I. Introduction: A Familiar Crisis

Nepal’s capital market already carries a structural fracture that we discussed in one of the previous posts. Hydropower companies – developed overwhelmingly under Build–Own–Operate–Transfer (BOOT) concession agreements with legally mandated handover to the state at the end of their license period – now account for approximately 16% of total market capitalization, valued at roughly NPR 567 billion. These same companies drive over 42% of total NEPSE trading turnover, amounting to approximately NPR 207 billion annually, fuelled largely by retail investors. The implication is stark: hundreds of billions of rupees in public capital are currently tied to assets with a predetermined expiry date, yet these assets are traded on the secondary market as ordinary perpetual equity – as though the underlying cash flows will continue indefinitely.

This review examines the proposed Alternative Development Finance (ADF) Fund Bill with a specific focus on this systemic tension. The bill represents Nepal’s most ambitious institutional attempt to mobilize alternative finance for national infrastructure. In designing the parent Fund, the drafters have adopted an internationally sound structure that correctly insulates the institution’s core share capital from public market pressures. However, this review argues that the bill’s subsidiary architecture – the legal framework governing how project-specific Special Purpose Vehicles (SPVs) raise capital and interact with public investors – contains a critical structural vulnerability. If left unaddressed, the ADF Bill does not merely replicate the existing hydropower problem; it provides a statutory mechanism to scale that identical terminal value risk across entirely new infrastructure sectors, from railways and airports to tunnels and cable cars, with potentially systemic consequences for Nepal’s capital market.

II. The Parent Fund: A Sound Institutional Design

The ADF Fund’s statutory mandate, as defined in Section 3 of the bill, is to mobilize alternative finance for projects that yield high economic returns, create employment, and support overall economic development. Section 4(1) further directs this investment toward critical, long-term national priorities – energy, railways, airports, tunnels, cable cars, IT parks, and urban infrastructure. The Fund is not conceived as a profit-maximizing commercial enterprise but as a policy-based development finance institution (DFI), mandated to catalyze national infrastructure investment that the private market alone cannot efficiently deliver.

Recognizing this developmental mandate, the bill’s drafters have adopted a tightly controlled ownership structure for the parent Fund’s core share capital. Under Section 8(3), shares are rigidly allocated: 51% to the Government of Nepal (Section 8(3)(Ka)), 25% to designated retirement funds – specifically the Employees Provident Fund, Citizen Investment Trust, and Social Security Fund (Section 8(3)(Kha)) – and 24% to life, non-life, and micro-insurance companies (Section 8(3)(Ga)). The general public is entirely excluded from the Fund’s corporate share capital.

This closely held structure is further fortified by secondary protective mechanisms. If shares allocated to retirement funds or insurance companies go unsubscribed, either entirely or partially, Section 8(6) vests the disposal of those shares entirely in the discretion of the Government of Nepal. Similarly, Section 8(7) provides that if an existing institutional shareholder wishes to sell, the first right of refusal goes to remaining institutions within the same group; failing that, the shares are sold as determined by the Government. Even when diversification of the parent company’s ownership is envisioned, the bill restricts it exclusively to international governmental or intergovernmental financial institutions under Section 8(8) and Section 8(9), carefully avoiding any public float. The Government of Nepal’s holding may be reduced to a minimum of 26%, but only through this controlled, institutional pathway.

This design mirrors established international practice. Entities such as Germany’s KfW Development Bank, Brazil’s BNDES (Banco Nacional de Desenvolvimento Econômico e Social), and the United Kingdom’s UK Infrastructure Bank remain government-owned and raise capital primarily through bonds rather than equity issuance to the general public, ensuring policy alignment and long-term financial stability. India’s National Bank for Financing Infrastructure and Development (NaBFID), even where diversification is envisaged, follows a gradual, controlled approach without full public listing of the parent institution. Singapore’s Temasek Holdings maintains state ownership at the holding level while allowing market participation exclusively through its portfolio companies. The ADF Fund’s parent-level architecture sits squarely within this international consensus: the core institution must remain insulated from short-term shareholder return expectations that could distort its developmental mandate.

The parent Fund’s design, therefore, deserves commendation. It represents a deliberate, well-informed legislative choice to build a DFI that can pursue long-term, catalytic infrastructure investment without being subjected to the governance distortions of public equity markets. Any suggestion to publicly list the ADF Fund’s core shares would be conceptually inconsistent with its statutory purpose and contrary to prevailing international practice.

III. Vulnerability at the Subsidiary Level

A. The Legal Pathway: How the Bill Enables Public Listing of Terminal Assets

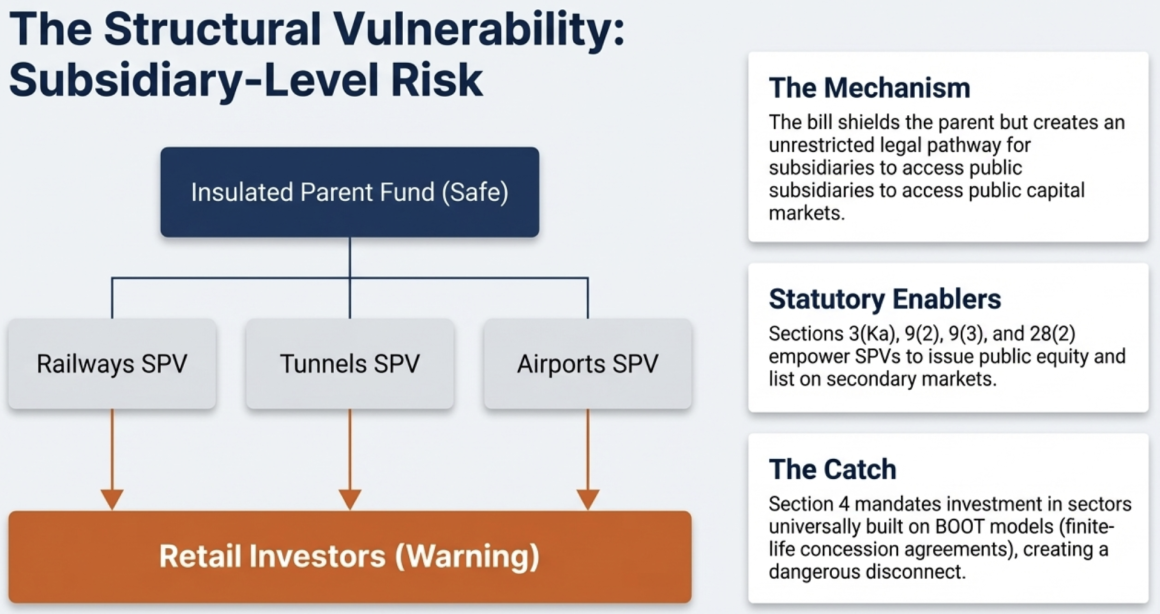

While the parent Fund is correctly shielded, the bill simultaneously creates a broad and largely unrestricted legal pathway for its project-level subsidiaries to access equity via public capital markets. Reading four key provisions together reveals the full scope of this pathway:

Section 3(Ka) explicitly authorizes the mobilization of alternative development finance for specific projects by raising funds from “investors or the general public” through financial instruments, debentures, equity, debt, or mixed financial instruments. Section 9(2) grants the Fund authority to establish separate subsidiary companies to operate designated projects. Section 9(3) legally empowers these subsidiaries to issue equity, bonds, or debentures directly to domestic and foreign investors to collect capital. And Section 28(2) explicitly allows financial instruments issued by the Fund to be listed in the securities market and traded on the secondary market.

This architecture, on its face, is a rational capital mobilization strategy – precisely the kind of project-level market participation that entities like Temasek facilitate through their portfolio companies. The critical problem is not that the bill allows subsidiary-level public participation; the problem is that it does so without any structural safeguard distinguishing finite-life infrastructure assets from perpetual ones.

B. The BOOT Model and the Terminality Problem

Section 4(1) mandates the Fund to invest in sectors such as energy, railways, airports, tunnels, and cable cars – sectors that, in Nepalese and international practice, are universally developed under limited-life concession agreements or the BOOT model. Section 4(2)(Ga) explicitly accommodates this by allowing the Fund to invest in projects recommended by the Investment Board Nepal for implementation under the Public-Private Partnership model. PPP frameworks are, in practice, the primary legal vehicles for BOOT and BOT concession agreements in Nepal.

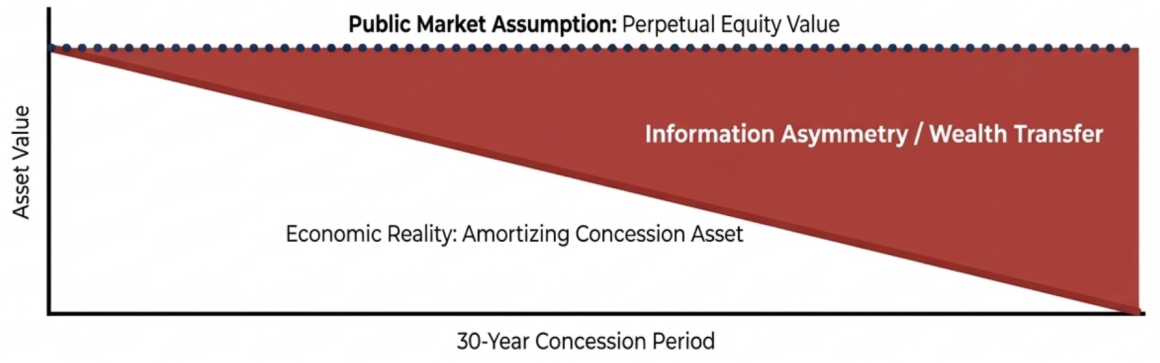

The fundamental characteristic of a BOOT project is its terminality: the project company builds, owns, and operates an infrastructure asset for a defined concession period, after which the asset is transferred to the state. The so-called “equity” in such an entity is not truly residual, growth-oriented capital. Due to regulated tariffs, capped returns, and finite concession periods, it behaves as what infrastructure finance literature describes as “debt-like equity” – generating predictable, bond-like cash flows with a pre-defined economic life. This logic is implicitly recognized in international accounting practice under IFRIC 12, which treats many such arrangements as financial (debt-like) assets rather than true ownership of perpetually productive assets.

Critically, the bill itself does not explicitly clarify the compensation mechanism at the end of a concession – whether assets are transferred at zero compensation or whether a residual buyout exists. The bill is a financial mobilization framework, not a concession law; it delegates the structuring of PPP project terms to external authorities. Under Section 4(2)(Ga) and Section 25(2)(Gha), the Fund invests in or guarantees projects implemented under the PPP model as recommended by the Investment Board Nepal. The specific terminal transfer conditions are governed by separate concession agreements, not by this bill. Yet the bill simultaneously authorizes unconditional public market listing of the equity instruments financing these projects – creating a dangerous disconnect between the financial structure visible to public investors and the contractual reality governing the asset’s lifespan.

C. Five Regulatory Blind Spots

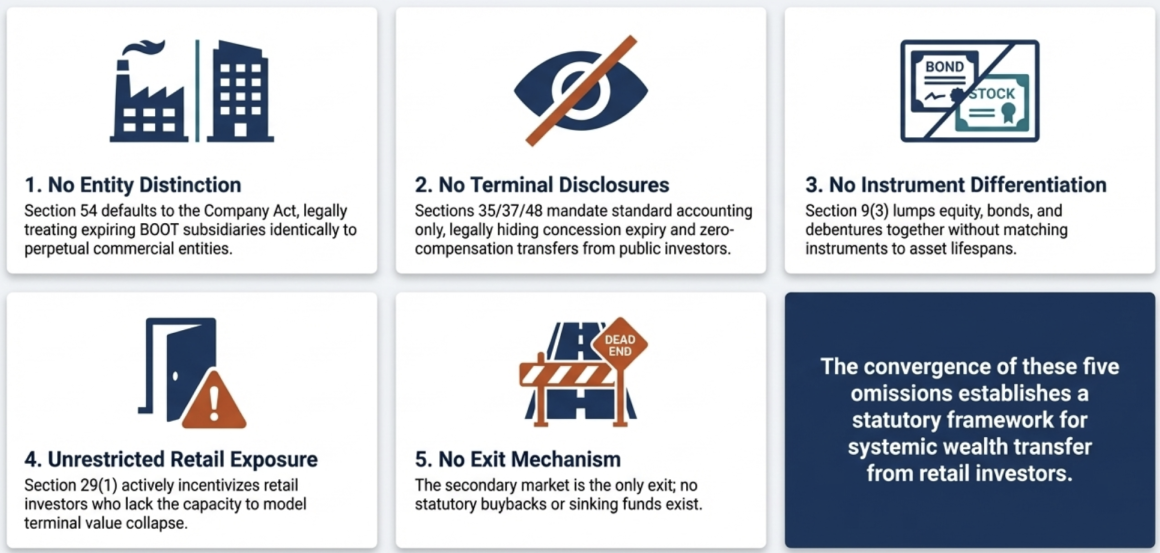

(i) No Distinction Between Finite-Life and Perpetual Entities

The bill uses a single, blanket term – “subsidiary companies” – in Section 9(2) to describe all entities operating projects. It contains no statutory language distinguishing subsidiaries that hold limited-life concession assets from those that hold permanent assets. Under Section 2(Kha), a “Project” is simply defined as any project listed under Section 4(2), categorized only by how it is recommended or approved – not by its lifespan or terminal transfer conditions. Furthermore, because the ADF bill lacks its own internal corporate governance code, Section 54 legally forces all matters not explicitly covered to be governed by the prevailing Company Act. Under standard corporate law, a registered company is inherently granted perpetual succession – meaning the law structurally treats an expiring BOOT hydropower subsidiary identically to a perpetually operating commercial IT park.

(ii) No Mandated Terminal Disclosures

The bill’s transparency provisions, defined in Section 35 (financial transparency), Section 37 (financial reports), and Section 48 (annual reports), are entirely focused on standard corporate accounting – quarterly financial statements, balance sheets, and profit-and-loss accounts. None of these sections compel the Fund or its subsidiaries to disclose the underlying concession period, the transfer conditions, or the terminal value assumptions to the investing public. Even Section 23 (project study requirements) and Section 24 (project implementation conditions), which require risk analysis and return evaluation, completely fail to identify concession expiry or terminal transfer as a mandatory risk factor for public shareholders. The delegated legislation under Section 35(3) merely states that additional financial transparency standards will be prescribed by future rules, without any statutory directive requiring terminal-value disclosure.

(iii) No Instrument Differentiation

The bill acknowledges different financial instruments – Section 2(Jha) defines “mixed financial instruments” as containing characteristics of both equity and debt, and Section 9(3) explicitly authorizes SPVs to issue equity, bonds, or debentures. However, the bill treats these instruments uniformly in terms of regulatory oversight. Section 9(3) lumps equity, bonds, and debentures into a single sentence as equally valid capital-collection tools, with no stipulation that finite-life projects should use debt instruments matched to their concession period rather than perpetual equity. The absence of differentiation allows SPVs to finance rapidly expiring BOOT assets by selling theoretically infinite-life equity shares to retail investors.

(iv) Unrestricted Retail Investor Exposure

The bill does not restrict SPV investment to institutional investors. Section 3(Ka) explicitly authorizes raising funds from “the general public”, and Section 9(3) empowers subsidiaries to issue equity to “domestic or foreign investors” without qualifying this as strictly institutional. Section 29(1) goes further, explicitly recognizing and incentivizing “individual and institutional investors” with tax exemptions. Individual retail investors – who typically lack the analytical capacity to model terminal value collapse in a concession asset – are thus not only permitted but actively incentivized to purchase equity in finite-life BOOT infrastructure SPVs.

(v) No Structured Exit Mechanism

The bill provides no structured exit mechanism for SPV investors. There is no statutory obligation for the parent Fund, the Government of Nepal, or the SPV itself to buy back shares at the end of a concession period. While Section 14(ana) allows the Board to convert debt into equity, and Section 9(1)(थ) positions the Fund as a financial intermediary, these are operational financing tools, not structured investor exit routes. The bill’s takeover provisions under Section 26(1) and Section 26(3) are strictly penal – triggered by loan default or fund misuse – and designed for debt recovery, not as a compensated exit for equity holders. The liquidation provisions in Chapter 10 (Sections 40–42) apply exclusively to the parent Fund’s insolvency, not to the structured wind-down of finite-life subsidiaries. The secondary market thus becomes the only available “exit” – forcing retail investors to sell fundamentally decaying equity to other uninformed buyers before the concession expires.

IV. The Hydropower Precedent: Practical Risk

The risk identified above is not hypothetical. Nepal’s hydropower sector provides a live, large-scale demonstration of what happens when perpetual equity is issued for terminal BOOT assets without adequate structural safeguards. As noted, hydropower now accounts for roughly 16% of total NEPSE market capitalization (approximately NPR 567 billion) and over 42% of total trading turnover (approximately NPR 207 billion annually). Retail investors are the dominant participants in this trading activity.

These companies operate under BOOT concession agreements with legally mandated handover to the state at the end of their license period. Yet their equity is issued, listed, and traded on the secondary market under the exact same regulatory framework as perpetual companies. There is no distinct trading class, no mandated concession-expiry disclosure in a form that affects market pricing, and no structured exit mechanism for shareholders as the concession nears its end. The result is a massive information asymmetry: the eventual value erosion is not theoretical but represents a large-scale transfer of long-term financial risk from promoters and banks to the general investing public.

The ADF Bill, as currently drafted, does not merely fail to address this precedent – it provides a statutory mechanism to replicate it. Section 4(1) treats all infrastructure sectors uniformly, placing energy, railways, airports, IT parks, and special tourism infrastructure on the exact same legal footing. The bill contains no acknowledgment of the structural distinction between terminal BOOT assets and perpetually owned commercial developments. Under the ADF framework, a new railway SPV operating under a 30-year BOOT concession would be authorized to issue public equity, list on the secondary market, and attract retail investors through tax incentives under Section 29 – all under the identical legal and regulatory treatment as a perpetually owned IT park.

V. Protecting Debt While Exposing Public Equity

The bill’s guarantee framework reveals an additional structural asymmetry that reinforces the terminal value concern. The Fund is explicitly designed to support projects through comprehensive guarantees: Section 22(2)(Gha) permits the Fund to provide specific guarantees for projects, Section 25(1) through Section 25(3) establish an approval pathway for Government of Nepal or intergovernmental institution guarantees, and Section 3(Ga) authorizes a dedicated guarantee fund backed by full or partial state guarantees. Crucially, Section 28(1) ensures that bonds issued with a Government guarantee are treated like government development bonds for listing purposes. The bill thus heavily de-risks debt instruments through state backing.

Yet the bill provides no equivalent statutory guarantee for the equity shares issued by project SPVs to the retail public. While the project’s debt is secured by state guarantees, retail investors buying SPV equity on the secondary market bear the full, unhedged exposure to the terminal expiry of the asset. This asymmetry – protecting institutional and debt capital while leaving retail equity capital fully exposed to terminal collapse – is both inequitable and systemically dangerous. It means the entities bearing the least analytical sophistication and risk tolerance are assigned the most vulnerable financial position.

VI. The ADF’s Capacity Without Safeguards

A potential defense of the bill might argue that the Fund lacks the sophistication to implement differentiated financial structures. This argument fails on the bill’s own terms. The ADF Fund is not a passive investor; it is explicitly designed as a highly active financial engineer. Section 9(1)(tha) mandates the Fund to act as a financial intermediary to help structure and mobilize capital. Section 9(1)(Da) positions it as a fund manager. Section 9(1)(Dha) requires it to provide consulting services for project development. Under Section 9(1)(Chha), the Fund is authorized to structure and issue mixed financial instruments in domestic or foreign capital markets. Section 14(ana) grants the Board the authority to convert debt into equity dynamically. Section 9(1)(ja) explicitly directs the Fund to actively develop the secondary market for its securities. The Fund is even mandated to arrange hedging for international loans under Section 9(1)(wa) and to structure joint ventures with international financial institutions under Section 50.

The Fund, therefore, possesses all the statutory tools required to structure specialized, finite-life fixed-income instruments for terminal BOOT projects. Its failure to do so – or rather, the bill’s failure to mandate that it do so – is a legislative design choice, not a limitation of institutional capacity. This makes the systemic risk not an accidental oversight but a structural gap in an otherwise sophisticated financial framework.

VII. Policy Recommendations

To prevent the ADF Fund from becoming a vehicle that inadvertently facilitates the transfer of terminal asset risk to retail investors, the following amendments to the bill are proposed. These recommendations are grounded in the principle that the financial instruments offered to the public must accurately reflect the economic substance of the underlying asset.

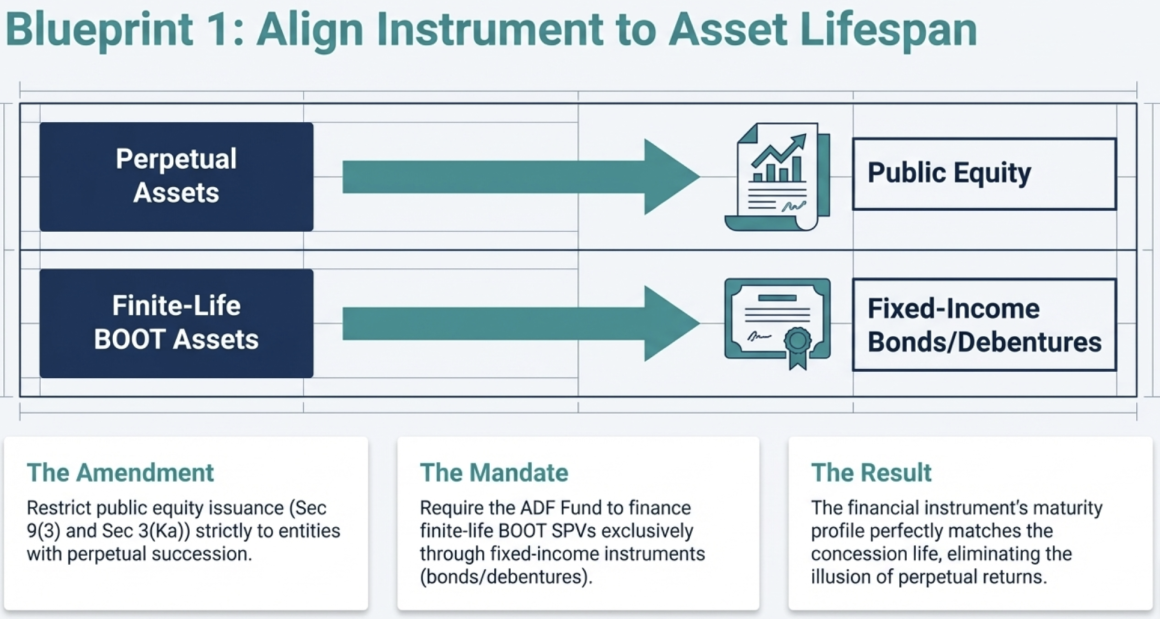

Recommendation 1: Restrict Public Equity Issuance to Entities with Perpetual Succession

The issuance of equity to the general public and its listing on the stock exchange is structurally premised on the assumption of perpetual corporate existence and indefinite upside potential. This assumption does not hold for infrastructure SPVs operating under fixed-term concession agreements. The bill should be amended to explicitly provide that public equity issuance and stock exchange listing under Section 9(3) and Section 3(Ka) are legally restricted to entities with perpetual succession – that is, entities whose underlying assets are not subject to mandatory state transfer at the end of a concession period. For finite-life SPVs under BOOT models, the ADF Fund should be mandated to raise capital through fixed-income instruments – such as bonds and debentures – whose maturity profiles are aligned with the project’s concession life. This ensures that the financial instrument accurately reflects the time-bound, amortizing nature of underlying cash flows, rather than mischaracterizing them as perpetual equity returns. The Fund’s existing statutory capacity to structure blended and mixed instruments under Section 9(1)(Chha) and Section 2(Jha) provides more than adequate legal basis for this approach.

Recommendation 2: Establish a Distinct Trading Class in the Secondary Market

If public participation in finite-life SPVs is nevertheless permitted, the bill must require the creation of a separate and clearly distinguishable trading class within the secondary market for equity instruments. This class should explicitly identify instruments as equity in finite-life concession entities, distinct from conventional perpetual equity. Section 28 should be amended to mandate that such classification triggers enhanced disclosure requirements – including concession expiry profiles and terminal transfer conditions – mandatory warnings regarding terminal value erosion, and specialized valuation frameworks that incorporate declining residual value over time. This would formally recognize the debt-like nature of concession equity and force the market to price in the instrument’s economic expiry, protecting retail investors from mispricing risks and abrupt capital loss at the end of the concession period. Currently, Section 28(2) applies uniform, government-bond-like secondary market treatment to all Fund instruments, and the prevailing Company Act (applied via Section 54) makes no distinction between finite-life and perpetual companies. Without an explicit legislative mandate in the ADF bill, no separate trading class can emerge.

Recommendation 3: Mandate Terminal Value Disclosures for All Concession-Based Instruments

The bill’s existing transparency provisions under Sections 35, 37, and 48 should be supplemented with a specific statutory requirement that any financial instrument issued to the public for a project operating under a concession or PPP agreement must be accompanied by mandatory disclosure of the concession period and remaining life of the asset, the transfer conditions at the end of the concession (including whether transfer occurs at zero compensation), terminal value assumptions and their impact on projected investor returns, and the declining residual value trajectory of the instrument over the concession’s remaining life. This requirement should apply at the point of issuance, in periodic reporting under Section 35, and in secondary market disclosures. Without this, the bill’s delegated legislation under Section 35(3) provides no assurance that future rules will address this gap, as the primary statute provides no directive to do so.

Recommendation 4: Require Structured Exit Mechanisms for Finite-Life SPV Equity

If retail equity issuance in finite-life SPVs is permitted, the bill should require structured exit mechanisms for investors as the concession nears expiry. This could include mandatory buyback provisions triggered at defined intervals before concession expiry, compulsory conversion of equity into fixed-income instruments (aligned with the Fund’s existing debt-to-equity conversion authority under Section 14(ana)), or a sinking fund mechanism funded from project revenues to provide terminal liquidity. The absence of any structured exit in the current bill – where the only exit is the secondary market – guarantees that the financial shock of a terminal asset’s expiry will be absorbed entirely by the last holders of the equity, who will overwhelmingly be retail investors.