Project Finance, Lender Rights, and the Legal Architecture of Hydropower Debt in Nepal – Findings based on reading of a typical consotrium loan agreement for hydropower financing in Nepal

Part 3 of the Hydro Series

1. What Is a Consortium Loan Agreement and Why Does It Matter?

In the two preceding parts of this series, we traced the regulatory lifecycle of a hydropower project through its two primary government-issued instruments: the Survey License that authorizes investigation, and the Generation License that authorizes construction and operation. Both of those documents represent the state’s role in the transaction – allocating river resources, setting technical parameters, imposing environmental obligations, and ultimately expecting the entire facility back after decades of operation.

The Consortium Loan Agreement represents the third pillar of that same project’s existence – and in many ways the most consequential one. While the generation license determines what gets built and under what conditions, the consortium loan agreement determines whether anything gets built at all. For most large hydropower projects in Nepal, the bulk of capital expenditure – often in the range of 70 percent of total project cost – comes from debt. Without bank financing, there is no dam, no tunnel, no turbine.

A Consortium Loan Agreement (CLA) is a comprehensive legal contract through which a group of banks and financial institutions – collectively called the consortium – pools their resources to provide a large credit facility to a single borrower. It is executed because the capital requirements of a hydropower project are typically too large, and carry too much construction and operational risk, for any single bank to shoulder alone. By forming a consortium, the participating institutions share both the funding burden and the associated risk in proportion to their respective commitments.

The CLA is not simply a loan sanction letter. It is the operational constitution of the project’s financial life – governing everything from the sequence in which the first rupee is disbursed to the conditions under which the last turbine must be tested before commercial operation. It establishes who controls the project’s bank accounts, what happens when a contractor fails, how insurance claims are settled, under what circumstances the banks can seize the generation license, and what the promoters’ personal liability is if the project’s cash flow falls short of what is needed to repay the debt.

| The CLA as the Third Pillar Survey License → permission to study. Generation License → permission to build and operate. Consortium Loan Agreement → the financial engine that makes building possible. All three documents must exist and interlock for a hydropower project to move from paper to power plant. |

2. Why a Consortium? The Logic of Pooled Risk

Large hydropower projects in Nepal – particularly those above 25 MW – carry project costs that frequently run into several billion Nepalese Rupees. A single bank’s exposure limit, prudential lending norms, and capital adequacy requirements typically prevent it from funding the entirety of such a project alone. Consortium lending solves this constraint elegantly: multiple banks each commit a portion of the total debt, their individual exposures remain within regulatory limits, and the developer receives a unified, coordinated credit facility.

The structure designates a Lead Bankthat takes on the primary administrative and coordination role – opening letters of credit, managing the escrow accounts, monitoring construction progress, and acting as the central point of communication between the borrower and the rest of the consortium. A Co-Lead Bank may share some of this administrative burden. The remaining institutions participate as Participating Banks, contributing their share of the debt and sharing in the associated risks and returns on a proportional basis.

The proportional commitment structure is not merely an administrative convenience – it has deep legal significance. Every right, every risk, every piece of collateral, and every rupee of recovered proceeds in the event of a default is shared among the participating banks in proportion to their respective lending commitments. No single bank gets to jump to the front of the line, and no bank can take unilateral enforcement action. This is enforced through a legally binding Inter-Creditors Mechanism that we will examine in detail later in this blog.

| A Typical Consortium Structure in Nepal’s Hydropower Sector For indicative purposes, a large hydropower project might attract a consortium of five to six banks, with the lead bank contributing around 25-30% of the total term loan, the co-lead bank around 20%, and three to four participating banks sharing the remainder. This pattern broadly reflects Nepal Rastra Bank’s consortium lending directives, which govern how these financing structures are organized and administered. |

3. The Legal and Regulatory Foundation

The Consortium Loan Agreement is governed by and construed in accordance with the laws of Nepal. Beyond general contract law, the specific mechanics of consortium financing – how banks coordinate, vote, share collateral, and handle defaults – are governed by the Nepal Rastra Bank (NRB) Directives. These directives are periodically updated and carry significant force: whenever the agreement conflicts with or is silent on a particular matter, the NRB directive governs.

NRB Unified Directives also governs interest capitalization, prepayment charges, and other banking parameters; the Secured Transaction Registry system, where the bank’s charges over assets must be publicly registered to be enforceable against third parties; the Credit Information Center Ltd. blacklisting rules; and the Guideline on Environmental and Social Risk Management issued by the NRB, which the borrower must comply with throughout the loan tenure.

Additionally, because the project’s most critical assets – the Power Purchase Agreement and the Generation License – are government instruments, the CLA must interface directly with the Electricity Act, 2049 and the Electricity Rules, 2050. The banks’ ability to transfer or assign those instruments in the event of a default depends on the consent of the Department of Electricity Development (DOED) and the Nepal Electricity Authority (NEA). This makes the regulatory framework unusually intertwined with government energy policy.

4. The Anatomy of the Loan: Distinct Facilities

A sophisticated hydropower CLA is not a single, monolithic loan. It structures the credit into distinct facilities, each designed to solve a specific financial problem at a specific stage of the project’s life. Understanding these facilities – and why each exists – is fundamental to understanding how project finance actually works.

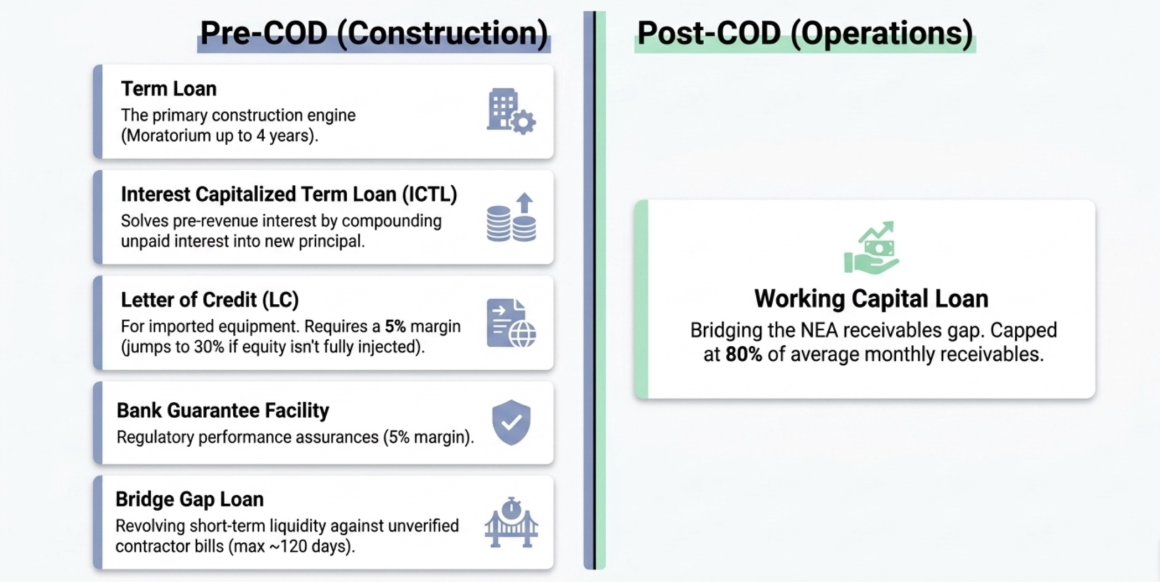

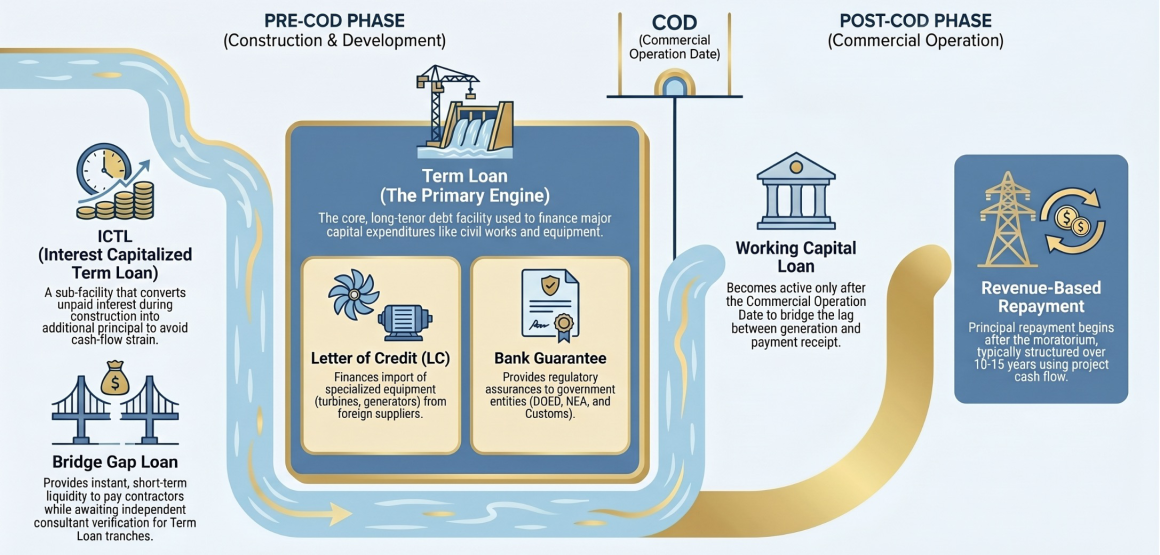

4.1 The Term Loan – The Primary Engine of Construction

The Term Loan is the core facility – the large, long-tenor debt that finances the actual capital expenditure of building the project. It covers the purchase of land, civil construction, hydro-mechanical and electro-mechanical equipment, transmission line installation, project management expenses, and pre-operating costs. It is structured with a moratorium period (typically four years from the date of first disbursement, or until the Commercial Operation Date – whichever comes first), during which no principal repayment is required. Following the moratorium, the total accumulated principal is repaid typically over a 10-to-15-year period in quarterly installments.

The term loan is not handed over in a lump sum. It is disbursed in tranches, strictly tied to verified construction progress. This verification-based drawdown mechanism – which we will examine in Section 7 – is one of the most important risk control features of the entire agreement. In indicative terms typical of Nepal’s hydropower market, a term loan might carry a repayment structure starting at around 3% of the total principal in Year 1 and stepping up progressively to around 10-11% in later years, reflecting the project’s anticipated revenue growth commensurate with the commercial operation.

4.2 Interest Capitalized Term Loan (ICTL) – Solving the Pre-Revenue Interest Problem

During construction, the developer is drawing down the term loan and accumulating debt but is not yet generating any electricity or revenue to service that debt. Rather than demanding cash interest payments that the developer cannot make, the banks provide the Interest Capitalized Term Loan (ICTL) – a sub-facility within the term loan that automatically converts unpaid interest into additional principal.

Here is how it works mechanically: Typically interest on the term loan is calculated daily on the outstanding balance, and at the end of every Nepali calendar quarter (Ashwin, Poush, Chaitra, Ashad), the accrued unpaid interest is formally “capitalized” – booked as a new disbursement under the ICTL and added to the outstanding principal. This has a critical financial consequence: because the unpaid interest is added to the loan balance, and subsequent interest is then charged on this enlarged balance, the mechanism is effectively compounding. The ICTL thus converts what would have been a cash flow problem into an accepted, pre-budgeted addition to total project cost.

The capitalization arrangement is also subject to NRB Directive and the total amount of capitalized interest cannot exceed the budgeted limit defined in the project cost schedule. The ICTL tenure runs in line with the main term loan tenure.

| The Compounding Effect of ICTL Because capitalized interest becomes principal, and that enlarged principal then accrues further interest, the ICTL results in genuine compounding. Developers must model this carefully in their financial projections. A four-year construction period with interest capitalization can meaningfully increase the total debt burden beyond the original term loan commitment, and this entire incremental cost must be absorbed within the approved project budget. |

4.3 Working Capital Loan – Managing Post-COD Cash Flow Gaps

Once the project is generating and selling electricity, it enters a recurring cash flow cycle: the Nepal Electricity Authority (NEA) owes payment for electricity purchased, but there is inevitably a lag between generation and receipt of payment. The Working Capital Loanstructured as a cash credit or overdraft, allows the developer to bridge this receivables gap and fund daily operational expenses.

This facility is only available after the Commercial Operation Date – it has no role during construction. The drawdown is typically capped at a maximum of 80% of the average monthly receivables owed by the NEA under the PPA, preventing the developer from over-borrowing against uncertain future payments. Interest is charged on the Lead Bank’s base rate plus a premium, and the facility is renewed annually based on satisfactory account performance.

4.4 Letter of Credit Facility – The International Procurement Mechanism

Hydropower projects require importing highly specialized equipment – turbines, generators, transformers, steel penstock pipes, and control systems – from foreign manufacturers. A Letter of Credit (LC)is the instrument that makes this possible. The bank issues a formal guarantee to the foreign supplier, promising payment upon delivery and presentation of shipping documents. This eliminates the supplier’s counterparty risk and enables the transaction.

In Nepal’s hydropower CLA structure, the LC facility is typically carved out as a sub-limit within the overall term loan. When an LC is settled – when the foreign supplier presents the shipping documents and the bank pays – that settlement triggers a disbursement of the term loan to fund the payment. The developer contributes their proportionate equity share (say, approximately 23% in indicative terms), and the bank contributes the rest (say, approximately 77%). A 5% cash margin must be deposited by the developer before the bank will open any LC, held in a non-interest-bearing margin account.

There is an important provision allowing the LC facility to be used for forward contract hedging. Because all foreign exchange fluctuation risk falls on the developer, they can use the LC facility to lock in exchange rates through forward contracts, protecting the project budget from currency volatility during the manufacturing and shipping lead time. If the developer needs to order equipment before completing their required upfront equity injection, they may do so – but the cash margin requirement jumps to 30% instead of 5%, reverting to 5% only once the equity injection is completed.

4.5 Bank Guarantee Facility – Regulatory Performance Assurances

The developer must provide financial assurances to several government entities during construction – the Department of Electricity Development, the Nepal Electricity Authority, and the Customs Office – that it will perform its contractual obligations. The Bank Guarantee facilityallows the developer to use its credit standing with the Lead Bank to issue these performance guarantees, rather than blocking large amounts of its own cash. Like the LC facility, it carries a 5% cash margin requirement and a quarterly commission charge. It is also carved out as a sub-limit within the overall term loan.

4.6 Bridge Gap Loan – Keeping Construction Moving

This is perhaps the most practically important facility for a developer managing a live construction site. The bank will not disburse the term loan against a running bill until its appointed independent consultant has physically verified the work. This verification process takes time. Meanwhile, contractors need to be paid immediately to keep construction progressing. The Bridge Gap Loansolves this by providing instant, short-term liquidity – typically up to NPR 500 million in a mid-size project – against unverified bills, with the understanding that it will be repaid within 120 days once the consultant verification is complete and the term loan disbursement is triggered.

Because it is a short-term, high-convenience facility carrying additional risk for the bank, the Bridge Gap Loan carries a higher interest rate than the term loan. It is revolving – the developer can draw, repay, and draw again within the limit – but it is explicitly not permanent in nature. If there are no bills pending with the consultant, the bridge gap balance must be cleared.

5. The Project Cost Structure and the DPR’s Financial Optimization

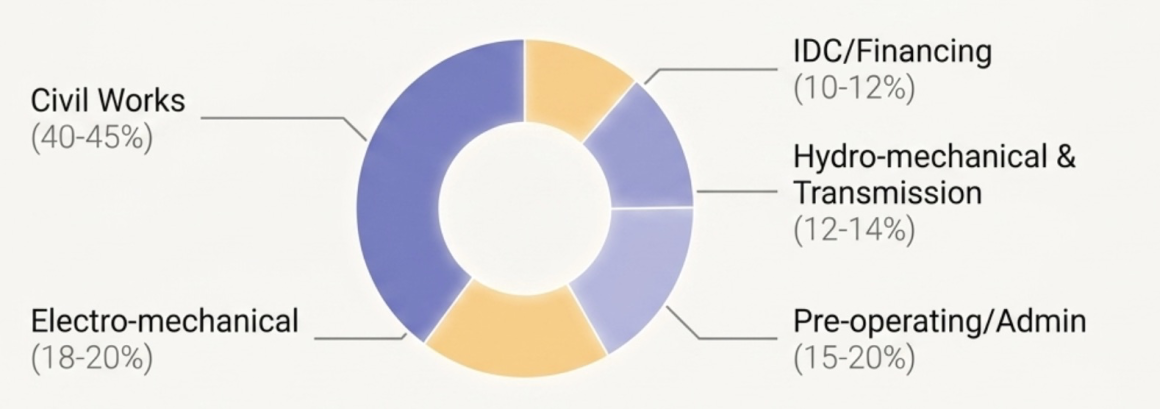

Every CLA is anchored to a specific, itemized total project cost that serves as the financial baseline for the entire agreement. This cost breakdown – derived from the project’s Detailed Project Report (DPR) – is attached to the loan agreement as an annexure and carries significant legal weight: it defines the ceiling of the banks’ lending commitment, the mandatory debt-equity ratio, and the benchmark against which cost overruns are measured.

In a typical mid-to-large hydropower project in Nepal, the cost components break down broadly as follows:

- Civil construction works: The dominant cost category, typically comprising 40-45% of total project cost. This covers dam construction, tunnel excavation, powerhouse cavern, access roads, and all related civil infrastructure.

- Electro-mechanical equipment: Typically 18-20% of total cost. This is the turbines, generators, transformers, and control systems – the heart of the power plant. Almost entirely imported, making it highly sensitive to foreign exchange movements.

- Transmission line and interconnection: Typically 6-7%. The infrastructure required to connect the project to the national grid.

- Hydro-mechanical equipment: Typically 6-7%. Steel gates, penstock pipes, and water-control structures.

- Financing cost including Interest During Construction (IDC): Typically 10-12%. This is the accumulated cost of the ICTL – the interest that compounds during the construction moratorium period.

- Pre-operating, development, land, environmental, engineering, insurance, and administrative costs: The remaining 15-20%, spread across the project’s preparatory and management activities.

A critical insight for anyone reading a DPR-derived cost schedule is that the project’s technical parameters are not purely engineering choices – they are financially optimized decisions. A project is not designed to generate the maximum possible megawatts or use the largest possible tunnel diameter. Instead, every major technical parameter is evaluated against a cost-benefit equation.

For example, a larger penstock diameter reduces friction losses and generates more energy – but costs significantly more in steel, installation, and anchor supports. Engineers calculate the most economic diameter by finding the point where the capital cost of a larger pipe exactly equals the financial value of the additional energy it would generate. Similarly, the number of turbine generating units is determined not just by capacity requirements but by a reliability-versus-cost analysis: a single large unit is cheapest to install but catastrophic if it breaks down (100% generation loss), while multiple smaller units provide partial-load efficiency during dry seasons and operational resilience.

| The DPR: A Financial Document as Much as an Engineering One The Detailed Project Report that underlies every hydropower CLA is the product of iterative financial and technical optimization. The MW capacity, tunnel length, turbine count, and penstock diameter on the Generation License are not arbitrary – they represent the configuration that maximizes the project’s Financial Internal Rate of Return (FIRR). Understanding this is essential for anyone analyzing or financing hydropower projects in Nepal. A separate blog in this series will explore the DPR optimization methodology in detail. |

6. Conditions Precedent: The Gate Before the Gate

Even after the CLA is signed and the ink is dry, not a single rupee of the term loan can be disbursed until the developer has satisfied a comprehensive list of Conditions Precedent (CP). These conditions represent the banks’ ultimate gate-keeping mechanism – their final opportunity to verify that the project is legally sound, properly capitalized, and ready for construction before committing billions of rupees. The CP requirements fall into six categories:

6.1 Equity Infusion and Financial Requirements

The most significant CP is the initial equity injection. Before the first term loan drawdown, the developer must have already invested a minimum of, say around – 30% of the total equity commitment – or a specific floor amount (depending on the project size), whichever is higher – in the form of verified cash or capital expenditure. This must be certified by a Class ‘A’ Auditor and/or independently valued.

The underlying logic is straightforward: the banks need to know that the promoters have genuine “skin in the game” before lending public deposits. By requiring a large, verified upfront equity injection before releasing any loan funds, the banks ensure that the promoters have already committed substantial personal capital to the project – creating a powerful incentive to see it through to completion. The overall debt-equity ratio (e.g. 70:30) must be maintained at all times throughout the project’s financial life.

6.2 Corporate and Legal Documentation

The borrower must submit certified copies of its Memorandum and Articles of Association, certificate of incorporation, income tax registration, shareholder register certified by the Office of the Company Registrar, and a special resolution from its Annual General Meeting or Extraordinary General Meeting authorizing the financing and designating the signatories.

6.3 Project Approvals and Core Contracts

The developer must complete a Due Diligence Review (DDR) conducted by an independent consultant appointed by the Lead Bank. The DDR must prove the satisfactory technical and financial feasibility of the project. Crucially, the banks explicitly reserve the right to revise the loan amount and terms based on what the DDR reveals – even after the CLA has been signed. This is the banks’ contractual escape valve from the developer’s initial representations, and it remains active not just before the first drawdown but throughout the entire construction period based on ongoing consultant reports. The developer bears all DDR costs.

Additionally, all major project contracts – civil, hydro-mechanical, electro-mechanical, and transmission line – must be submitted and carry prior bank approval before signing. The Construction of the Transmission Line, or a transmission line sharing arrangement, must be resolved and documented before the first drawdown.

6.4 Land Acquisition and Site Readiness

Private land required for all project core components and alignment must be acquired before the first drawdown (transmission line land is normally exempt at this stage). Government land lease agreements must be formally submitted. The banks conduct a mandatory site visit to physically verify the project’s preparation and conditions before committing funds. This is not a formality – it is a precondition. The overall project progress as of the drawdown request date must also be deemed satisfactory.

6.5 Guarantees and Undertakings

The developer must submit formal letters of undertaking supported by Board resolutions covering several critical risk scenarios:

- No shareholding changes: An undertaking that the share structure will not change without prior consortium consent.

- IPO contingency: If the developer plans to raise equity through a public offering and the IPO fails or is delayed, the promoters personally undertake to inject the required equity from their own sources to keep construction uninterrupted.

- Cost overrun management: Any cost overrun above the total project cost baseline will be financed entirely through equity – not additional bank debt.

- NEA direct payment: The developer must arrange for the NEA to submit a formal undertaking that all energy revenue payments will be made directly to the Lead Bank’s account after Commercial Operation Date.

6.6 Insurance

Comprehensive construction-phase insurance policies must be in force and premium receipts submitted before funds are released. This covers the marine-cum-erection and contractor’s all-risk policies discussed later in the insurance section.

7. How Drawdowns Work: The Disbursement Logic

Understanding how the term loan is actually disbursed is essential to understanding the entire financial structure of the project. The answer is not simply “the bank sends money when the developer asks for it.” The mechanism is far more controlled, and the disbursement ratio that governs each payment reflects the project’s underlying debt-equity structure.

After the initial equity injection unlocks the first drawdown, each subsequent disbursement follows a strict formula. For every verified running bill, invoice, or LC settlement, the bank finances, say, 77% of the verified amount, and the developer must simultaneously contribute the remaining 23% from their own equity. These proportions are not the overall project debt-equity ratio (which could be 70:30) – they are the marginal disbursement ratio applied to each individual payment after the front-loaded upfront equity has already been deployed – therefore the ratio is generally slightly higher than the D/E ratio.

The reason the marginal disbursement ratio differs from the overall ratio is a consequence of front-loading. The developer is forced to inject a disproportionately large chunk of their total equity before any bank money flows. Because that large initial equity injection has already been spent, the remaining unpaid costs need to be funded with a higher proportion of bank debt to ultimately land at, say, 70:30 overall target. Therefore the marginal 77:23 ratio is mathematically derived to achieve this balance.

Every single payment – whether to a civil contractor’s running bill, a foreign turbine manufacturer’s LC, or a project management firm’s invoice – must be verified by the consortium’s appointed independent consultant before the bank disburses its share. The consultant physically inspects construction progress, tests materials, reviews invoices, and certifies that the claimed work was actually completed to specification. Payment is made directly to the supplier or contractor as far as practicable, rather than routing through the developer. This eliminates the risk of fund diversion.

| The Bridge Gap Loan as the Verification Lubricant Because consultant verification takes time and contractors cannot wait for payment, the Bridge Gap Loan provides the developer with immediate liquidity against unverified bills. Once the consultant certifies the work, the term loan disbursement is triggered and repays the bridge gap balance. The developer pays a some % premium interest on the bridge gap rate as the price for this interim liquidity. |

8. The Collateral Web: Security Arrangements

The banks’ NPR multi-billion-rupee commitment is secured by a comprehensive portfolio of collateral that covers physical assets, legal instruments, financial guarantees, and personal liabilities. Together, these form what one might describe as a “belt and suspenders” security structure – one that goes far beyond what standard project finance theory would consider necessary, as we will discuss. Here is the full picture:

8.1 First Charge Over Fixed and Current Assets

The banks hold a first and priority charge over all present and future fixed assets of the borrower – land, buildings, civil constructions, plant and equipment, hydro-mechanical and electro-mechanical machinery, transmission lines, and office equipment, whether acquired with bank financing or not. They also hold a first charge over all current assets: receivables, spare parts, and bills.

For assets built on government-leased land – which is the situation for most projects where the river corridor falls within national parks or government forest land – the bank cannot hold a conventional mortgage on the soil itself. Instead, the developer provides a formal commitment supported by a Board Resolution to give the bank a sole charge over all structures built on the leased land, and commits not to assign or dilute the government land use rights (Bhogaadhikar) to any third party without prior consortium consent. A formal notification is also sent to the relevant government department regarding this arrangement.

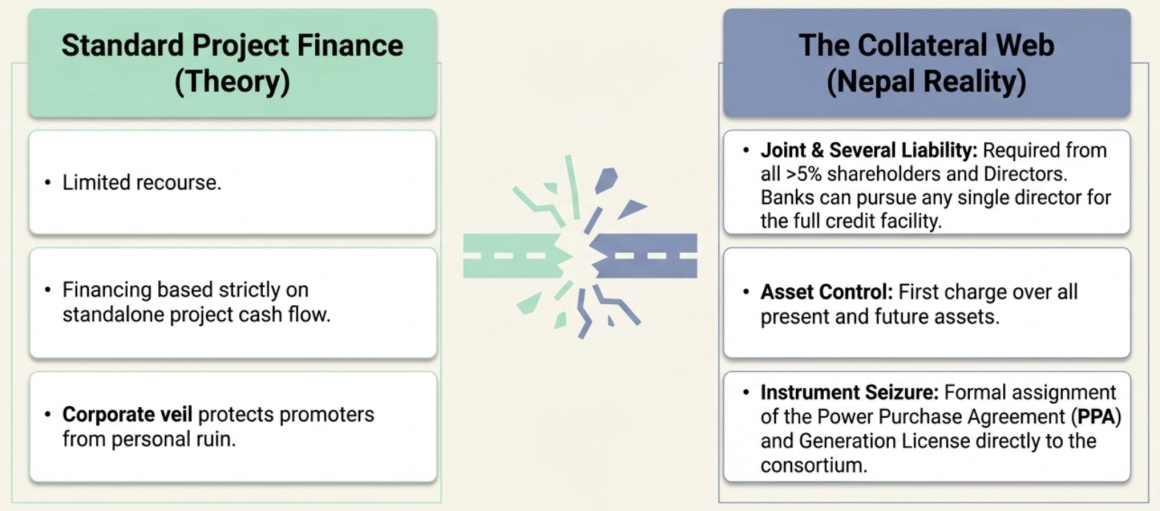

8.2 Assignment of the PPA and Generation License

This is the most strategically important security. The banks require the Power Purchase Agreement and the Generation License to be formally assigned in their favor. The actual PPA document must contain an explicit provision allowing it to be transferred into the names of the Participating Banks at the Lead Bank’s request in the event of specific default triggers. Similarly, the banks hold the right – with the consent of the DOED and NEA – to further transfer both instruments to any other individual, firm, or company if they need to exit their position.

This security is the financial equivalent of holding the keys to the project itself. Without the PPA and Generation License, the project has no legal right to operate, no revenue stream, and no value. By holding the assignment of these instruments, the banks ensure that in the worst case, they can hand the entire operational project to a new developer and recover their debt from that transaction.

8.3 Assignment of Insurance Policies and Project Development Guarantees

All insurance policies are assigned to the banks as co-beneficiaries. The banks generally hold the borrower’s irrevocable power of attorney over insurance claims – meaning the developer cannot negotiate, settle, or collect any insurance payout without the banks’ involvement. The banks have the absolute right to settle, adjust, or compromise any insurance dispute, with or without the developer’s consent. All claim money is paid directly to the Lead Bank.

The banks also require the assignment of Project Development Guarantees – the performance bonds and contractual guarantees that the developer holds against its own contractors and equipment suppliers. If a civil contractor fails and forfeits their performance bond, that payout is assigned to the banks, not the developer. This ensures that even contractor-related financial recoveries flow to the banks first.

8.4 Personal Guarantees: Breaking Through the Corporate Veil

Here the security structure enters territory that many would consider harsh. In standard project finance theory, lenders finance against the project’s standalone cash flow and physical assets. The corporate structure – the Special Purpose Vehicle (SPV) that holds the generation license – creates a legal separation between the project’s liabilities and the personal wealth of its promoters. This is the foundational premise of limited recourse financing.

Nepal’s consortium loan agreements, at least for domestic bank financing, routinely break through this premise. The agreement requires Joint and Several Personal Guaranteesfrom all Board of Directors members and from all shareholders holding more than 5% of the company’s shares, covering the full credit facility amount. “Joint and Several” means the bank does not have to divide the claim equally among the guarantors – it can pursue any single director for the entire outstanding balance, leaving that director to seek contribution from the others independently.

For institutional shareholders, a Corporate Guarantee covering the full facility is required. The entire promoter shareholding – including shares owned by Board members, corporate investors, and personal guarantors – is pledged in favor of the consortium, along with DeMAT records and pre-signed share sale orders that would allow the banks to liquidate those shares instantly in a default scenario.

| Personal Guarantees: The Developer’s Full Personal Exposure A director signing a Joint and Several Personal Guarantee for the full credit facility is personally betting their entire financial existence on the project’s success. If the project fails, the bank can pursue any named guarantor for the total outstanding balance. There is no limited liability protection from the corporate structure once a personal guarantee is signed. Developers entering Nepal’s hydropower financing market must fully internalize this consequence. |

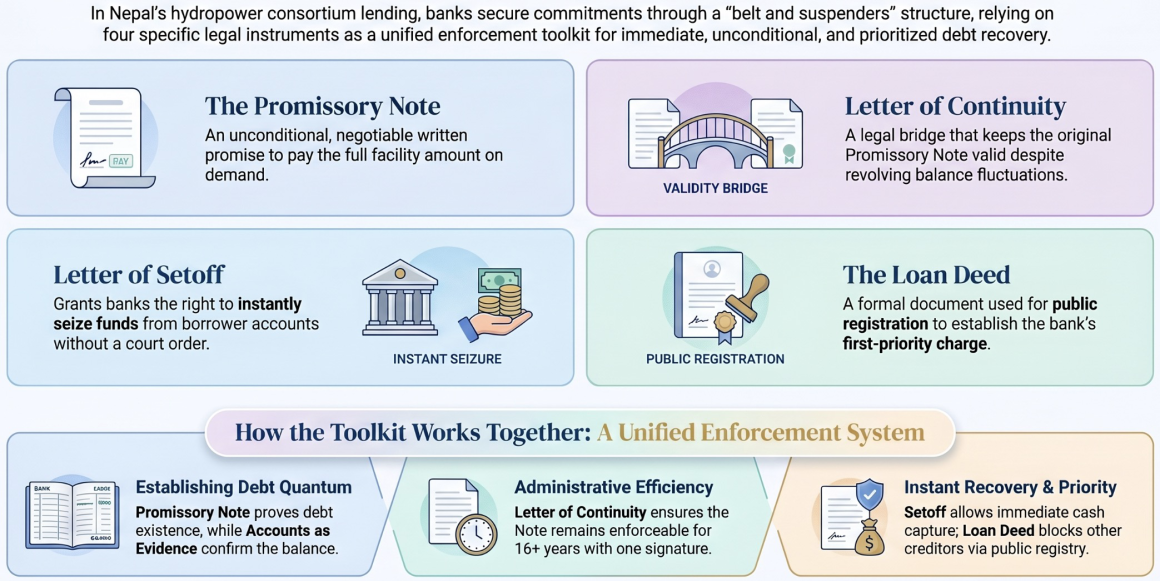

8.5 The Four Standard Enforcement Documents

Beyond the physical and legal collateral, the banks require four specific legal instruments that serve distinct and complementary purposes in the debt enforcement lifecycle. Understanding these is essential because they are the banks’ most direct and immediate recovery tools.

The Promissory Note

A Promissory Note is an unconditional written promise by the borrower to pay a specified sum – the full credit facility amount – to the lender on demand. It is, by design, stripped of the complex conditional language of the loan agreement. Its power lies in this simplicity: in a default scenario, the bank can present the note to a court and establish the debt obligation without arguing over the 40-odd pages of the CLA. The developer cannot use contractual disputes – “the bank breached Section 2.19 by failing to conduct a proper site visit” – as an excuse to withhold payment, because the promissory note is an unconditional instrument separate from the main agreement.

The note is signed for the maximum facility ceiling amount. Some developers question whether this is misleading, given that the loan balance amortizes over time. The answer lies in the “Accounts as Evidence” mechanism built into the CLA: when enforcing the note, the bank always presents it alongside the official account statement showing the actual outstanding balance as of the default date. The note establishes the existence and unconditional nature of the debt; the account statement establishes the quantum. Courts rely on the note to confirm the borrower’s promise and on the account records to determine what amount is actually owed.

There is also a strategic dimension: a promissory note is a negotiable instrument, meaning it can be endorsed and transferred to another party – essentially making the bank’s loan exposure “sellable” to other financial institutions without rewriting the entire CLA. This liquidity in the loan asset is an important feature for the banks’ own balance sheet management.

The Letter of Continuity

This document exists to solve a specific legal problem created by the revolving facilities in the credit structure. Standard contract law holds that when a specific debt is paid down to zero, the legal instrument securing that debt (including any associated promissory note) is “discharged” or fulfilled. For a simple term loan that only decreases, this is manageable. But the CLA includes a Working Capital Loan and a Bridge Gap Loan – both of which are revolving: the developer draws them, repays them, and draws them again.

Without a Letter of Continuity, each time the revolving balance returned to zero and was re-drawn, the bank would technically need the developer to sign a brand-new promissory note. Over a decade long facility, this could happen dozens or hundreds of times – an administrative nightmare and a legal vulnerability.

The Letter of Continuity fixes this by establishing, once and at the outset, that regardless of how much the borrower repays, or how many times the revolving balances fluctuate or hit zero, the original promissory note remains alive and enforceable. It is the equivalent of converting a single-use ticket into a permanent season pass. The note is signed once; the Letter of Continuity ensures it covers every rupee drawn under the facility for the entire 16-year life of the agreement – without the developer’s signature being required again.

The Letter of Setoff

The Letter of Setoff gives the banks the right to seize funds from any accounts the borrower maintains with the Lead Bank to satisfy a missed payment, without requiring a court order or prior notice. If the developer misses a quarterly principal installment, the Lead Bank can immediately sweep the Control Account and Operating Account – where all project revenue and equity is mandatorily held – and apply those funds to the outstanding debt.

This instrument is particularly powerful in combination with the escrow account structure: because all of the project’s cash is mandatorily routed through accounts held at the Lead Bank, the setoff mechanism can be executed instantly and entirely within the Lead Bank’s systems. There is no need to obtain an attachment order, wait for court proceedings, or locate the developer’s assets elsewhere.

The Loan Deed

The Loan Deed is a formally structured, government-registered summary of the debt obligation. Its primary function is public registration – it is the instrument used to file the bank’s charge over the project’s assets with Nepal’s Secured Transaction Registry. Public registration is what makes the bank’s security interest legally effective against third parties: it puts the world on official notice that these assets are encumbered. Without a registered charge, a subsequent creditor might claim equal or superior rights to the same assets. The Loan Deed, once registered, establishes the banks’ first and priority position in any future enforcement.

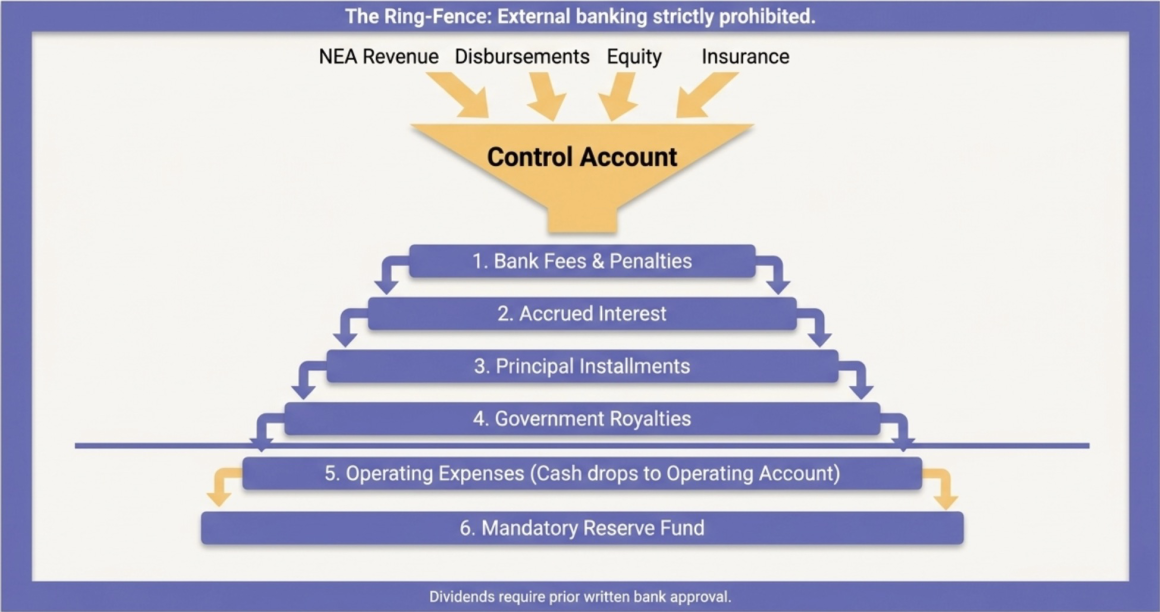

9. The Escrow and Control Account Mechanism

The Escrow Account Mechanismis the operational heart of the banks’ financial control over the project. It establishes a rigid, hierarchical system for how every rupee that enters the project – whether from equity injections, bank drawdowns, NEA revenue payments, or insurance claims – must flow, be stored, and be applied. It is not merely an administrative arrangement; it is a cash flow ring-fence that gives the banks absolute visibility and first-claim priority over the project’s money before the developer can access it for any other purpose.

9.1 The Control Account – The Master Hub

The Control Accountis a Nepali Rupee current account maintained exclusively with the Lead Bank. This is the sole point of entry for all money associated with the project – no exceptions. Every rupee flowing into the project must land here first:

- All revenue received from the NEA for electricity sales.

- All bank loan disbursements.

- All equity injections: share capital subscriptions, promoter contributions, subordinated debt.

- All insurance claim proceeds.

- Any other income from any source.

The Control Account cannot be overdrawn under any circumstances. Outflows from the Control Account are strictly limited to: transfers to the Operating Account for approved operating expenses; payments for taxes and government royalties; approved capital expenditure payments for construction; and payments required under the CLA itself (loan repayments, interest, fees).

9.2 The Operating Account – The Daily Expense Fund

The Operating Accountis a separate current account, also held at the Lead Bank, from which day-to-day operational expenses are paid. Critically, the developer cannot transfer money freely from the Control Account to the Operating Account. Transfers are permitted only in specific amounts required to pay pre-approved operating expenses as provided in a plan. Like the Control Account, the Operating Account can never be overdrawn.

9.3 The Waterfall Principle

The separation of the two accounts enforces a cash flow waterfall that runs directly counter to how a normal private company manages its cash. In a typical corporate scenario, a company collects its revenue, pays its staff and operational costs first, and services its debt from whatever is left. The escrow mechanism inverts this: the banks capture all gross revenue at the Control Account first, ensure their own debt service and non-negotiable government obligations are met, and only then release operating funds down to the developer’s Operating Account.

The specific waterfall order normally mandated in the CLA for project revenue is: (1) fees, commissions, and penalties; (2) accrued interest to the banks; (3) loan principal installment; (4) government royalty; (5) operational expenses through the Operating Account; (6) building up the mandatory reserve fund. Only after all of these have been satisfied can any surplus be considered for other purposes – including, notably, dividends, which also often require explicit prior written approval from the banks regardless of the project’s profitability.

The mechanism also requires the developer to formally arrange with the NEA to route all energy payments directly to the Lead Bank, rather than to the developer. This arrangement is confirmed through a formal undertaking letter from the NEA and is a mandatory CP before the first drawdown. It means the banks intercept the project’s primary revenue stream at the source.

9.4 The Prohibition on External Banking

To prevent any cash from escaping the ring-fence, the developer must close all accounts at banks outside the participating consortium and is prohibited from opening new accounts or obtaining additional credit facilities from outside institutions without prior consortium consent. The only exception is a non-operative account at a bank near the project site if no participating bank has a presence there. This creates a complete financial enclosure: every rupee associated with the project is visible to and controlled by the Lead Bank.

10. The Interest Rate Structure

Normally CLA, unless it is offered under fixed interest structure, establishes rate formulas tied to the banks’ own base rates, creating a floating structure that adjusts periodically.

- Term Loan rate: Calculated as the Weighted Average Base Rate (WABR) of all participating banks, weighted by their respective lending commitments, plus a fixed premium (typically around 2-4% per annum). The WABR is recalculated and applied on the first day of each Nepali calendar month based on the average base rates of the previous three months. There is a floor: if any individual bank’s minimum average base rate, plus the premium, exceeds the WABR-based rate, the higher figure applies.

- Bridge Gap Loan rate: Set at some % above the prevailing term loan rate, reflecting the higher short-term risk.

- Working Capital Loan rate: Based on the Lead Bank’s own average base rate plus the premium, fluctuating monthly.

- Penal Interest: If any payment falls into arrears or an Event of Default occurs, an additional ~2% per annum is levied on the overdue amount from the due date to the date of actual payment.

Interest is calculated on a daily basis on the outstanding debit balance and charged to the borrower’s account. During the construction moratorium, interest is capitalized quarterly rather than collected in cash, as described in the ICTL section above. This daily calculation, quarterly capitalization, and compounding structure means developers must model interest costs with care – particularly for projects with extended construction timelines.

11. Financial Covenants: The Ongoing Compliance Tripwires

Financial covenants are not one-time conditions – they are continuous obligations that the developer must satisfy throughout the entire term of the loan. Failure to maintain any of these ratios is not merely a financial inconvenience; it constitutes a breach of covenant and, under the Events of Default clause, can trigger the banks’ full enforcement arsenal. There are five principal financial covenants in a typical Nepal hydropower CLA:

11.1 Debt-to-Equity Ratio (e.g. 70:30 or better)

The debt-equity ratio – calculated as total liabilities against total effective capital/net worth (paid-up capital, reserves, undistributed profits, and subordinated promoter loans, net of intangibles and accumulated losses) – must be maintained at e.g. 70:30 or better at all times. This is the foundational financial covenant, ensuring the promoters always maintain meaningful equity exposure relative to the banks’ lending. If cost overruns or equity shortfalls push the ratio past 70:30, the promoters must inject additional equity to correct it.

11.2 Debt Service Coverage Ratio (e.g. 1:1 or better)

The DSCR – the ratio of net cash flow to the sum of interest expenses and current maturity of long-term debt – must be maintained at e.g. 1:1 or better. A 1:1 DSCR means the project is generating exactly enough cash to meet its upcoming loan obligations. Falling below 1:1 is one of the most immediate and severe covenants a developer can breach, because it signals that the project’s operating revenue cannot support its debt burden. If the DSCR drops – perhaps because the monsoon was weak and hydrology underperformed – the developer cannot simply point to the weather as an excuse: the covenant is breached regardless of the reason.

11.3 Current Ratio (e.g. 1:1 or better)

The current ratio – current assets to current liabilities – must also be maintained at e.g. 1:1 or better. This ensures the developer has sufficient short-term liquidity to meet immediate obligations, independent of the longer-term debt service picture.

11.4 Interest Coverage Ratio (e.g. 1.3:1 or better)

The interest coverage ratio – net profit before interest and tax divided by interest expense – must be maintained at e.g. 1.3:1 or better. Where the DSCR covers total debt service, the interest coverage ratio specifically ensures the project’s core earnings provide a 30% safety buffer above the pure cost of borrowing.

11.5 The Mandatory Reserve Fund

After reaching Commercial Operation Date, the developer must divert say, 2% of monthly revenue into a dedicated reserve account held at the Lead Bank, continuing until the fund reaches a certain level. The account may then be drawn upon for approved maintenance, supervision, insurance premiums, or contingency needs – but only with the Lead Bank’s prior approval. If drawn down, it must be replenished in periods. This creates a pre-funded buffer against operational disruptions, protecting the banks’ cash flow and ultimately the project’s ability to service debt.

| The Covenant-Default Loop The financial covenants create a particularly difficult trap for developers when project performance deteriorates. If a low hydrology year causes the DSCR to drop below specified DSCR ratio say, 1:1, the developer is technically in breach of a covenant and therefore in an Event of Default. This triggers the banks’ right to demand immediate repayment of the full outstanding balance. The only way to prevent escalation is to proactively inject equity or subordinated promoter loans to artificially prop up the cash flow ratios. Developers operating on thin equity buffers can find themselves in a self-reinforcing spiral. |

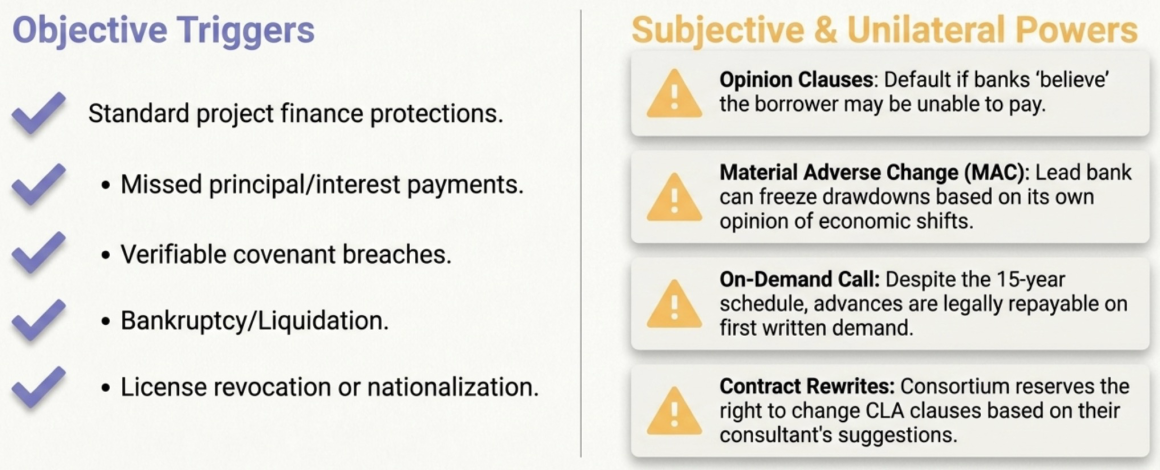

12. Events of Default: Standard Protections and Sweeping Subjectivity

The Events of Default section is where the legal architecture of the CLA reveals its full character. A well-structured events of default provision should enumerate the specific, objectively verifiable failures that legitimately threaten a lender’s position. Nepal’s hydropower consortium agreements include these – but they also include several provisions of a very different nature: subjective, catch-all clauses that grant the banks virtually unlimited discretion to declare a default based on nothing more than their own opinion of the situation.

12.1 The Legitimate Events of Default

These are the standard protections one would expect to find in any large infrastructure loan:

- Missed payments: Failure to pay principal, interest, or fees on the scheduled dates.

- Covenant breaches: Failure to maintain the DSCR, debt-equity ratio, current ratio, or other financial covenants.

- Bankruptcy or liquidation: Any order for suspension of payments, dissolution, winding-up, or appointment of a liquidator or receiver over the borrower or guarantors.

- Nationalization: Government action to nationalize the project’s assets or business.

- Regulatory non-compliance: Failure to adhere to rules and regulations of the Ministry of Water Resources, the NEA, or other government entities – including violation of the PPA or Generation License conditions.

- Secret debt restructuring: If the borrower negotiates with any bank about rescheduling its indebtedness without the Lead Bank’s knowledge or consent.

12.2 The Discretionary and Subjective Events of Default

This is where the analysis becomes critical. Several Events of Default typically seen in CLA are not triggered by objective, verifiable facts – they are triggered by the banks’ subjective assessment of a situation:

| The “Opinion” Clauses: Sweeping Discretionary Power Three Events of Default are explicitly triggered by what the banks “believe” or their “opinion” of the situation, rather than any objectively measurable breach. One clause triggers a default if an extraordinary situation arises which, in the opinion of the Participating Banks, makes it improbable that the borrower can perform its obligations – and explicitly states that the banks’ opinion in this regard is conclusive, final, and binding on the developer. Another triggers default if circumstances give reasonable grounds in the banks’ opinion to believe the borrower may be unable to pay. A third triggers default upon any event that, in the banks’ opinion, may affect the ability or willingness of the borrower to comply with its obligations. The developer has no objective standard to defend against these clauses. |

The “Material Adverse Change” (MAC) clause is the broadest of these. It allows the banks to withhold any drawdown – essentially freezing the project’s financing – if any event occurs or circumstance arises which, in the reasonable opinion of the Lead Bank, constitutes a material adverse change in Nepal’s or the international financial, economic or political conditions, or in the business or financial condition of the borrower. The developer has no right to dispute the Lead Bank’s assessment of what constitutes a material adverse change.

Two other Events of Default are worth flagging for their potential overreach. The clause triggering default on failure to pay “any of the Borrower’s debts” (not limited to debts owed to the consortium) could theoretically allow the banks to trigger a multi-billion rupee enforcement action over an unrelated minor commercial dispute. And the clause triggering default for failing to observe any covenant “as agreed in the meetings of the consortium” means the developer is bound not just by the written CLA but by verbal or minute-recorded decisions made in any consortium meeting – creating a potentially unlimited obligation that is nowhere comprehensively documented.

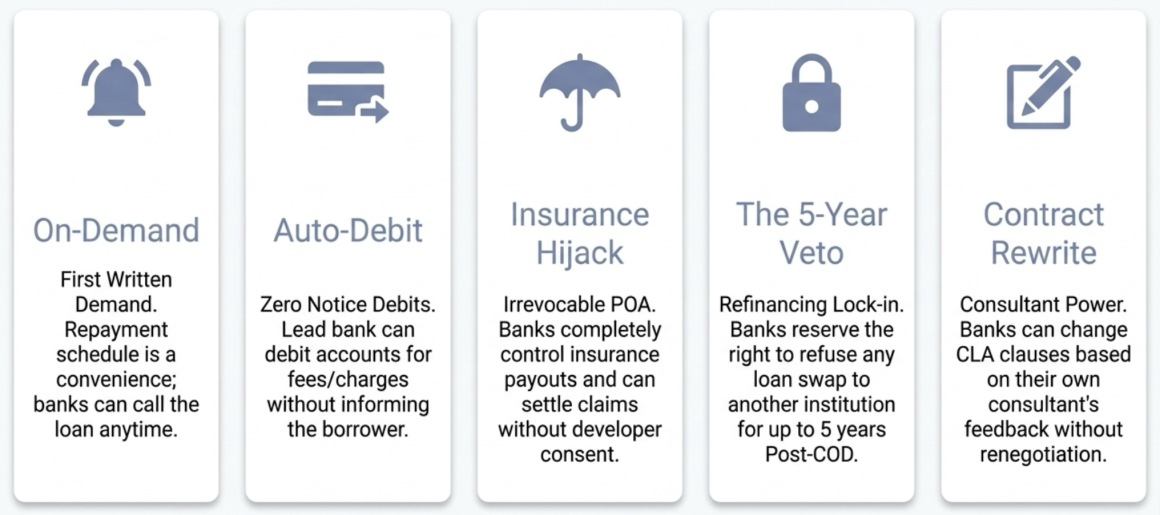

13. Lopsided Rights: The Banks’ Unilateral Powers

Beyond the Events of Default, the CLA contains several additional provisions that grant the banks unilateral powers – rights the banks can exercise at their sole discretion without the developer’s consent, often with immediate financial consequences. Taken together, these provisions transform what is nominally a bilateral agreement into something closer to full-bank-control corporate debt than traditional limited-recourse project finance.

- The “on demand” provision: Despite negotiating a repayment schedule, the CLA explicitly states that notwithstanding any terms mentioned, all advances are repayable on first written demand. The banks retain the unilateral right to cancel the facility and call all outstanding amounts on short notice, at their discretion. The repayment schedule is not a guarantee of tenor; it is a convenience that the banks can revoke.

- The right to rewrite the contract: The consortium explicitly reserves the right to review and change any clause of the CLA based on suggestions received from their own appointed consultants during project monitoring. The banks can modify the agreement’s terms based on their consultant’s feedback, without the developer’s agreement triggering a full renegotiation.

- Account debiting without notice: The Lead Bank can debit the borrower’s account to pay any charges or fees, or to keep the credit facility account in order, with or without prior information to the borrower.

- Insurance settlement without consent: As noted earlier, the banks hold irrevocable power of attorney over insurance claims and can settle, adjust, or compromise any insurance dispute without reference to or consent of the developer. In a catastrophic loss scenario, the bank could accept a below-replacement-value settlement that clears its own exposure while leaving the developer unable to rebuild.

- Rejection of the entire agreement for delay: If the credit facility is not drawn within two years of signing the CLA, the banks have the unilateral right to reject the entire credit facility and agreement, regardless of the reason for the delay.

- Blacklisting and public shaming: In the event of default, the banks have the contractual right to place the borrower, shareholders, directors, promoters, and guarantors on the Credit Information Center’s blacklist, and to publish their names, photographs, and other details in newspapers.

| Subverting Project Finance Principles Standard project finance theory holds that lenders finance against the standalone operating cash flow of the project entity, with recourse limited to the project’s own assets. The combination of personal guarantees, the “on demand” repayment right, the obligation to inject personal equity whenever the project’s cash flow is insufficient to service debt, the right to rewrite contract terms, and the on-demand account debiting effectively transforms this facility into full-recourse corporate debt. The developer’s personal financial existence is fully entangled with the project’s performance. This is not a criticism of Nepal’s banking practices per se – it reflects the risk environment in which domestic banks must operate – but developers entering this market must be under no illusions about the nature of the financing. |

14. Inter-Creditors Mechanism and Enforcement Strategy

When a developer defaults, multiple co-lending banks do not scramble independently. The Inter-Creditors Mechanismensures coordinated, unified enforcement through a structured governance framework. This serves the banks’ collective interest: uncoordinated individual enforcement by competing creditors would destroy value and leave everyone worse off.

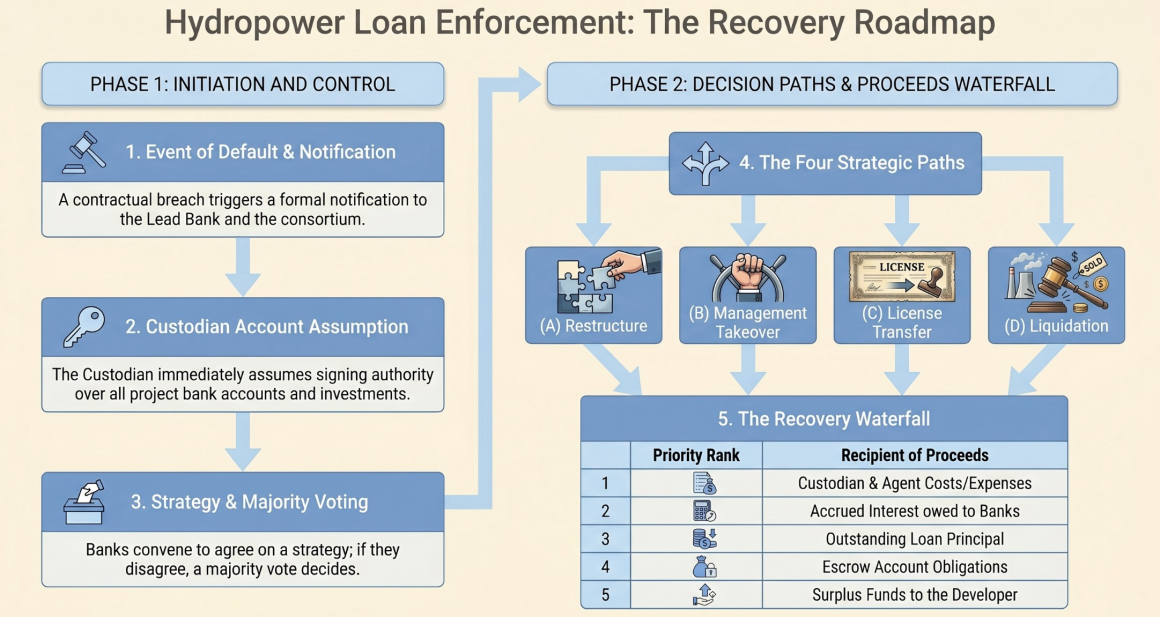

14.1 The Custodian

The Lead Bank serves as the Custodian – the entity that physically holds all collateral documents (land deeds, share pledges, insurance policies, the original promissory note) on behalf of the entire consortium. Individual banks cannot take enforcement action independently; only the Custodian may do so, and only with the approval of the participating banks as a group. Upon a continuing default, the Custodian immediately assumes the borrower’s signing authority over all bank accounts and investments.

14.2 The Enforcement Strategy

Upon a continuing default, the participating banks develop an Enforcement Strategy designed to maximize the net amount recovered from the collateral. This strategy is built on a mutual understanding basis and may include:

- Standstill arrangements: A temporary moratorium on enforcement while the developer and banks negotiate a restructuring.

- Debt rescheduling: Extending the repayment timeline to match the project’s actual cash flow capacity.

- Management takeover: The banks assume operational control of the borrowing company and run the project themselves.

- Liquidation: Forced sale of the project’s physical assets, shares, and legal instruments to recover cash.

If the banks cannot agree unanimously on the strategy, a majority vote – conducted in accordance with the NRB Directives on Consortium Lending – determines the course of action. All proceeds from any enforcement strategy are distributed among the banks in proportion to their outstanding exposure as of the date of payment, following the waterfall priority: first expenses of the Custodian and agents; second interest owed; third principal owed; fourth escrow account obligations; and finally any surplus back to the developer.

14.3 Transfer of the PPA and License in Default

The banks’ most powerful enforcement tool is the ability to transfer the PPA and Generation License to a new developer. This effectively allows the banks to sell the entire going-concern value of the hydropower project – not just its physical scrap value – to a replacement developer who will complete construction or continue operations. The proceeds from that transfer repay the outstanding debt. This mechanism is what gives the consortium real recovery value even in a project that is mid-construction or has not yet reached full commercial operation.

15. The PPA Paradox and the Two-Year Financial Closure Deadline

One of the most commercially challenging aspects of Nepal’s generation license framework – and by extension, the CLA – is the structural tension between the construction commencement deadline and the financing deadline. As discussed in Part 2 of this series (The Generation License), the developer is legally compelled to begin physical construction within one year of receiving the generation license, while the Power Purchase Agreement and Financial Closure may be finalized up to two years after the license is issued.

This timeline creates a critical bankability gap. Commercial banks in Nepal – and lenders generally – will not disburse project loans until a PPA is signed, because the PPA is the contractual guarantee of future revenue that makes the project’s cash flow model viable. Without a PPA, there is no proven revenue stream; without a proven revenue stream, there is no bankable project. Yet the government requires construction to begin before this commercial foundation is in place.

The practical consequence is that developers must fund the first year of construction entirely out of their own equity – the same, say, around 30% minimum upfront equity injection that is also a CLA Condition Precedent. Site preparation, access road construction, early civil works, contractor mobilization, and initial equipment procurement all begin on the developer’s own balance sheet, before a single bank rupee is committed.

The CLA compounds this by requiring that if the PPA and Financial Closure are not completed within two years, the developer must apply for an extension before the deadline expires or face automatic license cancellation. Extensions carry a capacity royalty penalty (indicatively 100 rupees per kW of installed capacity), which starts accumulating immediately and eats further into project economics. Even with extensions, the overall generation license period is fixed – delay in financial closure translates directly into fewer years of commercial operation before the mandatory handover.

| The Developer’s Dilemma The one-year construction start mandate forces developers to invest substantial personal capital before their financing is secured. If they successfully attract bank financing but it takes longer than two years to close, the penalty royalty accrues. If they fail entirely to close financing, the license is cancelled, the construction-phase investments are forfeited, and the land they purchased for the project cannot be sold. This creates a high-stakes, front-loaded risk profile that effectively restricts the market to well-capitalized developers with both patient equity and sophisticated financing capabilities. |

16. Insurance Requirements: Mandatory Coverage and Bank Control

Insurance in a hydropower project is not an optional add-on – it is a mandatory, specifically structured, bank-controlled risk management instrument. The CLA imposes comprehensive insurance requirements across both the construction and operational phases, with coverage that must meet not only the bank’s requirements but also the specifications in the PPA.

16.1 Construction Phase Insurance

- Marine cum Erection Policy: Covers all hydro-mechanical and electro-mechanical equipment – turbines, generators, transformers, steel pipes – against transportation and installation risks. This is particularly critical given that most EM equipment is imported by sea and transported through Nepal’s mountain terrain.

- Contractor’s All Risk Policy: Covers all civil construction works and associated risks during the construction period.

16.2 Post-Construction (Operational) Insurance

Once the project is operational, all project assets must be comprehensively insured against:

- Fire, storm, flood, landslide, burglary, riot, terrorism, strikes, malicious damage, and earthquake.

- Third-party liability and machinery breakdown.

- Consequential loss coverage: Covering loss of revenues and/or loss of profit for a minimum of six months. This is critical: if a flood destroys the dam, the consequential loss coverage compensates the developer – and by extension the banks – for the revenue that would have been earned during the repair period.

Typically, CLA requires that risk coverage must be maintained at 110% of asset value for normal operations. The developer bears all premiums and renewal costs. If the developer fails to renew any policy, the Lead Bank has the right to renew it directly and debit the developer’s account – without prior notice. All original insurance policies must be physically lodged with the Lead Bank, with copies circulated to the other participating banks.

The most consequential insurance provision is the banks’ irrevocable power of attorney over all insurance claims. The developer cannot negotiate, settle, or collect any insurance payout themselves. The banks control every aspect of claims – including settling disputes with the insurance company without the developer’s consent. All claim money is paid directly into the Control Account at the Lead Bank. This prevents a scenario where a developer collects an insurance payout from a project incident and applies it to other purposes before the bank’s debt is serviced.

17. Cost Overruns and the Financial Ring-Fence

The CLA establishes a fixed total project cost baseline as the financial ceiling of the banks’ lending commitment. Any expenditure that pushes the project cost above this baseline constitutes a “cost overrun,” and the agreement is unambiguous about who bears that cost: the developer. This is one of the most consequential provisions in the entire document because construction cost overruns are extremely common in Nepal’s hydropower sector – unpredictable geology, remote terrain, import logistics, weather events, and contractor issues regularly push projects over budget.

The Cost Overrun Clause mandates that the developer must finance all overruns – caused by whatever reason – through promoters’ or shareholders’ sources, specifically by way of additional equity or subordinated promoter loans. The developer is explicitly prohibited from taking on additional external debt to fund overruns without the consortium’s prior approval. Any additional loan injected for any reason is automatically subordinated to the consortium’s debt and cannot be repaid without the banks’ consent.

To prevent cost overruns from developing undetected, the independent project monitoring consultant is explicitly tasked with monitoring contract costs against the approved budget and advising the developer sufficiently in advance when any line item is trending toward its allocation limit. This early warning system gives the developer time to arrange additional equity before a shortfall becomes a crisis. Additionally, all major construction contracts – civil, electro-mechanical, and hydro-mechanical – require prior consortium approval before signing. The banks’ consultant reviews the contract terms to ensure they contain no clauses likely to result in cost overruns before the developer commits to them.

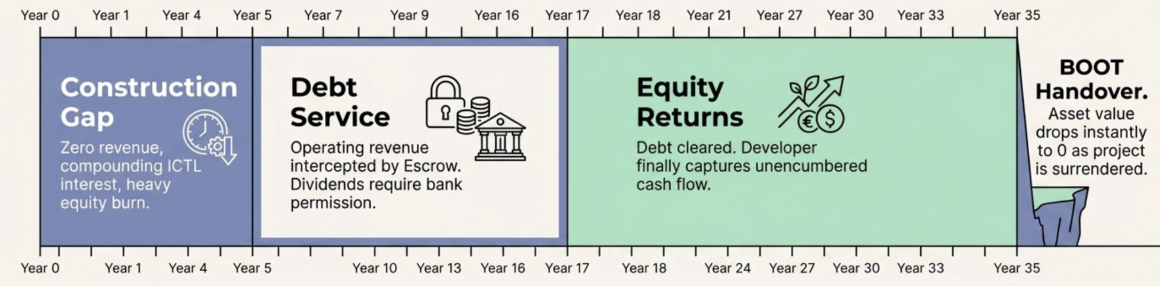

18. The BOOT Connection: How Lender Security Relates to the Project Lifecycle

As established in “Generation License” of this series, every hydropower project in Nepal is structured as a BOOT (Build-Own-Operate-Transfer) concession: the developer builds and operates the facility for the license period, then hands the entire project – land, structures, equipment – back to the government free of cost at the end. This lifecycle has a profound implication for the banks’ security position that is often underappreciated.

Unlike a standard industrial loan where a bank can foreclose on a factory and sell it to the highest bidder, the banks’ security over a hydropower project is fundamentally time-limited and non-transferable to the developer’s benefit. The land itself belongs to the government and is held under a use-right agreement. The structures on that land must eventually be surrendered. Even the private land purchased for the project cannot be sold by the developer if the project fails – it must be handed over to the government. The banks’ charge over these assets is therefore only as valuable as the project’s ability to generate revenue during the operating phase – which in turn depends entirely on the PPA remaining valid and the project operating efficiently.

This is why the banks treat the PPA and Generation License as their most critical security. Physical assets like turbines and concrete structures depreciate, flood, and become geologically unstable. A valid, revenue-generating PPA and an active Generation License are the security that truly matters. Every other provision in the CLA – the personal guarantees, the escrow mechanism, the covenant structure, the insurance requirements – is ultimately in service of protecting those two instruments and the cash flow they generate.

For the developer, the BOOT structure means that the return on investment must be fully realized during the operating period – the 30-35 years between Commercial Operation Date and the mandatory handover. Any delay in construction, any year lost to financing disputes, any period of below-capacity operation reduces the effective revenue-generating window. This is why the financial covenant structure, with its demand for personal equity injections whenever cash flow dips, is so consequential: the banks are effectively requiring the developers to subsidize the project from personal resources to ensure that every year of the revenue window is fully monetized.

| The Developer’s Return Window In a typical 35-year generation license, the first 4 years are consumed by construction (during which no revenue is generated and interest compounds), and the last 12 years are the primary debt repayment period. Only when the debt is repaid can the developer actually begin accumulating equity returns from the project. The BOOT handover at the end of year 35 returns the fully paid-up, fully operational facility to the government. Developers who understand this arithmetic will appreciate why delay in any phase is so expensive. |

19. Prepayment, Swap, and the Lock-In Structure

The typical CLA’s provisions on prepayment and loan swapping reveal another dimension of the banks’ protective architecture – one that explicitly limits the developer’s ability to refinance at better terms even after the project proves successful.

19.1 Prepayment

Normally, in CLAs prevalent in Nepal, prepayment – paying down the loan ahead of schedule – is permitted under two conditions: (a) if funded from the project’s own surplus cash flow or from a public equity offering, it is allowed without penalty; (b) if funded from any other source, a prepayment charge of ~2% of the prepaid amount applies, subject to NRB Directives. An additional 1% charge applies if prepayment/swap occurs within two years of commercial operation.

Operationally, prepayment normally requires 90 days’ written notice to the Lead Bank, must be in multiples of a specified threshold (indicatively NPR 50 million), is applied to the repayment schedule in reverse order (clearing the final installments first rather than reducing near-term obligations), and cannot be redrawn under any circumstances. The reverse-order application is notable: it means prepayment doesn’t reduce the developer’s upcoming installment obligations; it shortens the loan tail instead.

19.2 The Loan Swap – The Five-Year Veto

A loan swap – transferring the debt to a different bank or financial institution, typically to obtain better terms – is where the banks’ protective structure becomes most explicit. Regardless of the developer’s willingness to pay the swap charge (e.g. ~ 2%), the consortium reserves the right to refuse any swap for up to some years (e.g. 5 years) after the Commercial Operation Date. During those five years, the developer cannot refinance even if more favorable market conditions or international project finance lenders offer substantially lower rates.

The five-year lock-in reflects the banks’ interest in protecting their return during the most creditworthy period of the project’s life – the early operational years when cash flow is strongest and the risk profile is improving rapidly. Once the project is operating successfully, the developer’s market power increases. The five-year veto prevents the developer from immediately using that improved creditworthiness to exit the domestic consortium and refinance abroad. After five years, swap is permitted with consortium approval and the applicable charges.

20. Representations, Warranties, and the Developer’s Legal Commitments

At the time of signing the CLA, the developer makes a series of Representations and Warranties – legally binding statements of fact about the company, the project, and the developer’s legal standing. If any of these representations prove false or misleading, it constitutes an immediate Event of Default. The most significant among them:

- Legal validity and priority: The borrower warrants that this agreement constitutes a legal, valid, and binding obligation that ranks first and foremost in priority above all other present and future obligations to third parties.

- Accuracy of the feasibility report: The information contained in the Feasibility Study Report and supporting documents is warranted to be true in all material respects and does not omit any material facts.

- No hidden litigation: No legal proceedings, administrative actions, arbitrations, or government disputes are pending or threatened against the company or its assets.

- No secret liquidation: No action has been taken for winding up, dissolution, or amalgamation of the company.

- Government licenses obtained: All necessary authorizations, permits, and licenses from government authorities required to construct and operate the project have been obtained.

- Clean blacklist status: Neither the company nor its directors and shareholders are currently blacklisted under NRB directives or the Credit Information Center guidelines.

- NRB Environmental Guidelines: The developer commits to implementing and abiding by the NRB’s Guideline on Environmental and Social Risk Management throughout the loan tenure.

These representations are not made once at signing and then forgotten. The CLA explicitly states that they are deemed to be repeated at the time of every drawdown request and on every date on which any loan amount remains outstanding. This means the developer is continuously re-warranting that all of these statements remain accurate for the entire life of the facility.

21. Force Majeure

Force Majeure is the one provision in the CLA that offers the developer a genuine, lender-imposed grace period against certain catastrophic events. Given the risk profile of hydropower construction in Nepal’s mountainous terrain – where floods, landslides, earthquakes, and extreme weather events are not hypothetical but statistically probable over the life of a project – the Force Majeure clause is practically important.

The agreement defines Force Majeure events as: flood, landslide, earthquake, fire, major machinery breakdown, riot, terrorist activities, civil disturbance, insurrection, and civil war. The key threshold is that the event must render operations to a halt for more than say, 30 consecutive days.

If a qualifying event occurs, the default is not immediate. The agreement provides a say, 90-day grace period during which the default is held in suspension while the developer and banks negotiate a course of action to combat the situation. If an agreement is reached within those 90 days – whether a standstill, a construction timeline extension, a restructuring – the default is averted. If no agreement is reached within 90 days, the full default is deemed to have occurred and the banks may demand immediate repayment of all outstanding amounts.

Two conditions must be met to activate this protection: the developer must notify the Lead Bank promptly, and no later than say, 7 working days after the event occurs; and the Force Majeure event must be certified by an expert appointed by the Lead Bank in consultation with the participating banks. The developer cannot self-certify a Force Majeure – an independent expert appointed by the bank makes the determination.

| The Developer’s Only Automatic Grace Force Majeure is the only provision in the CLA that mandatorily suspends the banks’ enforcement rights without requiring the developer’s prior action. Every other potential default requires the developer to proactively inject equity, negotiate, or apply for extensions. Around 90-day Force Majeure shield is automatic upon occurrence and certification of a qualifying event. Developers should ensure their insurance coverage and their communication protocols with the Lead Bank are robust enough to activate this protection quickly when needed. |

22. Other Notable Provisions

22.1 Board Changes Require Bank Approval

Any change in the Board of Directors requires prior approval from the participating banks. The banks’ reasoning is straightforward: the Board members are the personal guarantors of the full facility. A change in Board composition could introduce untested personal guarantors or, conversely, allow existing guarantors to exit their personal exposure. The banks need to evaluate and approve any such change before it takes effect.

22.2 The IPO First Right: Cross-Selling Under the Loan Agreement

One of the more commercially revealing provisions is the requirement that if the developer launches an Initial Public Offering, the first right to act as Issue Manager must be given to the Lead Bank’s merchant banking subsidiary. Additionally, after the shares are listed on the stock exchange, the promoters’ Depositary Participant (DP) accounts – where the pledged shares are held – must be maintained at the Lead Bank’s subsidiary.

This provision serves two purposes simultaneously: it generates fee income for the Lead Bank through the IPO management and DP account services, and it consolidates the bank’s control over the pledged shares by keeping them within its own subsidiary’s custody. The developer has no ability to negotiate around this requirement – it is embedded as a covenant in the loan agreement.

22.3 Dividend Restriction

The developer cannot distribute any dividend without prior written approval from the participating banks. Unlike some loan agreements that permit dividends automatically once the DSCR exceeds a certain threshold, this agreement provides no automatic triggers. No matter how profitable the project is, the developer must seek bank permission to pay dividends. This effectively means the banks retain veto power over returns to equity investors for the entire term of the facility.

22.4 Loan Sell-Down

Any participating bank may sell its portion of the loan to another bank, subject to the prior consent of both the consortium members and the borrower, and in compliance with NRB Directives. The incoming bank must explicitly agree to be bound by all terms of the existing CLA. This provision gives the banks liquidity in their loan exposure – they are not locked into holding the same exposure for 16 years if their own balance sheet management requires adjustment.

23. Conclusion: The CLA as the Developer’s Most Binding Document

The Consortium Loan Agreement is, in many respects, the most consequential document in the hydropower developer’s file. The Survey License grants the right to study. The Generation License grants the right to build and operate. But the Consortium Loan Agreement determines the financial terms on which those rights can actually be exercised – and shapes the developer’s obligations, risks, and personal liability for the next sixteen years.

For developers, the most important takeaways from a careful reading of Nepal’s consortium loan framework are these: the financing is substantially more than limited-recourse project debt; personal financial exposure through joint and several guarantees is a direct and unavoidable consequence of borrowing from Nepal’s domestic banking market; the banks hold extensive unilateral powers that go well beyond what the term sheet typically highlights; the BOOT lifecycle means that the window for recovering equity investment is precisely defined and cannot be extended; and covenant compliance – particularly the DSCR – requires ongoing management as a critical operational priority, not just a reporting exercise.

For investors, the framework reveals why Nepal’s hydropower sector, despite its enormous potential, carries a distinctive risk profile for equity providers. The combination of a front-loaded equity requirement, a mandatory construction start before financing is closed, full personal guarantees, and a time-limited return window means that the equity investment demands both deep pockets and sophisticated project finance capability.

Understanding all three documents in this series – the Survey License, the Generation License, and the Consortium Loan Agreement – gives a complete picture of how a hydropower project is authorized, funded, built, and ultimately returned to the nation. Together, they are the legal architecture of Nepal’s energy future.