Introduction: The Illusion of Permission

Nepal’s banking and foreign exchange regulatory framework presents a paradox. On paper, it is internally coherent and appears to invite international integration by aligning with global standards, particularly in treasury management. However, in practice, a “triple lock” of statutory prohibitions, capital account controls, and liquidity penalties ensures that these permissions are largely theoretical, leaving operational control firmly with the central bank.

1. The Framework of Apparent Permissions

To an external observer, Nepal’s regulations offer a clear, technical pathway for banks to hold international assets. This is evidenced by two key components:

- The Capital Adequacy Framework (2015/2018): This Basel-aligned framework provides explicit “risk-weighting” rules for foreign investments. It categorizes “Claims on foreign governments and their central banks” and assigns risk weights from 0% to 150% based on international credit agency (ECA) scores. For example, high-grade sovereign claims can attract a 0% risk weight.

- The Long Form Audit Report (LFAR) Guidelines: These guidelines imply permission by requiring auditors to verify that “investment in foreign currency are made as per standard approved by the Board of Directors.”

In theory, these provisions create a roadmap for banks to invest foreign exchange balances in instruments like liquid government securities.

2. The Restrictive Reality in Practice

In reality, the aforementioned permissions are neutralized by a web of overlapping legal and regulatory barriers:

- Statutory Prohibition: The foundational barrier is the Act Restricting Investment Abroad, 2021 (1964), which imposes a blanket prohibition on all “persons” – explicitly including banks – from investing in foreign securities without a specific notification in the Nepal Gazette.

- Capital Account Controls: Nepal’s capital account is not fully convertible. The Nepal Rastra Bank Act, 2058 (2002) designates the NRB as the gatekeeper, with the default legal position being prohibition unless explicit, case-by-case approval is granted via directives like the Unified Circular.

- Liquidity Rules: Foreign treasury holdings are excluded from domestic liquidity compliance. They do not count towards the mandatory Statutory Liquidity Ratio (SLR) or the 20% Net Liquid Assets requirement, which are limited to domestic securities.

- Capital Penalties: Foreign investments are generally capped at 30% of a bank’s Primary Capital. Any exposure exceeding this threshold is directly deducted from Tier-1 capital, creating a powerful financial disincentive.

- Funding Restrictions: The Foreign Investment & Foreign Loan Management Bylaws, 2078 prohibit banks from using foreign loan proceeds to invest in foreign currency instruments.

A critical operational tool enforcing these restrictions is the Net Open Position (NOP) limit. The daily NOP – the difference between foreign currency assets and liabilities – is capped at 30% of Tier-1 Capital. To comply, banks must “square-off” their positions, often by selling excess foreign currency to the NRB. This daily requirement discourages long-term investment in foreign securities in favor of high-liquidity Nostro balances and short-term placements.

3. The Central Outcome

The structural result is that commercial banks (or any other investors) are effectively blocked from meaningful foreign investment. While they act as the nation’s primary “FX collectors” – holding nearly NRs 190 billion in liquid Nostro balances to facilitate trade – their actual investment in foreign government bonds is virtually zero, representing a mere 0.05% of their total portfolios. Consequently, the Nepal Rastra Bank remains the sole effective foreign investor, centralizing over NRs 1.1 trillion in foreign securities on its own balance sheet.

For a Nepali commercial bank, the current regulatory framework is akin to having a “passport without a visa.” The Basel framework and NRB directives provide the technical “travel document,” but the 1964 Act and capital account controls mean the border remains closed. Banks possess the papers to travel, but their funds are confined to simple “checking accounts” (Nostro placements) rather than being allowed to venture into foreign capital markets.

Capital Controls as the Hidden Governor

Although technical directives imply a permission framework, the true “governor” of Nepal’s banking system is a rigid structure of capital controls that prevents these technical permissions from becoming an operational reality. This restrictive environment is established by a hierarchy of laws and regulations that override any implied allowances.

1. The Foundational Barrier: The Act Restricting Investment Abroad, 2021 (1964)

The most significant statutory barrier is the Act Restricting Investment Abroad, 2021 (1964). This law establishes a baseline of prohibition from which all other regulations derive.

- Blanket Prohibition: Under Section 2, the Act states that “no person shall make any kind of investment abroad”.

- Broad Scope: The prohibition explicitly covers foreign securities, foreign bank accounts, bonds, shares, and treasuries. The Act defines “Foreign Security” to include any share, stock, bond, or debenture issued by a foreign government or organization.

- Applicability: This law applies to all “persons,” a term which explicitly includes banks and financial institutions.

- The Gazette Exception: The only legal exception is a specific authorization published by the Government of Nepal in the Nepal Gazette. This exception has not been broadly granted for commercial portfolio investments by banks.

- Effect: Due to this statute, foreign sovereign and corporate portfolio investment is statutorily barred for the private banking sector.

2. The Capital Account Context and Overarching Authority

The 1964 Act operates within the context of Nepal’s closed capital account, which is managed by the central bank.

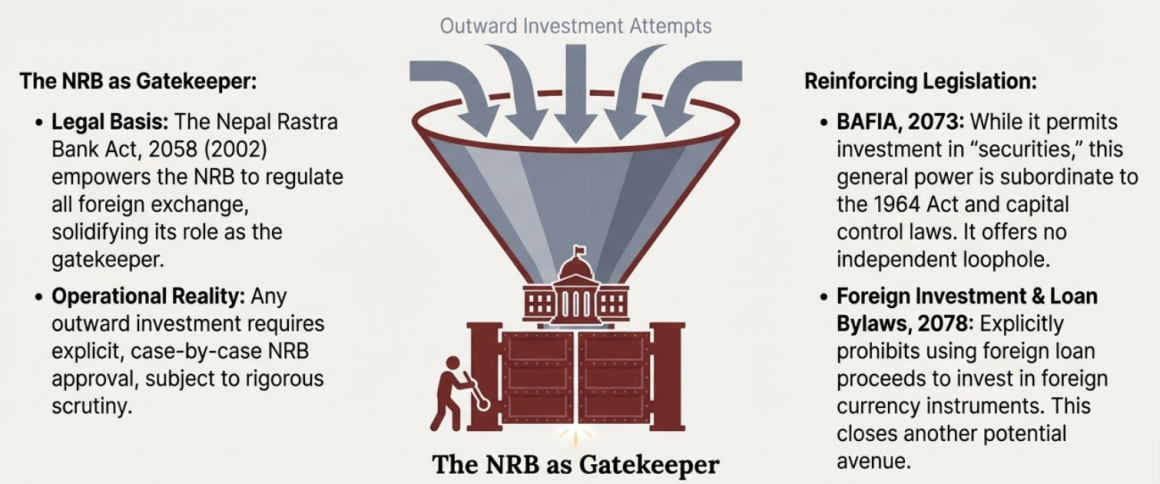

- Capital Account Status: Nepal’s capital account is not fully open, creating a default legal position of prohibition unless an action is explicitly permitted. Any outward investment requires explicit Nepal Rastra Bank (NRB) approval following rigorous case-by-case scrutiny.

- Regulatory Authority: The Nepal Rastra Bank Act, 2058 (2002) empowers the NRB to regulate foreign exchange, solidifying its role as the gatekeeper. This ensures the movement of capital remains under the direct and constant supervision of the central bank.

3. Reinforcing Restrictions: Other Key Regulations

Other laws and bylaws further tighten the restrictions, leaving no room for interpretation.

- Banks & Financial Institutions Act (BAFIA), 2073: While BAFIA provides the general authority for banks to operate, it offers no loophole for international investment. Section 49 permits investment in “securities,” but this general power must be read subject to the capital account laws and the 1964 Act. Consequently, BAFIA provides no independent legal basis for foreign portfolio investments.

- Foreign Investment & Foreign Loan Management Bylaws, 2078: These bylaws specifically restrict how banks can use foreign currency funding.

- Domestic Use Only: Foreign loans are permitted only for domestic use (e.g., infrastructure, energy, tourism).

- Explicit Negative List: Under Schedule 10, foreign loan proceeds cannot be invested abroad in foreign currency instruments or used for interbank FCY investment.

- Uniform Application: These restrictions apply uniformly to Commercial Banks (Class A), Development Banks (Class B), Finance Companies (Class C), and Infrastructure Development Banks.

- Practical Implication: This ensures that even when banks mobilize foreign funding, it must be deployed into the Nepalese economy and cannot be recycled into foreign assets.

4. The Illusion of Technical Permissions

Against this restrictive backdrop, certain directives create an illusion of permission, but they are effectively neutralized by the laws above.

- Recognition of Claims on Foreign Sovereigns: The Capital Adequacy Framework (2015/2018), based on Basel III, provides a technical “roadmap” by assigning risk weights (0% to 150%) to “claims on foreign government and their central banks” based on ECA scores. The permission is only implied because the framework defines capital requirements for assets that are otherwise statutorily barred.

- Board-Approved Standards for Foreign Currency: The Long Form Audit Report (LFAR) requirements mandate auditors to verify that foreign currency investments are made per board-approved standards. This creates a technical bridge for investing foreign exchange balances, but only within the confines of the overriding prohibitions.

- Maturity and Liquidity Provisions: Banks must classify foreign exchange into short-term and long-term periods to measure their net open position and risk, but this operational rule exists within the narrow space allowed by the capital control framework.

The directives imply what the laws explicitly forbid. The Basel framework and NRB directives provide a technical structure, but the 1964 Act and capital account controls ensure the border remains closed in practice.

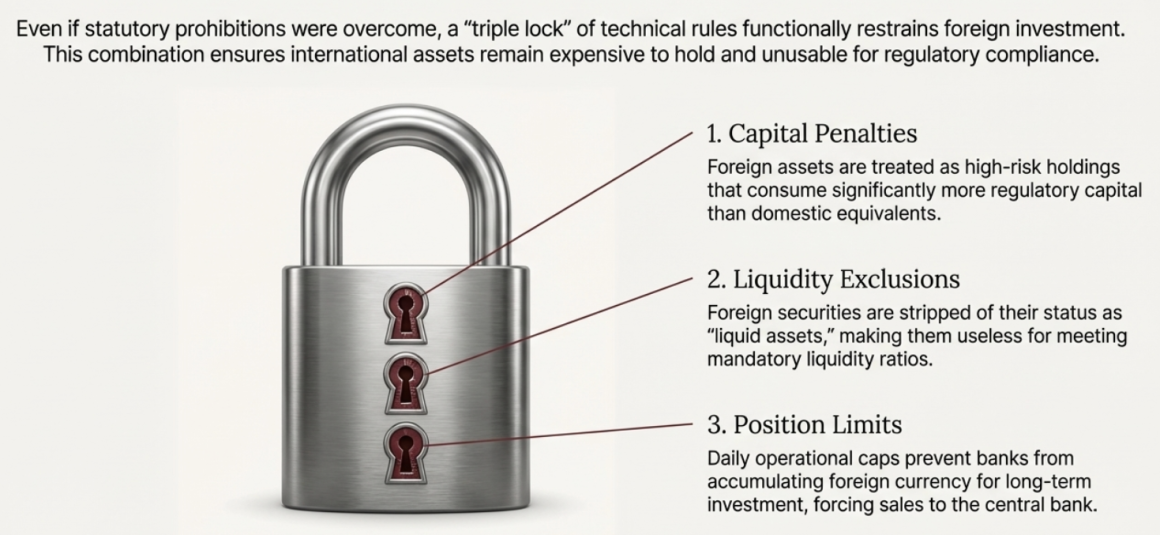

Risk Weights, Liquidity Rules, and NOP: A Triple Lock

The technical permissions for foreign investment are functionally restrained by a “triple lock” of capital charges, liquidity exclusions, and position limits. This combination ensures international assets remain expensive to hold and unusable for regulatory compliance, creating a powerful disincentive for banks.

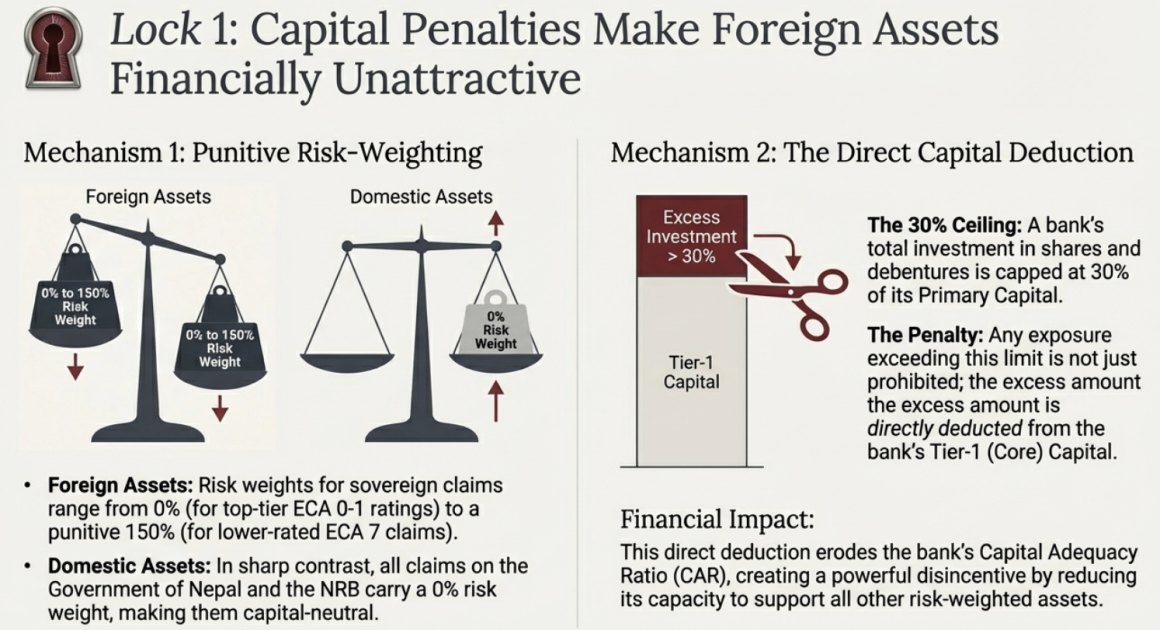

1. Capital Adequacy and the Risk-Weighting Disincentive

The Basel-aligned capital adequacy framework treats foreign assets as high-risk, capital-intensive holdings compared to domestic instruments.

- Risk Weights for Foreign Exposures: Risk weights for sovereign claims are determined by international Export Credit Agency (ECA) ratings. As per the Capital Adequacy Framework Section 3.3, weights range from 0% for high-grade sovereigns (ECA 0-1) to 150% for lower-rated claims (ECA 7).

- Specific 0% Risk Weight Categories: The framework assigns a 0% risk weight to claims on specific international bodies, including:

- The Bank for International Settlements, the International Monetary Fund, the European Central Bank, and the European Community.

- Key Multilateral Development Banks (MDBs) such as the World Bank Group, Asian Development Bank (ADB), and others listed, while claims on other MDBs receive a 100% risk weight.

- Domestic Neutrality: In sharp contrast, all claims on the Government of Nepal and Nepal Rastra Bank carry a 0% risk weight, making them capital-neutral.

- Implication: This disparity means foreign assets require significantly more capital to be set aside, creating a direct financial disincentive.

2. The Direct Capital Penalty: The 30% Investment Ceiling

Strict regulatory ceilings, enforced by severe penalties, prevent banks from committing significant resources to foreign markets.

- The 30% Ceiling: As established in NRB Integrated Directive No. 8/081, Section 3, Subsection 3.2, a bank’s total aggregate investment in shares, debentures, or collective investment funds of all organized institutions is capped at 30% of its Primary Capital.

- Capital Penalties: Crucially, any exposure exceeding this limit is not just prohibited; the excess amount must be directly deducted from the bank’s Primary Capital for calculating its Capital Fund.

- Effect: This direct deduction erodes the bank’s Tier-1 (Core) Capital, causing a immediate reduction in its Capital Adequacy Ratio (CAR). This creates a massive financial disincentive by making less capital available to support other risk-weighted assets.

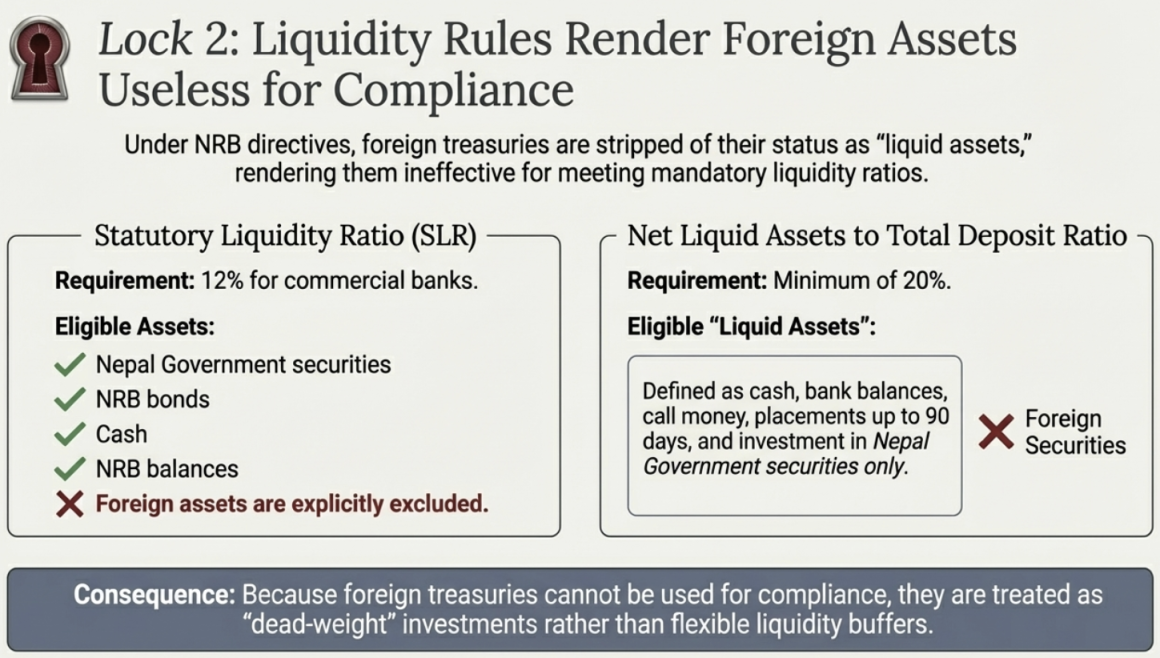

3. Liquidity Regulation: The Exclusion of Foreign Assets

Under NRB directives, foreign treasuries are stripped of their status as “liquid assets,” rendering them ineffective for meeting mandatory liquidity ratios.

- Mandatory Metrics: Banks must maintain a Net Liquid Assets to Total Deposit Ratio of at least 20%, as per the Capital Adequacy Framework 2015, Section 6.4, Subsection a, Point 6. A shortfall incurs an additional risk weight penalty.

- Definition of “Liquid Assets”: For this ratio, liquid assets are strictly defined (Capital Adequacy Framework 2015, Section 6.4, Point 6 Note) as: cash, bank balances, call money, placements up to 90 days, and investment in Nepal Government securities.

- Statutory Liquidity Ratio (SLR): Similarly, for the mandatory 12% SLR for commercial banks (NRB Integrated Directive No. 13/081, Section 3), eligible assets are strictly limited to Nepal Government securities, NRB bonds, cash in hand, and NRB balances.

- Explicit Exclusions: Foreign government bills and bonds are excluded from both liquidity calculations.

- Consequence: Because foreign treasuries do not support SLR or the 20% liquidity ratio compliance, they are treated as dead-weight, long-term investments rather than flexible liquidity buffers.

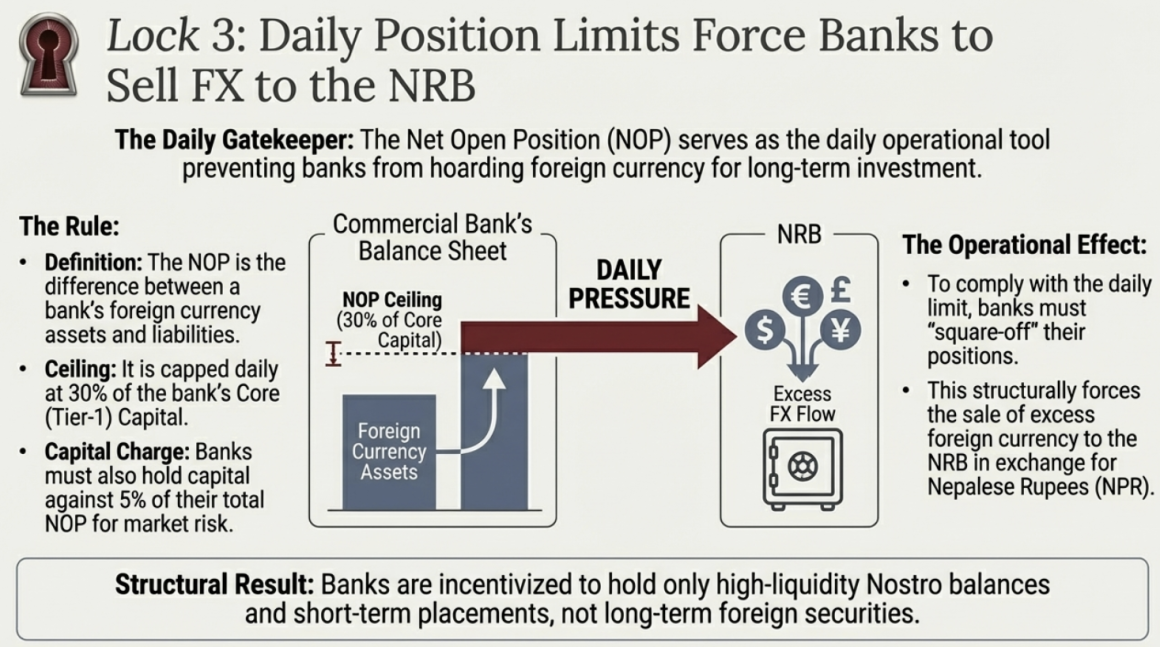

4. The Daily Gatekeeper: Net Open Position (NOP) Limits

The Net Open Position (NOP) serves as the daily operational gatekeeper, preventing banks from hoarding foreign currency for long-term investment.

- Regulatory Ceiling: The daily NOP – the difference between FCY assets and liabilities – is capped at 30% of Core (Tier-1) Capital, as per NRB Unified Directive No. 5/081, Section 9, Subsection 9(5).

- Definition and Capital Charge: The NOP is defined in the Capital Adequacy Framework 2015, Section 5.4. Banks must also allocate a fixed 5% of their total NOP as a capital charge for market risk (Section 5.3).

- Operational Effects: To comply with the daily limit, banks must “square-off” their positions. This often entails the mandatory sale of excess foreign currency to the NRB. Failure to comply within one month leads to penalties under the Nepal Rastra Bank Act, 2058.

- Structural Result: As required by NRB Unified Directive No. 5/081, Section 9, Subsection 9(4), banks must classify foreign exchange into short-term (one month or less) and long-term periods. To avoid capital charges and maintain flexibility, banks structurally prefer high-liquidity Nostro balances and short-term placements over long-term foreign securities.

Empirical Reality: A Rare Exception Proves the Rule

Despite a regulatory framework that technically permits international asset holdings, the actual participation of the private sector in global sovereign markets is nearly non-existent. The overwhelming majority of Nepali commercial banks report zero investment in foreign government bonds.

1. Widespread Absence of Foreign Sovereign Exposure

An exhaustive review of the banking sector reveals that most major Nepali commercial banks report zero investment in foreign government bonds. For institutions such as Nabil Bank, Nepal SBI Bank, Everest Bank, NIC Asia Bank, and Standard Chartered Bank Nepal, claims on “Foreign Government and Central Bank” across all credit rating categories are consistently reported as nil.

Statistically, “Non-Resident” (foreign) investments represent only 0.05% (approximately NRs 0.75 billion) of the total commercial banking investment portfolio as of mid-July 2024. This stands in stark contrast to the Nepal Rastra Bank (NRB), which acts as the nation’s primary foreign investor, holding over NRs 1.1 trillion in foreign securities. The only documented exceptions to this trend are Machhapuchchhre Bank Limited (MBL) and Sanima Bank Limited (SBL).

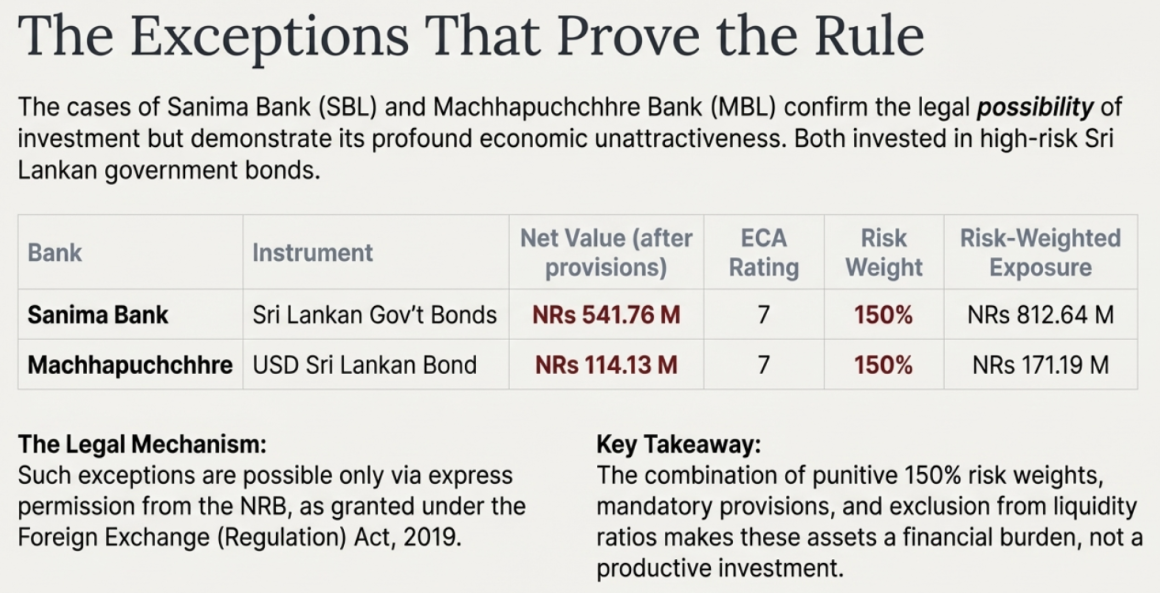

2. Case Studies: Sanima Bank and Machhapuchchhre Bank

These two banks serve as unique case studies for actual foreign sovereign investment under the current restrictive regime, both involving high-risk sovereign debt.

Sanima Bank Limited (SBL): SBL has the most significant disclosed exposure.

-

- Instrument: The bank holds claims on a foreign government, primarily related to Sri Lankan government bonds.

- Financial Valuation: As of Ashadh 2082, the Book Value of this claim is Rs. 574.51 million. After a specific provision of Rs. 32.75 million, the Net Value stands at Rs. 541.76 million.

- Risk Classification: The claim is categorized under ECA Rating 7.

- Capital Penalty: This high-risk rating carries a punitive 150% risk weight, resulting in a Risk-Weighted Exposure (RWE) of Rs. 812.64 million.

Machhapuchchhre Bank Limited (MBL):

-

- Instrument: The bank holds a USD-denominated Sri Lankan Bond.

- Financial Valuation: As of Ashadh end 2082, the Book Value is Rs. 565.13 million. The bank has maintained a substantial Specific Provision of Rs. 451.00 million, leaving a Net Value of Rs. 114.13 million. The investment is also measured at an amortized cost of USD 4.06 million (approximately NPR 559.09 million).

- Risk Classification: The bank classifies this under “Claims on Foreign Government and Central Bank (ECA Rating 7)”.

- Capital Penalty: This rating carries a 150% risk weight, leading to a Risk-Weighted Exposure of Rs. 171.19 million.

- Accounting Treatment: The bond is classified as an Investment Security measured at Amortized Cost and is listed under the “Other” sub-category of its investment securities table.

3. The Legal Framework for Exceptional Permissions

The existence of these investments is possible due to a specific legal mechanism. While the Act Restricting Investment Abroad, 2021 (1964) establishes a strict baseline by mandating that “no person shall make any kind of investment abroad”, the legislative framework governing the Nepal Rastra Bank (NRB) allows for regulatory exceptions.

- NRB Authority: The Foreign Exchange (Regulation) Act, 2019 (1962) and the Nepal Rastra Bank Act, 2058 (2002) provide the NRB with the statutory authority to regulate foreign exchange transactions and grant permissions to licensed entities.

- Licensed Dealing: The prohibition under Section 10 of the Foreign Exchange (Regulation) Act, 2019 is not absolute; it prohibits dealings only “without the notification or permission of the Bank”. Furthermore, Section 9C of the same Act reinforces that investment abroad is prohibited “except as permitted by the Bank” through public notice. This structure creates the mechanism by which the NRB can authorize specific Class “A” banks to hold foreign currency assets.

4. Significance of the Exceptions

The cases of MBL and SBL confirm the legal possibility of such investments within the existing NRB Unified Directives and capital frameworks. However, they simultaneously demonstrate their profound economic unattractiveness. The combination of high capital charges (150% risk weight), mandatory impairments (Expected Credit Loss provisions), and the fact that such instruments are excluded from the mandatory Statutory Liquidity Ratio (SLR) makes these bonds a financial burden rather than a productive asset for the banks that hold them.

NRB’s Monopoly Over Foreign Assets

While commercial banks are restricted from meaningful foreign investment, the Nepal Rastra Bank (NRB) operates as the nation’s sole, authorized accumulator of foreign assets. The regulatory framework creates a system where foreign currency is collected by commercial banks but ultimately centralized and invested by the central bank.

1. The Legal Dichotomy: Why the NRB Alone Invests

The stark difference in legal authority between commercial banks and the NRB is the foundation of this monopoly.

|

Entity |

Can Invest in Foreign T-Bills / Bonds? |

Legal Mechanism / Barrier |

|

BFIs in Nepal |

Generally, No |

Barred by the Act Restricting Investment Abroad, 2021 and specific loan utilization restrictions in the Foreign Investment & Foreign Loan Management (FIFL) Bylaws, 2078. (Exception: The cases of MLB and SBL with express permission from NRB). |

|

Nepal Rastra Bank |

Yes |

Explicitly authorized by Section 66 of the Nepal Rastra Bank Act, 2058 to hold foreign government securities as part of its international reserves. |

2. How Foreign Currency Enters Nepal and Flows to the NRB

Foreign currency enters the economy through several channels and is systematically transferred to the NRB’s balance sheet.

- Sources of Inflow:

- Remittances: The most significant source, reaching an eight-year peak in FY 2081/82 (2024-25), growing by over 16% in USD terms.

- Merchandise Exports: Earnings from goods sold internationally, which saw a recent increase of 81.8%.

- Tourism Receipts: Revenue from international visitors, a “key driver of recovery” for reserves, with over 1.01 million arrivals in 2023.

- Foreign Direct Investment (FDI) and Loans: Inflows from net FDI and borrowings from institutions like the World Bank and IFC.

- Role of Commercial Banks: Banks act as the first receivers, facilitating remittances, converting currency for beneficiaries, and holding funds in Nostro accounts to finance trade (e.g., Letters of Credit).

- Transfer Mechanism to NRB: Two factors drive this transfer:

- NOP Limits: Banks must manage their Net Open Position (NOP), capped at 30% of Primary Capital.

- NPR Liquidity Needs: Banks require Nepalese Rupees for domestic lending and sell excess foreign currency to the NRB to obtain it.

- The Process: The NRB, acting as the “buyer of last resort,” injects NPR into the banking system by crediting commercial banks’ reserve accounts in exchange for the foreign currency. In FY 2080/81 alone, the NRB purchased USD 589 million from banks.

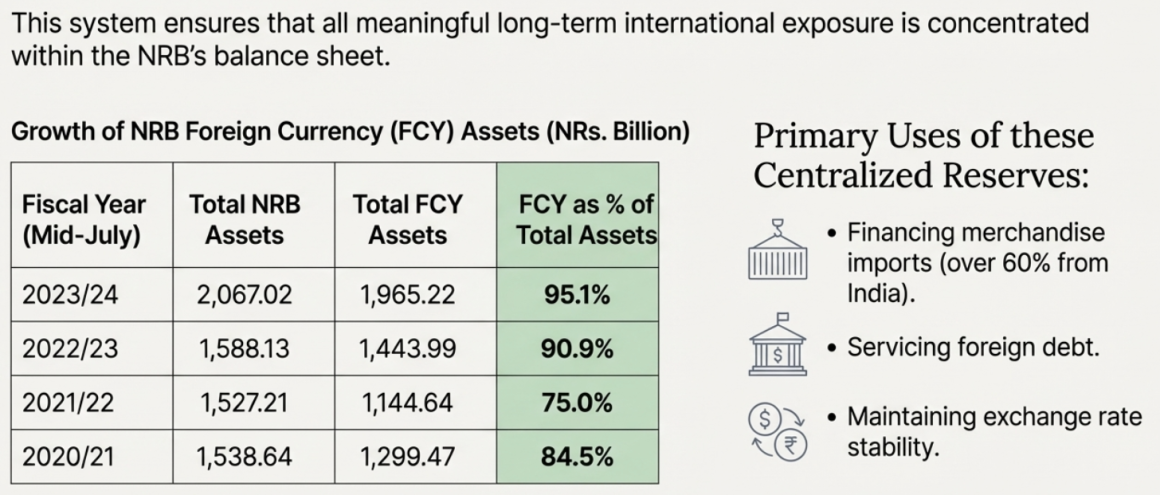

3. The Outcome: Centralized Accumulation on the NRB's Balance Sheet

This mechanism ensures the massive accumulation of foreign assets is centralized at the NRB.

- Reserve Creation & Investment: The acquired foreign currency is recorded as Gross Foreign Exchange Reserves. Under its legal mandate, the NRB invests these reserves in foreign government treasury bills, Special Drawing Rights (SDRs), gold, and other foreign debt securities.

- Structural Effect: The result is that commercial banks, while “foreign-currency rich” in daily operations, remain “foreign-investment poor.” All meaningful long-term international exposure is concentrated within the NRB’s balance sheet.

4. Trend of NRB Foreign Asset Growth

The table below illustrates the rapid growth and dominance of foreign assets on the NRB’s balance sheet. All figures are in NRs. Billion as of mid-July of the respective years.

|

Fiscal Year (Mid-July) |

Total NRB Assets [i] |

Total Foreign Currency (FCY) Assets [ii] |

% of Total Assets |

FCY Interest Income [iii] |

|

2023/24 (2081) |

2,067.02 |

1,965.22 |

95.07% |

79.79 |

|

2022/23 (2080) |

1,588.13 |

1,443.99 |

90.92% |

48.37 |

|

2021/22 (2079) |

1,527.21 |

1,144.64 |

74.95% |

18.73 |

|

2020/21 (2078) |

1,538.64 |

1,299.47 |

84.45% |

17.50 |

|

2019/20 (2077) |

1,400.90 |

1,226.12* |

87.52% |

25.97 |

|

2018/19 (2076) |

1,071.70 |

902.44* |

84.21% |

35.10 |

|

2017/18 (2075) |

1,155.10 |

989.40* |

85.65% |

23.80 |

Note: Figures for 2018–2020 are based on Gross Foreign Exchange Reserve data

5. Spending and Usage of Foreign Currency Reserves

The NRB utilizes these centralized reserves for critical national purposes:

- Merchandise Imports: Financing imports is the primary drain on reserves, with over 60% of imports coming from India.

- Foreign Debt Servicing: Repaying principal and interest on external loans from multilateral agencies.

- Service Account Payments: Covering costs for international services, which had a negative balance of NPR 55.86 billion in FY 2080/81.

- Repatriation of Profits: Allowing foreign-owned entities to send dividends abroad.

- Travel, Education, and Medical Expenses: Providing foreign currency to citizens for study, travel, and healthcare abroad.

- Reserve Management and Stability: Maintaining exchange rate stability and ensuring sufficient reserves to cover at least 13 months of imports.

5. Spending and Usage of Foreign Currency Reserves

The NRB utilizes these centralized reserves for critical national purposes:

- Merchandise Imports: Financing imports is the primary drain on reserves, with over 60% of imports coming from India.

- Foreign Debt Servicing: Repaying principal and interest on external loans from multilateral agencies.

- Service Account Payments: Covering costs for international services, which had a negative balance of NPR 55.86 billion in FY 2080/81.

- Repatriation of Profits: Allowing foreign-owned entities to send dividends abroad.

- Travel, Education, and Medical Expenses: Providing foreign currency to citizens for study, travel, and healthcare abroad.

- Reserve Management and Stability: Maintaining exchange rate stability and ensuring sufficient reserves to cover at least 13 months of imports.

6. Balance Sheet Impact: A Step-by-Step View

The following table summarizes the accounting impact of the foreign currency flow from a remittance to an NRB investment.

|

Step |

Action |

Commercial Bank Balance Sheet Impact |

NRB Balance Sheet Impact |

|

1 |

Remittance Sent |

Asset (+): Balance in Foreign Banks |

No Change |

|

2 |

Bank needs NPR |

Bank decides to sell FCY to NRB |

No Change |

|

3 |

The Sale |

Asset (-): Balance in Foreign Banks |

Asset (+): Balance in Foreign Banks |

|

4 |

NRB Invests |

No Change |

Asset (-): Balance in Foreign Banks |

Physical vs. Virtual Inflow:

- Virtual (90%+): Most remittances enter as digital balances (“Balance in Foreign Banks”).

- Physical: If currency enters as cash (e.g., from a tourist), it is recorded as “Cash Balance – Foreign Currency” and is eventually deposited into the NRB’s vaults.

Conclusion

Nepal’s banking system is designed to be foreign-currency rich but deliberately foreign-investment poor. While commercial banks facilitate massive capital inflows, a “triple lock” of statutory prohibitions, capital penalties, and liquidity rules functionally prohibits them from deploying that capital into global markets. The result is that banks act merely as FX collectors and liquidity intermediaries, with their nearly NRs 190 billion in foreign balances dedicated solely to trade finance, while their actual yield-bearing foreign investments represent a negligible 0.05% of portfolios. This restrictive environment is not an accidental outcome but a deliberate design that consolidates all meaningful foreign asset exposure within the Nepal Rastra Bank (NRB).

Consequently, the NRB holds an effective monopoly over foreign investment originating from Nepal. While the Basel framework provides banks with a technical “passport” for international finance, the foundational 1964 Act and capital controls act as a closed border. This centralizes the nation’s external asset accumulation entirely on the central bank’s balance sheet, where over NRs 2 trillion in foreign securities are held. The rare exceptions of two banks holding minor, penalized foreign bonds only serve to prove the rule, highlighting the profound economic disincentives for private sector participation. Ultimately, the framework ensures the NRB acts as the sole national wealth manager, aggregating foreign exchange from the private sector to maintain reserves and the currency peg, while other sectors of the capital and financial markets funds remain confined to operational “checking accounts” rather than being allowed to venture into international capital markets.