1. Introduction: The Nature and Typology of Guarantees

A financial guarantee represents a fundamental contractual nexus in modern finance, operating as a non-fund based, contingent liability wherein a guarantor (typically a bank or financial institution) undertakes to fulfill the financial obligations of a debtor (applicant) to a beneficiary (lender/creditor) in the event of the debtor’s default. This tripartite arrangement, governed by principle-agent relationships, serves as a critical risk transfer mechanism that substitutes the superior creditworthiness of the guarantor for that of the inherently riskier borrower, thereby facilitating transactions that would otherwise be commercially untenable.

The guarantee ecosystem comprises specialized instruments, each tailored to distinct transactional need and risk exposures:

- Bid Bond Guarantee: Securing the tender award stage, this instrument ensures the bidder’s commitment to honor its offer if selected, protecting the project owner from bid withdrawal or post-award renegotiation. The typical guarantee amount ranges from 1-5% of the bid value.

- Performance Guarantee: Activated during project execution, this covers the satisfactory completion of contractual obligations concerning quality specifications, timelines, and cost parameters. It typically amounts to 5-10% of the project value and remains valid until project completion certificates are issued.

- Advance Payment Guarantee: Protecting pre-payments made to contractors or suppliers, this guarantee ensures the advanced funds are utilized for the designated purpose and that the recipient performs accordingly. Coverage usually matches the advance payment amount.

- Financial Guarantee: This article’s focus, representing a direct credit substitute that guarantees repayment of financial obligations, such as loan principals and interest payments. Unlike performance-based guarantees, it directly addresses credit risk rather than contractual performance risk.

- Counter-Guarantee: A foundational instrument in cross-border transactions, where a local bank guarantees the obligation of a foreign bank, which in turn guarantees the foreign contractor, creating a risk distribution chain across jurisdictions.

The economic substance of these instruments lies not in immediate fund outflow but in the assumption of conditional liabilities that materially impact the risk profiles of all involved parties.

2. The Economic Rationale: Guarantees within the Credit Risk Allocation Matrix

Financial guarantees emerge as institutional responses to systemic capital market imperfections, particularly acute in developing economies like Nepal. The theoretical underpinnings rest on addressing four core market failures:

- Information Asymmetry: Lenders operate under uncertainty regarding borrower quality, future cash flows, and project viability especially for SMEs, agricultural ventures, and infrastructure projects with long gestation periods. This asymmetry leads to adverse selection and moral hazard, causing banks to either overprice risk or ration credit entirely.

- Regulatory Capital Constraints: Under Basel frameworks implemented by Nepal Rastra Bank (NRB), banks face punitive capital charges on risky exposures. Guarantees enable a single unit of public or development finance capital to mobilize multiple units of private lending through credit risk substitution, creating fiscal efficiency without expanding public balance sheets.

- Risk Aversion and Collateral Dependence: Banks exhibit inherent risk aversion toward non-traditional sectors and borrowers lacking tangible collateral. Guarantees facilitate the transition from asset-based lending to cash-flow-based lending, promoting financial inclusion.

- Liquidity and Tenor Mismatches: Long-term infrastructure projects face financing gaps due to banks’ preference for short-term liabilities. Guarantees can mitigate construction and revenue risks, making long-tenor projects bankable.

The following matrix illustrates the precise risk reallocation effected by financial guarantees:

Comprehensive Risk Allocation Matrix in Credit Transactions

Economic Actor | Risk Exposure (Without Guarantee) | Risk Exposure (With Financial Guarantee) | Economic Rationale for Change |

Borrower/Applicant | Business Risk: Full exposure to project failure, market volatility, operational inefficiencies. Retains full obligation to repay. | Business Risk: Unchanged. The borrower remains primarily liable for repayment. The guarantee does not absorb business risk. | The guarantee provides access to capital but does not insure against poor business performance. |

Lender/Beneficiary | Time Value Risk + Full Credit Risk: Bears the cost of funds (interest rate risk) and the complete risk of borrower default (credit risk). Must conduct full due diligence. | Time Value Risk Only: Retains liability for cost of funds and liquidity management. Credit Risk is transferred to the guarantor for the guaranteed portion. Due diligence focus shifts to the guarantor’s credibility. | The lender’s risk-return profile improves significantly. Capital allocation efficiency increases as regulatory capital requirements decrease for the guaranteed portion. |

Guarantor | – | Assumes Credit Risk: Bears the probability of default (PD) and loss given default (LGD) of the borrower for the guaranteed amount. Must hold regulatory capital against this contingent liability. | The guarantor earns a fee for assuming risk but must possess sophisticated risk assessment capabilities. This is their core business function. |

Regulator (NRB) | Systemic Risk: Faces potential contagion from correlated defaults across the banking system. Monitors overall leverage and asset quality. | Systemic Risk Management: The guarantee transfers risk to (typically) well-capitalized institutions. However, concentration risk to specific guarantors must be monitored. Systemic resilience may increase through risk distribution. | The regulator must ensure guarantors are adequately capitalized and that guarantee exposures are properly reported and risk-weighted. |

This reallocation demonstrates that guarantees do not nullify the credit risk; rather, they optimize the existing credit ecosystem by reallocating risk to parties best positioned to bear it, thereby enhancing overall economic efficiency and unlocking deadweight losses associated with credit rationing.

3. Regulatory Architecture: The Legal Foundation of Guarantees in Nepal

The legal framework governing guarantees is pluralistic, drawing from civil, corporate, banking, and foreign exchange laws.

3.1. Civil Code: The Contractual Bedrock

The National Civil (Code) Act, 2017 (NCC) provides the foundational contract law principles. Part 5, Chapter 7 is dedicated to contracts of guarantee.

- Definition (Section 68): A “contract of guarantee” is defined as a contract to perform the promise or discharge the liability of a third person in case of their default.

- Formality Requirement (Section 69): For enforceability, the contract of guarantee must be in writing. Oral guarantees are not legally binding, a crucial safeguard in financial transactions.

- Liability of Guarantor (Section 70): The guarantor’s liability is co-extensive with that of the principal debtor, unless the contract specifies otherwise. This means the beneficiary can demand performance from the guarantor immediately upon the debtor’s default, without first exhausting remedies against the debtor.

- Continuing Guarantee (Section 71): A guarantee that extends to a series of transactions is termed a continuing guarantee. The guarantor can revoke it for future transactions by providing three months’ notice to the creditor.

(Example: Company A signs a guarantee in favor of the bank for all working-capital loans that the bank may extend from time to time to Company B. This guarantee covers every loan disbursed under that arrangement over several years.) - Subrogation Rights (Section 75): Upon payment of the guaranteed debt, the guarantor is subrogated to all the rights and remedies the creditor had against the debtor. This indemnity principle is fundamental to recourse.

- Discharge of Guarantor (Sections 76-77): The guarantor is discharged from liability by any act or omission of the creditor that prejudices the guarantor’s rights or alters the original contract without the guarantor’s consent (e.g., granting the debtor an indefinite extension without the guarantor’s approval).

3.2. Corporate Law: Restrictions on Guarantee Provision

The Company Act, 2063 establishes a multi-layered defense system to prevent the misuse of corporate assets through guarantees, addressing distinct risks at different governance levels.

- Strict Prohibition Against Insider Benefitting (Section 101(1)): Companies are absolutely barred from providing guarantees for loans taken by their directors, substantial shareholders (1%+ holders), or their close relatives. This prohibition extends to insiders of parent/subsidiary companies, creating a robust shield against resource extraction by controlling parties. The sole exceptions apply to banks/FIs in their ordinary course of business and employee loan schemes governed by company rules.

- Calibrated Limits on Corporate Group Exposures (Section 176(1)): To prevent excessive risk contagion within corporate groups, a company’s guarantee for another entity’s debt is capped at the higher of 60% of its total equity (paid-up capital + free reserves) or 100% of its free reserves. Exceeding this threshold requires a special resolution (75% majority) by shareholders. Banks, insurance companies, infrastructure firms, and parent companies guaranteeing wholly-owned subsidiaries are exempt from this limit, as they operate under specialized prudential regimes or the guarantee aligns with existing economic exposure.

- Mandatory Transparency Through Record-Keeping (Section 51(2)): Companies must maintain a statutory register detailing all guarantees provided for loans from banks or financial institutions. This ensures these significant off-balance sheet contingent liabilities are transparent to shareholders, auditors, and regulators, forming the basis for disclosures in financial statements.

3.3. Banking Law: Prudential Governance

The Bank and Financial Institutions Act, 2073 (BAFIA) is the primary regulatory statute for guarantee issuance by financial institutions.

- Definition of Credit (Section 2(ba)): The term “Credit” is defined to include direct or indirect guarantees, bringing guarantees squarely within the regulatory ambit of NRB.

- Authority to Issue (Section 49):

- Class “A” Commercial Banks (Section 49(1)(chha)) are explicitly authorized to issue guarantees (Jamanatpatra) and obtain collateral for such issuance.

- Class “B” Development Banks (Section 49(2)(ka)) can issue bank guarantees but are generally restricted from guaranteeing projects they have promoted.

- Prohibited Guarantees (Section 50): Banks are prohibited from providing guarantees to their own directors, promoters holding more than 1% shares, their family members, or any entity where these insiders have a financial interest. This mirrors the Company Act but with stricter enforcement for regulated entities.

3.4. Foreign Exchange and International Contracts

The Foreign Investment and Foreign Debt Management Bylaw, 2078 regulates cross-border guarantee flows.

- General Prohibition (Schedule 10, Condition No. 5): As a rule, “No kind of collateral, guarantee, or bank guarantee shall be provided from Nepal” for foreign loans taken by Nepali entities. This is a capital control measure.

- Exception for Standby Letters of Credit (Unified Circular 2081): Licensed “A” class banks may issue a Bank Guarantee or Standby Letter of Credit (SBLC) for foreign loans, subject to stringent conditions, provided the borrower is not a manufacturer or exporter (aimed at facilitating import financing).

❌ Prohibited Case (Manufacturer / Exporter): ABC Cement Pvt. Ltd. (Nepal) wants to borrow USD 10 million from a foreign bank to expand its factory. It asks a Nepali commercial bank to issue an SBLC. Not allowed. Because ABC Cement is a manufacturer, Nepali banks cannot issue an SBLC or guarantee for its foreign loan.

✅ Permitted Case (Importer / Trader): XYZ Trading Pvt. Ltd. (Nepal) imports medical equipment. A foreign supplier agrees to give it a supplier’s credit (foreign loan) if backed by an SBLC. A Class “A” Nepali commercial bank issues an SBLC in favor of the foreign supplier, following NRB approval and conditions. Allowed. Because: XYZ is not a manufacturer or exporter, and the SBLC facilitates import financing, not capital flight.

3.5. Nepal Rastra Bank's Supervisory Role

The Nepal Rastra Bank Act, 2058 empowers the central bank to regulate the financial system. The definition of “Credit” in Section 2(c) includes guarantees, providing NRB with the legal basis to issue directives on guarantee exposure limits, capital adequacy, and risk management.

4. The Insolvency Waterfall

The treatment of guarantee claims during insolvency reveals critical fault lines between general corporate law and specialized banking law.

4.1. Claim Recognition and Valuation

The Insolvency Act, 2063 provides the general framework.

- Claim Definition (Section 50(1)): A “claim” includes any debt or liability, present or future, certain or contingent, arising from any guarantee given by the company. This unequivocally includes financial guarantees.

- Valuation of Contingent Claims (Section 50(4)): For future or contingent liabilities (like an uncalled guarantee), the liquidator must estimate the value for the claim to be admitted. If disputed, the court will determine the value upon application by the liquidator. This prevents guarantors from being left without recourse.

4.2. The Waterfall: A Fundamental Contradiction and its Supremacy Clause

The order of payment priority is starkly different under the two acts, creating a potential legal conflict:

Priority Rank | Insolvency Act, 2063 (Section 57) – General Corporate Insolvency | Bank and Financial Institutions Act, 2073 (Section 94) – Bank Insolvency |

1st | Costs of the interim administrator and liquidation proceedings. | Expenses of the liquidation and the Liquidator’s remuneration. |

2nd | Employees: Wages and remuneration of workers/employees due at the time of the winding-up order. | Depositors: Payment to depositors up to the insured amount, followed by remaining deposits. |

3rd | General Unsecured Creditors (This is where a standard guarantee claim would rank). | Employees: Salaries and allowances of the bank’s employees. |

4th | Shareholders (any residual value). | Liabilities to the Government of Nepal and Nepal Rastra Bank. |

5th | – | Other unsecured liabilities (including guarantee claims). |

This contradiction – whether employees or depositors are paid first, is resolved by the doctrine of legislative supremacy embodied in BAFIA Section 94(2), which states: “Notwithstanding anything contained in the prevailing laws, if any amount remains after the payment of expenses… the payment shall be made in the following order of priority…” The phrase “notwithstanding anything contained in the prevailing laws” (Prachalit kanunma jasukai kura lekhiyeko bhaye tapani) gives explicit overriding effect to the BAFIA waterfall for banks and financial institutions. This prioritization of depositors is a cornerstone of financial system stability, designed to prevent bank runs.

4.3. Secured Guarantees

Both acts respect the rights of secured creditors. Under Insolvency Act Section 57(3), a secured creditor can enforce its security outside the waterfall. Only any shortfall from the security sale becomes an unsecured claim. This principle is implicitly recognized in BAFIA, ensuring that guaranteed obligations backed by specific collateral are treated separately.

5. NRB Directives: A Two-Stage Capital Regime

Nepal Rastra Bank’s directives translate the broad legal principles governing guarantees into specific, actionable prudential rules. The core of this framework is a rigorous capital calculation system designed to ensure banks remain solvent even if their contingent liabilities materialize. This system hinges on two distinct but sequential concepts: the Credit Conversion Factor (CCF) and the Risk Weight, which together determine the Risk-Weighted Assets (RWA) and the ultimate capital charge.

5.1. Operational Standards: Upholding the Sanctity of the Guarantee

Before addressing capital, the directives ensure guarantees function reliably as financial instruments.

- Timely Payment: A bank must honour a valid guarantee claim within 7 working days. This enforceability is the bedrock of its value.

- NRB Enforcement Power: If a bank fails to pay without cause, NRB can directly debit the bank’s account to pay the beneficiary, a powerful tool to maintain market confidence.

- Verification: Banks must provide online portals for beneficiaries to verify guarantee authenticity, mitigating fraud risk.

5.2. The Capital Calculation Chain: CCF and Risk Weight Demystified

The prudential treatment of an off-balance sheet guarantee is a two-stage process that answers two different risk questions.

Stage 1: Credit Conversion Factor (CCF) – Quantifying the “Probability of Use”

- Conceptual Question: How likely is this contingent obligation to turn into an actual cash outflow?

- Purpose: The CCF converts the off-balance sheet “notional amount” of the guarantee into an on-balance sheet “Credit Equivalent Amount.” It measures contingency risk.

- NRB’s Stance: For financial guarantees (classified as “Direct Credit Substitutes”), the CCF is 100%. NRB deems it certain that a guarantee will be called if the borrower defaults.

- Credit Equivalent Amount = Nominal Guarantee Amount × 100% CCF

Stage 2: Risk Weight – Quantifying the “Loss Severity upon Use”

- Conceptual Question: If this guaranteed amount is paid out, how much might we ultimately lose based on the counterparty’s creditworthiness?

- Purpose: The Risk Weight is applied to the Credit Equivalent Amount (from Stage 1) to calculate the final Risk-Weighted Assets (RWA). It measures default risk.

- NRB’s Stance: The risk weight depends on the guarantor. For a standard corporate exposure, it is 100%.

- RWA = Credit Equivalent Amount × Risk Weight

The Sequential Calculation in Practice: An Example Consider a NPR 100 crore financial guarantee provided by a company.

- Apply CCF (Stage 1): 100 Cr × 100% = 100 Cr Credit Equivalent Amount. The guarantee is now treated as a hypothetical loan of 100 Cr on the bank’s books.

- Apply Risk Weight (Stage 2): 100 Cr (Credit Equivalent) × 100% (Risk Weight) = 100 Cr RWA.

- Calculate Capital Requirement: 100 Cr RWA × 11% Capital Ratio = NPR 11 Crore in required capital.

This two-stage process explains why financial guarantees are capital-intensive: the full amount is considered at risk (100% CCF) and that risk is priced at the highest level (100% Risk Weight).

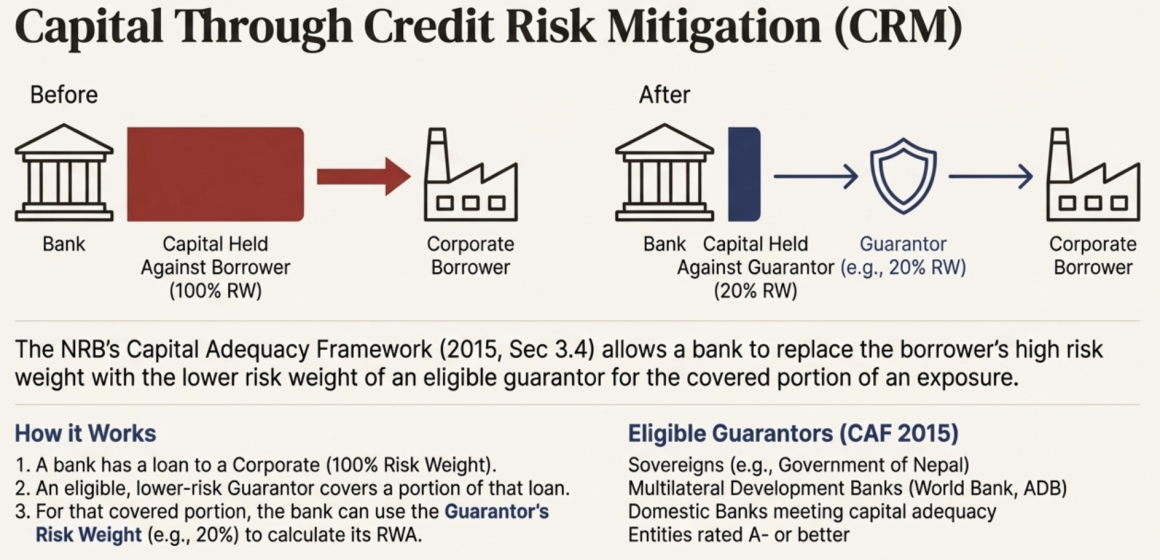

5.3. Credit Risk Mitigation (CRM): The Path to Capital Relief

The NRB framework, as detailed in the Capital Adequacy Framework 2015 (Section 3.4) and Capital Adequacy Framework 2018 (Section D.4), allows for capital relief through a process known as Credit Risk Mitigation (CRM). This is not an exemption but a recalculation based on the superior credit quality of the guarantor. The two-stage process of converting the exposure via CCF and then assigning a risk weight remains paramount.

Eligibility Criteria for CRM Recognition: For a guarantee to be recognized for CRM, it must meet strict operational and legal criteria as per CAF 2015, Section 3.4(a)(6):

- Direct and Explicit Claim: The guarantee must be a direct claim on the protection provider and explicitly referenced to specific exposures.

- Irrevocable and Unconditional: There must be no clause allowing the guarantor to unilaterally cancel the cover or prevent timely payment.

- Right of Pursuit: The bank must have the right to pursue the guarantor for payment without first having to sue the borrower.

Eligible Protection Providers (Guarantors): Capital relief is only permitted if the guarantor is an entity with a lower risk weight than the borrower. The list of eligible guarantors is explicitly defined in CAF 2015, Section 3.4(b) and includes:

- Sovereigns (Government of Nepal, Nepal Rastra Bank, foreign sovereigns with a 0-risk weight).

- Multilateral Development Banks (World Bank, ADB, IFC – 0% risk weight).

- Domestic Banks and Financial Institutions meeting Capital Adequacy Ratio (20% risk weight, subject to supervisory haircuts).

- Other entities rated A- or better.

The CRM Mechanism: Risk Weight Substitution as per Directive: The core of the CRM treatment is the substitution of risk weights, which occurs during the second stage of the RWA calculation. The directive stipulates that the portion of the exposure covered by the eligible guarantee shall be assigned the risk weight of the protection provider. The uncovered portion retains the risk weight of the underlying borrower (CAF 2015, Section 3.4(b)).

Example with Directive-Based Calculation:

A commercial bank has a NPR 100 crore loan to a domestic corporate, which carries a standard 100% risk weight. The loan is 50% guaranteed by the Government of Nepal (an eligible guarantor with a 0% risk weight, as per the standardised approach tables).

- Calculate Credit Equivalent Amount (Stage 1 – CCF Application): The guaranteed portion is converted to an on-balance sheet equivalent. As per the directive, financial guarantees have a 100% CCF.

Guaranteed Portion: 50 Cr × 100% CCF = 50 Cr Credit Equivalent Amount. - Apply Risk Weights (Stage 2 – Risk Weight Substitution): This is where the CRM provision is applied, following the directive’s rule.

- Covered Portion: 50 Cr Credit Equivalent × 0% (GoN’s Risk Weight) = 0 RWA.

- Uncovered Portion: The remaining NPR 50 crore of the loan is treated as a standard exposure to the corporate. 50 Cr × 100% (Corporate Risk Weight) = 50 RWA.

- Total RWA and Capital Savings:

- Total RWA = 0 RWA (Covered) + 50 RWA (Uncovered) = 50 RWA.

- Capital Required = 50 RWA × 11% Capital Ratio = NPR 5.5 Crore.

Without the guarantee, the total RWA would have been 100 Cr × 100% = 100 RWA, requiring NPR 11 Crore in capital.The eligible guarantee thus generates NPR 5.5 Crore in capital relief, demonstrating the powerful leverage of CRM for de-risking bank balance sheets.

Penalty for Unpaid Claims: The directive includes a crucial punitive measure. As per CAF 2015, Section 3.4, if a claim is made on a guarantee but remains unpaid by the institution, the exposure must be assigned a risk weight of 200%, significantly increasing the capital charge and penalizing the bank for failing to honor its obligations.

5.4. Regulatory Rigidity: The Standardized Approach and the Impossibility of IRB

NRB’s regime is characterized by its inflexibility, which is a deliberate prudential choice.

- Simplified Standardized Approach (SSA): The directives often provide a single “Risk Weight” for off-balance sheet items (e.g., 100% for financial guarantees). This is a pre-calculated product of the mandated 100% CCF and the standard 100% Risk Weight. It simplifies reporting but obscures the underlying two-step logic and removes any bank discretion.

- The Impossibility of IRB for NIFRA: The Internal Ratings-Based (IRB) approach, which would allow banks to use internal models to set parameters like CCF, is not a viable option for NIFRA or any Nepalese bank for fundamental reasons:

- No Regulatory Pathway: NRB has not established any guidelines or approval processes for IRB. The legal framework only recognizes the Standardized Approach.

- Data Insufficiency: IRB requires years of granular, reliable default data. NIFRA’s concentrated, long-term portfolio cannot generate the statistically significant data needed.

- Supervisory Capacity: NRB lacks the specialized teams required to validate and audit complex internal models.

- Policy Mandate: Development banks like NIFRA are kept under standardized rules globally to prevent model risk and ensure conservative capital planning. Using IRB to lower capital would contradict their risk-averse policy role.

5.5. Ancillary Provisions

- Recovery Order: Banks must pursue the primary borrower before the guarantor.

- Blacklisting: Guarantors who fail to pay can be blacklisted by the Credit Information Bureau.

- Class D (Microfinance) Rules: Allow for familial and collective guarantees for small loans, reflecting a different risk-management philosophy based on social collateral.

This detailed breakdown shows that NRB’s capital framework, while conservative and rigid, is logically structured. The high capital cost stemming from the 100% CCF and standard risk weight is the primary reason for the subdued market for financial guarantees in Nepal.

6. Market Reality: The Anemic State of Financial Guarantees

The theoretical benefits of guarantees are starkly contrasted by their volume in Nepal’s banking sector. An analysis of bank financial disclosures (as of 2080/81-2081/82) reveals a telling pattern:

- Nabil Bank: Total Contingent Liabilities: NPR 138.10 billion; Total Guarantees: NPR 96.02 billion; Financial Guarantees: NPR 0.

- Standard Chartered Bank Nepal: Total Contingent Liabilities: NPR 129.36 billion; Total Guarantees: NPR 68.33 billion; Financial Guarantees: NPR 0.

- Agricultural Development Bank Ltd.: Total Guarantees: NPR 57.63 billion; Financial Guarantees: NPR 4.13 million.

- Everest Bank Ltd. (An outlier): Financial Guarantees: NPR 376.85 million.

This data demonstrates that the vast majority of “guarantees” are performance or bid bonds related to trade and contracts. Pure financial guarantees are negligible. The primary reason is economic disincentive driven by capital regulation. Since a financial guarantee carries a 100% CCF and typically a 100% risk weight, the capital charge for a bank is identical to that of a direct loan. However, the fee income from a guarantee is a small fraction of the interest income from a loan. Consequently, banks have a clear profit motive to extend credit directly rather than issue financial guarantees. This regulatory treatment stifles the development of a vibrant guarantee market that could otherwise de-risk lending to priority sectors.

7. Mathematical Decomposition: Pricing a Financial Guarantee with Nepalese Data

Pricing a financial guarantee requires a fundamentally different analytical framework from pricing a loan. A loan interest rate represents a comprehensive charge that compensates the lender for four distinct components: (i) the time value of money (base rate), (ii) liquidity and funding costs, (iii) operational overhead, and (iv) the combined cost of credit risk and regulatory capital consumption. In contrast, a financial guarantee is a non-funded, contingent instrument. No principal is disbursed at inception. Therefore, its fee structure must systematically exclude the time value of money and liquidity transformation costs. The guarantee fee must price only three elements: the actuarial expected credit loss, the cost of holding regulatory capital against the contingent exposure, and administrative operational costs.

This distinction is foundational. Approaching a guarantee fee as simply “an interest rate minus the base rate” is analytically flawed and leads to an understatement of the true economic and regulatory cost of risk transfer. This misunderstanding is particularly critical in the Nepalese context, where the regulatory framework, through the Nepal Rastra Bank (NRB) directives, explicitly treats financial guarantees as direct credit substitutes, imposing a full capital charge.

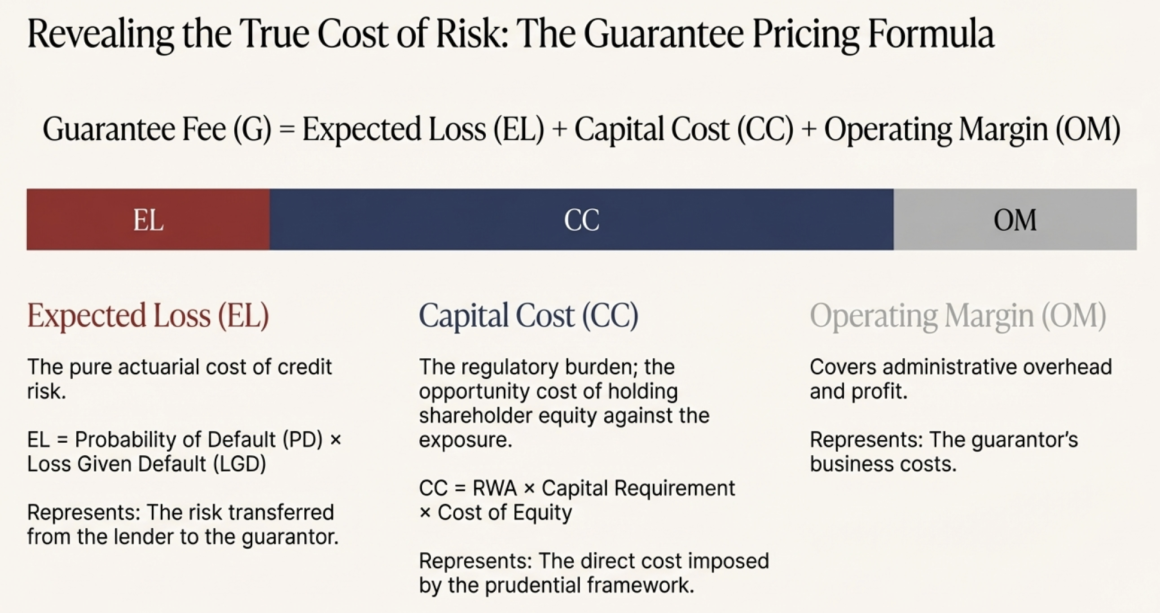

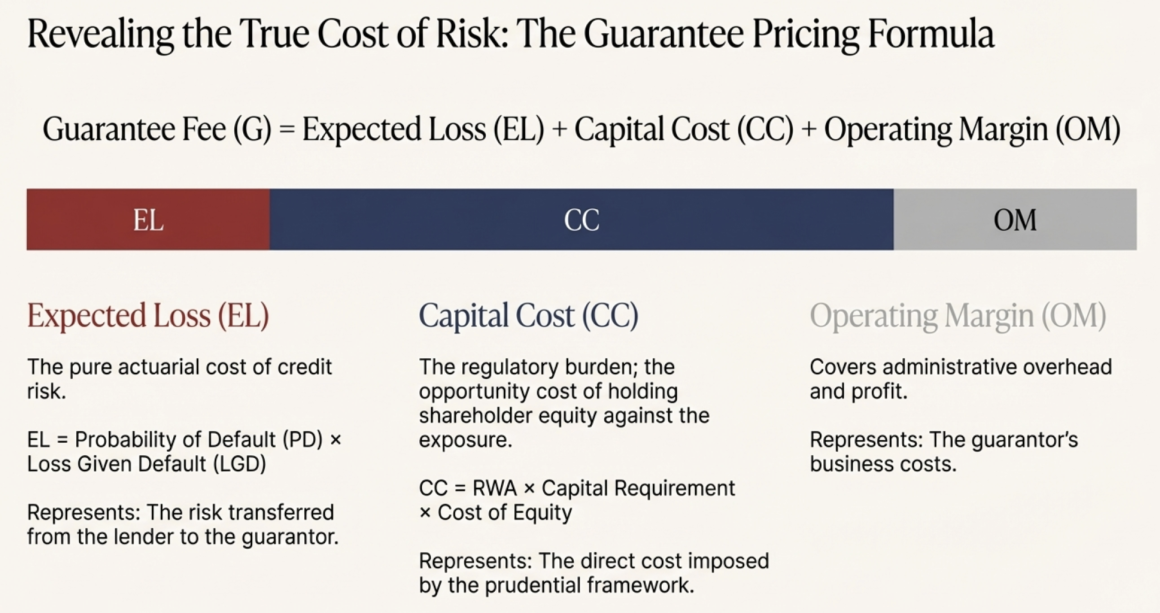

7.1. The Fundamental Guarantee Pricing Formula

The total annual Guarantee Fee (G) can be decomposed into three additive, non-overlapping components:

G = Expected Loss (EL) + Capital Cost (CC) + Operating Margin (OM)

Each term corresponds to a distinct economic or regulatory cost borne by the guarantor.

(a) Expected Loss (EL)

EL = Probability of Default (PD) × Loss Given Default (LGD)

The Expected Loss represents the pure actuarial cost of the credit risk being transferred from the lender (beneficiary) to the guarantor. It is the statistical expectation of the payout over a long-term horizon, calculated as the product of the likelihood of a default event (PD) and the magnitude of loss should that event occur (LGD). This component is independent of funding sources or liquidity considerations.

(b) Capital Cost (CC)

CC = Risk Weight (RW) × Credit Conversion Factor (CCF) × Capital Requirement (CR) × Cost of Equity (CoC)

The Capital Cost reflects the explicit regulatory burden imposed on the guarantor for issuing the guarantee. Under the NRB’s Basel-aligned capital adequacy framework, financial guarantees are classified as direct credit substitutes. This classification mandates a 100% Credit Conversion Factor (CCF), converting the entire notional guarantee amount into a credit equivalent exposure. This exposure is then assigned a Risk Weight (RW) to determine the Risk-Weighted Assets (RWA). Since the equity capital required to support these RWAs carries an opportunity cost (the return expected by shareholders, or Cost of Equity), this component becomes a dominant, fixed cost driver in guarantee pricing, often surpassing the expected loss.

(c) Operating Margin (OM)

The Operating Margin covers the guarantor’s administrative expenses, including legal documentation, credit appraisal, ongoing monitoring, compliance, reporting, and an embedded profit margin. While guarantees are intensely capital-intensive, they typically involve less operational overhead than managing a full loan portfolio (e.g., no disbursement, collection, or liquidity management activities), justifying an OM lower than that applied to funded credit.

7.2. Application of the Model with Nepalese Parameters and Sectoral Data

7.2.1. Base Parameter Assumptions (Uniform Across All Sectors)

Given the constraints of publicly available data and the prevailing regulatory environment in Nepal, the following conservative yet defensible assumptions are applied uniformly:

- Loss Given Default (LGD): 8%. This assumption reflects the highly collateralized nature of Nepalese banking, where loans are often secured by assets exceeding 100% of the loan value. Historical recovery rates, though slow, are high. It is critical to note that this 8% likely reflects accounting loss severity and may understate the true economic loss, including time value and resolution costs, a conservative bias explicitly acknowledged.

- Risk Weight (RW): 100%. As per the standardized approach under NRB directives for corporate exposures.

- Credit Conversion Factor (CCF): 100%. As per NRB’s treatment of financial guarantees as direct credit substitutes.

- Capital Requirement (CR): 11%. reflecting Nepal’s implementation of the Basel III minimum Capital Adequacy Ratio.

- Cost of Equity (CoC): 15%. A reasonable estimate of the required return on equity for Nepalese banks, accounting for country risk, market illiquidity, and alternative investment opportunities.

- Operating Margin (OM): 0.50%. Set lower than typical loan margins due to the absence of funding-related operational costs.

7.2.2. Sector-Specific Risk Input: The PD Proxy

In the absence of flow-based, point-in-time Probability of Default (PD) data by sector, the sectoral Non-Performing Loan (NPL) ratio is employed as a proxy for the long-run through-the-cycle average PD:

PD_sector ≈ Sectoral NPL Ratio

While NPLs are a stock measure and PD is a flow concept, this approximation is a standard practice in policy analysis within data-constrained environments, particularly in banking systems characterized by extended workout periods, frequent restructuring, and strong reliance on collateral, all hallmarks of the Nepalese market.

7.2.3. Capital Cost Calculation (A Fixed Cost Across Sectors)

Due to the uniform regulatory treatment of financial guarantees, the Capital Cost is constant for all sectors:

CC = 100% × 100% × 11% × 15% = 1.65%

This 1.65% represents a fixed, structural cost of issuing any financial guarantee in Nepal. It is inescapable, meaning that even exposures to zero-risk sectors incur this cost solely due to the prudential capital framework.

7.2.4. Illustrative Sectoral Guarantee Fee Calculations

(a) Construction Sector

PD (NPL proxy): 15.16%

LGD: 8%

EL = 15.16% × 8% = 1.21%

G = 1.21% (EL) + 1.65% (CC) + 0.50% (OM) = 3.36%

The resulting guarantee fee of 3.36% is driven by the sector’s high inherent credit risk combined with the mandatory capital charge.

(b) Electricity, Gas & Water Sector

PD (NPL proxy): 0.00%

EL = 0.00% × 8% = 0.00%

G = 0.00% (EL) + 1.65% (CC) + 0.50% (OM) = 2.15%

This example is critical: even for a sector with virtually no observed defaults, the guarantee fee remains significantly above 2% due purely to the fixed costs of capital and operations. This starkly illustrates why guarantees are intrinsically expensive instruments under the current NRB regulatory paradigm.

7.3. Sanity Check Against Observed Market Lending Rates

To validate the model’s output, we deconstruct the average sectoral lending rates to extract the implied risk premium priced by the market. The loan rate can be broken down as:

Loan Rate = Base Rate + Liquidity Cost + Operating Margin (Loan) + Implied Risk Premium

Using observed data:

Base Rate: ~5.41%

Liquidity Cost: ~0.50% (estimated from market spreads)

Operating Margin (Loan): ~0.75%

Non-Risk Floor = 5.41% + 0.50% + 0.75% = 6.66%

Construction Sector Analysis:

Average Loan Rate: 7.68% (As of Mid Nov, 2025)

Implied Risk Premium (Market) = 7.68% – 6.66% = 1.02%

Now, compare this market-implied risk premium with the full risk cost from the guarantee pricing model:

Guarantee Risk Cost (EL + CC) = 1.21% + 1.65% = 2.86%

The analysis reveals a disconnect: the loan market prices only a 1.02% premium for risk, while the actuarially and regulatorily sound cost of that same risk is 2.86%. This indicates that Nepalese banks do not fully price credit risk into their loan interest rates, instead relying on collateral liquidation, loan restructuring, and regulatory forbearance to manage losses. The conclusion is that the modelled guarantee fee is not excessively high; rather, it reveals the true, otherwise obscured, economic cost of risk that the loan market fails to price accurately.

Note: Please note that the above calculations are only indicative and involve multilevel assumptions because of the absence of the publicly available Probability of Default, Loss Given Default, Marginal Lending Rate, Implicit Liquidity Cost and so on. If I get that particular information, I will repost again with more precise policy pricing for financial guarantees.

7.4. Hypothetical Policy Illustration: Capital Relief via a Partial NIFRA Guarantee

Consider a commercial bank with a NPR 100 crore loan to a corporate borrower in the “Others” sector (NPL: 6.35%, Avg Loan Rate: 8.07%). The loan carries a standard 100% risk weight.

Scenario A: Baseline Without Guarantee

- RWA = NPR 100 crore × 100% = NPR 100 crore

- Regulatory Capital Required = NPR 100 crore × 11% = NPR 11 crore

Scenario B: With a 50% Guarantee from NIFRA (20% Risk Weight)

- NIFRA, as a specialized infrastructure development bank with state affiliation and a policy mandate, is assigned a 20% risk weight.

- Guaranteed Portion (NPR 50 crore): RWA = NPR 50 cr × 20% (NIFRA’s RW) = NPR 10 crore.

- Unguaranteed Portion (NPR 50 crore): RWA = NPR 50 cr × 100% = NPR 50 crore.

- Total RWA for the Bank = NPR 10 cr + NPR 50 cr = NPR 60 crore.

- Capital Required = NPR 60 cr × 11% = NPR 6.60 crore.

Capital Relief Effect:

Capital Relief = 11.00 crore – 6.60 crore = NPR 4.40 crore

This revised calculation demonstrates that assigning NIFRA a risk weight of 20%, reflecting its status as a regulated financial institution, significantly enhances the capital relief effect. The freed capital represents an increase in capital efficiency. This amplified leverage effect underscores the potential for a partial guarantee system to improve the banking sector’s capacity to support new lending without elevating systemic risk, provided the guarantor’s superior regulatory standing is formally recognized within the capital framework. While NIFRA’s current operational mandate may limit such activities, this illustration highlights the substantial quantitative impact of risk-weight calibration on the effectiveness of guarantee instruments.

This mathematical decomposition unequivocally demonstrates that under Nepal’s existing regulatory framework, the pricing of financial guarantees is dominated not by expected credit losses, but by the fixed cost of regulatory capital. Guarantees therefore appear economically unattractive not because they are mispriced, but because the prevailing loan market systematically underprices risk. A strategically designed guarantee system, particularly one involving public or highly-rated guarantors, holds the potential to correct this misallocation, unlock capital efficiency within the banking sector, and enhance broader financial stability by making the true cost of risk transparent and manageable.

8. Conclusion and Policy Implications

The analysis reveals a fundamental disconnect in Nepal’s financial system: while the legal and contractual framework for guarantees is robust, the prudential regulatory treatment inadvertently stifles their use. The application of a 100% CCF and standard risk weights to financial guarantees makes them capital-prohibitive for banks, who rationally prefer direct lending.

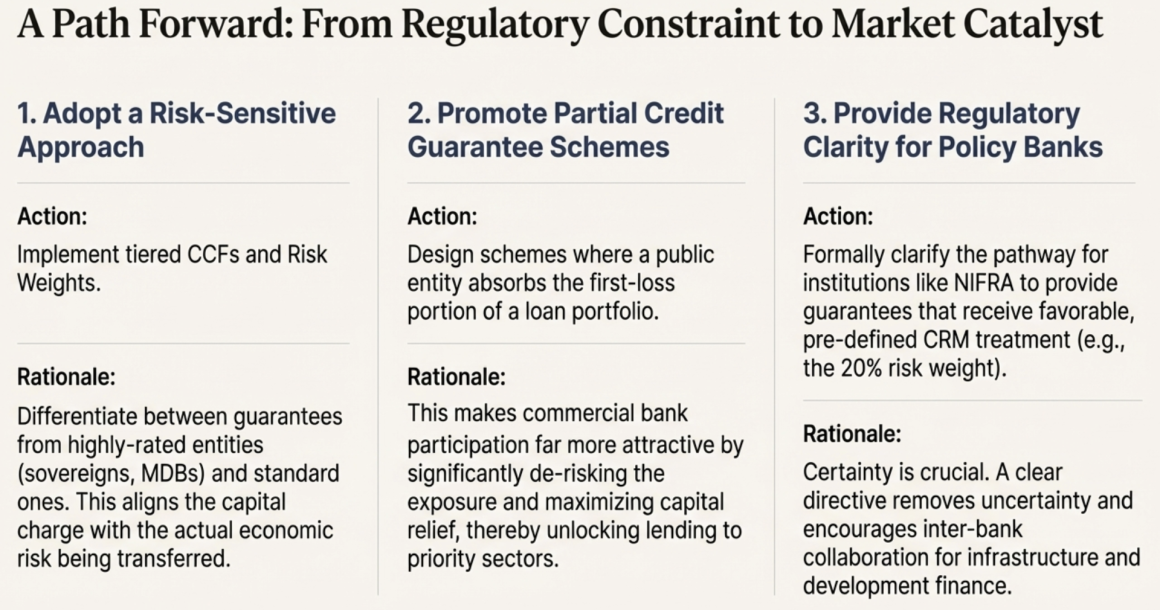

For financial guarantees to fulfill their potential as tools for risk-sharing, financial inclusion, and infrastructure financing, policymakers must consider a more nuanced regulatory approach. This could involve:

- Tiered CCFs and Risk Weights: Differentiating between guarantees provided by highly-rated entities (sovereigns, AAA corporations, MDBs) and others for both CCF and RWA purposes.

- Promoting Partial Credit Guarantees (PCGs): Designing schemes where the government or a development fund absorbs first-loss portions, making commercial bank participation more attractive.

- Clarifying CRM for Policy Banks: Creating a clear pathway for institutions like NIFRA to provide guarantees that receive favorable CRM treatment for partner banks.

By aligning the regulatory capital burden with the economic substance of risk transfer, Nepal can unlock the significant potential of financial guarantees to catalyze private investment, deepen financial markets, and drive sustainable economic growth. This requires a deliberate shift from a conservative, one-size-fits-all capital regime to a more risk-sensitive framework that recognizes the de-risking function of guarantees.