Read my other post which describes the problem – Nepal’s doomed BOOT Model Hydro SPVs. This one is more focused on possible solutions.

History of Independent Power Producers in Nepal’s Hydropower Development

1. Early foundations and the era of state monopoly (1911–1990)

Nepal’s hydropower journey began in 1911 (1967 BS) with the commissioning of the 500 kW Pharping Hydroelectric Plant, also known as Chandra Jyoti (named after PM Chandra Shamsher). Despite this early start, progress over the subsequent decades remained slow and uneven. Hydropower development was entirely state led, shaped by limited fiscal capacity, weak institutional depth, and the absence of a private investment framework. Until 1990, the sector functioned as a government monopoly, with no meaningful role for private capital, domestic or foreign. By the end of this period, Nepal’s vast hydropower potential remained largely untapped, constrained by the state’s inability to mobilize the scale of capital required for large infrastructure development.

2. Liberalization and the legal opening of the sector (1992 onwards)

The restoration of democracy in 1990 marked a structural break in Nepal’s economic governance, including in the energy sector. Recognizing that public resources alone were insufficient to develop hydropower at scale, the government adopted an open and liberal policy framework aimed at attracting private investment.

This shift was formalized through the Hydropower Development Policy, 1992 (2049 BS), which opened electricity generation to private developers, both domestic and foreign, and allowed them to sell power commercially. The Electricity Act, 1992 (2049 BS) provided the legal foundation for this transformation, establishing licensing procedures, defining the rights and obligations of developers, and formally enabling private sector participation in generation and transmission. Institutional responsibility for implementation rested with the Department of Electricity Development, which was tasked with assisting the ministry, issuing licenses, and providing one window services to private developers.

Together, these reforms dismantled the state monopoly and laid the groundwork for the emergence of Independent Power Producers as a central pillar of Nepal’s hydropower sector.

3. Emergence of pioneer IPPs and early private investment

Following liberalization, the first wave of IPP activity emerged in the 1990s, driven primarily by foreign direct investment and institutional private capital. These early projects played a foundational role in proving the bankability of Nepal’s hydropower sector.

Butwal Power Company stands out as a landmark case. Backed by a consortium of Nepali and Norwegian investors, BPC developed and operated the Andhi Khola project with a capacity of 5.1 MW and the Jhimruk project with a capacity of 12 MW. This represented one of the earliest examples of institutional private sector involvement in Nepal’s hydropower development.

The commissioning of the 60 MW Khimti Hydropower Project in July 2000 marked a decisive turning point. Developed with private investment and foreign direct investment, Khimti was the first large-scale privately developed hydropower project in Nepal and fundamentally altered perceptions of infrastructure risk in the country. It was followed by the Upper Bhote Koshi project, initially developed at 36 MW and later expanded to 45 MW, involving US private investment through Panda Energy Corporation. These projects demonstrated that private capital could finance, build, and operate complex hydropower assets in Nepal.

Alongside foreign investment, domestic private participation also began to take root. Indrawati III, with a capacity of 7.5 MW, became the first hydropower project developed entirely with domestic private investment, signaling the gradual localization of capital and expertise.

4. Institutional mechanisms governing IPP participation

Independent Power Producers in Nepal operate within a structure of regulatory and contractual framework. Developers are required to obtain three distinct licenses from the government through the Department of Electricity Development: a survey license, a generation license, and where applicable, a transmission license.

The Nepal Electricity Authority functions as the sole off taker of electricity. IPPs sell power to NEA under Power Purchase Agreements that define tariff structures, payment conditions, and contractual obligations. These PPAs are the financial backbone of project bankability.

Most projects are developed under the Build Own Operate Transfer model. Generation licenses are typically granted for periods of up to 50 years, after which the project assets must be transferred to the Government of Nepal in good operating condition. In addition, IPPs are required to pay royalties to the government, calculated on the basis of installed capacity and energy generation, with differentiated rates for projects serving domestic consumption and those oriented toward export.

5. Expansion and current contribution of IPPs

Over the past three decades, IPPs have transformed Nepal’s hydropower sector from a state dominated system into a competitive, privately driven industry. Their contribution now exceeds that of the public utility in both generation and installed capacity.

As of fiscal year 2024/25, IPPs generated 8,606 GWh of electricity, significantly surpassing the Nepal Electricity Authority’s generation of 2,953 GWh. The number of operational IPP projects has continued to grow rapidly. By the end of fiscal year 2024/25, the total number of operational IPP-owned projects reached 204, with a combined installed capacity of 2,929.7 MW,.

The construction pipeline remains substantial. As of fiscal year 2024/25, 142 IPP projects were under construction following financial closure, representing an additional 4,303 MW of capacity. Furthermore, another 148 projects totaling 4,203 MW are in various stages of development awaiting financial closure. The total number of Power Purchase Agreements (PPAs) signed with IPPs has reached 494, with a combined capacity of 11,436 MW. The shift toward mobilizing domestic capital through banks, financial institutions, and public equity continues to drive this expansion.

6. Structural and operational challenges faced by IPPs

Despite their growth, IPPs face persistent structural challenges. Transmission bottlenecks remain one of the most serious constraints. Delays in constructing high voltage transmission lines, including 220 kV and 400 kV corridors, have prevented timely evacuation of generated power, resulting in spillage and forced underutilization of operational plants.

Hydrological risk is another defining challenge. Most projects are run of river schemes, making generation highly sensitive to seasonal flow variations. Climate change, floods, landslides, and other natural disasters further compound operational and financial risks.

Uncertainty in Power Purchase Agreement terms, particularly debates around take or pay versus take and pay provisions, has historically affected revenue predictability. Procedural delays related to land acquisition, environmental approvals such as EIA and IEE, and forest clearance have also imposed significant time and cost overruns on projects.

7. Public participation, export orientation, and future direction

The sector is increasingly characterized by broader public participation and an outward looking orientation. The concept of People’s Hydro has promoted equity participation by the general public, with hydropower companies required to allocate a portion of shares, often around 10 percent, to local communities affected by project development.

As domestic electricity demand approaches saturation during certain periods, policy attention is shifting toward exporting surplus power to neighboring markets, particularly India and Bangladesh. Regulatory and policy frameworks are being adjusted to facilitate cross border electricity trade and long term export oriented development.

In sum, Nepal’s hydropower sector has evolved from a slow moving, state controlled initiative into a dynamic industry driven largely by Independent Power Producers. Liberalization in the early 1990s catalyzed this transformation, enabling private companies to now account for the majority share of electricity generation in the country and setting the stage for the structural challenges and financing questions that define the sector today.

The context of the problem

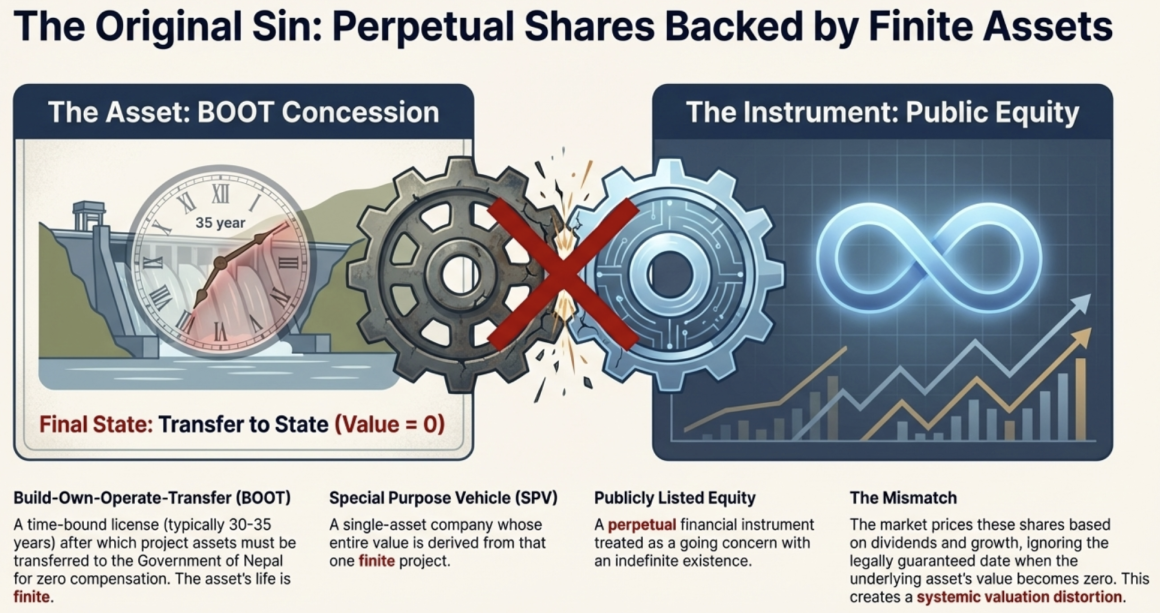

The core problem lies in a fundamental and systemic structural contradiction in Nepal’s hydropower financing model. The legal and regulatory framework compels the convergence of three incompatible elements: the Build Own Operate Transfer concession, which grants a private entity a time bound license, typically 30 to 35 years, after which the project must be transferred to the state for zero compensation; the Special Purpose Vehicle model, which creates a single asset, legally isolated company whose entire value is derived from that finite life project; and the public listing of perpetual equity on the Nepal Stock Exchange, which treats these SPVs as going concerns with indefinite existence. The result is a cliff edge in which a perpetual financial instrument, the share, is backed by an asset that is legally required to disappear. The terminal value of the equity is therefore guaranteed to be zero. The market, however, prices these shares on the basis of dividend yields and growth assumptions, creating a widespread valuation distortion that ignores the embedded expiration date.

This structural flaw is intensified by financial and governance practices that systematically shift long term risk from sophisticated insiders and promoters to retail investors. Promoters, typically supported by bank debt, de-risk projects through the construction phase and early operations, and then use the expiry of securities locked in periods to exit their holdings through the secondary market, effectively monetizing future cash flows. Retail investors are left holding what is treated as perpetual equity while the BOOT clock continues to run down. At the same time, listed SPVs often engage in aggressive capital raising, particularly through high ratio rights issuances, to repay bank loans or to invest in new and riskier subsidiary SPVs. These inter SPV investments undermine the ring fenced nature of the original project, diverting cash flows and retained earnings into new construction risks without shareholder consent, even as the original asset moves closer to its mandatory transfer date with no mechanism for capital redemption.

The crisis is further amplified by a regulatory vacuum that focuses almost entirely on capital mobilization and construction progress while ignoring the end of life scenario. Securities regulations permit initial public offerings even when projects have as little as ten years remaining on their license, and there are no requirements for a sinking fund, a capital redemption reserve, or clear disclosure of the BOOT countdown in financial statements. As a result, the market operates under a going concern illusion. Neither the Securities Board of Nepal nor the Electricity Regulatory Commission has put in place oversight frameworks or mechanisms for an orderly wind down, effectively embedding the eventual collapse of equity value into the system and exposing thousands of retail investors to a predictable terminal loss.

Main post: https://sushilparajuli.com/nepals-doomed-boot-model-hydro-spvs/

How Retail Investors Will Be Burnt

Nepal’s hydropower sector has undergone explosive growth in the past five years, transforming from a peripheral segment into a dominant force in the Nepal Stock Exchange (NEPSE). This growth has been driven largely by retail investors chasing high returns, often without appreciating the structural risks inherent in the Build-Own-Operate-Transfer (BOOT) model. The sector’s systemic dominance, sheer scale of equity, frenzied trading patterns, misaligned dividend incentives, repeated rights share issuances, and promoter exit strategies collectively expose retail investors to a significant risk of principal loss.

1. Quantifying Retail Exposure & Market Dominance

The rise of the hydropower sector can be observed in four dimensions: market capitalization, paid-up capital, trading turnover, and retail float.

1.1 NEPSE Total Market Cap vs. Hydropower Sector Cap

|

Fiscal Year |

Total NEPSE Market Cap (Rs. Millions) |

Hydropower Sector Cap (Rs. Millions) |

Systemic Weight (%) |

|

2020-2021 |

4,010,957.81 |

222,066.06 |

5.54% |

|

2021-2022 |

2,869,344.17 |

358,672.16 |

12.50% |

|

2022-2023 |

3,082,519.56 |

426,021.69 |

13.82% |

|

2023-2024 |

3,553,677.24 |

709,117.91 |

19.95% |

|

2024-2025 |

4,656,989.36 |

2,064,673.02 |

44.33% |

Insights:

- Explosive Growth: Hydropower’s share of total market capitalization increased nearly 8-fold from 5.54% to 44.33%.

- Resilience in Downturns: In 2021-2022, total market cap fell, yet hydropower grew from Rs. 222 billion to Rs. 358 billion, more than doubling its systemic weight.

- Market Dominance: By 2024-2025, hydropower alone controls almost half of NEPSE’s total capitalization, surpassing traditional heavyweights like commercial banks.

1.2 Number of Listed Hydropower Companies & Combined Paid-Up Capital

|

Fiscal Year |

No. of Listed Companies |

Combined Paid-Up Capital (Rs. Millions) |

Key Observation |

|

2020-2021 |

40 |

69,678.67 |

Moderate base with 40 companies |

|

2021-2022 |

51 |

71,306.10 |

Steady growth; 11 new companies added |

|

2022-2023 |

80 |

42,602.17* |

Listing surge (+29 companies); capital temporarily adjusted downward |

|

2023-2024 |

91 |

70,911.79 |

Continued listing boom (+11 companies) |

|

2024-2025 |

100+ |

206,467.30 |

Explosive growth: equity float nearly tripled (+191%) |

Insights:

- Tripling of Equity (2024-2025): Combined paid-up capital surged from Rs. 70.91 billion to Rs. 206.46 billion, indicating massive new share issuance.

- Listing Boom: Number of companies more than doubled from 40 to 91 in four years.

- Sector Depth: With 2.06 billion share units, hydropower has become a high-volume heavyweight in NEPSE.

1.3 NEPSE Turnover vs. Hydropower Turnover

|

Fiscal Year |

Total NEPSE Turnover (Rs. Millions) |

Hydropower Turnover (Rs. Millions) |

% Contribution |

|

2020-2021 |

1,454,444.24 |

222,066.06 |

15.27% |

|

2021-2022 |

1,202,101.40 |

358,672.16 |

29.84% |

|

2022-2023 |

467,126.94 |

130,231.67 |

27.88% |

|

2023-2024 |

734,684.46 |

207,684.92 |

28.27% |

|

2024-2025 |

2,188,476.24 |

822,997.89 |

37.61% |

Insights:

- Frenzied Trading: Even when the broader market cooled in 2021-2022, hydropower turnover grew 61%, reflecting a migration of retail traders into the sector.

- Volume Dominance: In 2024-2025, hydropower accounted for 42.6% of traded shares.

- Liquidity Driver: The sector dictates NEPSE’s sentiment, fueled by high-frequency retail participation.

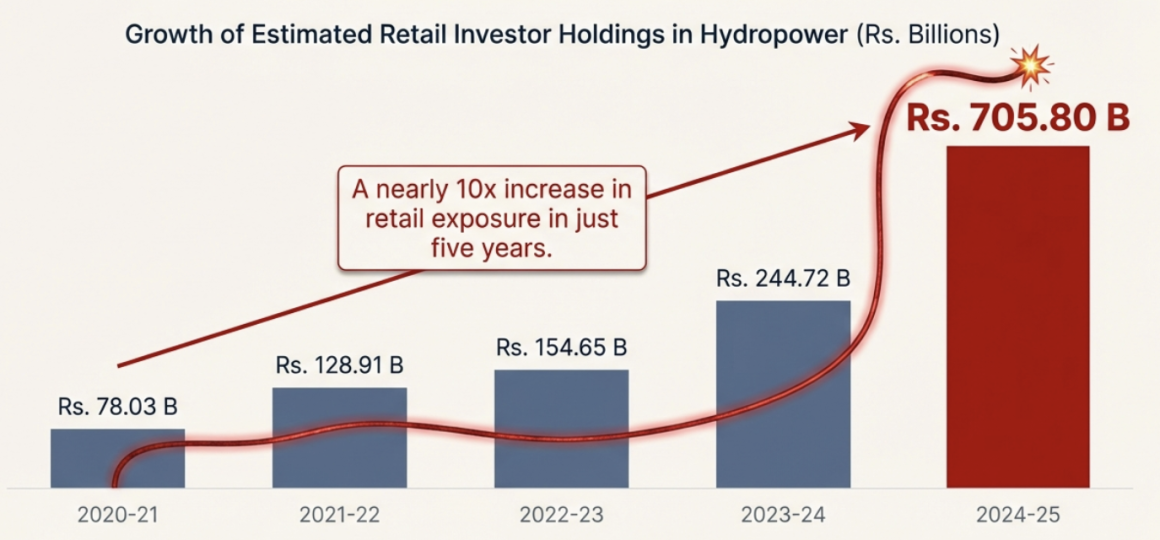

1.4 Estimated Retail Investor Holdings (Principal at Risk)

|

Fiscal Year |

Hydropower Sector Cap (Rs. Millions) |

Market-Wide Float % |

Est. Retail Holdings (Rs. Billions) |

|

2020-2021 |

222,066.06 |

35.14% |

78.03 |

|

2021-2022 |

358,672.16 |

35.94% |

128.91 |

|

2022-2023 |

426,021.69 |

36.30% |

154.65 |

|

2023-2024 |

709,117.91 |

34.51% |

244.72 |

|

2024-2025 |

2,064,673.02 |

34.18% |

705.80 |

Insights:

- 10x Retail Risk Growth: Retail exposure soared from Rs. 78 billion to Rs. 705 billion in just five years.

- 2024-2025 Surge: Rs. 461 billion added in a single year, driven by IPOs, rights shares, and bonus issuances.

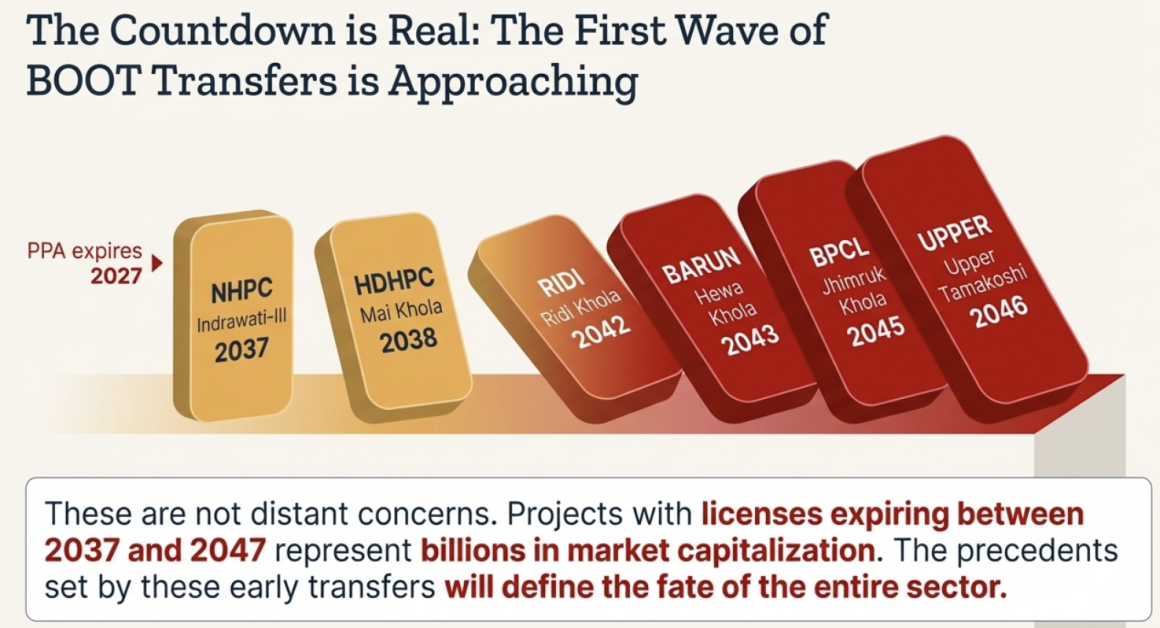

2. Pinpointing the "Cliff Edge": BOOT Transfers

Many hydropower projects are approaching the end of their 30–35 year licenses, at which point their primary asset will revert to the state under the BOOT model. Retail investors are heavily exposed to this terminal risk.

|

Company Symbol |

Project Name |

Capacity (MW) |

COD (AD) |

License Expiry (B.S.) |

Est. Expiry (AD) |

Project Status & Risk |

|

BPCL |

Andhi Khola |

9.4 |

1991-07-01 |

2075/02/13 |

2018 |

Initial license expired; 9.4 MW upgrade in 2072 |

|

NHPC |

Indrawati-III |

7.5 |

2002-10-07 |

2094/06/21 |

2037 |

License valid; PPA expires 2027 |

|

HDHPC |

Mai Khola Small |

4.5 |

2011-02-13 |

2095/04/14 |

2038 |

High terminal risk for early project |

|

RIDI |

Ridi Khola |

2.4 |

2009-10-26 |

2099/02/16 |

2042 |

Small, high-risk asset |

|

NYADI |

Nyadi HEP |

30.0 |

2022-05-10 |

2099/12/06 |

2043 |

Large asset nearing 20-year mark |

|

BARUN |

Hewa Khola |

4.5 |

2011-02-13 |

2100/01/21 |

2043 |

First of 2100 B.S. wave transfers |

|

BPCL |

Jhimruk Khola |

12.0 |

1994-08-01 |

2101/12/30 |

2045 |

Critical legacy portfolio |

|

MODI |

Tallo Modi-1 |

20.0 |

2021-09-30 |

2102/05/20 |

2045 |

Mid-life asset |

|

SANJEN |

Upper Sanjen |

14.8 |

2023-10-08 |

2103/08/11 |

2046 |

Subsidiary of Chilime Group |

|

UPPER |

Upper Tamakoshi |

456.0 |

2021-07-05 |

2103/08/17 |

2046 |

Debt-heavy, default risk |

|

CHCL |

Chilime HEP |

22.1 |

2003-08-25 |

2104/11/30 |

2047 |

Holding company; diversified |

|

UNHPL |

Lower Likhu |

28.1 |

2022-11-04 |

2104/10/20 |

2047 |

Early lifecycle project |

|

MANDU |

Bagmati Sana |

22.0 |

2019-04-02 |

2105/12/28 |

2049 |

Reconstruction after floods |

|

SAYAPATRI |

Daram Khola-A |

2.5 |

2016-06-25 |

2105/02/01 |

2048 |

Small-scale, stable |

Insights:

- Early-mover projects (pre-2100 B.S.) set regulatory precedent.

- BPCL and NHPC illustrate legacy and PPA mismatch risks, respectively.

- Smaller SPVs (HDHPC, Ridi) face structural terminal value decay.

3. Valuation Bubble & Misallocation

Hydro stocks are often traded for yield, masking the terminal BOOT risk.

Dividend Yield Comparison

|

Company/Bank |

Trailing Dividend Yield |

Observations |

|

CHCL |

0.40% |

Below historical median (1.24%), inflated stock price (~Rs. 498) |

|

Nabil Bank |

2.01% |

Lower P/E risk, higher sustainable yield |

Rights Share Issuances (Last 3 Years)

|

Company Name |

Ratio (Right Type) |

Shares Issued (Units) |

Issue Price |

Opening Date (B.S.) |

Primary Purpose / Utilization of Funds |

|

Ankhu Khola Jalvidhyut Co. Ltd. |

1 : 1.5 (150%) |

12,000,000 |

Rs. 100 |

2081/04/27 |

• Invest in Ankhu Khola-2 HEP (20 MW).• Pay off bank loans. |

|

Peoples Power Ltd. |

1 : 0.5 (50%) |

3,163,000 |

Rs. 100 |

2081/04/31 |

• Repay loans to Prime Commercial Bank Ltd. |

|

Joshi Hydropower Dev. Co. Ltd. |

1 : 0.65 (65%) |

2,414,100 |

Rs. 100 |

2081/04/15 |

• Repay bank loans (NMB Bank). |

|

Terhathum Power Company Ltd. |

1 : 1 (100%) |

4,000,000 |

Rs. 100 |

2081/04/05 |

• Repay bank loans.• Construct Khorunga Tangmaya Cascade (2 MW). |

|

Upper Solu Hydro Electric Co. Ltd. |

1 : 1 (100%) |

13,500,000 |

Rs. 100 |

2081/01/22 |

• Repay long-term bank loans. |

|

Dordi Khola Jal Bidhyut Co. Ltd. |

1 : 1 (100%) |

10,542,604 |

Rs. 100 |

2081/02/10 |

• Repay bank loans (Sanima Bank consortium). |

|

Ngadi Group Power Ltd. |

1 : 1 (100%) |

18,512,792 |

Rs. 100 |

2080/10/14 |

• Invest in Siuri Khola HEP (Strategic Partner).• Repay bank loans. |

|

Singati Hydro Energy Ltd. |

1 : 1 (100%) |

14,500,000 |

Rs. 100 |

2080/11/02 |

• Repay loans (Kumari Bank).• Invest in Upper Hongu Khola (14.15 MW). |

|

Ridi Power Company Ltd. |

1 : 0.5 (50%) |

7,744,506 |

Rs. 100 |

2080/11/18 |

• Invest in Tallo Balephi HEP (20 MW) (via Sajha Power).• Repay loans. |

|

Arun Valley Hydropower Dev. Co. |

1 : 1 (100%) |

18,679,626 |

Rs. 100 |

2080/11/17 |

• Invest in PK Hydropower (Likhu Khola).• Pay off loans for Kabeli B-1. |

|

Ghalemdi Hydro Limited |

1 : 2 (200%) |

11,000,000 |

Rs. 100 |

2080/09/10 |

• Invest in Chhujung Khola Hydropower (63 MW). |

|

Balephi Hydropower Limited |

1 : 1 (100%) |

18,279,700 |

Rs. 100 |

2080/08/21 |

• Repay bank loans (Global IME, Kumari, etc.). |

|

Upper Tamakoshi Hydropower Ltd. |

1 : 1 (100%) |

105,900,000 |

Rs. 100 |

2080/05/18 |

• Repay short-term loans.• Construct Rolwaling Khola HEP (22 MW). |

|

Arun Kabeli Power Limited |

1 : 1 (100%) |

18,552,105 |

Rs. 100 |

2080/05/11 |

• Repay bank loans related to Kabeli B-1 construction. |

|

Synergy Power Development Ltd. |

2 : 1 (50%) |

4,032,875 |

Rs. 100 |

2080/05/03 |

• Invest in Apex Makalu Hydro Power (22 MW). |

|

Himalaya Urja Bikas Company Ltd. |

1 : 1 (100%) |

9,900,000 |

Rs. 100 |

2080/04/24 |

• Pay loans for Upallo Khimti (12 MW) & Upper Khimti-II (7 MW). |

|

Rapti Hydro & General Construction |

1 : 1 (100%) |

6,127,938 |

Rs. 100 |

2080/03/29 |

• Repay bank loans.• Working capital management. |

|

National Hydro Power Company |

10 : 5 (50%) |

8,221,459 |

Rs. 100 |

2080/03/29 |

• Invest in Lower Erkhuwa Hydropower (14.15 MW). |

|

Himal Dolakha Hydropower Co. |

1 : 0.75 (75%) |

12,000,000 |

Rs. 100 |

2080/02/22 |

• Repay Bridge Gap Loan.• Invest in Mai Khola Small Hydro. |

|

Radhi Bidyut Company Ltd. |

1 : 1.47 (147.52%) |

9,535,760 |

Rs. 100 |

2079/06/05 |

• Invest in Kasuwa Khola Hydropower (45 MW). |

|

Ngadi Group Power Ltd. (Previous) |

1 : 1.5 (150%) |

10,603,986 |

Rs. 100 |

2079/04/18 |

• Repay loans.• Invest in other projects. |

|

Api Power Company Ltd. (Issuance 1) |

1 : 0.39 (39.36%) |

10,860,000 |

Rs. 100 |

2078/12/25 |

• Invest in/Construct Upper Chameliya HEP (40 MW). |

|

HIDCL |

1 : 1 (100%) |

110,000,000 |

Rs. 100 |

2078/04/05 |

• Equity investment in various hydro projects (subsidiaries). |

|

Api Power Company Ltd. (Issuance 2) |

1 : 0.29 (29.38%) |

5,670,000 |

Rs. 100 |

2078/02/20 |

• Invest in/Construct Upper Chameliya HEP. |

|

Arun Valley Hydropower (Previous) |

1 : 0.5 (50%) |

5,241,197 |

Rs. 100 |

2077/12/06 |

• Construction of Kabeli B-1 Cascade HEP. |

Key Patterns:

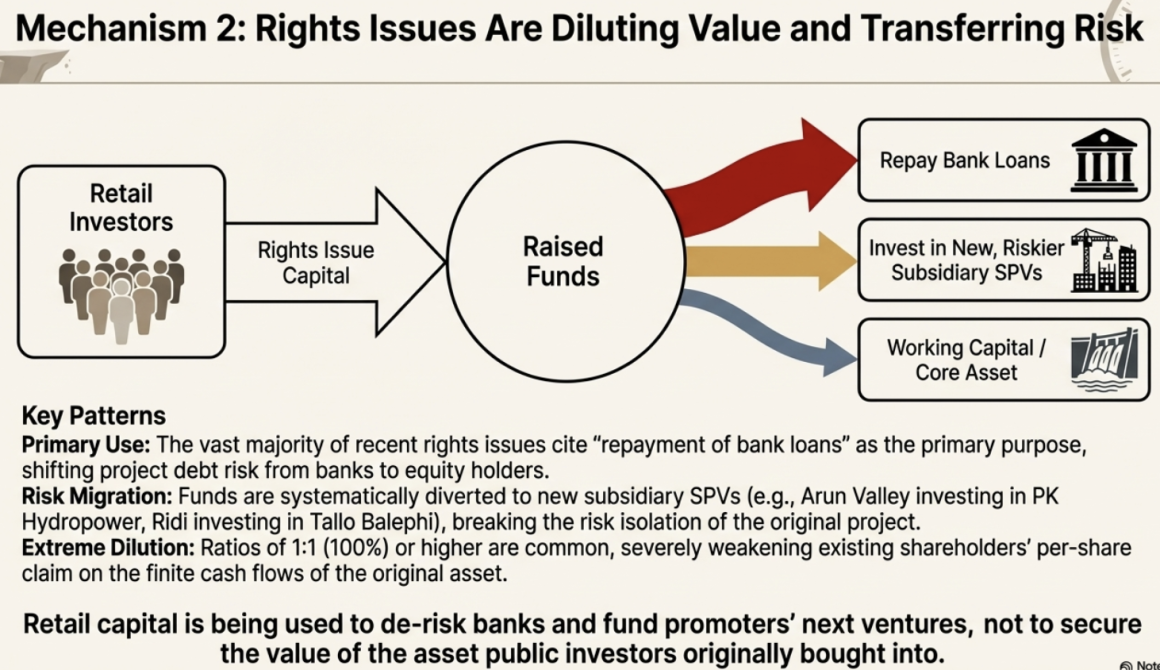

- Funds frequently redirected to new projects/subsidiaries.

- Majority used to repay bank debt → shifts risk to retail investors.

- Extreme dilution (>100%) weakens per-share claims.

4. Governance Risk & Promoter Exit

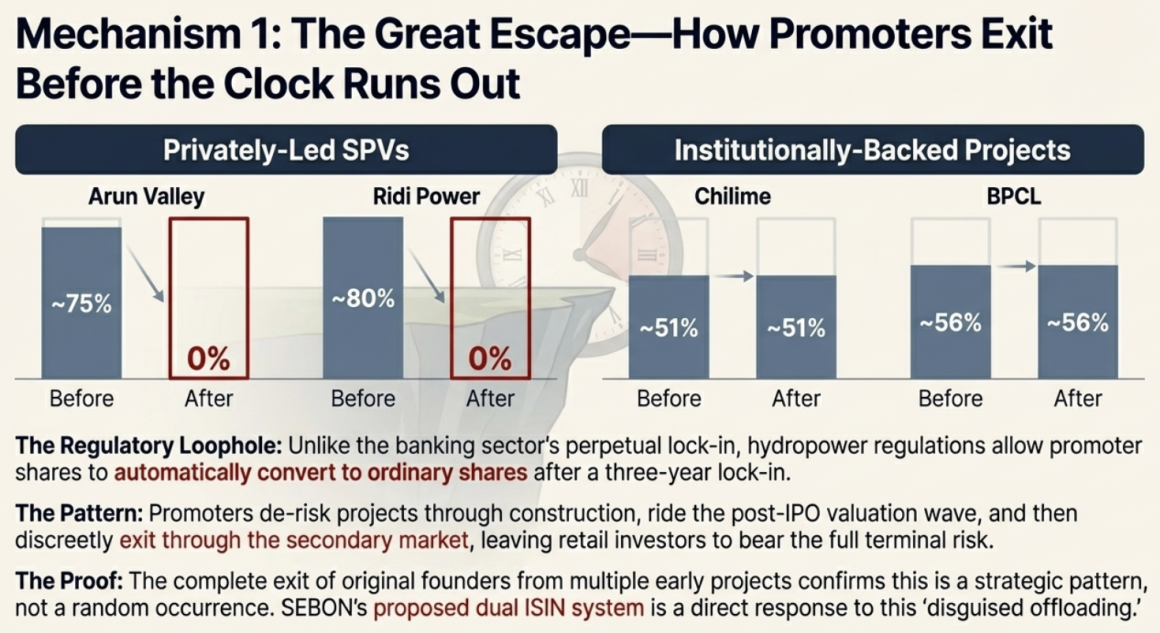

Based on the analysis of Nepal’s oldest listed hydropower companies, a clear pattern emerges: there is a significant and systematic drop in promoter shareholding for privately-led projects immediately following the expiration of the mandatory three-year lock-in period. This trend substantiates the hypothesis of early insider exits.

The data from key case studies reveals a stark divergence. Companies like Arun Valley Hydropower (AHPC) and Ridi Power (RIDI), which began with typical promoter holdings of 70-80%, now report 0% promoter holding, indicating a complete reclassification and exit of the original founders. Conversely, institutionally-backed projects show stability; Chilime Hydropower (CHCL), with the Nepal Electricity Authority as its anchor promoter, has maintained a consistent 51% holding, while Butwal Power (BPCL) retains a 56.27% stake under its strategic private promoter, Shangri-La Energy. This contrast highlights that the drop is not universal but is prevalent in privately-developed Special Purpose Vehicles (SPVs).

The significant drop in promoter shareholding is directly facilitated by a critical regulatory disparity unlike in the banking sector. In Nepal, the Bank and Financial Institution Act (BAFIA) typically mandates that bank promoters maintain a minimum shareholding (often 51%) indefinitely to ensure long-term commitment and financial system stability. Conversely, the hydropower sector operates under securities regulations that allow for an automatic conversion of promoter shares into ordinary shares immediately after the three-year lock-in period expires. This loophole means that once converted, the shares of the original founders become indistinguishable from those of the public on the trading floor, enabling discreet liquidation at market peaks without the transparency of a formal reclassification process. This mechanism, observed in the complete exit of promoters from companies like Arun Valley (0% holding) and Ridi Power (0% holding), confirms a strategic pattern of early departure. It allows promoters to capitalize on secondary market valuations and recycle capital into new ventures, leaving retail investors holding assets whose original creators have exited.

The recent push by SEBON for dual ISINs (International Securities Identification Numbers)—a system that would assign unique codes to separate promoter shares from public shares, thereby preventing them from being traded invisibly after the lock-in period—is a direct regulatory response designed to close this loophole and end the practice of “disguised offloading” that has characterized the hydropower sector.

Observations from Older Hydro Companies:

- Privately-led SPVs (Arun Valley, Ridi Power) show 0% promoter holding post-lock-in.

- Institutionally-backed projects (Chilime, BPCL) retain 51–56% stakes.

- Regulatory loophole allows promoter shares to automatically convert post-lock-in → early exits without disclosure.

- SEBON’s dual ISIN initiative seeks to prevent disguised offloading.

Therefore retail investors are exposed to a perfect storm:

Systemic Concentration: Hydropower now dominates nearly half of NEPSE, magnifying any sector shock.

Terminal Risk Cliff: Many projects will revert to the state under BOOT, rendering future equity essentially worthless.

Misallocated Capital: Rights issues largely recycle money to pay banks or fund new high-risk projects, rather than securing original asset value.

Governance Loopholes: Promoters can exit early, leaving retail holders to bear the terminal value and dilution risk.

Speculative Trading: Surging turnover and high valuations create a bubble that disguises the real risks.

Retail investors have collectively placed over Rs. 705 billion in a sector with finite asset life, rising leverage, and systemic structural risks – effectively setting the stage for a massive financial loss when BOOT expiries coincide with market corrections or rights issue failures.

Status of Listed Hydropower Companies and Mandatory Public Share Issuance

Nepalese hydropower companies, classified as “organized institutions” for securities law purposes, are subject to a legal and regulatory framework governing public share issuance and subsequent listing on NEPSE. These requirements are not merely procedural but are linked to statutory obligations designed to protect public investment, ensure capital mobilization, and promote local participation.

At the core, hydropower companies are compulsorily required to issue a portion of their shares to the public and list them, provided certain project milestones are met. This obligation arises from the intersection of the Securities Act, Securities Registration and Issuance Regulation, and specialized government programs, such as the People’s Hydropower Program (Janata ko Jalvidyut Karyakram).

1. Compulsory Public Share Issuance

1.1 Threshold-Based Requirement

Hydropower companies intending to raise capital via an Initial Public Offering (IPO) must adhere to Rule 9(1) of the Securities Registration and Issuance Regulation, 2073. This rule stipulates that 10% to 49% of the issued capital must be offered to the public unless otherwise specified by regulatory authorities like the Electricity Regulatory Commission.

- Purpose: Mobilize equity from a wider investor base while ensuring promoters retain controlling stakes (minimum 51%).

- Project Milestones: Only companies that have achieved at least 75% physical construction progress, secured financial closure, and have a valid Power Purchase Agreement (PPA) are eligible for registration and public issuance.

1.2 Local and Diaspora Participation

Hydropower projects must reserve a portion of equity for local residents and Nepalese working abroad:

|

Shareholder Category |

Mandatory Allocation |

Legal Source |

Notes |

|

Project-Affected Local Residents |

Up to 10% of issued capital |

Rule 9(4), Securities Regulation, 2073 |

Allocation based on Environmental Impact Assessment (EIA) classifications; unsold shares added to general public pool |

|

General Public |

Remaining portion up to statutory limit |

Securities Act, 2063 & Rule 9(1) |

Can include local and foreign-employed Nepalis |

|

Nepalese Abroad |

10% quota within general public offering |

Securities Regulation, 2073 |

Only valid labor permit holders |

This structure ensures that resource utilization benefits are shared broadly, while still allowing promoters and founder groups to maintain effective control.

1.3 Price Inflation and BOQ Adjustments

An important, and very important aspect of development of hydropower is the adjustment in project costing and BOQ (Bill of Quantities):

- Public issuance requires disclosure of project cost, construction schedule, and projected returns in the IPO prospectus.

- Developers unofficially defend that to ensure regulatory compliance and maintain investor confidence, they need to inflate BOQ and project costs, reflecting contingency, statutory approvals, and public offering expenses – as a need to meet the statutory obligations of public issuance and protect retail investors by aligning share pricing at par with the true cost of equity mobilization. Of course, this is a topic that warrants a separate research.

In short, price and cost adjustments are directly linked to the legal mandate of public issuance, a step intrinsic to hydropower company operations under current law.

2. Compulsory Public Listing

Once a hydropower company has issued shares to the public, it is mandated to list those shares on the stock exchange:

- Listing Requirement: Rule 3(1) of the Securities Listing and Trading Regulation, 2075 states that any organized institution issuing securities to the public must list those securities on NEPSE.

- Timeline: Rule 3(2) requires that a listing application be submitted within seven days of prospectus approval.

- Secondary Market Access: Section 43 of the Securities Act, 2063 obligates companies to facilitate market arrangements via a licensed stock exchange, ensuring liquidity for public investors.

Prerequisites for Listing:

- Minimum 75% construction completion.

- Full financial closure.

- Signed PPA with the energy offtaker.

- At least ten years of remaining license validity.

3. Lock-in Periods for Shares

Lock-in provisions are designed to stabilize ownership during early public stages and protect investors from premature promoter exits or speculative trading.

|

Shareholder Group |

Lock-in Duration |

Key Points |

|

General Promoters/Founders |

3 Years |

Applies to original and bonus/right shares; prevents early selling post-IPO |

|

Specialized Investment Funds (PE/VC) |

1 Year |

For registered funds, either domestic or government-approved foreign entities |

|

Project-Affected Local Residents |

3 Years |

Ensures locals retain investment for meaningful period; includes bonus/right shares |

|

Reserved Employees |

3 Years |

Shares issued to employees or as incentives are restricted |

|

Directors/Executives |

Tenure + 1 Year |

No buying/selling during tenure and for 1 year post-retirement; applies to immediate family members as well |

Special Notes:

- Shares under phased payments (“call for capital”) are only tradable after full subscription payment.

- Lock-in restrictions do not apply in the event of a shareholder’s death or the purposes of legal transfers.

- SEBON may grant exceptions for corporate necessity, e.g., intra-group transfers to maintain operations.

Hydropower companies in Nepal are legally bound to issue public shares and list them, with clear rules on local participation, diaspora quotas, and promoter retention. Meanwhile, lock-in periods act as a safeguard against premature promoter exits, speculative trading, and excessive short-term volatility. Collectively, these regulations aim to balance public investment protection with operational flexibility for project developers, creating a structured framework that governs both capital mobilization and market behavior.

Potential Solutions for Nepal’s Hydropower Terminal Value Crisis

Nepal’s hydropower’s problem: publicly listed BOOT SPVs are finite-life assets, but investors treat them as perpetual equities. The mismatch between instrument form (perpetual shares) and asset reality (fixed-term license with zero-compensation transfer) has created systemic risks, threatening retail investors and market stability. This chapter evaluates potential solutions across disclosure, capital structure, corporate governance, market structure, contractual arrangements, and capital market development.

|

Solution Category |

Specific Solution(s) |

Problem Addressed |

Mechanism / How It Works |

Effect / Outcome |

|

1. Disclosure-Based Reforms |

Mandatory BOOT Countdown & Reclassification |

Information asymmetry; perpetual-equity illusion |

Display license expiry in reports, prospectuses, and NEPSE; reclassify equity as finite-life infrastructure |

Forces rational pricing, destroys false perpetuity narrative |

|

2. Capital Structure Reforms |

Mandatory Capital Redemption Reserve / Sinking Fund; Instrument Conversion near License Maturity; Replace Equity Issuance with Redeemable/Fix-Yield Instruments |

Zero terminal value; late-stage investor risk; instrument mismatch |

Accumulate reserves for redemption; convert ordinary shares into preference/fixed-yield instruments near expiry; issue debt-like instruments instead of perpetual equity |

Ensures capital return, reduces late-stage risk, aligns investment instrument with finite asset life |

|

3. Corporate Governance Reforms |

Promoter Lock-in Redesign; Strict Ring-Fencing of Inter-SPV Investments |

Premature promoter exit; risk migration through cross-SPV investments |

Extend promoter holding periods toward license expiry; limit inter-SPV investments, require approvals and reporting |

Aligns promoter incentives, prevents cross-subsidization, maintains SPV risk isolation |

|

4. Market Structure Reforms |

Sectoral Consolidation Through Mergers; Conversion into Listed Holding Company Structures |

Single-asset SPV vulnerability; terminal value collapse |

Merge SPVs into diversified portfolio companies; shift SPV equity into holding companies with multiple subsidiaries |

Spreads license expiry risk, creates rolling-horizon infrastructure vehicles, preserves listed entity value beyond individual project expiry |

|

5. Contractual Solutions |

Post-BOOT Operator / Management Contracts; Optional Buyback / Redemption Windows |

Terminal value and liquidity risk |

Enable SPVs to continue as O&M service providers post-transfer; create structured buyback/redemption windows before expiry |

Maintains revenue and listed status post-transfer; provides orderly exit for late-stage investors |

|

6. Capital Market Development |

Project Bond Market Development; Preference Share / Participating Debenture Framework |

Asset-liability mismatch; finite-life financing gap |

Develop project-level or corporate-level bonds with maturity aligned to license; issue preference shares/debentures instead of perpetual equity |

Aligns financing with asset life, provides long-term, maturity-matched capital market instruments, deepens investor base |

Here is the detailed list of potential solutions:

|

Option |

What It Is |

What It Solves and How |

How It Could Be Implemented in Nepal |

Implementation Challenges |

|

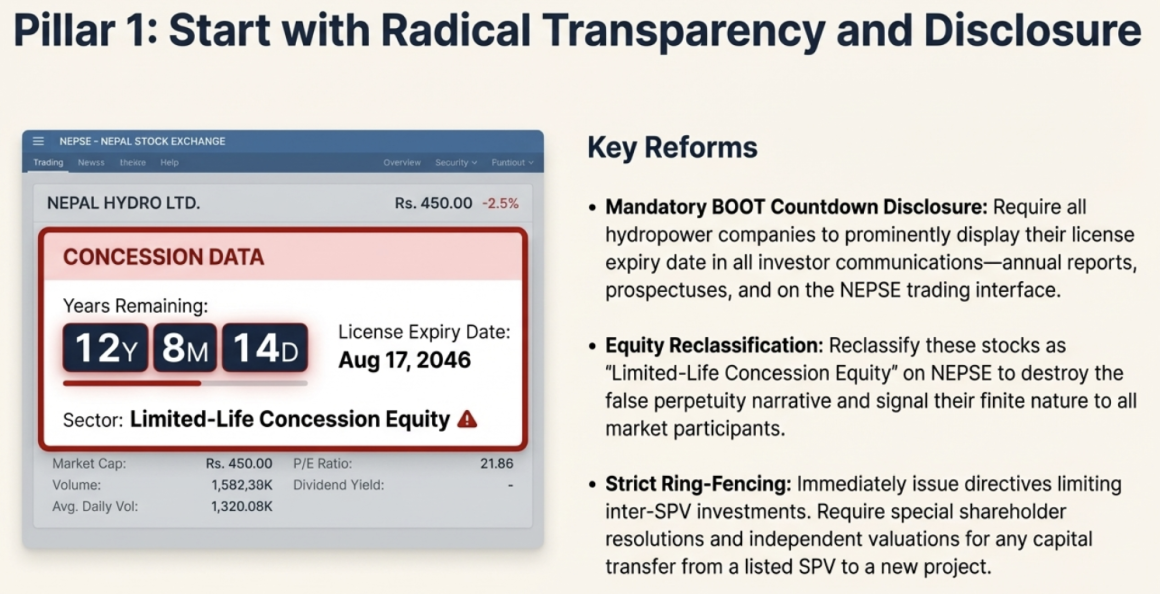

Mandatory BOOT Countdown (Doom Clock) Disclosure & Equity Reclassification |

A regulatory requirement that all listed hydropower companies prominently disclose their license expiry dates in all investor communications (annual reports, prospectuses, trading screens, promotional materials), accompanied by mandatory reclassification of such stocks as “Limited-Life Concession Equity” or “Finite-Life Infrastructure Equity” distinct from standard perpetual equities. This transforms informational disclosure into a structural market reclassification that forces rational pricing. |

This solution addresses the fundamental information asymmetry and perpetual-equity illusion that has allowed hydropower stocks to trade as if they possess infinite terminal value. By mandating a “BOOT Countdown Clock” in annual reports, IPO/FPO prospectuses, and NEPSE trading interfaces, the solution forces market participants to confront the legally predetermined zero-compensation transfer obligation embedded in every project’s lifecycle. The reclassification into a separate equity category destroys the false perpetuity narrative that has enabled speculative trading at prices disconnected from underlying asset economics. The solution is particularly effective because it operates through disclosure rather than prohibition, making it politically feasible while still achieving substantial market correction. Historical precedent from China’s toll road sector demonstrates that mandatory disclosure of finite concession terms, even without structural reform, has gradually shifted investor behavior and valuation methodologies. |

Implementation requires coordinated action by SEBON, NEPSE, and the Electricity Regulatory Commission. SEBON would need to issue a directive amending to include Schedule for Concession Disclosure Requirements, mandating specific disclosure formats, font sizes, and placement for license expiry information. NEPSE would need to modify its trading systems to display remaining license life as a data field alongside current price and volume, similar to how derivative contracts display expiry dates. The reclassification would require amendments to NEPSE Listing Rules to create a new sector or classification category, potentially “Limited-Life Infrastructure,” with distinct trading, margin, and investment guidelines for institutional investors. Implementation timeline could be rapid—90 to 120 days for regulatory amendments, with system modifications at NEPSE requiring an additional 60 to 90 days. The cost to companies is minimal (primarily disclosure formatting), making compliance burden low. |

The primary challenge is regulatory capture and political economy resistance. SEBON has historically been accommodating to hydropower promoters, and the securities industry benefits from high trading volumes in hydropower stocks regardless of fundamental value. There is genuine risk that the disclosure requirements, if implemented, would be weak—permitting small-font footnote disclosures rather than prominent dashboard-style presentations that actually influence investor behavior. A second challenge involves definitional complexity: determining the “true” license expiry date when many projects have received extensions, upgrades, or amendments. The Andhi Khola case (BPCL), which received a license extension following its 2072 upgrade from 5.1 MW to 9.4 MW, demonstrates that license life can be extended through capital investment, creating uncertainty about expiry dates that sophisticated parties can exploit. Finally, disclosure alone does not solve the terminal value problem—it merely reveals it—meaning retail investors may still purchase shares at inflated prices while fully aware of the expiry risk, preferring speculation to alternative investments in a market with limited options. |

|

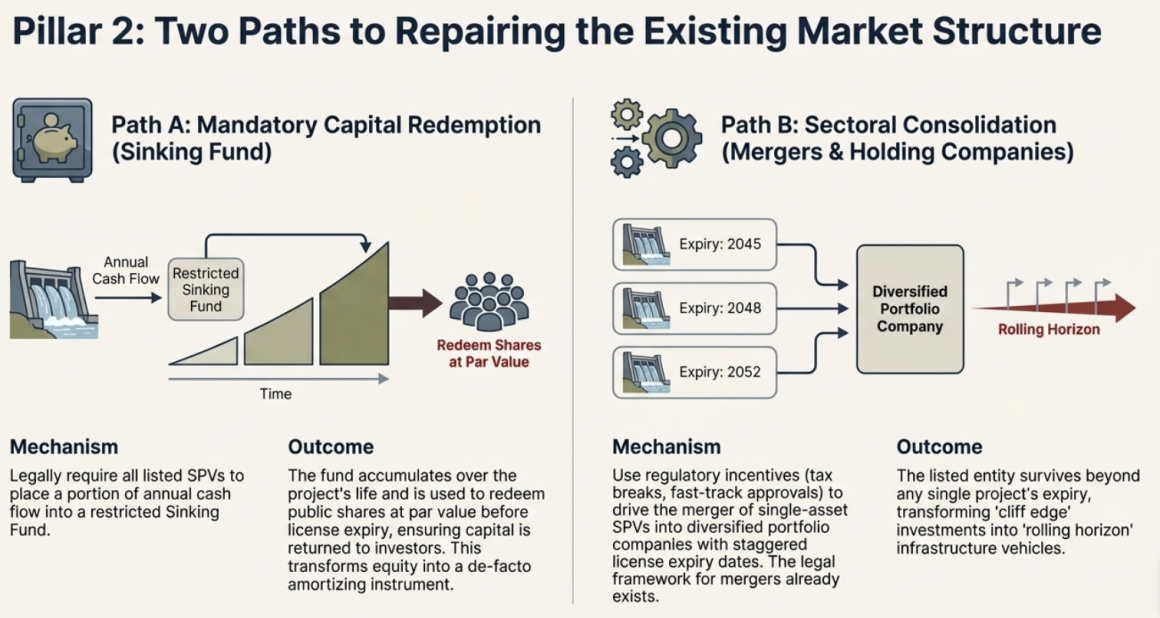

Mandatory Capital Redemption Reserve / Sinking Fund |

A regulatory requirement that listed BOOT SPVs retain a specified portion (typically 15% to 25%) of annual Net Distributable Cash Flow into a restricted Capital Redemption Reserve or Sinking Fund, which can only be used to repurchase or redeem public shares at par value (NPR 100) upon license expiry. This transforms perpetual equity into a de facto amortizing instrument by legally obligating companies to accumulate capital for shareholder return. |

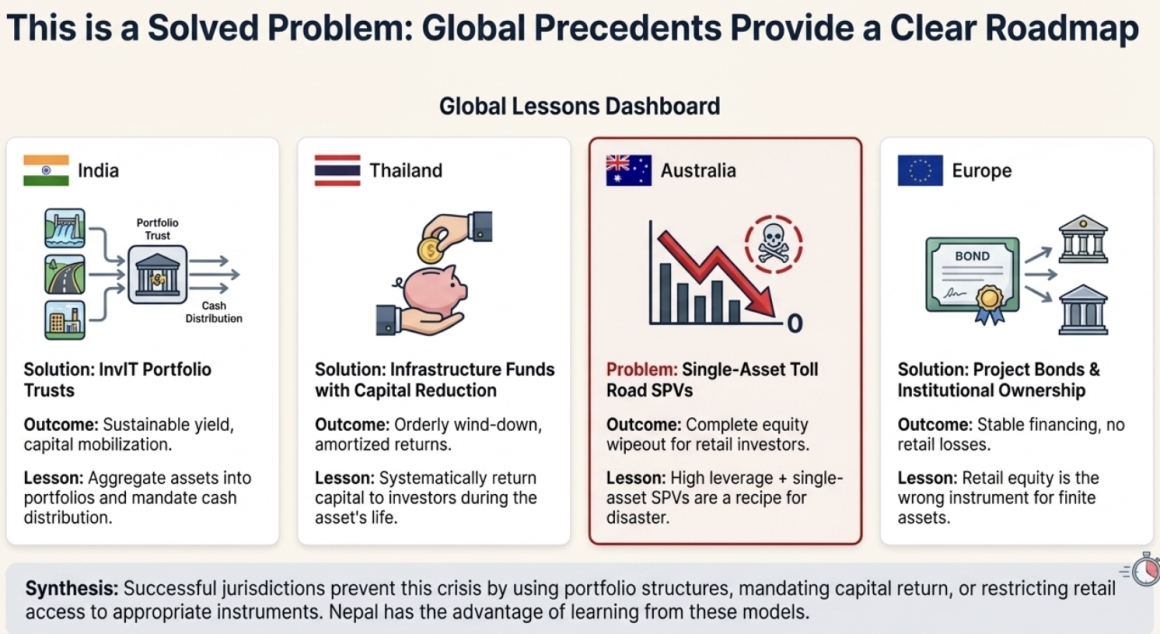

This solution directly addresses the guaranteed zero terminal value problem by creating a statutory mechanism for capital return. Under current law, shareholders face certain total loss at license expiry with no redemption pathway. The mandatory sinking fund requirement forces companies to systematically repay public capital during the operational phase, ensuring that the par value of shares is returned before the asset transfers to the state. The mechanism is economically equivalent to amortization—each year of operation sees a portion of share value “extinguished” through reserve accumulation rather than through share buybacks at market prices. The solution is particularly powerful because it targets the specific timing mismatch: retail investors provide permanent capital for finite assets, and the sinking fund corrects this by ensuring permanent capital is not required. International precedent from project finance structures in the UK and Australia demonstrates that mandatory reserve requirements for infrastructure with state reversion prevent the “zombie equity” scenario where shares become worthless shells after asset transfer. |

Implementation requires SEBON to promulgate the Hydropower Capital Redemption Regulations establishing mandatory reserve percentages, calculation methodologies, and restricted use provisions. The regulations should specify: (a) minimum annual contribution based on calculation methodology considering the remaining license life to ensure full accumulation by expiry; (b) prohibition on using reserve funds for inter-SPV investments, dividends, or debt substitution; (c) trustee oversight through an independent financial institution; and (d) clear waterfall for distribution at license expiry. The implementation should be phased: Phase 1 (immediate) requires new issuers to establish reserves from first year of commercial operation; Phase 2 (within 2 years) requires existing listed companies to begin accumulation, with catch-up provisions for late-stage projects. Nepal Rastra Bank would need to issue guidelines for trustee banks on reserve account management and reporting. The total cost to the sector is substantial but manageable: approximately NPR 10 to 15 billion annually across 91 listed companies, funded through modest dividend reduction rather than operational impact. |

The most significant challenge involves cash flow adequacy for late-stage projects. Companies with fewer than 10 years remaining on licenses cannot accumulate sufficient reserves to return full par value even at 100% cash flow retention. For hydros nearing expiry the accumulation requirement would be a substantial portion of the paid-up capital per year, which may exceed free cash flow after debt service and royalties. A second challenge involves promoter resistance and political economy dynamics. Promoters currently benefit from the zero-compensation transfer—they invest construction capital, extract dividends during operation, and exit before expiry with no obligation to return public capital. The mandatory sinking fund fundamentally alters this calculus, reducing promoter net present value and likely triggering industry opposition. |

|

Sectoral Consolidation Through Mandatory or Incentivized Mergers |

A regulatory-driven consolidation of the listed hydropower SPVs into approximately 15 to 20 portfolio companies through mandatory mergers for closely-related projects (common river basins, geographic proximity) and incentivized mergers for unrelated companies through tax benefits, expedited approvals, and simplified regulatory processes. The resulting entities would hold diversified portfolios of projects with staggered license lives, enabling portfolio NAV logic rather than single-asset terminal value collapse. |

This solution addresses the structural vulnerability of single-asset SPVs by creating diversified entities where license expiry risk is spread across multiple projects with different handover dates. Under current structure, each listed company faces a binary outcome: either the license is extended (value preserved) or it expires (value destroyed). A diversified portfolio company with 10 projects, each expiring in different decades, provides continuous revenue generation as older projects transfer while newer projects remain operational. The solution transforms the market from 100+ “cliff edge” listed investments into a smaller number of “rolling horizon” infrastructure vehicles. International precedent from Australia’s Spark Infrastructure and even Nepal’s Chilime Holding Company model demonstrates that diversified holding structures successfully maintain listed entity viability beyond individual project lifecycles. The consolidation approach is particularly effective for Nepal because it leverages existing market structures—listed entities remain listed, regulatory relationships continue, and investor portfolios merely rebalance—while fundamentally addressing the finite asset problem through portfolio construction. |

Implementation requires SEBON to promulgate the Hydropower Capital Redemption Regulations establishing mandatory reserve percentages, calculation methodologies, and restricted use provisions. The regulations should specify: (a) minimum annual contribution based on calculation methodology considering the remaining license life to ensure full accumulation by expiry; (b) prohibition on using reserve funds for inter-SPV investments, dividends, or debt substitution; (c) trustee oversight through an independent financial institution; and (d) clear waterfall for distribution at license expiry. The implementation should be phased: Phase 1 (immediate) requires new issuers to establish reserves from first year of commercial operation; Phase 2 (within 2 years) requires existing listed companies to begin accumulation, with catch-up provisions for late-stage projects. Nepal Rastra Bank would need to issue guidelines for trustee banks on reserve account management and reporting. The total cost to the sector is substantial but manageable: approximately NPR 10 to 15 billion annually across 91 listed companies, funded through modest dividend reduction rather than operational impact. |

The most significant challenge involves cash flow adequacy for late-stage projects. Companies with fewer than 10 years remaining on licenses cannot accumulate sufficient reserves to return full par value even at 100% cash flow retention. For hydros nearing expiry the accumulation requirement would be a substantial portion of the paid-up capital per year, which may exceed free cash flow after debt service and royalties. A second challenge involves promoter resistance and political economy dynamics. Promoters currently benefit from the zero-compensation transfer—they invest construction capital, extract dividends during operation, and exit before expiry with no obligation to return public capital. The mandatory sinking fund fundamentally alters this calculus, reducing promoter net present value and likely triggering industry opposition. |

|

Sectoral Consolidation Through Mandatory or Incentivized Mergers |

A regulatory-driven consolidation of the listed hydropower SPVs into approximately 15 to 20 portfolio companies through mandatory mergers for closely-related projects (common river basins, geographic proximity) and incentivized mergers for unrelated companies through tax benefits, expedited approvals, and simplified regulatory processes. The resulting entities would hold diversified portfolios of projects with staggered license lives, enabling portfolio NAV logic rather than single-asset terminal value collapse. |

This solution addresses the structural vulnerability of single-asset SPVs by creating diversified entities where license expiry risk is spread across multiple projects with different handover dates. Under current structure, each listed company faces a binary outcome: either the license is extended (value preserved) or it expires (value destroyed). A diversified portfolio company with 10 projects, each expiring in different decades, provides continuous revenue generation as older projects transfer while newer projects remain operational. The solution transforms the market from 100+ “cliff edge” listed investments into a smaller number of “rolling horizon” infrastructure vehicles. International precedent from Australia’s Spark Infrastructure and even Nepal’s Chilime Holding Company model demonstrates that diversified holding structures successfully maintain listed entity viability beyond individual project lifecycles. The consolidation approach is particularly effective for Nepal because it leverages existing market structures—listed entities remain listed, regulatory relationships continue, and investor portfolios merely rebalance—while fundamentally addressing the finite asset problem through portfolio construction. |

Implementation requires a two-track approach: mandatory consolidation for projects with obvious synergies (same river system, shared transmission infrastructure, geographic proximity) and incentivized voluntary consolidation for unrelated projects. For mandatory consolidation, SEBON and the MoWERI, ERC should jointly issue the Hydropower Consolidation Directive, identifying clusters of projects suitable for merger based on: (a) common river basin or hydrological system; (b) shared transmission infrastructure; (c) geographic proximity enabling operational synergies; and (d) promoter commonality. The directive would establish timeline for merger completion (24 months), governance framework for merged entities, and dispute resolution mechanisms for minority shareholders. For incentivized consolidation, the Ministry of Finance could offer: (a) corporate tax reduction for merged entities meeting diversification thresholds; (b) expedited approval for right share issuances and inter-SPV investments; (c) exemption from recharacterization taxes such as deemed disposals under Income Tax Act, 2058 – like those offered to the BFI sector, (d) NEPSE fee waivers for merger-related transactions. The merger implementation should be supervised by ERC with authority to appoint provisional management and resolve disputes. Implementation timeline is 36 to 48 months for full sector consolidation, with initial mandatory clusters completed within 24 months. |

The primary challenge involves valuation disputes and minority shareholder protection. When two listed companies merge, minority shareholders of both entities must receive equivalent value, but project-level valuations for finite-license assets are inherently contentious. The party receiving lower valuation will claim expropriation, potentially triggering litigation that delays consolidation. A second challenge involves promoter incentives—many current promoters built their reputations and extracted fees through single-project structures. Consolidated entities reduce individual promoter influence and may trigger resistance from established figures in the sector. Third, Nepal’s legal framework for mandatory mergers is underdeveloped. Drafting enabling regulation would require time and political consensus that may be time taking. Fourth, scale economies from consolidation must be genuine—merged entities must achieve cost savings through shared overhead, coordinated maintenance, and optimized dispatch. If merged companies merely replicate existing structures with added management layers, consolidation creates cost rather than value. Finally, the concentrated ownership resulting from mergers reduces market liquidity and may create “too-big-to-fail” dynamics that increase systemic risk rather than reducing it. |

|

Conversion into Listed Holding Company Structures |

A structural transformation where existing single-asset SPVs become subsidiaries of newly-formed or existing holding companies, with public equity shifted from project-level to corporate-level trading. The listed holding company holds stakes in multiple unlisted operating subsidiaries, each with its own BOOT license, and the consolidated entity survives beyond any single project’s license expiry through dividend income from remaining subsidiaries. |

This solution addresses the finite asset problem by aligning listed entity structure with the underlying asset reality. Under current structure, a listed company IS a project—license expiry equals entity death. Under the holding company model, the listed entity is a corporate shell that owns project stakes; when one project transfers, the entity continues because it owns other projects. The solution is structurally identical to sectoral consolidation but operates through market transactions (share swaps, asset sales) rather than regulatory mandates. The Chilime Hydropower (CHCL) model—where the 22.1 MW Chilime plant is one asset among a portfolio including Rasuwagadhi (111 MW), Sanjen (14.8 MW), and Madhya Bhotekoshi (102 MW)—provides proof of concept in Nepal’s market. Chilime’s equity value survives its own license expiry because dividends flow from subsidiary stakes. The holding company structure is internationally validated: Australian infrastructure trusts, European utilities, and Indian InvITs all operate on this principle. For Nepal, the solution offers the additional benefit of preserving the “perpetual entity” assumption embedded in securities law while making that assumption accurate through portfolio construction. |

Implementation operates through two pathways: organic conversion and acquisition-based conversion. For organic conversion, existing listed companies with sufficient capital and project pipelines would establish wholly-owned subsidiaries for new projects, gradually shifting their asset base from single-project to multi-project. SEBON would need to amend listing rules to permit (and eventually require) holding company classification for entities meeting portfolio thresholds. For acquisition-based conversion, smaller SPVs would be acquired by larger holding companies through share-for-share exchanges, with the acquired entity becoming a subsidiary. The Securities Registration and Issuance Regulation would need amendments to create streamlined approval processes for holding company formations and acquisitions. Implementation timeline is 24 to 36 months for regulatory framework development, with market-driven conversion proceeding over 5 to 10 years as companies pursue commercial advantages of holding company status. |

The fundamental challenge involves the zero-sum nature of holding company creation. When Company A acquires Company B, Company B shareholders become Company A shareholders. No new value is created—only transferred. Promoters of target companies may resist acquisition if they believe their stakes are undervalued, or may demand premium prices that reduce acquisition benefits. A second challenge involves corporate governance complexities. Holding company structures create agency problems between parent management and subsidiary minority shareholders, potential for related-party transactions that disadvantage subsidiaries, and opacity in consolidated financial statements. Nepal’s track record on related-party transaction oversight is poor, and extending this to holding company structures risks amplifying existing governance failures. Third, the solution requires sophisticated financial management capabilities that many current hydropower promoters lack. Managing a portfolio of projects with different hydrological profiles, license expiries, and capital requirements demands financial expertise beyond single-project development. Fourth, the regulatory framework for listed holding companies must address consolidated leverage limits, cross-guarantee prohibitions, and inter-company financial support rules. Finally, there is timing risk: if consolidation occurs slowly and the first BOOT transfers occur before the market has diversified sufficiently, the crisis may unfold before the solution takes effect. |

|

Post-BOOT Continuity Through Operator / Management Contracts |

A regulatory framework and contractual mechanism that enables listed SPVs to transition from asset ownership to asset operation upon license expiry, continuing as listed entities through O&M contracts with the government (or its designated entity) rather than through asset ownership. The listed company becomes an O&M service provider earning management fees, preserving a revenue stream and listed status after asset transfer. |

This solution addresses the terminal value problem by creating an alternative business model for post-transfer periods. Current law (Clause 6.5.1 of Hydropower Development Policy, 2001) grants the previous operator priority for continuing operations after transfer, but this provision has no regulatory framework or listed company adaptation. The operator contract solution explicitly structures this priority right into a continuing listed entity: when the asset transfers, the entity continues as an O&M contractor earning fees based on capacity, energy generation, or availability. The solution is elegant because it leverages existing legal provisions rather than requiring new legislation, transforms a forced transfer into a negotiated continuation, and preserves both investor capital and listed entity status. International precedent from airport and toll road concessions demonstrates that operator models successfully maintain private sector participation after public reversion. The solution is particularly appropriate for Nepal’s context because the private sector has developed operational expertise over 30+ years of BOOT projects—the same entities that built the assets are best positioned to operate them efficiently. |

Implementation requires coordinated regulatory action across multiple ministries and agencies. The Ministry of Energy should issue the BOOT Transition Framework Regulations, establishing: (a) standard O&M contract terms for post-transfer operations; (b) fee calculation methodology (capacity-based, energy-based, or availability-based); (c) contract duration (typically 10 to 15 years with renewal options); (d) performance standards and penalty provisions; and (e) dispute resolution mechanisms. SEBON should issue listing rule amendments permitting listed entities to continue trading after asset transfer if O&M contracts are in place, with appropriate disclosure requirements for contract terms and fee projections. The Nepal Electricity Authority should develop standardized O&M procurement processes for transferred assets, with priority to previous operators who built operational familiarity. Implementation should begin with pilot projects: companies with licenses expiring in the next 10 to 15 years should begin government negotiations now, establishing template contracts that other projects can follow. The Hydropower Association should develop industry-standard O&M contract templates to reduce negotiation costs and establish market norms. Implementation timeline is 12 to 18 months for regulatory framework, with company-specific negotiations proceeding over the remaining license life. |

The primary challenge involves government capacity and willingness to negotiate. The MoEWRI, NEA and ERC have limited experience with O&M contracting, and government bureaucracy may resist taking on procurement responsibilities that were previously unnecessary (assets transferred automatically). Political risk is significant: successive governments may refuse to honor predecessor commitments, particularly if O&M fees appear excessive in retrospect. A second challenge involves fee adequacy. O&M contracts generate substantially lower margins than asset ownership—the return on equity for a pure O&M business is typically lower than 8% compared to 15% to 20% for ownership operations (along with equity upside). This margin compression reduces shareholder returns and may not preserve par value. Third, the solution creates dependency on government procurement decisions. If the government chooses to operate transferred assets directly rather than contracting the previous operator, the continuity mechanism fails. Fourth, the priority right in Clause 6.5.1 is not exclusive—the government can choose any operator, not necessarily the previous one. Securing actual contracts requires competitive positioning and relationship management, not merely relying on legal priority. Finally, listed entity viability after transfer depends on O&M fee volume. Small projects may not generate sufficient fees to justify listed entity maintenance, leading to delisting and forced shareholder liquidation even with O&M contracts in place. |

|

Strict Ring-Fencing of Inter-SPV Investments |

A regulatory framework limiting the amount and conditions under which listed hydropower SPVs can invest retained earnings or raised capital into new subsidiary SPVs, affiliated projects, or related-party ventures. Limits would be expressed as percentages of free cash flow rather than equity, require shareholder approval for investments above thresholds, mandate separate financial reporting for invested entities, and establish clear ring-fencing to prevent cross-subsidization and risk contamination. |

This solution addresses the systematic risk migration from inter-SPV capital flows that currently transforms mature, low-risk operating assets into construction-risk funding sources. Under current practice, companies like Arun Valley (AHPC), Ridi Power (RIDI), and Api Power (API) have redirected substantial capital from operational projects into new construction through rights issuances and retained earnings. This practice breaks project-level risk isolation, misleads investors who purchase shares expecting stable dividend yields, and creates opacity that prevents accurate valuation. The strict ring-fencing solution restores the intended function of SPV structures: each listed company should stand on its own project economics, with diversification achieved through holding company structures (requiring investor consent) rather than through cross-investment (which often occurs without full disclosure). International precedent from infrastructure finance demonstrates that strict ring-fencing is essential for project finance viability—cross-subsidization between projects violates the risk allocation principles on which lender pricing depends. The solution is particularly urgent in Nepal because inter-SPV investment has become the dominant capital strategy, with over 70% of recent rights issuances indicating “new project investment” as a primary use of funds. |

Implementation requires SEBON and NRB joint action: SEBON and ERC through amendments in its regulations establishing inter-SPV investment limits, and NRB through Unified Directive amendments establishing banking limits on cross-SPV exposure. The regulatory framework could specify provisions along the line of: (a) maximum inter-SPV investment of 30% of free cash flow (not paid-up capital) per fiscal year; (b) mandatory special resolution approval for investments exceeding 10% of free cash flow; (c) requirement for independent valuation opinion for invested SPVs; (d) prohibition on guaranteeing subsidiary debt using parent assets; and (e) public disclosure of investment rationale, projected returns, and risk factors. |

The most significant challenge involves definitional complexity: distinguishing “inter-SPV investment” from legitimate business development activities. Companies legitimately expand into new projects, and distinguishing growth-oriented investment from risk-diversion requires careful regulatory design. Overly restrictive rules may prevent efficient capital allocation; under-restrictive rules fail to address the core problem. Secondly, the solution conflicts with the holding company development pathway that many companies are pursuing. If Chilime (CHCL) is the successful model, preventing other companies from following similar paths may limit future market development. Thirdly, companies may structure around limits through off-balance-sheet arrangements, related-party loans that technically fall outside “investment” definitions, or corporate restructurings that create affiliated entities outside regulatory scope. Finally, the aggressive rights issuance pattern suggests companies face genuine capital requirements—debt repayment, working capital, construction financing—that may not be satisfiable without inter-SPV fund flows. Simply prohibiting the behavior without addressing underlying capital needs may trigger liquidity crises. |

|

Instrument Conversion Near License Maturity |

A regulatory mechanism mandating automatic conversion of public ordinary shares into redeemable preference shares or fixed-yield instruments once remaining license life falls below a specified threshold (typically 10 to 15 years). The converted instruments would carry guaranteed dividends, priority in liquidation, and defined redemption values, gradually removing equity-like risk as terminal risk increases. |

This solution addresses the late-stage exposure problem by structurally transforming the investment instrument as license expiry approaches. Under current structure, retail investors hold perpetual ordinary shares regardless of remaining project life—someone purchasing shares in a project with 5 years remaining faces identical instrument risk as someone purchasing shares in a project with 25 years remaining. The equity conversion solution creates a graduated risk reduction: early-stage investors enjoy equity upside and dividend growth; late-stage investors receive preference shares with guaranteed yields and defined redemption values. The mechanism is conceptually similar to amortizing bonds, where principal is systematically returned over the instrument’s life rather than all at maturity. International precedent from infrastructure finance in developing markets demonstrates that maturity-contingent instrument structures successfully manage terminal risk—Mexico’s renewable energy certificates and Chile’s mining royalties both incorporate maturity-based transformations. The solution is particularly effective because it operates at the instrument level rather than requiring fundamental restructuring of project economics or corporate governance. |

Implementation requires SEBON to issue the Concession Equity Conversion Regulations, establishing: (a) trigger threshold (10 years remaining license life); (b) conversion ratio (par value preservation or slight premium); (c) preference share terms (dividend rate, cumulative vs. non-cumulative, redemption schedule); (d) conversion mechanics (automatic upon regulatory certification of license status); and (e) trading restrictions post-conversion (preference shares may trade on separate market or with price bands). The regulations should specify transition provisions: for existing listed companies, conversion would occur on the later of regulatory effective date or the 10-year threshold date. For new listings, conversion would occur automatically at the threshold date regardless of subsequent market conditions. ERC should issue guidelines for institutional investor treatment of converted preference shares, including capital adequacy and concentration limits. The conversion mechanism should be tested through pilot implementation with companies having licenses expiring in 2035 to 2038. |

The primary challenge involves market acceptance. Preference shares with guaranteed yields and defined redemption values are a fundamentally different investment proposition than ordinary equity. Retail investors accustomed to dividend growth and mainly capital appreciation may resist conversion, particularly if preference share pricing implies significant value reduction. A second challenge involves conversion pricing and valuation disputes. Determining fair conversion ratio requires projecting remaining cash flows, discounting at appropriate rates, and allocating value between ordinary and preference shareholders. Sophisticated parties will dispute these calculations, potentially triggering litigation that delays implementation. Third, the solution may create perverse incentives. If companies know conversion is mandatory at 10 years, they may accelerate value extraction in years 11 through 20, reducing long-term project maintenance or deferring necessary capital expenditure to maximize short-term dividends. The conversion trigger creates a “use it or lose it” dynamic that may harm long-term asset quality. Fourth, the preference share market in Nepal is underdeveloped. Creating a viable secondary market for converted instruments requires similar market makers, and sufficient trading velocity all of which are currently absent. Finally, regulatory complexity is substantial: the conversion mechanism must address multiple edge cases including license extensions, partial transfers, and corporate restructuring during the conversion window. |

|

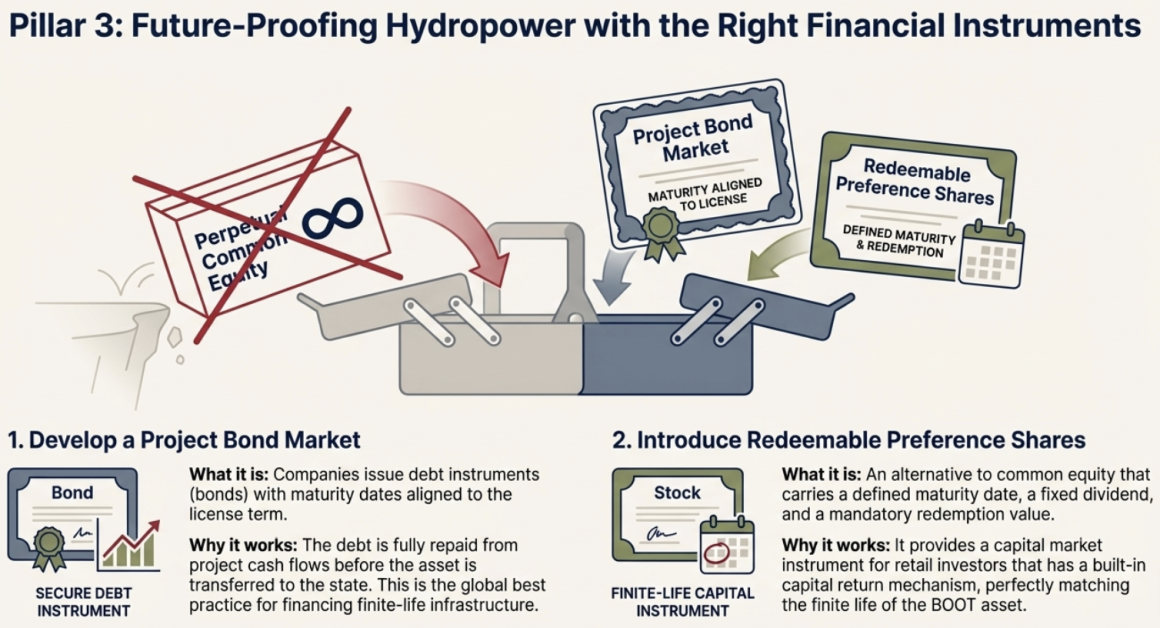

Replace Equity Issuance by Redeemable Preference Shares or Fixed-Yield Instruments |

A structural shift from ordinary equity IPOs and rights issuances toward preference shares, participating debentures, or other fixed-yield instruments for retail investor capital raising. These instruments would carry defined maturity dates (aligned with license life), guaranteed or participating dividends, priority in liquidation, and mandatory redemption at par or premium upon license expiry. The solution transforms the fundamental instrument structure from “perpetual ownership” to “maturity-matched debt-like investment.” |

This solution addresses the core instrument mismatch by replacing the inappropriate equity form with a more suitable instrument. Perpetual ordinary shares are appropriate for businesses with indefinite life; finite-concession hydropower assets require instruments with defined maturities and redemption mechanisms. Preference shares and participating debentures provide guaranteed returns, priority liquidation treatment, and maturity features that align investment economics with asset reality. The solution is conceptually simple but structurally transformative: rather than fixing the equity instrument through disclosure or conversion, it replaces equity with more appropriate instruments. International precedent from project finance globally demonstrates that debt instruments (bonds, debentures, project finance loans) are the appropriate form for finite-life infrastructure—equity is used only when residual value exists after debt repayment. Nepal’s Hydropower Development Policy, 2001 explicitly mentions mobilization of capital markets through “bonds as well as other financial instruments,” providing policy foundation for the solution. The UK PFI model and Luxembourg infrastructure bonds both demonstrate successful debt issuance for finite-concession assets. |

Implementation requires coordinated regulatory action: SEBON must develop preference share and participating debenture frameworks for hydropower issuers; Ministry of Finance should provide tax treatment clarity and waivers (e.g. preference dividends are not tax-deductible, affecting cost of capital); and NEPSE and SEBON must strengthen market for trading fixed-yield instruments. The implementation pathway should be: Phase 1 (immediate): Allow preference shares as alternative to ordinary equity for new issuers, with enhanced disclosure requirements and regulatory approval. Phase 2 (within 18 months): Require preference shares for projects with less than 20 years remaining license life. Phase 3 (within 36 months): Permit ordinary equity only for holding companies meeting diversification thresholds; single-asset SPVs must use preference shares or debt instruments. |

The most significant challenge involves investor expectations and market culture. Nepal’s retail investor base has been conditioned to expect ordinary equity with dividend growth potential. Preference shares with fixed yields represent a fundamentally different value proposition that may not appeal to the same investor base. If retail investors reject preference shares, companies may face capital-raising difficulties that slow hydropower development. A second challenge involves cost of capital. Preference dividends are not tax-deductible (unlike interest payments), making preference shares more expensive than debt. For projects already facing cost challenges, this increased financing cost may affect viability. Third, the solution may reduce promoter control. Preference shareholders arranged to receive governance rights including board representation and veto powers over certain transactions reduces the promoter control. Promoters accustomed to unfettered control may resist instruments that constrain their autonomy. Fourth, secondary market development currently designed for equity trading requires exchange modifications, market maker networks, and price discovery mechanisms. Fifth, the solution applies only to new issuances—existing ordinary shares remain outstanding, creating parallel markets and potential regulatory complexity. |

|

Promoter Lock-in Redesign |

An extension and restructuring of the existing three-year promoter lock-in period to create graduated lock-in that increases as projects approach license expiry. Early-stage promoters (construction phase) would face shorter lock-ins to facilitate capital recycling; late-stage promoters (operational phase) would face extended lock-ins or prohibited exits to prevent strategic abandonment of aging assets. The redesign aligns promoter incentives with long-term project stewardship rather than early exit. |

This solution addresses the promoter exit problem that systematically transfers terminal risk from insiders to retail investors. Under current regulations, promoters hold shares for three years from IPO, then can freely sell regardless of remaining project life. This creates perverse incentives: promoters invest construction capital, de-risk the project, extract maximum value through share sales at market peaks, and exit before the BOOT transfer date leaves retail investors holding doomed equity. The redesigned lock-in creates alignment: promoters who benefit from the project’s operational cash flows must remain invested through those flows, rather than monetizing future cash flows through secondary market sales. International precedent from infrastructure finance demonstrates that sponsor retention requirements—extended hold periods, clawback provisions, and minimum ownership thresholds—are essential for preventing adverse selection. The solution is particularly relevant for Nepal because the three-year lock-in has been systematically ganged: promoters time their exits precisely when construction de-risking aligns with market enthusiasm, leaving retail investors as “greater fools” who purchase at peak valuations. |

Implementation requires SEBON to amend Rule 38 of the Securities Registration and Issuance Regulation, 2073 to establish graduated lock-in provisions. The framework should specify: (a) minimum promoter holding requirement; (b) prohibition on promoter share sales in final 10 years of license life; (c) graduated lock-in for new issuers based on license maturity at listing; (d) clawback provisions for promoter shares sold at prices exceeding fair value (as determined by independent valuation); and (e) exception for transfers to affiliated entities meeting the same holding thresholds. The dual ISN system currently being developed by SEBON would support implementation by tracking promoter share locations separately from public float even when trading under the same parameters. |