Why does PCG seem essential in Nepal?

Nepal currently confronts a distinct infrastructure financing paradox: while the banking sector possesses substantial liquidity, capital constraints prevent the deployment of these funds into long-term infrastructure projects, exacerbating a significant financing gap. Commercial banks avoid these projects not necessarily due to a lack of funds, but because infrastructure loans carry high risk weights (100%+) that lock up regulatory capital for 15–25 years, hitting single obligor and sectoral limits. Partial Credit Guarantees (PCGs) are identified as the critical missing policy instrument because they reduce Risk-Weighted Assets (RWA), effectively freeing up regulatory capital and allowing banks to lend without increasing balance sheet risk.

This article discusses that the Nepal Infrastructure Bank (NIFRA) is the optimal institution to deploy these guarantees, including comparison with the Deposit and Credit Guarantee Fund (DCGF). While DCGF is legally permitted to issue infrastructure guarantees under the Fourth Amendment of the Credit Guarantee Regulation, it operates primarily as a “financial insurer” with over NPR 14 trillion in off-balance sheet liabilities, focusing on protecting the broader banking system rather than direct project financing. Conversely, NIFRA maintains a robust Capital Adequacy Ratio (CAR) of 77.56%, indicating substantial room for credit expansion and the capacity to absorb specific project risks.

Currently, NIFRA is restricted from providing such guarantees to commercial banks by NRB Directive No. 2, Clause 15, which prohibits inter-bank financial guarantees to prevent “paper capital” creation. However, international benchmarking confirms that Infrastructure Development Banks (IDBs) globally, such as KfW (Germany) and IIFCL (India), routinely provide credit enhancement to commercial lenders. Therefore, a targeted amendment to NRB Directive No. 2 is recommended to create a specific carve-out for NIFRA. This reform would allow NIFRA to function as a true policy bank, utilizing its capital to de-risk projects and crowd-in private capital, achieving a multiplier effect on infrastructure lending while adhering to Basel III prudential standards regarding risk transfer.

1. The Infrastructure Financing Crisis: A Comprehensive Regulatory Diagnostic

1.1 The Capital Adequacy Constraint: By the Numbers

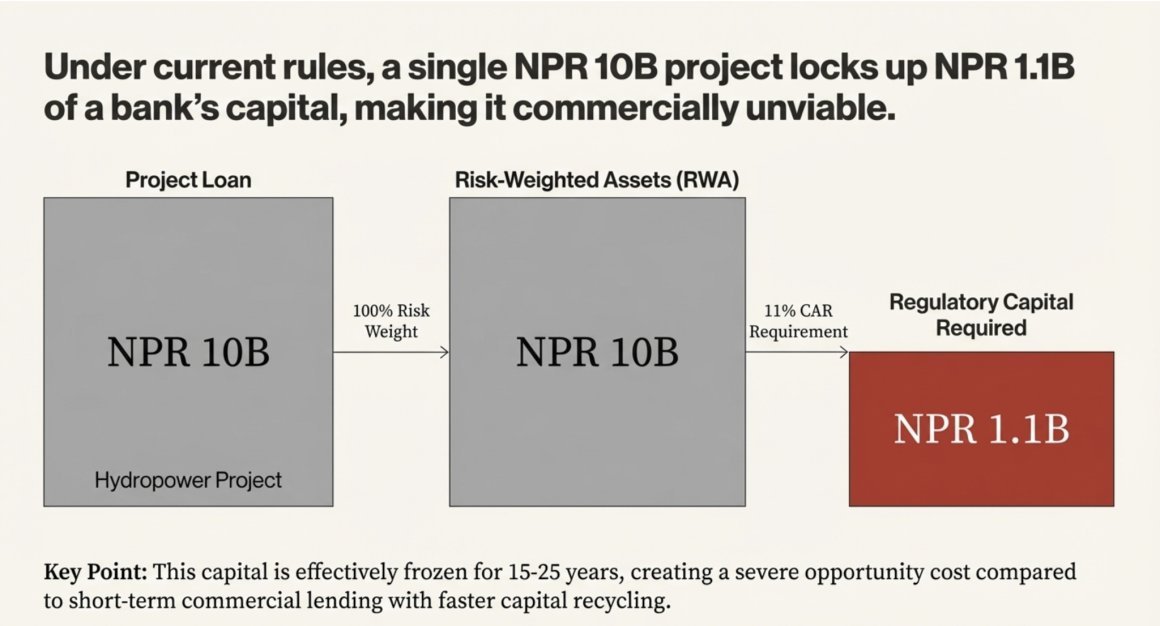

Current Regulatory Reality: Under the Nepal Rastra Bank Capital Adequacy Framework 2015, commercial banks are required to maintain a Minimum Total Capital Ratio of 8.5% plus a Capital Conservation Buffer (CCB) of 2.5%, totaling a mandatory 11% Capital Adequacy Ratio (CAR). For Infrastructure Development Banks like NIFRA, the framework similarly mandates a 11% minimum capital fund. Under the Standardized Approach, infrastructure loans to corporate entities generally carry a 100% risk weight, which creates severe capital allocation challenges by locking up significant equity for the duration of the loan.

Mathematical Impact Analysis:

- Hypothetical NPR 10 Billion Hydropower Project:

- Without Credit Risk Mitigation (CRM): A 100% Risk Weight leads to NPR 10 Billion in Risk-Weighted Assets (RWA).

- Capital Requirement: At an 11% CAR, this single project requires the bank to maintain NPR 1.1 Billion in regulatory capital.

- Bank Opportunity Cost: Capital is effectively locked for 15-25 years, whereas short-term commercial lending typically yields a higher Return on Equity (ROE) and allows for faster capital recycling. This is compounded by a tenor mismatch, as banks often fund with short-term deposits while infrastructure projects require long-term financing.

- Banking System Data: While the total banking capital is significant, individual lending is strictly constrained by Single Obligor Limits (SOL) to prevent concentration risk.

Regulatory Barrier: According to Unified Directive No. 3, the exposure to specific priority sectors is capped. The legal provision states that “Licensed institutions can provide credit and facilities to hydropower, renewable energy, electricity transmission line, and cable car construction projects up to a maximum of 50% of their Primary Capital“.

Critical Conditions:

- PPA Requirement: For hydropower and renewable energy projects, a Power Purchase Agreement (PPA) with the relevant authority is mandatory if the credit exposure exceeds 25% of the bank’s Primary Capital.

- Mixed Portfolio Restrictions: If a client involved in these sectors also utilizes loans for non-hydro or non-energy projects, the limit for those “other” facilities is capped at 25%, provided the total exposure across all categories does not exceed the overall 50% ceiling.

- Penalty Provision: Any credit provided to non-energy/non-hydro projects that exceeds these specified limits requires a 100% loan loss provision on the excess (over-limit) amount.

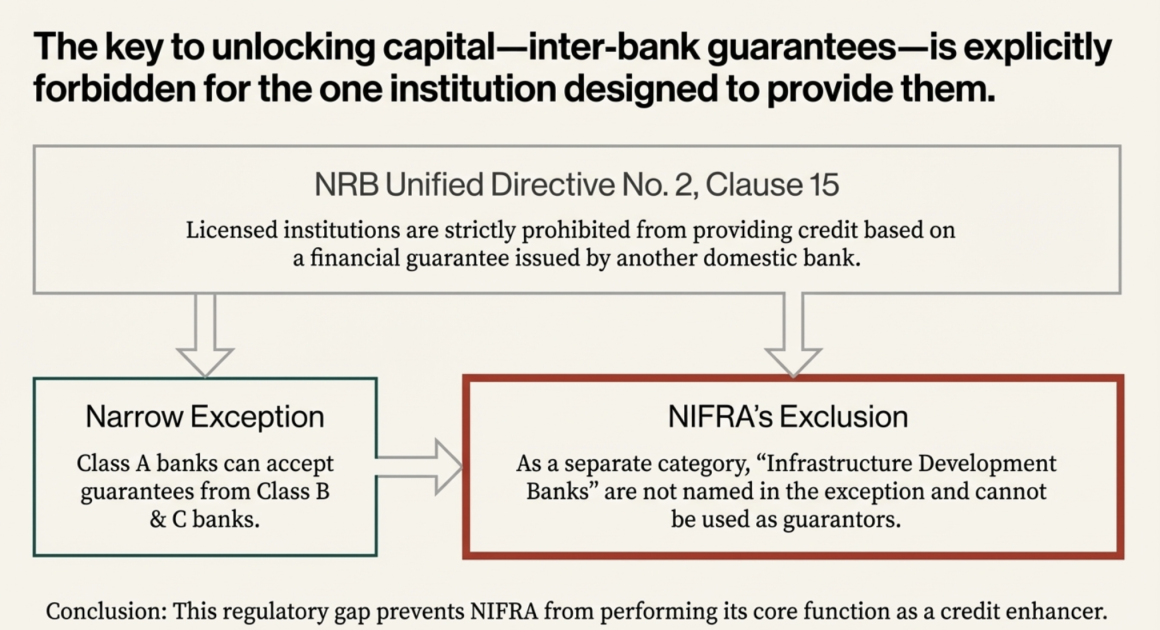

1.2 The Inter-Bank Guarantee Prohibition: The NIFRA Exclusion

Legal Framework: According to NRB Unified Directive No. 2, Clause 15 (for Class A, B, and C banks), licensed institutions are strictly prohibited from providing credit, facilities, or accepting deposits based on a financial guarantee issued by another domestic bank or financial institution established and operating within Nepal.

The Critical Regulatory Gap:

- Exception Clause: The regulations provide a narrow “downward” exception where Commercial Banks (Class A) are permitted to issue guarantees or Letters of Credit based on a guarantee provided specifically by Development Banks (Class B) or Finance Companies (Class C).

- NIFRA Exclusion: Because Infrastructure Development Banks are a separate category and are not explicitly named in this exception, Class A banks cannot accept NIFRA guarantees to back their lending.

- NIFRA’s Own Restriction: This is mirrored in NIFRA’s own Unified Directive No. 2, Clause 13, which prohibits it from providing credit or facilities based on a financial guarantee from any other domestic BFI.

Capital Deduction Framework (Unified Directive No. 8): Under the provisions for Investment and Subsidiary Companies (Unified Directive No. 8), certain investments must be removed from the capital base rather than risk-weighted:

|

Investment Type |

Limit |

Deduction Requirement |

|

Total Aggregate Investment (in shares, debentures, or collective funds) |

30% of Primary Capital |

Excess amount is deducted from primary capital. |

|

Investment in Institutions with Financial Interest (Associates) |

20% of Primary Capital |

Entire total investment amount is deducted from primary capital. |

1.3 Risk Weight Implications for NIFRA

0% Effective Risk Weight:

In general, any claims or assets that are deducted from Common Equity Tier 1 (CET1) capital are effectively removed from the Risk-Weighted Exposure (RWE) calculation, meaning they carry 0% risk weight.

Exception for Infrastructure Development Banks (IDBs):

NIFRA, as an IDB, enjoys a regulatory modification allowing certain high-risk investments to remain on the balance sheet without being deducted from CET1. Specifically:

|

Feature |

General Rule for Banks |

NIFRA / IDB Treatment |

|

Treatment of PE/VC Investments |

Typically deducted from CET1, effectively 0% RWE |

Not mandatory to deduct from CET1 (Capital Adequacy Framework 2018, Section 2.3) |

|

Risk Weight Assignment |

N/A (deducted from capital) |

150% risk weight, classified as “higher-risk category” |

|

Regulatory Logic |

Deducted assets are removed from RWE, reducing effective risk exposure |

Explicit 150% risk weight keeps PE/VC investments on the balance sheet, ensuring they contribute to risk while preserving capital base |

|

Departure from General Rules |

Directive No. 8: investments in institutions with “financial interest” must be fully deducted from primary capital |

NIFRA is allowed to retain these investments in its portfolio, provided it holds sufficient capital against the higher 150% risk weight |

Implication:

This modification enables NIFRA to invest in Private Equity (PE) and Venture Capital (VC) without directly reducing CET1, while still requiring adequate capital provisioning against these higher-risk exposures. It ensures that NIFRA can maintain a diversified infrastructure finance portfolio without eroding its primary capital, unlike typical commercial banks.

1.4 Credit Risk Mitigation Framework Analysis

CRM Eligibility (Capital Adequacy Framework 2015, Section 3.4):

- Government Guarantees: All claims on the Government of Nepal and the Nepal Rastra Bank are assigned a 0% risk weight. Under the “Substitution Approach” of the Credit Risk Mitigation (CRM) framework, the portion of an exposure covered by a government guarantee receives this 0% weight instead of the borrower’s risk weight.

- Domestic Bank Guarantees: Claims on domestically incorporated banks that have complied with Capital Adequacy Requirements are risk-weighted at 20%. When such banks are allowed to act as a guarantor, the lending institution can substitute the borrower’s risk weight with this 20% floor, effectively providing a capital discount.

Quality Requirements: To qualify for regulatory capital relief, a guarantee must represent a direct claim on the protection provider and be explicitly referenced to specific exposures. The agreement must be irrevocable, containing no clauses that allow the guarantor to unilaterally cancel the cover or increase the cost due to deteriorating credit quality. It must also be unconditional, meaning no factors outside the bank’s control can prevent the guarantor from paying out in a timely manner. Crucially, the bank must have the right to pursue the guarantor immediately upon default without first being required to take legal action against the original counterparty.

The Regulatory Gap: A significant “deadlock” exists between the capital frameworks and the operational directives. While the Capital Adequacy Framework defines the methodology and benefits for using domestic bank guarantees as a risk mitigant, NRB Unified Directive No. 2 (Clause 15 for Class ABC and Clause 13 for NIFRA) explicitly prohibits banks from providing credit or facilities based on a financial guarantee issued by another domestic bank or financial institution. This means that while the “math” for the capital discount is provided in the rules, the “action” of lending against such protection is generally forbidden by the regulator to prevent systemic interconnectedness.

2. The Technical Case for Partial Credit Guarantees: Basel-III Compliance

2.1 Basel-III Compliant PCG Mathematics

Nepal broadly follows the Basel III standardized approach for calculating capital requirements. This framework allows banks to use Credit Risk Mitigation (CRM) techniques, such as guarantees, to substitute the risk weight of a borrower with the (usually lower) risk weight of an eligible guarantor.

Base Scenario Assumptions:

- Project Loan: NPR 10 billion.

- Borrower: Infrastructure SPV (Corporate).

- Tenor: Long-term (15+ years).

- Original Risk Weight: 100% (Standard for unrated domestic corporate claims).

- Bank Capital Adequacy Ratio (CAR) Requirement: 11% (Minimum 8.5% total capital plus a 2.5% Capital Conservation Buffer).

Scenario 1: Status Quo (No PCG) In this scenario, the bank must hold capital against the full exposure at the borrower’s risk weight.

- Risk-Weighted Assets (RWA): Exposure × Risk Weight = 10,000 × 100% = 10,000.

- Capital Required: RWA × CAR = 10,000 × 11% = 1,100.

Outcome: This results in high capital lock-up, often causing banks to avoid long-tenor infrastructure loans.

Scenario 2: 30% PCG by NIFRA (Basel-III Compliant) Under Basel III, a Partial Credit Guarantee (PCG) requires exposure splitting, where risk weights are applied separately to the guaranteed and unguaranteed portions. As a compliant domestic bank, claims on NIFRA attract a 20% risk weight under the substitution approach.

|

Portion |

Amount (NPR bn) |

Risk Bearer |

Risk Weight |

RWA |

|

Guaranteed (30%) |

3,000 |

NIFRA |

20% |

600 |

|

Unguaranteed (70%) |

7,000 |

Project |

100% |

7,000 |

- Total RWA: 7,000 + 600 = 7,600.

- Capital Required: 7,600 × 11% = 836.

- Capital Released: 1,100 – 836 = 264 (24% reduction).

Benefit: This structure is prudentially sound because it involves genuine risk transfer outside the project and requires the bank to still hold the majority of the risk, preventing “paper capital” inflation.

Scenario 3: First-Loss Guarantee (More Conservative) In a first-loss structure, the guarantor covers the initial percentage of any losses incurred. Basel treatment dictates that only the first-loss portion receives the guarantor’s risk weight, while the remaining exposure remains at the original weight.

- First-loss (20%): 2,000 × 20% = 400 RWA.

- Remaining (80%): 8,000 × 100% = 8,000 RWA.

- Total RWA: 400 + 8,000 = 8,400.

- Capital Required: 8,400 × 11% = 924.

Outcome: While this provides less capital relief than a pari-passu PCG, it is considered even more conservative from a regulatory standpoint.

2.2 Addressing "Paper Capital" Concerns

The term “paper capital” refers to regulatory capital relief that exists only in accounting entries without a genuine, independent transfer of risk outside the domestic banking system. Basel III safeguards are specifically designed to prevent banks from artificially inflating their capital positions through mutual or circular promises that leave the financial system fragile during a crisis.

Basel III Safeguards:

- Exposure Splitting: Basel III mandates exposure splitting rather than total risk weight substitution. In a Partial Credit Guarantee (PCG) structure, the risk-weight substitution applies strictly to the guaranteed portion, while the remainder of the claim is assigned the risk weight of the underlying counterparty. This ensures that the lending bank continues to hold the majority of the risk, maintaining its “skin in the game”.

- Eligible Guarantors: Credit Risk Mitigation (CRM) is only recognized when provided by entities with real loss-absorption capacity, such as sovereigns, central banks, or highly-rated financial institutions with policy manadate. For local infrastructure banks like NIFRA, they must be prudentially regulated and maintain independent capital adequacy to qualify as eligible protection providers.

- No Double Counting: The framework explicitly prohibits double counting of capital; a guarantee may be used to reduce the Risk-Weighted Assets (RWA) in the denominator of the Capital Adequacy Ratio (CAR), but it can never be treated as regulatory capital to increase the numerator.

- Legal Enforceability: To qualify for capital relief, a guarantee must meet strict criteria: it must be direct, unconditional, and irrevocable. It must be enforceable in all relevant jurisdictions and allow the bank to pursue the guarantor for payment immediately upon default without first exhausting legal remedies against the primary borrower.

NIFRA’s Independent Strength:

NIFRA possesses significant independent capacity to absorb losses, ensuring that its guarantees represent a substantive transfer of risk rather than a circular arrangement:

- Capital Adequacy Ratio (CAR): As of projected financials for Mid-July 2025, NIFRA maintains an exceptionally high CAR of 77.56%, which far exceeds the regulatory minimum of 11%.

- Net Worth: NIFRA’s total equity (Net Worth) is projected at NPR 25.76 billion, providing a massive, solid foundation of paid-up capital and reserves to back its contingent liabilities.

3. Comprehensive Institutional Analysis: NIFRA vs DCGF

This section compares Nepal Infrastructure Bank (NIFRA) and the Deposit and Credit Guarantee Fund (DCGF) across capital structure, asset deployment, off-balance-sheet exposure, and operational capability, to assess their relative suitability for infrastructure risk-bearing and guarantee functions.

3.1 Capital Structure and Balance Sheet Strength

|

Component |

NIFRA (Mid-July 2025, Projected) |

DCGF (Mid-July 2024, Actual) |

|

Paid-up Share Capital |

NPR 21.60 bn (83.8%) |

NPR 10.00 bn (35.9%) |

|

Retained Earnings / Profit |

NPR 2.02 bn (7.8%) |

NPR 3.92 bn |

|

Reserves & Other Funds |

NPR 2.14 bn (8.3%) |

NPR 13.91 bn |

|

Total Equity |

NPR 25.77 bn (100%) |

NPR 27.83 bn (100%) |

|

Key Risk Buffer |

CAR 77.56% (substantial unused capacity) |

Large reserve base tied to guarantees |

NIFRA’s equity is capital-heavy and expansion-oriented, supported by an exceptionally high CAR, while DCGF’s balance sheet is reserve-heavy and risk-containment-oriented, reflecting its guarantee and deposit insurance mandate.

3.2 Asset Deployment and Investment Orientation

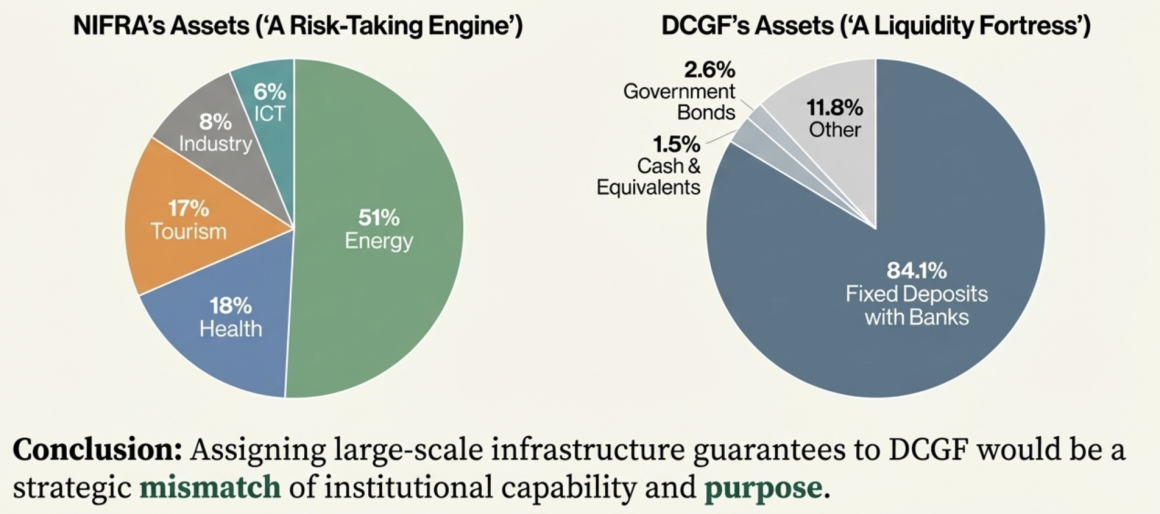

NIFRA’s asset deployment reflects a clear long-term infrastructure financing orientation, with NPR 25.14 billion invested across productive sectors. Energy dominates the portfolio, accounting for NPR 12.82 billion (51 percent), indicating deliberate concentration in capital-intensive, long-tenor projects where sector expertise and risk appraisal capacity are critical. This is complemented by diversified exposure to health (NPR 4.52 billion; 18 percent), tourism (NPR 4.27 billion; 17 percent), industry (NPR 2.01 billion; 8 percent), and ICT (NPR 1.51 billion; 6 percent). The overall composition demonstrates active balance-sheet deployment into real-sector assets, with returns and risks intrinsically linked to project performance over extended maturities.

In contrast, DCGF’s asset allocation of NPR 29.06 billion is structured primarily around liquidity preservation and capital safety rather than developmental risk-taking. A substantial NPR 24.44 billion (84.1 percent) is placed in fixed deposits with banks, supplemented by limited holdings of government development bonds amounting to NPR 0.75 billion (2.6 percent) and cash and cash equivalents of NPR 0.44 billion (1.5 percent). This conservative asset mix is consistent with DCGF’s institutional mandate of meeting contingent guarantee and deposit insurance obligations, but it also underscores the absence of direct exposure to infrastructure or project-level risk. Consequently, while NIFRA’s balance sheet is oriented toward long-term infrastructure development and risk absorption, DCGF’s portfolio is intentionally designed to prioritize liquidity, capital preservation, and immediate solvency over developmental investment.

3.3 Off-Balance-Sheet Exposure and Contingent Risk

|

Institution |

Nature of Exposure |

Amount |

|

NIFRA |

Undisbursed infrastructure commitments |

NPR 1.148 bn |

|

DCGF |

Outstanding guarantee liabilities |

NPR 14.40 trillion |

DCGF already carries system-wide contingent liabilities at a macro scale, while NIFRA’s off-balance-sheet exposure remains limited, project-specific, and manageable.

3.4 Operational Mandate and Technical Capacity

|

Dimension |

NIFRA |

DCGF |

|

Core Mandate |

Infrastructure financing & development |

Deposit insurance & credit guarantees |

|

Sector Expertise |

Strong (51% energy exposure indicates depth) |

SME & agriculture-oriented |

|

Project Appraisal |

In-house technical & financial due diligence |

Limited project finance capability |

|

Transaction Role |

Consortium leadership in complex deals |

Guarantee administration |

|

Scale Alignment |

Suitable for large infrastructure |

Guarantee cap of NPR 3 crore |

|

Institutional Focus |

Long-term project risk |

Liquidity and systemic stability |

NIFRA exhibits a capital-rich balance sheet, high regulatory headroom, infrastructure-focused asset deployment, and strong technical capacity aligned with complex project finance. In contrast, DCGF’s reserve-driven structure, highly liquid investments, extensive contingent liabilities, and SME-focused operational mandate constrain its ability to function as a large-scale infrastructure guarantor. Structurally and operationally, NIFRA is better positioned to absorb, price, and manage infrastructure risk.

4. International Precedent: Global Best Practices

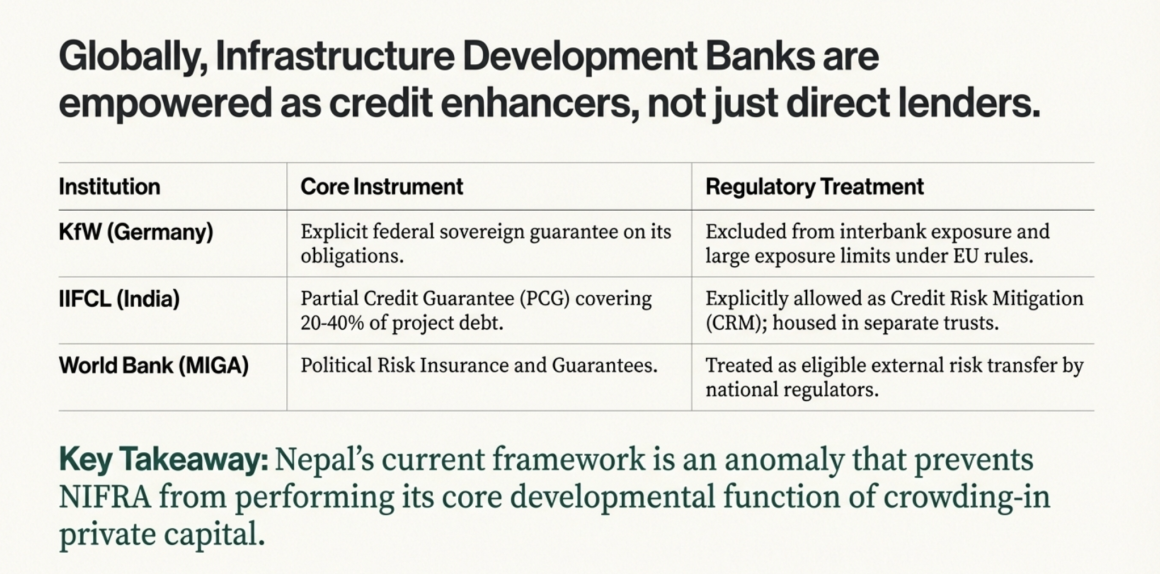

4.1 Infrastructure Development Banks as Credit Enhancers

International experience demonstrates that infrastructure development banks (IDBs) are most effective not as stand-alone lenders, but as credit enhancers that absorb specific risks and thereby crowd in private capital. Rather than replacing commercial banks, successful IDBs improve the risk profile of projects so that banks, bond investors, and institutional financiers can lend at scale.

Institution | Legal / Institutional Structure | Core Instrument | Regulatory Treatment | Developmental Impact |

KfW (Germany) | Public law institution with explicit federal sovereign guarantee | Guarantees, risk-sharing tranches, on-lending | Excluded from interbank exposure and large exposure limits under EU CRR Art. 400 | Enables banks to lend long-term to infrastructure and SMEs without breaching prudential limits |

IIFCL (India) | Government-owned infrastructure financier | Partial Credit Guarantee (PCG) covering 20–40% of project debt | Guarantee risk housed in separate trust/SPV, regulated outside normal bank books | Catalyzed infrastructure bond market and bank lending post-2019 |

World Bank – MIGA | Multilateral guarantee agency | Political Risk Insurance and Guarantees | Treated as eligible external risk transfer | Unlocks cross-border project finance by mitigating political and regulatory risk |

Common Design Features Across Jurisdictions

- Guarantees are treated as risk transfer mechanisms, not capital substitution.

- The guarantor is either sovereign-backed, multilateral, or legally segregated from the banking system.

- Regulatory frameworks explicitly allow lenders to recognize these guarantees for Credit Risk Mitigation (CRM) purposes.

- The objective is systemic: mobilize private capital, not concentrate risk on public balance sheets.

4.2 Nepal’s Regulatory Anomaly: A Structural Mismatch

In contrast to global best practice, Nepal’s regulatory framework creates a structural contradiction that prevents NIFRA from performing its intended role as a credit enhancer.

|

Issue |

Current NRB Treatment |

Resulting Effect |

|

Institutional Classification |

NIFRA regulated as a commercial bank peer under Unified Directives |

Policy bank functions are constrained by prudential rules designed for deposit-taking banks |

|

Guarantee Recognition |

Directive No. 2, Clause 15 generally prohibits BFIs from lending against guarantees issued by another domestic BFI |

NIFRA guarantees cannot be used as CRM |

|

Selective Exception |

Class A banks are permitted to issue guarantees or Letters of Credit (LCs) based on a guarantee provided specifically by Class B Class C banks. |

NIFRA is uniquely excluded despite its development mandate |

|

Regulatory Interpretation |

Guarantees viewed as capital substitution rather than risk transfer |

De-risking function is neutralized |

NIFRA was established precisely to absorb, structure, and manage infrastructure risk that commercial banks are unable or unwilling to take alone. However, by denying NIFRA in engaging in providing guarantees to infrastructure lendings within the country, the regulatory framework:

- Prevents commercial banks from reducing risk-weighted assets even when real credit risk could be manageable.

- Discourages co-financing and syndication for long-tenor infrastructure projects.

- Forces NIFRA into direct lending rather than its more efficient role as a risk absorber and catalyst.

- Deviates sharply from international norms where IDBs are explicitly empowered to de-risk projects.

Globally, infrastructure banks succeed when: Guarantees are recognized as genuine risk transfer, and Regulations are aligned with their developmental mandate, not their balance-sheet form.

Nepal’s current framework does the opposite—it recognizes NIFRA as a bank but denies it the tools of a development institution, resulting in underutilized capital and constrained infrastructure financing.

5. Addressing Regulatory Concerns: The Prudential Case

5.1 Preventing Systemic Risk

The current infrastructure financing model in Nepal is characterized by risk concentration, where large-scale project risks are held by a limited number of direct lenders. This creates a fragile “mountain climber” dynamic: if one bank or project slips, the lack of independent credit enhancement could pull the entire group down.

Partial Credit Guarantees (PCGs) transform this landscape by:

- Risk Distribution: Instead of a single bank holding 100% of a project’s risk, PCGs allow for risk sharing across multiple institutions, effectively pooling risk at a policy-level institution like NIFRA.

- Specialized Loss Absorption: NIFRA, functioning as a specialized “credit enhancer,” is designed to absorb first-loss positions, correcting market failures that commercial banks avoid, such as construction and regulatory risks.

- Better Risk Pricing: As a policy bank, NIFRA provides specialized technical appraisal and monitoring, which allows for more accurate risk pricing compared to standard commercial bank practices.

5.2 Capital Treatment Framework

To ensure financial stability, the framework distinguishes between the risk weight NIFRA carries as an issuer and the relief granted to the lending bank.

For NIFRA as Guarantor (Issuer Risk): Under the Capital Adequacy Framework 2018, NIFRA must hold capital against its contingent liabilities at the following rates:

- Direct Credit Substitutes (Financial Guarantees): 100% risk weight.

- Performance-Related Contingencies (Bid/Performance Bonds): 50% risk weight.

- Unpaid Guarantee Claims: 200% penalty risk weight for claims demanded but not yet paid within 7 days.

For Banks Using NIFRA PCGs (Substitution Approach): Lenders can use the Credit Risk Mitigation (CRM) “substitution approach” to calculate capital requirements.

- Guaranteed Portion: Receives a 20% risk weight, as NIFRA is a compliant domestic bank.

- Unguaranteed Portion: Retains the original risk weight of the borrower (typically 100% for unrated corporate claims).

- Net Effect: This results in genuine capital efficiency because the bank retains “skin in the game” for the majority of the loan, preventing the inflation of “paper capital” through circular or reciprocal crossholdings.

5.3 Legal and Operational Safeguards

The proposed PCG structure follows Basel III safeguards to ensure the guarantee is a robust risk transfer rather than a cosmetic accounting entry.

- Coverage Cap: Guarantees are capped at a maximum of 30–40% of project debt to ensure the lending bank maintains a primary interest in project success.

- Tenor Limit: PCGs primarily target the “Construction Phase Deadlock,” covering the initial 3–5 years of high-risk activity and automatically sunsetting once the project reaches operational stability.

- Legal Qualities: To qualify as a CRM, the NIFRA guarantee must be direct, unconditional, and irrevocable, allowing the bank to pursue NIFRA immediately upon default without exhausting legal remedies against the borrower.

- Independent Monitoring: Disbursement is strictly linked to technical milestones and verified through third-party audits to force project discipline.

6. The DCGF Alternative: Comprehensive Limitation Analysis

While the Deposit and Credit Guarantee Fund (DCGF) has an expanding mandate, it serves a fundamentally different purpose than a specialized infrastructure bank, creating significant limitations as a primary alternative for infrastructure credit enhancement.

6.1 Legal Authority Examination

The DCGF operates under a specific legal framework that allows for sectoral expansion, yet remains operationally tailored for smaller-scale interventions.

- DCGF Act, 2073 Provisions:

- Section 7(5): Grants the Fund power to perform “other functions” necessary to achieve its objectives of protecting credit and enhancing banking system credibility.

- Section 12(1)(k): Empowers the Board of Directors to submit proposals to the Government of Nepal to expand the scope of deposit and credit guarantees.

- Credit Guarantee Regulation, 2075: Under the Fourth Amendment (2080), Rule 35(4), the Fund is explicitly permitted to implement new guarantee programs for infrastructure development, climate change, and information technology.

- Operational Constraints:

- Scale Limits: Current specialized programs, such as the Provincial SME scheme, cap guarantees at NPR 3 crore (30 million) per borrower.

- Approval Requirements: Any loan exceeding NPR 1 crore (10 million) requires specific prior approval from the DCGF, creating potential procedural bottlenecks for large projects.

- Sector Focus: DCGF has traditionally focused on agriculture, SMEs, and the deprived sector, meaning it lacks the deep technical infrastructure expertise inherent to NIFRA’s mandate.

6.2 Financial Capacity Analysis

A comparison of the two entities reveals a paradox of scale and intent.

- Equity Comparison: DCGF maintains a larger total equity/net worth, projected at NPR 27.83 billion (Mid 2024), compared to NIFRA’s projected NPR 25.76 billion (Mid 2025).

- Liability Structure: The DCGF’s structure is designed to function as a financial insurer. It carries staggering off-balance sheet liabilities totaling NPR 14.40 trillion, the vast majority of which (NPR 12.32 trillion) covers deposit insurance for over 41 million accounts.

- Investment Strategy: To ensure it can meet these low-probability but high-impact deposit claims, DCGF keeps NPR 24.44 billion in fixed deposits at Class A banks for safety and high liquidity. In contrast, NIFRA is an “engine” designed for active risk-taking, placing its assets directly into physical infrastructure projects like energy (51%) and health (18%).

7. Recommended Regulatory Amendments: Specific Formulations

7.1 Targeted Amendment to Directive No. 2

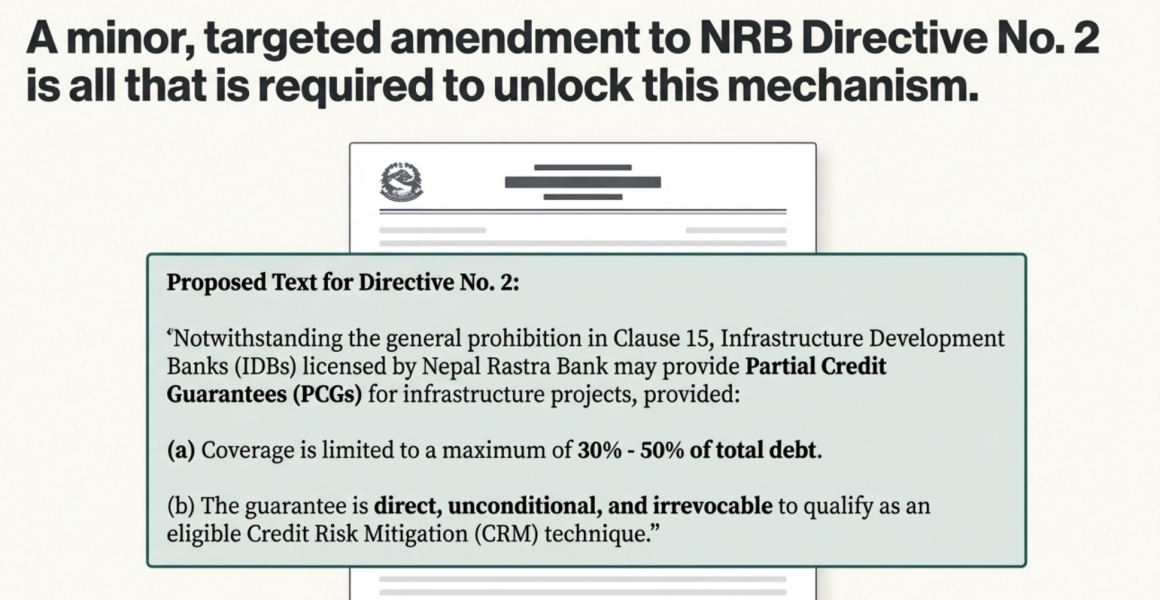

The current regulatory framework under Directive No. 2, Clause 15 of the Unified Directives prohibits domestic Banks and Financial Institutions (BFIs) from providing credit or facilities based on a financial guarantee issued by another domestic BFI. While a narrow exception exists for Class A banks to issue guarantees or Letters of Credit (LCs) based on a guarantee provided specifically by Class B Class C banks, NIFRA (categorized as an Infrastructure Development Bank) is not provided any exception.

To enable NIFRA’s core mandate as a credit enhancer, the following amendment to Directive No. 2 is proposed:

Proposed Clause 15.1: “Notwithstanding the general prohibition in Clause 15, Infrastructure Development Banks (IDBs) licensed by Nepal Rastra Bank may provide Partial Credit Guarantees (PCGs) for infrastructure projects meeting the following indicative/suggestive criteria:

- Project Size: The project cost must exceed NPR 10 to 20 billion .

- PCG Coverage: Coverage is limited to a maximum of 30% – 50% of total debt to ensure the primary lender retains significant risk and prevents systemic fragility.

- Quality of Guarantee: The guarantee must be direct, unconditional, and irrevocable, representing a direct claim on the IDB to qualify as an eligible Credit Risk Mitigation (CRM) technique.

- Sovereign Counter-Guarantee: For projects of national importance, a sovereign counter-guarantee framework should be utilized, effectively treating the exposure as a claim on the Government of Nepal.

Transparency and Reporting: IDBs must provide regular reporting on guarantee portfolio performance to NRB, following standard monthly and quarterly capital adequacy reporting protocols.

7.2 Capital Treatment Clarification

To ensure consistency with global best practices and the Basel III standardized approach, the Capital Adequacy Framework 2018 (applicable to IDBs) and the 2015 Framework (applicable to ABC classes) require alignment on PCG treatment.

Proposed Amendments / Recognition to the Capital Adequacy Framework:

- Eligible CRM Recognition: Formally recognize NIFRA-issued PCGs as an eligible form of Credit Risk Mitigation (CRM) for infrastructure lending.

- Substitution and Risk Weighting: Under the “Substitution Approach,” the portion of a loan covered by a NIFRA guarantee shall attract a 20% risk weight, provided NIFRA fulfills NRB’s capital adequacy requirements.

- Exposure Splitting: To prevent the inflation of “paper capital” (relief without real risk transfer), the framework must mandate exposure splitting. Only the guaranteed portion receives the 20% weight, while the unguaranteed portion retains the risk weight of the underlying counterparty (typically 100%).

- Sovereign Treatment: Portions of claims backed by an explicit sovereign counter-guarantee from the Government of Nepal shall be eligible for a 0% risk weight, consistent with existing treatments for direct claims on the sovereign.

8. Quantitative Impact Assessment

8.1 Capital Efficiency Multiplication

Under the current direct lending model, NIFRA’s impact is limited by the physical size of its balance sheet. With a paid-up capital of NPR 21.60 billion, NIFRA has currently mobilized approximately NPR 25.14 billion in disbursed loans. This 1:1 ratio is insufficient to meet Nepal’s massive infrastructure needs.

By transitioning from a lender to a credit enhancer, NIFRA can achieve a significant multiplier effect:

- Multiplier Effect: Internationally, development banks using credit enhancement tools can mobilize 3–5 times more private lending than direct loans using the same capital base.

- Lending Capacity: The same capital base currently supporting ~NPR 25 billion in loans could support NPR 60–100 billion in commercial bank lending.

- Bank Capital Relief: For participating commercial banks, a 30% NIFRA guarantee allows for exposure splitting, where the guaranteed portion attracts only a 20% risk weight. This provides a 24% reduction in capital lock-up for the lender, incentivizing them to provide the long-tenor debt infrastructure projects require.

Hydropower and energy constitute 51% of NIFRA’s current portfolio, yet many projects remain stalled due to the “Construction Phase Deadlock” where banks avoid front-loaded risks like construction delays and hydrology volatility.

- Catalyzing Investment: A PCG framework can convert “unlendable” pre-COD (Commercial Operation Date) projects into bankable ones by providing a first-loss safety net.

- Economic Impact: Catalyzing NPR 200–300 billion in investment would support the 28,500 MW national ambition. This scale of development creates massive direct and indirect employment in supply chains and contributes to an additional 1-2% in GDP growth through infrastructure-led expansion.

8.2 Risk Management Framework

To ensure financial stability and prevent the creation of “paper capital” (relief without real risk transfer), NIFRA’s guarantee activity must be strictly governed.

- Portfolio Limits: Total PCG exposure should be capped at 50% of NIFRA’s net worth (projected at NPR 25.76 billion for Mid-July 2025) to ensure independent loss-absorption capacity.

- Sector Concentration: To prevent systemic fragility, exposure to a single sector should not exceed 40% of the total guarantee portfolio, following general prudential norms.

- Single Project Limit: Guarantees should be capped at 30–40% of total project debt to ensure the primary lender maintains “skin in the game” and proper monitoring discipline.

- Operational Safeguards: Guarantees must be direct, unconditional, and irrevocable to qualify as Credit Risk Mitigation (CRM). Disbursement triggers should be linked to technical milestones to mitigate construction risk.