Nepal is preparing to build the most technically sophisticated hydropower project in its history on a river that originates in Tibet, flows past three Indian-controlled dams, and drains into the Ganges. The Upper Arun Hydroelectric Project (UAHEP) – 1,063 MW, peaking run-of-river, Sankhuwasabha district, 15 kilometres from the Chinese border – is simultaneously a flagship energy project, a sovereignty declaration, a geopolitical flashpoint, and an unfinished financing transaction. It has been imagined since 1985, suspended in 1995, revived in 2011, redesigned twice, and has consumed approximately USD 34 million in pre-construction expenditure without yet achieving financial closure.

This article covers everything that matters about Upper Arun: the engineering, the development history, the cascade geometry, the financing structure and its stress points, the PPA framework, the retail investor reality, the geopolitical triangle involving India, China, and the World Bank, the critical transmission infrastructure, the full risk landscape, and what Nepal must do in the next 24 months before the strategic window closes.

1. Technical Specifications

Upper Arun is a Peaking Run-of-River (PRoR) project – not a storage dam. It does not retain water across seasons. Instead, it captures the Arun River’s exceptional natural head and converts it into six hours of maximum-capacity electricity every day, year-round. That distinction – reliable daily firm power, not just monsoon surplus – is what makes it commercially and strategically exceptional.

Core Parameters

| Parameter | Specification |

| Installed Capacity | 1,063.36 MW (6 × 173.33 MW Pelton turbines) |

| Project Type | Peaking Run-of-River (PRoR) |

| Annual Energy Generation | 4,531 GWh (including 18 GWh eco-flow) |

| Year-Round Peaking Capacity | 697 MW × 6 hours/day minimum |

| Net Hydraulic Head | 508.3 metres |

| Design Discharge | 235 m³/s |

| Dam Type | RCC Gravity Dam |

| Dam Height | 100 metres |

| Dam Crest Length | 183 metres |

| Dam Site | Narrow gorge 350m upstream of Chepuwa Khola, near Chepuwa village |

| Headrace Tunnel | 8.4 km length |

| Sediment Bypass Tunnel | 1.4 km |

| Underground Desanding Chambers | 3 (in series) |

| Pressure Shaft | 484m vertical, 7.3m diameter |

| Underground Powerhouse | 230m × 25.7m × 59.4m |

| Turbine Type | Pelton (6 units) |

| Powerhouse Location | Chhongryang, near confluence of Arun and Leksuwa rivers |

| Transmission to Grid | 5.79 km, 400 kV double-circuit to Haitar Arun Hub substation |

| Project Location | Bhotkhola Rural Municipality, Sankhuwasabha, Koshi Province |

| Distance from Chinese Border | ~15 km |

| Displaced Households | 22 (99% compensation disbursed) |

| Construction Period | 68 months (targeted 2026–2032) |

| License Period | 35 years |

| Total Project Cost | USD 1.43 billion (NPR 214 billion at NPR 150/USD) |

Source: UAHEL Project Profile

Why 508 Metres of Head Changes Everything

The Arun River at the Upper Arun site drops 508.3 metres between the intake structure and the underground powerhouse. To put that in perspective: most Himalayan run-of-river projects operate on heads of 100–300 metres. Upper Arun’s head is nearly double the upper end of that range.

This matters because power output is directly proportional to both flow and head. At 235 m³/s – a relatively modest design discharge – Upper Arun generates 1,063 MW. A comparable project on a lower-head river would need three to four times the water flow to produce the same electricity. This means Upper Arun produces more electricity per cubic metre of water diverted than almost any project in Nepal’s pipeline, and it does so with a sediment bypass system, desanding chambers, and a 484-metre pressure shaft specifically engineered for the challenge.

The six Pelton turbines – the correct turbine type for ultra-high-head applications – each rated at 173.33 MW, will be among the most powerful individual generating units ever installed in South Asia.

The Firm Peaking Characteristic

Nepal’s grid is structurally imbalanced. As documented by the World Bank, over 97% of Nepal’s installed capacity is run-of-river – generating electricity proportional to river flow, peaking massively in the June–November monsoon and collapsing in the December–May dry season. Nepal exports around 1,000 MW daily in wet season while simultaneously importing from India during dry months.

Upper Arun’s 6-hour daily peaking storage reservoir changes this dynamic at a project level. By storing water during off-peak hours and releasing it in coordinated six-hour bursts, the project delivers 697 MW of firm power daily regardless of season – including in February, Nepal’s peak demand and lowest natural river-flow month. This dry-season firm capacity is Nepal’s most commercially valuable electricity product and its most strategically significant, reducing winter import dependence from the same country that controls the pricing and volume of those imports.

2. Development History: Four Decades

| Period | Milestone |

| 1985 | JICA Master Plan Study identifies Upper Arun’s potential for the first time |

| 1986 | NEA reconnaissance study recommends proceeding to feasibility |

| 1987 | Feasibility Phase I: Morrison Knudsen proposes 350 MW, USD 371 million |

| 1991 | Feasibility Phase II: Morrison Knudsen/Lahmeyer JV – 335 MW PRoR scheme, USD 479 million |

| 1995 | World Bank withdraws from downstream Arun III; Upper Arun suspended indefinitely |

| 2011 | NEA Project Development Department reviews 1991 study; estimates USD 750 million revised cost |

| 2013 | Cabinet authorises NEA to develop Upper Arun under government ownership (February) |

| 2017 | UAHEL incorporated as dedicated SPV (January 25) |

| 2018 | Cabinet formally decides development under UAHEL subsidiary (September 21) |

| 2018–19 | CSPDR-Sinotech JV contracted for optimisation; recommends 1,040 MW |

| 2019 | Survey license issued; Updated Feasibility Study (July/November); access road design finalised |

| 2020 | NEA obtains survey license from DoED (August) |

| 2021 | Updated Feasibility Study completed (May); current 1,063.36 MW design established |

| 2022 | Land acquisition cut-off date set (August); FPIC achieved (December 11) – first in WB global portfolio for project of this scale Free, Prior, and Informed Consent (FPIC) is a specific, collective right for Indigenous Peoples recognized under international human rights law (e.g., UN Declaration on the Rights of Indigenous Peoples). Indigenous community of Tamang and Lhwomi (Singbaba) people present in Sankhuwasabha District. |

| 2023 | Access road contract signed with Gayatri/Kankai JV (March); camp facilities contracted The 21.19 km access road for the Upper Arun Hydropower Project serves as the critical link between the powerhouse site at Chorang and the dam site at Rukuma Phedi in the Bhotkhola Rural Municipality. Navigating the rugged Himalayan terrain of Sankhuwasabha, the route features a 2.03 km road tunnel and a major 70-meter steel arch bridge over the Arun River. This infrastructure is essential for transporting heavy machinery and materials to the headworks, transforming a previously inaccessible region into a functional construction hub. |

| 2024 | Tractebel Engineering JV contracted for detailed design (February); ESIA/CIA disclosed (January) |

| April 2024 | World Bank “in-principle” agreement with Nepal Finance Minister – not Board approval |

| August 2024 | Financial closure deadline missed (original target) |

| Late 2025 | Nepal announces pivot to domestic financing model |

| January 2026 | Ministry of Finance grants in-principle approval for domestic financing |

| April 2026 | Financial closure pending; PPA unsigned; construction not commenced |

Source: UAHEL

The 1995 suspension is the defining event in Upper Arun’s history. When World Bank President James Wolfensohn withdrew from Arun III following civil society opposition, he effectively froze the entire Arun cascade for nearly two decades. That same project – now upgraded to 900 MW – is being completed by India’s state-owned SJVN Limited under a BOOT concession, with no Nepalese public equity and 78.1% of revenues going to India for 30 years. That outcome is the direct consequence of Nepal’s 1995 loss of multilateral financing. It is also precisely the scenario that Nepal is determined not to repeat with Upper Arun.

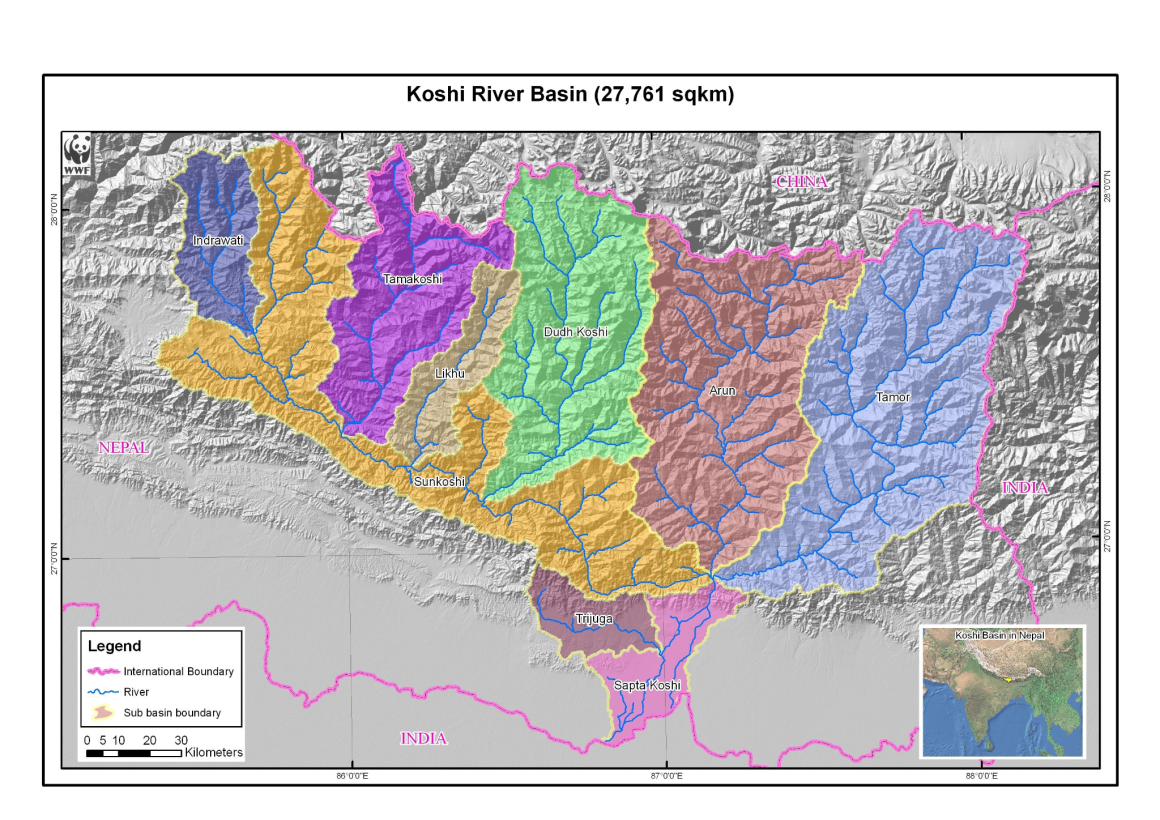

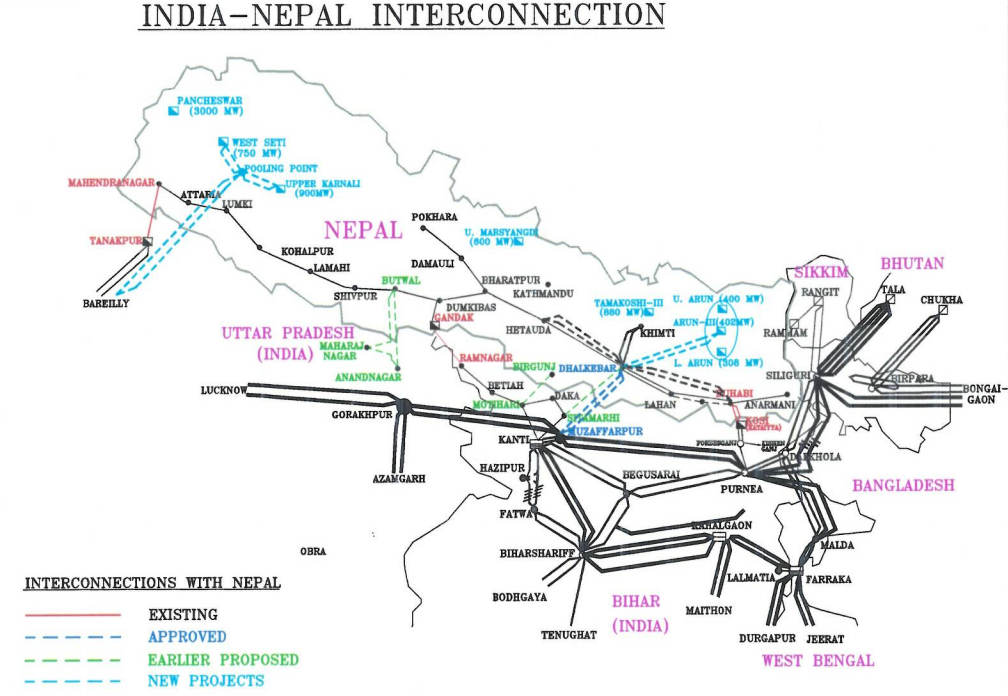

3. The Arun Cascade: Why Position Matters

Upper Arun sits in the middle of a six-project cascade on the Arun River. Understanding the cascade is essential to understanding why this project carries strategic weight beyond its electricity output.

| Position | Project | Capacity | Developer | Model | Nepal Revenue Share |

| Uppermost | Kimathanka Arun | 454 MW | VUCL (GoN) | 100% Nepal | 100% |

| 2nd from top | Upper Arun | 1,063 MW | UAHEL (NEA) | 100% Nepal | 100% |

| 3rd | Arun III | 900 MW | SJVN (India) | BOOT – 30 years | 21.9% (free power only) |

| 4th | Arun IV | 490 MW | SJVN + NEA JV | BOOT | 21.9% |

| 5th | Lower Arun | 669 MW | SJVN (India) | BOOT | 21.9% |

| Downmost | Ikhuwa Khola (companion) | 40 MW | UAHEL | 100% Nepal | 100% |

Source: UAHEL; Arun III Wikipedia; Nepali Times

See the complete map here. See Upper Arun Project Location here.

Under SJVN’s BOOT model: SJVN operates Arun III, Arun IV, and Lower Arun for 30 years. Nepal receives 21.9% of generated electricity as free power. Nepal’s retail public holds zero equity. After three decades, SJVN hands over fully depreciated assets to Nepal at residual book value – which after 30 years of depreciation is close to zero. SJVN’s stated goal is 5,000 MW across Nepal by 2030. It already controls 2,059 MW of the Arun cascade.

Upper Arun – 100% owned by Nepal through UAHEL – sits directly above this Indian-controlled cluster. Whoever operates Upper Arun controls the flow regime feeding all three SJVN projects downstream. That is not incidental. It is the commercial and strategic reason India sought either ownership or operational influence over this project, and why Nepal’s decision to retain full sovereign control represents a structurally significant assertion in the cascade.

SJVN has proposed expanding Arun IV’s capacity from 490 MW to 630 MW, which would extend Arun IV’s project boundary into Upper Arun’s operational zone. This territorial overlap – never formally adjudicated by Nepal’s Department of Electricity Development – is an unresolved dispute that SJVN will use as operational leverage once Arun III commissions. Nepal must formally rule on this boundary before financial closure.

4. Financing Architecture

The Two Pathways and What They Actually Cost

Upper Arun’s total project cost is USD 1.43 billion (NPR 214 billion) under a 70:30 debt-to-equity ratio.

Equity Structure (30% = NPR 64.2 billion / USD 428 million)

| Equity Holder | Share | Amount (NPR) | Amount (USD) |

| NEA (through UAHEL) | 41% | NPR 29.49 bn | USD 197M |

| EPF, CIT, SSF, HIDCL, Nepal Telecom, Provincial/Local Govts | 10% | NPR 6.42 bn | USD 43M |

| Public (NRNs, migrant workers, general public – IPO) | 49% | NPR 31.4 bn | USD 209M |

| Total Equity | 100% | NPR 64.2 bn | USD 428M |

Debt Structure – Pathway A: World Bank-Led International Consortium (70% = USD 1.0 billion)

| Lender | Committed | Status |

| World Bank | USD 550M | “In principle” only – not Board approved |

| European Investment Bank | Targeted | Part of USD 1bn consortium – not confirmed |

| JICA | Targeted | Part of USD 1bn consortium – not confirmed |

| Total International Debt | ~USD 1.0bn | Unconfirmed |

Debt Structure – Pathway B: Domestic Fallback (70% = NPR 149.8 billion / USD ~1.0 billion)

| Source | Amount (NPR) | Amount (USD) | Status |

| HIDCL-led consortium (EPF, CIT, Rastriya Banijya Bank, Nepal Bank) | NPR 53 bn | USD 353M | MOU signed August 2022 |

| Commercial banks | NPR 42 bn | USD 280M | Uncommitted |

| Domestic energy bonds | NPR 50 bn | USD 333M | Policy stated, not issued |

| NEA internal resources | Balance | – | Dependent on NEA profitability |

Source: Nepali Times; UAHEL; Clickmandu

The USD 64 Million Annual Gap That No One Is Talking About

The choice between these two pathways is not merely administrative. It changes the project’s entire financial geometry.

| Debt Scenario | Rate | Tenor | Annual Debt Service |

| World Bank concessional | ~2% | 30 years | ~USD 44 million/year |

| Domestic fallback | ~9% | 20 years | ~USD 108 million/year |

| Difference | USD 64 million/year |

USD 64 million per year in additional debt service – every year for 20 years – must come from somewhere. Either the ERC approves a substantially higher PPA tariff than the current NPR 10.55/4.80 (dry/wet) PRoR rates. Or NEA subsidises the difference from its own budget. Or equity investors accept materially lower returns than the 17% ceiling advertised under ERC regulations. None of these outcomes has been publicly modelled or disclosed.

The “In Principle” Problem

Nepal’s public discourse has consistently conflated the World Bank’s April 2024 “in-principle” agreement with actual financing. They are categorically different things.

“In principle” agreement means a regional Vice President expressed non-binding interest in exploring financing. A formal Board approval – the only instrument that actually commits World Bank funds – requires: completed project appraisal (12–18 months minimum); full compliance with the World Bank’s Environmental and Social Framework; resolution of transboundary consultation requirements under Operational Policy 7.50, which mandates notification and non-objection from downstream and upstream riparian states – meaning India and China. India has not formally withdrawn its objections. The World Bank Board has not voted. The April 2024 agreement has produced no downstream progress toward formal approval.

Treating “in principle” as equivalent to committed financing is not just analytically incorrect – it creates false confidence among domestic institutional investors and delays the hard decisions on the domestic fallback structure.

5. PPA Framework and Tariff Viability

Upper Arun is classified as a PRoR project under Nepal’s electricity purchase framework. The ERC-approved tariff structure applies:

| Season | Period | Approved Rate |

| Dry Season | December – May | NPR 10.55 per unit |

| Wet Season | June – November | NPR 4.80 per unit |

| Escalation | 3% per year | For 8 years |

Unlike Budhigandaki’s storage tariff – where the ERC-approved rates are demonstrably insufficient to cover realistic Nepalese financing costs – Upper Arun’s PRoR tariff is broadly viable under the World Bank concessional scenario. Under the domestic fallback at 9% interest, the viability narrows significantly.

The PPA has not been signed as of April 2026. Under Nepal’s legal framework for domestic investment projects, as documented by Medha Law & Partners, the PPA process takes 12–24 months from initiation to signing. Without a signed PPA, no lender – domestic or international – will commit to financial closure. This is the single most urgent procedural gap in the entire transaction.

There is a deeper structural problem with Nepal’s PPA framework that the Upper Arun transaction exposes. For domestic investment projects – which both Budhigandaki and Upper Arun are – Nepal’s PPA does not provide for monetary damages if NEA defaults. The developer receives only the right to terminate the agreement and attempt to wheel power to third-party buyers through NEA’s transmission lines. But there are no third-party buyers – NEA is the only legal purchaser of electricity in Nepal. This makes the domestic investment PPA materially less bankable than a foreign investment PPA, and represents a governance gap that Nepal’s institutions have not addressed.

The June 2025 attempt to shift all run-of-river PPAs to a “take-and-pay” model – where NEA pays only for electricity it actually uses – was reversed after industry pressure. But the attempt itself revealed something important: NEA is already under financial stress sufficient to prompt it to seek unilateral renegotiation of fundamental PPA terms. Any Upper Arun PPA will need to be negotiated against this institutional backdrop.

6. NEA’s Financial Distress as the Dominant Equity Holder

This is among the most underreported transaction risks in the Upper Arun story.

NEA holds 41% of equity in UAHEL – a commitment of NPR 29.49 billion (USD 197 million). This must be deployed over approximately 68 months of construction. The annual average equity call on NEA is roughly NPR 5.2 billion per year, rising to NPR 8–12 billion in peak construction years.

Against this obligation, consider NEA’s financial position:

| Metric | FY 2024/25 |

| Profit Before Tax | NPR 9.06 billion |

| Year-on-Year Change | −37.32% |

| Revenue from Electricity Sales | NPR 125.27 billion |

| Electricity Purchase Cost | NPR 77.10 billion (+11.73% YoY) |

| Total Assets | NPR 684.91 billion |

| Installed Capacity | 3,591 MW |

Source: Rising Nepal Daily, August 2025

NEA’s entire annual profit is NPR 9.06 billion. Its annual equity commitment to Upper Arun in peak construction years is NPR 8–12 billion. This means Upper Arun’s equity call could consume between 88% and 133% of NEA’s annual profit in peak years – while NEA simultaneously manages its own generation portfolio, its electricity purchase obligations from 3,591 MW of existing projects, and its debt service on prior borrowings including Yen-denominated loans whose cost has risen due to Yen appreciation.

NEA’s profitability decline is structural, not cyclical. The drop in Indian electricity exchange prices during wet season – when Nepal exports its surplus at competitive market rates – directly reduces NEA’s export revenue. As Nepal adds more run-of-river capacity (including all the cascade projects coming online between 2025–2028), wet-season export prices will fall further as Nepal’s surplus grows but India’s own renewable energy build-out reduces its import appetite.

An equity holder in secular financial decline is a transaction risk for every financier considering whether NEA can deliver its committed equity on schedule.

7. Public Equity: The Retail Investor Reality

The government’s “Nepal ko Paani, Janta ko Lagaani” programme allocates 49% of UAHEL equity to public investors – NRNs, migrant workers, and the general public. This democratic ownership model has political appeal. The financial reality requires careful examination.

The Timeline Problem

A retail investor who subscribes to Upper Arun’s IPO – expected perhaps in 2027 or 2028 – faces the following timeline:

| Phase | Duration | Investor Receives |

| Construction | 68 months from commencement | Nothing – no revenue |

| Testing and trial | 6–12 months | Nothing – no stable revenue |

| First stable dividend | ~Year 7–8 from subscription | First dividend possible |

This 7–8 year dividend-free period – during which the investor’s capital earns nothing while inflation erodes its real value – is the “dividend desert” that characterises Nepal’s large hydropower IPOs.

The IRR Reality

Under ERC regulations, Upper Arun’s PPA tariff is calculated to deliver a maximum 17% return on equity. But this assumes:

- No construction cost overruns

- On-time commissioning

- Full PPA revenue with no NEA payment delays

- No transmission constraints

- No hydrological shortfalls

The precedent from Nepal’s most comparable project is instructive. As documented by the Employees Provident Fund, Upper Tamakoshi’s equity IRR fell from a promised 15% to 12% from cost overruns alone – before any hydrological, market, or transmission risk materialised. The project has a 35-year license expiring in 2055 and the shortening remaining license period further erodes equity value with each passing year.

For Upper Arun, realistic equity IRR under optimistic assumptions: 13–16%. Under moderate stress (cost overrun, commissioning delay): 10–13%.

The relevant comparison: Nepal’s commercial banks currently offer fixed deposit rates of 8–9% per annum with full liquidity. For a retail investor to earn a premium over fixed deposits from Upper Arun equity, they need to receive at minimum 11–12% IRR after waiting 7–8 years for the first rupee of return. That is achievable – but it is not guaranteed, and Nepal’s listed hydropower track record is sobering: 17 of 31 (sampled) NEPSE-listed hydropower companies currently pay zero dividends.

8. Geopolitics: The India-China-Nepal Triangle

Why This River Is Not Just Nepal’s

The Arun River originates in Tibet as the Phung Chu, crosses into Nepal at Kimathanka, flows through Nepal for approximately 70 kilometres, and eventually joins the Saptakoshi before entering India and merging with the Ganges. It is a transboundary waterway – which means it triggers the World Bank’s Operational Policy 7.50 on Projects on International Waterways, requiring notification and non-objection from upstream and downstream riparian states.

In the case of Upper Arun: the upstream riparian is China. The downstream riparian is India. Both have reasons to want influence over this project.

India’s Position

India’s engagement with Upper Arun is driven by two distinct but overlapping imperatives.

The commercial/operational interest: SJVN’s three Arun cascade projects – Arun III (900 MW), Arun IV (490 MW), Lower Arun (669 MW) – generate over 2,000 MW of electricity in which Nepal receives only 21.9% as free power. SJVN has an explicit corporate target of 5,000 MW in Nepal by 2030. For SJVN, Upper Arun is the upstream project whose daily peaking releases directly determine the operational efficiency of all three downstream installations. India wants operational coordination over Upper Arun’s dispatch schedule – not merely for technical reasons, but because controlling that schedule is equivalent to controlling the cascade’s output.

India’s request to shift the Upper Arun dam 100 metres upstream was framed as a technical dispute about protecting Arun III’s land and water rights. It was also a tactical move to establish the precedent that India has standing to influence Upper Arun’s design.

The security interest: Following the June 2020 Galwan Valley clash, India’s Ministry of Finance issued General Financial Rules Amendment (OM No. 6/18/2019-PPD, July 23, 2020) restricting public procurement from countries sharing a land border with India on national security grounds. India applied this logic to Nepal’s hydropower sector – effectively pressuring Nepal to exclude Chinese contractors and equipment from Upper Arun, and then using the World Bank’s transboundary consultation requirement to delay multilateral financing that India had not endorsed. India reportedly even leaned on the Indian-born World Bank President Ajay Banga to cancel a Kathmandu visit – a signal of how sensitive India’s position on this project had become.

China’s Position

China’s influence over Upper Arun is structural, not diplomatic. As the uppermost riparian, China controls the headwaters. The Arun originates on the Tibetan Plateau near Mount Xixabangma and drains a Tibetan catchment of approximately 23,000 square kilometres before entering Nepal. This gives China what is effectively a hydrological veto – not through treaty but through geography.

Chinese engineering firms CSPDR and Sinotech conducted the optimisation studies that produced Upper Arun’s current 1,063 MW design. Their technical standards and design parameters are embedded in the project’s engineering documentation. As of early 2026, Chinese investment has been formally ruled out – but China’s technical influence over the design remains, as does its upstream control over the river.

China’s interests include preventing total Indian operational dominance over the Arun cascade, maintaining the option for trans-Himalayan grid connectivity, and using Nepal’s hydropower sector as part of a broader economic linkage between Tibet and South Asia.

A July 2025 GLOF event at Gyirong land port in Tibet – causing deaths and significant infrastructure damage – underscores that active glacial dynamics in the region are not theoretical. China monitors these developments and, critically, Nepal has no bilateral agreement with China requiring upstream notification of water management decisions on the Arun/Phung Chu system.

Nepal’s Strategic Pivot

By late 2025, Nepal concluded that international financing – specifically the World Bank pathway – had become a mechanism through which India was exercising geopolitical leverage over a sovereign infrastructure decision. The solution was direct: shift to a fully domestic financing model, eliminating the international clearance processes that required India’s non-objection.

The Ministry of Finance granted in-principle approval for domestic financing in January 2026. This was a genuinely bold move. It came at a cost – the domestic financing pathway is materially more expensive than concessional multilateral debt, as quantified in the financing section above. But it preserved Nepal’s operational and commercial sovereignty over the project.

The question now is whether Nepal’s domestic institutions can actually deliver the financing at the scale and tenor the project requires – a question addressed in the fiscal capacity analysis below.

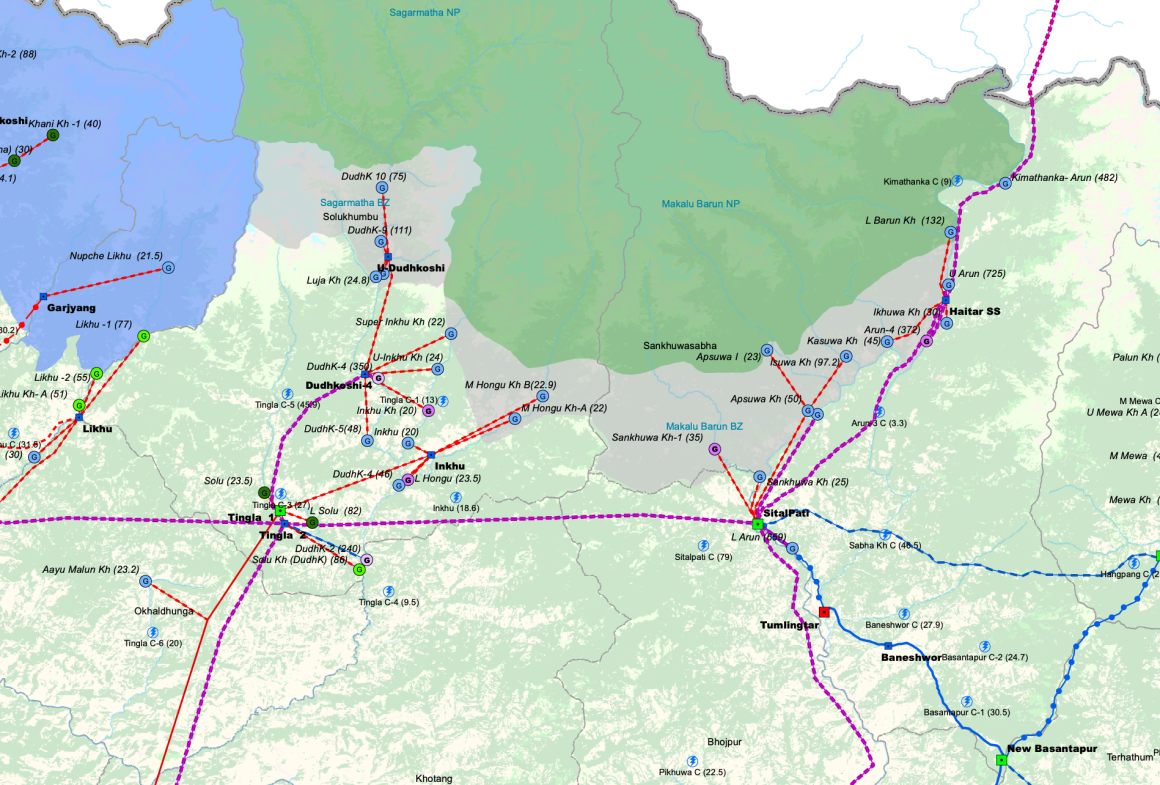

9. The Haitar Substation: Who Controls the Hub

All electricity generated at Upper Arun’s underground powerhouse at Chhongryang is evacuated through a 5.79 km 400 kV double-circuit transmission line to the 400 kV Arun Hub substation at Haitar, Sankhuwasabha. Haitar is the single convergence point for electricity evacuation from the upper Arun cascade – including Kimathanka Arun (454 MW) and Upper Arun itself.

See the complete complete Transmission Line Masterplan of Nepal here.

Who owns Haitar? The substation is developed under NEA’s own Project Management Directorate as part of the Arun Hub-Tingla 400 kV transmission project – Nepal’s sovereign national grid infrastructure. It is not SJVN infrastructure. It is not jointly operated with India.

SJVN’s Arun III electricity is evacuated through an entirely separate corridor – a 300 km 400 kV line from Diding to Dhalkebar in Nepal, then to Muzaffarpur in India. SJVN funded an extension of Nepal’s Dhalkebar substation for Arun III’s interconnection, but the substation itself remains NEA property.

This is significant. It means Nepal controls the physical hub through which the upper cascade’s Nepalese projects connect to the national grid. India cannot physically constrain Upper Arun’s grid access without interfering with Nepal’s sovereign transmission infrastructure – a very different leverage position than if Haitar were jointly operated or SJVN-funded.

However, this advantage comes with a critical timing risk: the Haitar-to-Tingla evacuation corridor – the path that carries Upper Arun’s power southward into the national grid – must be commissioned before Upper Arun generates its first electricity. If the transmission infrastructure is delayed, Upper Arun commissions into a grid it cannot fully evacuate, creating “deemed generation” payment obligations for NEA on electricity it cannot physically receive. This mismatch must be managed through coordinated construction scheduling, which is not currently publicly documented.

10. Risk Landscape

GLOF: The Teesta III Warning Nepal Must Not Ignore

The October 2023 destruction of the 1,200 MW Teesta III hydropower project in Sikkim by a glacial lake outburst flood from South Lhonak Lake is the most direct precedent for Upper Arun’s GLOF risk. The Teesta III dam – a 60-metre structure on a glacially-fed river, built at USD 1.7 billion, in terrain directly comparable to the Arun basin – was completely washed away within hours.

The insurance lesson from Teesta III is devastating in its specificity. The project carried total insurance coverage of approximately NPR 11,400 crore. But the GLOF-specific sublimit in the policy was only NPR 500 crore – 4.4% of the total sum insured, for the most relevant catastrophic risk. The remaining coverage applied to flash floods and cloudbursts. Since the central government’s investigation committee classified the event as a GLOF, not a cloudburst, the effective insurance recovery was capped at a fraction of the project’s actual loss. Two years later, the claim remains unresolved in legal dispute.

The Arun basin’s own GLOF history is not hypothetical. Two events are documented in the Barun Khola tributary of the Arun. Ten transboundary GLOF events from Tibet have entered Nepal since 1935. A 2017 rockfall-triggered GLOF in the Barun Valley formed a 2–3 km lake at the Barun-Arun confluence. GLOF frequency is increasing across the China-Nepal border area as glaciers accelerate their retreat.

Upper Arun’s 100-metre RCC gravity dam is lower than Teesta III’s 60-metre structure was when struck. A GLOF arriving with peak discharge exceeding the spillway’s design capacity could overtop the structure. The World Bank’s heightened E&S risk classification for Upper Arun is partly driven by exactly this concern.

Nepal has not publicly disclosed:

- Whether Upper Arun’s insurance policy carries a GLOF-specific sublimit

- What the design flood includes beyond probabilistic rainfall events

- Whether the project design incorporates GLOF-augmented flood discharge in the Probable Maximum Flood calculation

- Whether an Early Warning System is planned for upstream glacial lakes

These are not optional disclosures. They are fundamental bankability requirements that every serious lender – including any domestic institutional investor – should demand before committing capital.

Sediment: The Slow Degradation That No Financial Model Acknowledges

The Arun River carries approximately 8.26 million tonnes of sediment per year (including estimated bed load). Three underground desanding chambers and a 1.4 km sediment bypass tunnel are specifically designed to manage this load. The engineering is sophisticated. But no sediment management system eliminates the problem – it mitigates it.

Over 35 years of operation, progressive siltation of the diurnal peaking reservoir will reduce live storage volume. As storage shrinks, Upper Arun transitions from a 6-hour daily peaking project toward a 5-hour, then 4-hour peaking project. Each lost hour of dry-season peaking at NPR 10.55/unit costs approximately NPR 7.4 billion (USD 49 million) in cumulative revenue over the remaining license period.

The six Pelton turbine runners are also subject to abrasive wear from the fine sediment that passes through the desanding system. Periodic runner replacement – at significant cost – is required to maintain generation efficiency. This is an operational cost that standard financial models for Himalayan hydropower projects typically understate or ignore.

Sediment flushing – releasing accumulated material by opening dam gates – is the primary tool for managing reservoir siltation. But flushing releases concentrated sediment pulses downstream. For a standalone project, this is an operational consideration. For Upper Arun, whose downstream neighbour is Arun III, flushing creates a direct conflict: Nepal’s operational need to flush sediment directly threatens SJVN’s turbine efficiency and desanding systems at Arun III. A cascade dispatch and operational coordination protocol – covering both peaking schedules and sediment flushing – does not exist and has never been formally negotiated between UAHEL and SJVN.

Cascade Dispatch Coordination: A Closing Window

This is perhaps the most time-sensitive risk in the entire Upper Arun transaction.

When Upper Arun releases water for 6-hour peak generation, that discharge pulse travels downstream and arrives at Arun III’s intake approximately 4–6 hours later. If Upper Arun and Arun III are both independently optimising their dispatch schedules, their peaking releases can either compound – creating unmanageable flow spikes at downstream intakes – or conflict, reducing system-wide generation efficiency.

There is no bilateral cascade dispatch coordination protocol between UAHEL and SJVN. There is no Nepal-India Arun Cascade Coordination Committee. There is no mechanism in the 1954 Koshi Agreement – which governs the broader river system – for hydropower dispatch coordination between cascade projects.

The moment Arun III begins commercial operation – which is imminent – SJVN will start generating operational data on how Arun III’s intake responds to natural Arun River flow. Once Upper Arun is built and begins peaking releases, SJVN will have concrete technical grounds to demand operational coordination. That demand will be backed by the technical authority of a project that has been operating for several years. Nepal, arriving late with a newly commissioned plant, will negotiate from a weaker position.

The window to establish coordination protocols on Nepal’s terms is now – before Arun III commissions. It is not being used.

Currency Risk: The Structural Mismatch

If the World Bank financing pathway is ultimately pursued, approximately USD 1.0 billion in concessional debt will be denominated in USD or Special Drawing Rights. All of Upper Arun’s revenues will be in Nepalese rupees.

The NPR has depreciated from approximately NPR 75/USD in 2010 to NPR 150.67/USD in March 2026 – a depreciation of approximately 4–5% annually over the period.

At this rate, by Year 10 of Upper Arun’s operation, the NPR cost of repaying USD 1.0 billion in international debt would be approximately NPR 231 billion – a significant increase from the NPR 150.67 billion implied at current March 2026 exchange rates. This is not a marginal risk; it represents a structural exposure of approximately NPR 80 billion in additional effective borrowing costs that typically remains unaccounted for in standard public financial models.

Nepal’s limited domestic foreign exchange hedging is costly and limited to a few years in tenure and the Hedging Regulation 2079 is not yet commercially operational. Consequently, the only viable structural solutions are World Bank lending in NPR (available under specific IDA terms) or a government sovereign guarantee against exchange rate losses or sovereign backed hedging facility – both of which significantly increase Nepal’s contingent fiscal liabilities.

Market Saturation: The 2032 Grid Problem

Upper Arun targets commercial operation in 2032. By that date, Nepal’s grid will have received major additions from: Arun III (900 MW, 2025-26), Lower Arun (669 MW, ~2028-30), Arun IV (~490 MW, ~2027-28), Dudhkoshi (635 MW, ~2031), Kimathanka Arun (454 MW, ~2030-31), and Budhigandaki (1,200 MW, ~2033). Total additions exceed 4,000 MW.

Nepal is already exporting an average of 1,000 MW daily in wet season – the maximum capacity of the primary export corridor, the 400 kV Dhalkebar-Muzaffarpur interconnection. By 2032–2033, Nepal’s wet-season surplus could reach 20,000–30,000 GWh annually. The current transmission capacity cannot handle this.

Upper Arun’s dry-season firm power is protected from this problem – it produces its most valuable electricity precisely when Nepal’s grid is least supplied and most in demand. But wet-season generation (approximately 30% of annual output) will commission into an oversupplied market where prices on the Indian Energy Exchange could be near-zero during peak monsoon periods. No published financial model for Upper Arun explicitly scenarios this.

China’s Upstream Hydrological Control

Upper Arun’s exceptional dry-season performance – the 697 MW for 6 hours that makes the project commercially distinctive – depends on glacially-fed baseflow from the Tibetan Plateau. The Arun catchment in Tibet contains hundreds of glaciers whose meltwater contributes to the river’s dry-season low flow.

Climate models project that Himalayan glacier mass will peak in its meltwater contribution between 2030 and 2060 – the so-called “peak water” phenomenon – before declining as glacier volume is depleted. Post-peak, the Arun’s dry-season baseflow could decline by 15–30% in the second half of this century. For a project designed to peak on 235 m³/s, a 20% flow reduction could reduce output to approximately 190 m³/s – cutting peak capacity from 1,063 MW toward 860 MW and reducing annual generation by 15–20%.

Compounding this, China has no bilateral notification obligation toward Nepal on upstream water management decisions for the Phung Chu/Arun system. Nepal has no legal basis to claim compensation if upstream development reduces the river’s dry-season baseflow. This is an uninsurable structural risk that no treaty framework currently addresses.

11. Pre-Construction Expenditure: What Has Already Been Spent

As of July 16, 2025 (Ashad 32, 2082 BS), UAHEL’s financial statements record the following expenditure:

| Category | Amount (NPR) | Amount (USD) |

| Capital Work in Progress (CWIP) | NPR 2,535,558,154 | ~USD 16.9M |

| Property, Plant and Equipment (net) | NPR 2,396,933,388 | ~USD 16.0M |

| UAHEL total as of July 2025 | ~NPR 4.93 billion | ~USD 32.9M |

| NEA costs pre-UAHEL (Engineering Services) | NPR 599.8 million | ~USD 1.14M |

| Ikhuwa Khola companion project costs | ~USD 0.5M | USD 0.5M |

| Approximate total committed | ~USD 34M |

The CWIP includes consultancy services, infrastructure development, feasibility studies, environmental studies, and social development activities. The PPE category covers land, buildings, and vehicles already acquired.

USD 34 million is significant sunk cost that creates political and institutional momentum for completion. It is also, relative to the USD 1.43 billion total project cost, only 2.4% of the total – meaning 97.6% of the financial commitment lies ahead. The project is deeply pre-construction, not mid-stream.

12. The Post-35-Year Question

Upper Arun’s generation license runs for 35 years from commissioning – approximately to 2067 or 2068. At that point, the physical plant will have been operating for 35 years. Six Pelton turbine runners will have accumulated over 200,000 operational hours – well beyond standard major overhaul cycles. The headrace tunnel will require structural inspection. The pressure shaft casing may need replacement. The dam’s RCC concrete will show four decades of weathering in a high-humidity alpine environment.

Extending operation to 70–80 years – which is technically feasible if civil infrastructure is maintained – requires what the industry calls “rehabilitation CAPEX”: electromechanical replacement typically at 15–20% of original project cost. For Upper Arun at USD 1.43 billion original cost, this means USD 215–285 million in rehabilitation investment at approximately Years 20–25 and again at Years 40–50.

Nepal has no mandatory sinking fund requirement in its regulatory framework – no mechanism by which operating projects accumulate rehabilitation reserves from cash flows. At Year 35, Nepal will inherit a plant requiring hundreds of millions in renovation with no dedicated financial provision for that expenditure. The government of Nepal will need to find those resources from its general fiscal position – which, if current debt trajectory continues, will be considerably constrained.

This is not a problem unique to Upper Arun. It is a systemic gap in Nepal’s infrastructure governance framework that will arrive simultaneously across every major hydropower project commissioned in the 2025–2035 window when their licenses expire in the 2060s.

13. What Needs to Happen?

The next 24 months represent Nepal’s most important window in the entire Upper Arun transaction. Arun III is nearing commissioning. Once it operates, the cascade’s operational facts shift in India’s favour. The window for establishing Nepal’s terms on cascade coordination, haitar governance, and geopolitical positioning closes gradually but irreversibly.

The priority actions, ranked by urgency:

First: Sign the PPA. Nothing else is credible without it. Every financing instrument – domestic or international – requires a signed revenue contract as the foundational bankability document. The ERC approval process alone takes 6–12 months after the application is submitted. Nepal cannot afford further delay.

Second: Formally quantify the domestic vs international financing trade-off. A transparent financial model comparing World Bank concessional and full domestic fallback pathways – including the impact on PPA tariff requirements, equity returns, and NEA balance sheet stress – must be published. Institutional investors including EPF, CIT, and SSF deserve to see this analysis before committing their members’ savings.

Third: Establish the Arun Cascade Coordination Protocol before Arun III commissions. Nepal must – unilaterally if necessary, bilaterally if possible – establish the operational protocol for cascade dispatch, sediment flushing, and maintenance scheduling on Nepal’s terms, while it still controls all upstream cards.

Fourth: Commission an independent GLOF risk assessment using post-Teesta III methodology. The World Bank will require it as a loan condition. Nepal’s domestic lenders should require it as basic due diligence. Doing it now removes a financing obstacle and demonstrates institutional seriousness about risk management.

Fifth: Formally adjudicate the Arun IV boundary overlap. Nepal’s Department of Electricity Development must rule on whether SJVN’s proposed expansion of Arun IV to 630 MW encroaches on Upper Arun’s operational zone. This must happen before Upper Arun’s EPC tender is issued.

Conclusion

Upper Arun is a genuinely exceptional project. Its 508.3-metre hydraulic head gives it generation efficiency that few projects in Asia can match. Its 4,531 GWh of annual output would be the largest in Nepal’s history. Its 22-household social footprint is remarkable for a project of this scale. Its FPIC achievement – the first in the World Bank’s global portfolio for a project of this magnitude – demonstrates institutional maturity in community engagement.

It is also a project that has been planned for 40 years, suspended, revived, redesigned, contested by both its neighbours, and has not yet achieved financial closure. It faces an unsigned PPA, a stressed dominant equity holder, an unresolved GLOF insurance architecture, an imminent cascade coordination crisis, an acknowledged currency risk, and a domestic financing pathway that costs USD 64 million more per year than the international alternative it may never secure.

None of these challenges makes Upper Arun unviable. They make it complex – and complexity, in infrastructure finance, is the environment in which Nepal has historically underperformed. The country’s capital expenditure utilisation averages barely 60% of allocation over the past four years. Its public debt has nearly doubled in six years to NPR 2.878 trillion. The institutional investors it is counting on to fund Upper Arun are simultaneously being asked to fund Budhigandaki, service existing infrastructure loans, and meet their primary mandate of delivering returns to pensioners and depositors.

The project’s logic is sound. Its strategic necessity is clear. The question is not whether Upper Arun should be built. It is whether Nepal’s institutions will bring the same rigour and urgency to the transaction structure that the project’s engineering team has brought to the design. The 24-month window is real. The consequences of missing it – watching India’s operational footprint lock in the cascade dynamics on terms Nepal cannot later renegotiate – are permanent.

Sources and References

UAHEL – Upper Arun Project Profile | Tractebel Engineering on Upper Arun | Nepali Times – Upper Arun Question Mark | Nepali Times – World Bank Flip-Flop | Clickmandu – Domestic Financing Pivot | Khabarhub – Upper Arun Obstacles | Rising Nepal Daily – NEA Profits | Rising Nepal Daily – Public Debt | ERC PRoR Tariff – Himalayan Times | World Bank Nepal Development Update | Annapurna Express – Electricity Exports | Arun III Wikipedia | Teesta III Insurance – The Print | Teesta III GLOF Insurance Gap | Springer – Barun Valley GLOF 2017 | PMC – GLOF Frequency China-Nepal Border | World Bank – Glacial Lakes Nepal | NEA Project Management Directorate – Haitar | PPA Termination Risks – B360 | Take-and-Pay Crisis – Kathmandu Post | Hydro Shareholder Returns – myRepublica | Capital Expenditure – Annapurna Express | Nepal Public Debt Doubling | PPA Legal Framework – Medha Law | Gyirong GLOF Tibet 2025 – Springer | Arun Cascade Map