Somewhere in an office in Hong Kong, a team of sovereign analysts runs a regression model across 18 economic variables, reads a set of government documents, meets with finance ministry officials and commercial bankers, and then issues a two-character verdict: BB-. That verdict – published by Fitch Ratings in November 2024 and affirmed in November 2025 – is Nepal’s first-ever sovereign credit rating.

Most Nepalis have never heard of it. Most investors in New York, London, and Singapore noticed it immediately.

We will discuss that gap here in this post. The rating matters not as an abstraction but as a number that affects what the Government of Nepal pays every time it borrows, what an international infrastructure fund sees when it types “Nepal” into its screening tool, and whether the hydropower projects sitting in licensing pipelines ever get financed. Understanding it – and understanding why Nepal received the rating it did, what it gets right, and what it gets wrong – is not just a task for the Ministry of Finance. It is useful for anyone who works in Nepal’s economy.

1. What a Sovereign Credit Rating Is – and Who Issues Them

The definition

A sovereign credit rating is a forward-looking opinion on a government’s capacity and willingness to repay its debt obligations to private creditors, in full and on time. It is emphatically not a rating of the whole economy, or of the country as a place to do business, or of social development. It is specifically, narrowly about one question: if a government borrows money from international capital markets, how confident can lenders be that they will be repaid?

The word willingness matters as much as capacity. Governments cannot be taken to bankruptcy court the way a company can. They can choose not to pay. History is full of sovereign defaults – Argentina, Greece, Sri Lanka – where the government had some capacity to service debt but made a political decision not to, or lost access to financing because investors stopped believing it would. Rating agencies try to assess both dimensions simultaneously.

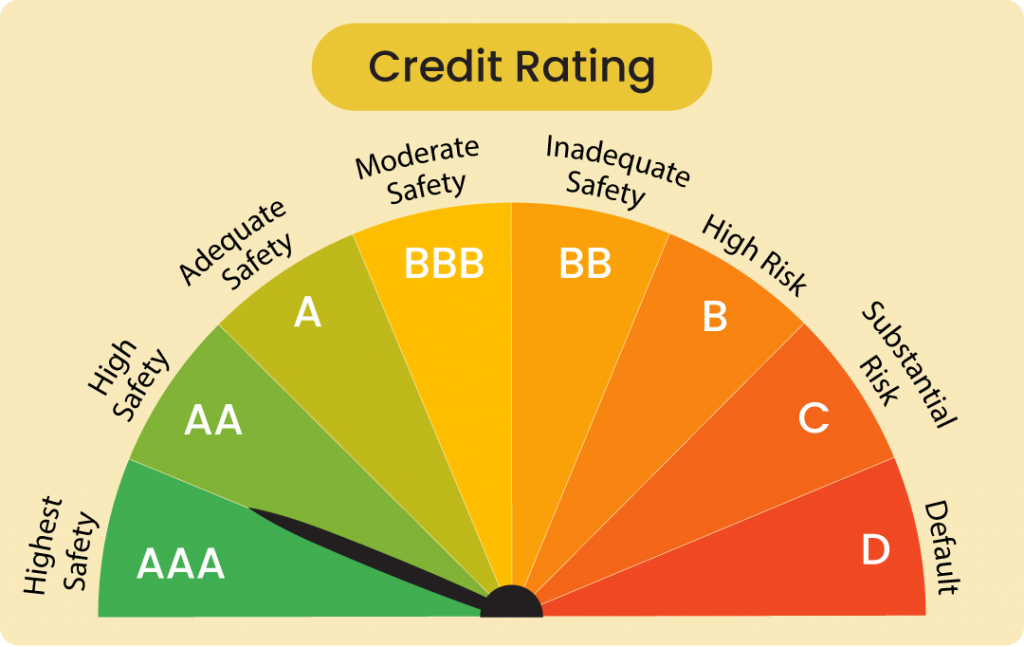

The rating scale

The industry uses a standardised letter-grade scale. Fitch’s scale, which Nepal is now part of, runs as follows:

| Rating | Category | What it means |

| AAA | Investment Grade | Highest credit quality; essentially zero default risk |

| AA+, AA, AA- | Investment Grade | Very high credit quality |

| A+, A, A- | Investment Grade | High credit quality |

| BBB+, BBB, BBB- | Investment Grade | Good credit quality; lowest investment-grade tier |

| BB+, BB, BB- | Speculative Grade | Elevated vulnerability; financial flexibility exists |

| B+, B, B- | Speculative Grade | Highly speculative; significant credit risk |

| CCC+, CCC, CCC- | Speculative Grade | Substantial credit risk |

| CC | Speculative Grade | Very high levels of credit risk |

| C | Speculative Grade | Near default |

| RD | Default | Restricted Default – defaulted on some, not all, obligations |

| D | Default | Default |

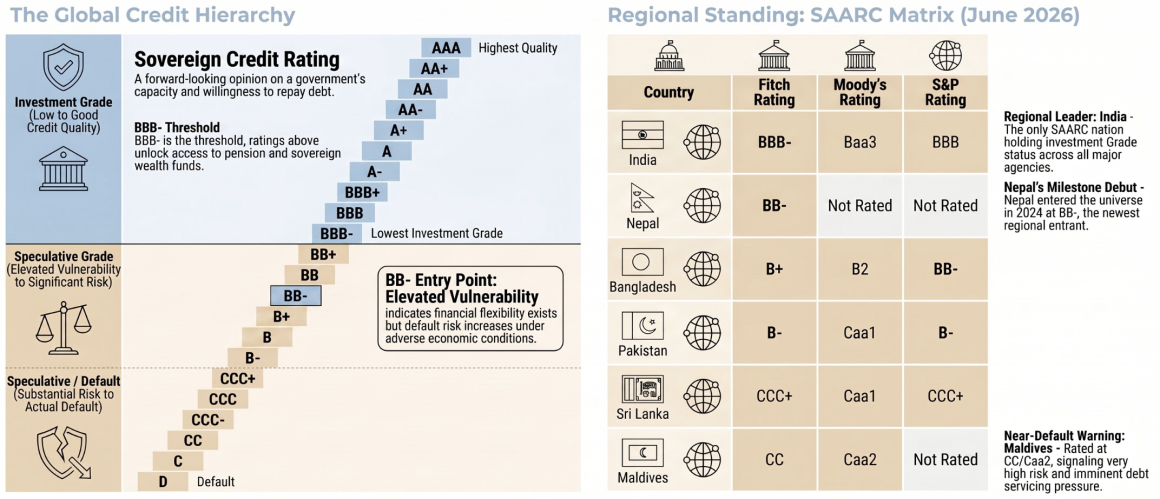

Nepal sits at BB- the entry level of the speculative, or “sub-investment-grade,” category. That sounds alarming, but it is important to contextualise. BB- means: elevated vulnerability to default risk, particularly under adverse conditions, but the government has financial flexibility that supports debt servicing. For a country that had never previously accessed international capital markets, a first-time BB- rating is a credible outcome. It is not, however, the destination.

The critical threshold above Nepal is BBB- the lowest investment-grade rating. Investment-grade status unlocks a fundamentally different investor base: sovereign wealth funds, pension funds, and insurance companies that are mandated by their own rules to hold only investment-grade assets. Getting from BB- to BBB- is the structural aspiration that should frame Nepal’s credit narrative.

A brief history

Sovereign credit ratings became systematic in the 1970s as the Eurodollar bond market expanded and governments began borrowing internationally in larger volumes. They became indispensable after the Latin American debt crisis of the 1980s, when investors discovered, painfully, that they had no reliable framework for distinguishing between sovereign borrowers. By the 2000s, a sovereign without an international credit rating was effectively invisible to the mainstream international capital market.

The three major agencies – and why they dominate

Three agencies – Fitch Ratings, Moody’s Investors Service, and Standard & Poor’s (S&P) – account for the overwhelming majority of sovereign credit opinions that matter to international investors. The reason is not quality of analysis alone; it is regulatory architecture. Banking regulations in the United States, Europe, and most of Asia require institutions to hold assets rated by a “Nationally Recognised Statistical Rating Organisation” (NRSRO) or its international equivalent. The Big Three hold those designations. An opinion from a smaller or regional agency – however rigorous – does not trigger the same capital-market access.

The three agencies differ in methodological emphasis. Moody’s places relatively greater weight on economic resilience and the structure of the debt stock. S&P emphasises the monetary policy framework and exchange rate flexibility. Fitch – which Nepal chose – weights governance and structural features most heavily in its quantitative model, as we will see. There is no universally “correct” choice; different agencies can and do assign different ratings to the same sovereign.

Solicited vs unsolicited ratings

Nepal’s rating is solicited: the Government of Nepal formally engaged Fitch, paid for the rating process, provided data and participated in due-diligence meetings with analysts. This is the standard model for most sovereign ratings and carries meaningful implications – the issuer gets to review and respond to draft analysis before publication, and the relationship becomes an ongoing engagement rather than a one-off event. Unsolicited ratings, which agencies sometimes issue based on public data alone, are generally viewed as less reliable and are given less weight by investors.

The regional picture

Of the eight South Asian sovereigns, most have held ratings from at least one major agency for years – India, Pakistan, Bangladesh, Sri Lanka, and the Maldives all had ratings before Nepal. Nepal was the last significant South Asian economy to seek a first-time rating. The delay reflected both the limited immediate need (Nepal did not need to borrow commercially) and the political complexity of submitting to external assessment. The decision to seek a rating now reflects a structural shift: Nepal recognises that the hydropower export economy and post-LDC financing requirements demand access to international capital markets that only a credit rating can unlock.

SAARC Sovereign Credit Ratings – June 2026

| Country | Fitch | Moody’s | S&P | Grade | Notes |

| India | BBB- Stable (Aug 2025) | Baa3 Stable (current) | BBB Stable (Aug 2025) | ✅ Investment grade (all three) | S&P raised India’s long-term sovereign credit rating by one notch to BBB from BBB-, its first sovereign upgrade in 18 years, in August 2025. Fitch and Moody’s remain at lowest investment grade. |

| Bangladesh | B+ Stable (May 2024) | B2 Negative (2024) | BB- (affirmed Jul 2025) | ❌ Speculative grade | Fitch downgraded Bangladesh to B+ from BB- in May 2024 citing weakening external buffers and falling FX reserves. S&P affirmed Bangladesh’s sovereign credit rating in July 2025, noting stabilised external profile and increased FX reserves. |

| Pakistan | B- Stable (Apr 2025) | Caa1 Stable (Aug 2025) | B- Stable (Jul 2025) | ❌ Speculative grade | Fitch upgraded Pakistan to B- in April 2025; S&P raised Pakistan’s rating to B- on July 24, 2025. Moody’s upgraded Pakistan to Caa1 from Caa2 in August 2025, citing improving external position under IMF oversight. All three upgraded in 2025. |

| Sri Lanka | CCC+ Stable (Oct 2025) | Caa1 Stable (Dec 2024) | CCC+ Stable (2025) | ❌ Speculative grade (deep) | Fitch affirmed Sri Lanka at CCC+ in October 2025, noting debt burden remains a key constraint with government debt-to-GDP projected at ~96% in 2027. Recovering from 2022 default. |

| Nepal | BB- Stable (Nov 2025) | Not rated | Not rated | ❌ Speculative grade | First-ever rating assigned November 2024. Only rated by Fitch. |

| Maldives | CC (Jun 2025) | Caa2 (Sep 2024) | Not rated | ❌ Speculative grade (near default risk) | Fitch maintained Maldives’ sovereign rating at CC in June 2025, citing rising external debt obligations and default risk. The government faces USD 688 million in debt servicing in H2 2025, rising sharply to USD 1.1 billion in 2026 including a USD 500 million sukuk repayment. |

| Bhutan | Not rated | Not rated | Not rated | – | No Big Three rating. Financed primarily through bilateral concessional lending from India. |

| Afghanistan | Not rated | Not rated | Not rated | – | No functioning sovereign credit relationship with international capital markets under current governance. |

Three observations worth noting:

- Nepal is the newest entrant into the SAARC ratings universe (2024), and the only country with a single-agency rating – giving it a specific engagement agenda: eventually seeking a second rating from Moody’s or S&P for redundancy and broader investor access.

- India’s S&P upgrade to BBB in August 2025 is the biggest rating event in the region in years – it moves India one notch above Nepal’s BB- across three investment-grade notches, though Fitch still holds India at BBB- (same lowest investment grade level as before, same agency as Nepal’s rating).

- The Maldives at CC is the clearest cautionary tale in the neighbourhood – a tourism-dependent small island economy with debt service obligations that dwarf its usable reserves, illustrating precisely the kind of external fragility Nepal must avoid by building and maintaining its reserve buffer.

2. Nepal’s Historic Milestone – The 2024 Rating and What It Means

Why now

Three factors converged to make 2024 the moment:

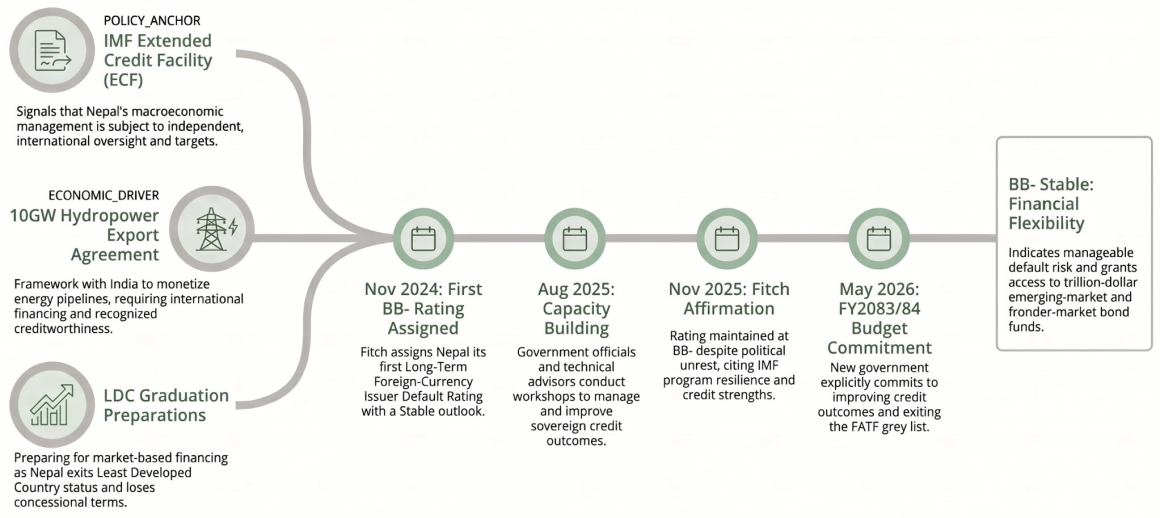

The IMF Extended Credit Facility (ECF): Nepal has had an active ECF arrangement with the IMF since early 2022, initially to address post-pandemic imbalances. The ECF functions as a policy anchor – it requires Nepal to meet fiscal and monetary targets under international scrutiny, and its presence signals to rating agencies that macroeconomic management is subject to independent oversight. Strong IMF programme performance directly reinforced the credit case.

Hydropower and the India electricity agreement: Nepal signed a framework with India in 2023 targeting 10GW of electricity exports over the next decade. Monetising that pipeline requires international financing – and international financing requires an internationally recognised credit rating.

LDC graduation: Nepal qualifies for graduation from Least Developed Country status. Graduation means losing preferential trade access and concessional financing terms. The credit rating is, in part, a preparatory step for the market-based financing environment that will follow.

The timeline

- November 2024: Fitch assigns Nepal its first Long-Term Foreign-Currency Issuer Default Rating (LT FC IDR) of BB- with a Stable outlook (Fitch press release, November 2024)

- August 2025: Nepal holds a Sovereign Credit Rating Capacity Building workshop with government officials and technical advisors

- September 2025: Youth-led political unrest; the government is overthrown; interim administration installed; elections announced for March 2026

- November 2025: Fitch affirms Nepal at BB- Stable, noting political uncertainty as a heightened risk but citing IMF programme resilience and credit strengths as offsetting factors (Fitch affirmation, November 2025)

- May 2026: New government presents FY2083/84 budget with explicit commitment to improve sovereign credit rating outcomes and exit FATF grey list

What BB- Stable actually means in practice

For the government, BB- means that international bond issuance is possible but expensive. A rough rule of thumb: each notch below investment-grade adds approximately 50–150 basis points to sovereign borrowing costs. For a hypothetical 10 year USD 500 million Eurobond, the difference between Nepal’s BB- and an investment-grade BBB- rating translates to roughly USD 25–75 million per year in higher interest costs, compounded over the bond’s life.

For investors, BB- means Nepal is now on their radar. It is too risky for the most conservative mandates but squarely within the universe of emerging-market and frontier-market bond funds, which collectively manage trillions of dollars globally. Nepal’s BB- rating makes it comparable to countries like Bolivia, Honduras, and Senegal in terms of investor category.

For the Stable outlook: Fitch does not expect a rating change in the next 12–24 months. The Stable outlook is a signal of equilibrium, not momentum. It does not mean things are improving – it means they are not expected to deteriorate enough for a downgrade, nor improve enough for an upgrade, in the near term. Nepal’s task is to convert Stable into Positive.

3. How Fitch Arrives at a Rating – The Methodology Explained

This section draws on Fitch’s publicly available Sovereign Rating Criteria, most recently updated in April 2026. Anyone who wants to understand how Nepal’s rating is built should read that document.

Before I rewrite this, I need to pull the individual variable weights from the Fitch criteria document – I know WBGI is ~22% of total model weight, but I don’t want to estimate the other 17. Let me read the source document directly.I now have every variable weight directly from Fitch’s Sovereign Rating Criteria (April 2026). Here is the complete rewritten section with the weight column added from the source document.

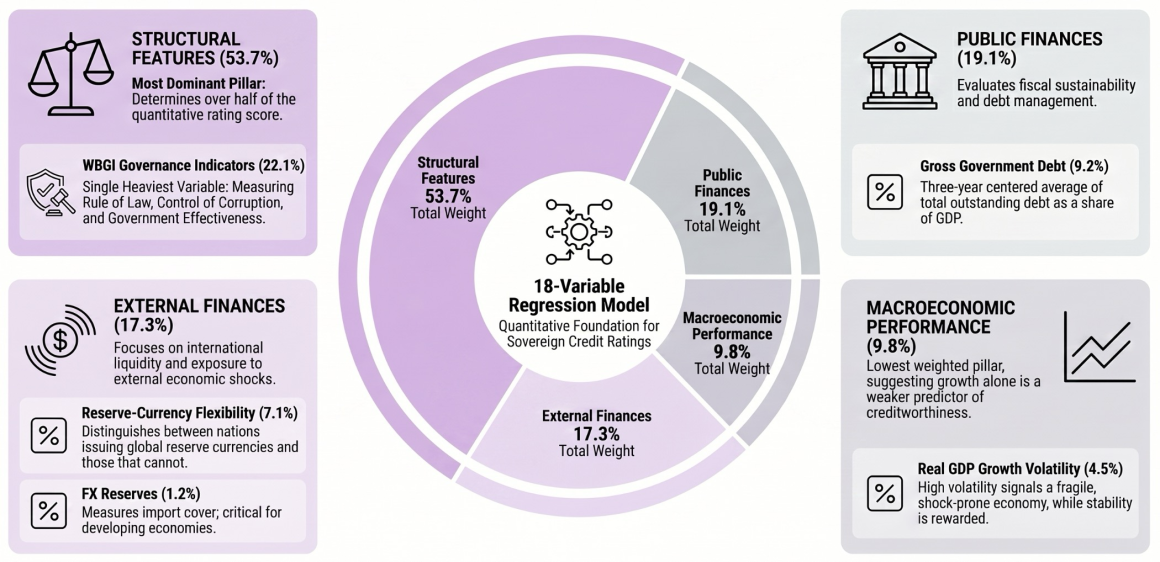

The Sovereign Rating Model (SRM)

Fitch’s starting point is a quantitative model – the Sovereign Rating Model or SRM. It is a multiple-regression Ordinary Least Squares model estimated from rating data across all Fitch-rated sovereigns going back to 2000. It takes 18 input variables across four analytical pillars, and produces an output score calibrated to the rating scale. The model is re-estimated annually to incorporate new data. All weights and coefficients below are sourced directly from Fitch’s Sovereign Rating Criteria, April 2026.

Pillar 1: Structural Features – 5 variables | 53.7% of SRM

| # | Variable | Weight | What it measures | Nepal’s position |

| 1 | Governance indicators (WBGI composite) | 22.1% | Average of six World Bank Governance Indicators – Rule of Law, Control of Corruption, Government Effectiveness, Voice & Accountability, Regulatory Quality, Political Stability. The single heaviest variable in the entire model. | Negative – 33rd–34th percentile vs BB median ~44th. Government Effectiveness and Regulatory Quality are the weakest sub-dimensions. |

| 2 | Share in world GDP | 14.5% | The sovereign’s weight in global economic output. Captures the vulnerability of very small economies to external shocks – a small economy has fewer buffers and less systemic importance. | Negative – Nepal’s share of world GDP is negligible (~0.05%). A structural penalty that cannot be changed in the short run. |

| 3 | GDP per capita (percentile rank) | 11.7% | Nepal’s GDP per capita ranked against all Fitch-rated sovereigns – not the raw dollar amount, but where it sits in the distribution. Percentile rank eliminates the upward drift in nominal incomes over time. | Strongly negative – ~USD 1,548–1,658 places Nepal at roughly the 5th–6th percentile among all rated sovereigns. Only improvable through sustained multi-year growth. |

| 4 | Years since default or restructuring event | 4.3% | A non-linear, time-decaying function that penalises sovereigns with recent debt-event history. The penalty halves approximately every 4.3 years. | Negative (QO-corrected) – Nepal’s DSSI participation in 2020 reset this variable and triggered a ~1.7 notch model penalty. Fitch applied a +1 QO notch to correct for this mechanical artefact. The penalty fades and will become effectively neutral by approximately 2028–2029. |

| 5 | Broad money supply (% of GDP) | 1.1% | Proxy for financial sector depth and intermediation capacity. High broad money relative to GDP indicates a deeper banking system capable of absorbing shocks and channelling savings. | Strongly positive – Nepal’s broad money is approximately 114.5% of GDP vs the BB median of ~49%. One of Nepal’s clearest model strengths, reflecting deep banking penetration driven by remittance inflows. |

Pillar 2: Macroeconomic Performance – 3 variables | 9.8% of SRM

| # | Variable | Weight | What it measures | Nepal’s position |

| 6 | Real GDP growth volatility | 4.5% | Exponentially weighted standard deviation of real GDP growth over a rolling window. Higher volatility signals a more fragile, shock-prone economy. The most recent year accounts for 15% of the calculation; the most recent 10 years account for 80%. | Positive – Nepal’s growth volatility score of ~2.7 is better than the BB median of ~3.0. Despite political instability, growth has been relatively stable, cushioned by the countercyclical buffer of remittances. |

| 7 | Consumer price inflation | 3.6% | Three-year centred average of CPI inflation, truncated between 2% and 50%. Both high inflation and deflation score negatively; the model rewards price stability. | Now positive – IMF projects inflation at 4.1–4.2% for 2025–2026, below the BB peer median of ~4.8%. A recent improvement; the prior 3-year average of ~6.4% had been a mild drag. The improvement should register in the next SRM re-estimation in July 2026. |

| 8 | Real GDP growth | 1.7% | Three-year centred average of real GDP growth. The lowest individual weight in the entire model – reflecting that growth alone is a weak predictor of creditworthiness compared to its volatility and the structural features that enable it. | Broadly neutral – 3-year average around 3–4% depending on the window. FY26 growth projected at 2.3–4.3% (World Bank/IMF range). Medium-term potential of ~5% is the positive story Fitch anchors. |

Pillar 3: Public Finances – 4 variables | 19.1% of SRM

| # | Variable | Weight | What it measures | Nepal’s position |

| 9 | Gross general government debt / GDP | 9.2% | Three-year centred average of total outstanding government debt as a share of GDP. The largest single variable in the public finances pillar – capturing fiscal sustainability and the scale of future repayment obligations. | Positive – ~46–50% of GDP (Fitch: 46.1% for FY26; IMF: ~49.9%) vs BB median of ~54%. A genuine strength. Further improvement requires revenue growth, not just borrowing restraint. |

| 10 | Government interest payments / revenue | 4.6% | Three-year centred average of the share of government revenue consumed by interest on debt. A high ratio crowds out spending and signals eroding fiscal space. | Positive – approximately 7.5% of revenues vs BB median of ~8.4%. The concessional nature of Nepal’s external debt (average ~1% interest rate, 13-year maturity) keeps this ratio low. Watch item: rising domestic borrowing at commercial rates could pressure this ratio over time. |

| 11 | FC government debt / gross government debt | 3.2% | Three-year centred average of the share of government debt denominated in foreign currency. High FC debt exposes the sovereign to exchange-rate risk – depreciation automatically raises the domestic-currency debt burden. | Moderate / neutral – FC share is roughly 45–50% of total debt (external debt ~23% of GDP, mostly multilateral). Partially offset by the concessional and long-maturity structure, and by the rupee peg to the Indian rupee which limits FX volatility risk. |

| 12 | General government fiscal balance / GDP | 2.1% | Three-year centred average of the overall budget surplus or deficit as a share of GDP. A persistent, widening deficit signals fiscal slippage. | Slightly negative – deficit of ~3.5–3.7% of GDP in FY26 (Fitch: ~3.5%; IMF: ~3.66%) vs BB median of ~3.0%. Not alarming in isolation, but slightly above the peer average with no medium-term numerical consolidation target anchoring the trajectory. |

Pillar 4: External Finances – 6 variables | 17.3% of SRM

| # | Variable | Weight | What it measures | Nepal’s position |

| 13 | Reserve-currency flexibility | 7.1% | Whether the sovereign issues debt in a global reserve currency (USD, EUR, GBP, JPY, CHF). Reserve-currency issuers face no refinancing risk – they can print to repay. The highest-weighted variable in this pillar and one of the key structural divides in sovereign ratings globally. | Negative – Nepal does not and cannot issue in a reserve currency. A fixed structural penalty shared by virtually all developing economies; no policy intervention can change it. |

| 14 | Sovereign net foreign assets / GDP | 7.5% | Three-year centred average of government external financial assets minus external liabilities as a share of GDP. A creditor position is rare and highly valued. | Strongly positive – Nepal is a net external creditor at approximately +13–15% of GDP. The BB median country is a net debtor at approximately -12% of GDP. Nepal sits on the opposite side of this ledger – an unusual and material strength. |

| 15 | Commodity dependence | 1.0% | Share of commodity exports (oil, minerals, agricultural commodities) in total current external receipts. High dependence exposes the country to commodity price swings beyond its control. | Strongly positive – Nepal’s commodity dependence is approximately 5.8% of current external receipts vs the BB median of ~21.6%. Nepal exports carpets, garments, and electricity – not extractives. A structural advantage most peers do not share. |

| 16 | FX reserves (months of current external payments) | 1.2% | Gross foreign exchange reserves relative to prospective imports of goods and services. The standard metric of external liquidity adequacy. Applies only to countries without reserve-currency flexibility. | Strongly positive – 18.4 months of import cover as of mid-April 2026 (NRB data) vs BB median of ~4.8 months. Nepal’s reserve coverage is nearly four times the peer median. This is the single most dramatic outperformance across all 18 variables – though its low model weight (1.2%) means the rating gain is smaller than the raw number implies. |

| 17 | External interest service / current external receipts | 0.2% | Three-year centred average of the share of export earnings and remittances consumed by servicing external debt. A high ratio signals vulnerability – the country is earning just enough to cover its external bills. | Positive – Nepal’s ratio is low, reflecting both the concessional structure of external debt (low rates, long maturities) and the very large denominator (remittances alone are ~28–30% of GDP). The lowest-weighted variable in the entire model. |

| 18 | Current account balance + net inward FDI / GDP | 0.4% | Three-year centred average of the combined external financing position – whether the country generates enough from trade, services, and foreign investment to cover its external needs without running down reserves. | Positive – Nepal’s current account registered a surplus of USD 4.32 billion in the nine months to mid-April 2026 (NRB data). Qualifier: FDI inflows remain thin (~0.3–0.5% of GDP), so the positive reading is almost entirely remittance-driven, not productive foreign investment. |

Summary across all 18 variables

| Position | Count | Variables |

| Strongly positive | 4 | Broad money/GDP (1.1%); FX reserves (1.2%); Net foreign assets (7.5%); Commodity dependence (1.0%) |

| Positive | 5 | Growth volatility (4.5%); Inflation – recently (3.6%); Govt debt/GDP (9.2%); Interest/revenue (4.6%); External debt service (0.2%) |

| Neutral / moderate | 2 | Real GDP growth (1.7%); FC debt share (3.2%) |

| Negative | 4 | WBGI (22.1%); World GDP share (14.5%); Reserve-currency flexibility (7.1%); Fiscal balance (2.1%) |

| Strongly negative | 1 | GDP per capita percentile (11.7%) |

| Negative but QO-corrected | 1 | Years since restructuring (4.3%) |

| Positive but remittance-dependent | 1 | Current account + FDI (0.4%) |

Nepal’s four strongest outperformances – reserve coverage (18.4 months), net creditor position, commodity independence, and broad money depth – together carry only 16.8% of total model weight. Nepal’s three largest penalties – governance, world GDP share, and GDP per capita – together carry 48.3% of total model weight. Nepal wins impressively on the variables that matter least to the model, and loses on the variables that matter most. That asymmetry is the entire story of the BB- rating. Rating Framework

The Qualitative Overlay (QO)

No quantitative model can capture everything. Fitch’s second step is the Qualitative Overlay (QO) – a structured system of notch adjustments applied by the rating committee on top of the SRM output. The QO can move the final rating up to +3 or -3 notches from the model output, with each of the four analytical pillars allowing up to ±2 notches of adjustment.

The QO captures factors that are real but not fully quantifiable: the credibility of the monetary policy framework, the risk of contingent liabilities crystallising, the resilience of external financing flows, geopolitical risks, the quality of the business environment. It also allows the committee to correct for cases where the model penalises a country in a way that does not reflect its actual credit standing.

Nepal’s specific QO adjustment

Nepal’s SRM produces an output of B+ – one notch below the published BB- rating. The +1 notch QO adjustment is applied to the structural features pillar, and the reason is specific: when Nepal participated in the G20 Debt Service Suspension Initiative (DSSI) in 2020, the model’s years since default or restructuring event variable was reset. This triggered an automatic penalty of approximately 1.7 notches in the model output – as though Nepal had just defaulted. Fitch’s rating committee judged that this was a mechanical model artefact, not a reflection of Nepal’s actual willingness or capacity to pay private creditors, and corrected for it.

This +1 notch is not permanent or guaranteed. If Nepal’s other structural variables weaken, the committee may decide to let the QO lapse. Conversely, if Nepal’s structural reforms are credibly delivered, the QO could expand. The QO is the most directly actionable lever in the rating.

Why this matters: The entire structure of Fitch’s methodology means Nepal can know, in advance, which variables to move to improve its rating. That is a powerful thing. Most governance challenges feel amorphous. The Fitch framework translates them into specific, measurable variables – WBGI percentiles, revenue/GDP ratios, NPL rates – with quantifiable relationships to the rating outcome.

4. Nepal’s Credit Profile – Where the Numbers Help and Where They Hurt

The strengths

External finances: Nepal’s most surprising competitive advantage

The area where Nepal most dramatically outperforms its ‘BB’ peers is external finances – and the gap is not marginal.

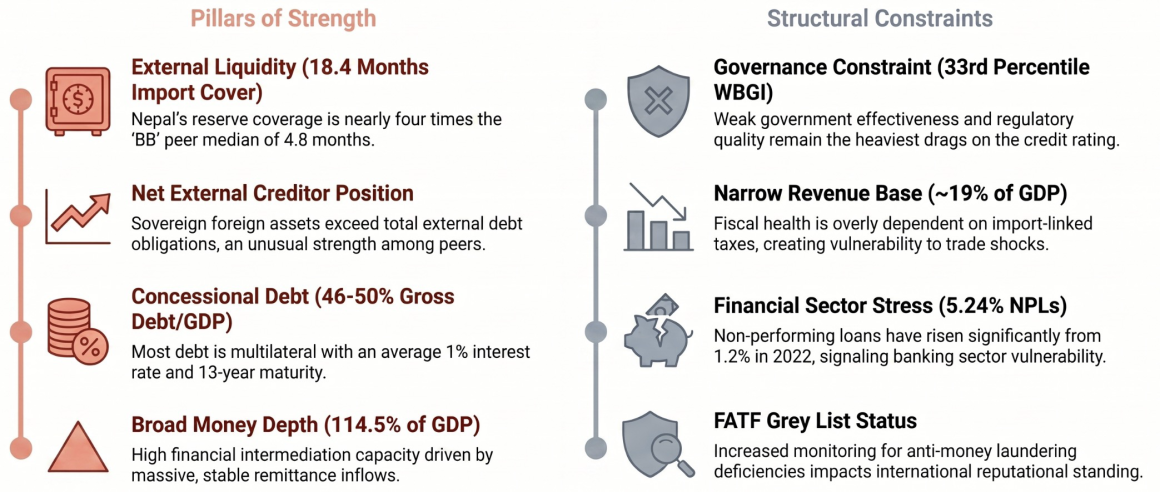

As of mid-April 2026, Nepal’s gross foreign exchange reserves stand at USD 23.55 billion, sufficient to cover 18.4 months of merchandise and services imports (Nepal Rastra Bank, Current Macroeconomic and Financial Situation, May 2026). The ‘BB’ peer median is approximately 4.8 months. Nepal’s reserve coverage is nearly four times the peer average. The World Bank’s April 2026 Nepal Development Update confirms that reserves of USD 22.5 billion at mid-January 2026 exceeded double the NRB’s own 7-month minimum requirement.

Nepal is also a net external creditor – its sovereign foreign assets exceed its external debt obligations. The ‘BB’ median country is a net external debtor. Nepal is on the opposite side of that ledger. This is unusual, and Fitch takes it seriously. Sovereign Net Foreign Assets (SNFA) are defined as official central bank foreign-exchange reserves plus other sovereign external assets less sovereign external debt. Other sovereign external assets include sovereign-controlled external assets (for example held by sovereign wealth funds or public pension funds) that are sufficiently liquid and could support fiscal and current account funding. Sovereign external debt would include liabilities held by non-residents issued by the government, the central bank and other sovereign entities.

Both outcomes flow from the same source: remittances. In FY2024-25, Nepal received USD 12.64 billion in remittances – approximately 28-30% of GDP (NRB data). In the first six months of FY2025-26, remittance inflows surged a further 39.1% year-on-year. This is an extraordinarily large and relatively stable external inflow for an economy of Nepal’s size, and it has built the reserve position that now sits as Nepal’s strongest credit asset.

Public debt: below the peer average and on concessional terms

Nepal’s gross government debt is approximately 46-50% of GDP (Fitch projects 46.1% for FY2026; the IMF’s slightly broader measure comes in at ~49.9%). Either way, it sits comfortably below the ‘BB’ peer median of approximately 54%. Nepal’s provinces and local governments carry zero debt.

More important than the level is the structure. Nepal’s external government debt – approximately 23% of GDP – is almost entirely owed to multilateral (World Bank IDA, ADB) and bilateral creditors, at an average interest rate of approximately 1% and an average maturity of 13 years. These are not commercial terms; they are as close to free money as sovereign debt gets. This means Nepal’s debt affordability is far better than its debt level suggests. Government interest payments are approximately 7.5% of revenues – below the ‘BB’ peer median.

Growth potential: the hydropower story

Nepal’s medium-term real GDP growth potential is estimated at approximately 5% by both Fitch and the World Bank. This is driven by a structural shift: Nepal has become a net electricity exporter and has installed hydropower capacity of over 3GW (as of late 2024), with 10GW under construction license and a further 24GW in earlier stages. A 2024 framework agreement with India targets 10GW of electricity exports over the coming decade. If executed, this transforms Nepal’s external sector from remittance-dependent to energy-exporting – a fundamental change in the country’s economic structure.

Inflation has also dropped sharply. The IMF projects Nepal’s inflation at 4.1% in 2025 and 4.2% in 2026 – now below the ‘BB’ peer median of approximately 4.8%. This is a positive data point for the model’s next re-estimation.

The weaknesses

Governance: the binding constraint

Nepal’s weakest area is simultaneously the area that carries the most weight in Fitch’s model. The composite World Bank Governance Indicator (WBGI) – which alone accounts for approximately 22% of the entire SRM model weight – places Nepal at the 33rd-34th percentile among all countries. The ‘BB’ peer median is approximately the 44th percentile. Fitch assigns Nepal an ESG Relevance Score of ‘5’ for both Political Stability and Rights, and for Rule of Law/Institutional & Regulatory Quality/Control of Corruption – the agency’s signal that these are key rating drivers with a negative credit impact.

The two weakest WBGI sub-dimensions are Government Effectiveness (the capacity to formulate and implement policy, the quality of the bureaucracy, the credibility of the government’s commitment to stated policies) and Regulatory Quality (the ability to formulate regulations that permit and promote private sector development). These are not abstract concepts – they map directly onto the experience of any investor or business trying to operate in Nepal.

What makes this constraint particularly binding is its weight in the model (22%) combined with the speed at which it moves: WBGI indicators reflect perception surveys with a 12-24 month lag, and governance improvements typically appear in ratings over a 3-5 year horizon, not a single budget cycle.

Political instability

Eight changes of government since 2014. The September 2025 youth-led uprising that overthrew the incumbent government. An interim administration, elections in March 2026, and a new political configuration. Fitch explicitly flagged in the November 2025 affirmation that “delays in the political transition and a more fragmented party landscape could undermine policymaking effectiveness and further weaken governance standards.”

In Fitch’s framework, political stability is valued not for its own sake but as a signal of policy predictability. What the agency actually cares about is: will the same core economic and fiscal policies persist through political changes? Nepal’s track record here is mixed but has a genuine strength: there has been broad political consensus on macroeconomic management – IMF engagement, the rupee peg, fiscal conservatism – across coalitions. That consensus, which persisted even through the September 2025 events, is the most important political story to tell Fitch.

Revenue/GDP: the structural fiscal weakness

Government revenues are approximately 19% of GDP – well below the ‘BB’ peer median. Nepal’s tax base is narrow and heavily dependent on import-linked indirect taxes (customs duties, import VAT), which account for approximately 70% of tax revenue. This means that when imports contract – as they did sharply in FY2023 due to foreign exchange pressure – the fiscal position deteriorates rapidly, with little alternative revenue to cushion the shock.

A medium-term Revenue/GDP target of 23%+ has been articulated in government strategy documents. But across a decade of annual budget speeches, not a single one has contained an explicit, binding Revenue/GDP anchor in its narrative text. Fiscal policy is treated as a nominal balancing exercise rather than a structural objective. This is a credibility concern that Fitch will continue to probe.

Financial sector stress

Nepal’s banking sector entered a difficult period following the 2021 credit boom. Non-performing loans have risen to 5.24% of gross loans (NRB data, confirmed by IMF ECF Sixth Review, October 2025) – up from 1.2% in 2022. Average provisioning coverage has dipped to approximately 65%, and commercial banks’ core capital has dropped to around 9.5%. The IMF and World Bank have both flagged continued financial sector vulnerabilities as a key downside risk.

Nepal was added to the FATF grey list in February 2025 – formally designated as a jurisdiction under increased monitoring for anti-money laundering and counter-terrorist financing deficiencies. The primary weaknesses cited: insufficient capacity to investigate and prosecute financial crimes; weak oversight of cooperatives, real estate, and informal money providers; and lack of transparency around beneficial ownership. FATF grey listing does not directly affect Fitch’s quantitative model, but it affects governance perceptions and reputational standing in ways that feed into the qualitative overlay.

Remittances: strength and fragility simultaneously

Remittances are Nepal’s greatest external asset and its most concentrated vulnerability. An estimated 3.5–4 million Nepalis are working abroad through formal channels – approximately 14% of the total population. Of these, 1.73 million are currently in the Middle East alone (Ministry of Foreign Affairs, 2026), with GCC countries and Malaysia together accounting for over 80% of annual new work permit approvals. The UAE, Saudi Arabia, and Qatar are the three dominant destinations. A geopolitical shock in the Gulf – a conflict escalation, an oil price collapse, or a policy shift on migrant labour – would transmit directly into Nepal’s remittance flows, reserve position, and current account within months. The concentration risk is structural and not easily diversified in the short run.

Capital expenditure execution

Nepal’s chronic underperformance on capital spending – historically around 60% of the planned capital budget actually disbursed by year-end – directly undermines the growth narrative. The hydropower story, the infrastructure story, the connectivity story: all of them depend on capital being deployed efficiently. When it is not, the projects that should be driving medium-term growth sit incomplete, and the rationale for the 5% growth potential looks increasingly aspirational. Fitch tracks capital expenditure execution as part of its assessment of public finance management quality.

5. Nepal Among Its Peers – and the Path to an Upgrade

How Nepal compares

To understand what BB- means and what the path forward looks like, it helps to look at countries rated one notch above and one below Nepal.

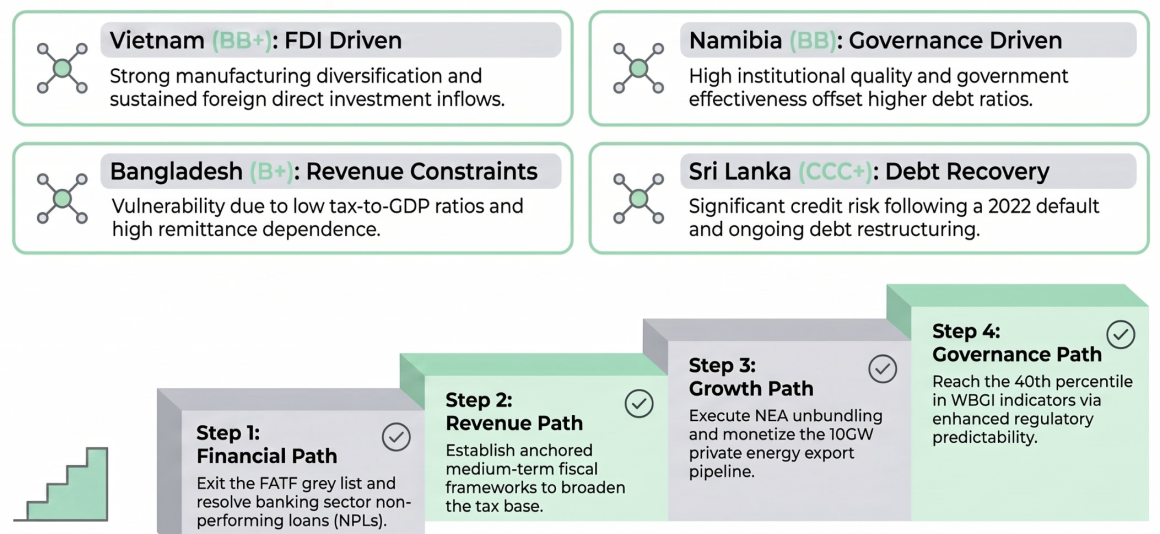

Vietnam (BB+): Vietnam sits one notch above Nepal and illustrates what a structurally transformative growth story can do for a credit profile. Vietnam’s strength is sustained high FDI inflows into export-led manufacturing, which has diversified its external sector away from remittance dependence. Its government debt is far below the ‘BB’ median, and its medium-term growth prospects are structurally stronger. Nepal has better external liquidity than Vietnam, but Vietnam’s economic diversification and FDI track record are what drive the rating premium.

Namibia (BB): Namibia is rated one notch above Nepal and offers a different lesson – on governance. Namibia’s World Bank Governance Indicators are substantially stronger than Nepal’s, particularly in the pillars of Government Effectiveness and Regulatory Quality. Strong institutions allow Namibia to carry a higher debt-to-GDP ratio than Nepal (well above the ‘BB’ median) without being penalised as severely in the model, because lenders trust the state’s fiscal management capacity.

Bangladesh (B+): Bangladesh sits one notch below Nepal and represents Nepal’s clearest comparator in terms of remittance dependence and development profile. Bangladesh’s strengths (low government debt, strong RMG export sector) are offset by weaker governance metrics and fiscal vulnerabilities. Nepal’s stronger external position justifies the notch premium.

Sri Lanka (recovering from RD): Sri Lanka’s 2022 default – the country’s first in its post-independence history – was triggered by a combination of unsustainable debt, a collapsing reserve position, and governance failures that prevented timely corrective action. It is the most proximate cautionary tale in the region for what Nepal must avoid. Sri Lanka entered the FATF grey list in 2025; its fiscal consolidation remains ongoing; its ratings recovery will take years. The lesson for Nepal: external liquidity buffers, maintained consistently, are not just a scorecard metric – they are crisis insurance.

What it would take to move the rating

Fitch’s November 2025 affirmation is explicit about the factors that could lead to a rating change (Fitch, November 2025).

Factors that could lead to a downgrade:

- Significant increase in government debt-to-GDP, particularly from contingent liabilities

- Evidence of weakening public finance management

- Material weakening of multilateral and bilateral creditor support (particularly slippage on the IMF programme)

- Political instability causing disruption to medium-term growth or governance

Factors that could lead to an upgrade:

- Strong, stable economic growth enabling substantial increases in GDP per capita

- Improvements in governance, regulatory standards, and investment climate that attract private and foreign investment

- A material reduction in government debt through sustained revenue mobilisation

Translating this into specific levers:

The governance path (hardest, highest-impact): Governance improvements that move Nepal’s WBGI composite closer to the 40th percentile – from the 33rd – would have a material effect on the SRM output. The specific levers: enacted conflict-of-interest legislation, operational digital accountability tools, measurable improvement in bureaucratic professionalism and regulatory coherence. These are 3-5 year reforms; no single budget cycle delivers WBGI movement.

The revenue path (most quantifiable): Closing the Revenue/GDP gap from ~19% toward 23%+ requires broadening the direct tax base, reducing reliance on import duties, and establishing a credible medium-term fiscal framework with explicit numerical anchors. The FY2083/84 budget takes important steps here – mandatory e-invoicing thresholds, AI-driven audit systems, digital payment incentives – but the structural commitment needs to be embedded in fiscal rules, not just annual budget speeches.

The financial sector path (most urgent): FATF grey list exit – with demonstrable progress on beneficial ownership transparency, financial crimes prosecution, and high-risk sector supervision – removes an active governance drag. Operationalisation of the Asset Management Company for NPL resolution, and bank recapitalisation, address the financial sector contingent liability risk. These are Fitch’s most immediate watch items.

The growth path (most visible): NEA unbundling into separate generation, transmission, and distribution entities – committed in the FY2083/84 budget – enables private-sector electricity export and is the structural step that turns the hydropower narrative from aspiration into realised revenue. Combined with the removal of Nepal Rastra Bank pre-approval requirements for FDI entry and profit repatriation (also in the FY2083/84 budget), these create genuine structural improvement in the external and macroeconomic outlook.

The prize and the risk

An upgrade from BB- to BB would not just feel good – it would be financially material in reducing the cost of government’s external borrowing.

More significantly, BB+ or investment-grade status would expand Nepal’s investor universe substantially. Funds that are restricted to ‘BB’ or better, or to investment grade, would open. This is not theoretical: many of the infrastructure funds that Nepal wants to attract for hydropower financing have exactly these rating-based investment mandates.

The downside risk – a downgrade to B+ – would cost Nepal the +1 QO notch and likely trigger a review of the QO itself. The DSSI variable that drove the original penalty is time-decaying and will fade over the next 4-5 years; a downgrade forced by political deterioration or fiscal slippage would be harder to reverse.

6. Conclusion – Why This Is Not Just a Finance Ministry Problem

Nepal’s sovereign credit rating is, in one sense, a dry technical exercise: analysts in Hong Kong running regressions on fiscal balance data. In another sense, it is one of the most honest external assessments of the Nepali state that exists – structured, internationally comparable, and directly linked to consequences.

What the BB- rating tells us is this: Nepal has genuinely impressive external buffers and a real growth story. Its FX reserves are extraordinary for a country of its income level. Its debt is manageable and affordable. Its hydropower potential is real and increasingly being monetised. These are not small things.

What it also tells us is that the governance gap – the 33rd versus 44th percentile WBGI, the 22% model weight – is the single constraint that holds Nepal back from the rating it could have on its fiscal and external merits alone. And governance is not just a rating problem. It is the same gap that causes capital expenditure to come in at 60% of target. It is the same gap that allowed AML commitments to be re-announced for nine consecutive years until the FATF made the consequences concrete. It is the same gap that makes international investors hesitate before committing to Nepali projects that are otherwise compelling on paper.

The FY2083/84 budget, presented by Finance Minister Dr. Swarnim Wagle, contains the most structurally ambitious institutional reform package I have seen in Nepal’s budget speeches across the past decade: a Conflict-of-Interest Law, Sunset Legislation, the explicit targeting of FATF exit, the NEA unbundling mandate, Alternative Development Fund to take the infrastructure liabilities off the sovereign book, the removal of NRB pre-approval for FDI. Whether these are delivered or re-announced in next year’s budget will be Nepal’s answer to the rating agencies – and, more fundamentally, to itself.

Nepal entered the sovereign credit rating universe from a position of genuine strength. It has a decade to build on that foundation. The question is whether institutional reform is sustained through political transitions – or whether, as has happened before, the next government reverses course and announces the same measures again with different phrasing.

The rating will reflect the answer.

Key references:

- Fitch Ratings, Sovereign Rating Criteria, April 2026

- Fitch Ratings, Nepal – BB- Rating Affirmation, November 2025

- Fitch Ratings, Nepal – First Rating Assignment, November 2024

- Nepal Rastra Bank, Current Macroeconomic and Financial Situation (9-month data, FY2025/26)

- International Monetary Fund, Nepal ECF Programme Page

- World Bank, Nepal Development Update, April 2026

- World Bank, Worldwide Governance Indicators

- Financial Action Task Force, FATF Grey List (Jurisdictions Under Increased Monitoring)