I. Introduction: The Mirage of Perpetual Growth

1. The Hydropower Gold Rush

The Nepal Stock Exchange (NEPSE) is presently in the grip of what can best be described as a “Hydropower Gold Rush.” Over the past decade – and with particular intensity since FY 2020/21 – the hydropower sector has emerged as the dominant driver of market activity, eclipsing traditional blue-chip sectors in both trading volume and investor attention. This surge has been fueled by a continuous pipeline of Initial Public Offerings (IPOs) and increasingly aggressive 1:1 (100 percent) right share issuances, which have become the principal instruments through which hydropower companies mobilize large volumes of public capital.

Unlike organic capital formation driven by retained earnings or long-term institutional investment, this expansion has been retail-led, speculative, and momentum-driven. Importantly, this retail enthusiasm is not merely market-driven; it is institutionally engineered.

At the core of this architecture lies the Government of Nepal’s “Janata ko Jalvidyut” (People’s Hydropower) policy framework. Section 5 of the People’s Hydropower Program (Operation and Management) Procedure, 2075 mandates that generation companies allocate 49 percent of their equity to the general public, while Section 7 requires priority allocation within this tranche to project-affected local communities. This policy has embedded public shareholding into the very DNA of hydropower project development, effectively transforming retail investors into long-term financiers of infrastructure assets.

2. Market Capitalization: From Peripheral Sector to Market Pillar

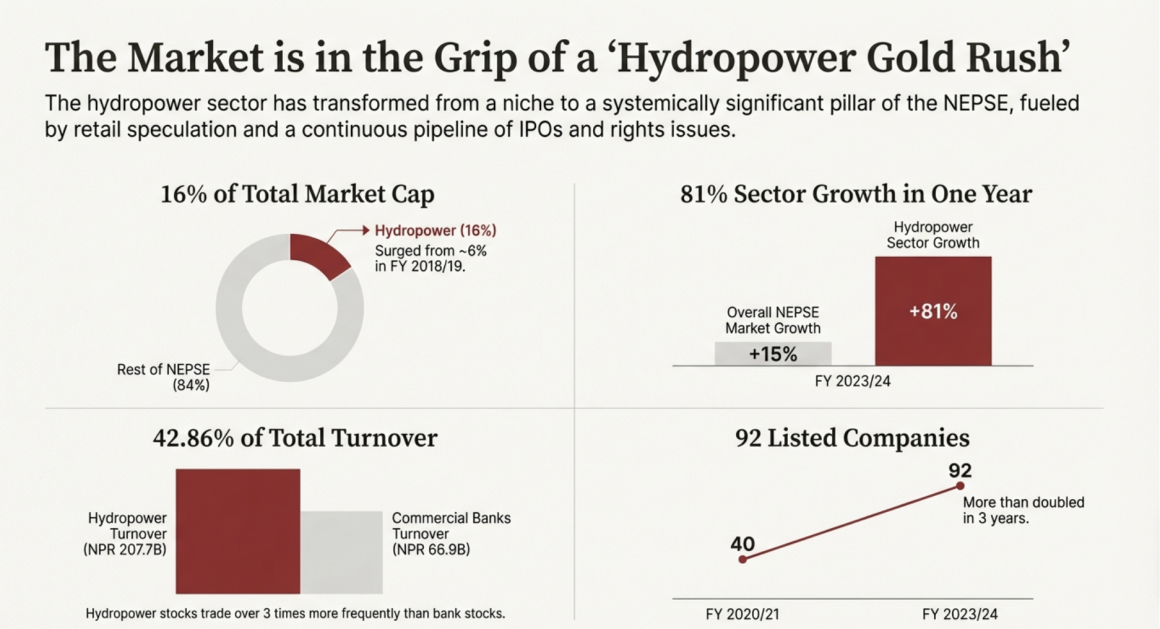

Data from NEPSE Annual Reports reveal that hydropower has transitioned from a peripheral niche to a systemically significant sector within a remarkably short period. Between FY 2018/19 and FY 2023/24, the hydropower sector’s share of total market capitalization expanded from approximately 6 percent to nearly 16 percent, a more than two-and-a-half-fold increase in relative weight within five years.

This growth was not linear but punctuated by three defining moments:

- The FY 2020/21 Breakout: During the post-COVID liquidity surge, hydropower market capitalization tripled, rising from roughly NPR 102 billion to over NPR 342 billion in a single fiscal year. This inflection point coincided with heightened IPO activity, accommodative monetary conditions, and an influx of first-time retail investors.

- Resilience During Market Contraction (FY 2021/22): When total NEPSE market capitalization contracted sharply – declining by over NPR 1.1 trillion – hydropower equities exhibited relative resilience. Although absolute valuations declined, the sector’s share of total market capitalization increased from 8.53 percent to 10.58 percent, indicating capital retention and defensive repositioning by investors within the sector.

- The FY 2023/24 Surge: The most striking development occurred in FY 2023/24. While total market capitalization grew by approximately 15 percent, hydropower sector capitalization expanded by over 81 percent, rising from NPR 313 billion to NPR 567 billion in a single year. As a result, hydropower alone accounted for nearly one-sixth of the entire exchange’s value.

This scale of expansion, concentrated in a single sector composed largely of project-specific companies, is without precedent in Nepal’s capital market history.

3. Liquidity Dominance in Hydropower’s Trade

Market capitalization captures size; turnover captures behavior. On this measure, hydropower’s dominance is even more pronounced. In FY 2023/24: Total NEPSE turnover amounted to approximately NPR 484.5 billion. Hydropower stocks alone accounted for NPR 207.7 billion, or 42.86 percent of total market turnover.

This concentration of liquidity is extraordinary. By comparison, commercial banks – which collectively command nearly double the market capitalization of hydropower – generated turnover of only NPR 66.9 billion during the same period. In effect, hydropower equities were traded over three times more frequently than bank stocks despite their smaller aggregate size. This divergence signals not long-term capital allocation, but high-velocity retail participation, speculative trading cycles, and price discovery driven by momentum rather than fundamentals.

4. Supply-Side Expansion: The Proliferation of Listed Projects

The surge in capitalization and turnover has been reinforced by a rapid expansion in the number of listed hydropower entities.

- In FY 2020/21, NEPSE listed 40 hydropower companies.

- By FY 2023/24, this number had more than doubled to 92, encompassing projects at vastly different stages of development, hydrological risk profiles, and financial maturity.

Crucially, many of these listings are regulatorily induced, arising from mandatory public and local share issuance requirements rather than voluntary market readiness. The result is a market increasingly populated by single-asset, finite-life project companies, each competing for the same pool of retail capital.

5. But Hydros are with a Mandated Date of Death

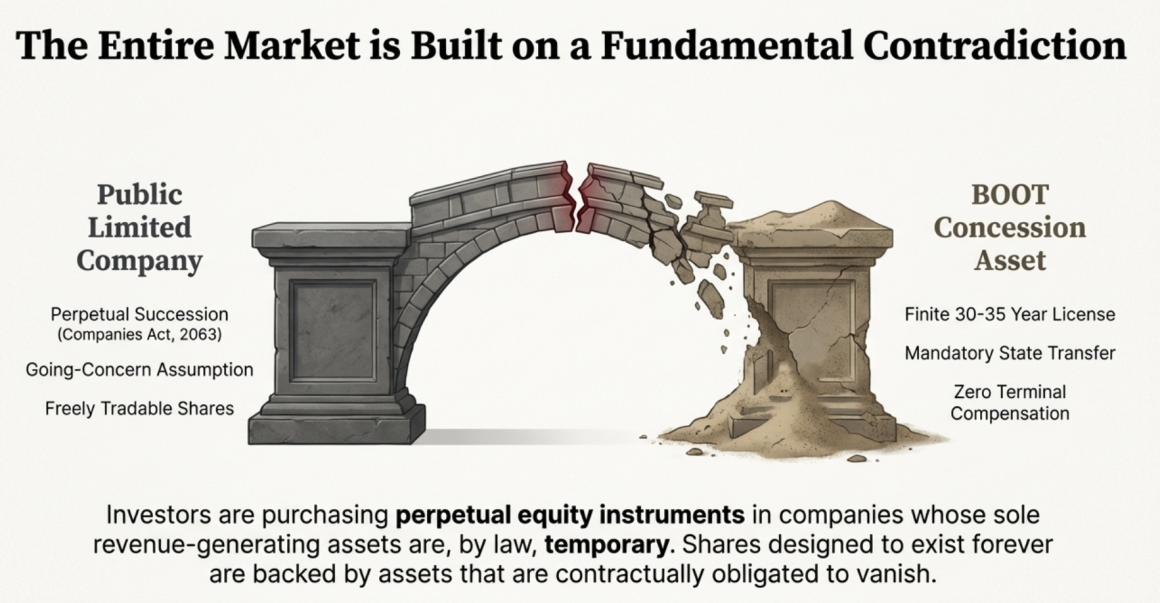

Beneath the optimism of price surges, dividend announcements, and subscription oversubscriptions lies a fundamental contradiction. Investors are purchasing perpetual equity in assets that are, by law, temporary. Under the Companies Act, 2063, listed hydropower companies are incorporated as Public Limited Companies with perpetual succession, and their financial statements are prepared on a going-concern assumption – implying indefinite operation. Yet the legal and regulatory framework governing their revenue-generating assets tells a very different story.

Hydropower projects in Nepal are developed under time-bound licenses, culminating in mandatory transfer of the entire project – dams, powerhouses, and associated infrastructure – to the Government of Nepal. This creates a structural “cliff edge”, where the asset base that sustains cash flows is legally destined to disappear. The consequence is stark: shares designed to exist forever are backed by assets that are contractually obligated to vanish.

6. The Forced Convergence of Three Incompatible Frameworks

The instability of Nepal’s hydropower equity market is not accidental; it arises from the forced convergence of three fundamentally incompatible constructs:

BOOT (Build–Own–Operate–Transfer): Under the Hydropower Development Policy, 2001, private developers receive licenses -typically 35 years for domestic projects and 30 years for export-oriented projects – after which projects must be transferred to the state free of charge and in good running condition.

SPV (Special Purpose Vehicle): To ring-fence financial risk, each project is developed through a dedicated licensee company, legally and financially isolated from other assets. While this structure enhances bankability, it also means the company is a single-asset vehicle with no inherent diversification or residual value beyond the project itself.

Public Listing (Perpetual Equity): Listing on NEPSE introduces perpetual, freely tradable equity into an entity whose only asset is finite. Retail investors, therefore, are encouraged to buy and trade a “forever” financial instrument whose economic foundation is legally temporary.

This mismatch – between perpetual equity, finite licenses, and single-asset corporate structures – is the central structural flaw underpinning Nepal’s hydropower capital market. Current valuations, trading behavior, and regulatory approvals largely ignore this contradiction, setting the stage for future market dislocation unless the architecture itself is re-examined.

II. General Lifecycle of a Hydropower Project in Nepal: A BOOT-Anchored, Finance-Layered Structure

Under Nepal’s prevailing legal and regulatory architecture – principally the Electricity Act, 2049 (1992), Electricity Rules, 2050 (1993), Hydropower Development Policy, 2001, and related directives – the hydropower sector operates under a Build–Own–Operate–Transfer (BOOT) concession framework. This framework governs not only technical development but also determines how bank finance and public capital are sequentially introduced into a project that is, by design, finite in duration.

The lifecycle of a hydropower project can be divided into five interlinked regulatory phases, each marked by escalating legal obligations and financial exposures.

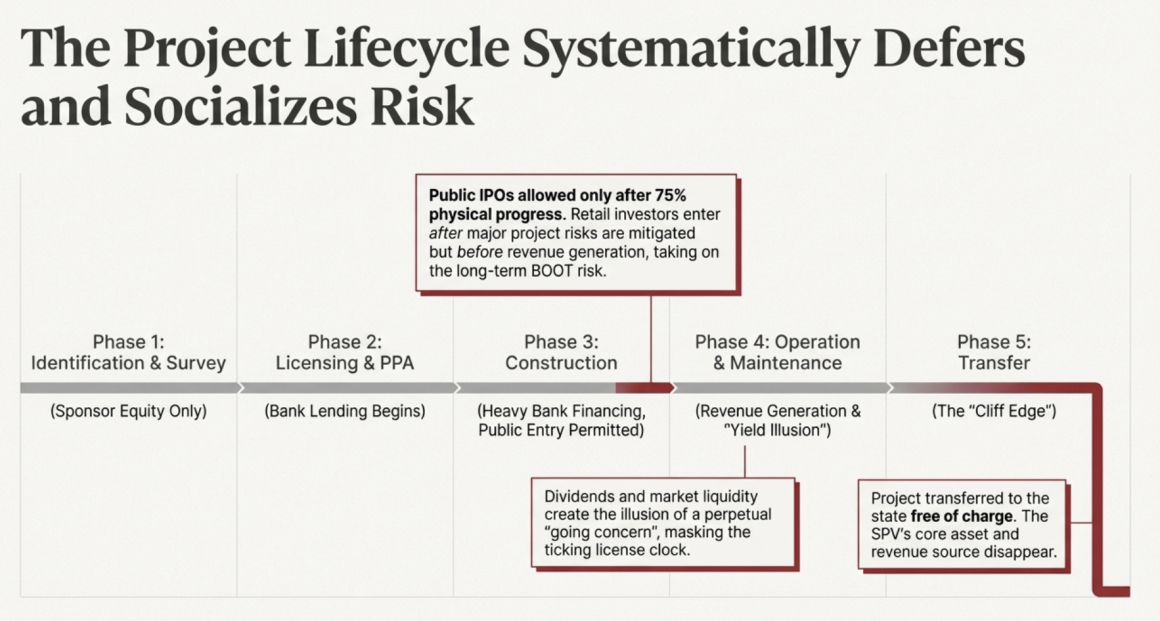

1. Identification and Survey Phase (Entry Phase)

The lifecycle begins with the identification of a hydropower site and the acquisition of legal authority to study it. At this stage, the project exists purely as a regulatory option, not as a bankable or investable asset.

Any person or corporate body intending to conduct a hydropower survey must apply to the Department of Electricity Development (DoED), submitting a project description and site map, as required under section 4(1) of the Electricity Act, 2049 and rule 4 of the Electricity Rules, 2050. The survey license is issued for a maximum duration of five years, pursuant to clause 6.12.11(1) of the Hydropower Development Policy, 2001.

During this period, the licensee is legally obligated to undertake detailed feasibility studies and environmental assessments (IEE or EIA). The Guidelines for Study of Hydropower Projects, 2018 mandate comprehensive hydrological, geological, and sedimentological investigations (clauses 2.1 and 3.1 of the Guidelines). Environmental approval must be secured under the Environment Protection Rules, 2077, failing which project approval lapses if construction does not commence within two years of approval (rule 13 of the Environment Protection Rules, 2077).

At this stage: No public capital is permitted, Bank lending is generally limited to sponsor equity and early-stage risk capital, and the project has no tradable financial identity

2. Generation Licensing and PPA Phase (Development Phase)

Upon successful completion of feasibility and environmental approvals, the project transitions from an exploratory option into a licensed concession asset.

The developer must apply for a Generation License by submitting feasibility studies, environmental approvals, and a financial plan, as required under rule 12 of the Electricity Rules, 2050. Parallel to or preceding license issuance, the developer must execute a Power Purchase Agreement (PPA) with the Nepal Electricity Authority (NEA) or another authorized off-taker. The Electricity Regulatory Commission (ERC) must approve the PPA to safeguard consumer and system interests, pursuant to section 13(1)(c) of the Electricity Regulatory Commission Act.

The generation license is issued for a fixed term, reinforcing the finite nature of the concession:

- Up to 35 years for projects supplying domestic consumption (clause 6.12.11(2)(a) of the Hydropower Development Policy, 2001)

- Up to 30 years for export-oriented projects (clause 6.12.11(2)(b) of the same Policy)

From a financing perspective, this phase marks the entry of formal bank lending. Commercial banks may extend large exposures to hydropower projects under relaxed prudential limits, including:

- Single Obligor exposure of up to 50 percent of Primary Capital, under clause 3.क of NRB Unified Directive No. 3

- Mandatory PPA requirement once exposure exceeds 25 percent of Primary Capital (clause 3.क of Directive No. 3)

However, access to public equity remains restricted. Completion of financial closure is a mandatory prerequisite before eligibility for an Initial Public Offering (IPO), as required under Section I (Prerequisites) of the Securities Registration and Issuance framework.

3. Construction Phase: Bank Dominance and Conditional Public Entry

Once the generation license is granted, the project enters the construction phase, during which regulatory oversight intensifies and capital requirements peak.

The licensee must commence physical construction within one year of license issuance, pursuant to rule 21(1) of the Electricity Rules, 2050. Construction must comply with government-prescribed quality and safety standards under section 23(1) of the Electricity Act, 2049.

This phase is characterized by heavy bank financing, supported by preferential regulatory treatment under the NRB Unified Directives:

- Interest accrued during the grace period may be capitalized for hydropower projects (clause 43.1.क of NRB Unified Directive No. 2)

- Delays due to transmission line non-availability allow partial interest capitalization (clause 43.2 of Directive No. 2)

- Grace period extensions linked to RCOD changes are not treated as loan restructuring (clause 7.ख of Directive No. 2)

Crucially, this phase also marks the conditional entry of public capital. Hydropower companies may issue an IPO only after achieving at least 75 percent physical progress, certified by the relevant authority, or 50 percent under special capital collection provisions, as stipulated under Section I (Prerequisites) and Section III (Special Capital Collection) of the Securities Registration and Issuance Regulation, 2073. Additionally, 10 percent of issued capital must be allocated to project-affected local residents, under Section II of the Securities Issuance and Allotment Directive, 2074.

Thus, retail investors are permitted to enter before revenue generation, but only after banks have already established priority claims over project cash flows.

4. Operation and Maintenance Phase (Commercial Phase)

Upon achieving Commercial Operation Date (COD), the project transitions into its revenue-generating phase. Cash flows during this period are governed by PPA tariffs, hydrology, and regulatory obligations.

Licensees are required to pay royalties to the Government of Nepal in two components:

- Capacity royalty, starting at NPR 100/kW and escalating to NPR 1,000/kW after 15 years (clause 6.13.1 of the Hydropower Development Policy, 2001)

- Energy royalty, rising from 1.75 percent to 10 percent of energy sales after 15 years (clause 6.13.1 of the same Policy)

Operational obligations are detailed in the Guidelines for Operation and Maintenance, 2017, which prescribe maintenance standards for civil and electromechanical components (clauses 4.3.1 and 4.2.1). Emergency or voluntary maintenance must be carried out promptly, with public notification, under section 27 of the Electricity Act, 2049.

From a banking perspective, loan classification rules become active: Installments overdue by more than 90 days are classified as “Loss” with 100 percent provisioning (clause 4.2 of NRB Unified Directive No. 2). National Priority hydropower projects may be restructured with minimal provisioning (clause 9.8.ङ of Directive No. 2)

At this stage, equity is fully tradable, dividends are declared, and hydropower companies are treated by the market as ongoing enterprises – despite the unchanged, finite tenure of their underlying licenses.

5. Transfer Phase (Exit Phase): The Legal Termination of the Asset

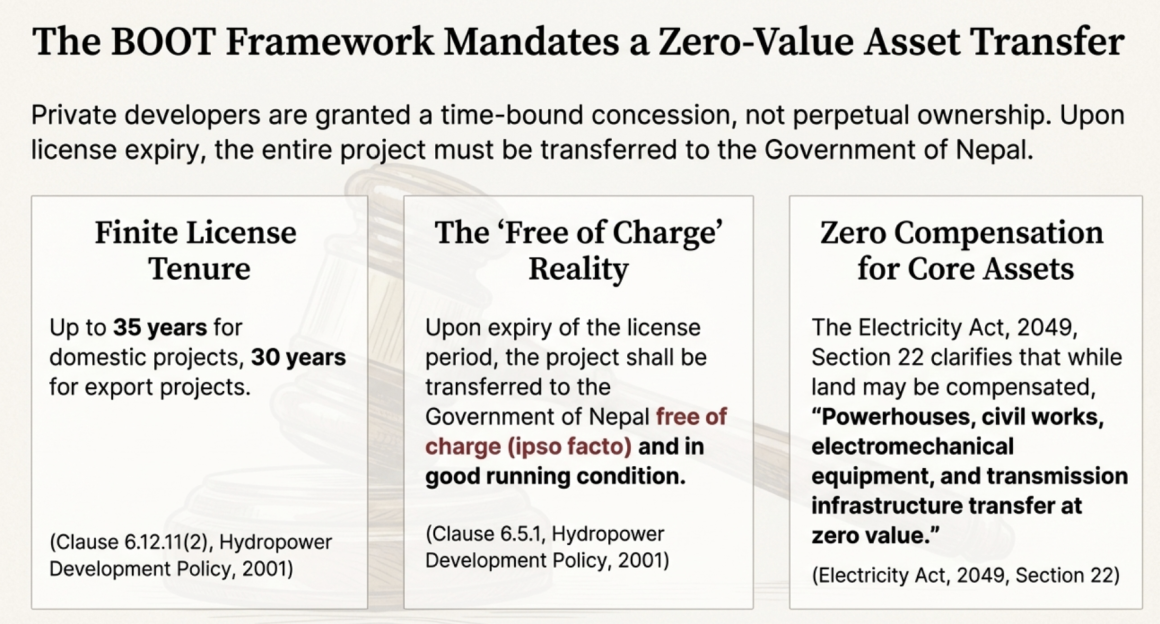

The final phase of the BOOT lifecycle is the mandatory transfer of the project to the state. Under clause 6.5.1 of the Hydropower Development Policy, 2001, the project must be handed over to the Government of Nepal free of charge (ipso facto) and in good running condition upon expiry of the generation license. Prior to transfer, the developer must submit a handover plan, including required Renewal Works and estimated Renewal Amount, as mandated under the Handover Plan provisions.

Post-transfer, the government may operate the project directly or enter into a new agreement, with priority given to the previous operator (clause 6.5.1 of the Hydropower Development Policy, 2001).

Notably:

- No securities law provides for shareholder compensation at transfer

- No banking directive addresses post-transfer equity extinction

- The corporate entity may legally survive, but its core revenue-generating asset ceases to exist

This lifecycle demonstrates that banking regulation, securities regulation, and BOOT concession law operate coherently within their own silos, yet collectively produce a structural contradiction: perpetual, tradable public equity is layered onto a time-bound, non-compensable infrastructure concession implemented through a single-asset SPV.

This contradiction – embedded at the very foundation of the hydropower lifecycle – sets the stage for the governance, valuation, and investor-protection challenges examined in the subsequent sections.

III. The Foundation: Understanding the BOOT Trap

1. The Context: Sovereignty over Assets and Temporary Licenses

The structural fragility of Nepal’s listed hydropower sector originates from a fundamental legal reality that is frequently misunderstood – or deliberately glossed over – in market discourse: private developers do not own hydropower assets in perpetuity.

Under Nepal’s water and electricity governance regime, sovereignty over water resources and associated infrastructure remains vested in the State. Private participation is permitted only through a time-bound concessionary arrangement, most commonly structured under the Build–Own–Operate–Transfer (BOOT) model.

Pursuant to the Hydropower Development Policy, 2001, a private developer is legally constituted as a “Licensee”, granted the exclusive right to utilize a specified water resource for electricity generation for a finite period only. The applicable license tenures are:

- Up to 35 years for projects supplying domestic demand

- Up to 30 years for export-oriented projects

(Clause 6.12.11(2)(a)–(b) of Hydropower Development Policy, 2001)

Critically, the license tenure begins from the date of license issuance, not from Commercial Operation Date (COD). Given that construction periods commonly span 4–6 years, the actual revenue-generating life available to equity investors is materially shorter than the headline license duration. This temporal mismatch is the first layer of the BOOT trap.

2. The “Free of Charge” Reality: Zero Terminal Compensation

The BOOT model culminates in a legally mandated and economically uncompensated transfer of assets to the Government of Nepal.

According to the Hydropower Development Policy, 2001: “Upon expiry of the license period, the project shall be transferred to the Government of Nepal free of charge (ipso facto) and in good running condition” (Clause 6.5.1 of Hydropower Development Policy, 2001)

This transfer is not a buyout, redemption, or market-based acquisition. The Electricity Act, 2049 (1992) further clarifies that: Compensation may be considered for land acquired by the licensee, but Powerhouses, civil works, electromechanical equipment, and transmission infrastructure transfer at zero value (Electricity Act, 2049 (1992), Section 22)

Moreover, the regulatory framework imposes a handover quality obligation:

- The licensee must transfer the project in “Good Operating Condition”

- A Handover Guarantee must be furnished two years prior to license expiry, ensuring continued operability for the State

(Guidelines on Handover Plan and Renewal Works, “Handover Guarantee” provision)

In effect, the private company is legally required to invest capital to preserve an asset it will no longer own, even as its revenue stream is extinguished. This creates a terminal value of zero for the project asset – by law, not by market forces.

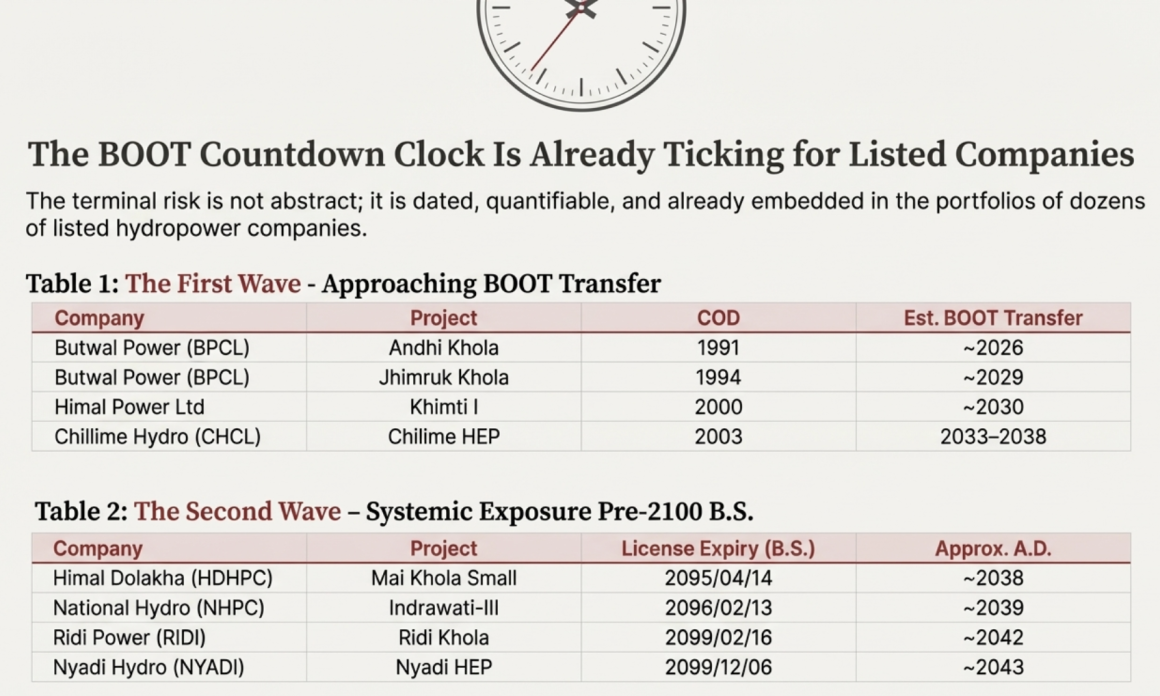

3. The BOOT Countdown Clock: Empirical Evidence from Listed Projects

The BOOT risk is not abstract or theoretical. It is dated, quantifiable, and already embedded in the portfolios of listed hydropower companies.

The “Canaries in the Coal Mine”: First-Generation IPPs Approaching BOOT Transfer

|

Company |

Project |

Capacity (MW) |

COD |

Est. BOOT Transfer |

|

Butwal Power (BPCL) |

Andhi Khola |

9.4 |

1991-07-01 |

~2026 |

|

Butwal Power (BPCL) |

Jhimruk Khola |

12.0 |

1994-08-01 |

~2029 |

|

Himal Power Ltd |

Khimti I |

60.0 |

2000-07-11 |

~2030 |

|

Bhote Koshi Power |

Upper Bhote Koshi |

45.0 |

2001-01-24 |

2031–2036 |

|

Chilime Hydro (CHCL) |

Chilime HEP |

22.1 |

2003-08-25 |

2033–2038 |

These projects represent the first real test cases for how BOOT transfers will be handled when the licensee is a listed public company with thousands of retail shareholders.

4. License Expiry: Listed SPVs with Near-Term Terminal Risk

Listed Hydropower Projects with License Expiry Pre-2100 B.S.

|

Company |

Project |

Capacity |

License Expiry (B.S.) |

Approx. A.D. |

|

Himal Dolakha (HDHPC) |

Mai Khola Small |

4.5 MW |

2095/04/14 |

~2038 |

|

National Hydro (NHPC) |

Indrawati-III |

7.5 MW |

2096/02/13 |

~2039 |

|

Ridi Power (RIDI) |

Ridi Khola |

2.4 MW |

2099/02/16 |

~2042 |

|

Nyadi Hydro (NYADI) |

Nyadi HEP |

30 MW |

2099/12/06 |

~2043 |

(Sources: respective IPO prospectuses; license disclosures under Securities Registration and Issuance Regulation, 2073)

5. The Second Wave: BOOT Transfers Scheduled for 2100–2105 B.S.

Systemic Exposure Window for Listed Hydropower SPVs

|

Company |

Project |

Capacity |

License Expiry (B.S.) |

Approx. A.D. |

|

Barun Hydro |

Hewa Khola |

4.5 |

2100/01/21 |

~2043 |

|

Upper Tamakoshi |

Upper Tamakoshi |

456 |

2103/08/17 |

~2046 |

|

Rasuwagadhi |

Rasuwagadhi |

111 |

2104/10/20 |

~2048 |

|

Sanjen |

Upper Sanjen |

14.8 |

2103/08/11 |

~2046 |

|

Modi Energy |

Tallo Modi-1 |

20 |

2102/05/20 |

~2045 |

|

Mandu Hydro |

Bagmati Sana |

22 |

2105/12/28 |

~2049 |

6. Key Observations: The Terminal Value Problem

The “Going Concern” Illusion: Although hydropower SPVs are legally finite, they are incorporated as public limited companies with perpetual succession, audited and valued as going concerns, and traded on NEPSE as indefinite equity instruments. This creates a structural mispricing, as the market fails to account for the legally mandated expiration of the underlying asset, giving investors a false sense of perpetual value.

Divergence Between Promoter and Retail Time Horizons: Promoters and lenders typically recover their capital within 15–20 years and exit via secondary market sales, dividends, or refinancing, aligning their strategies with the asset’s operational life. Retail investors, however, are left holding perpetual equity in a time-bound asset, bearing the residual BOOT risk without any structured exit mechanism, exposing them to potentially total loss at license expiry.

Holding Companies as an Implicit Escape Valve: Entities like Chilime Hydropower (CHCL) have been trying out a practical workaround to the BOOT trap by evolving into holding-company structures, investing in subsidiary SPVs such as Rasuwagadhi, Sanjen, and Madhya Bhotekoshi. This confirms the central thesis: single SPVs are not designed to be perpetual listed vehicles, and only through diversification and portfolio strategies can investors mitigate the structural risk inherent in finite-life hydropower projects.

7. Interim Conclusion: The BOOT Trap Defined

The combination of BOOT licensing, SPV-based project structuring, and perpetual public equity listings creates a near-certain collapse in terminal value for project-level shares. This is not a failure of the market but a regulatory design failure. As the following sections will show, inter-SPV investments exacerbate this risk, while international jurisdictions have systematically avoided it through holding-company structures, securitization, and time-bound financial instruments.

IV. The Conflict: Injecting Perpetual Equity into a Temporary Asset

1. The Core Structural Contradiction

The central structural flaw in Nepal’s hydropower capital market lies in the issuance of perpetual equity instruments against assets that are, by law, temporary. Hydropower companies listed on NEPSE are incorporated as Public Limited Companies with perpetual succession, issuing ordinary shares that are designed to:

- Exist indefinitely,

- Trade freely in the secondary market, and

- Represent residual ownership claims on a continuing business.

However, the sole economic engine of most listed hydropower companies – the generation license and associated physical infrastructure – is governed by the Build–Own–Operate–Transfer (BOOT) framework, which imposes a non-negotiable termination date.

This creates a severe financial paradox: The legal vehicle is perpetual, but the underlying asset has a legally mandated “date of death.” The capital market prices these shares as if they represent enduring ownership, while the governing sectoral laws dictate that the asset backing those shares must be transferred to the State free of charge at the end of the license term.

2. The Lifecycle of a Listed Hydropower SPV: From IPO to the Cliff Edge

The lifecycle of a typical single-project SPV systematically obscures its terminal nature until the very end. At the public issuance stage – whether an IPO, FPO, or Rights Issue – hydropower SPVs raise permanent equity capital from the general public, project-affected locals, and foreign-employed Nepalis, often under the “Janata ko Jalvidyut” mandate, which encourages up to 49% public ownership. Prospectuses emphasize project viability, tariffs, and expected returns, while the finite nature of the license is disclosed legally but economically underweighted, leading investors to assume a long-term ownership stake rather than a time-decaying claim.

During the construction phase, equity capital is absorbed into Capital Work in Progress (CWIP), with zero operating revenue, rising interest capitalization, and growing dependence on bank financing. This phase reflects a period where balance sheets expand, cash flows are absent, and shareholders have no exit other than speculative secondary trading. This phase deepens capital commitment while deferring confrontation with the asset’s terminal value.

Once the project reaches Commercial Operation Date (COD), it enters the yield illusion phase. Electricity sales to the Nepal Electricity Authority generate stable cash flows, dividend distributions, and apparent validation of the “going concern” assumption. This phase fuels secondary market liquidity, price discovery, and investor confidence, reinforcing the illusion that the asset will generate cash flows indefinitely. However, the license expiry clock continues to tick, with the terminal event remaining embedded but invisible.

Finally, at the BOOT transfer, typically 30–35 years after license issuance, the illusion collapses. The SPV is legally required to transfer the powerhouse, civil works, land, and transmission assets to the Government of Nepal free of charge and in good operating condition. At this point, the SPV loses its only revenue-generating asset, the equity backing evaporates, and the listed company faces an existential discontinuity, exposing retail investors to the full extent of terminal value risk.

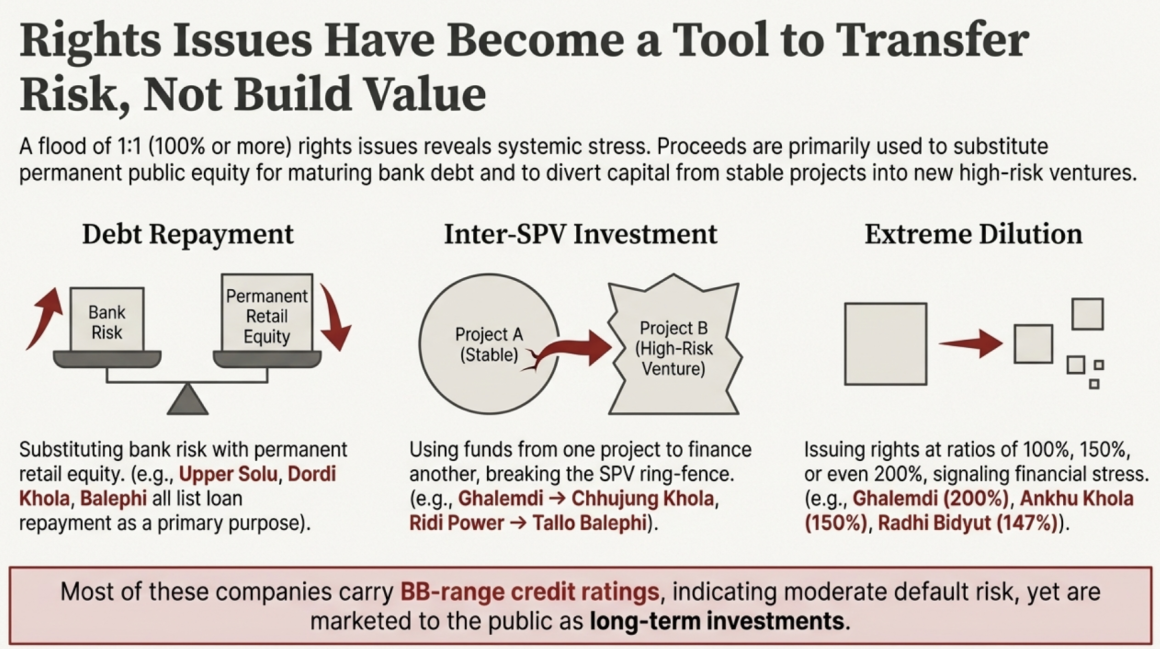

3. Rights Share Issuances: Evidence of Structural Stress

Rather than being an incidental financing tool, rights share issuance has become the dominant capital strategy for listed hydropower companies.

|

Company Name |

Ratio (Right Type) |

Shares Issued (Units) |

Issue Price |

Opening Date (B.S.) |

Primary Purpose / Utilization of Funds |

|

Ankhu Khola Jalvidhyut Co. Ltd. |

1 : 1.5 (150%) |

12,000,000 |

Rs. 100 |

2081/04/27 |

• Invest in Ankhu Khola-2 HEP (20 MW).• Pay off bank loans. |

|

Peoples Power Ltd. |

1 : 0.5 (50%) |

3,163,000 |

Rs. 100 |

2081/04/31 |

• Repay loans to Prime Commercial Bank Ltd. |

|

Joshi Hydropower Dev. Co. Ltd. |

1 : 0.65 (65%) |

2,414,100 |

Rs. 100 |

2081/04/15 |

• Repay bank loans (NMB Bank). |

|

Terhathum Power Company Ltd. |

1 : 1 (100%) |

4,000,000 |

Rs. 100 |

2081/04/05 |

• Repay bank loans.• Construct Khorunga Tangmaya Cascade (2 MW). |

|

Upper Solu Hydro Electric Co. Ltd. |

1 : 1 (100%) |

13,500,000 |

Rs. 100 |

2081/01/22 |

• Repay long-term bank loans. |

|

Dordi Khola Jal Bidhyut Co. Ltd. |

1 : 1 (100%) |

10,542,604 |

Rs. 100 |

2081/02/10 |

• Repay bank loans (Sanima Bank consortium). |

|

Ngadi Group Power Ltd. |

1 : 1 (100%) |

18,512,792 |

Rs. 100 |

2080/10/14 |

• Invest in Siuri Khola HEP (Strategic Partner).• Repay bank loans. |

|

Singati Hydro Energy Ltd. |

1 : 1 (100%) |

14,500,000 |

Rs. 100 |

2080/11/02 |

• Repay loans (Kumari Bank).• Invest in Upper Hongu Khola (14.15 MW). |

|

Ridi Power Company Ltd. |

1 : 0.5 (50%) |

7,744,506 |

Rs. 100 |

2080/11/18 |

• Invest in Tallo Balephi HEP (20 MW) (via Sajha Power).• Repay loans. |

|

Arun Valley Hydropower Dev. Co. |

1 : 1 (100%) |

18,679,626 |

Rs. 100 |

2080/11/17 |

• Invest in PK Hydropower (Likhu Khola).• Pay off loans for Kabeli B-1. |

|

Ghalemdi Hydro Limited |

1 : 2 (200%) |

11,000,000 |

Rs. 100 |

2080/09/10 |

• Invest in Chhujung Khola Hydropower (63 MW). |

|

Balephi Hydropower Limited |

1 : 1 (100%) |

18,279,700 |

Rs. 100 |

2080/08/21 |

• Repay bank loans (Global IME, Kumari, etc.). |

|

Upper Tamakoshi Hydropower Ltd. |

1 : 1 (100%) |

105,900,000 |

Rs. 100 |

2080/05/18 |

• Repay short-term loans.• Construct Rolwaling Khola HEP (22 MW). |

|

Arun Kabeli Power Limited |

1 : 1 (100%) |

18,552,105 |

Rs. 100 |

2080/05/11 |

• Repay bank loans related to Kabeli B-1 construction. |

|

Synergy Power Development Ltd. |

2 : 1 (50%) |

4,032,875 |

Rs. 100 |

2080/05/03 |

• Invest in Apex Makalu Hydro Power (22 MW). |

|

Himalaya Urja Bikas Company Ltd. |

1 : 1 (100%) |

9,900,000 |

Rs. 100 |

2080/04/24 |

• Pay loans for Upallo Khimti (12 MW) & Upper Khimti-II (7 MW). |

|

Rapti Hydro & General Construction |

1 : 1 (100%) |

6,127,938 |

Rs. 100 |

2080/03/29 |

• Repay bank loans.• Working capital management. |

|

National Hydro Power Company |

10 : 5 (50%) |

8,221,459 |

Rs. 100 |

2080/03/29 |

• Invest in Lower Erkhuwa Hydropower (14.15 MW). |

|

Himal Dolakha Hydropower Co. |

1 : 0.75 (75%) |

12,000,000 |

Rs. 100 |

2080/02/22 |

• Repay Bridge Gap Loan.• Invest in Mai Khola Small Hydro. |

|

Radhi Bidyut Company Ltd. |

1 : 1.47 (147.52%) |

9,535,760 |

Rs. 100 |

2079/06/05 |

• Invest in Kasuwa Khola Hydropower (45 MW). |

|

Ngadi Group Power Ltd. (Previous) |

1 : 1.5 (150%) |

10,603,986 |

Rs. 100 |

2079/04/18 |

• Repay loans.• Invest in other projects. |

|

Api Power Company Ltd. (Issuance 1) |

1 : 0.39 (39.36%) |

10,860,000 |

Rs. 100 |

2078/12/25 |

• Invest in/Construct Upper Chameliya HEP (40 MW). |

|

HIDCL |

1 : 1 (100%) |

110,000,000 |

Rs. 100 |

2078/04/05 |

• Equity investment in various hydro projects (subsidiaries). |

|

Api Power Company Ltd. (Issuance 2) |

1 : 0.29 (29.38%) |

5,670,000 |

Rs. 100 |

2078/02/20 |

• Invest in/Construct Upper Chameliya HEP. |

|

Arun Valley Hydropower (Previous) |

1 : 0.5 (50%) |

5,241,197 |

Rs. 100 |

2077/12/06 |

• Construction of Kabeli B-1 Cascade HEP. |

The rights issuance data highlights three systemic patterns that exacerbate the BOOT–equity conflict. First, a substantial portion of rights proceeds is not reinvested in the issuing project, but redirected into subsidiary SPVs, affiliate hydropower projects, or promoter-linked ventures. Examples include Ghalemdi → Chhujung Khola, Ridi Power → Tallo Balephi, National Hydro → Lower Erkhuwa, Synergy Power → Apex Makalu, and Radhi Bidyut → Kasuwa Khola. This practice breaks the principle of project-level risk isolation, obscures asset-specific financial discipline, and transfers undeclared risks to existing shareholders.

Second, nearly every rights issue is intended to repay term debt, effectively substituting permanent equity for bank loans. This shifts financial risk from banks to retail investors, cleaning the SPV’s balance sheet at the cost of dilution. While banks exit early, retail shareholders inherit the long-tail BOOT risk, exposing them to the terminal value problem.

Third, extreme capital dilution is common, with some companies issuing rights exceeding 100% of paid-up capital, including Ankhu Khola (150%), Ngadi Group (150%), Ghalemdi (200%), and Radhi Bidyut (147%). Such dilution weakens per-share claims on future cash flows, fundamentally alters capital structures, and often signals financial stress rather than growth. Compounding the concern, most issuing companies carry BB-range credit ratings (CARE-NP / ICRA NP), indicating moderate default risk. This raises a critical question: if project risk is significant enough to warrant BB ratings, why is perpetual equity being marketed as a safe, long-term retail investment?

4. The Valuation Gap: Perpetual Pricing vs. Zero Terminal Value

In conventional industries, firms own land, factories, and brands indefinitely, and equity valuations assume a positive terminal value. In contrast, a single-asset hydropower SPV has a legally predetermined terminal value of zero. Despite this, shares are priced based on dividend yield and growth multiples, with market participants implicitly assuming perpetuity. There is no statutory mechanism for buyback, redemption, or amortization at license expiry, creating a persistent valuation distortion in which the market price of shares is fundamentally disconnected from the legal and economic reality of the underlying asset.

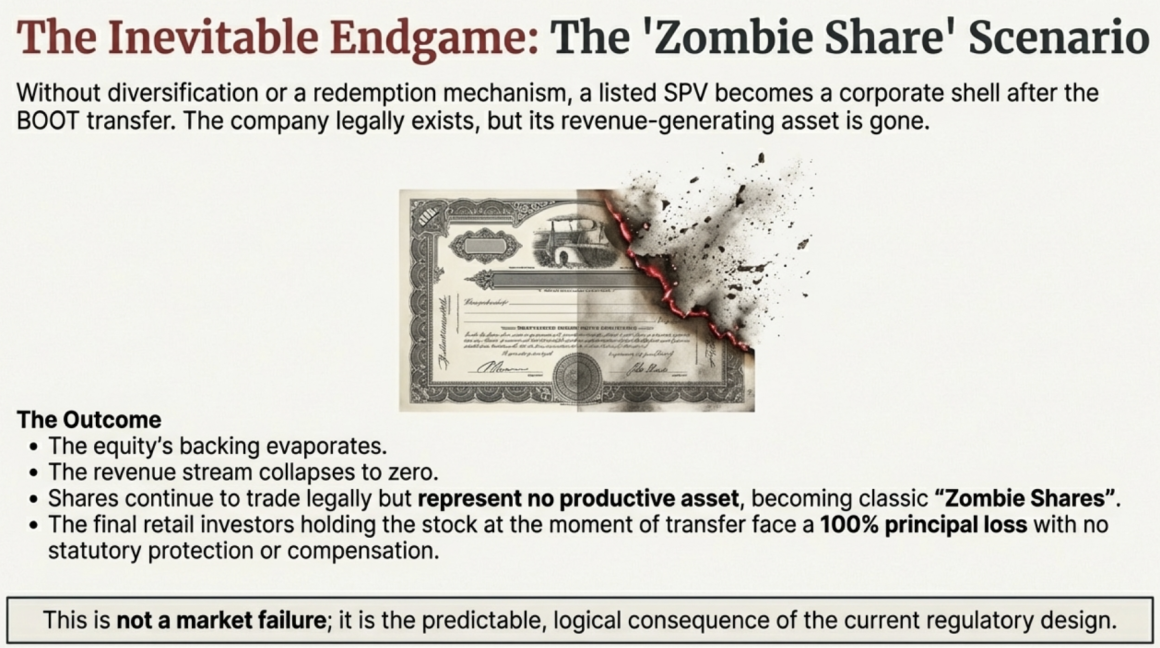

5. The “Zombie Share” Scenario: Post-Transfer Market Failure

In conventional industries, firms own land, factories, and brands indefinitely, and equity valuations assume a positive terminal value. In contrast, a single-asset hydropower SPV has a legally predetermined terminal value of zero. Despite this, shares are priced based on dividend yield and growth multiples, with market participants implicitly assuming perpetuity. There is no statutory mechanism for buyback, redemption, or amortization at license expiry, creating a persistent valuation distortion in which the market price of shares is fundamentally disconnected from the legal and economic reality of the underlying asset.

6. Interim Conclusion: Why This Is a Regulatory Failure, Not a Market Accident

This outcome is not the result of poor project execution; rather, it is the predictable consequence of allowing BOOT-based SPVs to issue perpetual equity, encouraging retail participation without time-bound instruments, and failing to mandate structural solutions such as holding companies, securitization, or redemption mechanisms. Unless addressed through explicit guidance from ERC and SEBON, Nepal’s hydropower market will continue to produce financially sophisticated projects underpinned by legally fragile equity, systematically exposing public investors to terminal value risk.

V. Real-World Consequences: How the Structural Doom Manifests

The misalignment between perpetual equity instruments and temporary BOOT-based hydropower assets is no longer a theoretical or future concern. It is already manifesting through observable corporate behaviors and regulatory permissions that systematically transfer long-term concession risk from sophisticated project developers to unsophisticated retail investors.

Two mechanisms are particularly dominant:

- Early promoter exit after de-risking, and

- Erosion of project-level ring-fencing through inter-SPV capital flows.

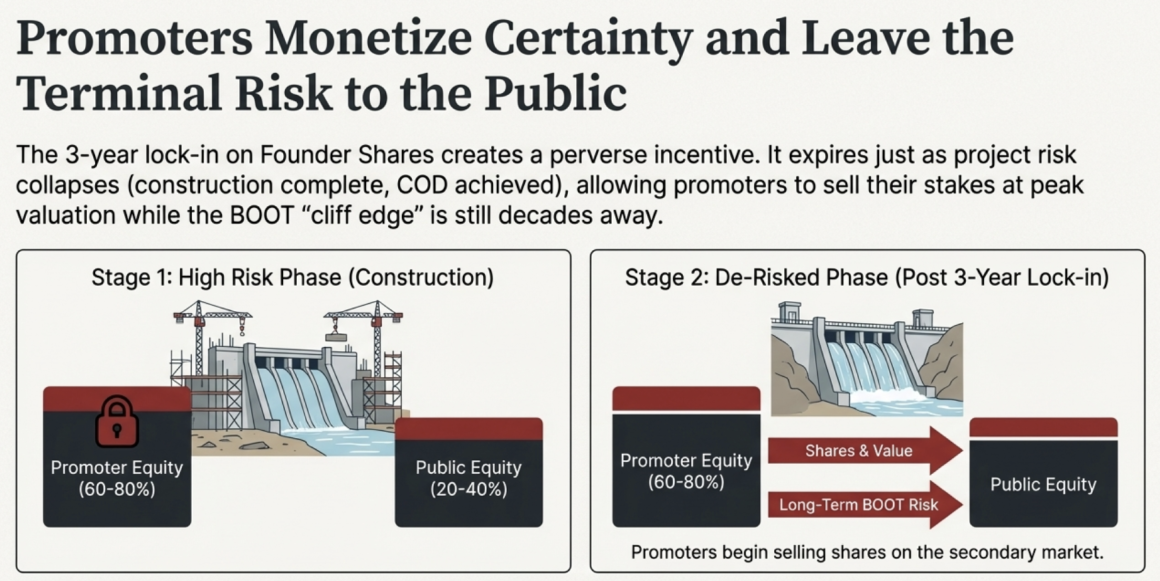

1. The Promoter Exit Problem: Monetizing Certainty, Leaving the Cliff to the Public

In orthodox project finance, a Special Purpose Vehicle (SPV) is used to isolate project risk and protect financiers. In Nepal’s listed hydropower sector, however, the SPV has evolved into a risk-transfer conduit, allowing promoters to extract value early while leaving the legally unavoidable BOOT termination risk with the general public.

The 3-Year De-Risking Strategy: Promoters typically retain 60–80% ownership during the construction phase – when geological, hydrological, and completion risks are highest. Under prevailing securities regulations, these Founder Shares are subject to a three-year lock-in period from the date of public allotment. This lock-in period frequently aligns with: completion of construction, achievement of Commercial Operation Date (COD), and stabilization of cash flows via NEA power purchase agreements.

At precisely the point when project risk collapses and valuation certainty peaks, the regulatory lock-in expires.

The Exit Gate: Once the lock-in period lapses, promoters are legally free to: sell shares in the secondary market, pledge shares for unrelated financing, or exit entirely from the project’s equity base. Public notices of lock-in expiration for companies such as Green Ventures Ltd (GVL), Balephi Hydropower (BHL), and River Falls Power Ltd (RFPL) illustrate how early-stage capital can lawfully exit shortly after de-risking (SEBON / NEPSE notices to be cited inline).

Retail Risk Accumulation: When promoters monetize future cash flows upfront through share sales, retail investors inherit the residual life-cycle risk. As time progresses, the BOOT clock continues to tick down inexorably toward a zero-compensation asset transfer.

By the time the license expires – typically 30–35 years from issuance – the original promoters have long exited. What remains is a publicly held equity stake in an SPV that no longer owns the project that once justified its valuation.

Promoter vs. Public Shareholding (Risk Transfer Snapshot)

|

Company Name |

Promoter Holding (%) |

Public Holding (%) |

Lock-in Status |

Source |

|

Green Ventures Ltd |

80% |

20% |

3-Year Lock-in (Notice Issued) |

SEBON / NEPSE |

|

Makar Jitumaya Suri |

70% |

30% |

3-Year Lock-in |

Prospectus |

|

Balephi Hydropower |

60% |

40% |

Expired / Trading |

NEPSE |

|

Upper Tamakoshi |

51% |

49% |

Operational (Legacy Structure) |

Annual Report |

The data reveals a consistent pattern: promoters exit soon after operational stability, while public ownership persists throughout the project’s legally finite lifespan – absorbing the full terminal-value collapse.

2. The Governance Nightmare of Inter-SPV Investment

To postpone the inevitable “Zombie Share” outcome, many listed hydropower companies have quietly abandoned project-specific risk isolation. Rather than returning surplus cash to shareholders as dividends while the license countdown continues, operational SPVs are increasingly used to finance new construction risk. Current directives allow licensees to establish subsidiary SPVs for additional projects, and while permissible in isolation, this framework enables capital to flow from a stable, revenue-generating SPV into high-risk greenfield projects, fundamentally altering the risk profile of the original investment without renewed investor consent.

Retail investors, who purchase shares in established operators – often perceived as “blue-chip” hydropower stocks – do so primarily for stable dividend yield. However, when retained earnings or rights proceeds are diverted into new construction, these investors inadvertently underwrite geological uncertainty, hydrological variability, construction delays, and refinancing risk.

The regulatory loophole exacerbates this behavior. The Electricity Regulatory Commission (ERC) allows rights share issuances of up to 200% of paid-up capital, explicitly for debt repayment or investment in new projects. This creates a perpetual construction cycle, where public capital is continuously recycled into fresh risk, preventing shareholders from ever fully realizing the free cash flow of the original asset before it must be surrendered to the state.

Inter-SPV Financial Flows

|

Source (Listed Co.) |

Method |

Destination (New SPV) |

Amount / Nature of Investment |

Source |

|

Arun Valley (AHPC) |

1:1 Right Share |

Kabeli B-1 & PK Hydro |

Rs. 186.79 Crore (Equity + Debt Repayment) |

Prospectus |

|

Api Power (API) |

1:0.4 Right Share |

Upper Chameliya |

Rs. 56.70 Crore (Construction / Loan Repayment) |

Prospectus |

|

Ridi Power (RIDI) |

1:0.5 Right Share |

Tallo Balephi |

Rs. 22 Crore (Direct Equity Injection) |

Prospectus |

|

Sanima Mai (SHPC) |

Retained Earnings |

Middle Tamor |

1,51,69,020 Shares (Major Promoter Stake) |

Annual Report |

These transactions demonstrate how cash flows from mature, low-risk assets are systematically diverted into high-risk projects – without resetting the BOOT clock or offering investors a true exit.

3. Synthesis: How the Trap Closes

Promoter exits combined with inter-SPV investments create a one-way risk escalator. Promoters exit early after de-risking their capital, while public investors are left to replace temporary debt with permanent equity. Dividends are diluted or deferred through reinvestment into new projects, and license expiry approaches with no redemption mechanism in place. The result is not organic capital formation but deferred loss realization, concentrated on the least informed and least mobile participants: retail shareholders. Unless regulators implement structural – not cosmetic – interventions, Nepal’s listed hydropower SPVs are on course to become mass zombie equities, with the final generation of investors bearing losses that were foreseeable, avoidable, and entirely the product of regulatory design.

VI. The Regulatory Vacuum: A Lack of Exit Oversight

Nepal’s hydropower crisis is magnified by a regulatory framework that conceptualizes project-specific entities as perpetual businesses rather than fixed-term infrastructure projects. Oversight from the Securities Board of Nepal (SEBON) and the Electricity Regulatory Commission (ERC) focuses heavily on capital inflow and construction milestones, while remaining silent on the mandatory asset transfer at the end of the license period – a transfer that effectively renders the invested capital theoretically valueless.

1. SEBON/ERC Critique: The Entry-Phase Fixation

A central critique of Nepal’s regulatory approach is its fixation on entry requirements, ignoring the long-term nature of hydropower investments.

- The Construction Milestone Trap: ERC approval for public offerings requires at least 50% physical progress, while SEBON mandates 75% construction completion before an IPO can proceed. While these measures ensure the physical asset exists, they do not consider the finite operational life of the project.

- Perpetuity vs. Reality: Regulations treat these companies as standard “going concerns,” with an expectation of indefinite operation. There is no requirement for a Terminal Value Analysis or Wind-Down Disclosure, leaving shareholders uninformed that revenue streams will cease upon license expiry.

- Sanctioning the “Zombie” Structure: By focusing on capital injection rather than the tenure mismatch of the underlying asset, regulators have effectively endorsed “Zombie Share” structures. Temporary debt (which naturally matures) is being replaced by permanent equity for assets that must ultimately be handed over to the government at zero cost.

2. The 10-Year Loophole: A Ticking Clock for Investors

The Securities Registration and Issuance Regulation, 2073, illustrates the regulatory disregard for long-term shareholder protection:

- The Rule: Section I allows water resource entities to register and sell securities publicly if the remaining term of the operational license is at least 10 years.

- The Paradox: This provision enables IPOs for projects merely a decade away from mandatory state handover, exposing investors to extreme tail-end risk.

- No Mandatory Redemption: SEBON does not require a capital redemption plan or a mechanism to convert equity into debt before the asset is lost. Promoters can exit through the secondary market within three years of the IPO, leaving retail investors holding shares whose underlying asset is rapidly approaching zero value.

3. The Missing Sinking Fund: No Safety Net for Public Capital

The most glaring regulatory omission is the absence of a Mandatory Sinking Fund or Capital Redemption Reserve:

- Profit Retention Gaps: In standard international practice, a Sinking Fund accumulates over time to repay investors at concession end. Nepal’s regulations do not compel hydropower companies to retain profits for this purpose.

- Dividend vs. Redemption: Regulators permit, and sometimes encourage, companies to distribute all profits as dividends or divert them into Inter-SPV investments, leaving the Paid-up Value of shares artificially fixed, despite the underlying asset approaching obsolescence.

- Lack of Classification: Regulators do not distinguish between a “Growth Company” (perpetual) and a “Yield Company” (finite). As a result, all hydropower stocks are traded as standard equities, denying retail investors the protective financial engineering essential for finite-life assets.

VII. International Precedent: Doing It Right

To fully grasp the structural instability of Nepal’s hydropower market, it is instructive to examine how other jurisdictions manage infrastructure projects with finite lifespans. Unlike Nepal, where individual, temporary SPVs are listed as perpetual equities, leading markets design investment instruments that mirror the lifecycle of the underlying asset, aligning risk, return, and exit mechanisms with reality.

1. India’s Infrastructure Investment Trusts (InvITs): Aggregation and Exit

India has pioneered a structural alternative to the direct listing of single-project SPVs through Infrastructure Investment Trusts (InvITs).

- Portfolio Diversification: An InvIT aggregates multiple infrastructure projects – such as power generation, transmission, or renewable assets – into a single, regulated investment vehicle. This mitigates the “ticking clock” problem inherent in single, finite-life projects.

- Clear Exit and Income Structures: Projects are held either directly or via a Holding Company (HoldCo). Examples include the India Grid Trust (IndiGrid) and PowerGrid Infrastructure Investment Trust (PGInvIT), which leverage capital markets to refinance debt and provide investors with stable, predictable income streams and structured exit mechanisms.

- Contrast with Nepal: By aggregating multiple assets, InvITs prevent the “finite-life equity” problem that plagues Nepalese hydropower IPOs. Even as one project’s concession expires, the trust continues to operate as a viable, revenue-generating entity.

2. The Holding Company Model: Australia and Europe

In mature markets, standalone, finite-life SPVs are rarely listed. Instead, investors gain exposure via diversified holding companies:

- Australian HoldCo Structure: Australia’s listed infrastructure groups, such as Spark Infrastructure, hold stakes in multiple power networks. Investors participate in the cash flows of a diversified operating company rather than a single, expiring project.

- European Utility Model: In Europe, major hydropower assets are typically controlled by integrated utilities, e.g., Verbund (Austria). These companies maintain long-term license rights and manage diversified energy portfolios.

- Mitigating the “Cliff Edge”: Holding companies enable capital recycling – as one license expires, the parent reinvests returns into new assets. This ensures that public equity remains backed by revenue-generating assets, unlike Nepal’s single-SPV model. The Chilime Hydropower (CHCL) model, which holds 51% equity in multiple subsidiaries like Rasuwagadhi and Sanjen, represents Nepal’s closest approximation of this international best practice.

3. Project Bonds: Aligning Maturity with Concession

A core flaw in Nepal’s framework is the reliance on perpetual equity for temporary assets. International precedent shows that debt instruments – rather than equity – are better suited for BOOT-style projects:

- Maturity Matching: In the UK, Luxembourg, and other markets, SPVs issue project bonds whose maturities align precisely with the project’s cash flow and license period.

- Principal Repayment: Unlike equity, which implies indefinite ownership, bonds ensure full repayment of principal before the asset is transferred to the government, insulating investors from terminal value risk.

- Existing Policy Support in Nepal: The Hydropower Development Policy, 2001 already mentions mobilization of capital markets through “bonds as well as other financial instruments.” Shifting from IPOs to project-specific bonds would allow developers to raise capital without passing the end-of-life risk onto retail equity holders.

4. Comparative Takeaways: Nepal vs. International Best Practice

|

Feature |

Nepal Model |

International Best Practice |

|

Listed Entity |

Single-Project SPV |

Portfolio Holding Company / InvIT |

|

Equity Nature |

Perpetual |

Diversified / Maturity-Matched |

|

Exit Value |

Zero (Handed to State) |

Defined via Bonds or Portfolio Growth |

|

Risk Isolation |

Broken via Inter-SPV flows |

Preserved via Ring-Fenced Securitization |

Nepal’s current framework misaligns investment instruments with asset lifecycles, creating systemic tail-risk for retail investors. Global models demonstrate that aggregation, diversified holdings, and maturity-matched debt instruments can resolve this structural misalignment while maintaining capital market participation.

VIII. The Way Forward: Solutions Before the Crash

To avert a systemic collapse where public equity is wiped out upon the expiration of generation licenses, Nepal must bridge the regulatory chasm between the Companies Act, 2063 (which assumes corporate perpetuity) and the Electricity Act, 2049 (which mandates asset termination). The following structural and regulatory reforms are necessary to protect retail investors and ensure the long-term health of the capital market.

1. For Existing Listed Companies: Transparency and Operational Transition

- Mandatory Disclosure: The “BOOT Countdown Clock” Current regulations from SEBON and the Electricity Regulatory Commission (ERC) focus heavily on entry milestones, such as requiring 75% physical progress before an IPO, but they remain silent on the terminal value of the shares. Regulators must mandate a “Truth in Labeling” standard where every annual report and prospectus prominently features a “BOOT Countdown Clock”. This disclosure must explicitly state the license expiry date and provide a warning that the primary asset will be transferred to the government for zero compensation, potentially rendering the shares valueless. Shares in single-asset hydro companies should be reclassified as “Limited-Life Assets” or “Concessionary Equity” to distinguish them from perpetual banking or manufacturing stocks.

- Transitioning from Owners to Operators: Management Contracts The Hydropower Development Policy, 2001 (Clause 6.5.1) provides a legal “soft landing” by allowing the government to contract out the operation of transferred projects, giving first priority to the previous operator. Companies should prepare to transition from asset owners to Asset Operators under a Management Service Arrangement (MSA) or leaseback model. This would allow the listed entity to retain a revenue stream through operations and maintenance (O&M) fees, preserving some residual value for shareholders even after the physical plant is surrendered.

- Renegotiated Energy Prices at BOOT Transfer: As an alternative or complement, companies could renegotiate energy tariffs at the point of BOOT transfer and continue to operate the project under a limited-price, long-term contract or management agreement. This approach allows the SPV to maintain revenue generation and a degree of operational control, providing shareholders with a continuing, predictable income stream while respecting the legal transfer obligations to the government.

2. For Future Structure: Systemic Sustainability and Diversification

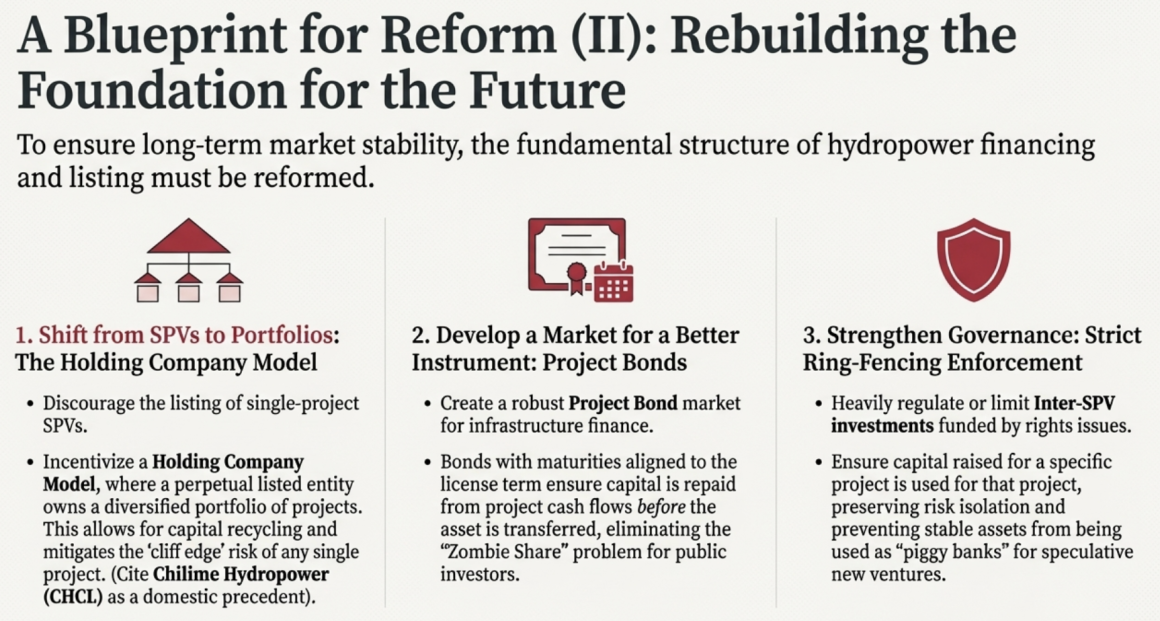

- The Holding Company Model: Portfolio Diversification To match the “perpetual” nature of the stock market, Nepal must shift away from listing individual, finite-life SPVs. Instead, the market should encourage the Holding Company Model, where a perpetual listed entity owns a diversified portfolio of unlisted, finite-life subsidiary SPVs. As one project’s license expires, the parent company survives through its other projects and the reinvestment of capital into new licenses. This model, exemplified de facto by Chilime Hydropower (CHCL), allows for “capital recycling” and reduces the binary risk of a single project’s “cliff edge”.

- Mandatory Sinking Funds: Capital Redemption Reserves Currently, there is no regulatory requirement for hydropower companies to set aside funds to repay the public’s initial investment. Regulators should mandate a Capital Redemption Reserve or Sinking Fund, where a portion of annual profits is restricted specifically to buy back or repay the par value (Rs. 100) of shares at the time of the BOOT transfer. This ensures that the passive retail investor – who funded the nation’s infrastructure – recovers their principal even if the company’s asset-backing vanishes.

- Preferential Shares: Protecting the Public Group A tiered equity structure could differentiate between the Founder Group (who reap construction profits) and the General Public Group. As the project nears maturity, public ordinary shares could be converted into Preferential Shares. These shares would carry a guaranteed dividend yield and could be “carried over” by the government post-transfer. In this scenario, the government (NEA) operates the plant and pays a fixed dividend to the public investors as a “royalty” for providing the initial capital, while the original promoters exit the project.

3. Critical Points for Strengthening the Model

- Developing a Project Bond Market The sector currently suffers from an asset-liability mismatch by financing 30-year assets with infinite-life equity. The government should develop a Project Bond market where debt instruments are issued with maturity dates that align with the license term. This ensures that the capital is fully repaid out of project cash flows before the asset is handed over, eliminating the “Zombie Share” problem entirely.

- Strict Ring-Fencing Enforcement The practice of using operational “cash cow” SPVs as piggy banks for risky new construction (Inter-SPV investment) must be strictly regulated. While it aids the holding company strategy, it often breaks project-specific risk isolation and misleads investors regarding the stability of their dividends. Regulators should limit inter-SPV investments to a small percentage of free cash flow, ensuring that dividends from the original asset are not fully cannibalized to fund new risks.

- License Tenure and Renewal While the Electricity Act, 2049 permits licenses up to 50 years, most are issued for 30–35 years. Extending the license to the maximum 50-year cap or allowing for license renewal fees – where the company pays the state to keep the plant instead of surrendering it – would instantly align the legal reality of the company with the economic reality of the asset.

IX. Conclusion

Nepal’s hydropower market is a ticking time bomb: perpetual equity is being sold for finite-life assets, leaving retail investors exposed to a guaranteed terminal value of zero while promoters and sophisticated investors exit early. Inter-SPV investments and the lack of exit-phase oversight have created a market bubble, with shares priced as if the assets will last forever. Without urgent reforms – such as Sinking Funds, Holding Company structures, or maturity-matched Project Bonds – investors will be left holding a “perpetual ticket” to a show that legally ends in 30 years, underscoring the urgent need for structural and regulatory intervention.