Why earning capacity – not share price – is the only defensible basis for valuing hydropower assets under Section 57 of the Income Tax Act, 2058

I. The Question Nobody is Answering Consistently

When Section 57 of the Income Tax Act, 2058 (ITA) is triggered on a hydropower company – whether at development stage, mid-construction, full operation, or near the tail end of its concession – the immediate question is: at what value are the company’s assets deemed to have been disposed?

Section 57(1) is clear in its instruction. The entity is treated as having disposed of its assets and liabilities at their prevailing market value (बजार मूल्य). Section 41 reinforces this: the deemed consideration equals the market value of the asset at the time of disposal. Section 2(ssha) defines market value as the ordinary transaction value for the asset among unrelated persons in an ordinary market transaction.

The legal instruction is unambiguous. The practice is not.

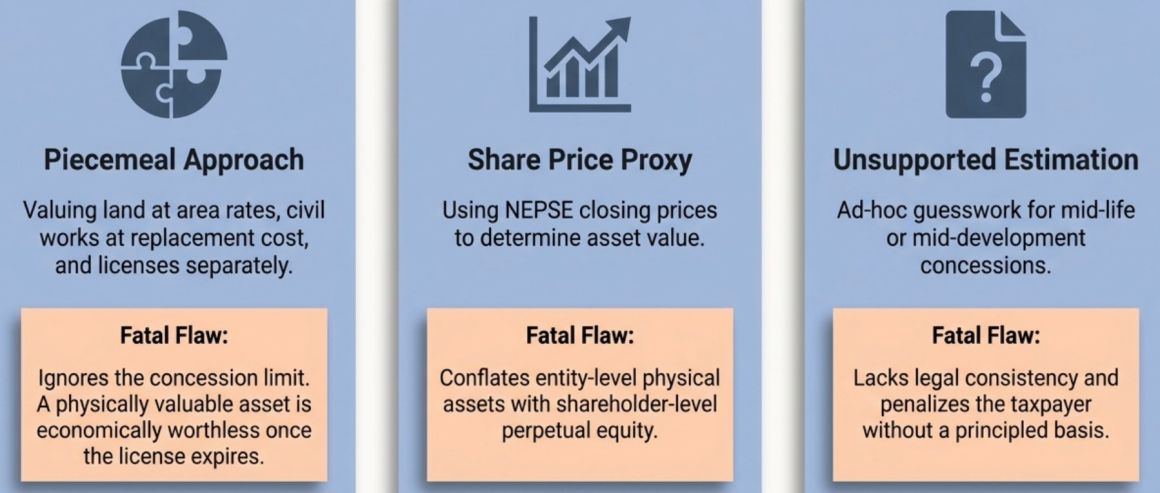

Some assessors value each asset separately – land at prevailing area rates, civil infrastructure at replacement cost, the generation license in isolation. Some reach for the NEPSE closing price of the company’s shares as a proxy for asset value, particularly where the company is listed. Some acknowledge that neither approach is satisfactory for a mid-development or mid-life concession and produce unsupported, inconsistent numbers. There is no principled consistency in the market, and the taxpayer bears the consequences of that inconsistency.

This article argues that all three approaches are wrong – the piecemeal approach, the share price approach, and the unsupported estimation – and that the correct method, simultaneously grounded in Section 57’s legislative intent, the Section 2(ssha) definition of market value, and the accounting framework that governs concession assets under IFRIC 12, is an earning-capacity-based valuation of the concession as a bundle, applied consistently across all lifecycle stages, declining toward zero as the BOOT transfer date approaches.

II. Section 57 on a Concession Asset: The Legal Foundation

Before addressing valuation method, it is worth anchoring the purpose of the provision. Section 57 is an anti-abuse rule, not primarily a taxing provision. Its legislative purpose – derived from the model tax law on which the ITA is substantially based – is to prevent the harvesting of accumulated tax attributes, principally carried-forward losses and deferred interest deductions, by new owners who acquire an entity not for its business prospects but for its accumulated tax shields.

Section 57(2) operationalizes this. Upon a 50% or more change in underlying ownership within a rolling three-year window (measured per Section 57(1), counting only shareholders holding 1% or more per Section 57(1Ka)), the entity loses the right to: carry forward pre-change losses under Section 20(Kha); deduct pre-change interest carried forward under Section 14(3)(Ka); carry back post-change losses to pre-change periods; and utilize several other pre-change tax attributes including foreign tax credits under Section 71(3)(Ja).

The deemed disposal under Section 57(1) – revaluing all assets and liabilities to market value – serves this anti-abuse purpose by resetting the tax base. The new owner cannot access the old tax losses because the unrealized gains embedded in the assets are crystallized and taxed before the new ownership commences, eliminating the arbitrage.

This framing matters critically for valuation. The market value being sought under Section 57 is the value of the entity’s assets – the concession, the plant, the licenses, the PPA rights – as economic instruments in the hands of the entity, for the purpose of resetting the tax base. It is not the value of the shares being transferred between shareholders, which is a separate transaction governed at the shareholder level under Section 95Ka.

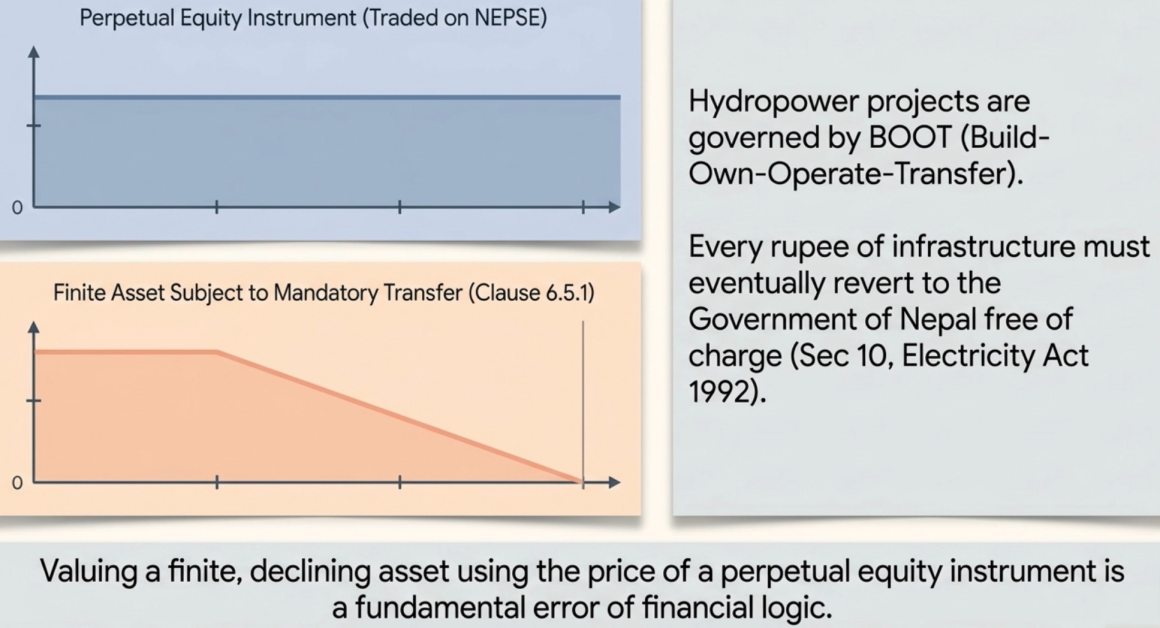

One might ask: where a hydropower project is already generating revenue under a fixed PPA, with stable cash flows and predictable earnings, is the loss-harvesting abuse risk even present? The answer requires intellectual honesty. When PPA tariffs are contractually fixed for the remaining concession life, revenue is substantially predetermined, operating costs are largely known, and every rupee of plant and concession infrastructure will ultimately revert to the Government of Nepal free of charge under the mandatory BOOT handover under Clause 6.5.1 of the Hydropower Development Policy, 2001, the generation licence, under the text of the law and project development agreements, the structural space for tax arbitrage through loss acquisition is narrower than in a normal commercial enterprise. This does not remove Section 57’s applicability – the law applies wherever the ownership threshold is crossed – but it does inform why the valuation must accurately reflect economic reality: a finite-life, declining-value asset, not a perpetually growing commercial business.

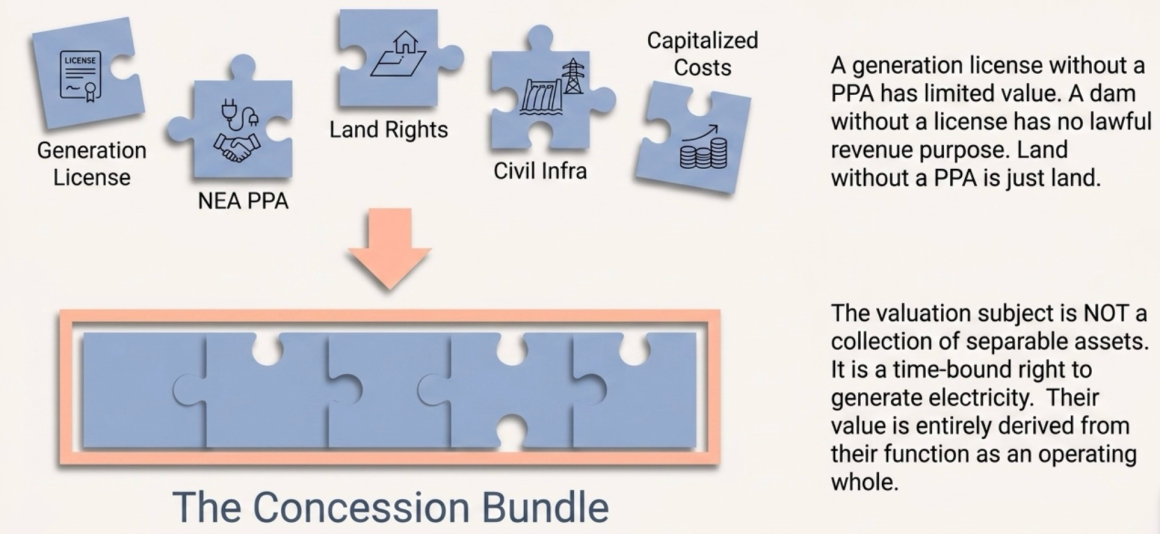

III. What is Actually Being Valued: The Concession Bundle, Not Individual Parts

Section 57(1) deems the entity to have disposed of “the property under its ownership or the liability borne by it.” For a hydropower concession company, this property comprises: the generation license issued under the Electricity Act, 2049 and Electricity Rules, 2050; the Power Purchase Agreement (PPA) with the Nepal Electricity Authority (NEA) approved by the Electricity Regulatory Commission under Section 13(1)(c) of the Electricity Regulatory Commission Act; land rights or leasehold interests in government land; civil infrastructure and electromechanical equipment; and capitalized development and construction costs.

These assets are not economically independent of each other. A generation license without a PPA has severely limited value. A dam without a generation license has no lawful revenue-generating purpose. Land rights stripped of the license and PPA are land, nothing more. The value of each component is entirely derived from its function within the concession as an operating whole. And the concession itself is a finite, time-bound right to generate electricity and sell it under prescribed terms – after which, as Clause 6.5.1 of the Hydropower Development Policy, 2001 and Section 10 of the Electricity Act, 1992 makes explicit, the project must be transferred to the Government of Nepal free of charge and in good running condition.

The valuation subject under Section 57 is therefore not a collection of separable assets. It is the concession – a bundle of rights and obligations whose collective value is entirely a function of the earning capacity it embeds over its remaining life.

This is precisely the principle that IFRIC 12 Service Concession Arrangements encodes in accounting standards. Under IFRIC 12, Paragraph 11 is unambiguous: the infrastructure “shall not be recognised as property, plant and equipment of the operator.” The operator does not own the asset in the conventional sense. What it holds is either a financial asset (Paragraph 16 – an unconditional contractual right to receive cash from the grantor, as arises under a take-or-pay PPA where the NEA is obligated to pay whether or not it dispatches the energy, per the compensation mechanism in such agreements) or an intangible asset (Paragraph 17 – a right to charge users, where demand risk remains with the operator).

For the valuation question under Section 57, the classification between financial asset and intangible asset does not ultimately change the method. What matters is the convergent principle both models share: under either IFRIC 12 model, the value of a concession asset is measured and amortized over the concession life based on the earning capacity it embeds. A financial asset under Paragraph 16 is the present value of the contractual cash flows the grantor must pay. An intangible asset under Paragraph 17 amortizes over the period the operator can charge users. In both cases, the value is a function of future earnings over a finite period. In both cases, the value declines as that period shortens. In both cases, the value is zero – or near-zero – at the moment the concession transfers to the state.

The piecemeal approach that some IRD assessors apply – civil works at replacement cost, land at area market rates, license separately assessed – ignores this substance entirely. It attributes asset values that are independent of the remaining earning life of the concession. Applied to a project in the last decade of its concession, it would systematically overstate value because a dam worth NPR 10 billion to replace has an economic value to its operator of precisely zero the day after the license expires and the asset passes to the government. The replacement cost of the asset and the earning-capacity value of the right to operate it are entirely different things, and only the latter is relevant for Section 57.

IV. Why NEPSE Share Price Cannot Be the Basis

The use of NEPSE-listed share prices as a proxy for the market value of a hydropower company’s assets under Section 57 fails at the level of legal principle and is compounded – severely – by the empirical reality of Nepal’s hydropower secondary market.

The Legal Argument

Section 57 operates at the entity level. Section 57(1) deems the entity to have disposed of its assets. The valuation required by Section 41, read with Section 2(ssha), is the ordinary transaction value of those assets – the concession, the plant, the license – among unrelated persons in an ordinary market. This is an asset-level inquiry, not a share-level inquiry.

A share transaction is a transaction between shareholders in the equity of the entity. It is governed at the shareholder level under Section 95Ka, which imposes capital gains tax on the seller’s gain from the transfer of shares. The price at which a share changes hands between two investors reflects: the underlying net asset value of the entity, plus a control premium or minority discount depending on the stake, plus goodwill and market sentiment, adjusted for liquidity and instrument-specific factors. It is not, and has never been, the market value of the underlying assets.

Section 49 of the ITA, which governs apportionment of costs and proceeds in acquisitions, is instructive here: costs and amounts derived must be apportioned between assets according to their market values at the relevant time – not according to the share price paid. Goodwill – which is inherently embedded in any share price that trades above net asset value – is, as the Ncell case analysis and subsequent commentary have acknowledged, a non-identifiable asset for tax purposes. Under Section 2(Ka.dha), an asset includes goodwill, but goodwill cannot be independently valued for deemed disposal purposes because it is inseparable from the other assets of the business. For the Section 57 deemed disposal – which is not an actual transaction but a legal fiction – goodwill cannot be attributed to the underlying assets because no actual sale has occurred from which a premium over asset values could be observed.

To use NEPSE share price as the basis for Section 57 asset valuation is to conflate the share price with the asset value, to attribute goodwill and market speculation to the underlying concession assets, and to use a shareholder-level instrument to answer an entity-level question. These are legally distinct exercises, and conflating them is an error of principle.

The Practical Argument

Even if one accepted, for the sake of argument, that share price could serve as a proxy for asset value in a well-functioning, arm’s-length market, Nepal’s hydropower secondary market fails every condition that Section 2(ssha)’s “ordinary market among unrelated persons in an ordinary market transaction” demands.

The structural features of this market make this case plainly. The average public float of listed hydropower companies is approximately 20%, with an additional 10% mandatorily allocated to project-affected local residents under the Securities Issuance and Allotment Directive, 2074 – residents who may have little choice or financial sophistication in their participation. Promoter shares – typically 60–80% of the company – are subject to a three-year lock-in from public allotment, structurally suppressing supply. Demand is elevated by the government’s Janata ko Jalvidyut (People’s Hydropower) policy under Section 5 of the People’s Hydropower Program (Operation and Management) Procedure, 2075, which mandates 49% public equity allocation in hydropower projects, effectively making retail investors policy-induced infrastructure financiers rather than voluntary market participants exercising unconstrained economic judgment.

The numbers speak for themselves. As of early 2026, the sector trades at an average price-to-earnings ratio of approximately 180, against an average EPS of NPR 2.54 and a net worth per share of approximately NPR 96.55. More than 60% of listed hydropower companies do not distribute cash dividends – returning value instead through bonus shares that dilute the very earnings base investors are being asked to value. Average return on equity stands at approximately 4.2%, against a sector historical average lending rate of 10.35%. Of rights issues analyzed as of early 2026, approximately 51% of proceeds are deployed to repay bank loans rather than fund productive assets, and approximately 36% flow into inter-company investments in new SPVs – meaning the cash flows of operational projects are being recycled into new construction risk without the original shareholders’ meaningful awareness.

Beneath these numbers lies a structural distortion that goes to the root of the instrument being traded. The underlying asset of a listed hydropower SPV is a finite BOOT concession – a time-bounded right to generate and sell electricity, culminating in mandatory asset transfer to the government at zero compensation. The share being traded on NEPSE is a perpetual equity instrument, legally designed to exist indefinitely. The market prices the share as if the concession were indefinite. It is not. A PE ratio of 180 on a project with a BOOT clock ticking toward zero terminal value is not the discovery of the price of the underlying concession assets. It is the product of a structurally distorted market trading a mischaracterized instrument under policy-induced / abused demand conditions. It does not constitute an “ordinary market among unrelated persons” under Section 2(ssha), legally or practically.

Where an actual arm’s-length share transaction has recently occurred – a negotiated deal at a price between sophisticated, unrelated parties – that transaction price may provide useful evidence. But even here, the share price must be disaggregated from goodwill and market sentiment before it can serve as a proxy for underlying asset value, and the analysis of what unrelated buyers actually pay for hydropower concession rights in Nepal is best observed through actual M&A deal data (enterprise value per MW from completed transactions), not through NEPSE secondary market prices.

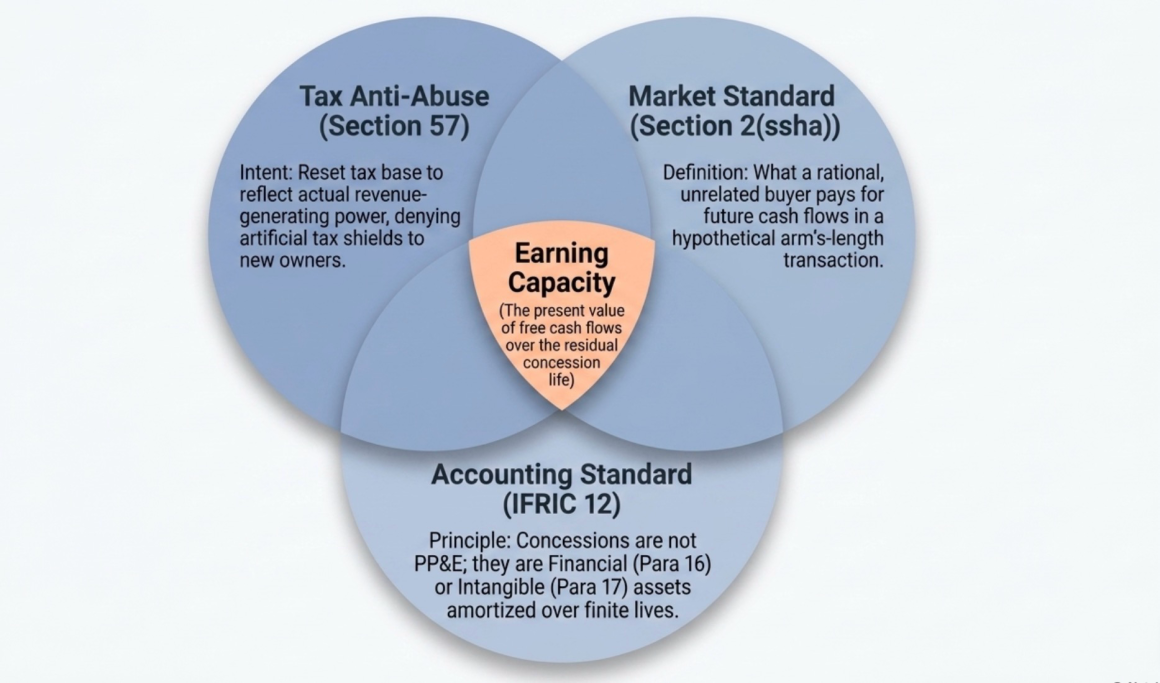

V. Earning Capacity as the Convergent Principle

Three independent lines of analysis converge on a single conclusion: the correct basis for Section 57 valuation of a hydropower concession asset is the present value of the concession’s remaining earning capacity – its ability to generate free cash flows over the residual concession life.

The first line: Section 57’s anti-abuse intent. The deemed disposal under Section 57(1) resets the tax base of the entity’s assets. For this reset to serve its anti-abuse purpose – denying new owners access to old tax shields – the reset value must accurately reflect what those assets are actually worth as revenue-generating instruments. An inflated valuation, derived from a distorted share price or a replacement-cost approach that ignores remaining earning life, would produce an unjustifiably high reset tax base, gifting the new owner an excessive future depreciation base. This is the inverse of the provision’s intent. The correct value is the one that represents the earning capacity of the assets at the time of the change in control – neither inflated by market speculation nor deflated by a piecemeal approach that ignores the finite life.

The second line: Section 2(ssha) and the absence of an ordinary market. Where no active, arm’s-length market exists for a mid-life or mid-development concession asset – and demonstrably, in Nepal, no established market for partial or ongoing hydropower concession interests exists – the Section 2(ssha) definition of market value must be operationalized through what a rational, unrelated buyer would pay in a hypothetical arm’s-length transaction. That rational price is, by definition, the present value of the asset’s future earning capacity, discounted at a rate reflecting the risks of those earnings. This is not a novel concept: it is the foundational logic of income-based valuation, and it is consistent with IRD practice of accepting DCF analysis as a primary method for Section 57 valuations where actual market evidence is unavailable or unreliable.

The third line: IFRIC 12 convergence. Whether the concession assets are classified as a financial asset under Paragraph 16 or an intangible asset under Paragraph 17, the IFRIC 12 framework measures and amortizes the asset over the concession life based on earning capacity. The present value of contractual cash flows (financial asset) and the amortized value of the license right (intangible asset) both produce a declining, finite-life value anchored to future cash flows. This is what the accounting standard recognizes the asset to be. The Section 57 market value should be consistent with this economic substance.

The Method: DCF on Remaining Concession Life

The primary valuation method is a discounted cash flow model built on the remaining concession life, with a terminal value of zero – reflecting the mandatory handover obligation and the absence of compensation for plant and infrastructure under Section 22 of the Electricity Act, 1992.

Free cash flows are projected across the remaining concession years: generation revenue under PPA tariff terms (fixed or formula-based, with any scheduled escalation), operating and maintenance costs, escalating royalty payments, debt service, and taxes. The terminal value is zero.

The discount rate is a project-specific WACC derived from actual debt terms (reflecting real financing costs, not market-implied rates), the project’s hydrological risk, completion risk where applicable, and a cost of equity reflecting the genuine risk characteristics of the concession. Using a NEPSE-implied cost of equity in the discount rate would introduce, through the back door, the very market distortion we have already excluded from the numerator.

One critical exclusion: the tax loss shields that Section 57(2) is designed to neutralize – carried-forward losses under Section 20 and deferred interest under Section 14(3) – must be excluded from the DCF cash flows. Section 57(2) handles these attributes separately and denies them to the new owner. The earning-capacity valuation reflects the pre-loss-shield earning power of the concession; the loss of those shields is a consequence of Section 57(2)(Kha) and Section 57(2)(Ka), not an input to the Section 57(1) asset valuation.

VI. Across the Lifecycle: The Principle Holds, the Value Moves

The earning-capacity framework applies consistently at every stage of the concession lifecycle. What changes is the degree of visibility, the risk adjustments applied, and the weight given to supporting methods – not the underlying principle.

Early Development Phase. At this stage the concession is a set of regulatory options: a survey license, environmental approvals, possibly a generation license in early stages but no PPA, no financial closure. Free cash flows are entirely negative. The DCF must be heavily probability-weighted, reflecting material risk that the project does not reach commercial operation. In practice, the cost-to-date plus a premium for de-risking achieved (license secured, EIA cleared, PPA term-sheet agreed) provides a defensible floor, while a probability-weighted DCF sets the ceiling. A project with NPR 500 million in capitalized development costs but no PPA and no financial closure has an earning-capacity value close to – but not necessarily equal to – its cost base, adjusted for the probability of reaching operation.

The case against using NEPSE prices is most stark at this stage, even as an adjusted proxy (although the hydropower projects don’t get listed at this stage in Nepal). The project has no revenue, no operational history, and a share price driven entirely by speculative demand under policy-induced supply constraints. Applying that price to the Section 57 asset valuation would produce a number with no relationship to any economic reality the assets actually embody.

Construction Phase. Once a generation license is secured, a PPA executed, financial closure achieved, and construction commenced, the DCF acquires significantly more substance. Revenue is projectable from fixed PPA tariff terms, costs are estimable from EPC contracts, and the debt structure is defined. A completion probability adjustment – reflecting residual geological, hydrological, construction delay, and regulatory risk – is applied. As illustrative figures: for an 80 MW run-of-river project at 55% completion, with total project cost of NPR 18 billion and cost spent of NPR 9.2 billion, a risk-adjusted DCF at 11% WACC with 85% completion probability might indicate an enterprise value of approximately NPR 7.6 billion, while a cost-to-date plus 15% de-risking premium approach might indicate NPR 10.1 billion, and a comparable transactions approach at NPR 220 million per MW (operational equivalent) adjusted for a 45% stage discount might indicate NPR 9.7 billion. These three anchors, weighted with DCF at 40%, cost approach and comparables at 25% each, and NAV discounted back at 10%, produce a defensible valuation range – not a NEPSE closing price multiplied by outstanding shares (even if used as a proxy).

Generation Phase. Once the project reaches commercial operation, the earning-capacity DCF becomes most tractable. Revenue is substantially fixed by the PPA tariff, costs are known, and the remaining concession life is the primary determinant of value. Comparables – enterprise value per MW derived from actual arm’s-length M&A transactions – provide a useful cross-check at this stage, but must be drawn from deal data, not from NEPSE market capitalization per MW, which embeds the structural distortions already analyzed.

Tail-End Phase (Last 5–7 Years Before BOOT Transfer). This is where the earning-capacity framework produces its most important result, and where the divergence from share price is most consequential. As the concession approaches mandatory handover, the remaining earning life shortens, the annuity of cash flows diminishes toward zero, and the DCF value of the concession asset declines accordingly.

A Section 57 trigger in the final three years of a concession produces a low deemed asset value – the present value of approximately three years of net operating cash flows, discounted at the project’s WACC. The deemed gain, if any, is modest. The reset tax base for the incoming owner is low. This is economically correct: the incoming owner is acquiring a near-exhausted concession right with a legally mandated zero terminal value.

NEPSE share prices in this scenario – if the market continues applying its structurally distorted perpetual-equity pricing, as the PE ratio of 180 and the policy-induced demand dynamics suggest it would – would produce an inflated deemed asset value, an inflated deemed gain, and an excessively high reset tax base. This would tax the entity on fictional value and benefit the incoming owner with an unjustifiably high future depreciation base. It would be economically incorrect, contrary to Section 57’s anti-abuse purpose, and a product of market distortion rather than ordinary market pricing as required by Section 2(ssha).

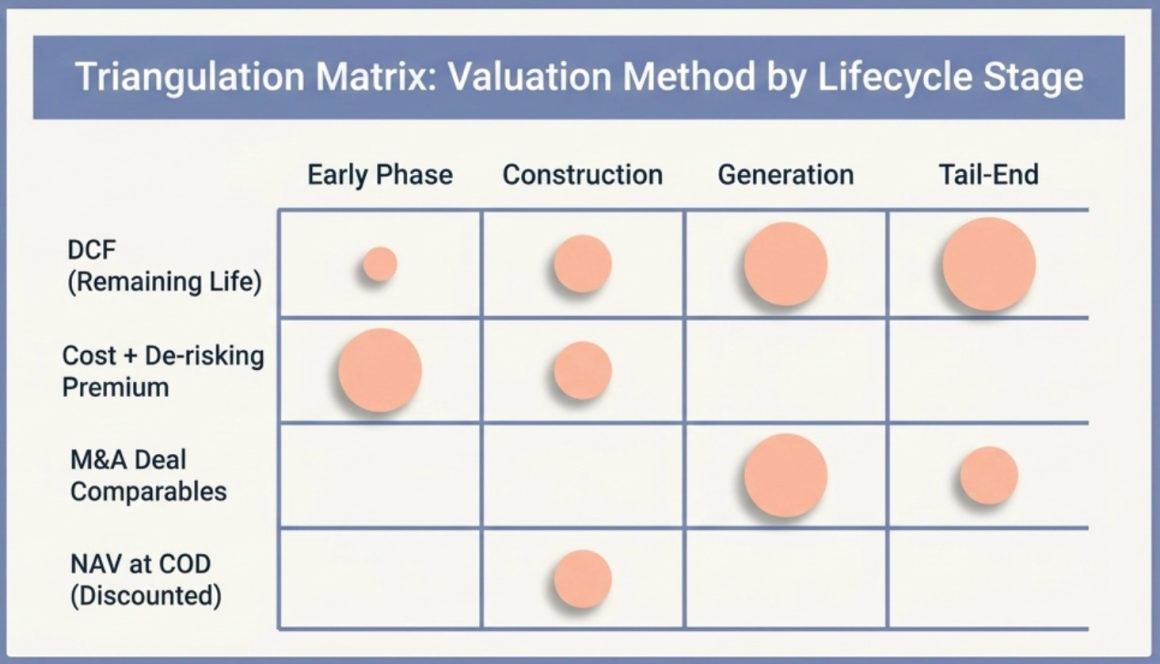

VII. Triangulation in Practice

The earning-capacity principle does not mandate a rigid single-method approach. Triangulation – using multiple methods, reconciling them, and weighting toward the most theoretically appropriate for the stage and circumstances – is consistent with the principle, and is what a rational, sophisticated buyer in an actual arm’s-length transaction would undertake. Section 2(ssha)’s “ordinary market” standard implicitly demands this rigor.

The four methods relevant in Nepal hydropower concession valuation – DCF on remaining concession life (primary), cost-to-date plus de-risking premium (floor check in early and construction stages), comparable enterprise value per MW from actual transactions (cross-check in operational stage), and NAV at COD discounted back for development risk (equity-level check in construction stage) – all, when correctly applied, produce values rooted in earning capacity. The cost approach is a proxy for earning capacity when future cash flows are too uncertain to project. Comparables drawn from actual deal data reflect what informed buyers pay for earning-capacity rights in real transactions. NAV at COD discounted back for completion risk is a DCF expressed from the equity perspective with a different entry point.

None of these methods, properly applied, deviate from the central principle. All of them produce a value that declines as the concession shortens and approaches zero at BOOT transfer. The weighting across methods should reflect the stage of the project and the quality of available data: DCF weighted most heavily where data supports it, cost approach weighted more heavily at early stages, comparables weighted where actual deal evidence exists. The resulting valuation range is the Section 57 market value – it is what the Section 2(ssha) “ordinary market” standard, operationalized for an asset that has no active secondary market in its own right, would produce.

The current state of practice – some assessors using piecemeal asset values disconnected from earning life, some reaching for distorted NEPSE share prices, some producing unsupported estimates – is not an inevitable consequence of complexity. It is a consequence of the absence of a clearly articulated principle. The principle is available. It is consistent across three separate legal and accounting frameworks: the anti-abuse intent of Section 57, the Section 2(ssha) definition of market value, and IFRIC 12’s framework for measuring concession assets. A practitioner facing a Section 57 trigger on a hydropower concession company at any stage of its lifecycle should apply this framework, document it with the rigor that a Private Ruling application under Section 76 of the ITA would demand, and resist the path of least resistance – whether that is the NEPSE closing price or the replacement cost of the dam.

CONCLUSION- SECTION 57 MUST RESPECT THE VALUATION !!

References: Income Tax Act, 2058 (Nepal), Sections 2(ssha), 14(3), 20, 41, 49, 57, 71(3), 76, 95Ka; Hydropower Development Policy, 2001, Clauses 6.5.1, 6.12.11, 6.13.1; Electricity Act, 2049, Section 22, Section 10; Electricity Regulatory Commission Act, Section 13(1)(c); Securities Issuance and Allotment Directive, 2074; People’s Hydropower Program (Operation and Management) Procedure, 2075; IFRIC 12 Service Concession Arrangements (IASB, November 2006), Paragraphs 5, 6, 11, 16, 17; IAS 38 Intangible Assets