1. Regulatory and Policy Framework Problems

1.1 Absence of Finalized Regulatory Instruments

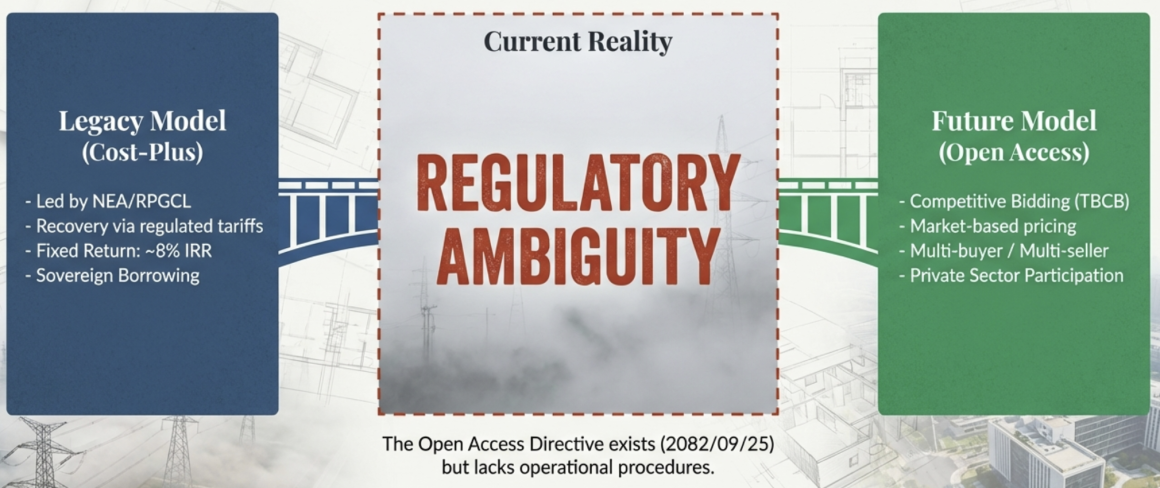

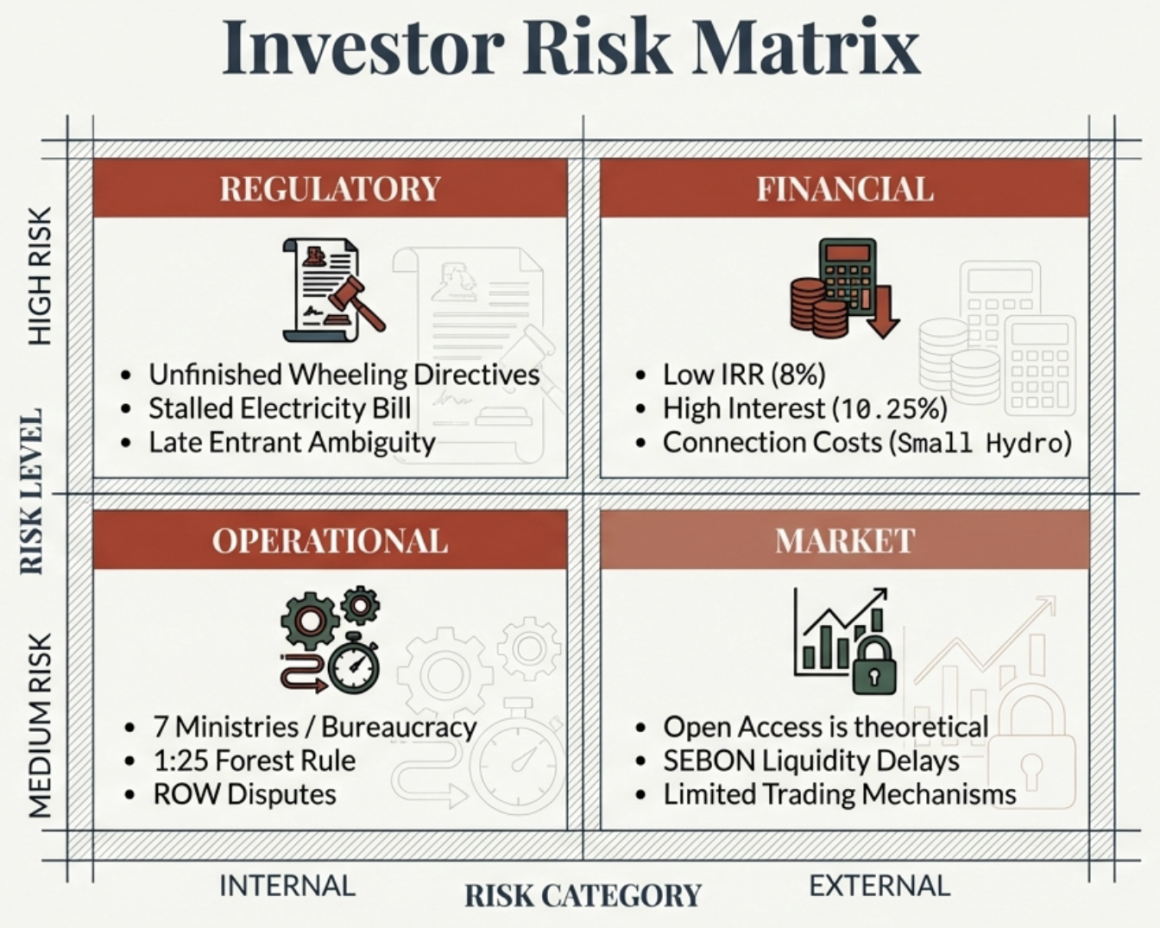

The Electricity Regulatory Commission (ERC) has not yet finalized specific regulatory instruments that prescribe a single, rigid costing methodology for transmission lines. While the current framework effectively operates under a transitional structure, it reflects a shift between two distinct regulatory paradigms. Under the current cost-plus framework, the Nepal Electricity Authority (NEA) and Rastriya Prasaran Grid Company Limited (RPGCL) construct transmission infrastructure and recover their investment through regulated tariffs or wheeling charges designed to ensure a predetermined return – typically around an 8% Internal Rate of Return (IRR). In contrast, the future framework envisions a competitive, open-access regime, where transmission charges will be determined through Tariff-Based Competitive Bidding (TBCB) and market-based mechanisms, subject to finalized regulatory directives.

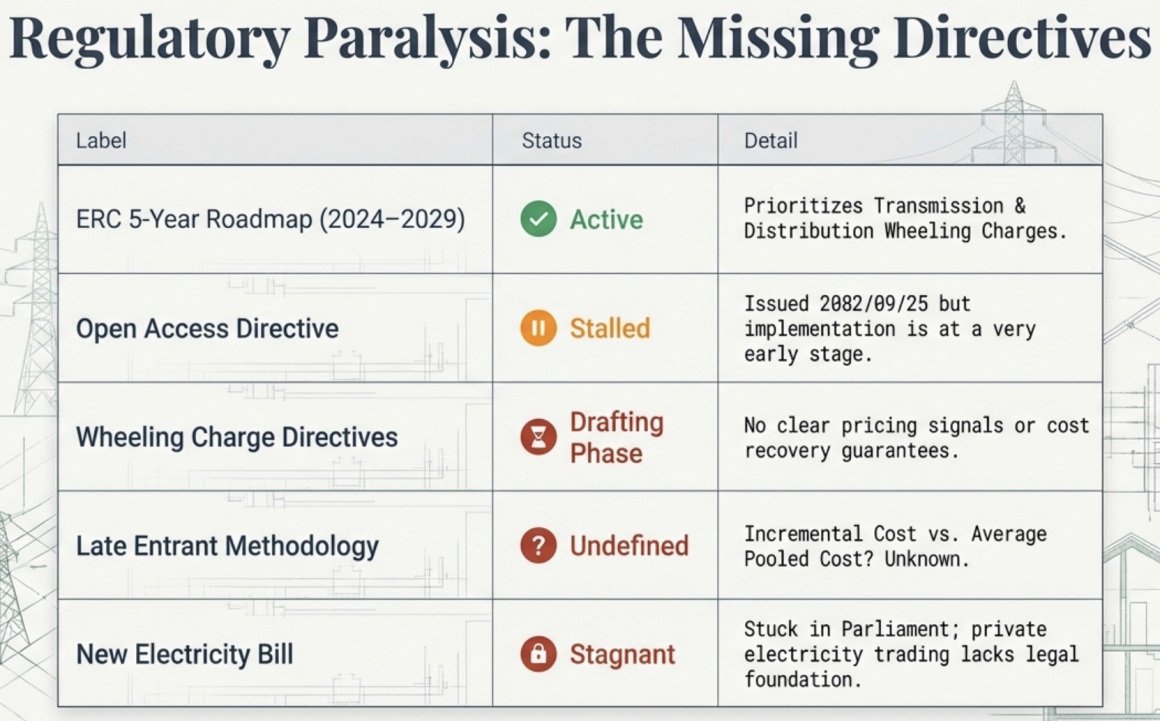

However, this transition remains incomplete. The ERC’s Five-Year Roadmap (2024–2029) explicitly identifies the development of detailed directives on “Transmission and Distribution Wheeling Charges” as a priority to operationalize Open Access, yet these directives remain in the drafting phase. This regulatory ambiguity creates substantial uncertainty for private investors, who require clear, predictable pricing signals and cost recovery frameworks before committing capital to long-gestation transmission assets. Moreover, the absence of finalized instruments prevents the establishment of definitive methodologies for charging late entrants into transmission systems – particularly whether such charges will be based on incremental cost, average pooled cost, or another allocation model. Until the Open Access and wheeling charge directives are formally issued and operationalized, the costing framework for transmission infrastructure will remain uncertain and subject to regulatory interpretation.

1.2 Delayed Implementation of Open Access

Although the Open Access Directive for the Electricity Transmission and Distribution System was formally approved and issued on 2082/09/25 by the Electricity Regulatory Commission, its implementation remains at a very early stage. As a result, there has been limited practical movement in operationalizing open access provisions, particularly with respect to wheeling charges, transmission pricing methodologies, and the facilitation of third-party access to the grid. Because the directive is newly introduced, institutional mechanisms, operational procedures, and market practices necessary for its full implementation are still evolving. Consequently, potential market participants – including independent power producers, private transmission developers, and electricity traders – continue to face uncertainty and are unable to plan investments, financing, or commercial arrangements with confidence.

This delay is compounded by the continued stagnation of the new Electricity Bill in Parliament, which is intended to provide the broader legislative foundation for opening transmission infrastructure and electricity trade to private sector participation. The absence of this enabling legislation has slowed the structural transition toward a competitive electricity market. As a result, the envisioned multi-buyer, multi-seller framework enabled by Open Access remains largely theoretical rather than fully operational. This has constrained the emergence of competitive electricity trading, limited efficient allocation of transmission capacity, and delayed the development of a transparent, market-driven transmission pricing regime.

1.3 Jurisdictional Overlaps and Bureaucratic Hurdles

Transmission and hydropower developers face extensive bureaucratic hurdles arising from fragmented institutional responsibilities and overlapping jurisdiction among multiple government agencies. Project approvals require coordination with the Nepal Electricity Authority (NEA), the Department of Electricity Development (DoED), the Electricity Regulatory Commission (ERC), and the Ministry of Energy, Water Resources and Irrigation (MoEWRI), among others. At the same time, there are significant overlaps in policy formulation and regulatory authority between the ERC and the Water and Energy Commission Secretariat (WECS). This institutional fragmentation frequently results in conflicting guidelines, duplicative procedures, and prolonged delays in decision-making, particularly where coordination is required across ministries such as the Ministry of Forests and Environment and the Department of National Parks and Wildlife Conservation. The cumulative effect is a complex and time-consuming approval process that significantly increases project costs, uncertainty, and investment risk.

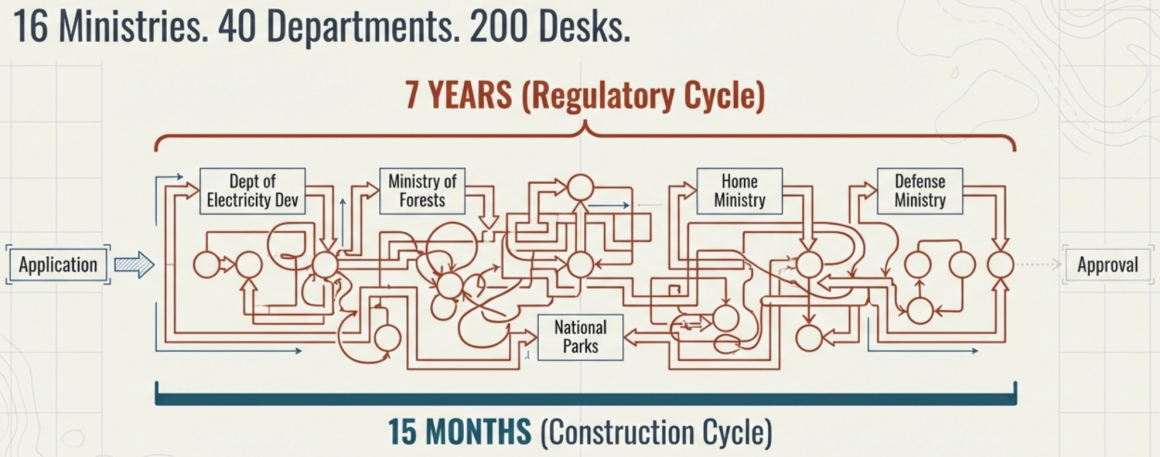

The administrative burden imposed on developers is exceptionally high. Developers must coordinate with as many as seven ministries, twenty-three departments, and navigate thirty-six separate laws to advance a hydropower project. Other stakeholders estimate the burden to be even greater, requiring engagement with fourteen ministries, forty departments, and more than two hundred individual desks or approval points. While the actual physical construction of a hydropower project may take as little as fifteen months, the legal procedures, clearances, and approvals required before construction can begin often extend up to seven years. Despite longstanding demands from investors for a one-window approval mechanism, no effective system has been implemented, forcing developers to physically move files between multiple agencies, often facing delays due to weak accountability and administrative inefficiency.

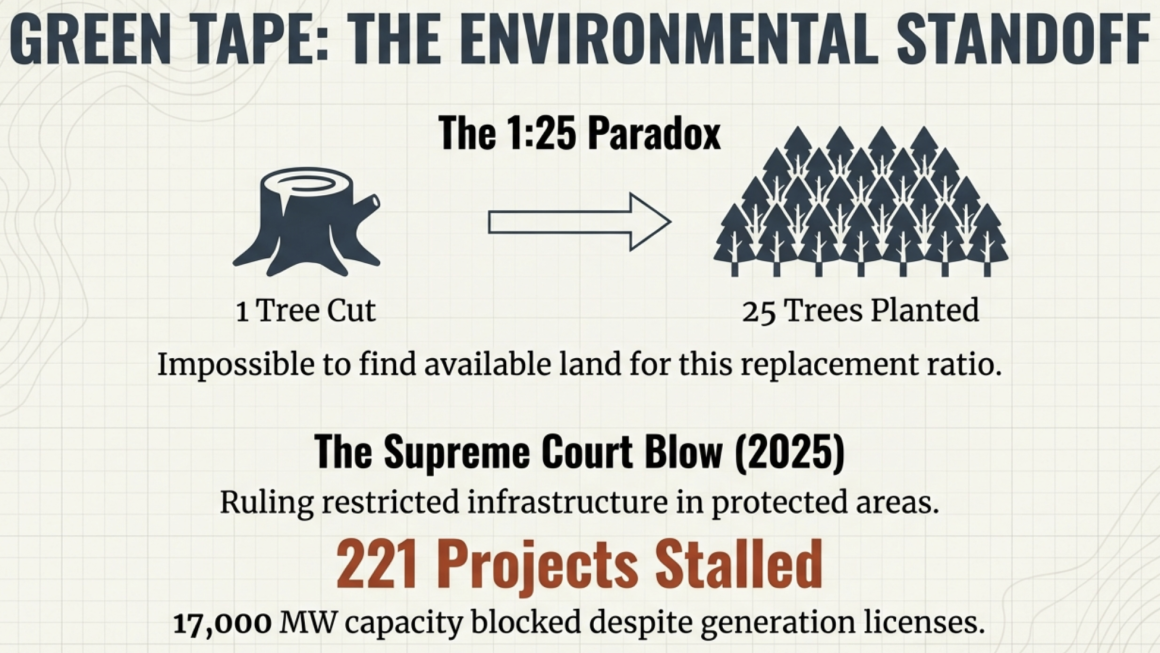

Conflicts between the Department of Electricity Development and the Ministry of Forests and Environment represent one of the most significant sources of institutional fragmentation. The DoED grants project licenses and approves Environmental Impact Assessment (EIA) reports, often without full coordination with forest and conservation authorities. As a result, developers may receive generation licenses but subsequently face project blockages when forest authorities impose stricter standards or deny access to required forest land. This lack of coordination has had severe consequences. A recent Supreme Court ruling restricting infrastructure development in protected areas has stalled 221 projects with a combined capacity of approximately 17,000 MW, preventing them from accessing forest areas despite having secured other regulatory approvals.

Environmental compliance requirements further compound these challenges. Developers must comply with the “1:25” compensatory plantation rule, requiring the planting of twenty-five trees for every tree cut. This requirement is often impractical due to limited availability of suitable land near affected forest areas, prompting requests from developers to reduce the ratio to 1:5. Similarly, although legal provisions mandate EIA approvals within thirty days, approvals frequently take years in practice due to procedural delays and bureaucratic inefficiencies.

Institutional fragmentation is also evident in the unclear division of authority among federal, provincial, and local governments. Responsibilities related to hydropower development, royalty sharing, land acquisition, and river conservation remain ambiguously defined, creating further uncertainty and administrative delays. Even the Electricity Regulatory Commission, established as an independent regulator, faces operational limitations, as major decisions are often routed through the Council of Ministers rather than being resolved through independent regulatory processes.

Additional regulatory and financial bottlenecks further constrain project development. The Securities Board of Nepal (SEBON) has delayed approvals for public share issuance for extended periods – sometimes exceeding eighteen months – creating liquidity shortages for projects nearing completion. Developers also face delays in obtaining permits for importing explosives, which require approvals from multiple agencies, including foreign authorities and domestic ministries such as Energy and Finance.

The consequences of these systemic barriers are evident in key national infrastructure projects. The Hetauda–Dhalkebar–Inaruwa 400 kV transmission line, a strategically critical project, has remained under construction for approximately fifteen years due to delays related to forest clearance, land acquisition, and right-of-way disputes. Similarly, private hydropower developers face financial penalties when they fail to generate contracted electricity due to hydrological variability or climate-related changes, even though hydrological assessments are often conducted with the involvement of NEA experts. The private sector argues that such risks should be more equitably shared, rather than being borne exclusively by developers.

Overall, these jurisdictional overlaps, regulatory gaps, and bureaucratic inefficiencies create a highly uncertain and burdensome environment for transmission infrastructure development, significantly affecting project timelines, financing viability, and private sector participation.

2. Financial and Investment Challenges

2.1 Massive Financing Gap

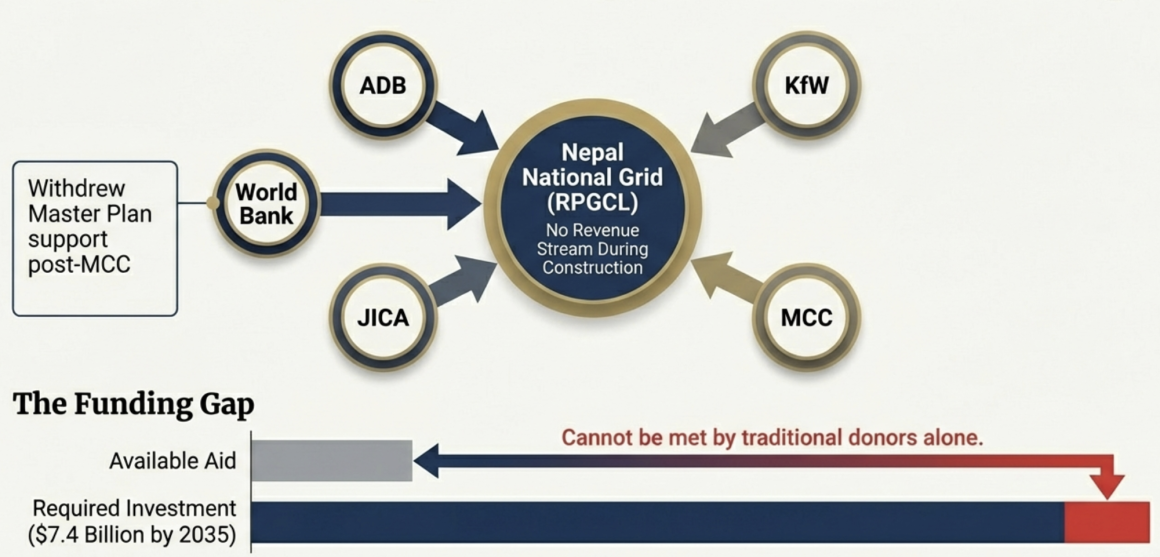

Nepal faces an enormous financing requirement to develop its energy infrastructure, with the government estimating a total investment need of USD 46.5 billion by 2035 for the overall energy sector. Within this, a specific transmission financing gap of USD 7.4 billion has been identified for transmission infrastructure alone. This represents a staggering investment requirement relative to Nepal’s economic capacity, fiscal resources, and current public expenditure capabilities.

The financing gap is particularly severe in the transmission segment because transmission projects require very high upfront capital investments and have long asset lives with extended payback periods. Unlike hydropower generation projects, which offer higher returns and more direct revenue streams through Power Purchase Agreements (PPAs), transmission infrastructure typically generates lower and more regulated returns. This makes transmission projects inherently less attractive to private investors.

The current financing model further exacerbates this challenge. Under the sovereign borrowing structure, the Government of Nepal secures loans from multilateral and bilateral development partners and then relends these funds to the Nepal Electricity Authority (NEA). These relending rates have been noted to reach as high as 10.25% for a significant portion of the borrowings, creating substantial financial stress on NEA. This high cost of capital reduces NEA’s financial capacity to undertake additional transmission investments and constrains overall sector expansion.

As a result, Nepal faces a structural mismatch between the massive transmission infrastructure investment required to support future generation growth and the limited financial capacity of the public sector to fund these projects.

2.2 Low Return on Investment

Transmission infrastructure investments in Nepal offer significantly lower returns compared to hydropower generation projects, creating a major barrier to attracting private investment.

Rastriya Prasaran Grid Company Limited (RPGCL), the national transmission company, calculates its wheeling charges based on an Internal Rate of Return (IRR) of only 8%, which is less than half the 17% Return on Equity (ROE) permitted for large hydropower generation projects.

This disparity reflects the broader regulatory transition in Nepal’s transmission sector:

Summary of the Regulatory Transition:

- Current Framework (Cost-Plus):

Under the current cost-plus regulatory model, NEA and RPGCL construct transmission infrastructure and recover their investment through regulated wheeling charges designed to ensure a fixed and predictable return, typically around 8% IRR. - Future Framework (Competitive/Open Access):

The sector is gradually transitioning toward a more competitive model based on Tariff-Based Competitive Bidding (TBCB) and Open Access. Under this framework, transmission charges will be determined through competitive bidding processes or finalized regulatory directives, which are currently still in the drafting phase.

Despite these reforms, the underlying return profile for transmission remains relatively low.

This low return structure makes transmission investments considerably less attractive to private equity investors, who have alternative investment opportunities in hydropower generation that offer substantially higher returns. While the regulatory framework acknowledges the need to provide a “reasonable profit” under cost-plus arrangements, the actual profit margins remain modest compared to infrastructure investments in other sectors or countries.

In addition, transmission infrastructure is highly capital-intensive and involves significant sunk costs that cannot be recovered if demand projections or regulatory conditions change. The combination of high upfront investment, lower returns, and long recovery periods creates a fundamental structural challenge in mobilizing private capital for transmission development.

2.3 Absence of Established Wheeling Charge Mechanisms

Although the Electricity Regulatory Commission (ERC) Act mandates the establishment of wheeling charges, detailed regulatory directives defining the specific methodology are still under development. This absence of finalized wheeling charge regulations creates major revenue uncertainty for transmission investors.

Without a clear and legally established wheeling charge framework, private investors cannot accurately estimate their potential return on investment for standalone transmission projects or third-party access arrangements. This lack of revenue predictability presents a significant barrier to financial closure and limits private sector participation, particularly under models such as Tariff-Based Competitive Bidding (TBCB), which depend on stable and predictable revenue streams.

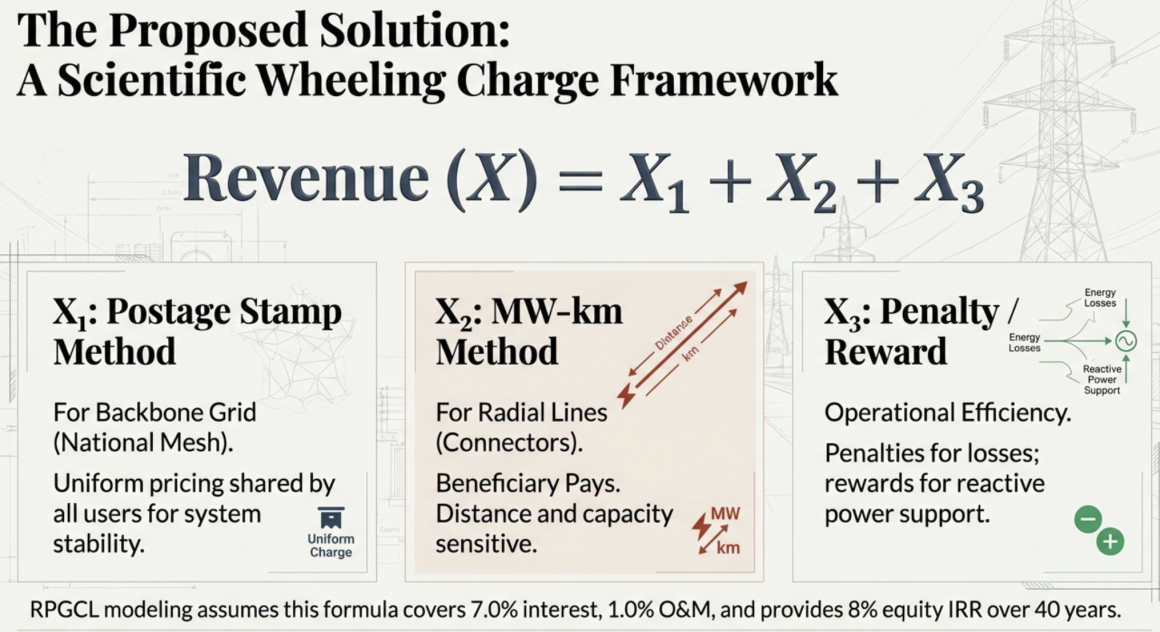

To address this, Rastriya Prasaran Grid Company Limited (RPGCL) has developed a proposed “Scientific Wheeling Charge” framework, based on its corporate planning documents, designed to ensure cost recovery and financial sustainability for transmission entities through a transparent and structured pricing mechanism.

Under this proposed framework, the total annual revenue requirement (X) for a transmission project is composed of three components: X = X₁ + X₂ + X₃

Each component serves a distinct function in ensuring cost recovery and operational efficiency:

The first component, X₁ (Postage Stamp Method), applies to the backbone grid, defined as the national mesh network, such as the East-West 400 kV transmission highways. This component uses a uniform pricing approach, similar to a postal stamp, where the same rate applies regardless of the distance electricity travels within the backbone network. This charge is collected from load-serving entities, including distribution utilities and bulk consumers. The rationale behind this approach is that the backbone grid provides system-wide benefits, including stability, redundancy, and alternative power flow routes under contingency conditions. Therefore, its costs are shared broadly among all grid users.

The second component, X₂ (MW-km Method), applies to radial transmission lines that connect specific hydropower generation hubs or project clusters to the backbone grid. This component is both distance-sensitive and capacity-sensitive, meaning it is calculated based on the megawatts of capacity booked and the distance electricity is transmitted. This cost is borne directly by the specific hydropower projects utilizing the corridor. This reflects the “beneficiary pays” principle, ensuring that generators located far from the main grid bear proportionately higher connection costs, thereby preventing cross-subsidization by other users.

The third component, X₃ (Penalty/Reward Component), is a variable operational mechanism designed to incentivize efficient grid operation. It imposes financial penalties on users whose actions increase system losses and provides financial rewards to those whose actions improve efficiency, such as providing reactive power support or reducing congestion. This component encourages grid users to operate in ways that optimize system performance and stability.

Together, these three components are designed to create a viable revenue structure for transmission investors.

For private investors participating in TBCB or Public-Private Partnership (PPP) models, these mechanisms help address multiple financial risks. The combined revenue from X₁ and X₂ ensures recovery of capital expenditures, financing costs, and operational expenses. RPGCL’s internal financial modeling assumes that wheeling charges must cover a 7.0% interest rate, 1.0% operation and maintenance costs, and provide an 8% equity IRR over a 40-year project life.

Under a TBCB model, private developers calculate their required Annual Revenue Requirement based on these parameters and submit competitive bids accordingly.

The X₁ backbone charge provides baseline revenue stability by distributing costs across the entire system load, protecting investors from the risk associated with individual generator failure. The X₂ component ensures that specific generators pay for the infrastructure they directly benefit from, providing clear price signals regarding the economic viability of remote generation projects. The X₃ component further ensures operational performance by linking financial incentives to technical efficiency and system reliability.

However, despite the development of this framework, RPGCL acknowledges that transmission pricing remains a major unresolved issue because wheeling charge regulations have not yet been formally approved by the Electricity Regulatory Commission.

Until the ERC formally issues binding wheeling charge directives, private investors cannot be legally assured that they will be allowed to collect these revenue components. This regulatory uncertainty significantly complicates financial closure and remains a major barrier to private sector participation in transmission infrastructure.

2.4 High Connection Costs for Small Projects

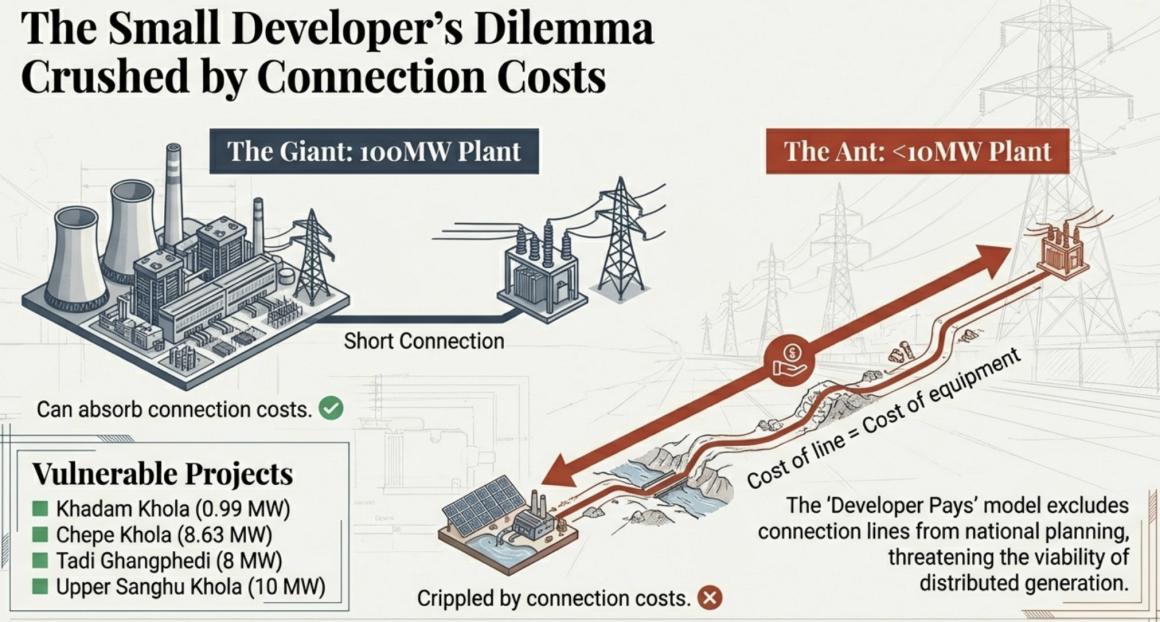

For small hydropower projects, particularly those under 10 MW, the cost of interconnection infrastructure – including transmission lines and switching facilities – can be disproportionately high, sometimes approaching or equaling the cost of the electro-mechanical equipment itself.

The current regulatory and policy framework explicitly places the responsibility for building interconnection lines on private developers. The Transmission System Development Plan (TSDP) clearly states that the cost of power plant connection lines is excluded from national transmission investment planning, based on the assumption that hydropower developers will construct their own connection infrastructure up to the nearest substation.

This “developer pays” model creates a significant structural disadvantage for smaller projects. A small 5 MW hydropower plant located far from the grid must bear the full cost of a dedicated transmission line, whereas a larger 100 MW project can spread this cost across much higher electricity sales and revenue.

Numerous small-scale hydropower projects fall within this vulnerable category and face these structural barriers. These include:

Khadam Khola SHP (0.99 MW), Chepe Khola SHEP (8.63 MW), Tadi Ghangphedi HEP (8 MW), Upper Sanghu Khola HEP (10 MW), Ankhukhola 1 HEP (8.4 MW), Upper Khoranga Khola SHP (7.5 MW), Upper Puwa-1 (3 MW), Chaku Khola (3 MW), Bhairab Kund Khola (3 MW), Midim Khola (3 MW and 0.1 MW), Ridi Khola (2.4 MW), Jiri Khola SHP (2.4 MW), Middle Chaku Khola (1.8 MW), and Syange (183 kW).

These projects are critical contributors to Nepal’s distributed generation capacity but face significant financial barriers due to high interconnection costs.

This barrier is even more pronounced in micro-hydropower projects, typically under 1 MW. The expansion of the national grid has begun to encroach upon areas served by existing micro-hydropower plants supported by the Alternative Energy Promotion Centre (AEPC). Without affordable interconnection options, many of these plants risk abandonment, resulting in wasted community investment and national resources.

A specific example is the Tara Khola Mini Hydropower Project (380 kW), which required extraordinary effort to achieve financial closure. The community had to establish a public limited company and rely on government subsidies covering 44% of the total project cost because raising sufficient equity was extremely difficult. This demonstrates how connection costs and overall capital expenditures create major financial barriers for small-scale projects.

Recognizing these challenges, the government has introduced several policy measures to mitigate these barriers. These include extending “Take-or-Pay” Power Purchase Agreements to projects under 10 MW to ensure revenue stability, providing transmission facility support for projects up to 3 MW operated at the local level, and offering escalation benefits for projects up to 25 MW that are financed in Nepali currency.

These policy interventions implicitly acknowledge that standard transmission connection costs are prohibitively high for smaller projects and require targeted support to ensure their viability.

3. Coordination Failures Between Generation and Transmission

3.1 The Persistent "Chicken-Egg" Problem

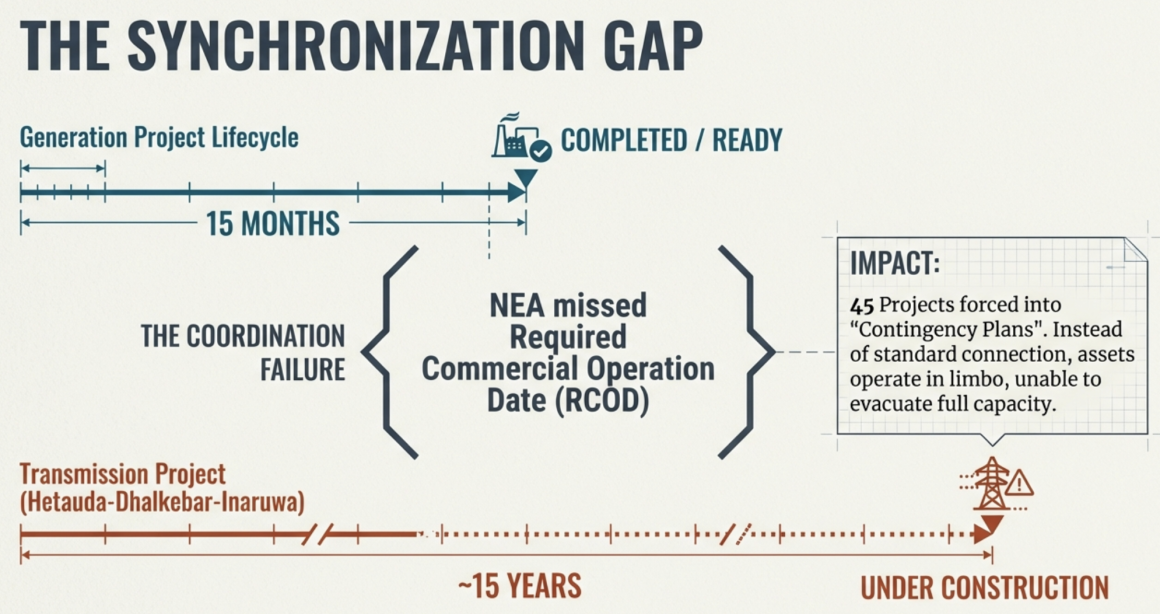

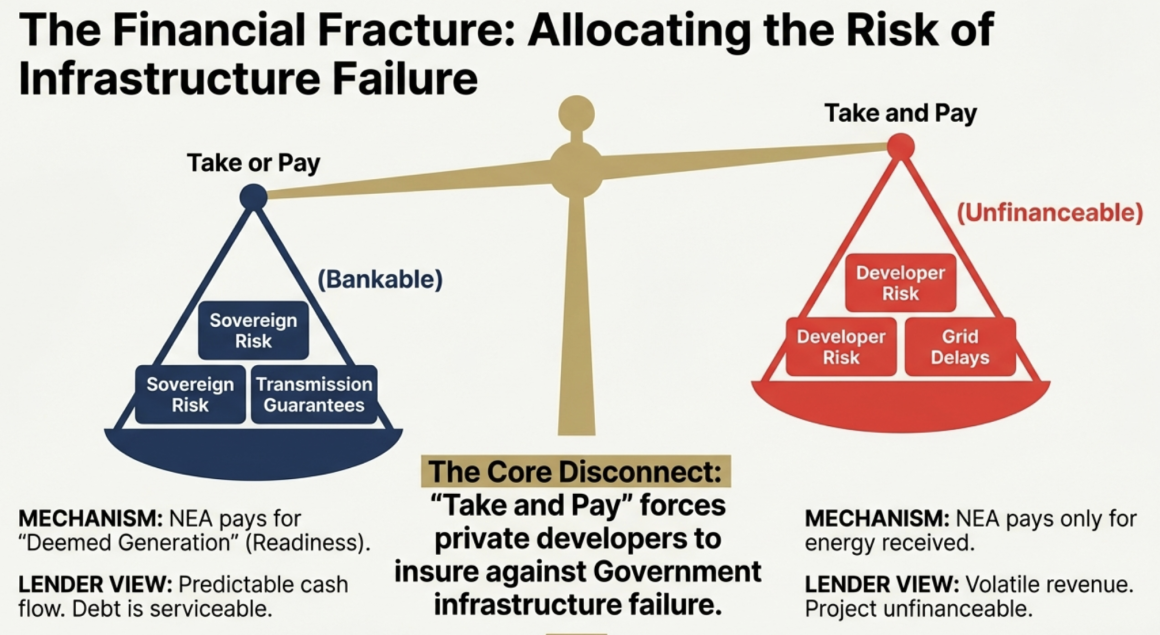

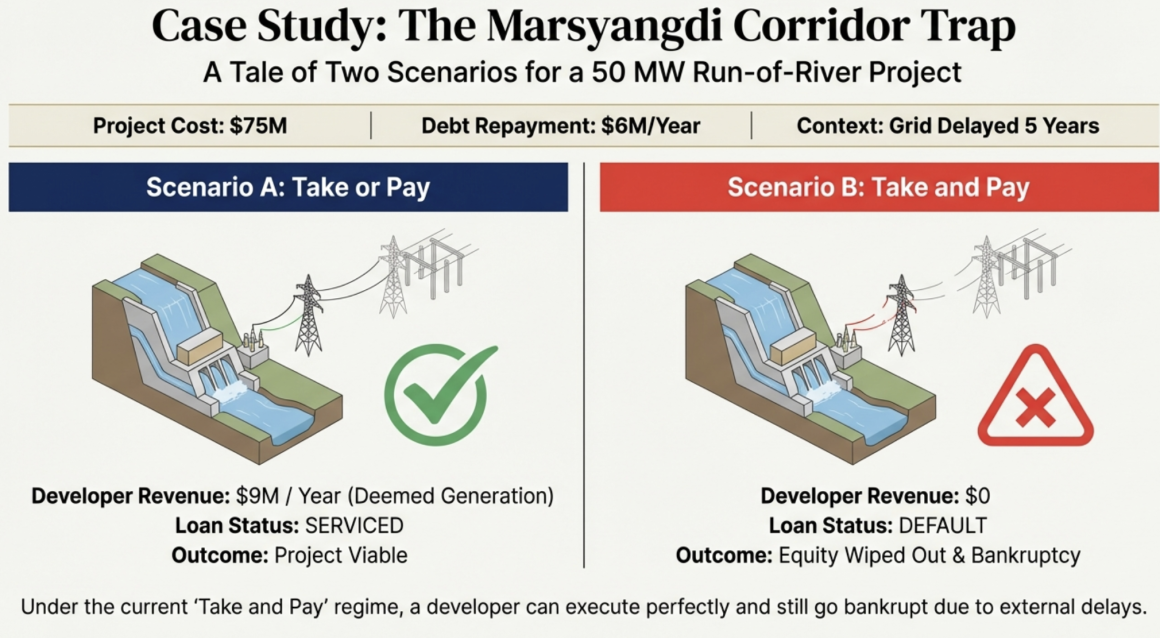

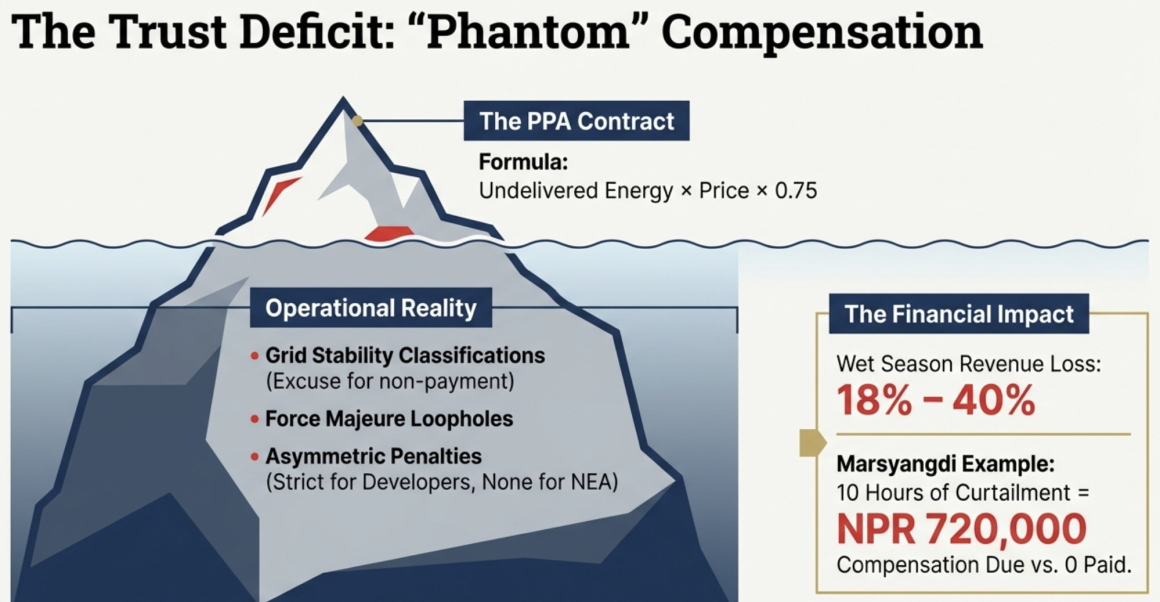

The most prominent structural challenge in Nepal’s power sector is the persistent infrastructure bottleneck in which generation projects are completed before the necessary evacuation infrastructure becomes operational, resulting in significant energy spillage and wastage. This coordination failure creates a classic “chicken-egg” dilemma: transmission infrastructure requires confirmed generation capacity to be financially viable, while generation projects require assured transmission availability to be bankable. When these timelines are misaligned, the consequences are severe and financially damaging. Approximately 45 hydropower projects have been forced to operate under “Contingency Plans” due to the Nepal Electricity Authority’s (NEA) failure to complete transmission lines and substations by the Required Commercial Operation Date (RCOD). Instead of benefiting from the standard “Take or Pay” protection, these projects were compelled to accept a “Take and Pay” arrangement, resulting in operating losses ranging from 18% to 40% of their expected income because they were unable to evacuate their full generation capacity.

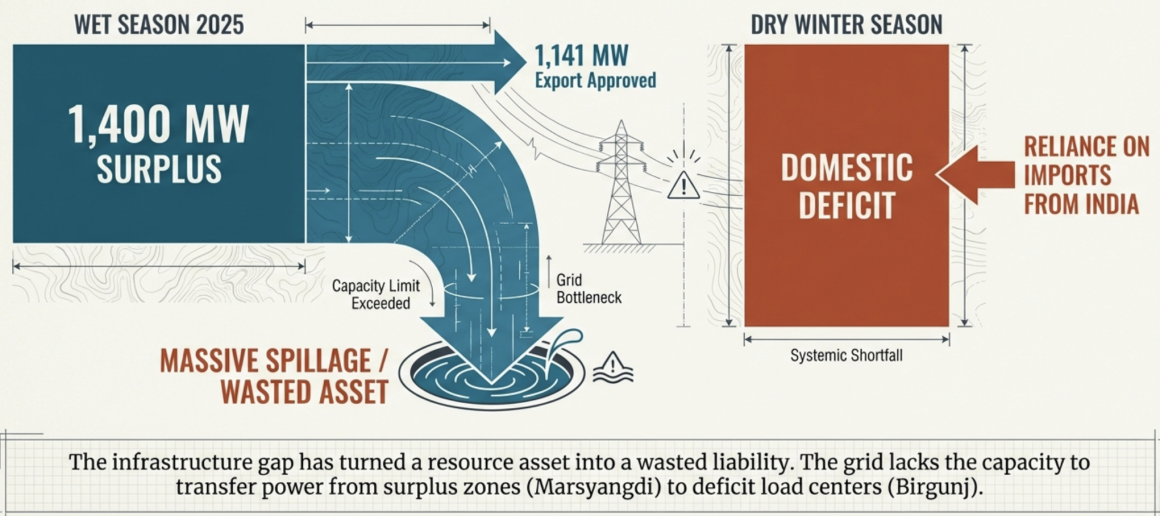

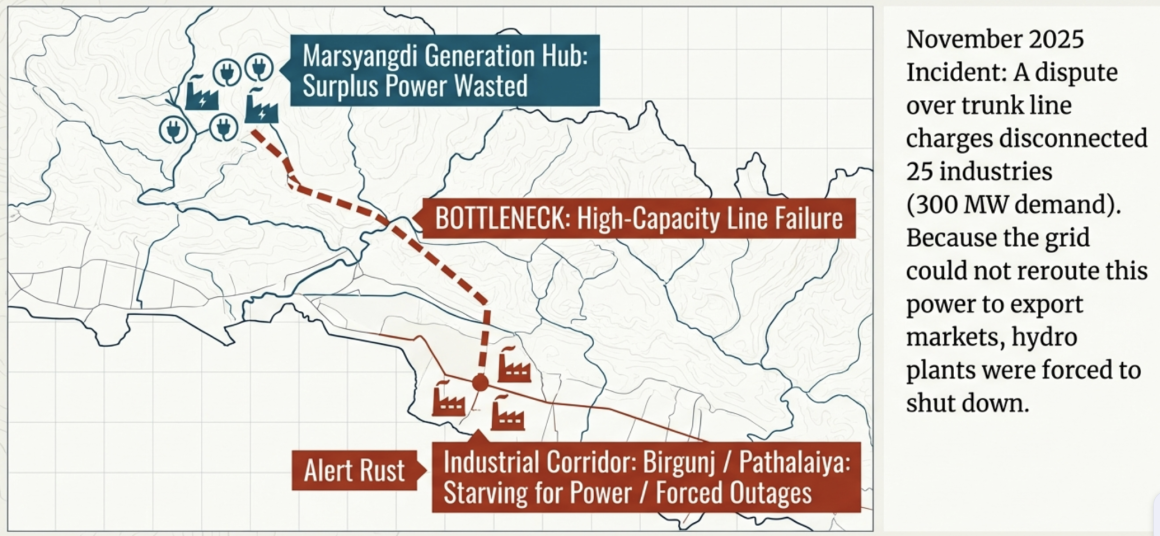

This infrastructure bottleneck has been widely described as a paradox in which Nepal possesses a vast reservoir of hydropower potential but lacks sufficient transmission capacity to deliver that energy to demand centers, effectively allowing valuable electricity to spill unused while shortages persist elsewhere. The Marsyangdi corridor provides one of the clearest examples of this inefficiency. Due to the failure to expand high-capacity internal transmission lines, electricity produced in the Marsyangdi corridor has been wasted, even as major industrial corridors such as Birgunj, Pathalaiya, and Biratnagar simultaneously face power shortages. This illustrates a fundamental structural inability to transfer power from surplus generation zones to deficit load centers.

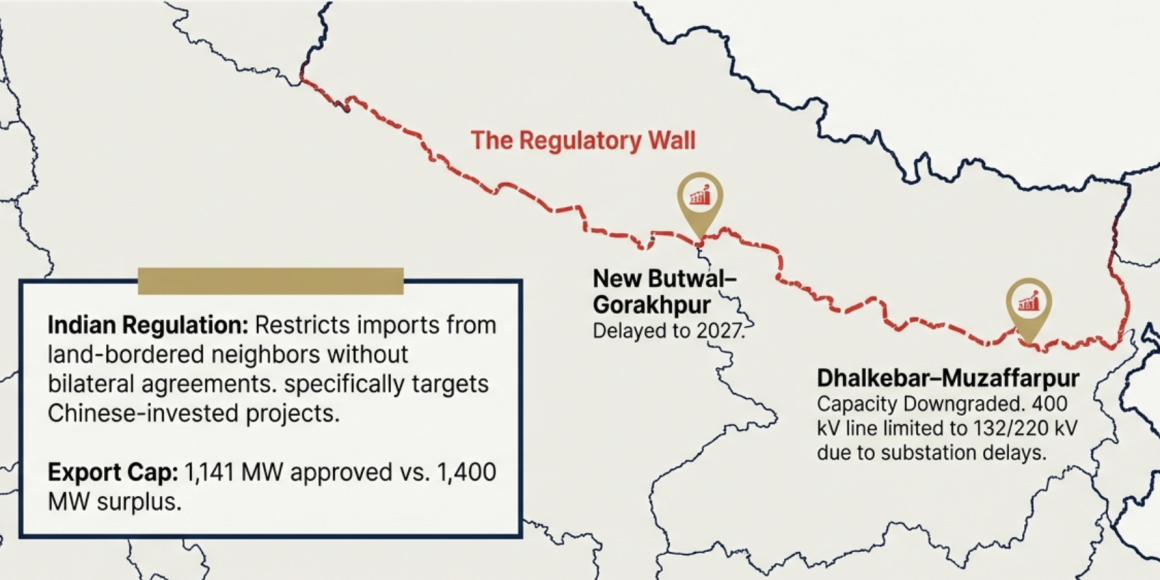

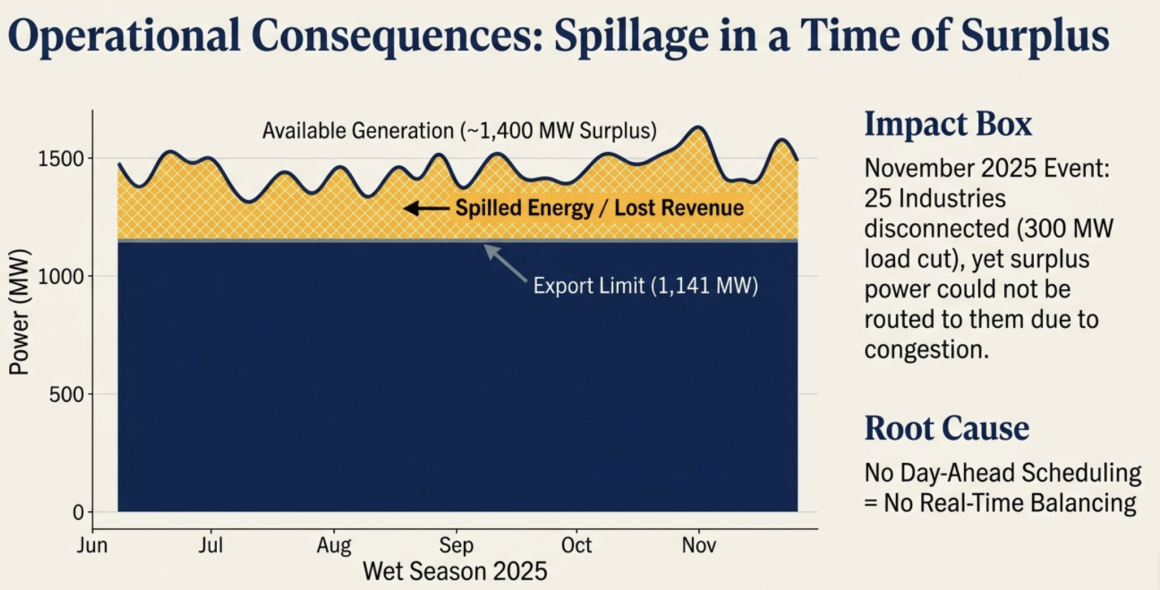

Seasonal surpluses have further exposed the weakness of the transmission network. During the wet season of 2025, Nepal’s electricity generation surplus reached approximately 1,400 MW. However, due to limited transmission capacity and export approval constraints – only 1,141 MW was approved for export – significant power spillage occurred. Notably, this spillage occurred primarily at NEA’s own power stations, demonstrating that even publicly owned generation assets were unable to fully utilize available transmission infrastructure.

Coordination failures have also been exacerbated by abrupt changes in domestic demand that transmission and export systems are unable to accommodate in real time. In November 2025, a dispute regarding dedicated trunk line charges led to the disconnection of 25 industries representing approximately 300 MW of demand. This sudden drop in domestic load, combined with the inability to immediately export surplus electricity due to infrastructure and protocol limitations, forced certain hydropower projects to shut down generation, resulting in additional financial losses and inefficiencies.

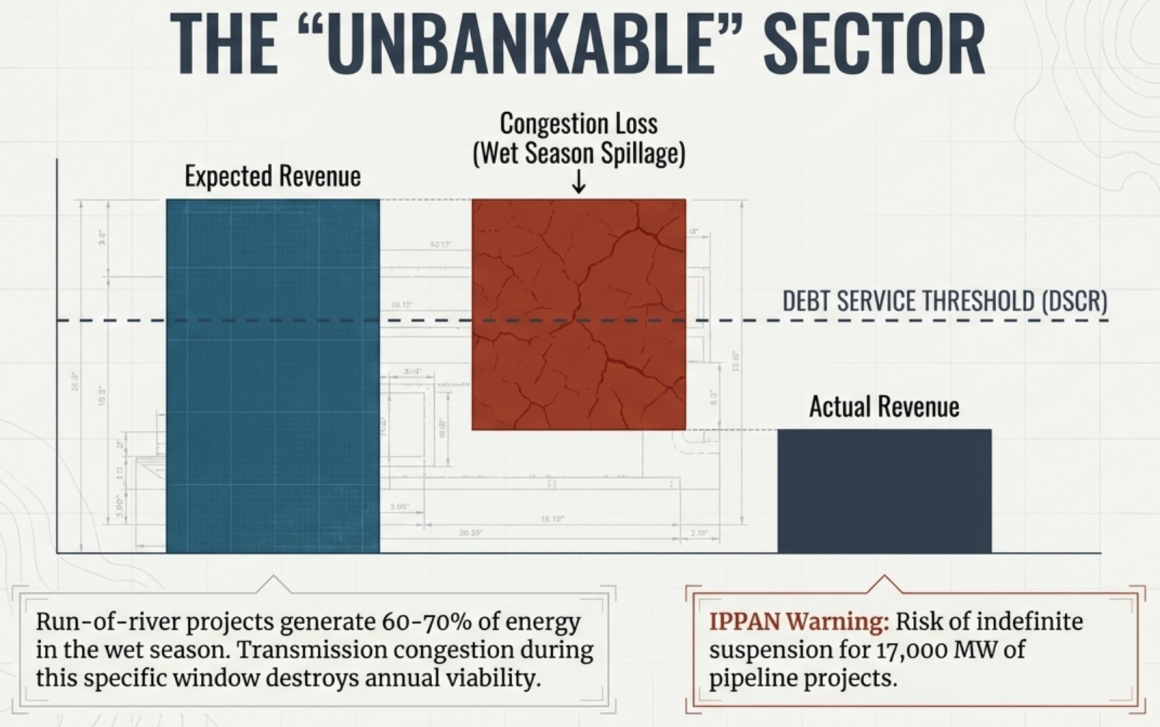

The financial consequences of this coordination failure have been compounded by a regressive policy shift from the protective “Take or Pay” model to the risk-shifting “Take and Pay” model. Under the standard “Take or Pay” arrangement, the NEA guarantees payment for deemed generation even if transmission infrastructure is not ready, thereby protecting developers from infrastructure delays. However, the fiscal policy for 2025/26 reintroduced the “Take and Pay” provision, under which the utility pays only for electricity that is actually delivered into the grid. This effectively transfers the risk of transmission unavailability from the state to private developers. Lenders have argued that projects operating under “Take and Pay” conditions are effectively unfinanceable due to the absence of guaranteed revenue streams. The Independent Power Producers Association Nepal (IPPAN) has warned that this policy shift could result in the indefinite suspension of approximately 17,000 MW of hydropower projects. Although the government has retained “Take or Pay” protection for small projects up to 10 MW, this exception implicitly confirms that projects larger than 10 MW are exposed to significantly greater financial risk under the current framework.

Major delays in backbone transmission infrastructure have further intensified the “chicken-egg” problem. The Hetauda-Dhalkebar-Inaruwa 400 kV transmission line, a strategically critical 288 km project, has been under construction for approximately 15 years without completion. This delay has severely limited the ability to transfer electricity from generation hubs to load centers, contributing directly to energy wastage and regional supply imbalances.

Cross-border transmission coordination failures have also illustrated this structural vulnerability. The NEA signed a Power Sales Agreement with PTC India to export electricity through the Dhalkebar–Muzaffarpur transmission line, but the agreement could not be executed because the transmission infrastructure was not commissioned on schedule. Simultaneously, the designated power generation plant on the Indian side failed to come online as planned. This situation exemplifies the “chicken-egg” problem in a cross-border context, where generation and transmission infrastructure must be developed in precise coordination to avoid stranded capacity.

Operational misalignment is further reflected in Nepal’s seasonal power imbalance. During the summer, surplus electricity is spilled due to inadequate transmission capacity and storage, while during the winter, the country faces a firm power deficit and must import electricity from India. This seasonal mismatch is exacerbated by the dominance of run-of-river projects, the lack of reservoir-based storage, and insufficient transmission corridors capable of balancing seasonal flows.

Private developers also face additional risks arising from hydrological variability. Developers are penalized for failing to generate contract energy due to changes in river flows associated with climate variability, despite the fact that hydrological assessments are conducted with the involvement of NEA experts. The government’s roadmap has acknowledged these challenges and indicated plans to remove such penalties, implicitly recognizing the systemic coordination failures that contribute to these risks.

3.2 Specific Cases of Generation Loss Due to Transmission Constraints

The Marsyangdi corridor remains one of the most prominent examples of generation loss caused by transmission constraints. Electricity produced in this corridor is being wasted due to the failure to expand high-capacity transmission infrastructure, even as major industrial centers such as Birgunj, Pathalaiya, and Biratnagar face simultaneous power shortages. This situation clearly illustrates the structural inefficiency of Nepal’s transmission network, which is unable to redistribute electricity from surplus regions to deficit areas.

The wet season of 2025 further demonstrated the magnitude of this problem. During this period, Nepal’s electricity generation surplus reached approximately 1,400 MW. However, export approvals and transmission constraints limited exports to only 1,141 MW, resulting in significant spillage of electricity. The available evidence indicates that this spillage occurred primarily at NEA-owned generation facilities, highlighting the systemic nature of the transmission bottleneck.

The prolonged delay in constructing the Hetauda-Dhalkebar-Inaruwa 400 kV transmission line has been a central factor contributing to these inefficiencies. After 15 years of construction, the line remains incomplete, severely restricting the transfer of electricity between generation centers and major load centers and exacerbating regional imbalances between supply and demand.

Financial losses resulting from transmission constraints are particularly severe for smaller projects. A study of 35 financially distressed small hydropower projects found that frequent disconnections in the 33 kV and 132 kV transmission systems resulted in annual generation losses of approximately NPR 190 million. Although this specific figure is not available, the broader financial distress of small hydropower projects is well documented. Among 91 listed hydropower companies, many have been unable to distribute dividends, and several have reported negative net worth, reflecting the systemic financial strain caused by transmission bottlenecks and evacuation constraints.

Additional coordination failures further illustrate the extent of the problem. In November 2025, the disconnection of 25 industries representing approximately 300 MW of demand led to forced shutdowns of hydropower plants because surplus electricity could not be immediately exported. Similarly, despite the Dhalkebar–Muzaffarpur transmission line having the capacity to import up to 800 MW, internal high-voltage transmission limitations have prevented effective distribution of imported electricity to domestic load centers.

Natural disasters have also exposed vulnerabilities in transmission infrastructure. Flooding in eastern Nepal affected more than 21 hydropower projects, damaging transmission lines and disrupting evacuation capacity. In total, more than 36 hydropower projects were impacted by flooding, further highlighting the fragility of transmission systems.

Institutional coordination failures have also stalled major projects at the planning stage. Approximately 221 hydropower projects with a combined capacity of 17,000 MW remain stalled due to conflicts involving national park and forest authorities, preventing construction of both generation and associated transmission infrastructure.

These constraints have contributed to a paradoxical situation in which Nepal exports surplus electricity during the wet season while simultaneously importing electricity and even resuming load shedding during the winter months due to inadequate transmission capacity, storage, and seasonal balancing capability.

3.3 Inadequate Risk Allocation

The allocation of risk associated with transmission availability remains one of the most contentious structural weaknesses in Nepal’s electricity sector. The government has increasingly shifted transmission and market risk from the public sector to private developers through the introduction of “Take and Pay” provisions. This policy shift fundamentally alters the financial risk structure of hydropower projects.

Under the standard “Take or Pay” Power Purchase Agreement model, the Nepal Electricity Authority guarantees payment for electricity that a project is capable of generating, even if transmission infrastructure is not available to evacuate the power. This model places the risk of transmission delays on the utility and ensures predictable revenue streams for developers, allowing them to repay loans and attract financing. Recognizing the importance of this protection, the government has retained the “Take or Pay” principle for smaller projects under 10 MW.

However, under the “Take and Pay” arrangement, the NEA pays only for electricity that is actually delivered into the grid. This shifts the risk of transmission delays entirely onto private developers. If transmission infrastructure is not available, electricity is spilled and developers receive no payment for the lost generation. This creates a destructive cycle: developers complete projects, transmission lines are delayed, the NEA refuses payment for deemed generation, developers are forced into contingency arrangements, revenues collapse, and loan defaults become likely.

The financial consequences of this shift are severe. Because run-of-river hydropower projects generate approximately 60% to 70% of their annual energy during the wet season, transmission congestion during this period can result in substantial energy losses. For example, if a project generates 100 units of electricity annually but loses 20 units due to transmission constraints, revenue falls by 20%. In practice, such losses can range between 18% and 40% of total income, as reported by IPPAN. This level of revenue loss destroys the Debt Service Coverage Ratio required by banks, rendering projects financially unviable and unfinanceable.

Although Power Purchase Agreements formally provide for compensation for “Undelivered Energy” resulting from dispatch instructions or curtailment, this provision is rarely implemented in practice. Because the NEA controls the Load Dispatch Center, curtailments are often classified as technical or grid stability requirements rather than commercial failures, allowing the utility to avoid compensation obligations. As a result, developers bear the full financial impact of curtailment.

In practical terms, this risk allocation framework has transformed Nepal’s hydropower sector from a predictable, bankable investment environment into one characterized by volatile revenue streams, reduced investor confidence, and increased financing risk. Under the theoretical “Take or Pay” model, revenue stability is high and bankability is strong. Under the current “Take and Pay” reality, revenue stability is low, financial losses range between 18% and 40%, and many projects are considered unfinanceable due to the absence of guaranteed transmission access and payment security.

4. Land Acquisition and Right of Way Challenges

4.1 Critical Delays in Land Acquisition

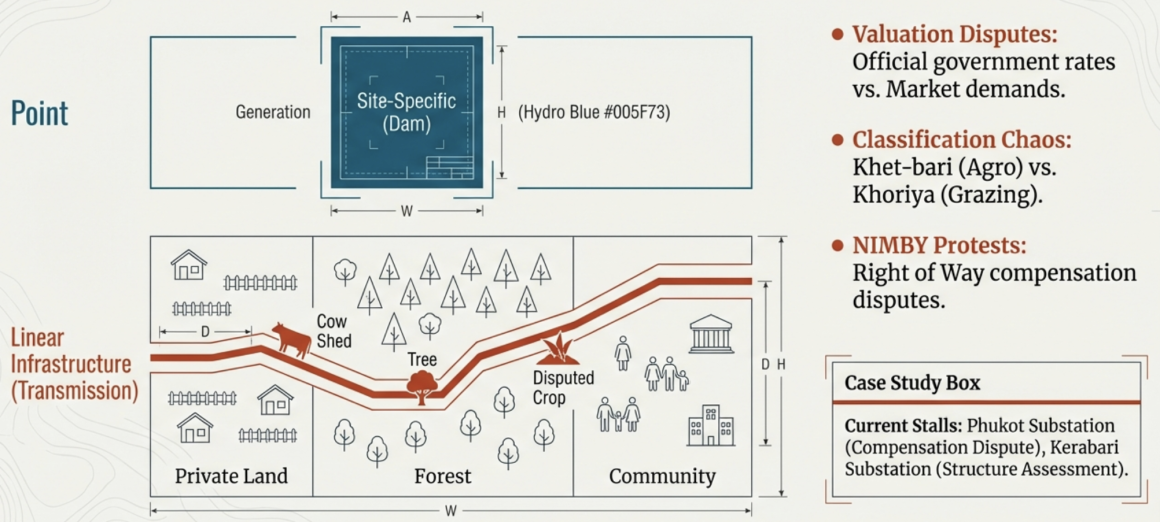

Securing land and Right of Way (RoW) is widely described as a “critical undertaking” and remains one of the most significant causes of delay in transmission projects. There are frequent disputes over land compensation, compounded by difficulties in classifying private land – particularly in distinguishing between agricultural land (khet-bari), grazing land (khoriya), and residential plots (gharedi). The absence of clear and consistent legal provisions governing compensation determination for RoW creates local disputes that can stall construction for extended periods. Unlike generation projects, which are typically confined to specific sites, transmission lines traverse vast distances across multiple jurisdictions, making land acquisition exponentially more complex. This process often requires negotiating with hundreds of individual landowners, each with different expectations, claims, and socio-economic circumstances, creating an enormous administrative burden and increasing the likelihood of prolonged delays.

Land acquisition for transmission is far more complex than for generation because it involves numerous jurisdictions and stakeholders. The RPGCL Corporate Plan explicitly identifies land acquisition and RoW as a “critical undertaking,” and highlights how the absence of a coherent land management policy leads to conflicts over land classification and valuation. The government’s land valuation system is described as “dated” and “largely unacceptable” to local communities, forcing projects in many cases to pay compensation several times higher than official valuations in order to secure cooperation.

Operational challenges specific to RoW also create further delays. For example, in the Kerabari–New Marsyangdi transmission line, compensation assessment must cover not only land but also houses, sheds (including cow sheds), crops, and trees located within the RoW corridor. Determining compensation for these physical structures has proven to be a major procedural hurdle. There is also persistent policy friction over how to treat permanent versus temporary structures, further complicating the process. Public resistance is common, reflecting a widespread “Not In My Backyard” (NIMBY) sentiment, with even senior policymakers acknowledging that communities often protest when transmission towers are proposed on their land.

Specific project cases illustrate the practical consequences of these challenges. At the Phukot Substation in the Karnali Corridor, although 113 ropanies of land were technically acquired, the project remains stuck in the compensation determination phase. Similarly, the Kerabari Substation project has faced delays while assessing compensation for tower pads and structures under the RoW. The Nalgad Substation in the Bheri Corridor required acquisition of 116 ropanies and involved lengthy coordination with the Jajarkot district administration. At a broader level, land access and forest clearance failures have stalled 221 hydropower projects totaling 17,000 MW, demonstrating the systemic scale of land-related bottlenecks.

The administrative burden associated with land acquisition is also exceptionally high. Developers must navigate 7 ministries, 23 departments, and 36 different laws, with approval files moving through multiple layers – from the Department of Electricity Development to the Ministries of Energy, Forests, Land Management, Home, and Defense – often becoming stalled at lower administrative levels for months. Legal constraints further complicate the process; for example, the 75 ropani ceiling on land acquisition is widely considered insufficient for large-scale infrastructure, forcing developers to seek special exemptions. Similarly, the 1:25 tree replacement requirement, which mandates planting 25 trees for every tree cut, creates a paradox in which developers cannot find sufficient land to meet replacement obligations, thereby delaying RoW clearance and project execution.

4.2 Environmental and Forest Clearance Bottlenecks

Obtaining approvals for tree cutting and Environmental Impact Assessments (EIA) is an extremely cumbersome and time-consuming process, involving coordination with up to 16 ministries, 40 departments, and over 200 desks or administrative units. Although the law requires environmental clearance within 30 days, in practice approvals often take years. Nepal’s geography ensures that transmission corridors frequently pass through forested areas, national parks, and other environmentally sensitive zones, adding further layers of regulatory complexity. Conflicting guidelines between the Department of Electricity Development, the Ministry of Forests and Environment, and the Department of National Parks frequently create procedural deadlocks. As a result, developers are often forced to redesign transmission routes, undertake additional environmental mitigation measures, and absorb significant cost increases.

The scale of the administrative burden is is such that while physical construction of hydropower infrastructure might take as little as 15 months, the regulatory approval process alone can take up to seven years. Redundancies in regulatory processes further worsen delays. For example, developers seeking to issue public shares must obtain approvals from both the Electricity Regulatory Commission and the Securities Board, creating duplicative procedures that slow project financing.

One of the most significant regulatory disruptions occurred following a Supreme Court ruling in early 2025, which restricted infrastructure development in protected areas. This single ruling stalled 221 hydropower projects totaling 17,000 MW, as developers were denied permission even to enter forest areas despite having obtained generation licenses. Many of Nepal’s most economically viable hydropower sites are located in environmentally protected regions, meaning this regulatory conflict directly undermines national energy development targets.

Environmental approval delays are further aggravated by institutional conflicts and procedural inefficiencies. Although EIAs are legally required to be approved within 30 days, approvals frequently take years. Forestry authorities often blame developers for submitting inadequate or “copy-paste” environmental studies, while developers accuse officials of unnecessarily delaying files. Even minor design changes after approval require complete revision of environmental studies, resulting in delays and cost increases amounting to crores of rupees.

Specific forestry regulations also create impractical implementation challenges. The 1:25 tree replacement rule is particularly difficult to comply with due to land scarcity near community forests, prompting developers to request a reduction to a 1:5 ratio. Additionally, land classification errors – particularly in the Terai region, where long-settled areas are still officially designated as forests – complicate land acquisition and RoW clearance. Institutional coordination failures exacerbate the situation, as the Department of Electricity Development often grants licenses without prior coordination with forest authorities, leading to situations where developers obtain licenses but are later blocked by forest agencies.

These challenges are reflected in real project delays. The strategic Hetauda–Dhalkebar–Inaruwa 400 kV transmission line, for example, has remained under construction for 15 years largely due to forestry clearance and RoW disputes. Similarly, the Kerabari–New Marsyangdi transmission line faced prolonged delays due to forest clearance and compensation determination. Even unrelated regulatory requirements, such as approvals to import explosives necessary for tunneling, must pass through multiple ministries, creating further bottlenecks and forcing developers to request extensions to project completion deadlines.

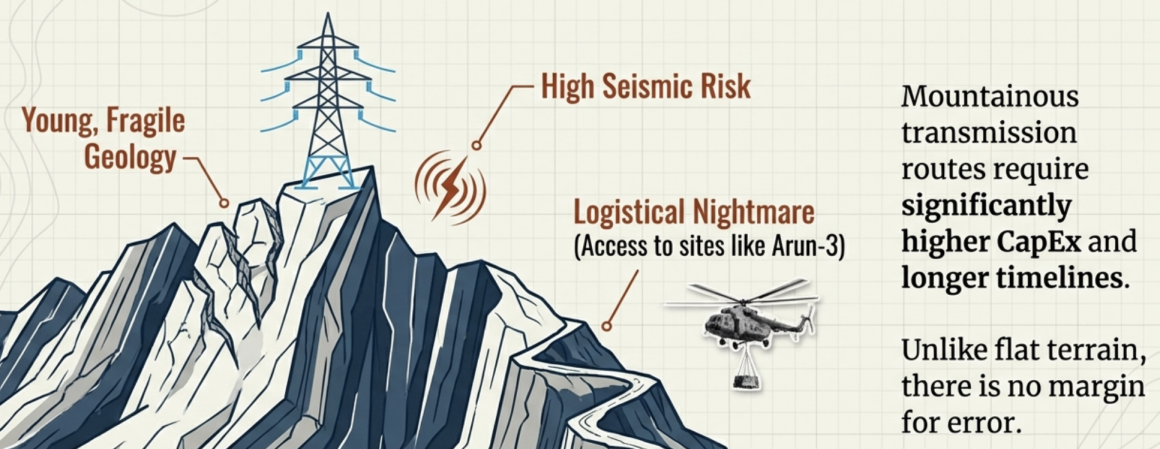

4.3 Geographic and Terrain Challenges

Nepal’s rugged Himalayan terrain presents fundamental physical challenges for transmission infrastructure development. Mountainous routes require specialized engineering, longer construction timelines, and significantly higher costs compared to flat terrain. Transmission lines must traverse steep slopes, unstable geology, and remote regions, increasing both construction complexity and long-term maintenance requirements. The terrain is described as young, steep, and geologically fragile, requiring detailed geological assessments that extend project timelines and increase costs.

Natural disasters further compound these challenges. Climate-induced floods and landslides increasingly threaten infrastructure stability, introducing significant operational and financial risks. In the eastern region, floods originating in Sankhuwasabha affected over 21 hydropower projects, damaging infrastructure and preventing power evacuation. More broadly, recent flooding events have damaged more than 36 hydropower projects, disrupting both generation and transmission systems. Monsoon-related flooding has repeatedly damaged transmission infrastructure, while the release of water from reservoirs such as Kulekhani has caused downstream destruction, demonstrating the interconnected risks of hydropower and transmission systems.

Glacial Lake Outburst Floods (GLOFs) present an additional and growing threat. For example, a GLOF event in Rasuwa damaged infrastructure including the Miteri Bridge near the Nepal–China border. These disasters highlight the vulnerability of transmission infrastructure in high-altitude regions exposed to climate change impacts.

The geography itself also complicates construction logistics. Projects such as the Arun-3 Hydroelectric Project faced significant delays due to remoteness and difficult terrain, which made transportation of equipment and construction materials extremely challenging. Transmission corridors must connect remote Himalayan generation sites with load centers in the Terai plains, exposing infrastructure to storms, landslides, and geological instability along the entire route.

These physical risks translate directly into financial and investment challenges. Insurance companies are increasingly reluctant to insure hydropower and transmission infrastructure due to the rising frequency of climate-related damage. Even when insurance is available, coverage conditions are stringent and claims are difficult to obtain. As a result, developers face greater financial uncertainty, and the sector increasingly requires climate finance and specialized risk-sharing mechanisms to manage these unpredictable risks.

5. Institutional and Ownership Structure Issues

5.1 NEA Monopoly and Incomplete Unbundling

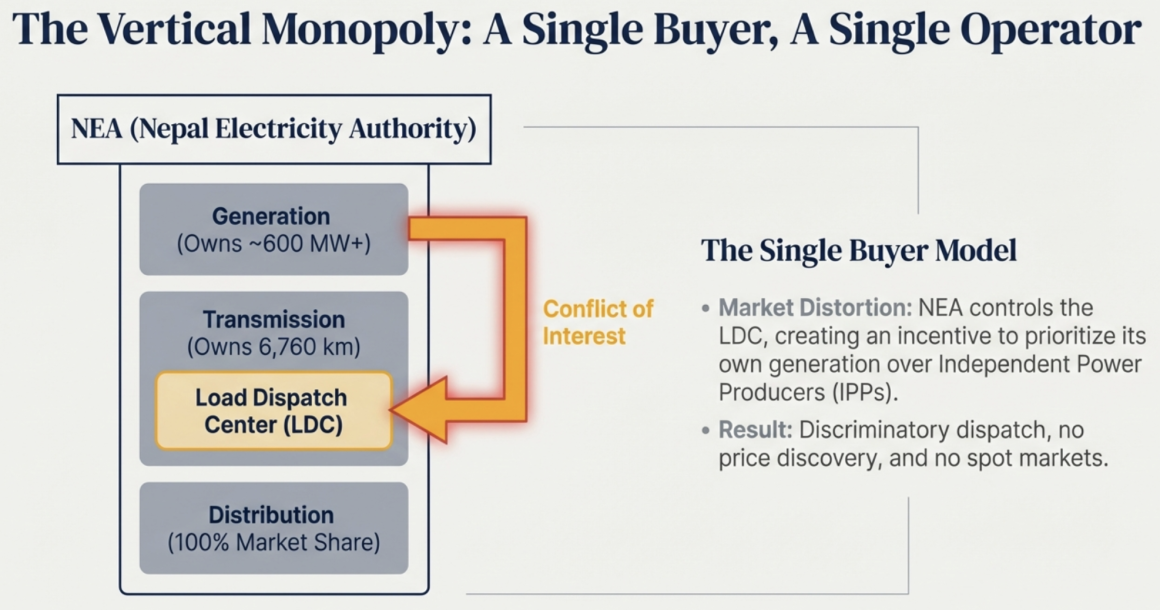

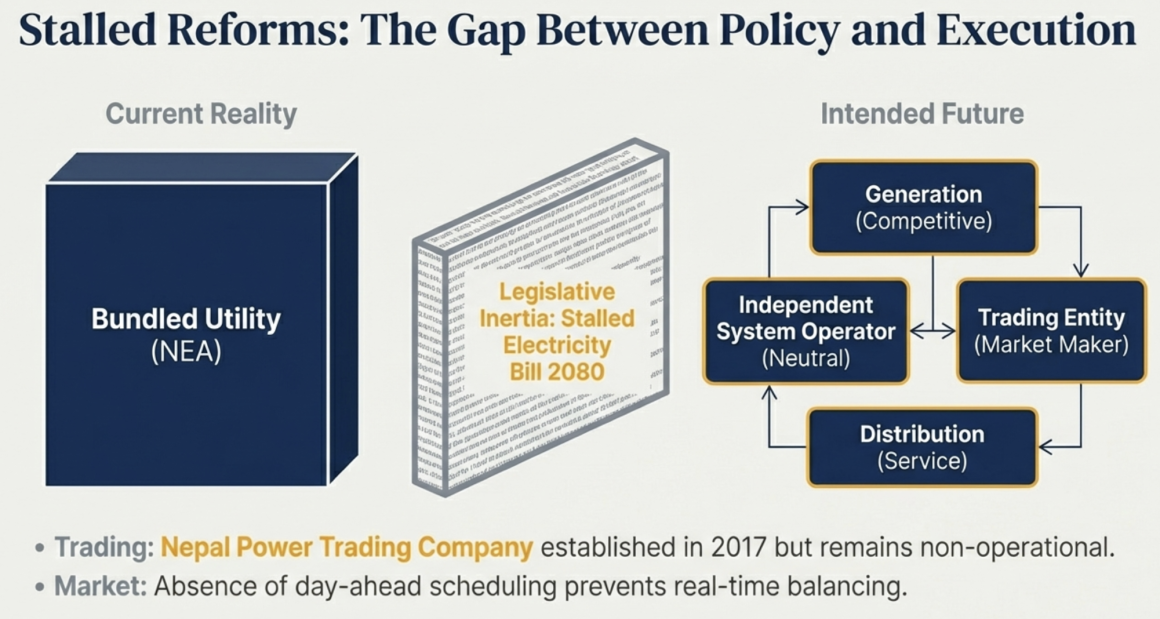

The Nepal Electricity Authority (NEA) currently holds a dominant monopoly over Nepal’s electricity sector, functioning as a vertically integrated utility that owns and operates more than 95% of the value chain, including generation, transmission, and distribution. Although Nepal’s policy framework formally supports the unbundling of NEA into separate generation, transmission, system operation, and trading entities to enable a multi-buyer, multi-seller electricity market, this structural reform remains incomplete. The proposed Electricity Bill 2080 is intended to dismantle the vertically integrated monopoly and establish an independent and competitive market structure. However, its stalled passage has prevented the implementation of these reforms. As a result, NEA’s vertically integrated monopoly continues to limit competition, weaken efficiency incentives, and create inherent conflicts of interest, particularly because NEA simultaneously functions as a major generator, transmission owner, system operator, and single buyer.

Unbundling is fundamentally intended to transition the electricity sector from a state-controlled monopoly to a competitive, efficient, and transparent market system. One of the primary structural problems unbundling seeks to resolve is the conflict of interest in system operation. At present, NEA controls the Load Dispatch Center (LDC), which determines dispatch priority and decides whose electricity enters the national grid. This creates a structural bias because NEA, as both generator and system operator, has the ability and incentive to prioritize its own generation over that of private Independent Power Producers (IPPs). Unbundling would separate the System Operator from generation ownership, ensuring a neutral and independent grid operator – proposed to be the Rastriya Prasaran Grid Company Limited (RPGCL) – which would manage the grid under a non-discriminatory Open Access regime. This would ensure equal treatment of all generators, both public and private.

Unbundling is also necessary to enable the transition from the current “single buyer” model to a competitive multi-buyer, multi-seller electricity market. At present, NEA is the only authorized bulk buyer of electricity, which prevents the development of power trading markets. Structural separation would allow the establishment of independent trading entities, such as the licensed but not yet operational Nepal Power Trading Company, enabling electricity to be bought and sold both domestically and across borders. It would also enable the operationalization of General Network Access (GNA), allowing generators to sell power directly to bulk consumers, including industries and cross-border markets, by paying wheeling charges to the transmission network operator instead of being forced to sell exclusively to NEA.

Unbundling is further critical from the perspective of financial sustainability and investment mobilization. Nepal’s power sector expansion targets for 2035 require approximately USD 46.5 billion in investment, an amount that cannot be financed solely through government and NEA resources. Structural separation would allow private sector participation specifically in transmission infrastructure and trading through mechanisms such as Tariff-Based Competitive Bidding (TBCB), reducing the sovereign financing burden while introducing private sector efficiency, innovation, and risk-sharing into infrastructure development.

The current vertically integrated bundled structure of NEA has also created significant operational inefficiencies and market stagnation. Because NEA controls the entire electricity value chain, power trading by entities other than NEA has virtually no operational space. There are no functional market-based trading rules, and the sector continues to operate under a single-buyer framework, preventing price discovery and competitive efficiency. The absence of a market-based structure has also resulted in operational inefficiencies, including the lack of day-ahead scheduling and demand forecasting. The Load Dispatch Center does not receive advance demand estimates from distributors or large consumers, which prevents the functioning of spot markets and real-time balancing mechanisms. Consequently, electricity may be spilled in surplus regions while shortages persist elsewhere.

The vertically integrated structure has also contributed to infrastructure bottlenecks and delayed transmission development. For example, the strategic Hetauda-Dhalkebar-Inaruwa 400 kV transmission line has remained under construction for over 15 years without completion, preventing efficient evacuation of electricity from surplus hydropower corridors such as Marsyangdi to major load centers and industrial corridors such as Birgunj. This has resulted in both economic losses and inefficient utilization of generation capacity.

In addition, the monopoly structure has created significant barriers to private sector participation and market evolution. Even though a power trading company was established as an NEA subsidiary in 2017, it has not been operationalized, effectively preserving NEA’s dominance over domestic and cross-border electricity trade. This institutional inertia reflects the natural monopoly characteristics of vertically integrated utilities, which tend to resist structural reforms that would dilute their market control.

While unbundling is widely recognized as necessary, the transition itself presents implementation challenges. Transmission infrastructure remains a natural monopoly network business, and shifting to competitive bidding models such as TBCB may result in limited participation or higher tariffs if not supported by appropriate regulatory benchmarks and safeguards. Furthermore, the transfer of transmission assets from NEA to newly created entities such as RPGCL involves complex legal, financial, and administrative restructuring processes that are still ongoing.

5.2 RPGCL's Evolving Role

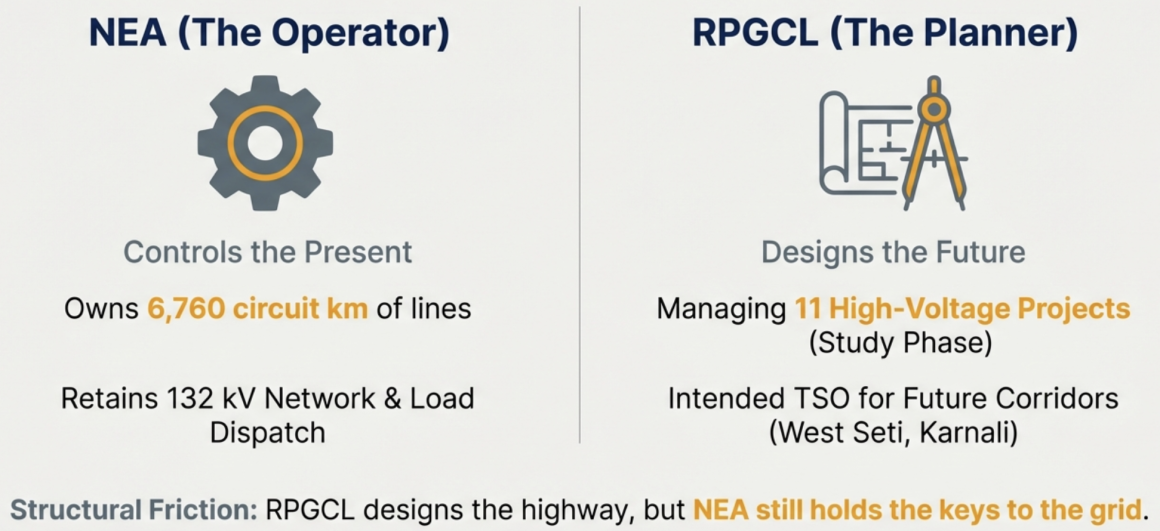

The Rastriya Prasaran Grid Company Limited (RPGCL) was established in 2015 as a government-owned company under the Ministry of Energy, Water Resources and Irrigation to specialize in the development, ownership, and operation of Nepal’s national transmission infrastructure. RPGCL was created as a key institutional vehicle to support the unbundling of NEA and to eventually function as an independent Transmission System Operator (TSO). However, despite its establishment and strategic importance, RPGCL’s operational role remains incompletely defined, and its institutional capacity continues to evolve.

At present, RPGCL performs multiple overlapping functions, including project developer, infrastructure owner, transmission operator, and public-private partnership facilitator. However, the transition of actual operational transmission assets from NEA to RPGCL has not yet been completed. NEA continues to own and operate Nepal’s existing high-voltage transmission grid, which consists of more than 6,760 circuit kilometers of transmission lines, while RPGCL is currently undertaking only 11 high-voltage transmission projects. These projects are primarily in the study, design, or pre-construction phases rather than being operational assets transferred from NEA. This has resulted in a dual-entity structure where RPGCL is largely responsible for planning and future expansion, while NEA remains the operator of the existing grid. This arrangement creates coordination challenges, operational overlaps, and unclear delineation of institutional responsibilities.

Although no operational transmission infrastructure has yet been formally transferred, the policy framework and corporate governance structure clearly mandate such a transition. RPGCL’s Articles of Association and government policy explicitly state that NEA’s electricity transmission assets will be gradually transferred to RPGCL to facilitate sector unbundling and establish RPGCL as the independent grid owner and operator.

RPGCL’s corporate strategic plan specifically outlines a phased acquisition strategy targeting high-voltage transmission assets of 220 kV and above, while leaving lower-voltage networks such as 132 kV lines with NEA to simplify the restructuring process. The transferred assets would be reflected as equity contributions by NEA in RPGCL, thereby preserving government ownership while separating operational responsibilities.

Several existing and under-construction NEA transmission assets have been identified as future candidates for transfer. These include 220 kV lines such as Khimti-Dhalkebar, Hetauda-Bharatpur, and Chilime-Trishuli; key Koshi Corridor lines including Inaruwa-Basantpur-Tumlingtar; Marsyangdi Corridor lines including Udipur-Bharatpur and Marsyangdi-Kathmandu; and Kali Gandaki Corridor lines including Dana-Kusma-New Butwal. Major 400 kV assets identified for future transfer include the Hetauda-Dhalkebar-Inaruwa backbone corridor, the Tamakoshi-Kathmandu line, and the Dhalkebar 400/220 kV substation.

Instead of managing transferred assets, RPGCL is currently focused on developing new high-capacity corridor-based transmission infrastructure designed to evacuate power from major hydropower generation hubs. These include the West Seti Corridor 400 kV line, Karnali Corridor transmission infrastructure, Bheri Corridor projects such as Nalgad-Maintada, Arun Corridor projects such as Haitar-Sitalpati, and smaller interconnection lines such as Nupche Likhu.

Overall, the current institutional arrangement effectively reflects a transitional “planning versus operation” split. RPGCL is responsible for planning and developing Nepal’s future transmission highways, while NEA continues to operate the existing national grid. The legal and financial transfer of high-voltage backbone infrastructure remains a strategic objective for implementation in the coming years, but it has not yet been fully executed.

5.3 Limited Private Sector Participation

Private sector participation in Nepal’s transmission sector remains limited, particularly in terms of ownership of national grid infrastructure. Independent Power Producers (IPPs) typically own only dedicated connection lines linking their generation facilities to the nearest NEA substation rather than owning or operating common carrier transmission infrastructure. Although Nepal’s legal framework formally permits private participation through mechanisms such as the Build-Own-Operate-Transfer (BOOT) model, practical implementation has been constrained by multiple institutional, regulatory, and financial barriers.

Private investors face significant uncertainty due to incomplete sector reforms, lack of operational power trading rules, and absence of a fully functional open access regime. Transmission investments are also structurally less attractive than generation investments because they involve lower financial returns, longer payback periods, and higher regulatory risks. In addition, developers face “contingency risk,” where transmission bottlenecks prevent evacuation of generated electricity, forcing developers to absorb financial losses due to underutilized capacity.

The regulatory framework for Public-Private Partnerships (PPP) in Nepal’s transmission sector is currently evolving from a traditional cost-plus government-controlled model toward competitive, market-based investment models designed to attract private capital. This framework is governed by the PPP and Investment Act 2019, the Electricity Act 1992, and newly introduced investment partnership procedures developed by RPGCL.

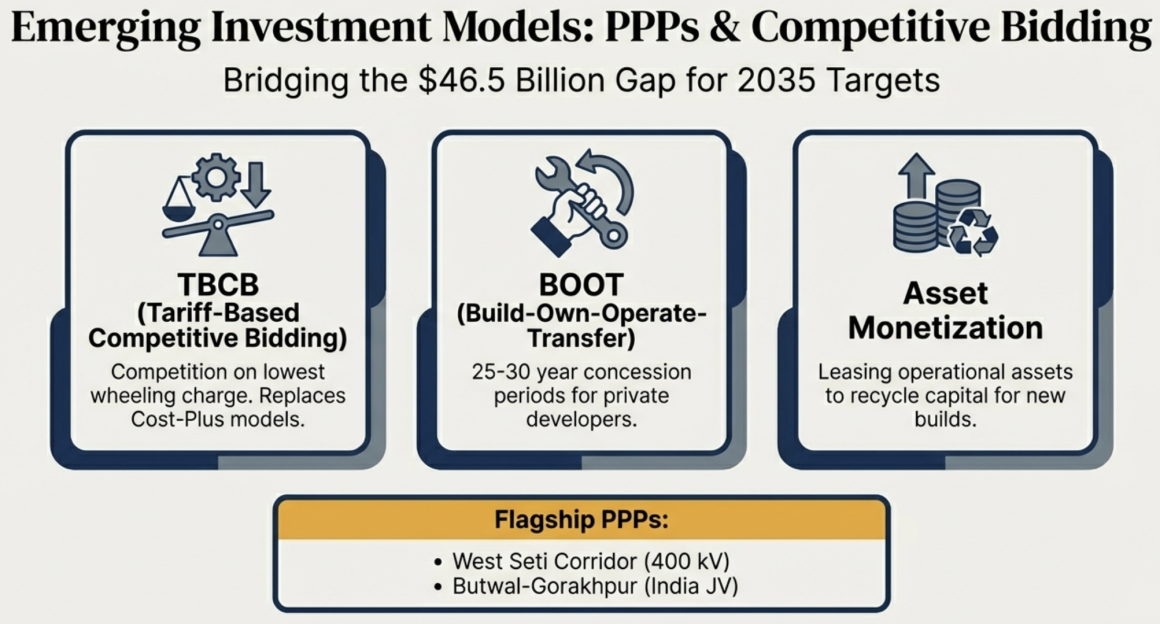

A major reform is the introduction of Tariff-Based Competitive Bidding (TBCB), under which private developers compete to build and operate specific transmission lines based on the lowest wheeling charge they require. This approach allows market competition to determine transmission tariffs instead of relying on administratively determined costs, improving efficiency and reducing public financing burdens.

The PPP and Investment Act 2019 designates the Investment Board Nepal as the primary agency responsible for facilitating large transmission PPP projects exceeding NPR 6 billion, providing centralized approvals and investment facilitation. RPGCL has also introduced the Transmission Project Investment Partnership Procedure 2082, allowing the formation of joint venture companies and special purpose vehicles with private investors to develop specific transmission corridors.

Another emerging mechanism is asset monetization, which involves leasing operational transmission assets to private operators for fixed concession periods in exchange for upfront payments. This model enables the government to recycle capital from existing infrastructure into new transmission investments.

The BOOT model remains the foundational legal instrument for private transmission investment, allowing developers to construct, own, and operate transmission infrastructure for concession periods typically ranging from 25 to 30 years before transferring ownership back to the government.

Several major transmission projects have been identified for development under PPP modalities. These include the West Seti Corridor 400 kV transmission line, the Tamor-Dhungesanghu 220 kV project developed through a subsidiary company structure with RPGCL equity participation, the Haitar-Sitalpati 400 kV Arun Corridor transmission line, and the Lambagar-Barhabise 220 kV transmission project supporting the Upper Tamakoshi region. Cross-border transmission projects such as the Butwal-Gorakhpur 400 kV line, implemented through joint venture structures between NEA and India’s Power Grid Corporation, also represent important precedents for corporate-structured transmission ownership.

Despite these developments, most privately owned transmission infrastructure in Nepal remains limited to dedicated connection lines rather than integrated national grid corridors. The transition toward meaningful private sector participation in backbone transmission infrastructure is still in its early stages and depends heavily on the successful implementation of unbundling, regulatory reform, and market development.

6. Technical and Planning Deficiencies

6.1 Historical Infrastructure Lag

Transmission infrastructure development in Nepal has historically lagged behind generation expansion rather than anticipating or keeping pace with the needs of new power plants. The existing transmission network remains heavily dominated by 132 kV lines, while higher-capacity infrastructure such as 220 kV and 400 kV lines is still in the process of development. This imbalance reflects a historically “pessimistic” planning approach toward domestic electricity demand growth, resulting in undersized transmission infrastructure that has quickly become congested as generation capacity expanded. This historical underinvestment has created a structural bottleneck in which generation capacity has outpaced transmission capability, forcing curtailment of electricity generation even when water resources and generation capacity are available.

This pessimistic planning approach is explicitly documented in the Transmission System Development Plan (TSDP), which critiques earlier master plans such as the 2015 plan and the Joint Technical Team (JTT) plan for failing to adequately incorporate newly identified generation projects and for underestimating Nepal’s domestic load growth. These earlier plans assumed relatively low internal demand growth and consequently designed transmission infrastructure primarily to facilitate export-oriented generation rather than to support high domestic consumption. As a result, transmission infrastructure was not sized to accommodate the scale of hydropower development that subsequently occurred.

Historically, transmission development received comparatively less attention than generation expansion. Transmission planning was treated as a secondary priority and evolved through an ad hoc approach rather than a coordinated, forward-looking national strategy. While government and private sector stakeholders aggressively licensed and developed hydropower projects, transmission infrastructure development did not progress at a comparable pace. This mismatch created a widening gap between generation capacity and transmission capability, resulting in increasing congestion and inefficiencies in the grid.

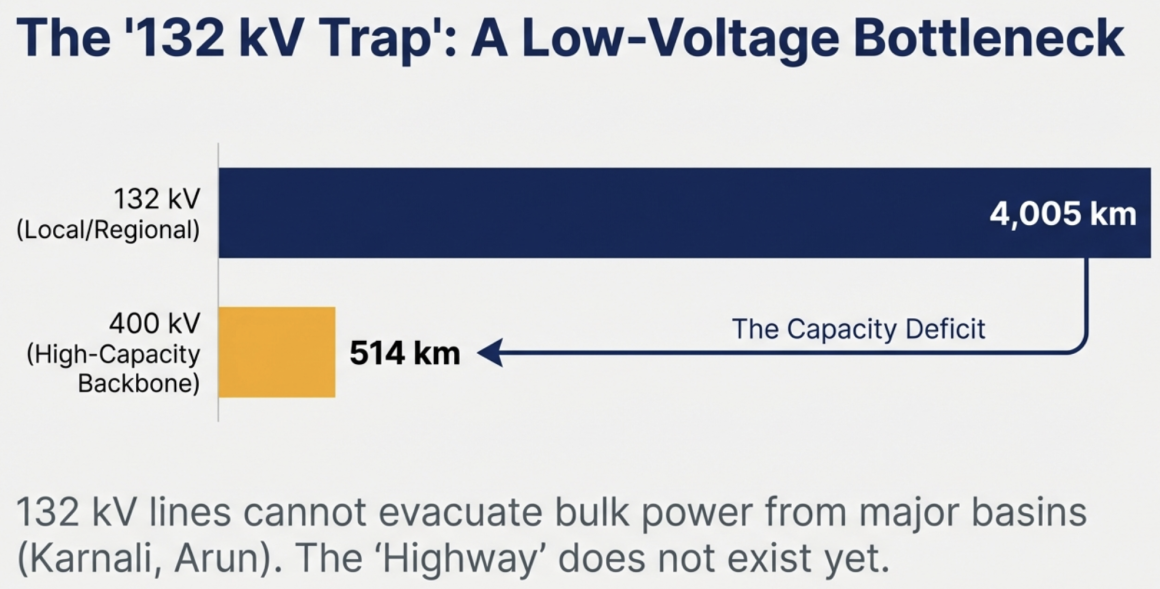

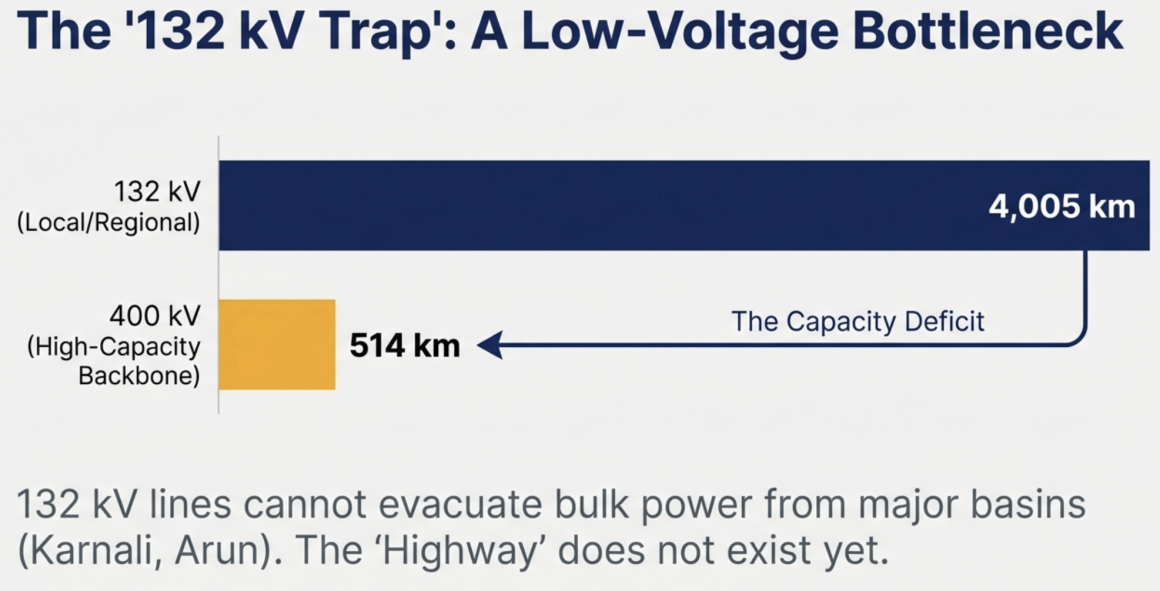

The existing transmission system is heavily skewed toward lower-voltage infrastructure, creating what is often described as the “132 kV trap.” The grid currently includes approximately 4,005.87 circuit kilometers of 132 kV transmission lines, compared to only about 514.46 circuit kilometers of 400 kV lines. While 132 kV lines are sufficient for regional transmission, they are inadequate for evacuating bulk power over long distances or supporting the scale of generation envisioned under Nepal’s long-term development targets, which aim to reach approximately 40 GW of installed capacity by 2040. Achieving these targets requires the development of a high-capacity 400 kV backbone, including the East-West Power Highway and interconnected mesh networks, many of which remain in planning or early construction stages.

This structural imbalance has resulted in tangible bottlenecks and curtailment of electricity generation. A notable example is the Marsyangdi corridor, where inadequate expansion of high-capacity transmission infrastructure has led to situations in which electricity produced in hydropower plants cannot be fully evacuated to load centers. At the same time, industrial corridors such as Birgunj and Biratnagar have experienced electricity shortages due to insufficient transmission capacity to deliver power from surplus regions.

A particularly significant example of delayed infrastructure is the Hetauda-Dhalkebar-Inaruwa 400 kV transmission line, a strategic backbone project that has remained under construction for more than 15 years without completion. This delay has severely limited the ability to transfer electricity between eastern, central, and western regions, exacerbating regional imbalances and reducing overall system efficiency.

The consequences of transmission constraints became especially evident during the wet season of 2025, when electricity generation surplus reached approximately 1,400 MW. However, due to transmission bottlenecks and export approval limitations – only 1,141 MW of export capacity was authorized – significant volumes of electricity were spilled, including at power plants operated by the Nepal Electricity Authority. Similarly, in November 2025, when approximately 25 industries were disconnected from the grid, resulting in a reduction of roughly 300 MW of domestic demand, the system was unable to immediately export the surplus electricity due to infrastructure and operational constraints. This forced hydropower plants to reduce generation or shut down temporarily, illustrating the severe operational inefficiencies caused by inadequate transmission capacity.

The sector has therefore been characterized as facing a structural paradox – possessing abundant hydropower resources but lacking sufficient transmission infrastructure to deliver that electricity to markets. This paradox is also illustrated by cross-border coordination failures. For example, NEA signed a Power Sales Agreement with PTC India for electricity exports via the Dhalkebar-Muzaffarpur transmission line, but the agreement could not be implemented because the transmission infrastructure and associated generation facilities were not commissioned on schedule.

Even where cross-border transmission infrastructure exists, internal transmission limitations prevent effective utilization. The Dhalkebar-Muzaffarpur transmission line, for instance, has a capacity of approximately 800 MW, but insufficient internal high-voltage transmission capacity restricts the ability to distribute imported or exported electricity efficiently within Nepal’s domestic grid.

6.2 Grid Reliability Concerns

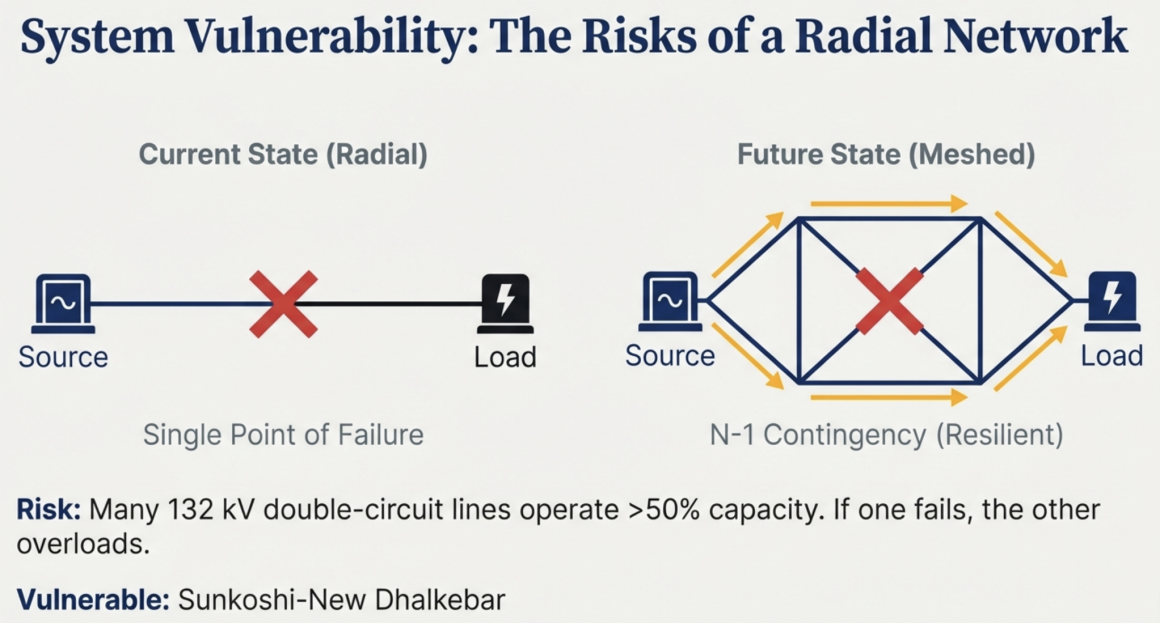

Although Nepal’s Transmission System Development Plan proposes the development of a mesh network that would provide multiple alternative paths for electricity flow in case of transmission failures, much of the existing transmission system remains radial rather than looped. In a radial system, individual transmission lines connect generation clusters directly to the grid without alternative pathways, creating single points of failure. While the planned network is designed to meet the N-1 reliability standard – where the system can continue operating despite the failure of a single circuit – this standard is not uniformly achieved across the existing network. As a result, single failures can disconnect entire regions or generation hubs from the grid. Because the critical high-capacity backbone infrastructure, particularly the East-West Power Highway, is still under construction, the full reliability benefits of a meshed network have not yet been realized.

Historically, transmission infrastructure was developed primarily as radial transmission lines following river corridors to connect hydropower generation sites to load centers or the East-West transmission backbone. In such radial configurations, if a dedicated transmission line fails, there is no alternative route to evacuate power, resulting in complete isolation of the generation cluster.

Cross-border transmission infrastructure also exhibits radial characteristics. Existing 132 kV, 33 kV, and 11 kV cross-border links with India operate in radial mode and are not integrated into synchronized looped networks capable of automatically redistributing power flows. This limits operational flexibility and system resilience.

The dominance of 132 kV infrastructure further contributes to reliability challenges. Many of these lines operate as double-circuit radial lines, but in the event of tower failure affecting both circuits, there is no alternative path for power evacuation. In contrast, a properly meshed 400 kV network would allow electricity to be rerouted through alternative transmission paths, improving system resilience.

Although the N-1 contingency standard requires that the remaining circuit of a double-circuit line should be able to carry the full load if one circuit fails, system analysis indicates that many existing transmission segments do not meet this requirement. Several 132 kV double-circuit lines already operate at load levels exceeding 50% of their capacity. Under N-1 contingency conditions, the remaining circuit would be overloaded beyond safe operational limits, potentially resulting in cascading failures and widespread outages.

Reliability simulations of the planned future network have also identified vulnerability in certain high-voltage segments. Specific transmission lines identified as susceptible to N-1 violations include the Sunkoshi-New Dhalkebar 400 kV line, the Betan-Dododhara 400 kV line, and the Bafikot-Nalgadh 400 kV line. In addition, tower contingency scenarios, where both circuits of a transmission tower fail simultaneously, have revealed further vulnerabilities. For example, failure of the Sunkoshi-Dhalkebar line would overload the Khimti-Dhalkebar 220 kV line, while failure of the Tamor-Inaruwa line would overload the Hangpang-Basantapur 220 kV line.

The incomplete status of the East-West Power Highway represents the most significant limitation in achieving a fully reliable meshed transmission system. The Hetauda-Dhalkebar-Inaruwa 400 kV transmission line, spanning approximately 288 kilometers, remains unfinished despite more than 15 years of construction. Similarly, the New Dhalkebar-Hetauda segment remains under construction, while the New Butwal-Phulbari section remains under study. In addition, the proposed mid-hill 400 kV transmission corridor, intended to form a second backbone and create looped redundancy with the Terai corridor, remains largely in the planning phase.

Until these major 400 kV backbone corridors are completed and integrated, Nepal’s transmission system will continue to function largely as a collection of radial transmission lines, leaving the system vulnerable to outages, congestion, and evacuation failures.

6.3 Voltage Level Optimization Challenges

Nepal’s transition from a transmission system dominated by 132 kV infrastructure to a modern high-capacity grid based on 220 kV, 400 kV, and eventually 765 kV voltage levels presents significant technical, operational, and financial challenges. Although the Nepal Electricity Grid Code (2080) has established regulatory provisions allowing transmission infrastructure up to 765 kV, the practical implementation of such high-voltage systems requires substantial investment in transmission lines, substations, advanced equipment, technical expertise, and sophisticated operational procedures.

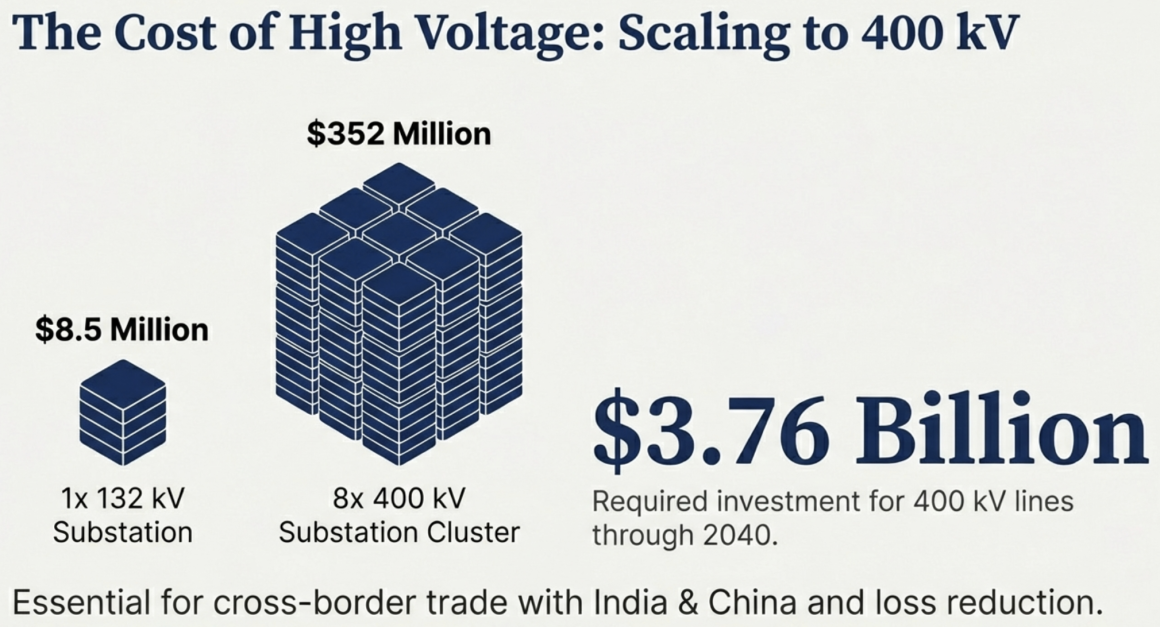

Currently, Nepal’s transmission system remains heavily reliant on 132 kV infrastructure. However, to achieve the national generation target of approximately 40,000 MW by 2040, the Transmission System Development Plan proposes a major shift toward a 400 kV backbone network. The plan includes approximately 3,192 kilometers of 400 kV transmission lines compared to approximately 2,515 kilometers of 132 kV lines, effectively establishing 400 kV infrastructure as the new national transmission backbone.

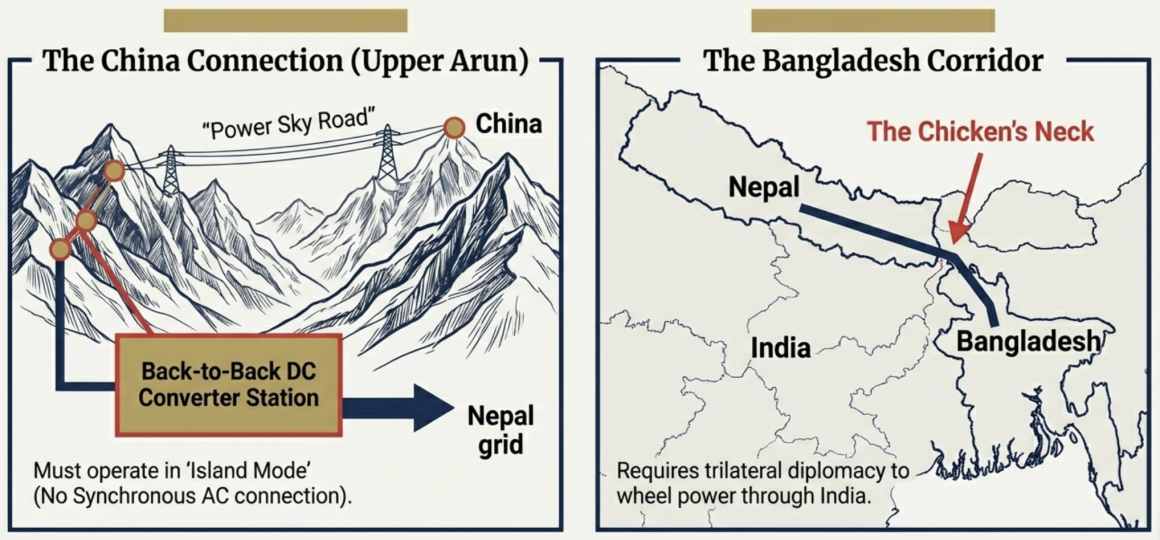

The Nepal Electricity Grid Code (2080) has also enabled the development of transmission lines up to 765 kV capacity, particularly to facilitate long-distance cross-border electricity trade with China. Due to the vast distances between Nepal’s generation centers and load centers in Tibet and the challenging Himalayan terrain, higher voltage transmission is essential to minimize technical losses and ensure economic feasibility. High-voltage transmission allows large quantities of electricity to be transmitted efficiently over long distances with lower losses compared to lower voltage alternatives.

However, the financial requirements for high-voltage infrastructure are enormous. Substation construction costs illustrate the scale of investment required. For example, the development of eight 400 kV substations in one zone is estimated to cost approximately USD 352.76 million, whereas a single 132 kV substation costs approximately USD 8.55 million. Similarly, the development of eleven 400 kV substations in another zone is estimated to cost approximately USD 449.41 million, compared to only USD 20.88 million for two 132 kV substations. Overall, the total estimated investment required for Nepal’s planned transmission network through 2040 is approximately USD 6.03 billion, with approximately USD 3.76 billion allocated specifically for 400 kV transmission lines.

Despite these high costs, high-voltage infrastructure offers substantial technical advantages. Higher voltage transmission lines can carry significantly larger quantities of electricity with lower losses and reduced land requirements compared to multiple lower-voltage lines. For example, a single 750 kV transmission line can carry power equivalent to approximately four 400 kV circuits, reducing both land acquisition requirements and transmission losses.

The transition to high-voltage transmission is also critical for evacuating bulk power from major hydropower basins such as Karnali, Bheri, and Arun, where generation capacity is expected to reach several thousand megawatts. The planned 400 kV East-West Power Highway and mid-hill transmission corridors are designed to serve as high-capacity evacuation routes connecting these generation hubs to domestic and international markets.

Cross-border transmission infrastructure is also being developed at 400 kV capacity, including major projects such as the New Butwal-Gorakhpur line, the Inaruwa-Purnea line, the Dododhara-Bareilly line, and the proposed Kimathanka-Latse line connecting Nepal with China.

However, the transition to high-voltage transmission also introduces operational complexity. For example, the Dhalkebar-Muzaffarpur cross-border transmission line, originally charged at 132 kV and later upgraded to 220 kV and 400 kV, requires complex synchronization and coordination to operate at full capacity. Effective utilization of such infrastructure requires advanced system management, technical expertise, and institutional coordination, which have historically posed challenges for Nepal’s electricity sector.

Overall, while high-voltage transmission infrastructure is essential for Nepal’s long-term energy strategy, its implementation requires overcoming substantial technical, financial, and operational barriers.

7. Risk and Uncertainty for Stakeholders

7.1 Policy and Legal Uncertainty

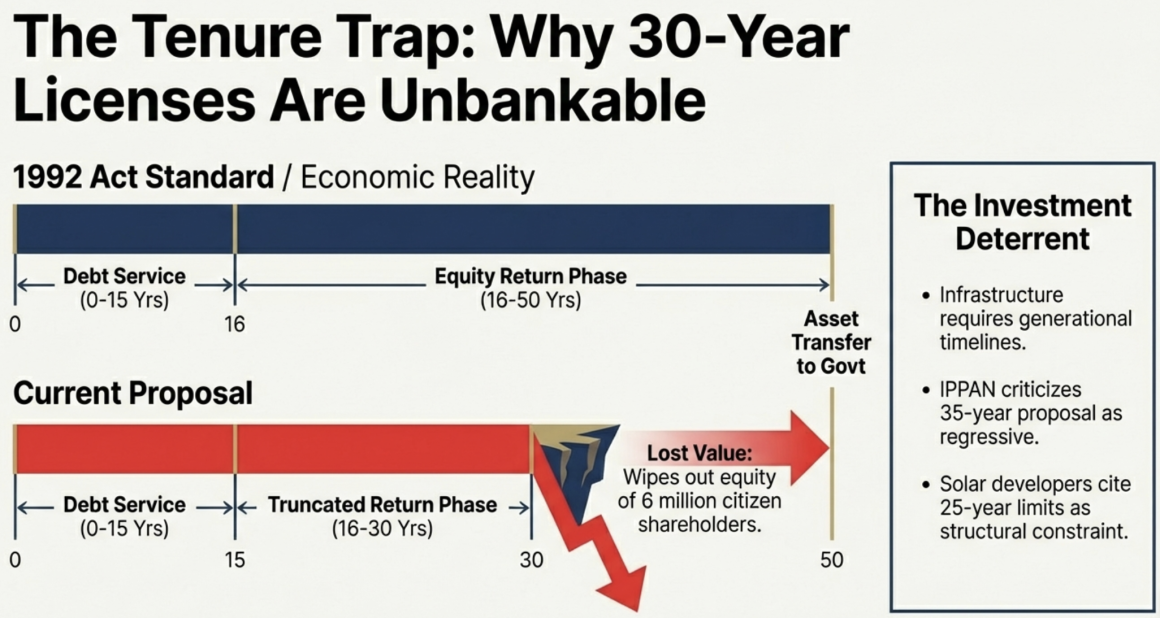

Nepal’s transmission sector continues to face substantial policy and legal uncertainty, which significantly increases business risk for potential investors. Currently, there is no comprehensive legal framework enabling the private sector to engage in electricity trading or cross-border power sales, a crucial requirement for ensuring the financial viability of private transmission lines connected to export markets. The ongoing delays in legislative development and regulatory finalization make it extremely difficult for investors to forecast the regulatory environment over the 25–30 year concession periods typical of transmission projects. Consequently, even developers willing to participate are often deterred by the unpredictability of the legal and regulatory landscape.

There is strong advocacy from IPPs for the adoption of a 50-year concession model – or a Renewable/Perpetual Operation model – as a superior alternative to the current 25–30 year framework. The shorter concession period is widely seen as insufficient to support financial viability, protect public shareholders, and align with the long gestation periods inherent in infrastructure projects.

Limitations of the Current (25–35 Year) Model

The private sector and industry experts consistently argue that the current or proposed short-duration concessions fail to reflect the sector’s economic realities.

- Investment Deterrent: The Independent Power Producers’ Association of Nepal (IPPAN) explicitly criticizes the proposal in the new Electricity Bill to reduce permit durations to 35 years, describing it as regressive and a disincentive for private investment.

- Solar Constraints: Solar developers similarly note that the short 25-year PPA and generation license periods create a structural limitation, hindering sectoral growth.

- Public Shareholder Risk: Under the existing BOOT (Build, Own, Operate, Transfer) model, assets revert to government ownership at the end of the license period. This potentially wipes out the value of investments by over six million citizens who have purchased shares in hydropower projects, a risk that was likely not fully appreciated by the public at the time of purchase.

The Case for the 50-Year Model

The private sector considers a 50-year concession period as essential for long-term stability.

- Strategic Demand: Stakeholders have formally requested that reservoir projects retain a 55-year license and other hydropower projects maintain a 50-year license to create an attractive investment climate.

- Restoring Original Standards: IPPAN emphasizes that the Electricity Act of 1992 (2049 BS) originally provided for 50-year permits, and the new bill should maintain this standard.

- Financial Viability: Given the capital-intensive nature of reservoir projects and high-voltage transmission lines, long payback periods, bureaucratic delays, and hurdles such as forest and land acquisition, a 50-year license period is necessary to recover investment costs and generate reasonable returns.

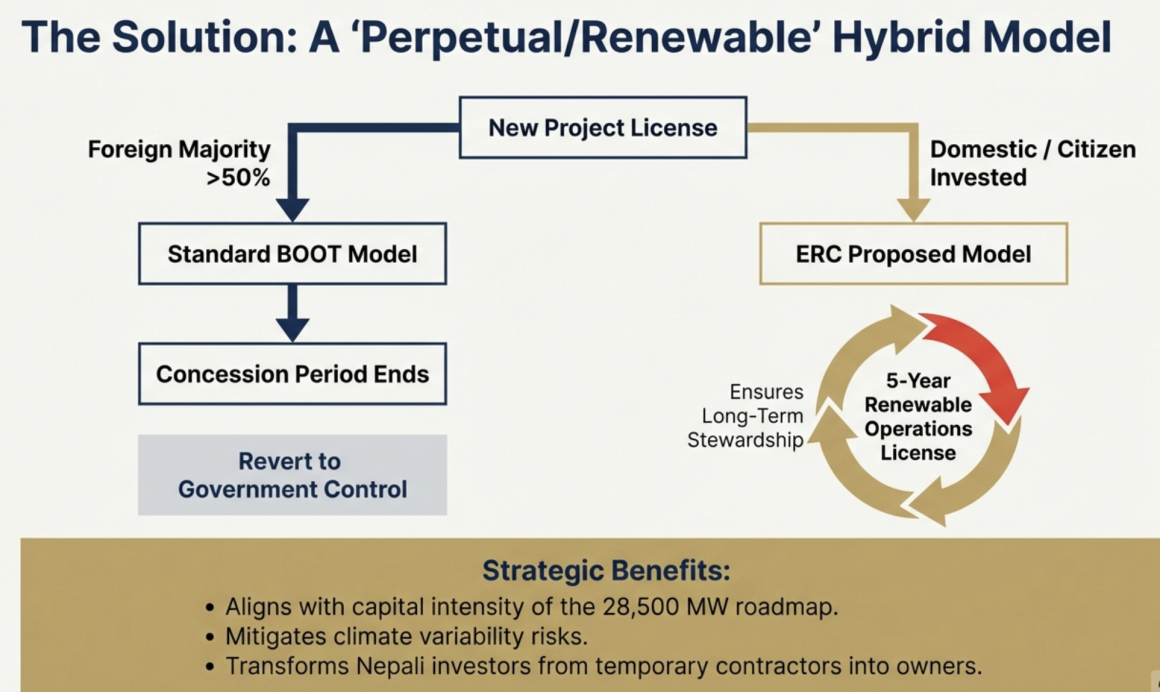

The Emerging “Perpetual / Renewable” Hybrid Model

A more progressive approach involves enabling domestic investors to continue operating projects beyond the initial license period, effectively bridging the gap between conventional concessions and perpetual ownership.

- ERC’s Proposed Solution: The Chairperson of the Electricity Regulatory Commission has proposed a framework in which developers can renew operational agreements every five years after the initial permit period.

- Protection of Domestic Investment: While foreign-majority projects (>50% foreign ownership) may revert to government control, domestic projects could continue operations, ensuring that Nepali investors’ contributions are safeguarded and that private entities remain long-term partners rather than temporary contractors.

In conclusion, for Nepal’s context, retaining the 50-year model – or transitioning to a renewable license framework for domestic entities – offers clear advantages over the current 25–30 year arrangement. This approach is necessary to secure public investments, align with the “28,500 MW by 2035” roadmap requiring substantial private capital, and mitigate risks associated with climate variability and regulatory delays.

7.2 Risk Transfer to Developers