber or Transitional” category comes in. If an activity currently causes some harm but the investment is explicitly tied to taking remedial action to fix those harmful practices, it can be classified as “Amber.” This recognizes that transitioning to a green economy takes time and encourages improvement. If it causes harm and does nothing to address it, it falls into the “Red” category.

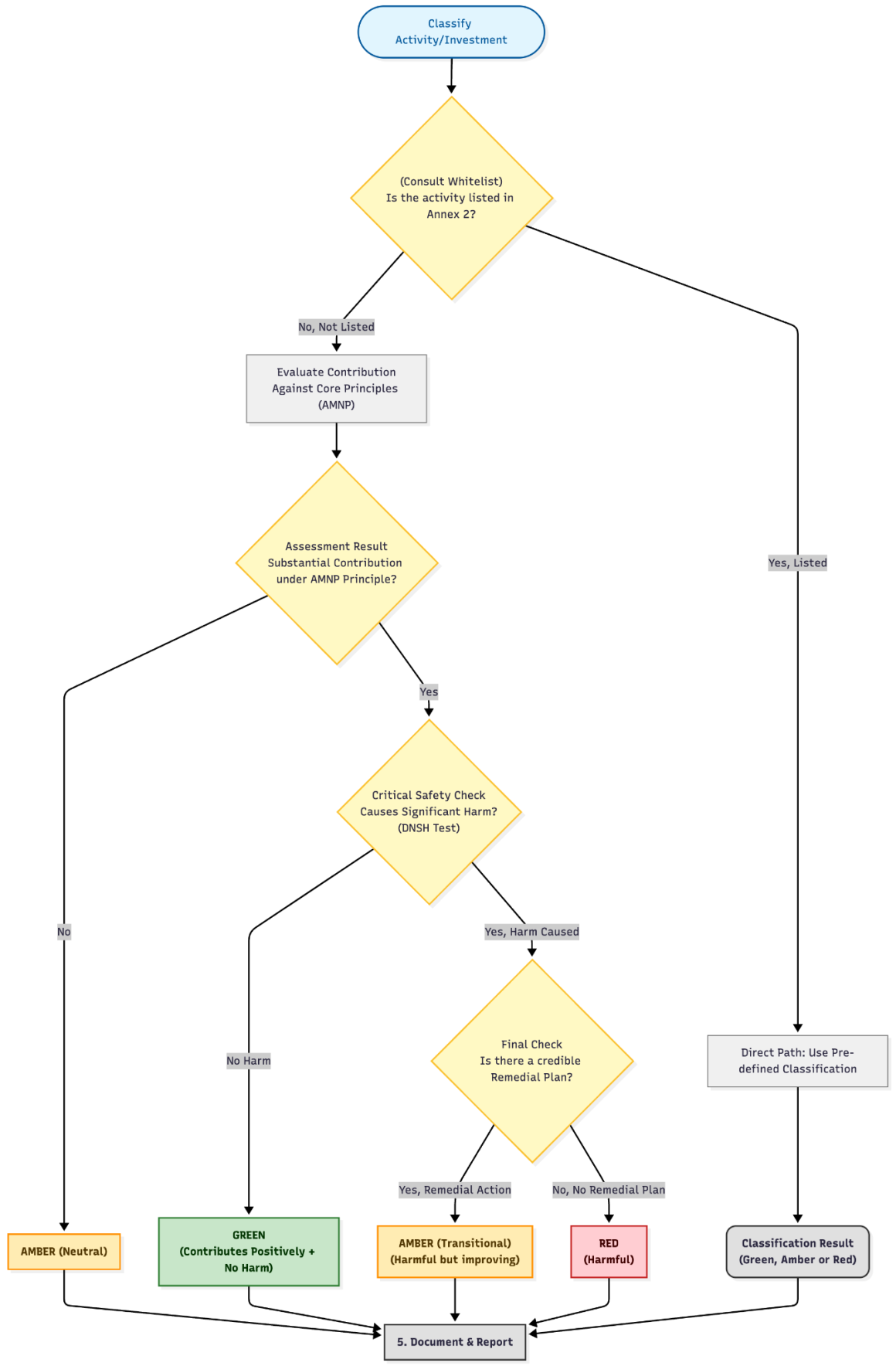

12. The NGFT uses both a “Principle-based” and a “Whitelist-based” approach. Which one should be used?

Both should be used, as they are designed to work together. The Whitelist (in Annex 2) is the first stop – it’s a pre-approved list of activities in various sectors (e.g., agriculture, energy) that are already classified as Green, Amber, or Red. If the activity is on the list, we can use that classification.

The Principle-based approach provides the flexibility to assess activities not on the whitelist. If a new, innovative project clearly aligns with one of the AMNP principles and meets the DNSH criteria, we can classify it as “Green” by justifying our assessment.

13. What if the activity aligns with the principles but isn’t on the official whitelist?

We can still classify it as “Green”. The principle-based approach allows for this. However, the institution must be prepared to conduct a thorough assessment, gather evidence of the environmental benefits, and rigorously document how it meets the AMNP and DNSH criteria. This ensures the system can adapt to innovation while maintaining integrity.

14. How does one classify a general business loan that funds a mix of green and non-green activities?

We use the Proportional Approach. A single loan to a company can be broken down into the specific activities it funds. For example, a Rs. 10 million loan might be used for:

- Rs. 5M (50%) for energy-efficient machinery (Green).

- Rs. 3M (30%) for general working capital (Amber – neutral).

- Rs. 2M (20%) for expansion with potential environmental harm (Red).

The loan is then reported as 50% Green, 30% Amber, and 20% Red. This provides a transparent and accurate picture.

Category 3: Application and Compliance - Who Does What?

16. Who are the key regulators involved?

The NGFT is a collaborative effort led by Nepal Rastra Bank (NRB) but involving all key financial regulators:

- NRB for banks and financial institutions.

- Securities Board of Nepal (SEBON) for the capital market.

- Nepal Insurance Authority (NIA) for the insurance sector.

These bodies are responsible for monitoring, reporting, and supervising the taxonomy’s application within their respective sectors.

16. The NGFT is an NRB document. How is it relevant to institutions under SEBON or NIA?

The NGFT is intentionally designed as a cross-sectoral framework. Even though NRB led its development, SEBON and NIA were integral partners. The taxonomy includes sectors and activities directly relevant to capital markets (e.g., green bonds) and insurance. Its goal is to create a unified “green language” for the entire financial system, not just banking.

17. What is the ESRM Guideline and how does it apply to banks?

The Environmental and Social Risk Management (ESRM) Guideline is a mandatory regulation that requires banks to assess environmental and social risks before making lending decisions. It’s the first essential step before applying to the NGFT. The ESRM acts as a due diligence filter to identify and mitigate major risks, ensuring that only projects that pass this initial screen are then classified using the taxonomy’s Green/Amber/Red criteria.

16. A step-by-step process for classification?

The Nepal Green Finance Taxonomy provides a systematic two-path approach for classifying economic activities. The process begins by consulting the official Whitelist in Annex 2, which contains pre-classified activities. If an activity is listed, its pre-defined Green, Amber, or Red classification is adopted directly, as the necessary analysis is already complete.

For activities not found in the whitelist, a principle-based assessment is required. This evaluation first determines if the activity substantially contributes to any of the four core environmental objectives: Climate Change Adaptation, Mitigation, Natural Resource Conservation, or Pollution Prevention. A negative outcome results in an Amber (Neutral) classification. A positive outcome requires a DNSH test to ensure no significant harm is caused to other objectives. Passing this test leads to a Green classification. If significant harm is identified, the presence of a credible remedial action plan determines the final classification: Amber (Transitional) with a plan, or Red without one.

For complex investments like general business loans, this process is applied to each individual segment, resulting in a proportional classification across the portfolio. The final step involves thorough documentation of the justification and reporting through official channels. This framework ensures both efficiency for standard activities and robust assessment for innovative projects.

19. What are the disclosure requirements?

Financial institutions are expected to report annually on both:

- Financial Disclosure: The proportion (percentage) of their portfolio or investments that are aligned with the taxonomy (Green/Amber).

- Non-Financial Disclosure: Qualitative information on how the taxonomy was used, the environmental benefits achieved, and their governance processes for managing green finance.

The aim is transparency, allowing regulators and the public to track progress.

Category 4: Challenges and The Path Forward

20. What are the major implementation challenges?

The NGFT is a pioneering document, and its success hinges on addressing several challenges:

- Regulatory Coordination: Seamless collaboration between NRB, SEBON, and NIA is crucial to avoid siloed efforts. Policy mismatches in areas like land acquisition and forest clearance can also hinder green projects.

- Clarity on Mandate: A key policy decision is needed on whether the taxonomy should remain voluntary or become mandatory in the future to ensure widespread adoption.

- Capacity Gap: Many financial institutions and even regulators lack the technical expertise to implement the taxonomy effectively. Widespread training is essential.

- Verification: The lack of accredited third-party verifiers in Nepal means institutions must self-certify, which requires robust internal systems to maintain credibility.

21. Where are the bankable green projects?

This is a classic “chicken and egg” problem. Investors report a shortage of readily available, financially viable green projects. To bridge this gap, the government and regulators can:

- Offer incentives like tax breaks, guarantees, or subsidies to de-risk green investments.

- Develop a pipeline of projects through public-private partnerships.

- Provide technical support to project developers to improve their proposals.

22. Is green finance actually less risky?

There is a perception that green products are riskier. While long-term data might prove their resilience, the immediate focus is on using incentives to change behavior. Regulators can assign lower risk weights to taxonomy-aligned loans, making them more attractive for banks. Government guarantees can also mitigate perceived risks, encouraging more investment in the green sector.