The Nepal Rastra Bank (NRB), through Circular No. 12/081 dated 2082/12/03 (mid-March 2026), has introduced a significant amendment to Directive No. 17/081, Clause 15, sub-clause (3), establishing a formal mechanism for the purchase and sale of “Reporting Rights” pertaining to the Agriculture and Energy sectors. This mechanism permits Banks and Financial Institutions (BFIs) of Class “A,” “B,” and “C” to trade the administrative right to count specified loan amounts toward their mandatory sectoral lending ratios, without transferring the underlying credit asset, risk, or borrower relationship.

This post presents a comprehensive analysis of the Reporting Rights framework across seven dimensions: (i) the regulatory architecture and its legal basis under the NRB Act, 2058 and BAFIA, 2073; (ii) a detailed comparison with India’s Priority Sector Lending Certificates (PSLCs), which have grown to INR 8,951 billion in annual trading volume since their 2016 launch; (iii) the securitization-adjacent provisions already present within Nepal’s unified directives; (iv) a mathematical pricing model for Reporting Rights fees; (v) an assessment of whether and how these rights could be structured as tradable compliance certificates with broader institutional participation; (vi) the applicability to the insurance and pension sector under the Investment Directive, 2082; and (vii) reform recommendations for Nepal’s financial regulatory ecosystem.

The central thesis of this post is that Nepal’s Reporting Rights, while currently structured as a bilateral, short-term, fee-based repurchase arrangement between BFIs, possess the structural DNA to evolve into a more robust, platform-traded compliance certificate – analogous to India’s PSLC – if supported by targeted legal amendments to the Secured Transaction Act, 2063, the Securities Act, 2063, and the NRB Unified Directives. Such evolution would not only deepen price discovery and market efficiency but could potentially extend participation to non-banking institutional investors, including insurance companies and pension funds, who face their own sectoral investment mandates under the Insurance Act, 2079 and related directives.

Part I: Regulatory Architecture of the Reporting Rights Mechanism

The Reporting Rights mechanism derives its authority from a layered statutory and regulatory framework. At the apex, Section 79 of the Nepal Rastra Bank Act, 2058 empowers the NRB to issue binding directions to licensed BFIs regarding their operations and credit flow. Section 81 of the same Act provides the specific legal basis for monitoring sectoral targets and imposing quarterly monetary penalties on shortfalls – the very penalties that create the economic demand for Reporting Rights. Section 88 empowers the NRB to establish a Credit Information Center and regulate the flow of credit data, which underpins the reporting infrastructure.

Under this statutory authority, the NRB has codified the mechanism within Directive No. 17/081 (now referenced as Directive No. 17/082 in the latest unified updates), specifically within Clause 15, sub-clause (3). The Banking and Financial Institutions Act (BAFIA), 2073 further supports the framework through Section 49 (which grants BFIs the power to provide credit, issue guarantees, and enter consortium arrangements) and Directive No. 2, Clause 14 (which details the procedures for Credit Sale, Purchase, Repurchase, and Takeover).

The mechanism operates under the following tightly defined parameters, each designed to ensure it remains a supplementary administrative tool rather than a substitute for direct lending:

Parameter | Regulatory Specification |

Applicable Sectors | Agriculture and Energy only (Clause 15(3) of Directive 17/081 as amended) |

Eligible Institutions | Class “A,” “B,” and “C” BFIs. Class “D” MFIs are excluded. |

Purchase Limit | Maximum one-third (1/3) of the total required percentage for that specific sector |

Maximum Duration | 6 months per transaction |

Fiscal Year Rule | Must be fully concluded within the same fiscal year; no transactions in the final month (Ashad) |

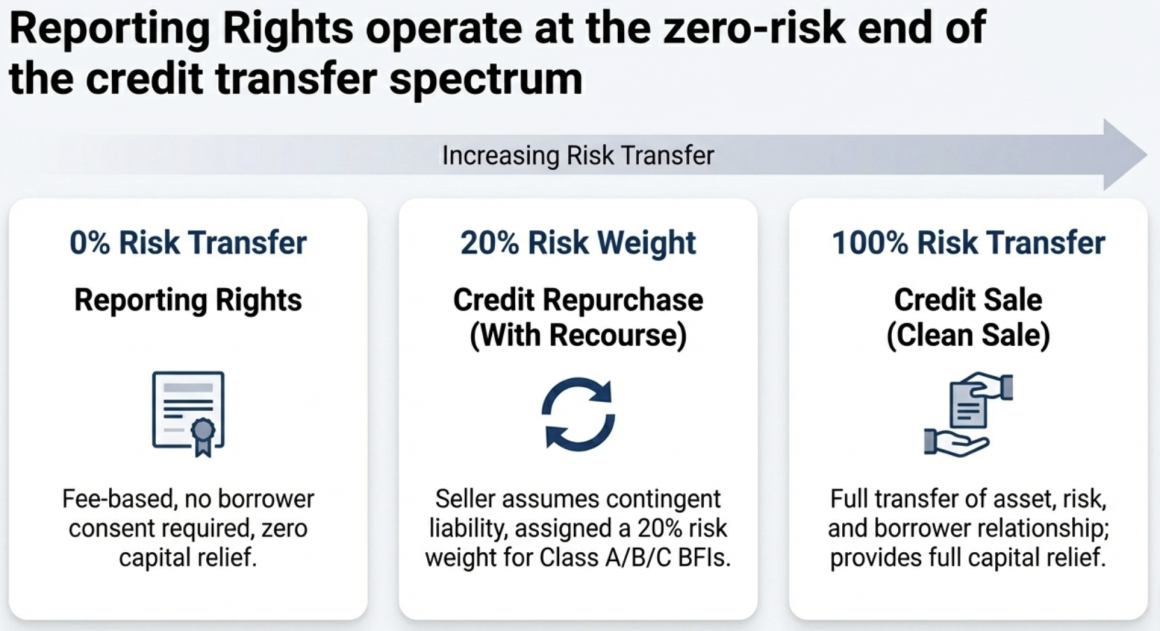

Risk Transfer | None. Risk, reward, and control remain entirely with the selling institution. |

Borrower Consent | Not required. The borrower’s legal relationship with the original lender is unchanged. |

Fee Determination | Mutual agreement (आपसी सहमति) between BFIs. No prescribed regulatory rate. |

Resale | Strictly prohibited. Once sold, the right cannot be transferred to a third institution. |

The demand side of the Reporting Rights market is driven by the mandatory lending targets imposed on each class of BFI. Under the latest amendment (Circular No. 12/081), these targets have been restructured as follows:

BFI Class | Agriculture Target | Combined Specified Sectors | Key Notes |

Class “A” Commercial Banks | Minimum 10% of total credit | Minimum 20% (Tourism, SME/MSME, Energy, ICT, Export) | Excess agriculture credit above 10% may count toward the 20% combined target |

Class “B” Development Banks | Part of combined target | Minimum 20% combined | Agriculture, Tourism, SME, Energy, ICT, Export consolidated |

Class “C” Finance Companies | Part of combined target | Minimum 15% combined | Same consolidated sectors as Class B |

Class “D” MFIs | 1/3 of total credit | N/A | Excluded from Reporting Rights mechanism |

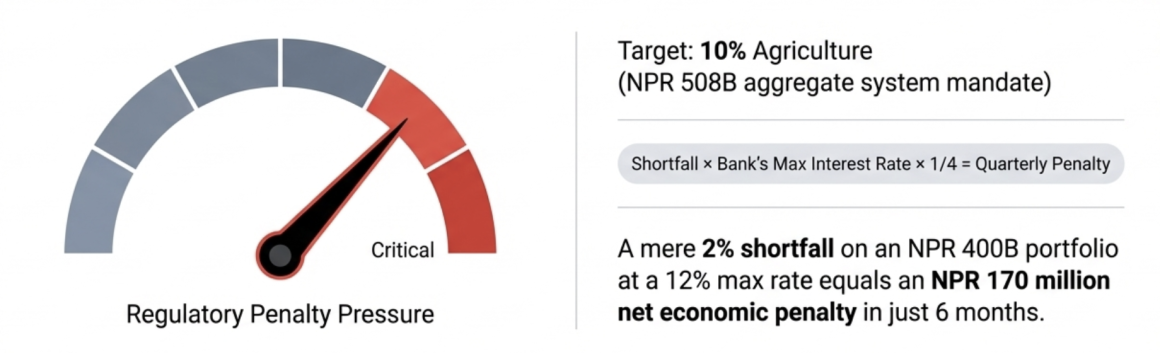

The quarterly monetary penalty under Section 81 of the NRB Act, 2058 serves as the primary economic driver for the Reporting Rights market. The penalty is calculated as follows: the NRB identifies the shortfall amount – the difference between the mandatory lending requirement and the adjusted actual lending (including any purchased Reporting Rights, capped at the 1/3 limit). The penalty is then equivalent to the interest that would have been earned on that shortfall during the quarter, calculated at the maximum interest rate charged by that specific BFI on its own loans during the assessment period.

To quantify the scale of penalty exposure, consider the actual system-wide data as of Mid-February 2026. Total Class A commercial bank lending stands at NPR 5,076 billion (~ USD 36 billion). The mandatory agriculture target of 10% implies a required agricultural credit flow of NPR 508 billion (~ USD 3.6 billion). The other 20% for the combined specified sectors comes to around USD 7.2 billion. Portfolio specific lending are available here from NRB: Monthly Statistics Data from NRB

However, the critical insight is that aggregate compliance masks individual bank shortfalls. The penalty rate is institution-specific: it uses each BFI’s own maximum interest rate. NRB data for Mid-February 2026 shows the weighted average lending rate for consumption loans – typically the highest-yield sector – stood at 7.75% for commercial banks. Individual bank maximums would be higher. For a bank with a maximum rate of, say, 12% and a 1% agriculture shortfall on a total credit portfolio of NPR 300 billion, the quarterly penalty exposure would be: NPR 3 billion × 12% × 0.25 = NPR 90 crore per quarter, or NPR 360 crore annualized. This penalty quantum – running into hundreds of crores for a single percentage point of shortfall at a mid-sized bank – is what creates the fundamental economic demand for Reporting Rights.

Part II: Market Structure and Interest Rate Structure

As of mid-October 2025, Nepal’s financial system comprises 20 Class “A” commercial banks operating nationwide, 17 Class “B” development banks (of which 8 are national-level, 6 provincial, and 3 district-level), 17 Class “C” finance companies, 52 Class “D” microfinance institutions, and 1 infrastructure development bank (NIFRA) – totaling 107 licensed BFIs. This structure reveals a highly segmented market in which the supply and demand dynamics for Reporting Rights will differ markedly across classes.

The latest NRB data (Mid-February 2026) provides a comprehensive picture of the sectoral credit distribution across all three eligible BFI classes. The following table presents the aggregate sector-wise lending positions:

Sector | All A+B+C (NPR Mn) | Class A (NPR Mn) | Class B (NPR Mn) | Class C (NPR Mn) |

Agricultural & Forest Related | 353,545 | 312,049 | 33,895 | 7,601 |

Fishery Related | 15,822 | 13,883 | 1,520 | 418 |

Mining Related | 12,025 | 11,680 | 242 | 103 |

Agri, Forestry, Beverage & Non-Food Prod. | 969,050 | 932,630 | 31,645 | 4,774 |

Construction | 251,449 | 221,729 | 26,382 | 3,338 |

Electricity, Gas and Water | 472,664 | 463,005 | 9,100 | 559 |

Wholesaler & Retailer | 1,039,827 | 955,654 | 69,727 | 14,446 |

Finance, Insurance & Real Estate | 432,566 | 360,934 | 59,430 | 12,203 |

Tourism Service | 266,019 | 225,660 | 35,037 | 5,323 |

Consumption Loans | 1,274,374 | 1,076,767 | 164,380 | 33,227 |

Others (incl. Services, Local Govt, etc.) | 707,676 | 583,525 | 101,690 | 22,461 |

TOTAL (NPR Million) | 5,795,567 | 5,157,515 | 533,047 | 105,004 |

TOTAL (USD Billion) | 41.40 | 36.84 | 3.81 | 0.75 |

Interest Rate Structure: Commercial Banks (Mid-July 2025 to Mid-February 2026): The NRB’s weighted average interest rate data for Class A commercial banks reveals a consistent downward trend across all sectors over the eight-month period from Ashar 2082 (Mid-July 2025) to Magh 2082 (Mid-February 2026). The following summary captures the latest rates as of Mid-February 2026, which are directly relevant to both the penalty calculation (the maximum rate) and the yield differential analysis for pricing Reporting Rights:

Note: The weighted average interest rate data presented in this section only includes Class A commercial banks from NRB publications.

Sector | Wt. Avg. Rate Mid-Jul 2025 | Wt. Avg. Rate Mid-Feb 2026 | Change (bps) | Outstanding (NPR Mn) |

Agricultural & Forest Related | 7.37% | 6.16% | -121 | 308,436 |

Fishery Related | 7.22% | 6.40% | -82 | 13,883 |

Agri, Forestry & Beverage Prod. | 7.49% | 6.59% | -90 | 287,869 |

Electricity, Gas and Water | 7.61% | 6.81% | -80 | 462,343 |

Consumption Loans | 8.61% | 7.75% | -86 | 1,076,643 |

Construction | 8.20% | 7.15% | -105 | 221,268 |

Others (highest-rate category) | 8.78% | 6.78% | -200 | 226,607 |

AGGREGATE (All Sectors) | 7.85% | 7.00% | -85 | 5,076,881 |

Two critical observations emerge from this data. First, the yield differential between the highest-yield sector (consumption loans at 7.75%) and agriculture lending (6.16%) is 159 basis points as of Mid-February 2026 – down from 124 bps in Mid-July 2025. This spread represents the opportunity cost component for a bank maintaining excess agricultural lending instead of redeploying that capital into consumption lending. Second, the energy sector at 6.81% sits between agriculture and the aggregate, with a 94 bps spread to consumption. These yield differentials form the foundation of the seller’s floor in the pricing model developed in Part IV.

Part III: Mathematical Pricing Framework for Reporting Rights (Revised)

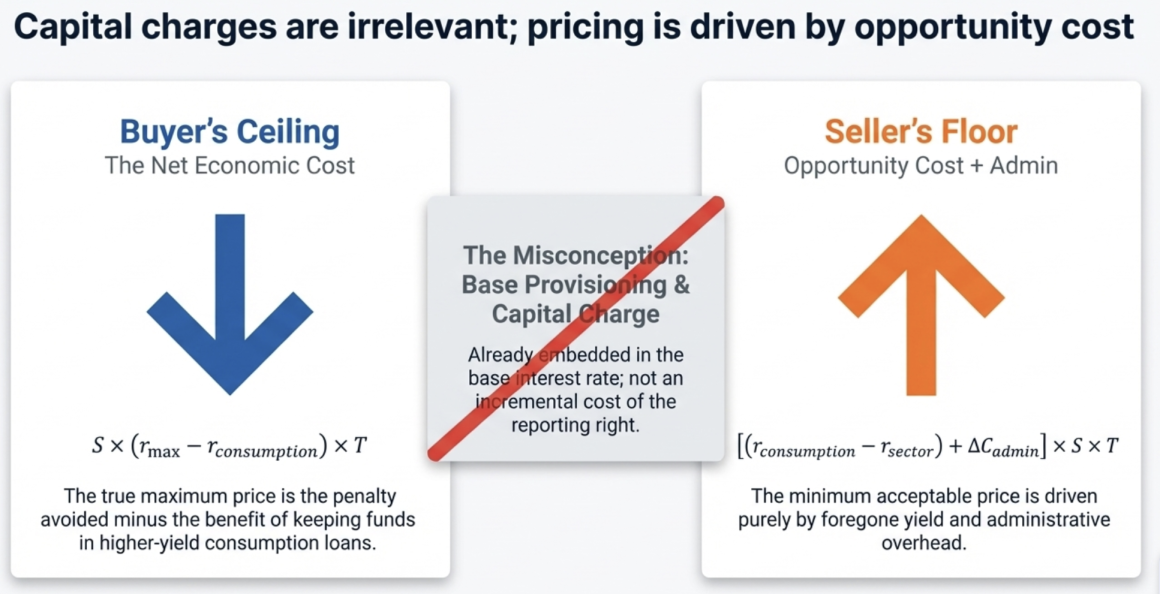

The price of a Reporting Right is bounded by two regulatory-economic forces: (a) the penalty for non-compliance, which establishes the buyer’s maximum willingness to pay; and (b) the opportunity cost of maintaining excess sectoral lending, which establishes the seller’s minimum acceptable price. The fee is determined through bilateral negotiation within these bounds, as prescribed by the directive’s mutual agreement provision.

Definition of Variables

S = Shortfall Amount (the volume of reporting rights sought, in NPR)

r_max = Maximum interest rate charged by the purchasing BFI during the quarter (the penalty rate)

r_consumption = Weighted average yield on consumption loans (highest-yield sector benchmark)

r_agri = Weighted average yield on agricultural lending

r_energy = Weighted average yield on energy sector lending

T = Duration of the Reporting Rights arrangement (in years; maximum 0.5)

ΔC_admin = Incremental administrative cost of maintaining agricultural/energy lending vs. commercial lending

P_rr = Price (fee) for the Reporting Right per unit of shortfall

3.1. Buyer’s Maximum Price (Penalty Ceiling)

The buyer will not pay more than the penalty it avoids. The quarterly penalty under Section 81 of the NRB Act, 2058 is:

Penalty_quarterly = S × r_max × (1/4)

For a 6-month arrangement covering two quarters, the buyer’s ceiling is:

P_rr(max) = S × r_max × T

However, from a strict economic perspective, the buyer’s maximum willingness to pay is the net cost of non-compliance: the penalty avoided minus the economic benefit retained from deploying funds in higher-yield sectors. Since a non-compliant bank continues to earn returns from alternative lending (proxied by r_consumption), the effective ceiling is reduced accordingly. Thus, the economically adjusted ceiling is: P_rr(max) = S × (r_max − r_consumption) × T

Numerical Example:

A Class A bank with total credit of NPR 400 billion, a 10% agriculture target, and a 2% shortfall. The bank’s maximum lending rate during the quarter is 12%.

Shortfall: S = 2% × NPR 400B = NPR 8 billion

Buyer’s Ceiling (6 months):

P_rr(max) = NPR 8B × (12% − 7.75%) × 0.5

= NPR 8B × 4.25% × 0.5

= NPR 170 million

Expressed as a percentage of the notional shortfall: 170 / 8,000 = 2.13% for 6 months, or 4.25% annualized

This represents the true economic maximum – the net cost the bank would incur if it chose non-compliance while continuing to deploy funds in higher-yield sectors.

3.2. Seller’s Minimum Price (Opportunity Cost Floor): A Critical Decomposition

A precise construction of the seller’s floor requires distinguishing between costs that are genuinely sector-specific and those that are sector-agnostic. The seller is a BFI that has excess agricultural or energy lending – lending that already exists on its balance sheet and that it could, in theory, have deployed in higher-yielding sectors.

Why Capital Charge and Base Provisioning Do Not Enter the Floor: A common analytical error is to include the cost of capital (risk weight × CAR × cost of equity) and base loan loss provisioning (the 1.2% general provision for “Pass” loans under Directive No. 2) as components of the seller’s floor. This is incorrect for the following reason: these costs are identical regardless of the sector to which the loan is deployed. A NPR 100 million agriculture loan at 100% risk weight and a NPR 100 million consumption loan at 100% risk weight both require the same regulatory capital (11% × 100% = NPR 11 million) and the same base provision (1.2% = NPR 1.2 million). The capital charge, credit risk premium, time value of capital, and base provisioning are all already embedded in the interest rate that the bank charges on each loan. The difference in interest rates across sectors therefore already captures the net impact of all these components.

What Actually Constitutes the Seller’s Floor: The seller’s floor has exactly two components:

(a) Yield Differential (Opportunity Cost): This is the foregone income from maintaining capital in agriculture/energy rather than redeploying it into the highest-yield alternative. Using Mid-February 2026 NRB data for Class A commercial banks:

Agriculture yield differential = r_consumption − r_agri = 7.75% − 6.16% = 1.59%

Energy yield differential = r_consumption − r_energy = 7.75% − 6.81% = 0.94%

This spread is the economic cost the seller bears by keeping its money in agriculture/energy loans rather than in consumption lending. It already incorporates all differences in credit risk premia, capital costs, and provisioning between the sectors because these are priced into the respective lending rates.

(b) Incremental Administrative and Compliance Cost (ΔC_admin): Agricultural lending requires specialized costs that commercial or consumption lending does not: field visits to farms, agricultural valuation expertise, seasonal monitoring, weather-related restructuring assessments, and the compliance overhead of NRB’s sectoral reporting requirements (Form No. 17.1). The incremental cost – the excess of these agricultural administration costs over the administration cost of standard commercial lending – is estimated at 0.15–0.40% per annum based on the higher operational intensity of rural agricultural credit delivery versus urban consumption lending.

A precise construction of the seller’s floor requires distinguishing between costs that are genuinely sector-specific and those that are sector-agnostic. The seller is a BFI that has excess agricultural or energy lending – lending that already exists on its balance sheet and that it could, in theory, have deployed in higher-yielding sectors.

Why Capital Charge and Base Provisioning Do Not Enter the Floor: A common analytical error is to include the cost of capital (risk weight × CAR × cost of equity) and base loan loss provisioning (the 1.2% general provision for “Pass” loans under Directive No. 2) as components of the seller’s floor. This is incorrect for the following reason: these costs are identical regardless of the sector to which the loan is deployed. A NPR 100 million agriculture loan at 100% risk weight and a NPR 100 million consumption loan at 100% risk weight both require the same regulatory capital (11% × 100% = NPR 11 million) and the same base provision (1.2% = NPR 1.2 million). The capital charge, credit risk premium, time value of capital, and base provisioning are all already embedded in the interest rate that the bank charges on each loan. The difference in interest rates across sectors therefore already captures the net impact of all these components.

What Actually Constitutes the Seller’s Floor: The seller’s floor has exactly two components:

(a) Yield Differential (Opportunity Cost): This is the foregone income from maintaining capital in agriculture/energy rather than redeploying it into the highest-yield alternative. Using Mid-February 2026 NRB data for Class A commercial banks:

Agriculture yield differential = r_consumption − r_agri = 7.75% − 6.16% = 1.59%

Energy yield differential = r_consumption − r_energy = 7.75% − 6.81% = 0.94%

This spread is the economic cost the seller bears by keeping its money in agriculture/energy loans rather than in consumption lending. It already incorporates all differences in credit risk premia, capital costs, and provisioning between the sectors because these are priced into the respective lending rates.

(b) Incremental Administrative and Compliance Cost (ΔC_admin): Agricultural lending requires specialized costs that commercial or consumption lending does not: field visits to farms, agricultural valuation expertise, seasonal monitoring, weather-related restructuring assessments, and the compliance overhead of NRB’s sectoral reporting requirements (Form No. 17.1). The incremental cost – the excess of these agricultural administration costs over the administration cost of standard commercial lending – is estimated at 0.15–0.40% per annum based on the higher operational intensity of rural agricultural credit delivery versus urban consumption lending.

The Seller’s Floor Function:

P_rr(min) = [(r_consumption − r_sector) + ΔC_admin] × S × T

Where r_sector is the applicable yield for the sector whose reporting right is being sold (agriculture or energy).

Numerical Example (Agriculture, 6 months):

Seller’s Floor = [1.59% + 0.25%] × NPR 8B × 0.5 = NPR 73.6 million

Expressed as a percentage of notional: 73.6/8,000 = 0.92% for 6 months, or 1.84% annualized

Numerical Example (Energy, 6 months):

Seller’s Floor = [0.94% + 0.20%] × NPR 8B × 0.5 = NPR 45.6 million

Expressed as a percentage of notional: 45.6/8,000 = 0.57% for 6 months, or 1.14% annualized

3.3 Indicative Pricing Matrix (Annualized, as % of Notional)

Component | Agri (Low) | Agri (High) | Energy (Low) | Energy (High) |

Yield Differential | 1.59% | 1.59% | 0.94% | 0.94% |

Incremental Admin Cost | 0.15% | 0.40% | 0.15% | 0.35% |

Seller’s Floor (annualized) | 1.74% | 1.99% | 1.09% | 1.29% |

Buyer’s Ceiling (Adjusted) | 4.25% | 4.25% | 4.25% | 4.25% |

Expected Negotiated Range | 2.0–3.5% | 2.5–4.0% | 1.5–2.5% | 2.0–3.0% |

The compression of the buyer’s ceiling from the full penalty rate (~10–12%) to the net economic cost of non-compliance (~4.25%) significantly narrows the feasible pricing band. The gap between the seller’s floor (~1.1–2.0% annualized) and the adjusted buyer’s ceiling (~4.25%) implies a more efficient and economically grounded negotiation range. In early stages, regulatory considerations may still anchor pricing above pure economic levels; however, as market depth grows and competitive dynamics among sellers intensify, prices are likely to converge toward 2.0–3.5% for agriculture and 1.5–2.5% for energy – consistent with India’s PSLC experience of 1–3%.

Part IV: International Comparison - India’s PSLC Framework

4.1 Overview of India’s Priority Sector Lending Certificates

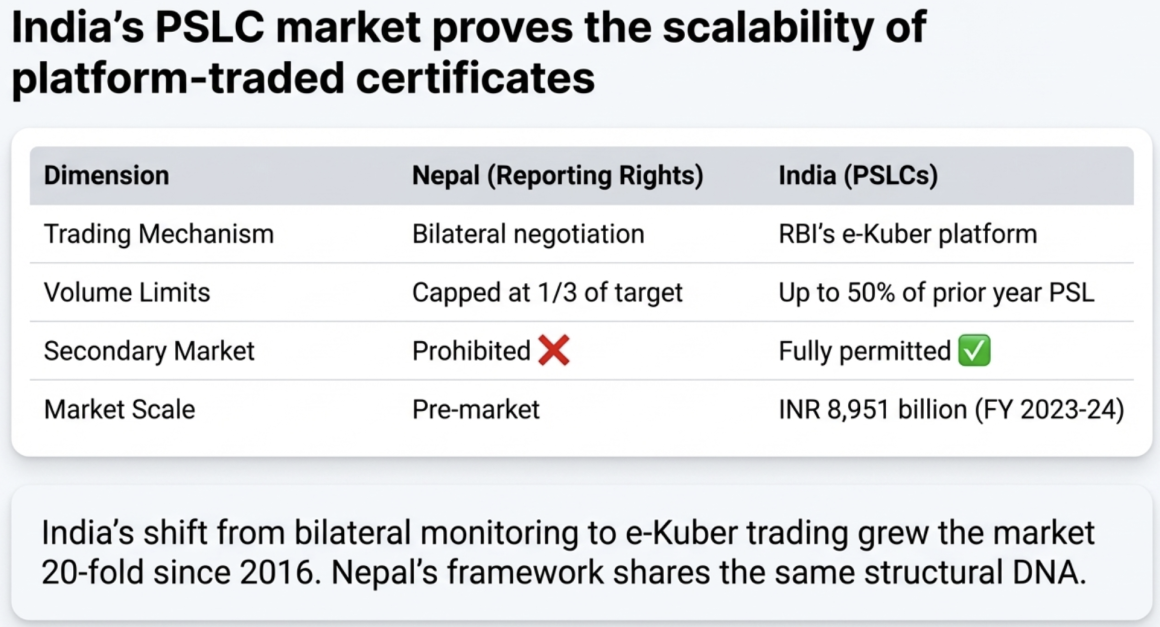

India’s Reserve Bank of India (RBI) launched Priority Sector Lending Certificates (PSLCs) on April 7, 2016, following the recommendation of the High-Level Committee on Financial Sector Reforms (Raghuram Rajan Committee, September 2008). PSLCs are non-tangible tradable certificates representing the achievement of a specific amount of lending to eligible priority sectors. The mechanism operates on the RBI’s e-Kuber electronic platform with four categories: PSLC-Agriculture, PSLC-Small & Marginal Farmers, PSLC-Micro Enterprises, and PSLC-General. All Scheduled Commercial Banks, Regional Rural Banks, Local Area Banks, and Small Finance Banks can participate.

In FY 2016–17 (the inaugural year), total trading volume reached INR 430 billion. By FY 2023–24, this had grown to INR 8,951 billion – a 20-fold increase – demonstrating the market’s scalability. Premiums initially ranged from 3–5% in the first quarter of FY 2016–17, with India Ratings expecting settlement between 1–3% depending on the sub-segment deficit.

4.2 Structural Comparison

Feature | Nepal Reporting Rights | India PSLCs |

Launch Date | 2082/12/03 (March 2026) | April 7, 2016 |

Legal Structure | Fee-based Repurchase Arrangement under mutual agreement | Tradable certificate on electronic platform (e-Kuber) |

Trading Platform | None; bilateral negotiation | RBI’s e-Kuber (CBS portal); standard lot INR 25 lakh |

Sectors | Agriculture and Energy only | Agriculture, SF/MF, Micro Enterprises, General |

Purchase Cap | 1/3 of mandatory target % | No % cap; up to 50% of prior year PSL without underlying |

Duration | Maximum 6 months | Expires March 31 (fiscal year-end) |

Risk Transfer | None | None |

Resale/Secondary Trading | Prohibited | Permitted on platform |

Non-Compliance | Interest-rate-based quarterly penalty (Sec. 81 NRB Act) | Deposit in RIDF/SIDBI at below-market rates |

Tax Treatment | Fee income taxable; TDS applicable | 12% GST (Circular 62/36/2018); treated as goods |

Annual Trading Volume | Pre-market (no transactions yet) | INR 8,951 billion (FY 2023-24) |

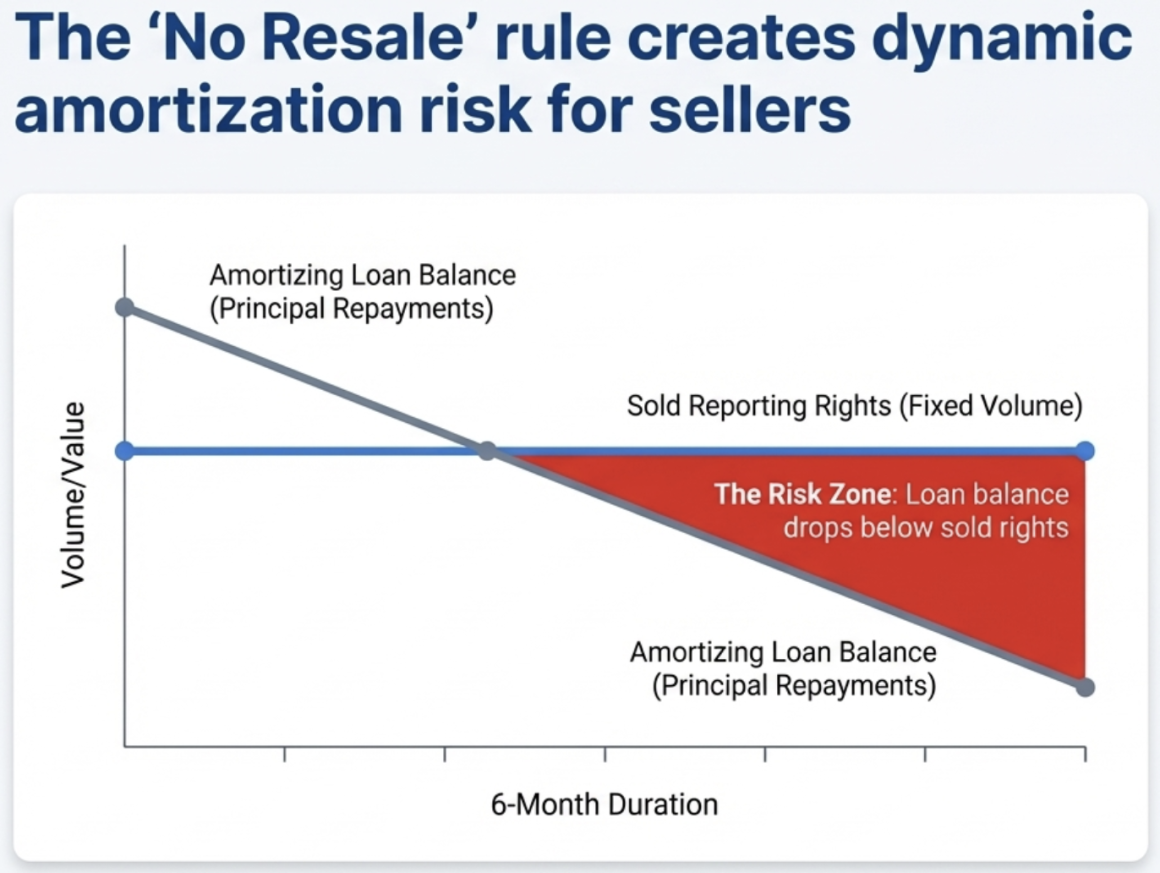

4.3 The Amortization Tracking Problem

A critical operational question that arises in both the Indian PSLC framework and Nepal’s Reporting Rights mechanism is: as the borrower services the underlying debt through principal repayments, the outstanding loan balance declines – how does the holder of the certificate (or reporting right) track and report this diminishing balance?

Under India’s PSLC framework, the certificate is issued against the aggregate priority sector lending portfolio, not against specific individual loans. A bank’s PSL achievement is computed as the sum of its outstanding priority sector loans plus the net PSLCs purchased, assessed as of the reporting date. If underlying loans amortize, the bank must maintain sufficient outstanding PSL loans (or purchase fresh PSLCs) to cover its target on the reporting date. The certificate itself has no dynamic linkage to specific loan balances.

In Nepal’s Reporting Rights structure, the mechanism is similarly portfolio-based rather than loan-specific. The directive requires the purchased amount to be shown as an addition to the purchaser’s sectoral count and a deduction from the seller’s count via Form 17.1. As borrowers amortize their loans during the 6-month arrangement period, the selling institution’s total sectoral portfolio naturally declines. If the seller’s excess shrinks below the volume of sold reporting rights, the seller may find itself in regulatory non-compliance with its own targets. This creates a dynamic risk for the seller, who must monitor its sectoral portfolio throughout the arrangement period and ensure that the loans underlying the sold rights remain outstanding and performing. The NRB’s resale prohibition further constrains the system: if the sold rights can no longer be supported by the seller’s actual portfolio, the arrangement cannot be unwound mid-term through a secondary sale.

This amortization risk is a structural argument for the reform proposal in Part VIII: a centralized registry at the STRO with real-time loan-level data would allow both parties and the regulator to track the dynamic balance of the underlying loans, ensuring that the reporting right is always backed by sufficient performing credit.

4.4 Bangladesh and Pakistan: Absence of Comparable Mechanisms

Neither Bangladesh nor Pakistan has introduced a tradable compliance certificate mechanism comparable to India’s PSLCs or Nepal’s Reporting Rights. Bangladesh Bank sets annual agricultural credit disbursement targets under the Agricultural & Rural Credit Policy and Programme, with compliance managed through direct monitoring and refinance facilities rather than inter-bank trading. Pakistan’s State Bank allocates regional agricultural targets under the ACAC framework, with enforcement through monitoring and, more recently, digital platforms such as Zarkhez-e with government-backed first-loss guarantees. Nepal’s mechanism is thus a regional innovation – second only to India in the SAARC region.

Part V: Securitization and Related Provisions in NRB Directives

5.1 Credit Sale, Purchase, Repurchase, and Takeover (Directive No. 2, Clause 14)

The NRB Unified Directives provide a framework for the actual transfer of loan assets between financial institutions, which is structurally distinct from Reporting Rights but forms the broader ecosystem of credit management. Both with-recourse and without-recourse arrangements are permitted, though they receive different regulatory treatment.

Credit Sale Without Recourse: A straightforward sale where the selling institution transfers the loan asset and its associated credit risk to the purchasing institution. The purchaser assumes the right to recover the loan directly from the customer, and the loan is moved from the seller’s balance sheet to the purchaser’s balance sheet under the relevant loan sub-head. The purchaser can count the acquired loan toward its mandatory sectoral lending targets.

Credit Repurchase (With Recourse): In this arrangement, the seller agrees to buy back the loan if the purchaser is unable to recover it from the borrower. The directive defines this as a condition where the selling institution has an obligation to repurchase the loan itself. The seller must record the amount as a Contingent Liability in its financial statements until the repurchase occurs or the loan is fully recovered. Risk Weights for the Seller: For Class A, B, and C banks, the resulting Contingent Liability is assigned a 20% risk weight for capital adequacy calculation. For NIFRA (Infrastructure Development Bank), the risk weight is significantly higher at 100%, and NIFRA is additionally subject to a 1% capital charge on the sale value for credit sold with recourse.

Key Requirements for Credit Transfer

- Borrower Consent: Unlike Reporting Rights, the actual movement of loan assets via sale or repurchase requires the explicit consent of the borrower, as the purchaser must obtain the legal right to recover the debt directly from the customer.

- Capital Adequacy Threshold: BFIs may only engage in credit sales, purchases, or repurchases if they maintain the minimum capital fund required by NRB.

- Timeframe Restriction: Identical to Reporting Rights, BFIs are prohibited from performing these transactions during the final month of the fiscal year (Ashad).

- Due Diligence: The purchasing institution must obtain a detailed history of the loan, including classification status, repayment history, and any findings from external auditors or NRB inspections.

- Relationship Management: Even if a loan is sold, the originating bank can retain the customer relationship management by mutual agreement.

5.2 Securitization under Special Administration (Section 88G(13), NRB Act, 2058)

The provision under Section 88G(13) of the NRB Act, 2058 provides a legal framework for the resolution of distressed BFIs through securitization and asset pooling. This authority is vested in a Special Administration Group (SAG) appointed by the NRB to take control of a BFI deemed to be in a state of resolution (Farfarak).

Mandate for Asset Pooling and Securitization: The SAG is granted explicit authority to: (a) pool assets specifically for the purpose of securitization; (b) issue new shares or other financial instruments to raise capital or restructure debt; and (c) make forward-looking estimates and arrangements for the BFI’s liabilities as part of the pooling process.

Assignment to Asset Management Companies: The SAG can delegate the management of pooled assets to specialized Asset Management Companies (AMCs) established under prevailing laws. The law specifically allows the transfer of Non-Performing Loans (NPLs) and assets that are “difficult to value” to these AMCs, effectively cleansing the BFI’s balance sheet by moving toxic assets into a specialized recovery vehicle.

The Non-Consent Clause: Under Section 88G(4), the SAG can perform asset pooling and securitization without requiring the prior consent of: shareholders, depositors, creditors, or any other public or private entity. The SAG assumes all powers of the General Meeting, the Board of Directors, and the CEO. Actions taken by the SAG in good faith are protected from personal liability. This establishes a unique legal precedent in Nepal for mandatory asset pooling to protect the stability of the financial system.

5.3 Significant Risk Transfer for Capital Relief (Capital Adequacy Framework, Basel III)

For securitization or credit sale arrangements to qualify for capital relief, the NRB must deem the risk transfer “significant.” If the transfer is insufficient, capital relief is denied and higher requirements may be imposed. Since Reporting Rights involve zero risk transfer, they provide no capital relief – but this framework provides the regulatory template for assessing any future structured products.

5.4 Special Purpose Vehicles (Directive No. 8, Clause 3(d) for NIFRA)

Authorization to Establish SPVs: Infrastructure Development Banks are explicitly permitted to establish and invest in sector-specific SPVs for: (a) identifying potential infrastructure projects and performing technical and financial analysis; (b) conducting feasibility studies and preparing cost estimations; and (c) ring-fencing risks associated with specific types of projects (energy, transport, urban infrastructure).

Prohibition on Credit to SPV-Operated Projects: The bank is strictly prohibited from providing loans or credit facilities to any project operated through an SPV in which the bank itself holds an investment. This restriction remains in effect for the duration of the bank’s equity holding in the SPV. The intent is to prevent circular exposure – where a bank could essentially fund its own equity risk by lending to its own vehicle, leading to artificial inflation of assets and hidden leverage.

AT1 Capital Instruments: All Additional Tier 1 instruments (Perpetual Non-Cumulative Preference Shares and Perpetual Debt Instruments) must be issued directly by the bank itself. These instruments cannot be issued through an SPV or any third-party vehicle, ensuring investors have a clear and direct claim on the bank’s capital for loss-absorption purposes under the Basel III framework.

Capital Adequacy and Governance: Investment in an SPV’s equity must generally be deducted from the bank’s Common Equity Tier 1 (CET1) capital. If not deducted, it attracts a risk weight of typically 150%. The Chairperson and members of the bank’s Board of Directors are prohibited from serving on the board of the subsidiary/SPV company, ensuring governance independence.

5.5 Deprived Sector Wholesale Lending

Class A, B, and C banks can meet their 5% deprived sector target by providing wholesale credit to Class D MFIs. This mechanism – where the larger bank “reports” the lending toward its regulatory target while the MFI manages the customer relationship – is the conceptual predecessor of the fee-based Reporting Right.

5.6 Agriculture and Energy Bonds

Commercial banks are permitted to issue Agriculture Bonds and Energy Bonds to raise long-term resources, functioning as a form of sector-specific capital mobilization that could, in theory, interface with a Reporting Rights securitization structure.

Part VI: Insurance and Pension Fund Applicability

6.1 Current Investment Mandates Under the Investment Directive, 2082

Life Insurance: Minimum 35% in Nepal Government/NRB Securities; minimum 30% in Fixed Deposits of Class A banks or Infrastructure Development Banks. Priority sectors (agriculture, hydropower, solar, roads, electricity transmission) are permitted under Category 10 but subject to a maximum cap of 10% of total investment – not a mandatory minimum.

Non-Life Insurance: Minimum 30% in government securities; minimum 30% in fixed deposits. Same 10% maximum for priority sector investments.

BFI Bonds: Insurers can invest up to 30% (life) or 20% (non-life) of total investment in bonds, debentures, and loans of Class A, B, and C BFIs, with a single-issuer cap of 10% of the issuing company’s paid-up capital.

6.2 Barriers to Insurance Sector Participation

(a) Authorized Investment List: The Investment Directive restricts insurers to specifically listed asset classes. Fee-based contractual rights and administrative receivables from BFIs are not among the authorized categories.

(b) No Repurchase Arrangement Provision: There is no specific regulatory provision permitting insurance companies to enter into repurchase arrangements or fee-based administrative agreements with BFIs.

(c) Substance Over Form Recognition: The Risk Based Capital (RBC) and Solvency Directive applies a “substance over form” principle (Section 35) and a “look-through approach” for indirect exposures. While the regulator assesses economic substance for risk calculation, the primary investment mandates remain structured around holding actual assets.

(d) Lack of Synthetic Exposure Recognition: The Insurance Authority recognizes economic exposure for RBC purposes but does not currently accept “synthetic” or administrative exposure for meeting primary investment mandates. A compliance certificate giving insurers “synthetic” agricultural exposure would not count toward the 10% sectoral cap – and even if it did, insurers have a cap, not a mandate.

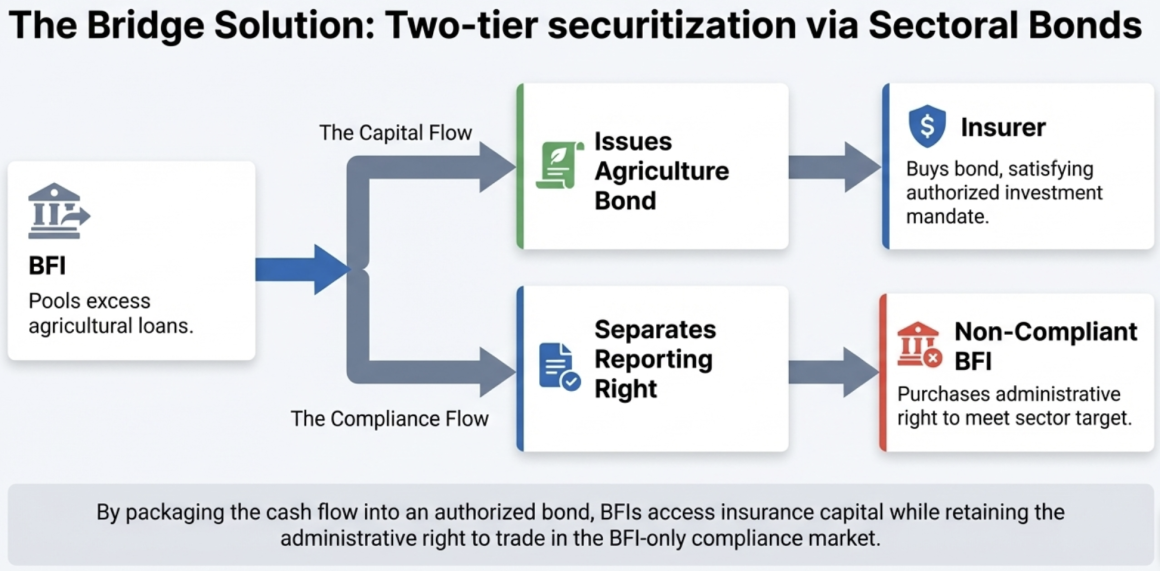

6.3 Potential Pathway: Agricultural Bonds as the Bridge Instrument

The most viable pathway for insurance sector participation lies not in direct Reporting Rights trading but in a two-tier securitization structure: BFIs with excess agricultural/energy lending issue Agriculture Bonds or Energy Bonds (already authorized under NRB directives) backed by their surplus sectoral loan portfolios. Insurance companies, which are already permitted to invest in BFI bonds (up to 30% for life insurers), would purchase these bonds as part of their authorized investment portfolio. The bond proceeds provide the selling BFI with fee-like revenue and fresh lending capital, while the Reporting Rights attached to the underlying loans are traded separately among BFIs. The borrower information and loan-level detail would be maintained at the Secured Transaction Registry Office (STRO), providing transparency into the dynamic pool backing the bonds.

Part VII: Could we do a TCC?

8.1 Vision: From Bilateral Arrangement to Platform-Traded Certificate

(a) Electronic Trading Platform: Hosted on the NRB’s existing Supervisory Information System (SIS) or a dedicated module thereof, with real-time matching of sellers and buyers. India’s e-Kuber experience demonstrates that platform-based trading dramatically improves price discovery. Standard lot sizes (suggested: NPR 1 crore) would facilitate liquidity.

(b) STRO Registry Integration: Each TCC would be registered at the Secured Transaction Registry Office with a unique identifier linked to the underlying loan pool data – borrower sector classification, outstanding balance, risk classification, and remaining tenure. The Secured Transaction Act, 2063 already contemplates intangible property and future receivables. An amendment to include “administrative regulatory compliance rights” would provide legal certainty.

(c) Sector-Specific Categories: TCC-Agriculture, TCC-Energy, and TCC-General (for the combined specified sectors target).

(d) Relaxation of the Resale Prohibition: Replace with registry-tracked secondary market. STRO registration prevents double-counting while enabling price discovery and liquidity.

(e) Extension to Non-Banking Institutional Investors: Phased authorization for insurance companies and pension funds to purchase TCCs (or TCC-backed bonds) as admissible investments, requiring amendments to the Investment Directive, 2082 and coordination between NRB, Nepal Insurance Authority, and SEBON.

8.2 Required Legal Reforms for TCC

Legislation/Directive | Required Amendment | Purpose |

Secured Transaction Act, 2063 | Add “Regulatory Compliance Rights” to registerable intangible property | Enable STRO registration of TCCs, providing third-party notice and preventing double-counting. |

NRB Directive No. 17/081, Clause 15(3) | Remove resale prohibition; add platform-trading provisions | Enable secondary market trading while maintaining registry safeguards |

Securities Act, 2063 / SEBON Regulations | Define TCCs as a new class of tradable instrument | Legal clarity for issuance, trading, and settlement |

Investment Directive, 2082 (NIA) | Add TCCs or TCC-backed bonds as authorized investment category | Enable insurance company participation in the compliance market |

NRB Unified Directives (Capital Adequacy) | Define risk weight and exposure treatment for TCC holdings | Ensure prudential treatment consistent with zero-risk-transfer nature |

Nepal’s introduction of Reporting Rights through the amendment of Directive No. 17/081 (Circular No. 12/081 dated 2082/12/03) represents a significant step in the evolution of Nepal’s financial regulatory architecture – from rigid, penalty-driven compliance to a more flexible, market-based approach to priority sector lending management. The mechanism’s core innovation lies in its separation of the “administrative benefit” (the right to report toward regulatory targets) from the “credit substance” (the risk, reward, and control of the underlying loan), creating a new category of tradable regulatory right. India’s decade-long experience with Priority Sector Lending Certificates provides a compelling case study for Nepal’s next steps. The growth from INR 430 billion in trading volume in FY 2016–17 to INR 8,951 billion in FY 2023–24 demonstrates the scalability of platform-traded compliance certificates.

The pricing analysis demonstrates that Nepal’s Reporting Rights should trade at an estimated 2.0–4.5% annualized premium for agriculture and 1.5–3.5% for energy, anchored by the penalty ceiling (the BFI’s maximum interest rate, applied under Section 81 of the NRB Act, 2058) and the seller’s opportunity cost floor (driven by the yield differential between sectoral lending and consumption lending, plus incremental administrative costs). As market depth increases and platform trading is introduced, this range will compress toward the Indian experience of 1–3%.

The broader vision – the evolution toward a Tradable Compliance Certificate with STRO registry integration, platform-based trading, and phased extension to insurance companies and pension funds – leverages Nepal’s existing legal infrastructure while addressing the structural limitations of the current bilateral framework. The regulatory architecture for this evolution already exists in embryonic form. What is needed is the regulatory will to connect these existing provisions into a coherent, market-enhancing framework – one that transforms Reporting Rights from a bilateral administrative convenience into a tradeable instrument of Nepal’s priority sector financing ecosystem.